Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreWhat impact will lower interest rates in Canada and the U.S. have on the dollar?

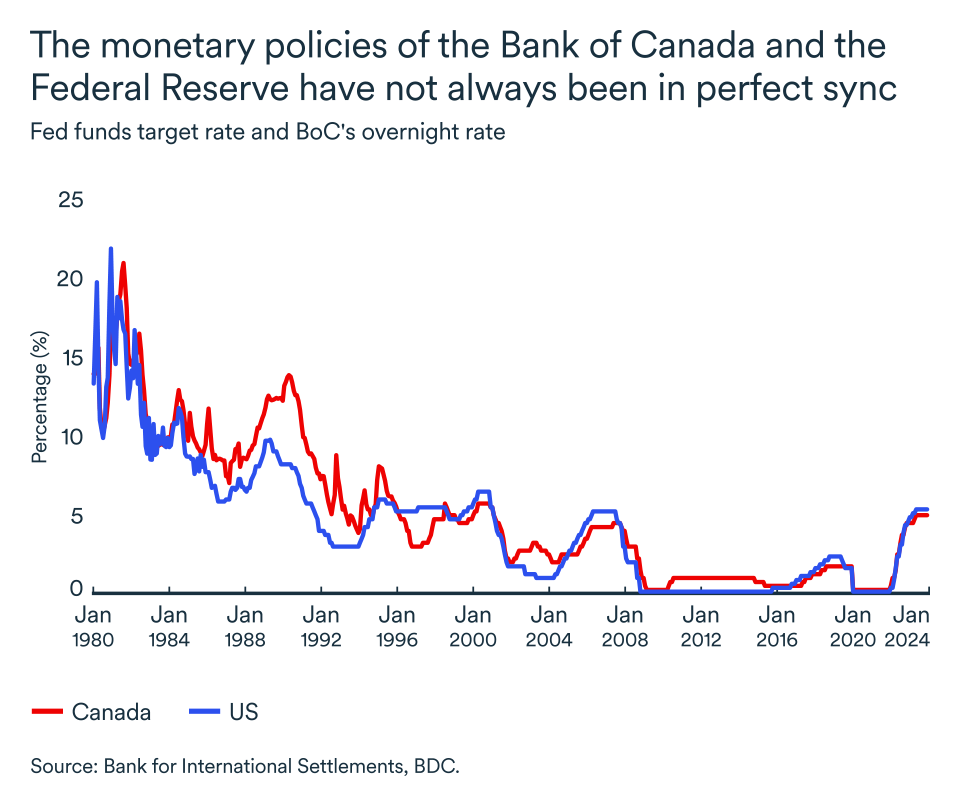

The last interest rate hikes on either side of the Canada-U.S. border took place in July 2023. Most central banks around the world have hinted at rate cuts for 2024, but the timing of the first reductions in Canada and the U.S. remains an open question.

The Bank of Canada was once again evasive on its plans following a March 6 meeting while U.S. Federal Reserve Chair Jerome Powell basically closed the door on a rate cut in the early spring.

The Bank of Canada doesn’t need to align itself with the Fed on interest rates, but it usually takes into account the effect of a change in U.S. policy on the Canadian dollar when assessing the best monetary policy to adopt on this side of the border.

When can we expect rate cuts?

In the contest to see which economy is most likely to need a rate cut first, Canada seems to have a slight lead based on macroeconomic data as real GDP growth geared down and even turned negative in Q3. Meanwhile, inflation in the U.S. appears to be more under control, which also favours rate cuts. (More details in the articles on the U.S. and Canadian economic outlooks.)

Ultimately, BDC expects the Bank of Canada to make its first cut in June. South of the border, a strong majority of economists are predicting the Fed will cut the federal funds rate for the first time in the second quarter.

Therefore, rate policy is likely to change more or less in tandem and the impact on the dollar should prove limited in the short term. In the longer term, the question is how fast rates will come down on either side of the border.

A rate differential will impact the loonie

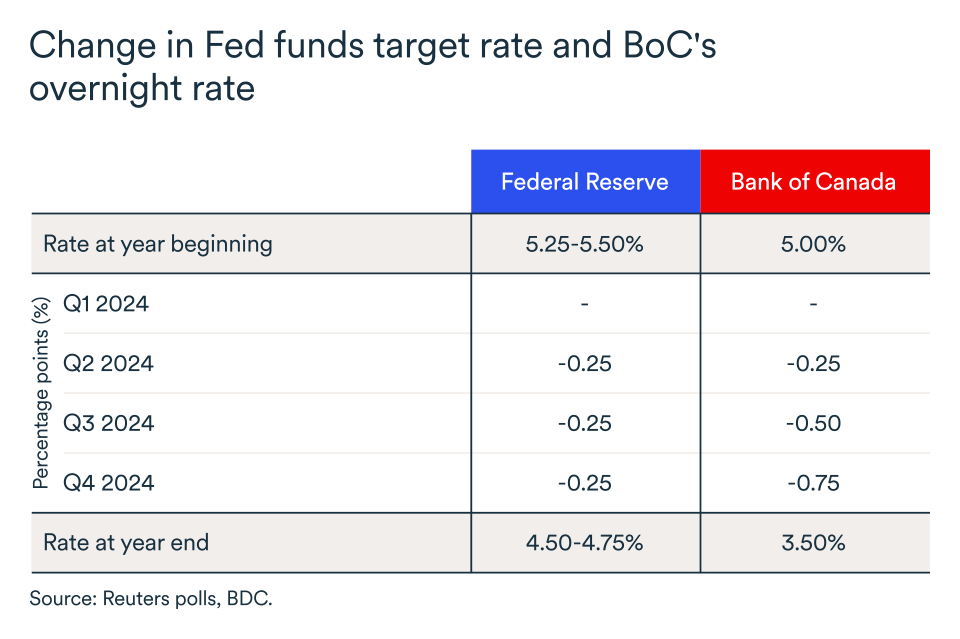

The current expectation is that the Fed will probably have to keep its key rate higher for longer this year. Fed officials are currently predicting three cuts totalling 75 basis points between now and the end of 2024. In Canada, BDC economists expect twice as many cuts, totalling 150 basis points.

Under this scenario, a substantial rate differential would develop between the two countries in the second half of the year. The Canadian rate would fall to 3.5% by year-end compared to a range of 4.5% to 4.75% in the U.S.

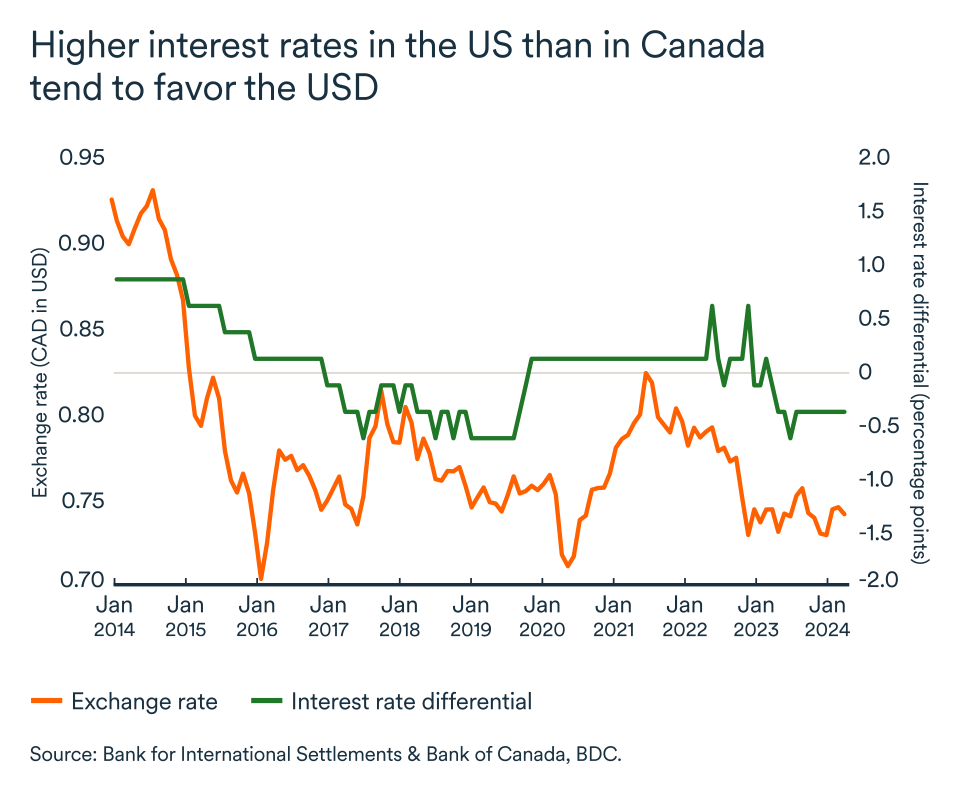

When interest rates are higher in the U.S. than in Canada, investors tend to favour U.S. markets where they can get higher expected returns. This increases demand for the U.S. dollar and boosts its value.

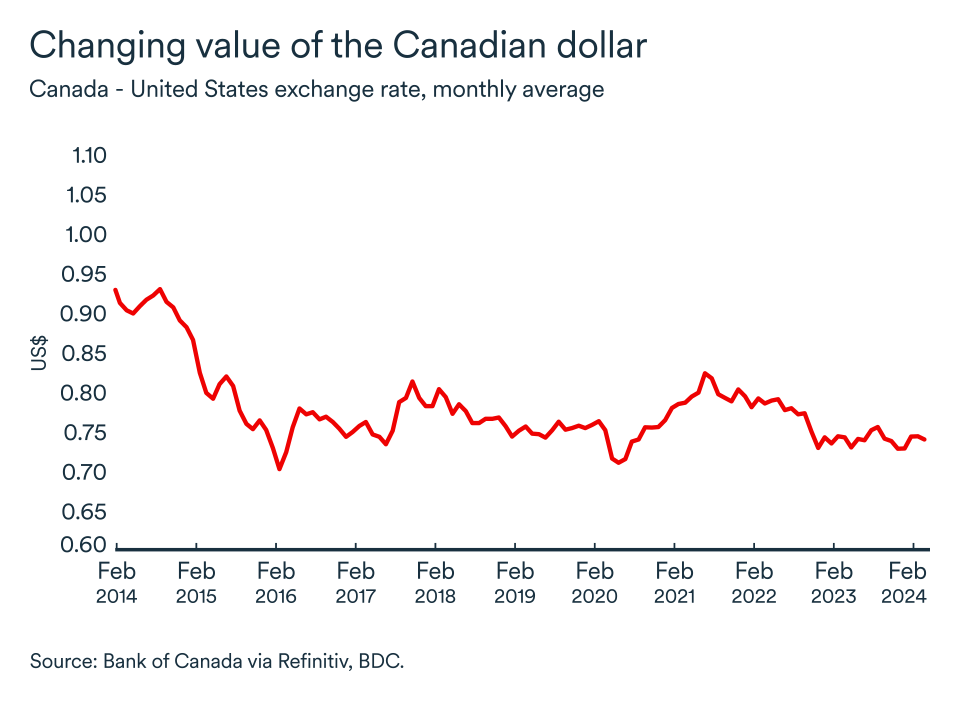

The markets are forward looking and, while it's unclear exactly when rate reductions will begin, traders are already placing bets on the impact they will have on various currencies. For this reason, the loonie has fallen by just over 2.5% against the U.S. greenback so far this year, from US$0.75 in January to US$0.73 in early March.

More weakness ahead for the loonie

Given the extraordinary rate-tightening cycle of the past two years, interest rate fluctuations are playing an even greater role in the global foreign exchange market. The Canadian dollar could therefore lose further value in the second half of the year.

By then, companies can expect the Canadian dollar to hover around recent levels of US$0.73-0.74.

The impact on your business

- A weak Canadian dollar is good for exports. Whatever your company's sector of activity, this is a great opportunity to attract new American customers.

- The exchange rate should also boost Canada's attractiveness to American tourists. The loonie may descent further in the second half, just in time for the summer season. Prepare your business to make the most of the foreign visitors that will come.

- While a weaker exchange rate has advantages for many companies and can create business opportunities, the dollar’s weakness also means higher import prices, particularly for raw materials, including some foodstuffs. As a result, the price of your inputs could rise further in the second half of the year. Find the right balance between cutting costs and investing in growth to protect your profits.

Canadian economy remains under strain

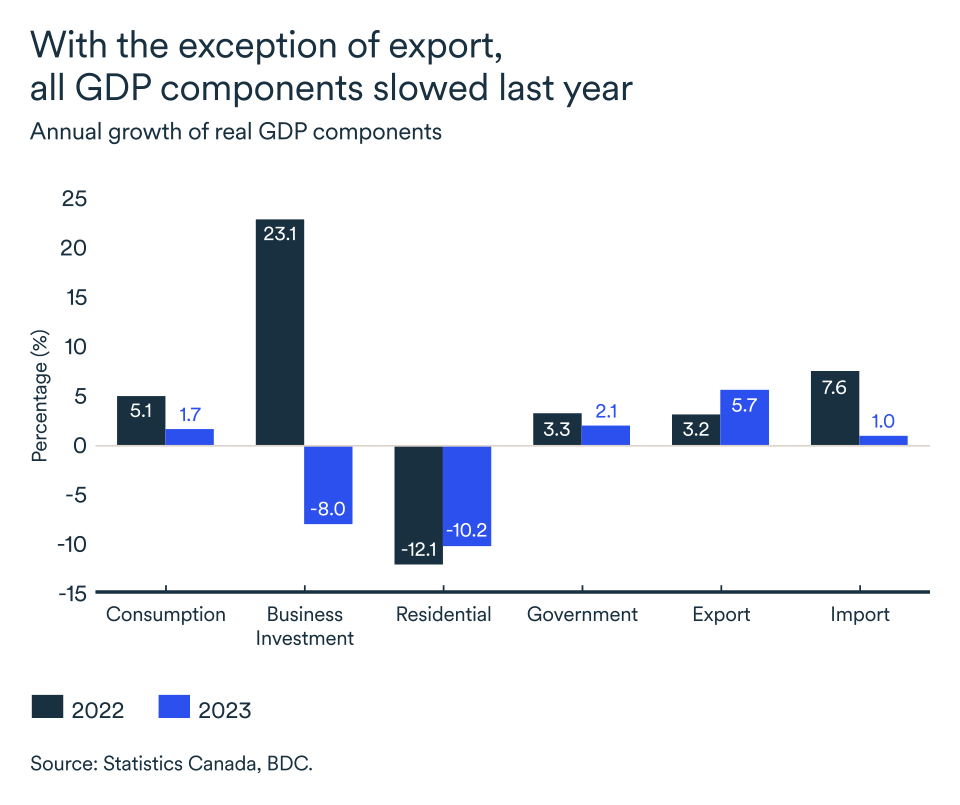

After a downturn in activity in the third quarter of 2023, the Canadian economy regained strength at the end of the year, posting annualized growth of 1.0% in the fourth quarter. For all of 2023, Canada recorded growth of 1.1%, the worst performance since the recession of 2020 and well below the economy’s 2.0% potential.

Economic activity was hurt last year by a downturn in business and residential investment. Those forces were offset by gains in consumer and government spending, although growth here was also slower than in 2022.

Statistics Canada anticipated a 0.4% increase in real GDP in January, pointing to continued slow but positive growth in the first quarter. Growth at the end of 2023 was driven by international trade. Exports rose by 5.6% in the fourth quarter while imports were down 1.7%.

Households shift their savings

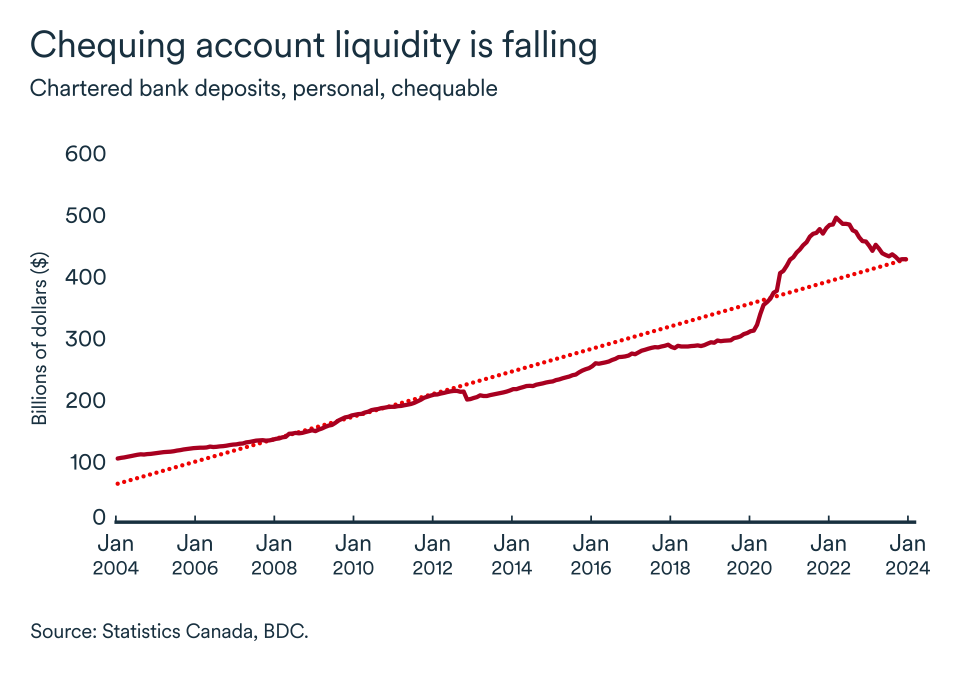

Consumer spending improved even as the rate of household savings increased, supported by rising disposable incomes (+5.3%).

More liquid (i.e. easily accessible and transferable) personal bank deposits are still high but have been falling since the Bank of Canada began raising interest rates in March 2022. Households appear to be spending the savings they accumulated in liquid accounts during the pandemic as they weather a weaker economy, high inflation and rising interest payments.

The decline is even more significant when we consider the record population growth. We would have expected it to push up the overall level of deposits in the country.

Therefore, accumulated savings are likely to be concentrated at the upper end of the income distribution in longer-term account.

In the end, the financial cushion that is being built up is not as readily available as it was at the end of pandemic lockdowns. This money is unlikely to be spent in the short term—good news for the Bank of Canada and inflation, but a slightly less attractive sign for businesses, who will have to be patient before consumer enthusiasm returns.

Wage growth remains strong

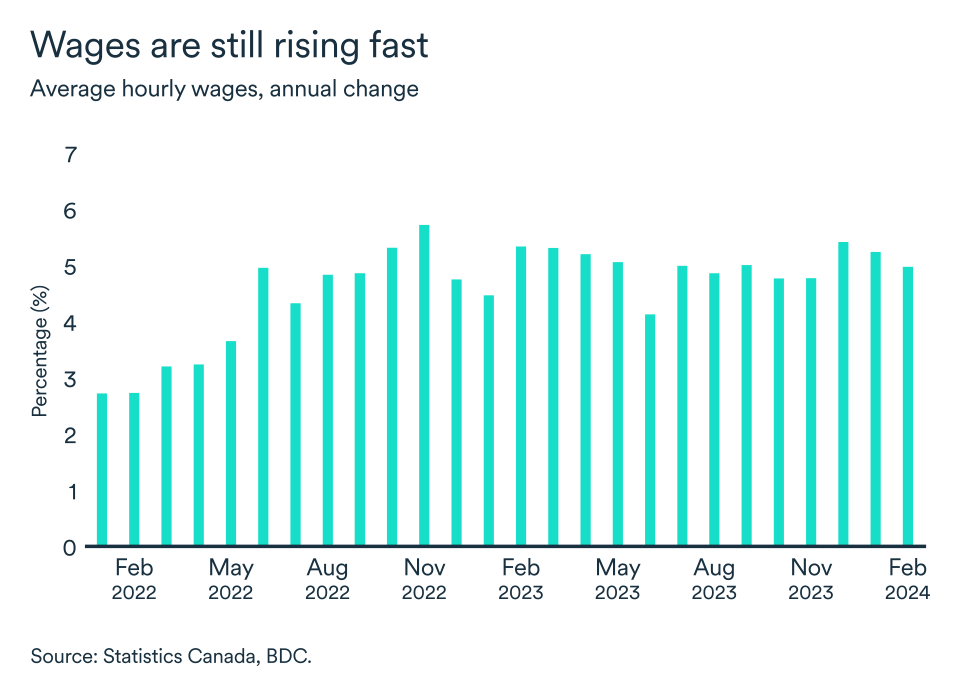

The Canadian job market remains in good shape. The unemployment rate ticked up at 5.8% in February after employment rose by 41,000 jobs compared to January.

Nationally, average hourly earnings rose again in February by 5.0% year-on-year. It will therefore come as no surprise if inflation measures in the labour-intensive services sector were to rise above the Bank of Canada's target range in the next data release.

However, with more potential workers on the labour market, companies should still expect wage growth to slow this year. The job vacancy rate is back close to its pre-pandemic level, and the proportion of companies suffering from labour shortages is below the long-term average.

The Bank of Canada will continue to be patient

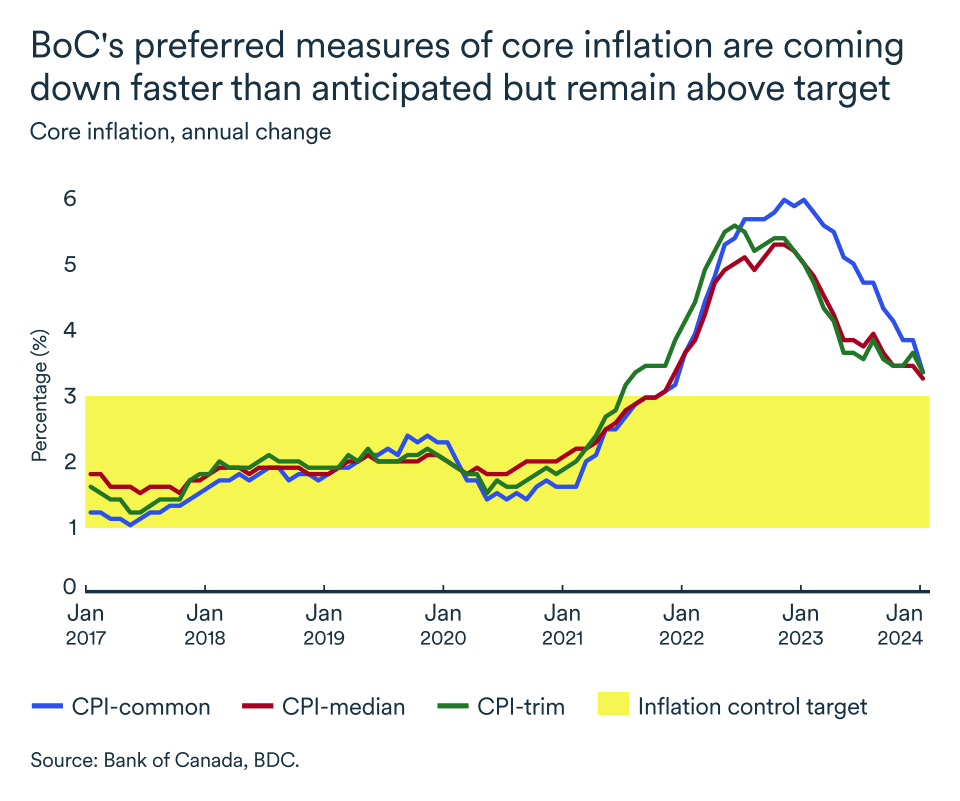

The central bank kept its key rate at 5.0% in its March 6 announcement. We expect the bank to continue to hold the line on rates at its next meeting in April even though the inflation outlook is improving.

A significant drop in food prices was the best news to emerge from the country's latest inflation report. Consumers are confronted by higher food prices on a weekly basis and it’s not discretionary spending. Therefore, a slowdown in food inflation should be reflected in lower household inflation expectations and improved consumer confidence.

January's encouraging inflation data followed two months of acceleration. It’s therefore too early for the Bank of Canada to be fully confident that underlying inflationary pressures have eased.

It's a safe bet the bank's Board of Governors will want to see at least three months of consistently falling data, to be sure that core inflation is heading towards 2.0%. We still expect a first rate cut to come as early as June.

The impact on your business

- Canada avoided a recession in 2023 and Canadian consumers should continue to regain confidence in the economy and return to a higher pace of spending in the second half of the year. Make sure you have an action plan to get your business through a slow spring and be ready to capitalize on rate cuts in the second half of the year.

- The recent easing of inflation, and the continuing good situation on the labour market should help to support basic household spending in the shorter term.

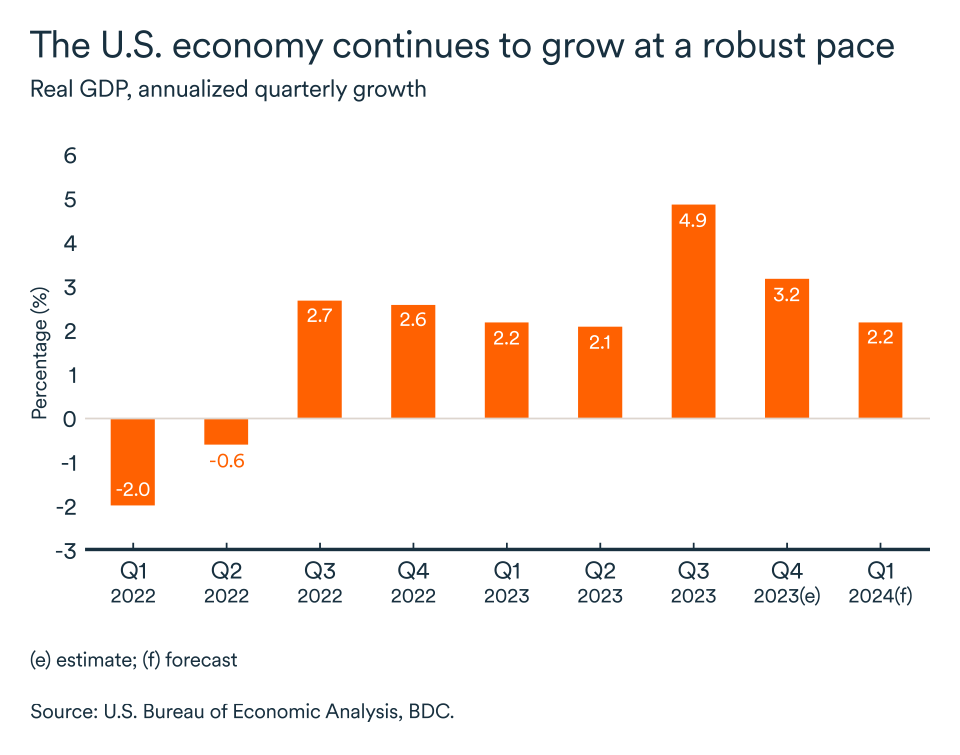

The U.S. economy’s vigorous growth continues

U.S. gross domestic product grew by 3.2% in the fourth quarter of 2023, bringing growth for the full year to 2.5%. The economy continued its momentum in the first quarter of this year with growth approaching 2.0%, according to initial estimates.

The chances of a Fed victory against inflation without causing a severe recession are still promising. Although there are signs of a slowdown in economic growth, the continuing strength of the labour market testifies to the enduring resilience of the world's leading economy in the face of interest rates that have not been this high since the 1980s.

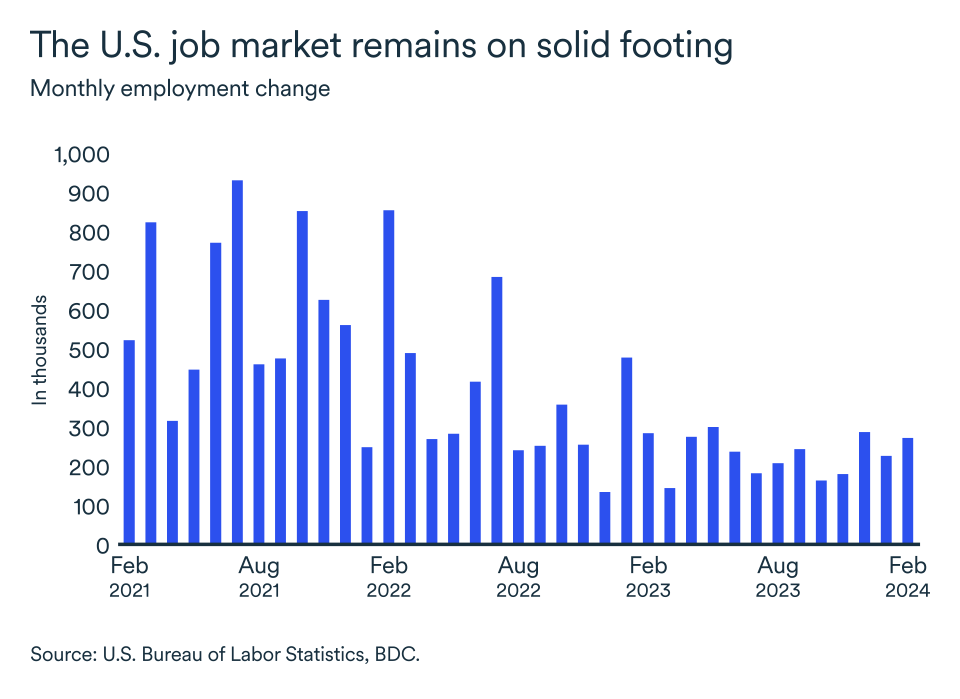

Sustained employment gains

Strength in the job market has raised optimism for another year of solid economic growth in 2024. Employment rose by 275,000 jobs in February, following January's increase of 229,000 and upward revision of December's figures.

By way of comparison, the average monthly addition of jobs last year was about 250,000, so the labour market is off to a very robust start to the year. The unemployment rate stood at 3.9% in February, a two-year high although, overall similar to its level of recent months.

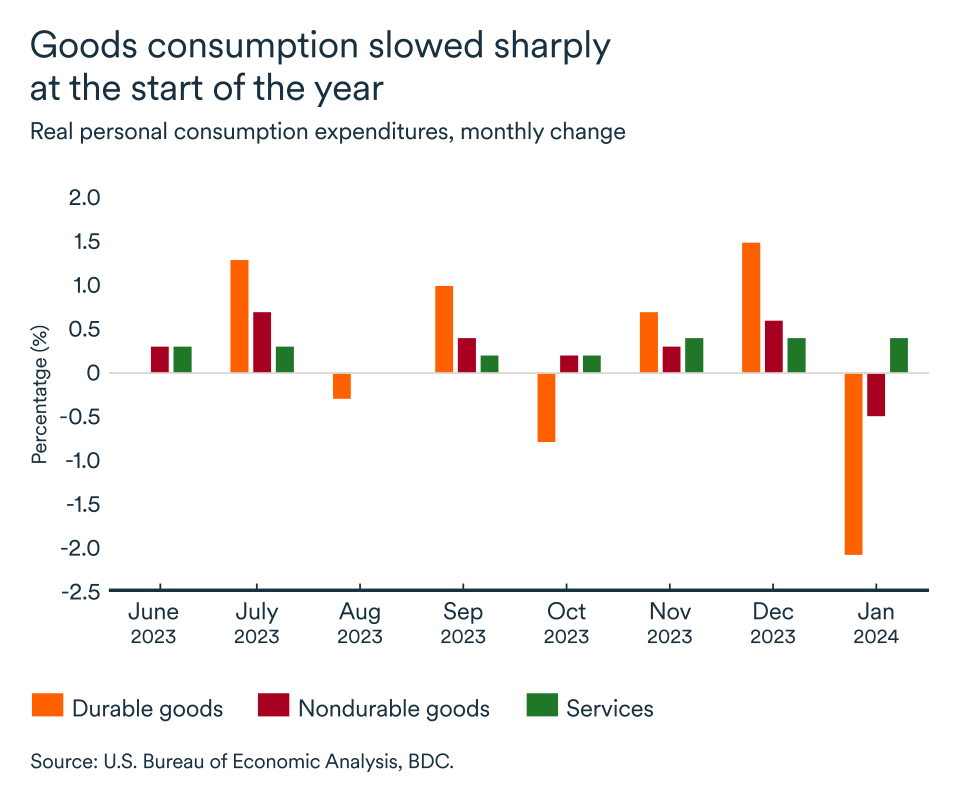

First signs of a slowdown in consumption

After registering a decline in personal consumption expenditures, the U.S. Census Bureau anticipated a drop in nominal retail sales in January.

This suggests that consumption growth is (finally) running out of steam. Over the course of 2023, consumption held steady despite a series of interest rate hikes by the Federal Reserve's to counter inflation. The rising cost of credit could finally be taking a toll on purchases as American consumers become more sensitive to higher prices.

However, according to the Federal Reserve Bank of New York, many Americans are prepared to take on more debt to maintain their lifestyle, with total credit card debt reaching $1.13 trillion.

The Federal Reserve remains cautious

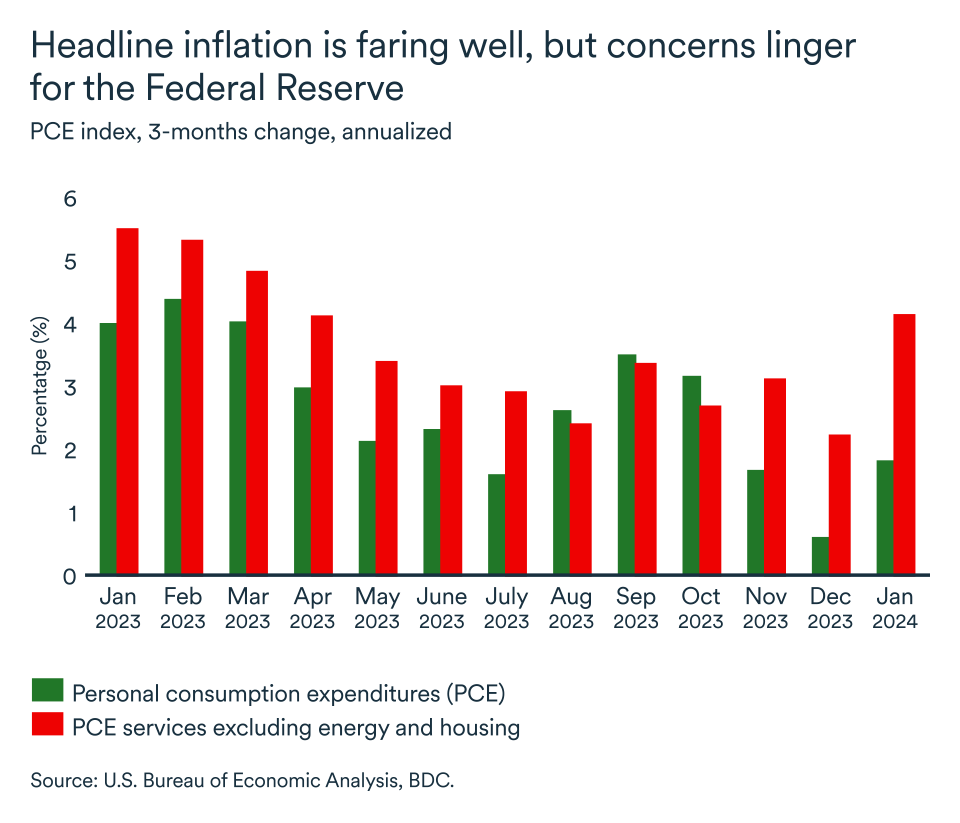

Inflation continues to slow in the United States with broad inflation measures moving closer to the 2% target each month. The annual personal expenditure deflator slowed to 2.1% in January from 3.2% in December. Inflation as measured by the consumer price index (CPI) also declined, hitting 3.1%.

However, these two measures could prove to be misleading when it comes to predicting the Federal Reserve's next move. That’s because several indicators of core inflation could be more worrisome for U.S. central bankers.

Indeed, one of the Federal Reserve's favourite measures accelerated sharply at the start of the year. The annualized quarterly change in personal spending on services excluding energy and housing rose from 2.2% in December to 4.1% in January.

The Fed may find it prudent to remain patient on rate cuts this spring if the economy continues to grow and underlying measures of inflation rise.

The impact on your business

- Taking advantage of vigorous growth south of the border, Canadian companies should continue to benefit from an expanding market and the advantage of a weaker currency.

- The strength of the labour market is likely to continue to support U.S. consumer spending in the short term. On the other hand, as Americans increasingly turn to credit to maintain their spending pace, rising household debt could hurt the U.S. economy later in the year.

- U.S. inflation appears to be under control, but a close reading of the latest price growth reports suggests that the Federal Reserve will likely be cautious in lowering interest rates. A rate differential between Canada and the U.S. has repercussions for our economy—find out what impact this differential could have on the economy and your business.

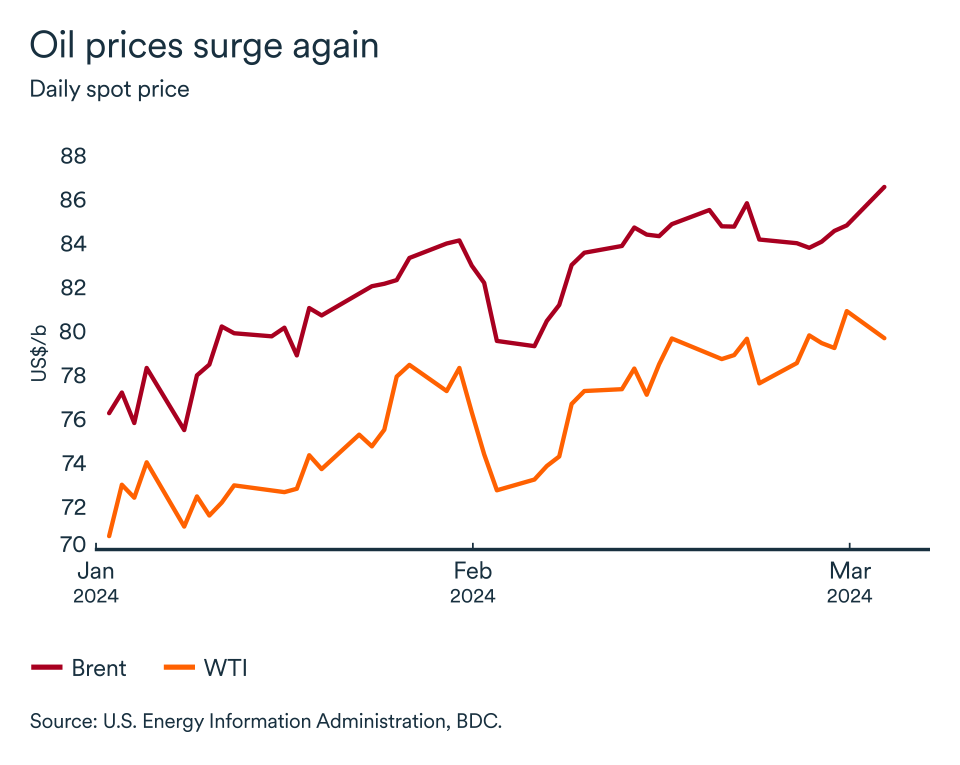

Crude oil prices rise in response to Middle East risk

The main global benchmarks for crude oil prices both continued to rise during February. Brent began March at US$83 a barrel, while U.S. West Texas Intermediate (WTI) futures settled near the US$80 a barrel mark.

Middle East tensions increasingly reflected in prices

The price of Brent has rallied since the start of the year as attacks on ships in the Red Sea have intensified. The premium associated with geopolitical risk and the prevailing uncertainty in the Middle East, combined with the ongoing risk of supply disruptions in that part of the world, are pushing crude oil prices ever closer to the US$90 a barrel mark. Nearly 12% of the world's oil trade is transacted there.

For the time being, the risk remains contained. Crude prices are rising but gradually. They should hold in the middle of the $80-$90/barrel range over the next few months. Downward pressure on prices could appear at the end of the second quarter as global oil inventories trend upwards.

OPEC+ to limit global supply in the second quarter

The Organization of the Petroleum Exporting Countries and its allies (OPEC+) has confirmed that voluntary cuts of 2.2 million barrels per day (Mb/d) will continue into the second quarter of 2024. The goal is to reinforce market stability against a backdrop of fluctuating global demand. This extension is further evidence of the cartel's desire to maintain a floor price above $80 a barrel in the second quarter.

The market had already largely anticipated the extension of production restrictions, limiting the impact of this latest decision on world prices.

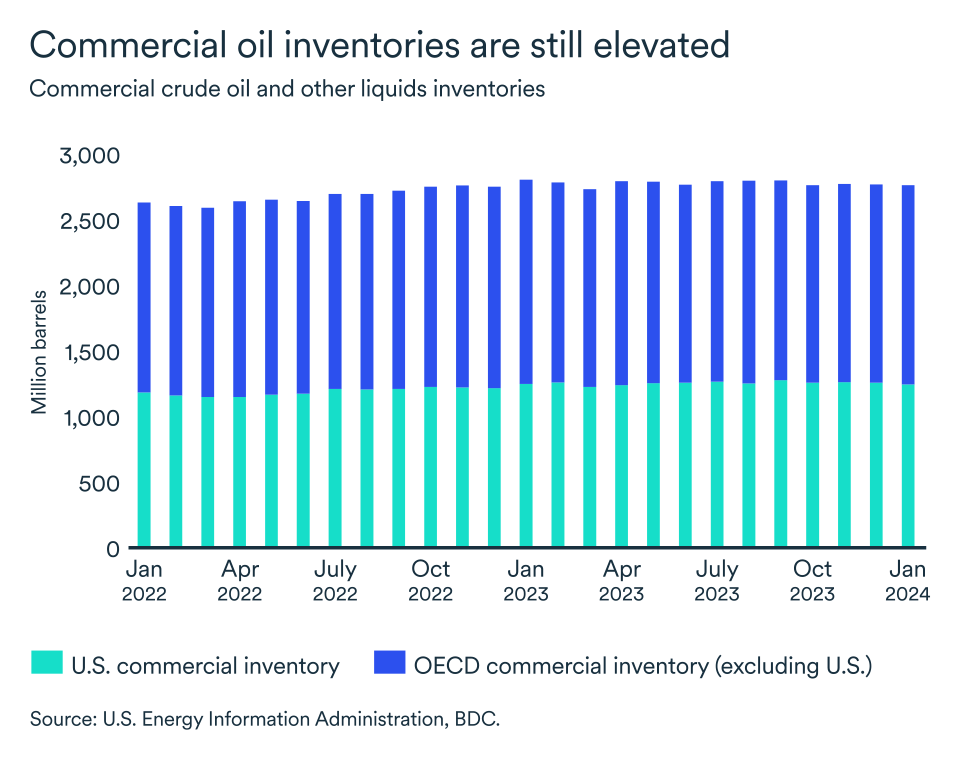

Inventories are rising elsewhere in the world

According to the U.S. Energy Information Administration, U.S. production reached a new record high in December, before falling back in January. Monthly production fell by more than 5%, from 13.3 Mb/d to 12.6 Mb/d in January.

January's slowdown was probably temporary. After a cold snap in the United States in the first month of the year, the weather turned milder in February, and production is said to have recovered to a level close to the December record. Total oil consumption in the U.S. is expected to rise by 200,000 b/d to 20.4 Mb/d in 2024.

In a nutshell...

Despite the extension of production restrictions by OPEC+, crude inventories continue to build. The rise in prices since the beginning of 2024 reflects geopolitical risk in the Middle East. However, higher prices are constricting demand. Ultimately, crude oil prices could rise to US$85-90 a barrel before settling closer to US$80 in the coming months.

The Bank of Canada will continue to wait and see

The Bank of Canada will continue to monitor incoming inflation data and economic developments. Latest inflation data was encouraging showing that underlying pressures eased in January. However, the better-than-expected economic growth in the fourth quarter and the downward revision of the third quarter contraction reinforces our view on the Bank’s next move. We still believe that the bank will be patient and give more time for policy to work its full effect through the economy. We reiterate that the Bank of Canada should start lowering interest rates around June this year, bringing them down to close to 3.5% by year-end.

The loonie weakens in February

The Canadian dollar weakened in February, averaging US$0.74. The long-term outlook continues to be muted for the Canadian dollar. The Canadian economy is set to slow down in 2024, oil prices remain in range despite geopolitical tensions and OPEC cuts. The U.S. economy is heading toward a soft landing with growth expected to reach about 2% in 2024, outperforming Canada, and major trading partners. We expect the exchange rate to remain in range this year and fluctuate between US$0.72 and US$0.75.

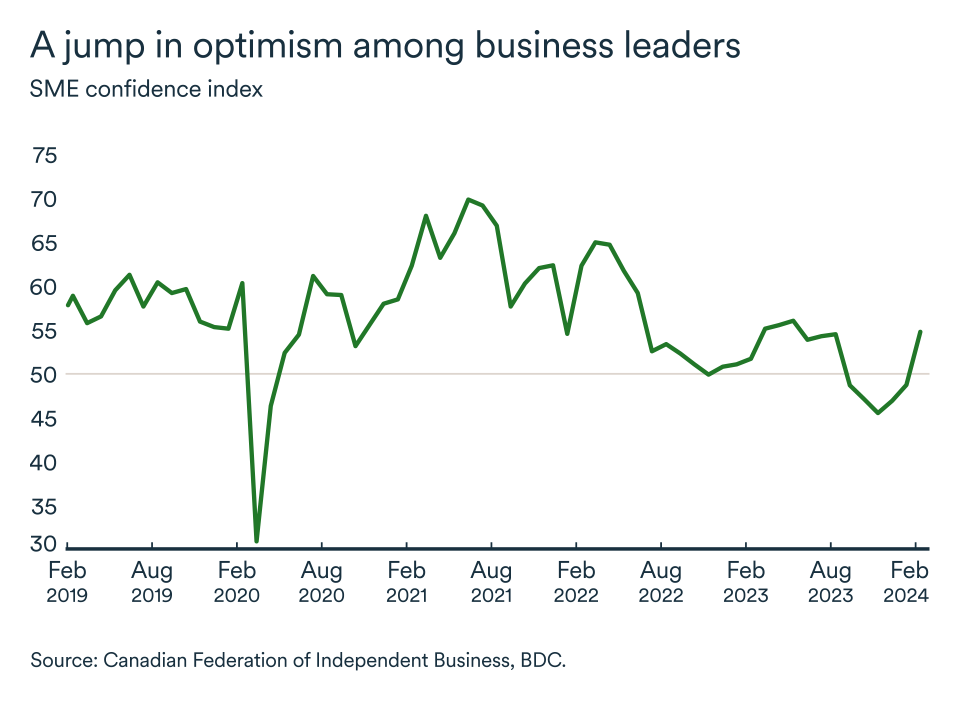

Business leaders are more optimistic

The CFIB's confidence index for the year ahead crossed the critical 50 mark for the first time in six months. Optimism increased from 49 to 54.9 between January and February. An improvement in confidence was seen in all sectors except the finance, insurance, and real estate sector. On average, shortage of skilled labour and insufficient demand remain the most important factors limiting sales according to the survey. All provinces registered a gain in confidence; however, Quebec and New Brunswick remain below the 50 mark.