Current ratio calculator (Working capital ratio)

Profitable businesses go bankrupt all the time. All that needs to happen is a few missed payments due to accounts receivables and payables not lining up well.

Though the reasons may vary, growing companies often run into cash flow problems because they need increasing amounts of working capital to pay for the inventory and employees they need to grow.

Tracking the current ratio, also called the working capital ratio, can help you avoid this all-too-common pitfall.

What is the current ratio?

The current ratio is the difference between current assets and current liabilities. It measures your business’s ability to meet its short-term liabilities when they come due.

Current refers to money you need and use in your short-term operations. This means that working capital excludes long-term investments in fixed assets, such as equipment and real estate.

Current assets include: cash, short-term investments, pre-paid expenses, accounts receivables and inventories.

Current liabilities include: credit card debt, accounts payable, bank operating credit, the portion of long-term debt expected to be repaid within one year, accrued expenses and taxes payable.

However, which elements are classified as assets and liabilities will vary from business to business and across industries. not every business—and every industry—will fit precisely into such a range.

How to calculate the current ratio:

Formula

Complete the fields below:

What is a good current ratio?

"Banks like to see a current ratio of more than 1 to 1, perhaps 1.2 to 1 or slightly higher is generally considered acceptable," explains Trevor Fillo, Senior Account Manager with BDC in Edmonton, Alberta.

"A current ratio of 1.2 to 1 or higher generally provides a cushion. A current ratio that is lower than the industry average may indicate a higher risk of distress or default," Fillo says.

Some businesses may prefer an even higher current ratio, say 2 to 1 or 3 to 1.

But Fillo says a very high current ratio is not always best practice.

"If a company has a very high current ratio compared with its peer group, it indicates that management may not be using its assets efficiently," explains Fillo.

However, a higher current ratio—meaning a business is cash-rich—may be acceptable if planning an expansion or major purchase.

Another reason to run a higher current ratio is to weather economic uncertainly. For business operators who want a cushion and security— to deal with such uncertainties as fires, floods, COVID-19 or other events—a higher current ratio can be helpful.

"If you want to prepare for unexpected tough times, you might feel comfortable in having some money on the side," says Fillo. “For some people, running a higher current ratio may help them sleep better.”

Paying attention to the current ratio allows you to correct issues quickly, as they arise.

Trevor Fillo

Senior Account Manager, BDC

Why use the current ratio?

Keeping track of your current ratio, will help you identify early warning signs that your business doesn’t have sufficient cash flow to meet current liabilities.

Fillo advises calculating a current ratio each month—or at a limit quarterly—and then watching for trends. The ratio may fall below 1 to 1, but Fillo says as long as that's only an exception rather than a trend, a business is in good shape. He does warn that doing the calculation only annually may end up with you finding problems too late—and being able to take action to rectify the situation.

"Paying attention to the current ratio allows you to correct issues quickly, as they arise," Fillo explains.

Keeping an eye on your current ratio will also give you a better sense of how much liquidity you can devote to new opportunities and can help you gain better credit terms.

Example of a current ratio calculation

Let's look at a business like a corner store that sells chocolate bars. Each week there is money coming from the sale of chocolate bars. That cash provides money to cover operations, including part of the wages paid, and also is available when the chocolate bar company delivers a new supply the following week. Money is coming in and going out—so a current ratio just above 1 to 1 would be fine.

A different company doing project work may not see payment until the job is completed. Consider a hypothetical house building company; in many cases, a lot of money will have to be spent—on such things as property, wages and materials—without regular cash inflows. The company is only paid when the property is sold. In such a case, a higher current ratio—for example, 1.3 to 1—might be more appropriate.

How to calculate the current ratio using a balance sheet?

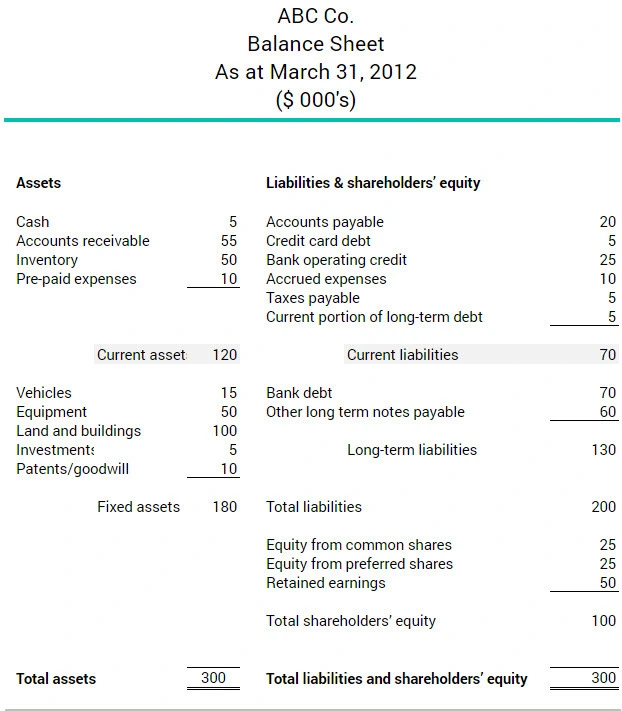

Current assets are listed on the balance sheet from most liquid to least liquid. Cash, for example, is more liquid than inventory. In the example below, ABC Co. had $120,000 in current assets with $70,000 in current liabilities.

Current ratio = $120,000 / $70.000 = 1.7

The business has a very healthy current ratio of 1.7.

What is the difference between the current ratio and the quick ratio (acid test)?

The quick ratio provides the same information as the current ratio, however the quick ratio excludes inventory. The quick ratio therefore provides a portrait of the company’s immediate liquidity, since inventory, which cannot be quickly converted into cash, is not taken into account. Note that the quick ratio applies mainly to businesses that have inventory, as opposed to service businesses.

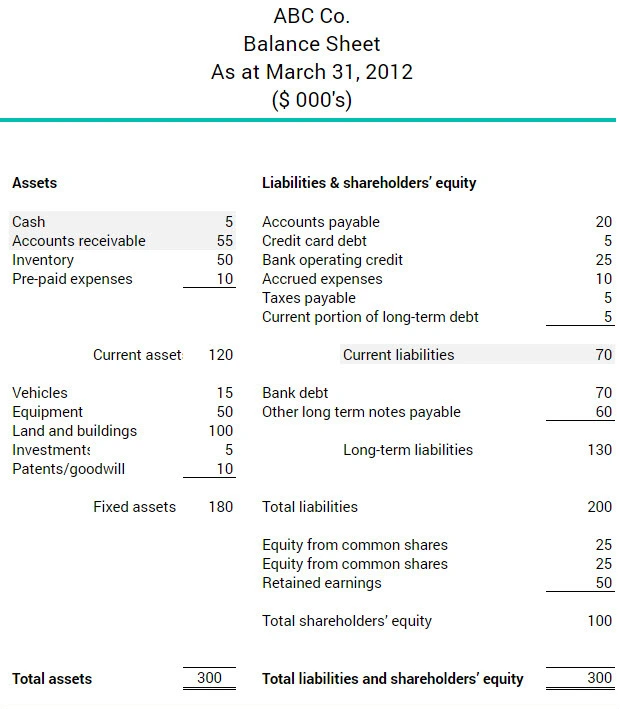

Based on the balance sheet excerpt below, ABC Co. would calculate its acid-test ratio as follows:

Quick assets (cash + accounts receivable) / current liabilities

$5,000 + $55,000 / $70,000 = 0.86

This means ABC Co. has 86 cents to cover each $1 of bills it has to pay. It may want to create more quick assets to get the ratio to 1:1.

Learn more by reading our guide Taking Control of Your Cash Flow: A Financial Management Guide for Entrepreneurs.