Promissory note

What is a promissory note?

A promissory note is a documented promise to repay borrowed money. Promissory notes are binding legal documents used to protect both the lender and the borrower.

The promissory note is paper evidence of the debt that the borrower has incurred. It outlines the amount of the loan, the interest rate to be paid, and either the date when it needs to be paid in full or the repayment schedule.

“Basically, a promissory note is a promise to pay back money. It is probably the simplest representation of a debt. All you need to document on paper is who is lending to whom, the amount, the date of the transaction and when it should be paid back, and both signatures—that’s it!” says Nicolas Fontaine, Senior Business Advisor, BDC Advisory Services.

It is probably the simplest representation of a debt.

Nicolas Fontaine

Senior Business Advisor, BDC Advisory Services

Common example of a promissory note

The most common type of promissory note is for a simple lump sum to be repaid by a certain date.

Example:

You lend your friend John $1,000. John agrees to repay you. The full amount of the loan is due on December 1st, with no payment schedule involved.

How to write a promissory note?

The promissory note transaction involves the borrower and lender agreeing on the terms of the loan and then creating a promissory note to reflect the agreed-upon terms.

The promissory note is issued by the lender, signed by the borrower, and then witnessed and initialized by the lender. Once signed, it becomes a legally enforceable document. The payment terms can be whatever the borrower and lender agree to.

Here are some possible terms of a promissory note:

- The loan will be repaid within 12 months in one lump-sum payment.

- Payments will be made on a monthly basis.

- The loan repayment schedule will run beyond a year, with one portion of the sum (the current portion) re-paid within 12 months and the other portion re-paid after 12 months (the long-term portion).

The most common types of lenders using promissory notes are family, friends and angel investors.

Nicolas Fontaine

Senior Business Advisor, BDC Advisory Services

How does a promissory note work?

Typically, promissory notes are used when companies don’t have access to cash or financing from a lending institution. The promissory note allows them to borrow without a loan guarantee.

Because they are higher-risk investments, funds accessed through promissory notes may be loaned at higher-than-normal rates. Promissory notes are often used by angel investors providing new companies with seed funding.

The most common types of lenders using promissory notes are family, friends and angel investors, but there are also financial institutions that sometimes use promissory notes.

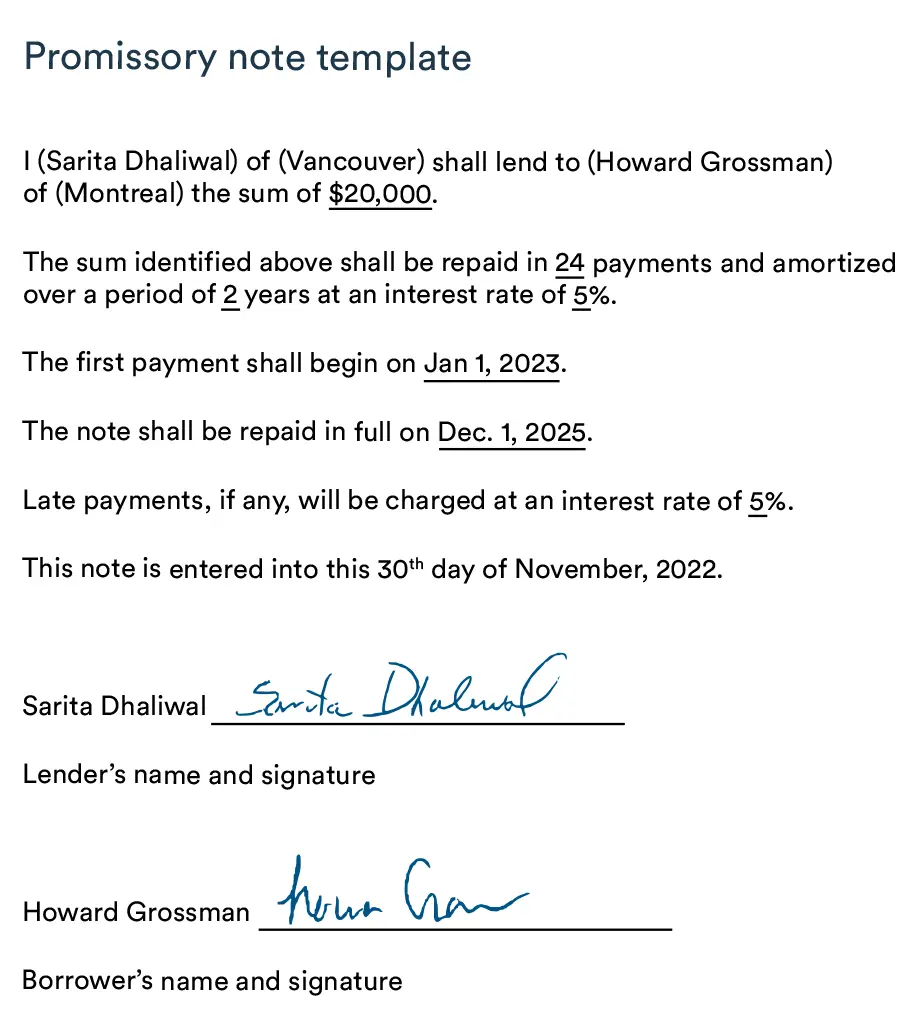

What does a promissory note look like?

There are a variety of different templates for promissory notes, but in general most include the information in the promissory note template example below.

Promissory note example

Free promissory note template

Download our free promissory note template. It’s an easy-to-use tool that will guide you in making sure the terms of your promissory notes are clearly set out.

Who are the parties involved in a promissory note?

Promissory notes typically involve two, and occasionally three, individuals:

- Drawee: The drawee is the lender.

- Drawer: The drawer is the borrower, who agrees to pay the drawee when the promissory note comes due.

-

Payee: The payee is a third party that the drawer (or borrower) has designated to receive the money.

Example: Joan owns company XYZ, which is a start-up. She has signed a promissory note with Stella, who has agreed to lend Joan $1,000 to help with the start-up of XYZ.

Joan is the borrower or drawer, and Stella is the drawee on the promissory note. If, however, Stella decides to transfer the promissory note to her daughter Jill, then Jill becomes the payee.

In most instances, the payee and drawee are the same person. The drawee, or lender, keeps the promissory note until the amount owing has been repaid. Once the loan has been repaid, the payee or drawee cancels the note and gives it to the drawer or borrower.

Features of the promissory note

- It is a written agreement.

- There is a defined amount to pay.

- Documents are signed by both parties.

- Payment is in the currency of the country where the note was signed.

- Contains name of drawer and drawee, principal amount of loan, rate of interest, date of maturity, terms of repayment, issue date, and signatures of drawer and drawee

Where is a promissory note located on a balance sheet?

A promissory note is recorded as a liability. Depending on the terms of repayment, the promissory note could be listed on a balance sheet as a:

- short-term liability if the note is payable in full within 12 months

- long-term liability if the full amount of the note is repayable in more than 12 months

- short-term and long-term liability if a portion of the note is repayable within 12 months, and the balance repayable beyond 12 months

Because promissory notes are usually not secured by a tangible asset, the risk is greater to the lender.

Nicolas Fontaine

Senior Business Advisor, BDC Advisory Services

Is a promissory note guaranteed?

The promissory note is a legal document that is signed by a borrower who promises to pay a debt in the form and manner as described in the note. The note may include a personal guarantee, which is a promise by the borrower to pay the lender. In the event of noncompliance with the terms of the promissory note, the lender has the right to pursue the guarantor in court.

“Typically, in a mortgage situation, the loan is secured by the house. If you don’t pay your mortgage, the bank can repossess your house. In a supplier situation, a vendor note is secured by the goods the borrower is purchasing. If the borrower doesn’t meet the terms of the vendor note, the vendor will take back the goods. Because promissory notes are usually not secured by a tangible asset, the risk is greater to the lender,” says Fontaine.

What makes a promissory note legal?

A promissory note must include the date of the loan, the loan amount, the names of both the lender and borrower, the interest rate on the loan, and the timeline for repayment. Once the document is signed by both parties, it becomes a legally binding contract.

What happens if I default on a promissory note?

Borrowers who do not repay their promissory note (based on the terms in the note) can be sued by the lender. A promissory note is legally enforceable through an ordinary breach of contract claim.

Borrowers who are struggling to meet the terms in the promissory note can reach out to their lender to request an amendment to those terms.

Can the promissory note be changed?

As with any legal document, the promissory note can be amended with the agreement of both the borrower and the lender.

To protect both parties, all changes to the agreement should be clearly documented in an amendment, which would be dated, signed by both parties and then attached to the original promissory note.

Do promissory notes hold up in court?

In general, if the promissory note includes loan terms, legally acceptable interest rates, and the signatures of both the lender and the borrower, it can be upheld in court.

A promissory note is a legal contract and is enforceable in court.

Nicolas Fontaine

Senior Business Advisor, BDC Advisory Services

Is a promissory note the same as a vendor note?

A promissory note is different from a vendor note in that a vendor note is a short-term secured loan that a vendor provides to a customer. The vendor note is a form of vendor financing, which is secured by goods the customer buys from the vendor. If the customer does not pay the vendor note, the vendor would be able to take back the goods, which are securing the loan.

What is a demand promissory note?

A demand promissory note is a loan which must be repaid when the lender demands it. Because the repayment date is unknown to the borrower, this type of loan can reduce the borrower’s flexibility in the use of the loan.

What should entrepreneurs know about promissory notes?

It’s important to remember that a promissory note is a legal contract and is enforceable in court. A breach of contract gives the promissory note lender all the legal means available to them to retrieve their money.

“When you are creating a promissory note, it’s also important to think about whom you will be dealing with throughout the term of the note and how that will impact your organization. Is it an individual or company or a financial institution and what will that mean for you?” says Fontaine.

Promissory notes vs. bank loans

The promissory note should essentially be used as short-term financing. It is not a tool you want to use continuously.

“Because it’s a nonstandard type of financing, the promissory note will typically dictate higher terms, so it’s a type of financing you only want to use if you don’t have any assets you can use as guarantees. As you become more profitable and established, traditional financing will become more easily accessible,” says Fontaine.

What are the advantages of promissory notes?

Promissory notes offer a quick and easy way to access short-term financing. They are often used as seed funding for new organizations, and can be a good resource for new or emerging companies that are unable to secure financing with banks and more traditional financial organizations.

“That’s often the problem—banks will typically finance you when you don’t need financing anymore, and they often don’t want to finance you when you need it! Promissory notes provide you with the opportunity to get your company to a point where you can access that bank financing,” Fontaine explains.

Who signs the promissory note?

The signatures of both the lender and the borrower are required for the promissory note to become an enforceable contract.

Are promissory notes securities?

Businesses using promissory notes need to understand that they are potentially subject to securities laws. If the promissory note is found to be a security, there are significant and serious implications for the business. Ensuring compliance with securities laws can be extremely costly, so most businesses would want to avoid issuing promissory notes that are securities.

Generally, the transaction will not likely be classified as a security if the promissory note:

- has a term of less than nine months,

- is used strictly for business purposes,

- doesn’t provide the lender with any interest or investment in the business.

Promissory notes that are longer than nine months, and/or that provide the lender with interest in the company, are much more likely to be classified as securities. If you are concerned that your promissory note could be classified as a security, you should consider consulting with a lawyer with expertise in the field.