Depreciation

Tangible assets, such as buildings, equipment, vehicles and so on, are purchased in large lump sums. The value of these assets decreases over time after their purchase because of wear and tear (i.e. use of the asset) and obsolescence. Depreciation represents the estimate for how much this value has declined in a given fiscal period.

Accounting standards do not allow us to expense the entire value of the asset in the year they are purchased because their value is derived over a longer period of time—called their expected useful life.

Once this cost is recognized on the income statement, the value on the asset balance sheet is also reduced. This continues until the cost of the asset is fully expensed or the asset is sold or replaced.

Depreciation is an accounting method for estimating that decline over time. It helps businesses match their revenues with costs, including those of assets used to generate revenues.

Businesses need to take this decreasing value into consideration when analyzing their performance and determining the cost of producing their products and delivering services. This allows them to then build reserves to replace these assets once they can no longer be of productive use.

When a depreciation expense is charged to the income statement, the value of the long-term asset recorded on the balance sheet is reduced by the same amount.

This continues until the cost of the asset is fully expensed or the asset is sold or replaced. The Canada Revenue Agency sets annual limits on how much of a long-term asset’s cost can be amortized in a given year. These limits are called capital cost allowances.

How to calculate depreciation

Several methods can be used to calculate depreciation. Business owners are usually familiar with depreciation methods used for tax purposes. These require businesses to spread out the reporting of costs of longer-term assets over the useful life of the asset. The Canada Revenue Agency sets the depreciation rates of different assets according to how it is categorized. Companies often have leeway to accelerate or defer some depreciation to optimize their tax liability.

But depreciation for tax purposes doesn’t necessarily represent a company’s actual costs for use of its fixed assets. It is common and acceptable for businesses to use a parallel depreciation method for financial reporting purposes that more accurately reflects the assets’ decrease in value.

The most common depreciation methods are straight-line and declining balance.

Straight-line method

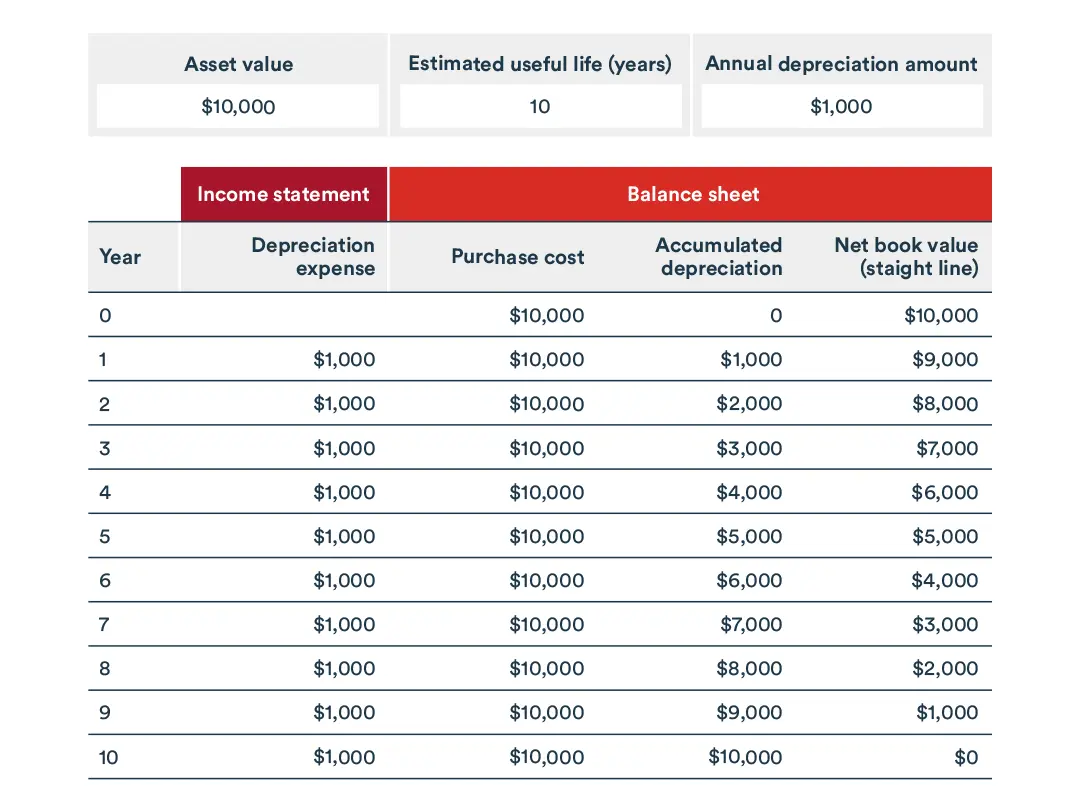

In the straight-line depreciation method, the asset is depreciated by the same amount for each year of its useful life.

For example, for a machine with a $10,000 purchase price, scrap value of $0 and a 10-year lifespan, the depreciation expense is $1,000 each year.

Example of straight-line depreciation

Declining balance method

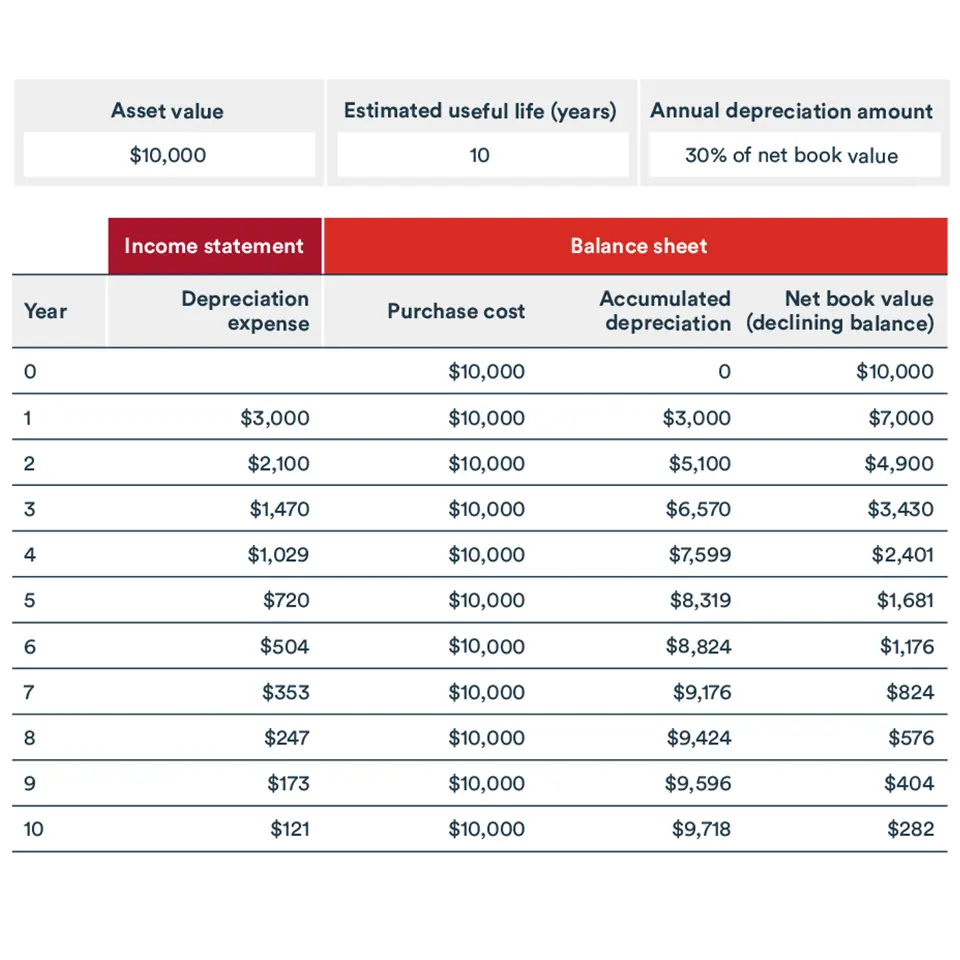

With the declining balance depreciation method, the asset is depreciated by the same rate for each year of its useful life. This method is sometimes used to reflect the fact that assets lose more value early in their life.

For example, for the machine above, using a 30% depreciation rate, the depreciation expense is $3,000 in the first year, $2,100 the second year, $1,470 the third year and so on.

Example of a declining balance depreciation

This is the method required by the CRA, and prescribed depreciation rates are termed Capital Cost Allowance (CCA).

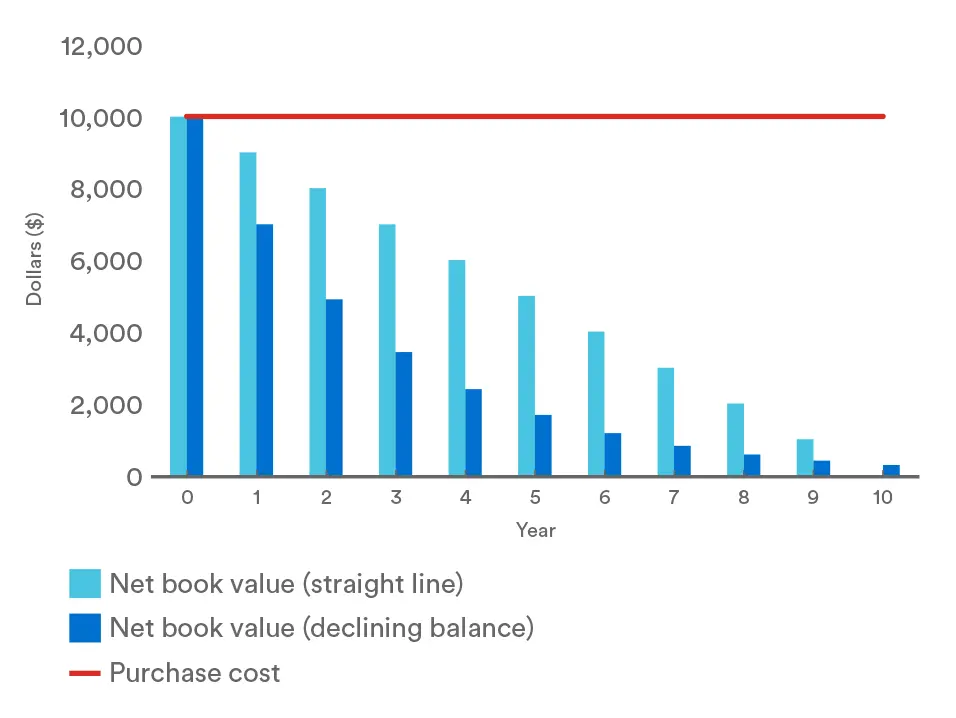

How different depreciation methods affect the value of assets on the balance sheet

Depreciation example

Let’s say a manufacturer has bought a machine-tool. To reflect wear and tear on the machine-tool, as well as the rate at which its use generates revenue, a company might decide to depreciate the cost of the machine using the declining balance method at a rate of 30% per year. It estimates that as the machine gets used, it will become less productive and require more maintenance and repair.

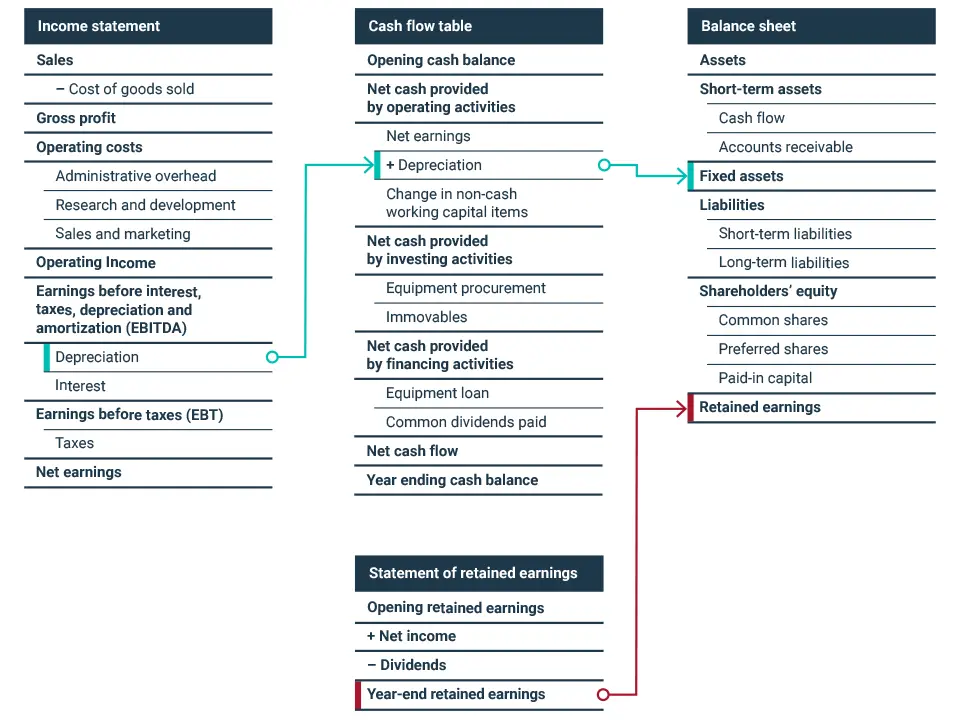

The net book value of fixed assets will be recorded in the balance sheet, and will show up as an expense in the income statement. The depreciation expense for the previous year will be included in retained earnings, under shareholders’ equity. This will continue until the cost of the asset is fully depreciated, or is sold or replaced. The image below shows these links between the various financial statement documents.

Is depreciation an expense?

Depreciation is a non-cash expense, which means that it does not require a cash outflow, but it does reduce the asset’s value. Therefore, since the expense has already been incurred, the depreciation does not affect the company’s liquidity.

However, the depreciation expense is recorded in the income statement. It reduces the earnings before tax and, consequently, the tax that the company will have to pay.

Non-cash expenses, such as depreciation, are often excluded from the calculation of a company’s performance because they are not directly related to its ability to generate cash flow and meet its financial obligations. To assess performance, we will instead use EBITDA (earnings before interest, taxes, depreciation and amortization), which is more directly related to a company’s financial health.

Can intangible assets be depreciated?

Many intangible assets such as a trademark or goodwill, will exist as long as the business is active. These assets cannot be depreciated on the balance sheet, but their value may be re-assessed.

However, the cost of these assets can be amortized for tax purposes over time.

Depreciation vs. amortization

Depreciation is used to calculate the wear and tear on tangible assets, such as equipment and buildings. Amortization is a more general term that can be used for both tangible and intangible assets. Amortization is also used to refer to the amortization period of a loan.

Note that depreciation and amortization do not have the same meaning in French and English.

Understand your financial statements

Depreciation is a key concept in understanding your financial statements. Learn more to understand your financial statements and inform smart business decisions. Download our guide.