5 tips to manage your cash flow

Cash is king—it’s a common saying in the business world. But surprisingly few entrepreneurs take steps to manage their cash flow so that they don’t wind up with an empty bank account and nothing with which to pay the bills.

The good news: Cash flow management is easy to improve with a few simple steps.

Below are five tips to help you manage your cash flow, and to better prepare you for the future and help your business avoid financial challenges.

But first, its important to understand the concept itself.

What is cash flow?

Simply put, cash flow refers to the amount of cash that goes in and out of a company’s coffers during a given period of time.

Normally, you will find three types of cash flow on a cash flow statement:

- Cash flow from operations. This is the money generated, spent or lost in the course of a company's main business activities.

- Cash flow from investments. This is the money coming in or going out of the company that is related to the purchase and sale of long-term investments such as property, buildings and equipment.

- Cash flow from financing. This category includes all flows related to raising cash as well as paying back debts to investors and creditors.

Although not usually listed on a cash flow statement, one could add a fourth type: free cash flow. That’s the cash that a company has left over after accounting for operating expenses and capital expenditures. It should not be confused with net cash flow, which is listed on a cash flow statement, and refers to the sum of the three categories above.

Can cash flow be negative?

Since a company’s net cash flow is a sum of three different positive or negative figures, cash flow can turn out to be negative. When this happens, it means there is more cash leaving the company than there is cash coming in.

This situation can spell financial trouble, of course, but it need not always be negative in the colloquial sense, explains Karanjit Singh Kochar, Manager, Major Accounts, BDC. “It can also be a sign of seasonality,” he says, referring to businesses like a snow clearing company or ice cream shop that have high and low seasons, resulting in higher expenditures and lower revenues depending on the time of year.

Is cash flow the same as profits?

Cash flow is different from profits, although both concepts are related.

When your company makes a sale, it does not necessarily get paid right away. Conversely, when you buy a product or service, you don’t necessarily pay right away. In some instances, for example when a client goes out of business, you may never see the payment for a sale.

Cash flow refers to the money that actually flows in and out of your business during a given period, while profits equal your revenue minus your costs.

“Profits also differ from cash flow in that it will sometimes be affected by non-cash items like depreciation,” explains Kochar.

The cash flow statement: A short intro

The cash flow statement is a financial document detailing where a company’s money is coming from and where it is going over a given period. More specifically, it records:

- cash inflows: how much money is coming into the company’s accounts

- cash outflows: how much money is going out of the company’s accounts

While cash flow statements can be prepared monthly, quarterly and semi-annually, they are more often prepared annually.

So, where can you start to understand your cash flow? Kochar explains that flow from operations are the most critical component to examine.

“This is where you start your analysis because all other activities, like investing and paying back creditors, depend on the state of your business operations,” says Kochar.

How to prepare an annual cash flow budget

A cash flow budget estimates all cash receipts and expenditures that are expected to occur during a given period. It can help you make sure you have cash on hand when, for instance, there’s a big order coming up and you need to buy large amounts of inventory.

To prepare an annual cash flow budget, you essentially need to write down all estimated future income and expenditures.

“Amongst other advantages, doing a cash flow budget helps business owners understand their borrowing requirements,” explains Kochar.

With a budget in hand, the next step is to compare actual results with your budget on a monthly basis. Businesses will usually use management reports and performance dashboards to keep track of key performance indicators such as the health of their cash flow.

Ratios to keep track of cash flow

Although not calculated using the cash flow statement, the quick ratio and the current ratio are two financial ratios that can help you understand and keep track of your cash flow. Here is a short summary of both.

- Quick ratio: The quick ratio, also called the acid test or the cash ratio, is your available assets divided by current liabilities. It lets you know if your company has enough money on hand to pay your bills and staff.

- Current ratio: The current ratio is the difference between current assets and current liabilities. It measures your business’s ability to meet its short-term liabilities when they come due. Note that the quick ratio provides the same information as the current ratio; however, the quick ratio excludes inventory, thus providing a portrait of the company’s immediate liquidity, since inventory, cannot be quickly converted into cash.

What is a cash flow loan used for?

A cash flow loan (also known as a working capital loan) does not require collateral, such as a machine or building, and is approved based on the strength of a business’s operating cash flow.

These loans can be used to finance growth projects such as marketing campaigns, product research or the hiring of salespeople. They are also commonly used when a business goes through an ownership change.

5 tips to manage your cash flow

1. Tailor your customers’ payment terms to your vendor’s term

The quicker you collect, the better your cash flow will be. That’s because you’re turning an expected revenue into actual cash, explains Kochar. “As a general rule, try to match the payment terms you offer to your clients to the terms offered by your suppliers. To be more specific, don’t extend your customers’ terms above and beyond what your vendors are offering you.”

For example, if your vendors are expecting payment within 30 days while you are asking your clients to pay within 90 days, your cash flow will be negatively affected. To improve your cash flow, adjust your terms to 30 days.

2. Offer early payment discounts

Another simple way to improve cash flow is to offer early payment discounts to your customers.

Early payment discounts are those that vendors or suppliers offer to their customers for paying their invoice or bill within a certain period. “For example, you could offer a discount of 2% if the clients pay within 10 days,” Kochar says. Conversely, you can charge interest if the client pays in 90 days, since your terms stipulated that payment had to be made within 30.

Both approaches create a strong incentive for customers to pay their bills early, which helps your cash flow by bringing in the money sooner. And if the bill is paid late, the interest charged means there is some extra cash on hand when a payment is eventually made.

3. Take the longest possible amortization on loans

Choosing the longest possible amortization period on a loan reduces each payment and allows businesses to have more financial flexibility.

“My advice is to take longer amortizations, but to make extra payments during periods of stronger cash flow,” suggests Kochar. “It helps preserve healthy cash flow during periods when money is tighter.”

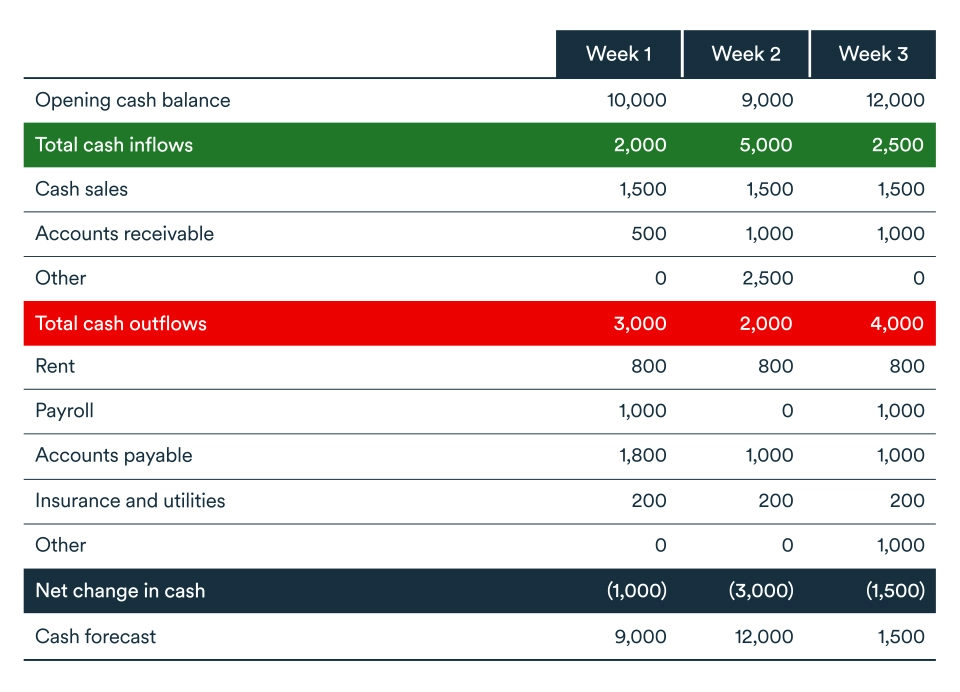

4. Complete a cash flow projection

Prepare a cash flow projection for the coming year.

Using a spreadsheet or accounting software, write down expected monthly cash inflows and outflows, including anticipated big-ticket purchases. These projections will allow you to anticipate slow periods and work out solutions in advance.

“This becomes especially important in a seasonal business, when you have highs and lows throughout the year,” Kochar says. “Looking historically at how much you make and spend will allow you to plan accordingly and be prepared for the future.”

5. Choose and use the right tools

There are three types of tools that can be useful for managing cash flow: accounting software, cash flow planners and dashboards.

Accounting software helps prepare cash flow projections, track your bills to avoid late fees and interest, and track unpaid accounts. However, you’ll need the right tool for the job.

“At BDC, we can help you select the right financial reporting tools,” Kochar says. “A manufacturer, for instance, needs to manage inventories and will not have the same needs as a service provider.”

Cash flow planners are spreadsheets comparing all the money coming in and going out of your business over a given period. They help you determine how much cash you can expect to have in your bank account at the end of that period. They help ensure you have sufficient cash to pay your bills and avoid a cash flow crunch.

Dashboards are a component of accounting software and lists incoming and outgoing money for the previous month. They help you understand your cash position.

“They’re a powerful tool,” says Kochar. “You may think you’re in a great position because you just made a sale of $100,000 with a 20% profit margin, but dashboards will remind you that your bank account is negative $70,000 because you have not collected the money yet.”

Next step

Discover ways to manage cash flow for your business by downloading BDC’s free guide, Taking Control of Your Cash Flow.