Inventory

Inventory is often one of the most valuable assets that a business owns. It consists of items in various stages of production, as well as finished products and the supplies used to support operations.

Managing inventory is important for keeping customers happy and production chugging along. “You want enough inventory to be able to offer what you’ve promised your clients,” says Patrick Choquette, a Senior Business Advisor with BDC’s Advisory Services who coaches business owners on operational efficiency.

But inventory is also expensive to maintain, with annual carrying costs ranging from 20% to 30% of the inventory’s value. “You don’t want to have excess inventory of any type on your shelves,” says Éric Trudeau, CPA, a fellow Senior Business Advisor with BDC’s Advisory Services, who holds CPA and CMA designations. “If you have $1 million in excess inventory, you’re paying $200,000 to $300,000 a year just to maintain it.”

The best inventory is inventory you don’t have. If you really need to carry something, the less you have the better.

Éric Trudeau

Senior Business Advisor, BDC Advisory Services

What are the four main types of inventory?

There are four main types of inventories, which can be grouped into two larger categories. The first category counts items in various stages of production:

1) Raw material—Items that will become part of the final product. These can be goods that require further processing (e.g., steel, chemicals) and goods ready for use (e.g., buckles, shipping material).

2) Work in process (WIP)—Partially completed items that are being produced.

3) Finished goods—Items that have completed the production process but aren’t yet sold.

The second category of inventory covers goods that are used in the production process:

4) Maintenance, repair and operation (MRO) supplies—Goods that are used to support any operational process, examples being lubricants, office supplies and protective equipment.

Found within each of the four types is a certain amount of inventory for which no demand exists, also known as “dead stock.” These are goods that can’t be sold or aren’t needed for production, but still exist on the balance sheet and on the production floor (or on the shelves).

Being able to forecast demand with a certain level of accuracy is key to inventory management.

Éric Trudeau

Senior Business Advisor, BDC Advisory Services

How to manage inventory

Optimal inventory management allows you to keep inventory—and thus carrying costs—to a minimum, while achieving desired service levels and satisfying production needs.

“The best inventory is inventory you don’t have,” Trudeau says. “If you really need to carry something, the less you have the better. There’s no risk or cost related to not having inventory, especially if you can get items quickly enough from suppliers that you don’t miss opportunities with your clients.”

Here are five steps to help you manage your inventory successfully:

1. Create a process of accountability

Appoint someone to manage inventory. They should be responsible for:

- ensuring inventory is kept at optimal levels to achieve your service levels and production goals

- instituting good inventory controls to ensure stock is properly recorded and safeguarded from loss

- holding regular meetings with your sales, marketing, production and finance teams to review inventory levels, reordering, sales forecasts and operational needs

- setting, monitoring and reporting key performance indicators to ensure continual improvement in inventory management

2. Set your business goals and service levels

Make sure you have a well-defined business model and understand your goals, customers and value proposition. This will allow you to determine service levels for various customer segments. Do you need to have the product available right away, or can it wait?

“It starts with knowing what you’re trying to accomplish with your clients,” Trudeau says. “Then you can set up the appropriate process to serve them well and efficiently.”

Regularly review your goals and service levels with your team to ensure they’re in line with evolving circumstances.

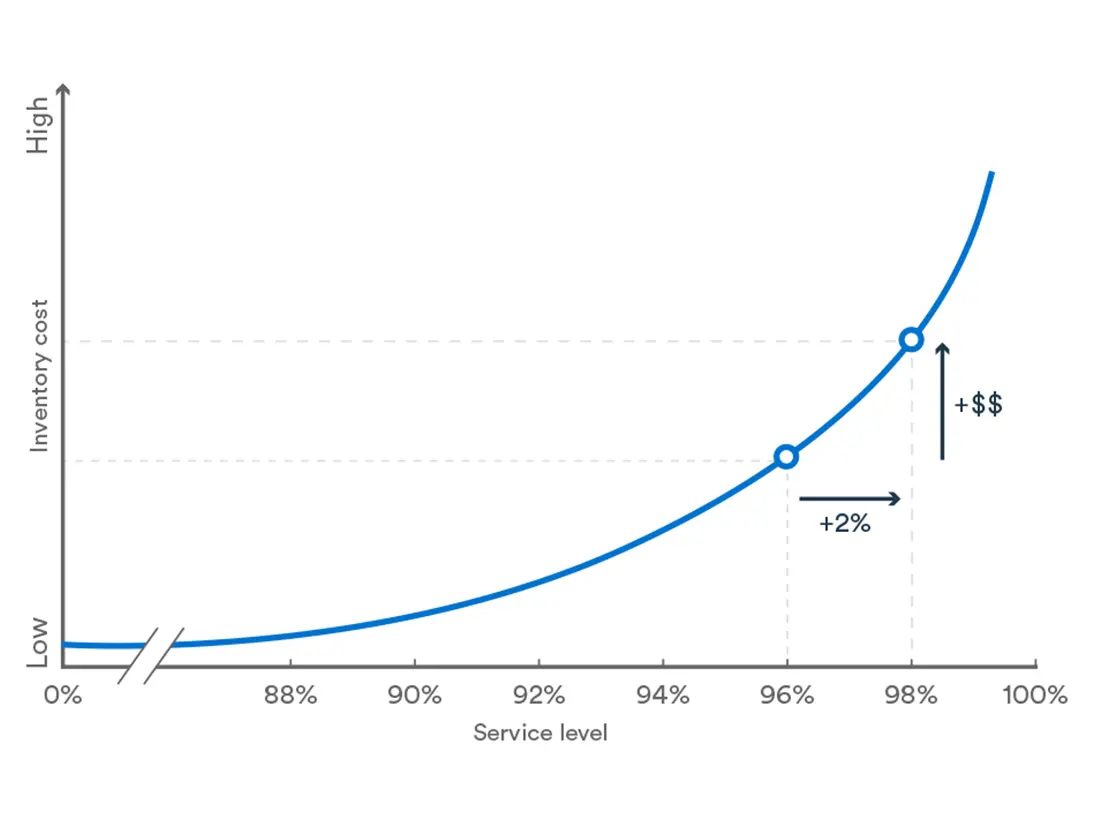

A small improvement of your service level can represent a large cost increase

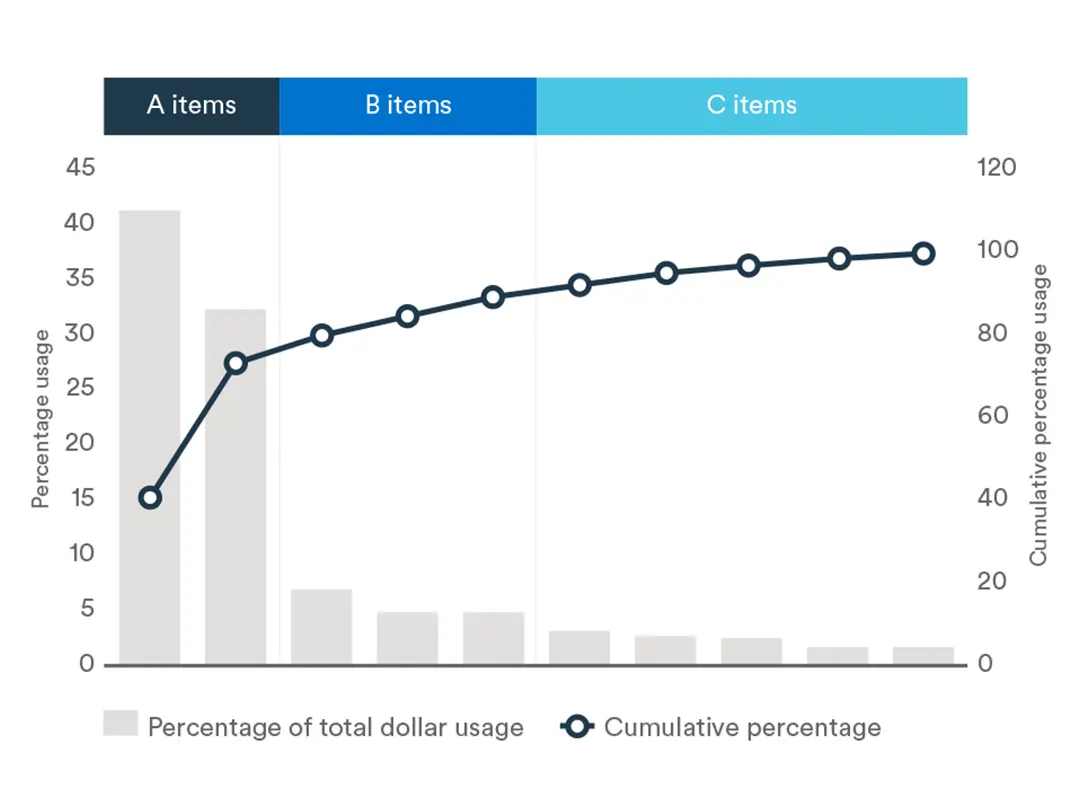

3. Classify your inventory

Next, classify all items in your inventory based on their turnover ratios and value to your company. “It’s important to understand the way inventory gets sold or used so you can manage it properly,” Trudeau says.

A common approach to classifying your inventory is the ABC method:

- Category A: Items with high turnover, good margins or high production importance that you can’t afford not to have in stock.

- Category B: Items with moderate or low turnover or value that you still need to keep in stock.

- Category C: Low-volume items that you can carry in minimal quantities or offer on demand only.

It’s important to regularly update your categorizations. You may need to move an item to a different category as purchase trends and other conditions evolve. “Just because you’ve been selling 1,000 units every day doesn’t mean you’ll always keep up that pace,” Choquette says.

Example of an ABC analysis for inventory use

4. Choose an inventory management system

At this point, you’re ready to put in place an inventory management system. You’ll need to set out maximum and minimum quantities for each inventory item and create a reordering plan.

“Your minimum stocks should be different for every item based on how much you sell or how much of it your team uses in production,” Trudeau says. “By knowing the category of each SKU, you can better plan your new system.”

Appropriate levels for each item should also take into account:

- carrying cost of the item (e.g., storage space, utilities, insurance, shrinkage, financing, risk of obsolescence)

- ordering cost (e.g., shipping, tariffs, procurement)

- “stock-out” cost (the potential cost in lost sales or delayed production from not having something in stock)

- reordering lead time via your suppliers

Sales forecasts are another crucial consideration for knowing how much to order of various items. “Being able to forecast demand with a certain level of accuracy is key to good inventory management,” Trudeau says. “If you don’t, you expose yourself to having a lot of dead stock and parking a lot of money in inventory. It’s very important that forecasts are done as accurately as possible and reviewed often.”

People in different departments often work in silos, but they all need to have input into inventory management.

Patrick Choquette

Senior Business Advisor, BDC Advisory Services

Because there’s so much to track, it’s a good idea to invest in digital technology to help you manage your inventory. Enterprise resource planning systems typically have an inventory management module. You can also buy stand-alone inventory management software.

But as useful as such systems are, you shouldn’t simply execute the systems’ purchasing or production recommendations without some analysis. “It’s important to do your own forecasts and have a proper discussion about your business,” Choquette says. “Too often, we see people blindly following the system’s recommendations. It should be seen as a tool that supports your decision and not some artificial decision machine where you become an order taker.”

Trudeau agrees. Another common mistake, he says, is to make bulk orders just to obtain the accompanying discounts, without weighing the extra carrying costs. “If you get a 10% discount but you have to hold extra inventory for a year, you’re losing money.”

5. Develop solid inventory controls

It’s important to develop solid controls over what’s in your inventory. This means systems that reliably and accurately know what’s in stock and safeguard it from loss.

6. Optimize your efforts

Optimizing inventory management isn’t a one-off exercise. It’s a continual process. Choquette recommends holding, at a minimum, monthly meetings and, ideally, weekly ones for the team to review the status of in-transit items, possible shipment delays and changes to sales forecasts.

“People in different departments often work in silos, but for this they all need to have input and accountability,” he says.

Discussions about inventory management can even inspire initiatives to improve processes in other parts of your business. For example, improving your supplier relationships or production planning may allow you to hold on to less raw material or WIP. “The tighter your processes, the less material you’ll to need to store,” Trudeau says.

It's important to use key performance indicators (KPIs) to gauge your inventory management and any improvements. Commonly used KPIs for inventory management include:

- service level ratio: the percentage of customer orders filled on time

- inventory turnover ratio: cost of goods sold as a portion of the average inventory value in a given period

- inventory count accuracy: actual inventory stock as a portion of recorded inventory quantities

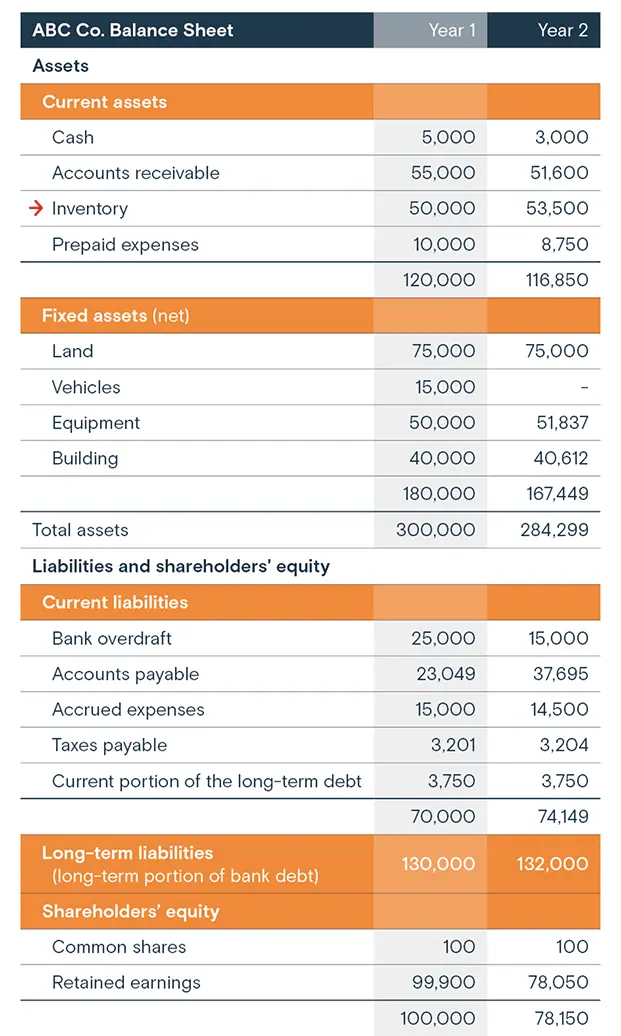

Is inventory an asset or liability?

In accounting terms, inventory is considered an asset. On the balance sheet, it is recorded as a current asset because businesses typically use, sell or replenish it in less than 12 months.

Example of inventory on a balance sheet

Keep in mind that the value of inventory on balance sheets may be inflated because it often includes items that have since been marked down or written off.

What is inventory control?

Inventory control involves using systems to accurately determine what’s in stock and safeguard it from damage, theft or other loss.

“Most businesses have discrepancies between what’s in the system and what’s on the shelf,” Trudeau says. “You need to be able to make decisions based on facts, so having accurate inventory numbers is critical.”

Inventory control involves taking these steps:

1. Physically organize your stock

Label or tag inventory items with clear and consistent descriptions, numbering and units of measure.

2. Create an inventory recording system

You should have a system to record your current inventory and update it regularly. It should include breakdowns by inventory category and include when items were bought, where they’re located in your facility and how to reorder them.

It’s important to make sure that inventory transactions are entered in the system in a reliable, accurate and timely fashion.

You need to know where all items are located and in which quantity; this will significantly reduce time wasted searching for things.

3. Do regular inventory counts

Regularly do a physical count of your inventory to make sure your actual quantities are consistent with what’s recorded in your system.

A monthly count is suitable for most businesses, but some companies may need to do it more frequently, especially for higher-volume items. “Some businesses may count their Category A items every day, and their Bs and Cs every week,” Choquette says.

4. Physically safeguard your inventory

Since inventory may be one of your company’s most valuable assets, it’s important to keep it safe. This includes implementing controls to protect it from:

- theft

- being misplaced

- damage during handling or transport

- damage from fire, water, infestation, heat, cold and humidity.

You may also need to address possible hazards to your employees from certain types of inventories, such as chemicals, and heavy or sharp items.

What happens to excessive inventory?

Excessive inventory, or dead stock, can use up a lot of capital, as well as storage space. “Dead stock drains cash flow because of the carrying costs, skews the value of the business and sacrifices opportunity because the capital is tied up and can’t be used for other revenue-generating activities,” Choquette says.

What should you do about dead stock? Here are three steps to follow:

1. Promptly identify it

If you’re regularly reviewing your inventory, you will surely spot items that aren’t moving. Decide how long different items can sit on the shelf before you consider them dead stock.

2. Develop a liquidation strategy

Come up with ways to get some money or benefit out of dead stock. You could sell it to customers or employees at a discount, give sales reps extra incentives to sell it, or give it away to charity or to employees as a perk.

3. Address the causes

Investigate why you have the dead stock. “Look for root causes,” Trudeau says. “Maybe a process wasn’t followed or one was lacking, or someone wasn’t trained. Maybe the market evolved. The better you are with your forecasts, the sooner you’ll know if you have any excess and the better positioned you’ll be to liquidate it and not buy any more.”

How does inventory relate to supply chain management?

The management of inventory and supply chains is intertwined. If your supply chain is flexible and reliable, you will likely hold less inventory without service levels being affected. “If your processes are in line, you can minimize how much inventory you need,” Choquette says.

Trudeau agrees: “Managing your supply chain is the first element I would work on to make sure you don’t have excess inventory, before even talking about inventory management or controls.”

He also recommends having more than one supplier, especially for critical SKUs.

How do you set up warehouse inventory?

Your warehouse should be organized in a way that minimizes the need for movement of people, equipment and material. This reduces wasted time and effort.

An efficiency expert can help you reorganize your facility to optimize the layout. The exercise typically involves mapping your facility, as well as streamlining the flow of people, products and information.

For example, when optimizing an inventory warehouse, it’s a good idea for the most high-volume items to be easily accessible. “You need to understand what you’re selling in order to organize the warehouse,” Trudeau says. “If you sell a lot of one thing, it should be at the front instead of somewhere in the back or on a high shelf.”

How do you calculate average inventory?

Average inventory is calculated over an accounting period and uses this formula:

Next step

Discover how to set KPIs and ensure you always have the right amount of inventory on hand by downloading the free guide, Inventory Management.