Quick ratio calculator (acid test ratio)

The quick ratio, also called the acid test ratio or cash ratio, calculates whether a company can meet a sudden demand from its creditors with liquidity, which includes cash as well as temporary investments and readily marketable securities that can quickly be converted into cash.

Although not widely used by financial institutions, this ratio can tell you a lot about your company’s ability to meet its short-term financial obligations.

What is the quick ratio

The quick ratio lets you know if your company will be able to meet its immediate financial obligations—whether its available assets are sufficient to pay its current liabilities.

“For available assets, we look to cash or securities, which fluctuate very little and are very easy to sell. These would include Treasury bills or money market mutual funds. In other words, you have to be able to quickly access these assets. That means you make the transaction and then have the money in your account the next day,” explains Pierre Lemieux, Manager, Business Centre at BDC.

Also included in this type of asset are accounts receivable. “Provided that your accounts receivable portfolio is relatively healthy, meaning that they are collected within a normal operating cycle for your industry,” says Lemieux.

Short-term financial obligations include salaries payable, accounts payable, credit cards and line of credit, current portion of long-term debt and accrued expenses—these are expenses that don’t require an invoice (such as a monthly rental payment) or have not yet been invoiced.

How to calculate the quick ratio?

Formula

Complete the fields below:

What to include in the quick ratio calculation

| Available assets | Current liabilities |

|---|---|

|

|

Example of a quick ratio calculation

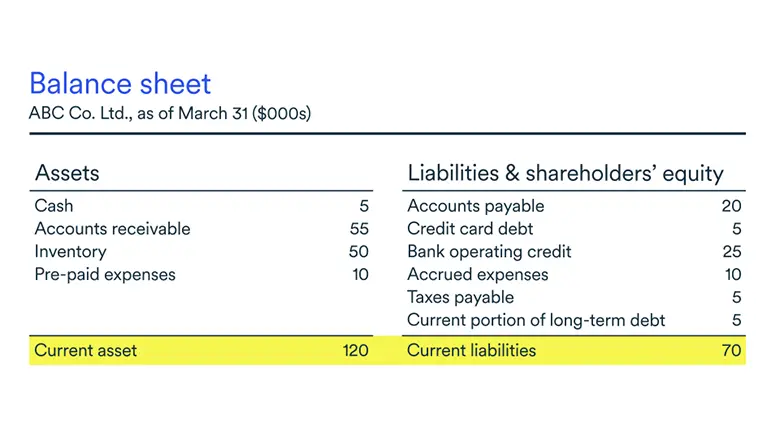

To better understand the ratio, let's take the above example of the ABC Company.

In the above balance sheet, the ratio is calculated by adding together the $5,000 cash and the $55,000 accounts receivable for a current asset of $60,000. It’s worth noting that inventory and prepaid expenses are not included in the calculation, since they cannot be easily converted to cash.

On the liabilities side, the company has:

- $20,000 of accounts payable

- $5,000 in credit card debt

- $25,000 on its line of credit

- $10,000 in accrued expenses

- $5,000 of tax payable

- a $5,000 current portion of long-term debt.

The total current liabilities are $70,000.

This would be calculated as follows:

Interpreting the quick ratio

A low quick ratio could means that your company is having difficulty meeting its obligations and may lose out on opportunities that require quick access to cash.

Liquidating your inventory could improve this ratio if the cash received is used to pay off short-term debt. You may also want to review your credit policies to collect receivables more quickly.

A higher ratio may mean that your capital is being underutilized. You may instead want to invest more of your capital in projects that drive growth, such as innovation, product or service development, research and development (R&D) or international marketing.

What is a good quick ratio?

To understand the quick ratio, you need to remember it relies on items from the balance sheet. The balance sheet is simply a snapshot of the company, while the results of the calculation, whether good or bad, are therefore the result of the company's performance and financial management over the past months or years. The ratio does not take into account future needs and what’s anticipated by the management team in terms of sales or changes in the operating cycle.

The quick ratio reveals whether, in a theoretical liquidation context, the company would have enough cash or cash equivalents to meet short-term financial obligations. This is a static approach.

Although imperfect and incomplete, the quick ratio does provide relevant information. For example, all things being equal, a ratio of 1.2 is preferable to a ratio of 0.8.

With the quick ratio, you can observe year-over-year trends: if you see your company going from 1.1 to 1.0 and then to 0.9, over three years, you’re seeing a deterioration, perhaps due to low profits or inventory management shortcomings.

The ratio can also be used to compare industry averages for similar-sized companies.

It would be wrong to conclude that if your company has a quick ratio of 1.6 and your industry average is 1.4, you won't run out of cash in the next year.

To make sure cash flow needs are met, a dynamic approach is required and future changes in the business cycle must be considered. To do this, there are some important things to look at:

Four elements to assess your liquidity needs

- Sales growth: has a clear impact on the level of inventory to be maintained and the amount of accounts receivable and accounts payable on the balance sheet

- The speed at which accounts receivable are collected: the faster your customers pay you, the less additional cash you’ll need

- Inventory turnover rate: indicates the average amount of cash needed for inventory at any given time

- How fast you pay your accounts payable: the faster you pay, the more overall cash you’ll require

“If the analysis of the company's future operating cycle reveals significant liquidity needs, perhaps a ratio of 1.4 or even 2 is required. But, if the company has few needs, maybe 0.9 will do the job,” says Lemieux.

In any case, the ideal tool to ensure that your business will not run out of cash is a cash budget, also called a cash flow calculator. This forecasting tool, which can be used for monthly forecasts over 12 months or weekly over 13 weeks, considers the anticipated cash flow variations. It allows the company to know if its quick ratio needs are more than 1.2, 1.5 or 1.6.

What explains an increase or decrease in the quick ratio?

Changes in the quick ratio can initially be explained by the changes in your available assets.

Let’s say you liquidate inventory to increase your cash on hand. Your company currently holds $10,000 in cash and $55,000 in receivables, meaning $65,000 in current assets. Your current liabilities remain at $70,000.

If, on the other hand, you decrease your cash on hand, for example, by buying inventory, you will lower your ratio. Let's say your company now has $2,000 in cash and $55,000 in receivables, so $57,000 in current assets. Your current liabilities remain at $70,000.

You can also move your denominator, meaning your current liabilities. For example, refinancing your long-term debt could help lower your monthly payments.

Let's say your company has current assets of $65,000 and decreases its monthly payments on long-term debt by $3,000. With other liabilities remaining unchanged, this would give you a current liabilities total of $67,000 and a quick ratio coming close to 1.

Let’s see what happens instead if the company increases its current portion of long-term debt by $3,000, but other liabilities remain unchanged, resulting in total current liabilities increasing to $73,000.

What’s the difference between the quick ratio and the current ratio?

It is generally accepted that the quick ratio is a more realistic measure of a company's ability to meet its short-term obligations than the current ratio, the reason being that it excludes inventories and prepaid items that cannot be immediately turned into cash.

The quick ratio is generally used as a complement to the current ratio.

Why use the quick ratio?

Including inventory in your company’s current assets can be misleading. “Say the company has a lot of inventory, but much of it is not selling well, or is outdated. That inventory may be included in current assets but, in reality, it is not,” says Lemieux.

The term “acid test ratio” is a fitting term. “The name refers to the acid test used historically to detect gold. If another metal, like pyrite (called fool's gold because for its resemblance to real gold), is detected, it will react differently to the acid than gold would.”

Much like the acid test on gold, the quick ratio can separate the real from the fake. “You have to stop pretending it's gold if it isn't. Inventory can really improve your situation on the surface and give you a ratio of 1.3, but if you remove the inventory, it can drop to 0.7, which is a much less attractive position,” says Lemieux. “It’s best to remove the inventory to get a more accurate picture.”

Next step

Learn more by reading our Taking Control of Your Cash Flow: A Guide for Entrepreneurs.

Our other ratio calculators

BDC recommends

Taking Control of Your Cash Flow

Discover proven ways to better manage your cash flow and gain more peace of mind knowing you can take on any challenge or opportunity. Learn how to build a healthy, durable business with smart cash flow management principles.