Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreHousing market: Is the roller-coaster ride finally over?

Year in, year out, the arrival of spring heralds the start of the hot season for the real estate market. Just a few years ago, observers were arguing that Canadian real estate was in a speculative bubble. Today, from coast to coast, the talk is of a housing crisis.

Between population growth, housing shortages, the prospect of interest rate cuts, government measures to improve affordability and the announcement of new mortgage rules, it's becoming difficult to get a fix on what's in store for the housing market in 2024. Can we expect market stability? The short answer is not yet.

The spark that goes boom

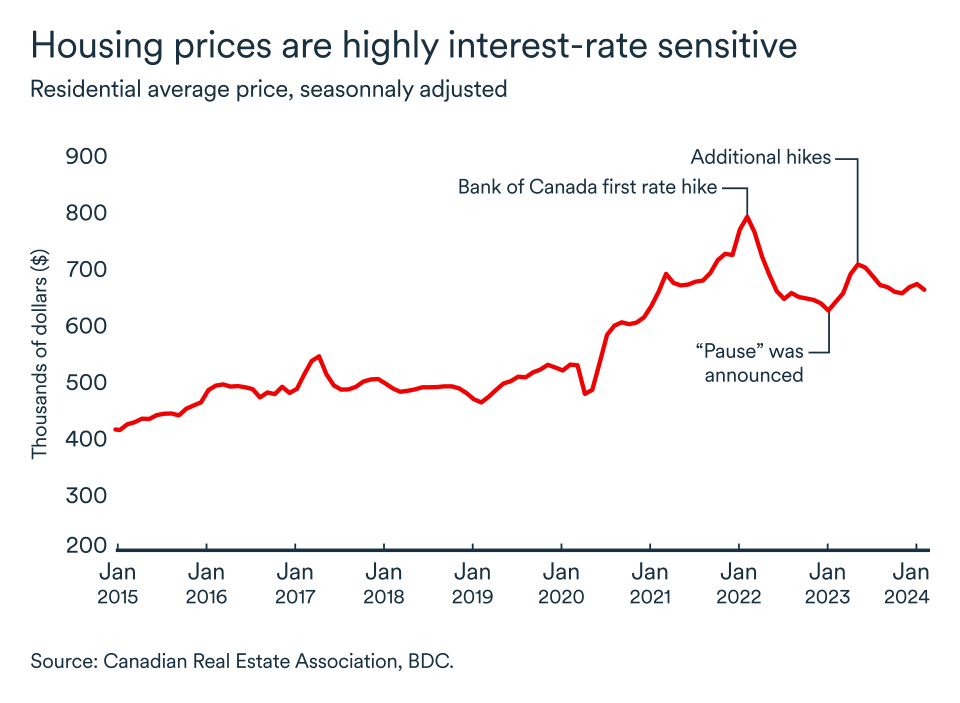

The Canadian housing market is the most interest-rate-sensitive of all sectors. Since the Bank of Canada’s first rate hike in March 2022, the average price of a home has fallen by 16.3%, according to data from the Canadian Real Estate Association.

However, interest rate cuts could quickly reverse the trend. When the Bank of Canada paused rate hikes between January and June 2023, the average home price jumped 13% across the country before rates resumed their upward march.

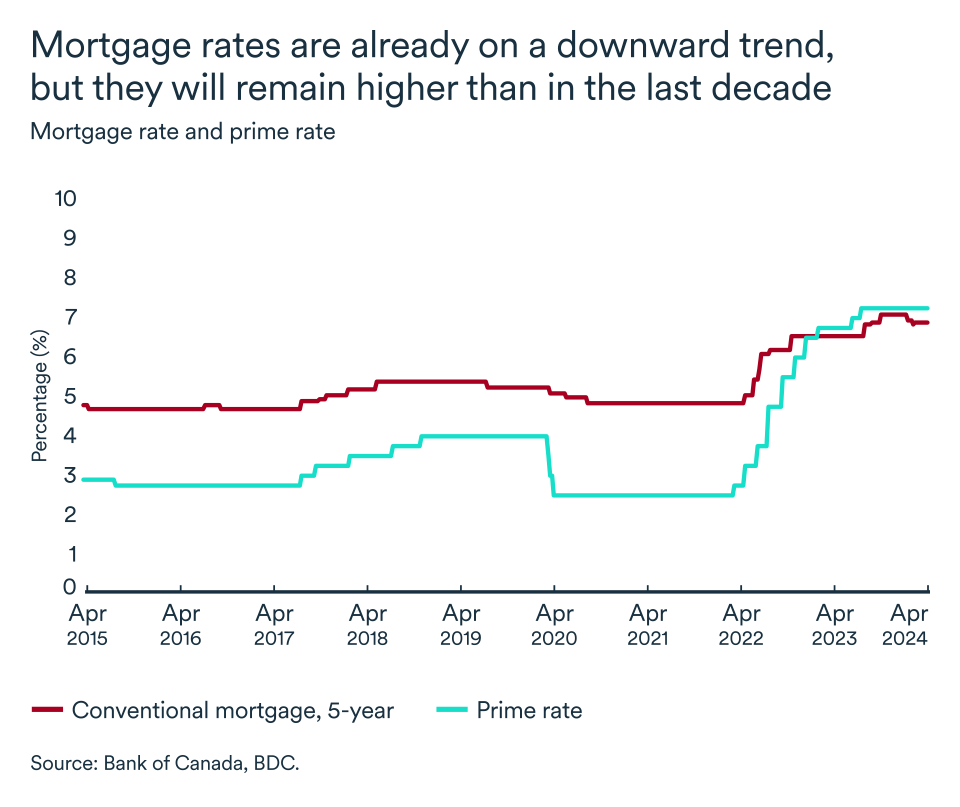

Buyers are already returning to the market, encouraged by the prospect of rate reductions this year. Effective interest rates in the bond market, which serve as a benchmark for mortgage rates, are falling, and households have become increasingly accustomed to dealing with higher interest rates. Lower borrowing costs will help restore some purchasing power for home buyers—provided prices don’t rise too quickly.

A tightrope act in the short term

The central bank could start cutting its key rate as early as June, but it’s likely to be cautious in easing credit conditions, given the potential impact on housing prices and the growing importance of the residential sector for the economy and inflation. Therefore, although mortgage rates will come down in the second half of the year, they could remain higher for longer than you might hope.

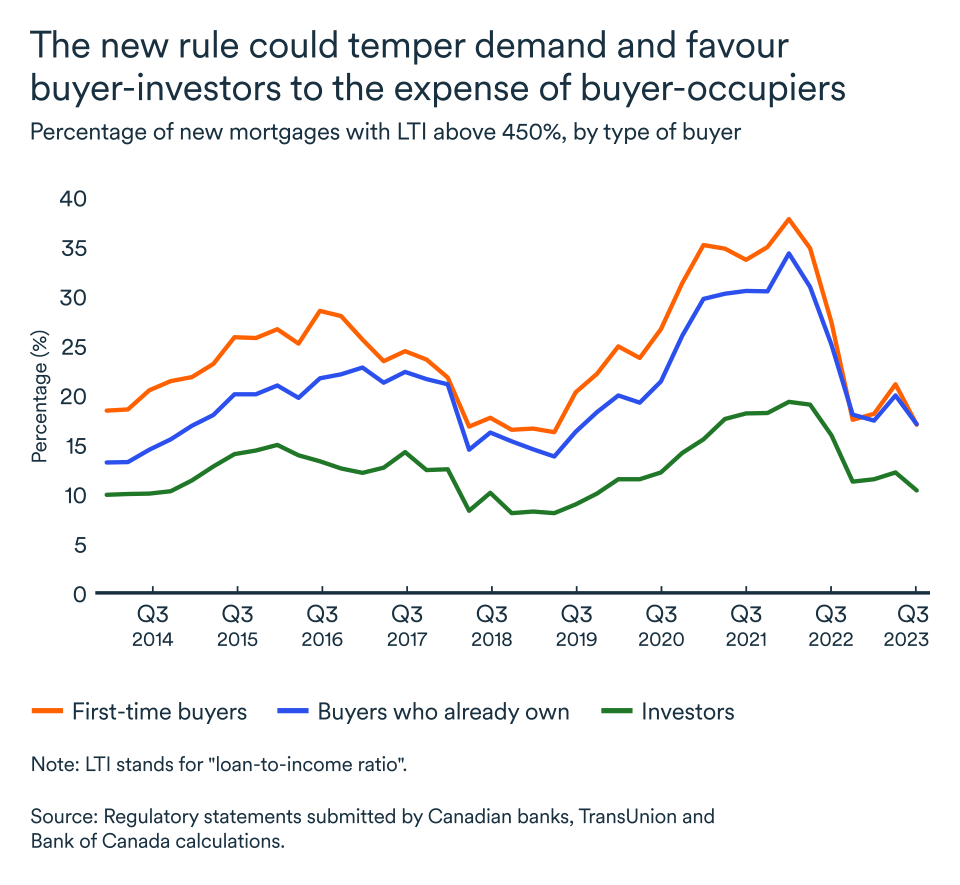

While the Bank of Canada focuses on price stability, the Office of the Superintendent of Financial Institutions (OFSI) is responsible for maintaining the health of the Canadian financial system. The system remains sound, but a new OFSI rule could make it harder for some consumers to get a mortgage.

On the eve of interest rate cuts, OSFI has warned lenders to prepare for a new rule on mortgage management and allocation. Lenders' portfolios will soon be limited in the number of borrowers who can obtain mortgages exceeding 4.5 times their annual income.

According to the regulator, the new limit is designed to help prevent the buildup of risky leverage during periods of low interest rates. The rule involves a portfolio test for lenders, not borrowers directly, unlike the mortgage stress tests introduced in 2018. The new cap is expected to come into force at the beginning of 2025.

The new rule comes at a time when house prices are still high and housing in short supply. There is still much uncertainty over what its impact will be on the market. However, we can expect it to limit new housing starts and the ownership transfers that would normally result from anticipated rate cuts. It could also favour investors to the detriment of owner-occupiers, who are more likely to have a mortgage-to-income ratio over the 4.5 times limit.

The real puzzle is the medium to long term

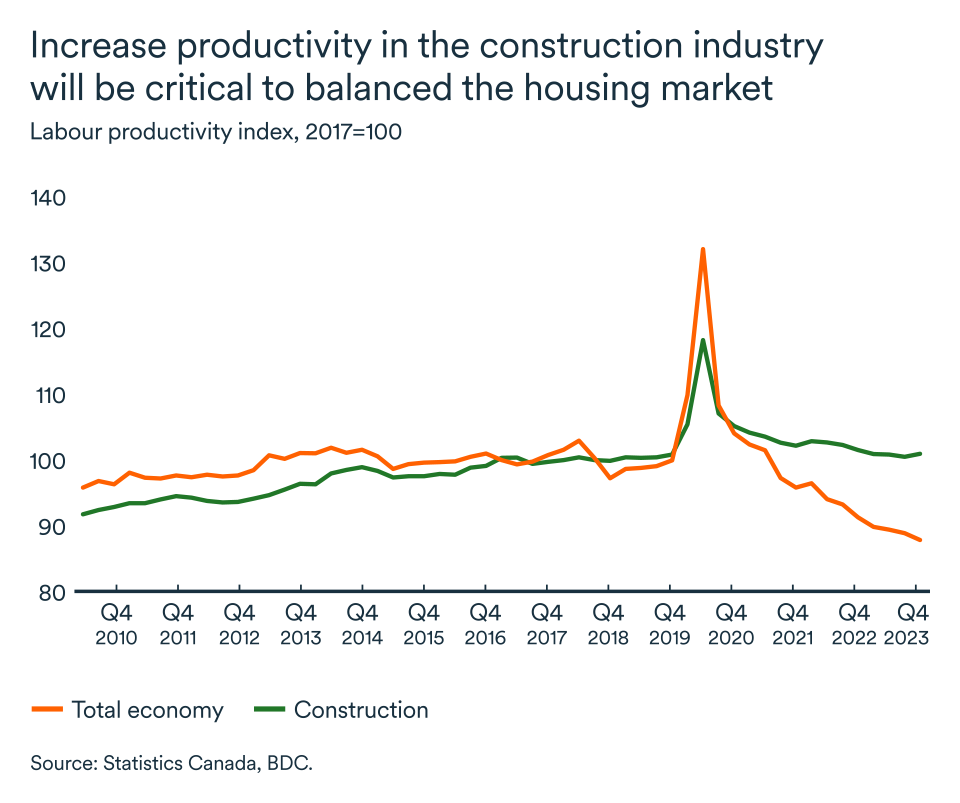

The government wants to restore affordability to the housing market in Canada and encourage new construction to meet the growing needs of the population. According to the Canada Mortgage and Housing Corporation, nearly 5 million additional housing units are needed to solve the affordability problem in the country by 2030.

To achieve this, the annual pace of residential construction would have to triple, at a time when construction productivity is declining and almost a quarter of the industry's workers are set to retire over the next decade.

How does Canada's housing crisis affect your company?

According to a new survey by KPMG Canada, business leaders see the housing crisis as the greatest risk facing the economy. The affordability issue weighs heavily on executives as they strive to attract and retain the staff they need for their operations. Discover three strategies you can implement now to recruit, hire and retain talented staff in a competitive job market.

Businesses in the residential, construction and furniture sectors should benefit from a housing boom triggered by lower interest rates as early as this spring. However, house prices should resume their upward trend as buyers return to the market. This could leave households with less money to spend elsewhere in the economy, especially if rates remain relatively high. Learn how to ensure the survival and prosperity of your business when the economy doesn't cooperate.

The Canadian economy shows resilience

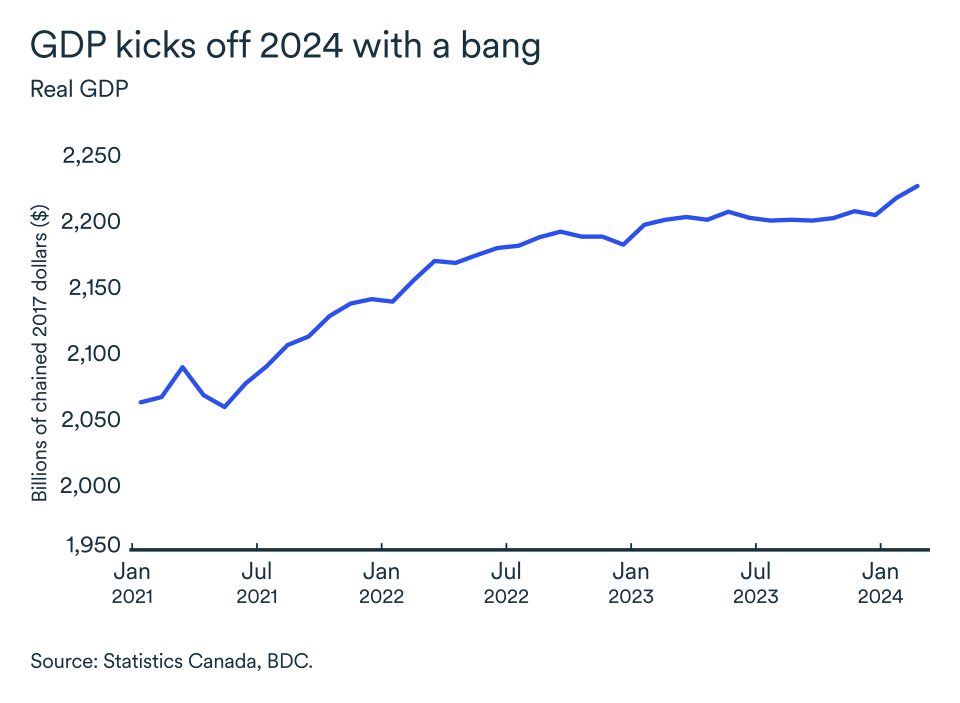

Canadian GDP rose by a strong 0.6% in January, representing a solid rebound from December, when real GDP contracted by 0.1%. The gains appear to have continued in February, according to Statistics Canada, which forecast growth of 0.4% for that month.

The recovery in January was widespread, with 18 of 20 sectors recording gains. The outlook for the first quarter, therefore, looks promising. We estimate annualized GDP growth above 2.0% for the quarter. The Bank of Canada has updated its forecast and now expects growth of 2.8% for the period, an upgrade from its January report when it was forecasting growth of just 0.5%.

Inflation data increasingly point toward rate cuts

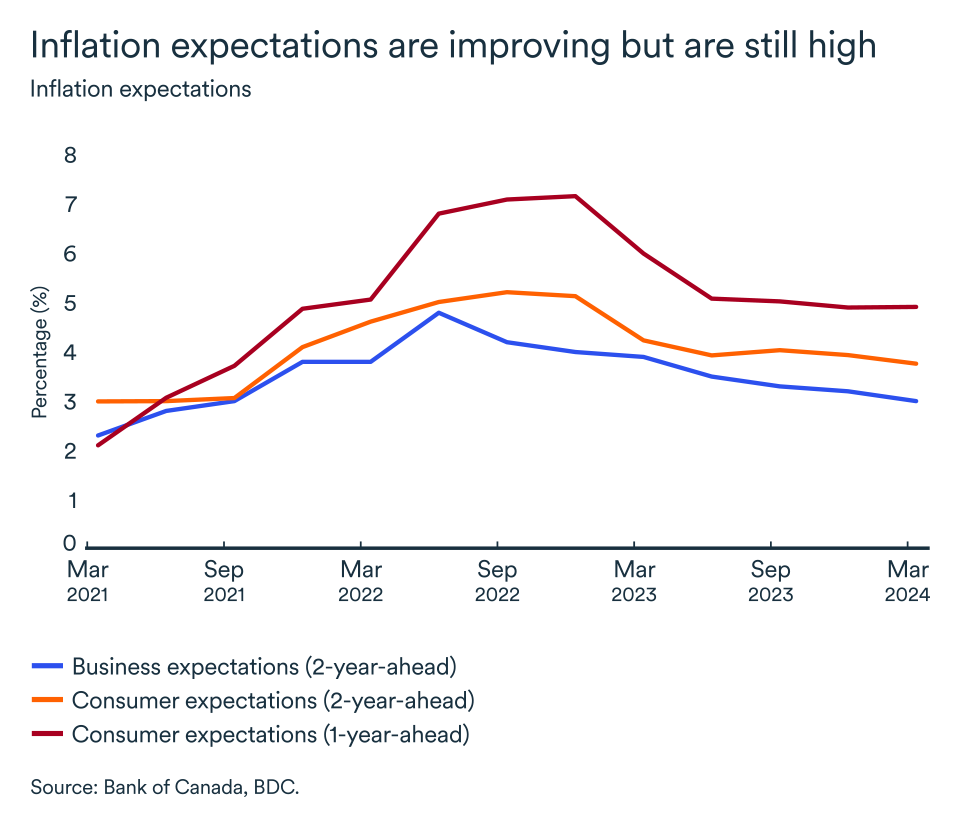

Although the economy showed momentum in the first two months of 2024, inflation has continued to moderate, slowing to a rate of 2.8% in February from 2.9% in January. While the inflation data is supportive of a first rate cut by the Bank of Canada, there remain a number of hurdles, including stubbornly high inflation expectations among consumers.

According to the latest Bank of Canada survey, many consumers still believe that inflation will be above the bank’s 1-3% target range in the coming year. The good news is that only 27% of businesses expect inflation to stay above 2% for more than three years (compared with 37% last quarter).

Moderating business expectations lead us to believe that inflation will continue to slow and move closer to target. (Companies tend to raise prices in anticipation of inflation, not in reaction to it.) On the other hand, high household inflation expectations will put pressure on wages. Indeed, companies expect wages to increase an average of 4.1% in the coming year.

The Bank of Canada maintained its key rate at the current level of 5.0% in its April announcement. We continue to expect a first rate cut at the next announcement in early June. However, the Bank of Canada may want to wait until the inflation outlook for Canadian households eases slightly before proceeding. This would push back the first rate cut to mid-July.

A more flexible labour market

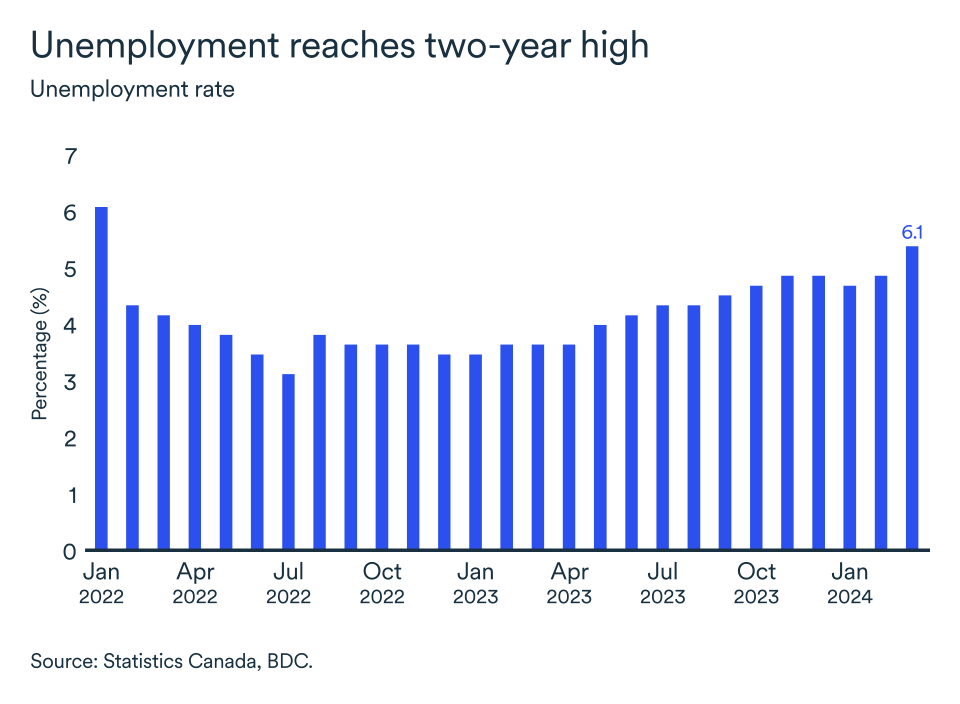

The Canadian job market remains strong but is stabilizing with a marginal loss of 2,200 in March. The unemployment rate, while rising, remains low by historical standards. At 6.1% in March, it was at its highest point in 26 months, and was well above the 5.0% low it reached in this cycle.

The number of job vacancies held steady in January compared with December, at just over 630,000. We have to go back to the winter of 2021 to see such a low number of available jobs in Canada. However, hiring intentions are slowly picking up as companies see the demand outlook improve slightly. According to the Bank of Canada, almost 43% of companies plan to increase their workforce in the coming year.

Average hourly earnings rose by 5.1% year-on-year in March. That was higher than in February and remains too strong to be compatible with the central bank’s 2% inflation target. Other wage measures, however, came in weaker. Growth in average weekly earnings (including overtime) for all employees, for example, was 3.9% in January compared with the same month in 2023.

What does it mean for your company?

- So far, the Bank of Canada's monetary policy is having the desired effect. Inflation is coming down. However, inflation expectations are still too high and so is wage growth. Businesses and households will have to be a little more patient before seeing a rate cut in Canada.

- The strength of the Canadian economy has continued to surprise in early 2024, but headwinds remain at home, including high interest rates and inflation above target. Make sure you have a solid plan for dealing with the challenges your business will face in the months ahead. Although interest rates will come down in the second half of the year, they will remain above the level households were accustomed to in recent years and will continue to dampen demand.

- Salaries will continue to rise faster than the historical average in the coming year. If your company is still struggling with labour issues, and rising costs are holding you back, it may be time to explore new avenues to increase productivity and win in the longer term.

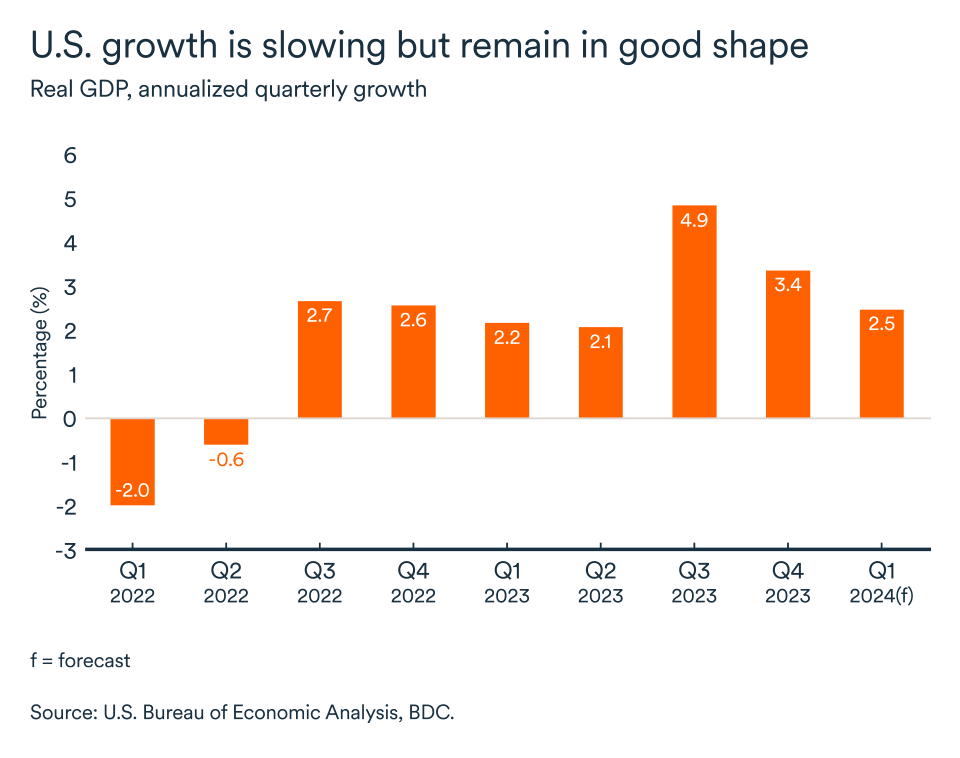

The U.S. economy maintaining momentum

The U.S. economy is still on a roll with preliminary data pointing to 2.8% growth in GDP for the first quarter of 2024. If confirmed, this performance will be all the more impressive as it follows an increase of 3.4% GDP in the fourth quarter of 2023.

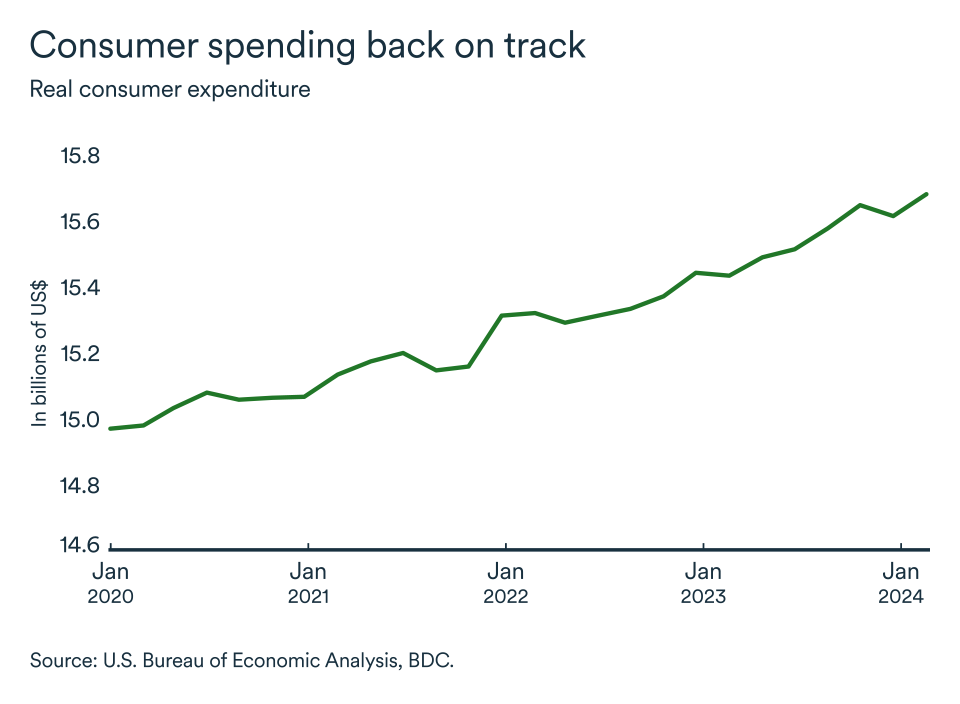

Consumer spending recovers

Excess savings accumulated during the pandemic and 30-year fixed mortgages have helped keep consumer spending high, despite repeated interest rate hikes over the past two years.

After spending less in January, Americans picked up the pace in February. However, there are signs that high interest rates are beginning to bite south of the border. Delinquencies on credit cards and car loans are higher than at any time in the past decade.

On the plus side, the wealth effect might be helping buoy consumer spending. Home prices are rising again and the stock market has surged in recent months, with the S&P 500 index jumping nearly 25% since the end of October.

When consumers see the value of their assets rising, they feel better off and tend to be less cautious in their spending, regardless of their income status. A major correction in asset prices could therefore pull consumption down quickly.

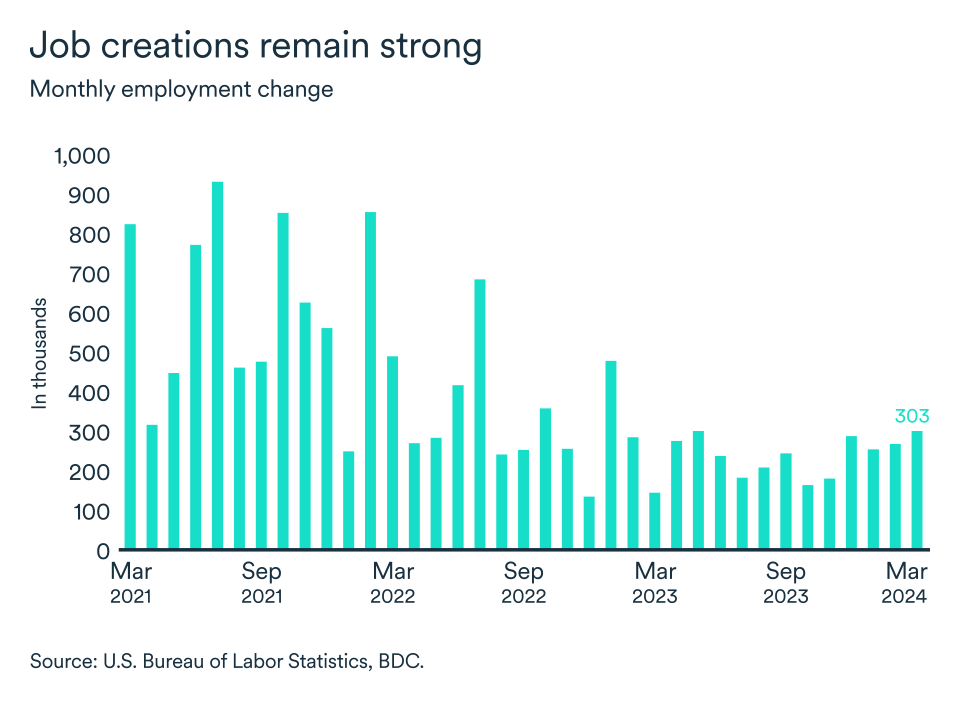

Job gains remain robust

It's been another strong start to the year for the U.S. labour market. Employment rose by 303,000 in March, following an increase of 270,000 in February. Even so, the unemployment rate remained at a two-year high of 3.8% last month. Most of the recent increase in the unemployment rate was concentrated among younger workers, aged 16 to 24.

The NFIB (National Federation of Independent Business) survey showed that hiring intentions are declining in the United States. As a result, wage growth is likely to continue its downward trend over the coming months, which bodes well for a first interest rate cut.

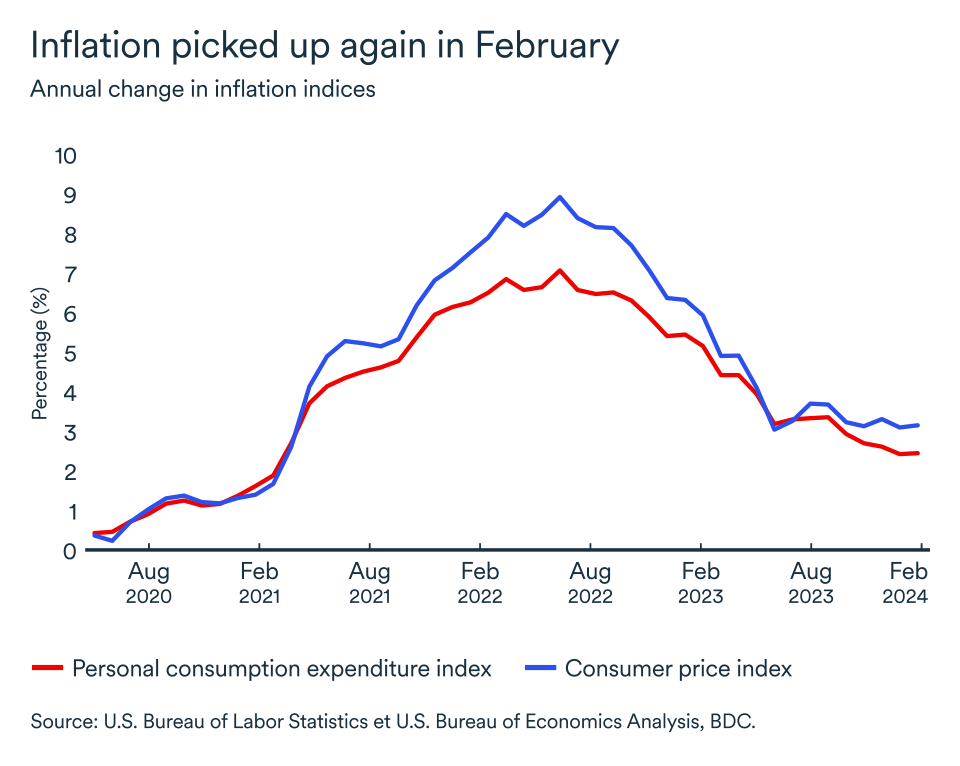

Awaiting better inflation indicators

Federal Reserve officials have not changed their interest rate forecast. They are still looking for further evidence that inflation is heading to a sustainable 2% before easing interest rates.

Fed Chairman Jerome Powell had explicitly indicated that a rate cut in March was unlikely. Recent data, including a strong rise in employment in January and a higher-than-expected Consumer Price Index report, have delayed the expected date for the first cut. Remarks by some board members at the March meeting further tempered expectations of a rapid easing of monetary policy.

Fed observers currently expect rate cuts totalling 75 basis points this year, but economic data are leaning toward fewer cuts. The Fed appears to be under less pressure to cut given that the economy remains strong and non-farm job gains have come in around 250,000 per month.

Subject to favourable inflation news, the first U.S. rate cut is now unlikely to take place in June, but rather in September. However, a preferred measure of core inflation known as the supercore rate—basic services excluding housing—remains stubbornly high, leading us to believe that the first cut is likely to come later in the summer.

The impact on your business

- Solid gains in the U.S. labour market should support U.S. consumption in the short term. As such, the loonie value is favorable for canadian exports.

- The outlook remains favorable for Canadian exports, but gains could prove short-lived with Americans using more credit to maintain spending, fueling what may be unsustainable economic growth.

- The differential between U.S. and Canadian rates is set to widen in the second half of the year, adding downward pressure to the exchange rate. A weaker Canadian dollar against the U.S. dollar tends to favour Canadian exports. On the other hand, a weaker dollar will hurt Canadian companies that depend on inputs traded on world markets or that source their supplies from the United States.

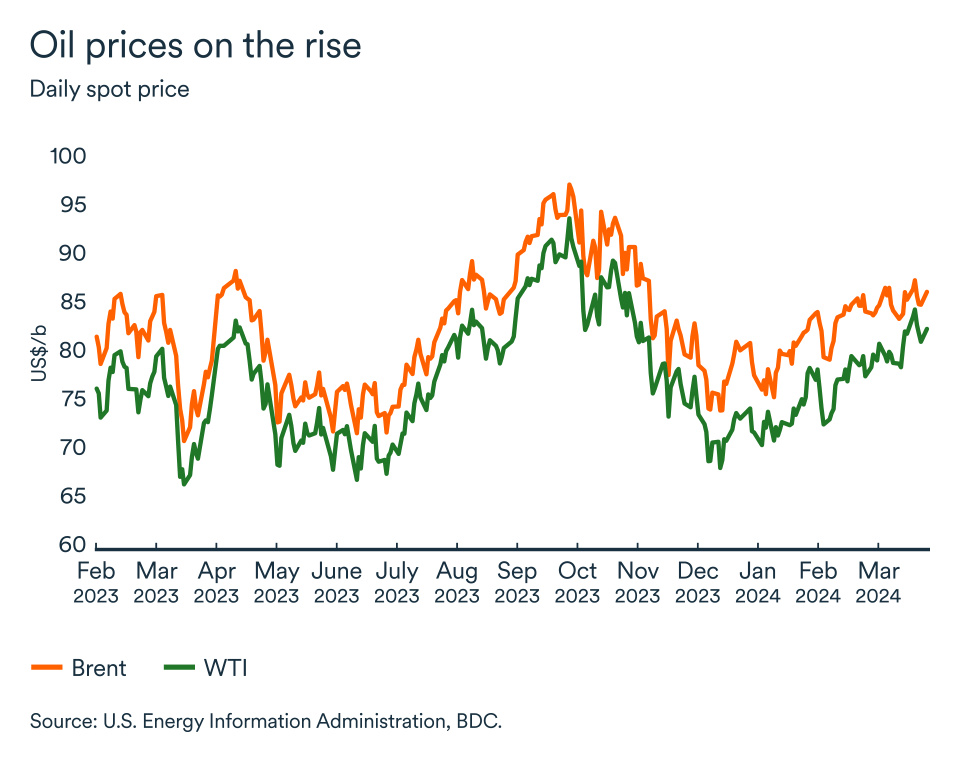

Oil prices are on the rise

Both global crude price benchmarks moved higher in March. Brent began March at US$83 a barrel and reached US$88, representing an increase of 2% month-over-month and a gain of almost 20% the same period last year.

The same was true in the United States, where West Texas Intermediate (WTI) futures closed March above US$82 a barrel, the highest level in nearly six months.

OPEC maintains restrictions

Despite efforts to cut oil production, OPEC+ (the Organization of the Petroleum Exporting Countries and its allies) fell short of its March reduction target by around 190,000 barrels per day (bpd).

Members of the group will have the opportunity to review the voluntary cuts on June 1. Until then, the production restrictions will amplify the disruptive effects on oil market from the geopolitical conflicts raging around the world.

The market expects OPEC+ to maintain its cuts during the first half of the year. Russian production cuts following Ukrainian drone attacks on its refineries could push the price of Brent to $100 a barrel this year. Ukrainian strikes on Russian refineries may have disrupted more than 15% of Russian capacity. Russia is the third largest oil producer in the world, behind the United States and Saudi Arabia, and the largest oil exporter.

Although crude inventories are still well stocked, the market for refined products is under considerable pressure. Refining capacity is limited by the situation in the Red Sea and Russia. Therefore, petroleum products, not crude oil, are the real short-term challenge.

Renewed demand

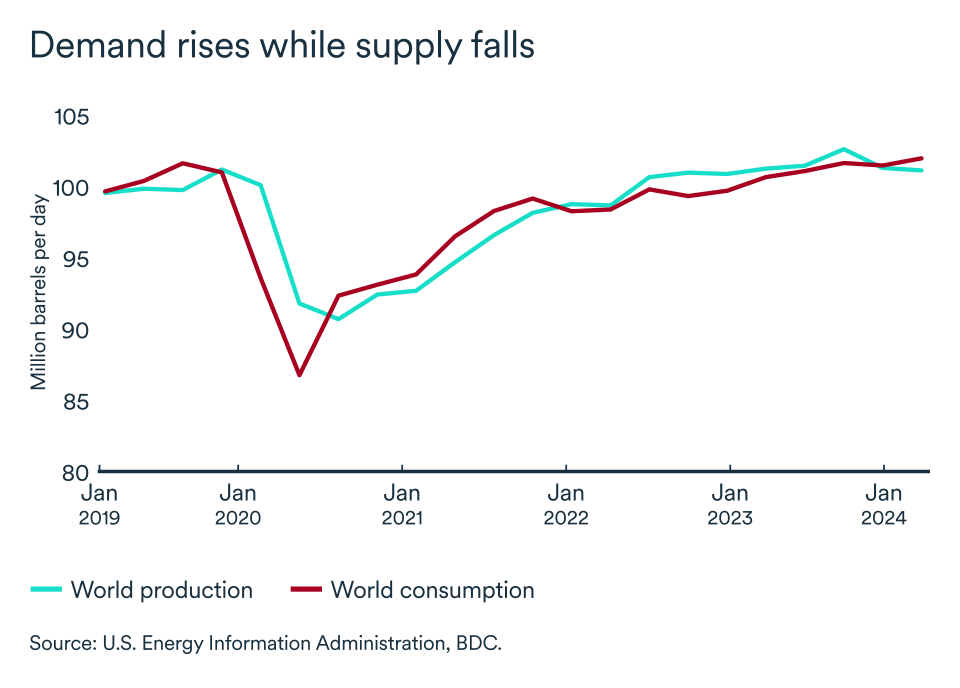

Fears of recession around the globe are fading fast and monetary policy tightening appears to be coming to an end. As a result, the outlook for global oil demand is being revised upwards.

The resilience of energy demand has probably been underestimated and is a significant factor in explaining the recent rise in prices. Prices had remained low for months due to expectations of a decline in demand, despite OPEC's production cuts of over 2 million bpd and forecasts of a slowdown in U.S. shale growth. Now the tide is turning.

Bottom line…

OPEC+ failed to meet its production reduction targets in March but rising geopolitical tensions and stronger global demand as recession fears fade have put upward pressure on oil prices. The refined products market is particularly tight and oil prices could continue to rise in the coming months.

The Bank of Canada is nearing the finish line

Incoming data has been encouraging with inflation standing just inside the Bank of Canada’s target range at 2.8% in February. Economic growth in the fourth quarter of 2023 and the first two months of 2024 was better than expected, but recent employment figures indicate growing slack in the labour market with unemployment reaching 6.1% in March. A faster than expected slowdown in employment in combination with easing inflation should prompt the Bank of Canada to begin cutting rates this summer. We reiterate that we expect the Bank of Canada to start lowering interest rates around June this year, and bringing them down to closer to 4.25% or 4% by year-end.

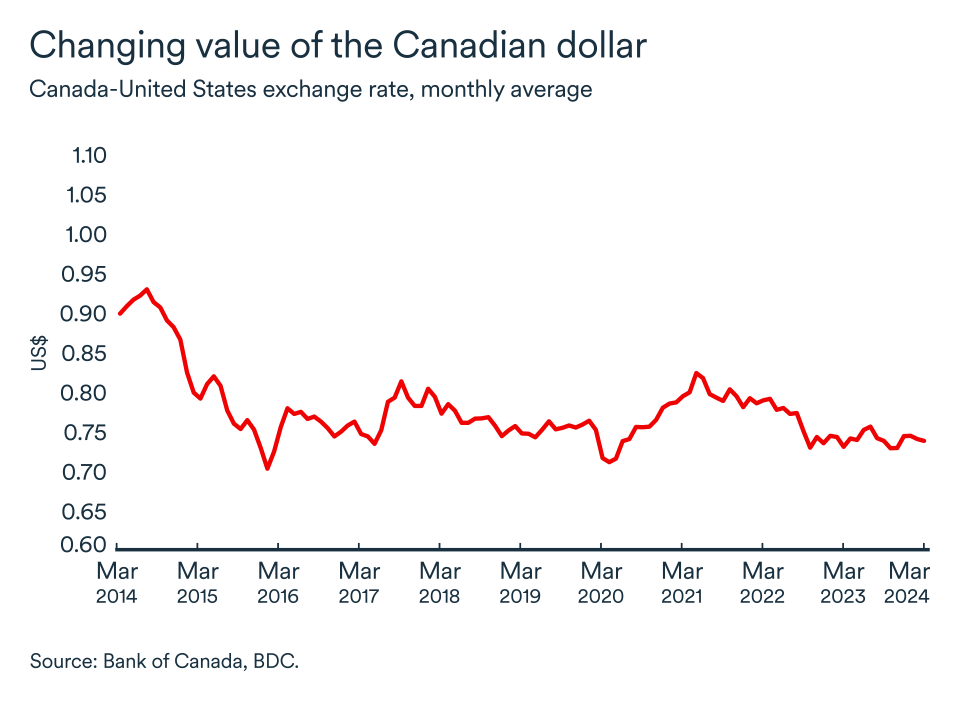

The loonie stabilizes in March

The Canadian dollar was stable in March, averaging US$0.74, the same level as the previous month. The long-term outlook continues to be muted for the Canadian dollar, with some downside risk.

The Bank of Canada is likely to cut rates earlier and probably faster than the US Federal Reserve. The yield differentials would drive the exchange rate to the lower bound of our expectations for this year. We expect the exchange rate to fluctuate between US$0.72 and US$0.75.

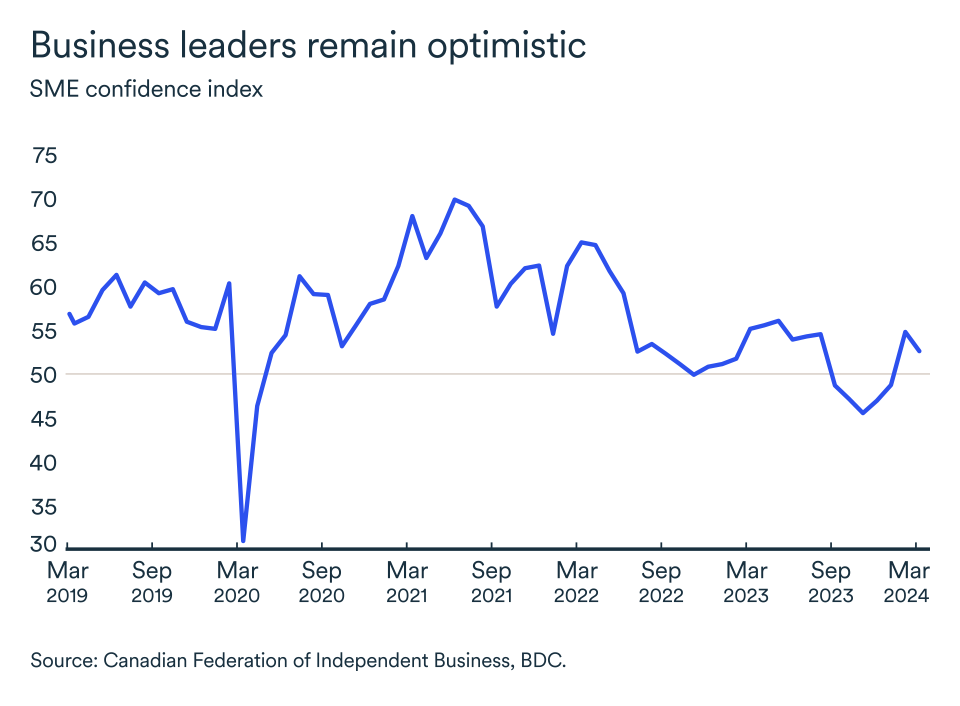

Business leaders remain optimistic in March

The CFIB's confidence index for the year ahead remained above the critical 50 mark for a second consecutive month. Optimism decreased slightly from 54.9 to 52.7 between February and March, with confidence levels mixed on the by-sector level. Some sectors such as the retail and financial services sectors showed less optimism, while others, such as transportation and professional services, gained some optimism. All provinces registered a gain in confidence; however, Quebec and New Brunswick remain below the 50 mark while Nova Scotia stands out as the most confident province with an index at 59.3.