Definition

One-time expenses/revenues

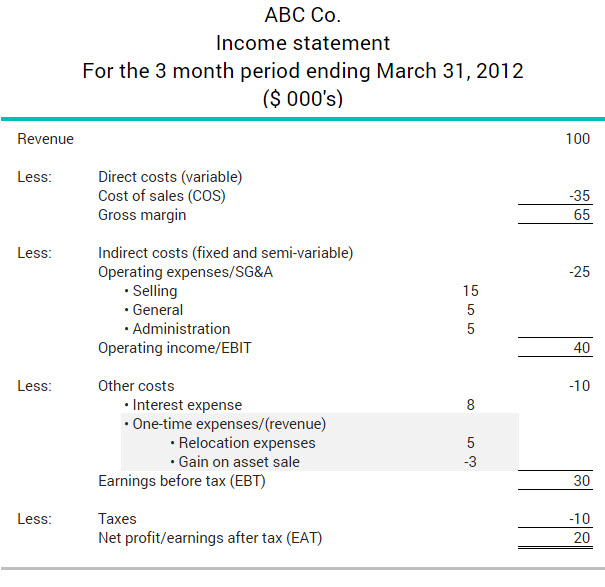

One-time expenses or revenues are non-recurring financial transactions that are not part of a company's regular activities, such as relocating the business or selling a building.

One-time expenses and revenues are not included in the calculation of operating income (EBIT) to ensure the owner/managers get an accurate picture of the company’s operating potential. They are, however, included in net income before income taxes are calculated.

More about one-time expenses/revenues

The excerpt below shows how the one-time expenses and revenues for the examples above appear on the income statement of a retail or wholesale company.