Accounts receivable

Accounts receivable refer to the money a company’s customers owe for goods or services they have received but not yet paid for. For example, when customers purchase products on credit, the amount owed gets added to the accounts receivable. It’s an obligation created through a business transaction.

The faster the accounts receivable are paid, the better, since you can use your receivables to pay off liabilities such as accounts payable.

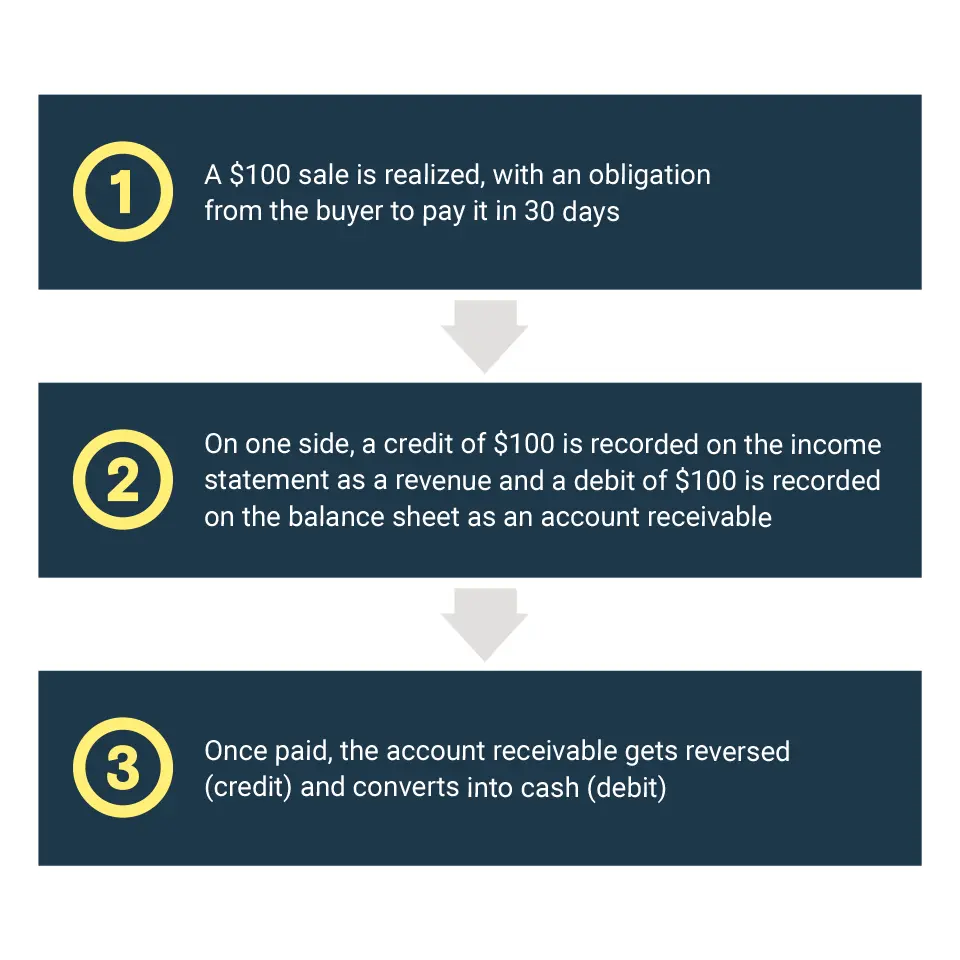

An account receivable is an asset recorded on the balance sheet as a result of an unpaid sales transaction, explains BDC Advisory Services Senior Business Advisor Nicolas Fontaine. “More specifically, it is a monetary asset that will realize its value once it is paid and converts into cash.

An account receivable is recorded as a debit in the assets section of a balance sheet. It is typically a short-term asset—short-term because normally it’s going to be realized within a year.”

What is a trade receivable?

A trade receivable is the most common name for an account receivable and is created through day-to-day business and normal sales transactions.

How an account receivable is created

As long as this monetary asset remains unpaid, it will be considered an account receivable.

Nicolas Fontaine

Senior Business Advisor, BDC Advisory Services

Accounts receivable example on a balance sheet

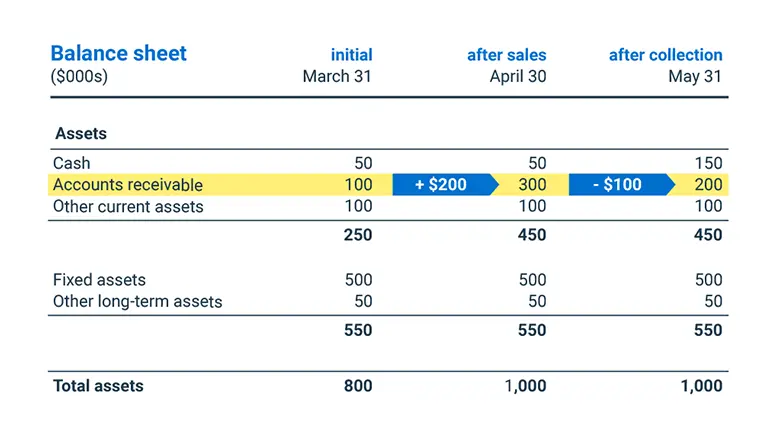

Let’s say your company has an initial balance sheet, as presented below, where accounts receivable total $100,000 on March 31st. For simplicity, we will illustrate just the assets components of the balance sheet.

In the month of April, you record sales on credit of $200,000. For simplicity, it’s the only transaction of the month. You then record an increase in accounts receivable, from $100,000 to $300,000. In the chart below, balance sheet after sales reflects the impact of sales on accounts receivable.

In the month of May, your company collects accounts receivable of $100,000. Again, for simplicity, it’s the only transaction of the month. You then record a decrease in accounts receivable, from $300,000 to $200,000. Balance sheet after collection reflects the impact the collection has on accounts receivable.

Accounts receivable vs. payables

Accounts receivable refer to the money a company’s customers owe for goods or services they have received but not yet paid for. Accounts payable, on the other hand, refer to the money a company owes its suppliers for goods and services that have been provided and for which the supplier has submitted an invoice. Therefore, as part of the same business transaction, one party (seller) records an account receivable for the goods and/or services sold while the other (buyer) records an account payable for the goods and/or services purchased.

Setting up payment terms for accounts receivable

Payment terms (also referred to as “terms of payment” or simply “terms”) are the deadlines and interest charges you give your customers to pay back what you sold them. It’s an important part of the accounts receivable equation.

Terms can differ, depending on your company’s need for cash and the trust you have in your client.

- If you’re in need of liquidity, you might offer customers a discount to pay more quickly so that you can access the funds you need to pay your bills.

- If your product or service has low margins, you may sacrifice that quicker cash with a longer payment timeline. That way, you don’t lose any money on the discounts you give clients as compensation for paying you sooner.

“There’s always a choice to be made between liquidity and profitability,” says Fontaine. “Ideally, you want to reach a balance between the two.”

Negotiating favourable payment terms with clients

Going through a crash crunch? You may want to look at giving favourable terms temporarily, such as a discount, to certain clients in order to shore up some funds.

“Those should first be customers that you have a strong relationship with,” suggests Fontaine, noting that disclosing this to too many might hurt your company’s reputation. He adds that a client should know that you are not offering the standard terms of payment. “There is an understanding that this is for a given period of time.”

Accounts receivable risk assessment

Risk assessment is important in the accounts receivable equation; knowing your client is key to that. If the client is a well-established company, there is a lower risk in extending a lot of credit in high-volume sales. But if they are a company whose future is less than secure, extending a lot of credit for high sales numbers will come with increased risks.

“The terms you’re willing to give to that customer depend on your confidence that you’ll realize this transaction and get the cash. Looking at the customer’s credit worthiness is one way to do this,” he says, adding that he applies a simple yardstick to the timeline each debt requires: “The higher the risk, the shorter the period.”

Who negotiates the terms of payment?

Fontaine says many businesses make the mistake of having sales staff set the terms of payment.

“You need to look at that client not only from a potential business perspective but also from a credit perspective.” He says that when a new lead is found, someone from the financial or accounting side of the company should be involved. If you’re a bigger business, the credit department should research the potential client’s credit worthiness and history.

“If you don't do that, then you'll have a surprise at the end of the process,” says Fontaine. “What’s the point of making huge sales if you can’t collect them down the road?”

How do you collect accounts receivable?

Fontaine offers a simple answer when you ask how to collect accounts receivable: “Ideally, by doing nothing!”

“If the terms are respected, you should be paid within those terms that you've given, whether they’re 30 days, 60 days or anything else. Unfortunately, the reality is often very different.”

If an account receivable does become overdue, a company will typically email an account statement, often following that up with a phone call. The more you apply this principle on a periodic basis, the less you’ll find yourself with collection issues that get out of control.

The way you collect will depend on the size of your clientele. “As your customer base and the number of transactions become bigger, your accounts receivable will also become bigger. At one point, the collection ‘task’ may need to become a collection ‘function’ within your organization if the weight of this task becomes too important,” says Fontaine.

Much of today’s accounting software will have an embedded function in it that will track invoices for the seller and allow for overdue dates to be identified. It will also remind the buyer of agreed-upon payment due dates and have the ability to select those invoices that are needing to be paid.

In the worst-case scenario, some companies sell their unpaid debts at a discount to collection agencies that then collect on the amounts owing.

Provision for doubtful debts

Fontaine recommends going over your accounts receivable and evaluating the quality of each one. “Are the terms being respected, give or take 15 days?”

“You want to be proactive and prudent rather than reactive and have surprises on your income statement.”

Fontaine suggests looking at the quality of your accounts receivable, ideally on a monthly basis. “You don’t want to find yourself in a situation where you suddenly realize that out of all your accounts receivable, 50% are now over 90 days due.”

Fontaine suggests you get to know how many uncollected or overdue debts you typically incur so that you can make provisions for lost payments. You can accumulate these potential debts on the balance sheet, which are referred to as “provision for doubtful debts” (or doubtful accounts).

“You’re creating a liability—a potential bad debt,” he says. “You’re basically recording in advance a future potential expense.” He adds that if you end up collecting for more than your planned provision, you end up realizing a gain and will reverse the provision as income.

What are other types of accounts receivable?

Other receivables are expected payments that don’t fall under trade or regular sales transactions such as tax refunds or advances to employees. A note receivable is also another type of non-trade account receivable. It is the opposite, and falls on the side of the lender, as a promissory note, which is an obligation to pay a certain amount at a certain date and under predetermined conditions.

Free guide on cash flow

Learn how forecasting sales and inventory and shortening customer payment terms can improve your cash conversion cycle. Download BDC’s free guide called Taking Control of Your Cash Flow