Accounting 101: Everything business owners need to know

Accounting is a professional activity that involves recording and summarizing a company’s financial transactions. Financial management uses that accounting information to analyze financial information and guide management decision-making.

The goal of accounting is to prepare accurate, reliable and timely financial information so that business owners, management and others can make informed data-driven decisions.

Accounting will allow you to understand your company’s finances, make business decisions and present information to other readers of financial information, including external readers (e.g., bankers, investors, buyers) and internal users (e.g., valuation specialists, managers).

Accounting is vital for you to get the financial information you need to make sound decisions about your company.

Why is accounting important?

Accounting provides you objective financial information that can be directly linked to a business or financial transaction within a company. The information can be verified against documentation such as bank statements, supplier invoices and customer invoices.

Accounting provides essential information to help businesses:

- measure and monitor financial performance

- manage cash flow

- mitigate fraud and other risks to your company

- develop pricing strategy

- plan your business strategy

- optimize your taxes

- obtain a loan or investment

- determine a company’s valuation

- undergo due diligence during a business acquisition

Even if finances aren’t your forte, it’s important for you to familiarize yourself with how financial records are kept and communicate regularly with the people maintaining those records.

You may want to take our free quiz for entrepreneurs and business leaders and identify the weak spots in your financial and accounting knowledge.

It’s also important for entrepreneurs to engage qualified financial professionals, such as bookkeepers and accountants, to prepare reliable, meaningful financial reports. Relying on people with inadequate expertise can increase the risk of recordkeeping mistakes that could potentially cost your company money and give a misleading picture of your financial health.

In a BDC study on financial literacy, 67% of business owners surveyed said they usually consult their accountant or financial advisor before making an important financial decision pertaining to their business.

Accounting best practices for entrepreneurs

No matter your level of comfort with financial data, you should ensure that the following best practices are followed by the people responsible for accounting in your business.

1. Proper recordkeeping

At the heart of accounting is the proper recording of financial data. This requires:

- Accuracy—The correct data must be recorded. It should be based on a verified, precise figure, not a guess or estimate.

- Reliability—Financial transactions must be recorded and categorized properly. For example, a direct cost should be allocated under cost of goods sold—not under selling, general and administrative expenses. Also, you must record a debit and credit for every transaction (also known as double-sided entry).

- Timeliness—Financial transactions should be recorded as soon as they occur; otherwise, details can be forgotten. Recording it when it’s fresh helps ensure accuracy.

- Consistency—Recording financial transactions must not only comply with generally accepted accounting principles (GAAP), but they must be recorded the same way each time.

- Simplicity—Data entry should be done through a simple process. For example, a record should be entered only once. Multiple entries of the same information increase the risk of error.

2. Meaningful information

You need financial information to be presented in a way that helps you make business decisions.

Talk with your bookkeeper, accountant or other financial professional about what kind of reporting will help you most. Consider investing in accounting software to improve your recordkeeping and reporting capabilities.

Reporting can include:

- interim and year-end financial statements

- budgets and actuals

- financial projections

- accounts receivable and payable reports

- cash flow statements

- financial ratio analysis

3. Safeguarding against losses

Accountants can institute several types of controls to mitigate the risk of asset loss. These typically include:

- Segregation of duties. The practice of separating functions to reduce the risk of fraud. For example, the person who buys something shouldn’t be the person who pays the bill.

- Delegation of authority. Setting limits on what people can buy and how much they can spend.

- Security of assets. Protecting financial and other assets, such as restricting access to cash, locking doors and immediately depositing cheques.

- Performance measurement. Holding people accountable for the results their operations generate.

- Verifications. Performing audits, inventory checks, reconciliations and steps to ensure that reported numbers are accurate.

The three types of accounting for managing businesses

- financial accounting

- managerial accounting (also known as cost accounting)

- tax accounting

1. Financial accounting

Financial accounting is accounting in accordance with recognized accounting standards (see more on standards below).

This method of accounting is generally done at the aggregate level of the company. For example, sales and costs reflect total company-wide transactions and are generally not broken down by department, product line or other category. This accounting method leads to financial statements and indicators for the overall business. It also allows company executives and shareholders, and external readers such as bankers and potential investors, to get a general view of the financial health of the business.

Financial accounting can be done using one of two available approaches:

- Historical cost accounting (also called fair value accounting). This involves accounting for assets based on their original cost.

- Current cost accounting (also called mark-to-market accounting or current value accounting). This involves accounting for assets based on their current market value.

2. Managerial accounting

Managerial or cost accounting is done according to the same accounting principles as financial accounting, the difference being that the former breaks down company finances into relevant segments.

Data is typically broken down by:

- department or division

- geographic territory

- business line

- product line

- customer type

The goal is to present a more fulsome picture of the company’s revenues, costs, assets and other aspects so those elements can be better understood in context. For example, a company may have a 30% net margin, but a product line breakdown could show that one product has a margin of 60% while another shows a 20% loss. Such information can help the company address weaker areas of the business.

3. Tax accounting

Tax accounting is done in accordance with specific rules that tax authorities require businesses to follow. These may not necessarily align with other accounting standards. In some cases, it may be necessary to prepare separate financial statements, one for tax purposes, a second one based on financial accounting methods and a third for managerial reporting.

For example, tax authorities may require you to use a different rate of depreciation for assets than you would use in financial accounting.

What are the main accounting standards?

Accounting is done according to broadly accepted principles for recording, measuring, presenting and disclosing transactions. These are set by the Accounting Standards Board in accordance with GAAP.

Canadian private businesses can use one of two accounting standards:

What does accounting mean?

Accounting is perhaps best known as the process of recording the money that flows in and out of a business. But it can also include many other tasks, such as:

- tracking the value of the company’s assets and liabilities

- recording the money that the business accumulates in earnings and investments

- preparing interim and year-end financial statements

- preparing a company budget and financial projections

- assisting with business management decisions

What are the responsibilities of an accountant?

An accountant has three major responsibilities:

- ensuring the accuracy, reliability and timeliness of financial records

- presenting meaningful financial information to business owners and leadership

- safeguarding the business from the risk of fraud and other potential loss of assets

What is the role of the auditor in accounting?

An auditor is an independent third-party accountant who validates a company’s financial information and prepares audited financial statements. This type of statement provides a high degree of assurance to external parties that the information is correct.

To prepare audited financial statements, the auditor may:

- request supporting documents

- review internal controls

- verify accuracy of numbers

- conduct on-site spot checks

- perform an audit count of inventory

- evaluate accounts receivable

What is forensic accounting?

Forensic accounting is a specialized type of accounting used to investigate fraud and other financial crimes. It involves investigating and analyzing financial records and adapting the findings for legal inquiries.

Forensic accounting is used for:

- uncovering fraud, theft, embezzlement or identity theft

- establishing damages during litigation

- investigating insurance claims

- finding hidden assets

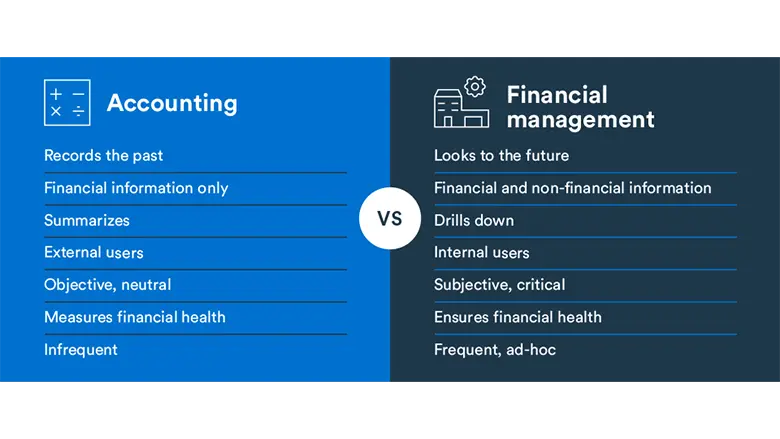

What is the difference between accounting and financial management?

Accounting involves recording and reporting past financial transactions, with the goal being to generate financial records.

Financial management, on the other hand, looks to the future. It draws on accounting information to create a business strategy, set a budget, develop forecasts and measure performance. Its goal is to maximize profits and growth and to help achieve the company’s wider goals.

What is the difference between accounting and bookkeeping?

Bookkeeping mainly involves recording the day-to-day financial transactions of a business. It is one part of the larger activity of accounting.

A bookkeeper’s responsibilities often include drawing up invoices, paying employees and balancing books. Unlike an accountant, a bookkeeper doesn’t require any formal training or certification.

An accountant can perform the tasks of a bookkeeper, but they also have training to ensure that financial records are accurately and reliably recorded and presented in accordance with accounting standards.

An accountant can also conduct managerial accounting to help entrepreneurs make decisions about their business, as well as advise on safeguards to reduce financial risks.

Next Step

Discover how to track and interpret pertinent financial information for your business. Download for free Understand Your Financial Statements: A Guide for Entrepreneurs.