Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreLet's talk recession!

More and more Canadians are worried the economy will soon slip into recession. Some economists have already sounded the alarm. Our current analysis indicates the Canadian economy will experience a marked slowdown this year, but avoid a recession. Yes, there’s a difference between a slowdown and a recession. So, what does recession actually mean? More importantly, how can you ensure the survival and continued growth of your business when the economy simply won't cooperate?

Recessions 101

Recessions are a normal and expected part of the business cycle. A recession, in its simplest and most widespread definition, is characterized by two consecutive quarters of falling real GDP.

However, many economists, including our team at BDC, prefer a less mechanical definition. We believe widespread and significant declines in GDP and employment are more useful indicators in deciding whether a recession has occurred.

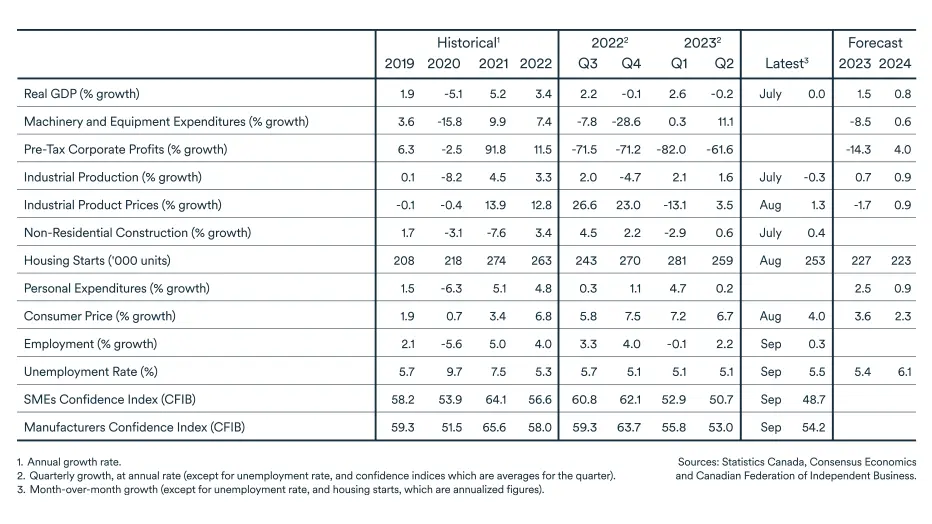

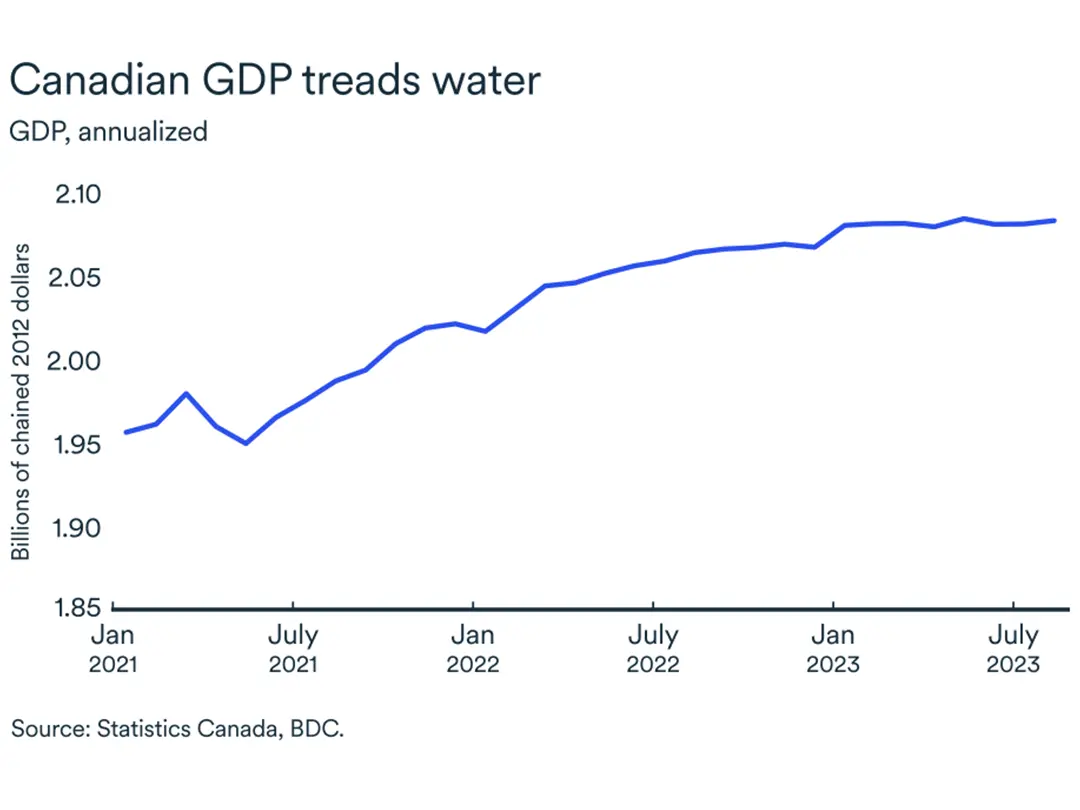

So, where are we now? Real GDP in Canada fell in the second quarter by 0.2%, and we expect weak growth in the third quarter, if not outright stagnation.

Therefore, it’s possible we will see two consecutive quarters of negative growth, the technical definition of a recession. Again, while this is a necessary condition of a recession, we don’t believe it’s sufficient to declare one has occurred. As proof, recall that U.S. real GDP contracted in the first two quarters of 2022, but there was little talk back then of recession.

An economic slowdown turns into a recession when linked parts of the economy contract one after the other like falling dominos. Hence, a drop in consumer spending, retail sales, industrial production and corporate profits leads to layoffs and higher unemployment, a loss of income and finally a reduction in real GDP.

In evaluating whether we are in a recession, we must also consider how widespread the negative growth becomes. If the slowdown does not produce a sequence of reductions across the various links in the economy, we can’t say we’re in a recession.

Where are we headed?

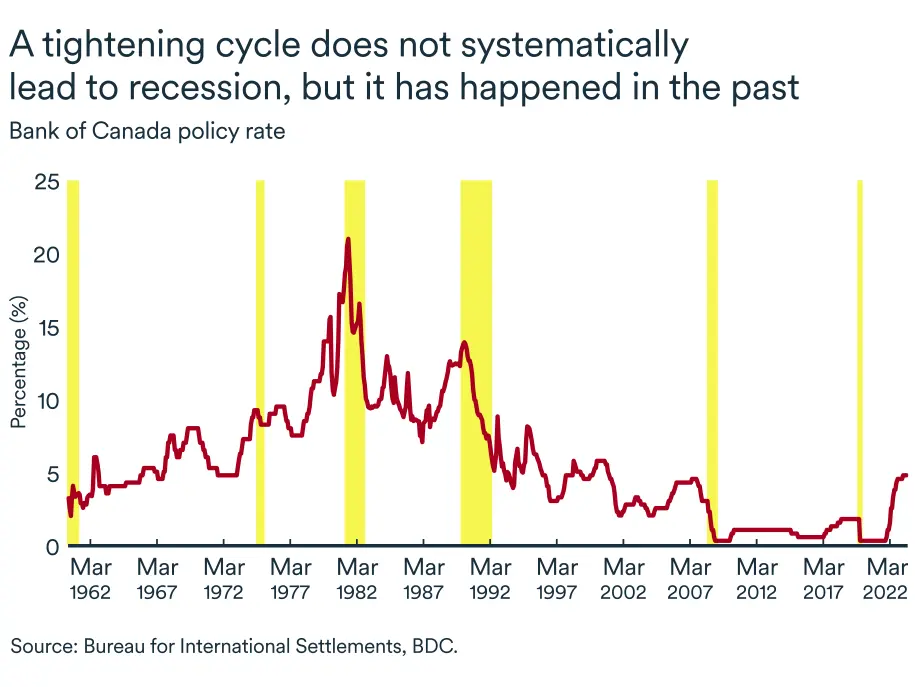

Canada has experienced twelve recessions since 1929, including five since 1970. The most recent one, caused by COVID-19, is probably the most unusual, since it was triggered by an unforeseen and unpredictable event. It was also the shortest on record. History shows that recessions are triggered by a shock to the economy—such as an oil shock or financial imbalances (those famous bursting bubbles). The economy is not currently facing these same trends.

Recessions are often blamed on rising interest rates (the third potential trigger of recession). And rightly so, since the objective of central banks in raising rates is to slow down the economy to reduce demand and cool inflation.

This is precisely what’s happening in Canada today. A series of interest rate hikes by the Bank of Canada is slowing demand. A tightening cycle doesn’t always lead to recession, but it has in the past. What's more, we are currently in the midst of the most rapid tightening of credit conditions in decades.

Our current analysis indicates that the Canadian economy should experience a marked slowdown this year, but avoid a recession.

How can your business continue to prosper in a slowdown?

Whether we're talking about a recession or a slowdown, the important thing for entrepreneurs is the steps they can take now to ride out the jolts in the economy over the coming months. Here are some strategies to keep your company on track.

Before

- Your finances must be at the center of your concerns: You can't rely on guesswork or intuition. You need hard data and a process that tells you how your results fluctuate over time if you're to prepare adequately for a downturn. Discover the key steps to healthy finances and cash flow here.

- Focus on efficiency: When demand slows and it becomes harder to make gains on sales volume, it's important to maximize returns while limiting unnecessary expenses. This includes reviewing and optimizing your costs.

During

- Reframe the situation: Seeing a slowing economy only as a threat can make you freeze. By contrast, seeing it as an opportunity can lead you to seek ideas, innovations and new markets that could fuel your company’s growth well into the future. What worked last year may not this year, so your company needs to be open to adapt and change with current conditions.

- Look for opportunities: Turbulent times can bring opportunities, but much depends on your sector and company characteristics. Take stock of your company's strengths and discover the opportunities available to your business today to ensure its long-term survival.

- Stay agile but be prepared for setbacks: Proceed in small steps and adopt practices and methods that enable you to change course quickly.

- Focus on the short term first: To counterbalance the negative effects that typically accompany an economic slowdown, keep a keen eye on your finances.

- Plan for the long term: Companies that are most resilient to economic cycles are those with a long-term strategy focused on productivity gains (doing more with less) and diversification. It's never too late to prepare for the next recession since they are an integral part of business cycles.

Read more about how to make the most of economic downturns here.

Canada's economy enters dangerous waters

As we enter the final quarter of the year, challenges continue to mount for the Canadian economy. GDP gains will prove increasingly difficult in the months ahead as the impact of past interest rate hikes weighs on households and businesses.

The economy was stuck in neutral over the summer months with a GDP decline of -0.2% in June, followed by flat growth in July (+0.0), when more than half of economic sectors posted declines, according to Statistics Canada.

Gains in the service sector in July were offset by losses in goods-producing industries. The manufacturing sector posted its biggest monthly decline (-1.5%) since April 2021, amid a British Columbia ports strike and inventory drawdowns.

Nevertheless, the economy may still avoid slipping into negative growth for the third quarter as a whole. For August, Statistics Canada is forecasting positive growth of 0.1%, anticipating a muted rebound following closures caused by forest fires in western Canada.

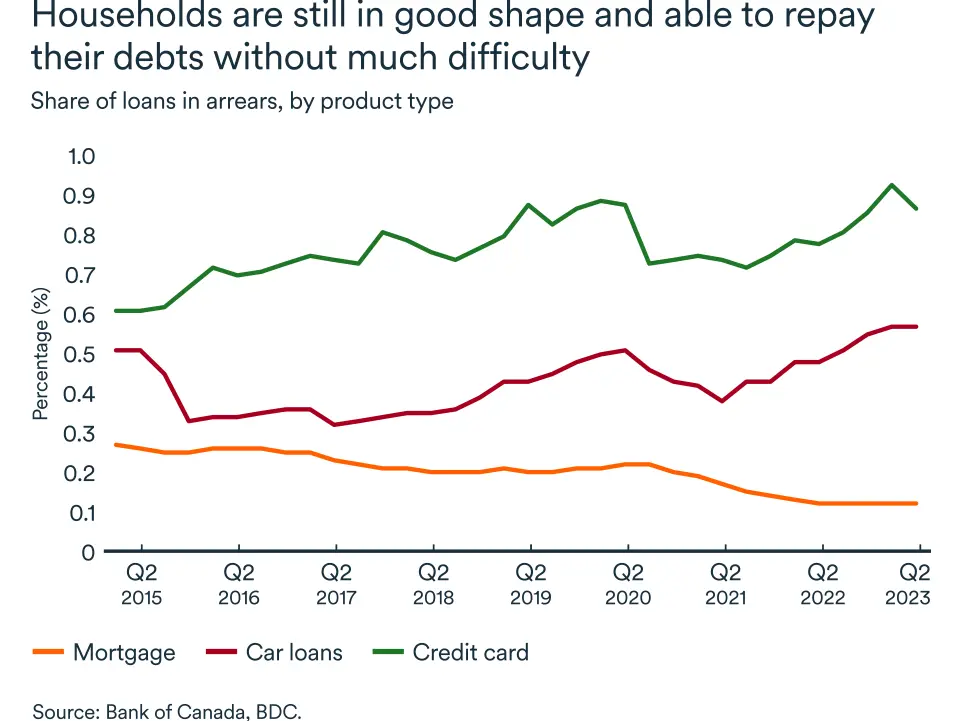

Households are repaying their debts

Solid economic growth depends on households, since consumer spending accounts for 60% of GDP in good times and bad. With high interest rates and inflation still well above the Bank of Canada’s 2% target, the purchasing power of Canadian consumers is under increasing pressure.

What's more, the high level of household debt in Canada makes the country's economy more sensitive to higher interest rates than, for example, that of our neighbours in the U.S.

There are signs that Canadian households were becoming more cautious. Household debt to disposable income fell to 180.5% in the second quarter—almost four percentage points lower than the level in the first three months of the year. This implies that income growth has outstripped credit growth as households avoid taking on new debt.

The latest interest rate hikes in June and July should continue to slow the pace of borrowing in the second half of the year as households pare debt and boost savings. Indeed, the household savings rate rose in the second quarter, with disposable household income growing more than twice as fast as household consumption expenditures.

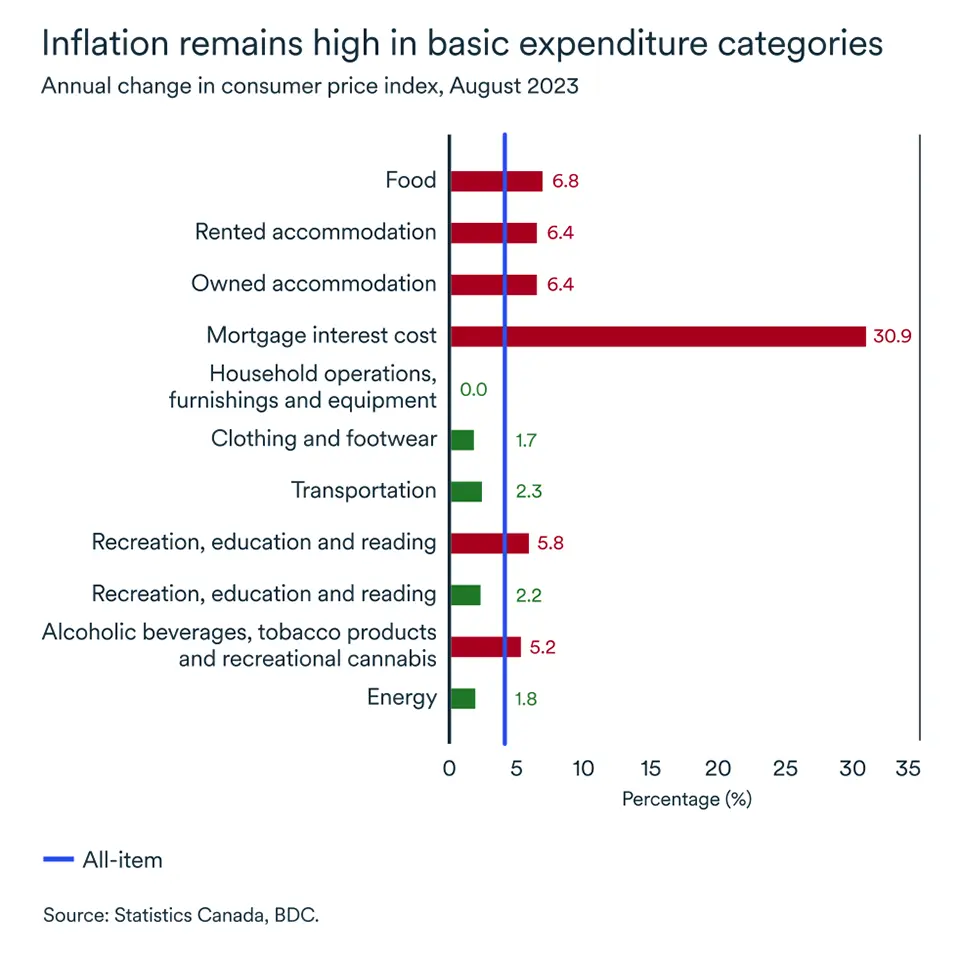

Inflation still above target

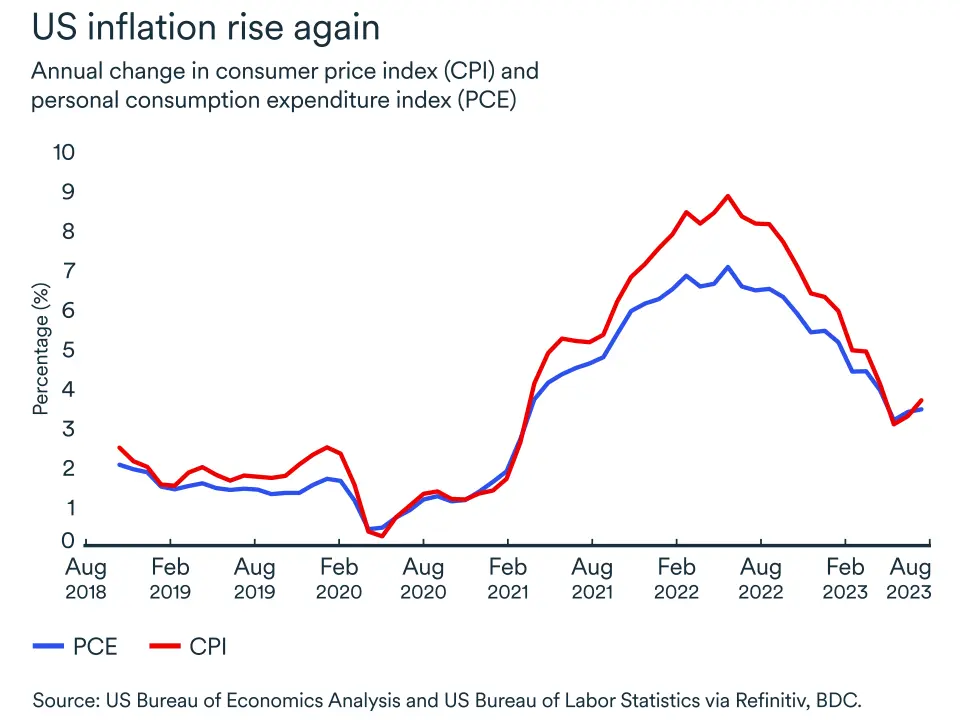

On the inflation front, the situation remains less than ideal. The consumer price index climbed back above the upper limit of the Bank of Canada’s 1%-3% target range in July and August, after reaching 2.8% in June.

It appears a number of challenges persist. Food price inflation remains stubbornly high at 6.8%, although a significant drop in August from July’s reading that was more than welcome by consumers.

Mortgage interest costs have risen 31% over the past twelve months. When they are excluded from the August data, inflation would have been 3.2%, rather than 4%. It should also be noted that inflation in durable and semi-durable goods remains within the target range—a sign that restrictive monetary policy has had the desired effect.

A slightly more worrying aspect of the August data was increases recorded in all three of the Bank of Canada's preferred core inflation measures. This re-acceleration of inflation heightens the risk that further interest rate hikes may be necessary. However, the slowdown in the economy suggests the Bank of Canada will stay on the sidelines at its October 25 meeting.

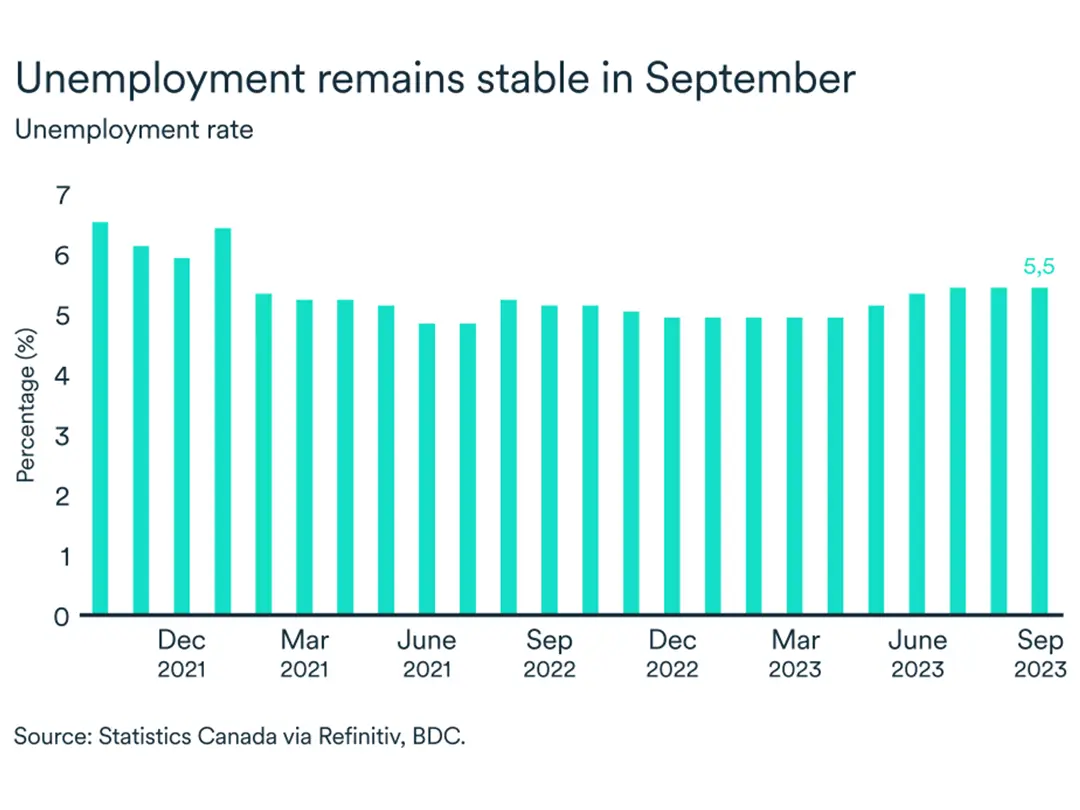

Rising employment and stable unemployment rate

The unemployment rate held steady at 5.5% in September, while total employment jumped sharply (+64,000 compared to August). However, employment gains were concentrated in the education sector (+66,000) and as pointed out by Statistics Canada, employment figures in this sector can be volatile at the start of the new school year.

Since the start of 2023, overall job creation stands at 388,000, while the unemployment rate has risen by half a percent. Hiring demand is expected to weaken further relative to the ever-increasing labor supply, but a few factors mitigate the anticipated slowdown in the labour market.

In July, the number of job vacancies fell again, but remains above the pre-pandemic trend. The wave of retirements continued into September, as students returned to school.

The impact on your business

- Consumers will continue to slow their purchases of expensive items or turn to substitute products. Find out how you can improve the value of your products and services to maintain sales. Make sure to manage your inventories well.

- Interest rates are likely to remain at current levels for some time to come. This is a good time to review your strategic plan.

- The expected economic slowdown has finally begun, but it's not too late to adopt good practices and adjust your company's finances accordingly.

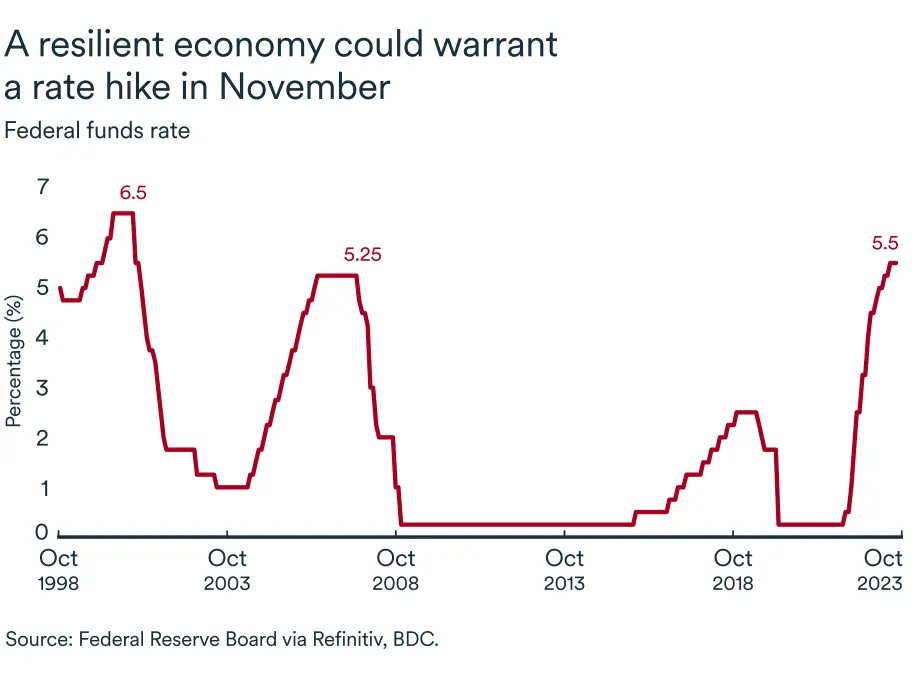

The U.S. economy remains on track for a soft landing

The U.S. economy continues to perform well despite higher interest rates and that could open the door for the Federal Reserve to raise the federal funds rate again on November 1, bringing it to 5.75%.

At its September meeting, the Fed maintained the target range for the rate at 5.25%-5.5%, its highest level in 22 years, following a 25-basis point increase in July. The majority of participants on the Federal Open Market Committee said they believe a further increase would be in order before the end of 2023.

The economy continued to expand at a good pace in the second quarter, with GDP growth reaching 2.1%. The increase was supported by business investment, consumer spending and government spending.

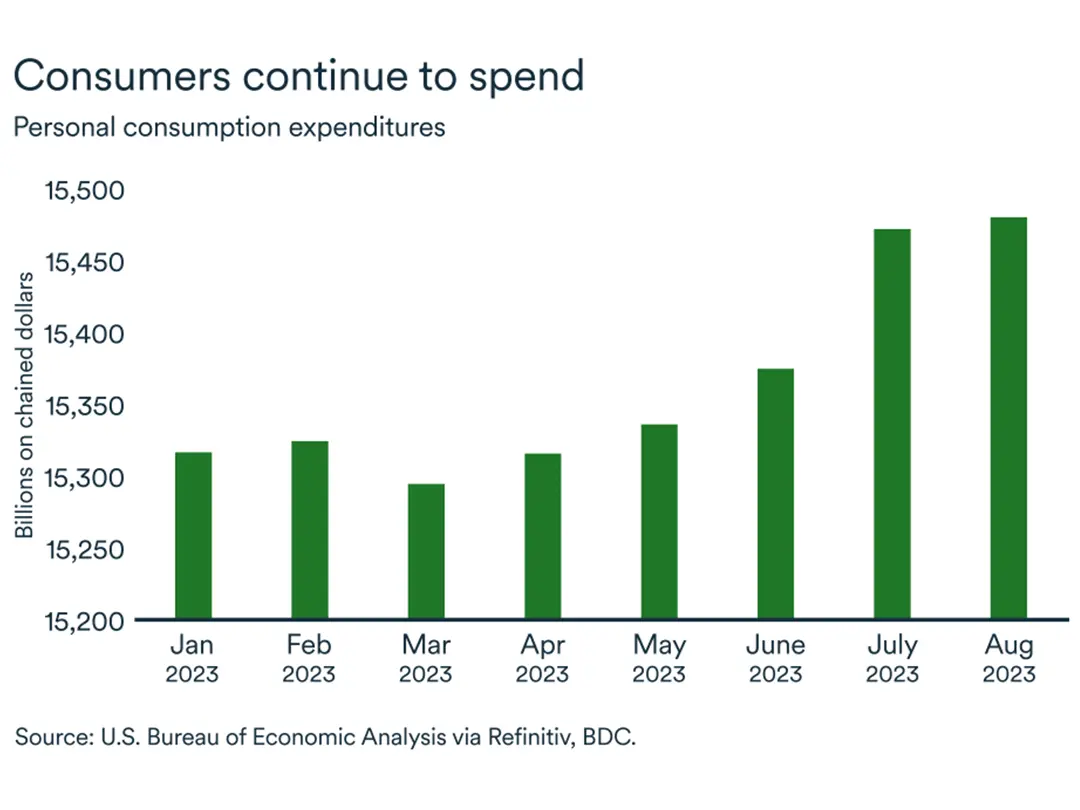

Americans keep their wallet open

U.S. households continued to make purchases despite high interest rates. Personal consumption expenditure rose by 0.1% in real terms (taking inflation into account) between July and August, even though disposable income fell during the summer.

U.S. savings have dropped continuously since May, sending savings as a share of disposable income to its lowest level of the year in August at 3.9%.

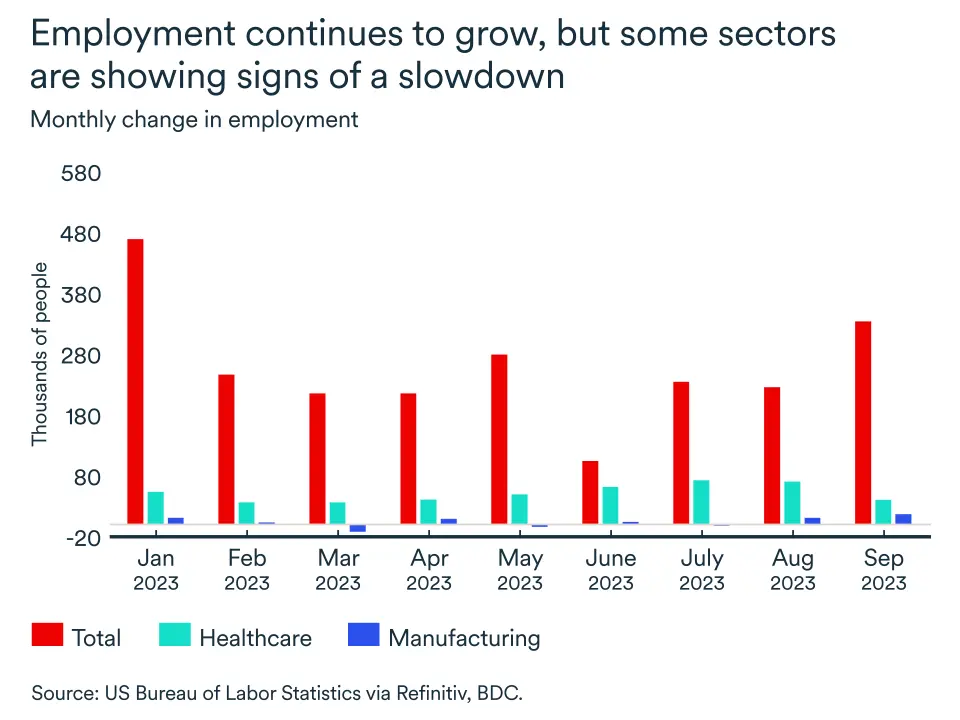

Can the strong U.S. job market continue?

The U.S. is enjoying historically low unemployment rates across much of the country, and net job creation is still very strong, averaging almost 266,000 per month in the third quarter alone. Another sign of strength is that there are currently almost 1.5 jobs available for every unemployed person.

However, there were signs the picture may not be as rosy as it seems. Job creation has been heavily concentrated in the healthcare sector recently, a sector that’s typically considered to be sheltered from economic cycles.

Job creation in manufacturing, meanwhile, has fallen sharply, from an average of 32,500 per month last year to just 4,100 per month this year. Job growth in the service sector has also slowed, but not as dramatically. A slowdown may be in the offing in sectors that are more sensitive to economic cycles.

A mixed inflation picture in August

Inflation measured by the Personal Consumption Expenditure (PCE) price index was 3.5% in August. Excluding food and energy, it was 3.9%. The former reading was a slight increase over July, while the latter was lower.

The Federal Reserve generally places greater emphasis on inflation as measured by the PCE spending index, rather than the consumer price index (CPI), which also picked up to 3.7% versus 3.2% in July).

The impact on your business

- Rising interest rates in the U.S. will have an impact on Canada. Anyone who borrows in U.S. dollars will see their interest costs rise, including banks that borrow on the wholesale market. Banks will likely pass on these higher costs to Canadian businesses and consumers who borrow in Canadian dollars.

- The loonie should depreciate against the greenback, as the interest rate differential between the two countries continues to widen, especially as the recent outlook points to a U.S. economy that’s more resilient to interest rate increases. Canadians exporting to the U.S. will be more competitive, but Canadian businesses will face higher costs to import goods and services from the U.S. or to trade on international markets.

- Global financial conditions are gradually tightening as the U.S. dollar appreciates. If you have suppliers or buyers in other countries who have debts in U.S. dollars, they may be put to the test.

Faced with uncertainty, oil market is hit by great volatility

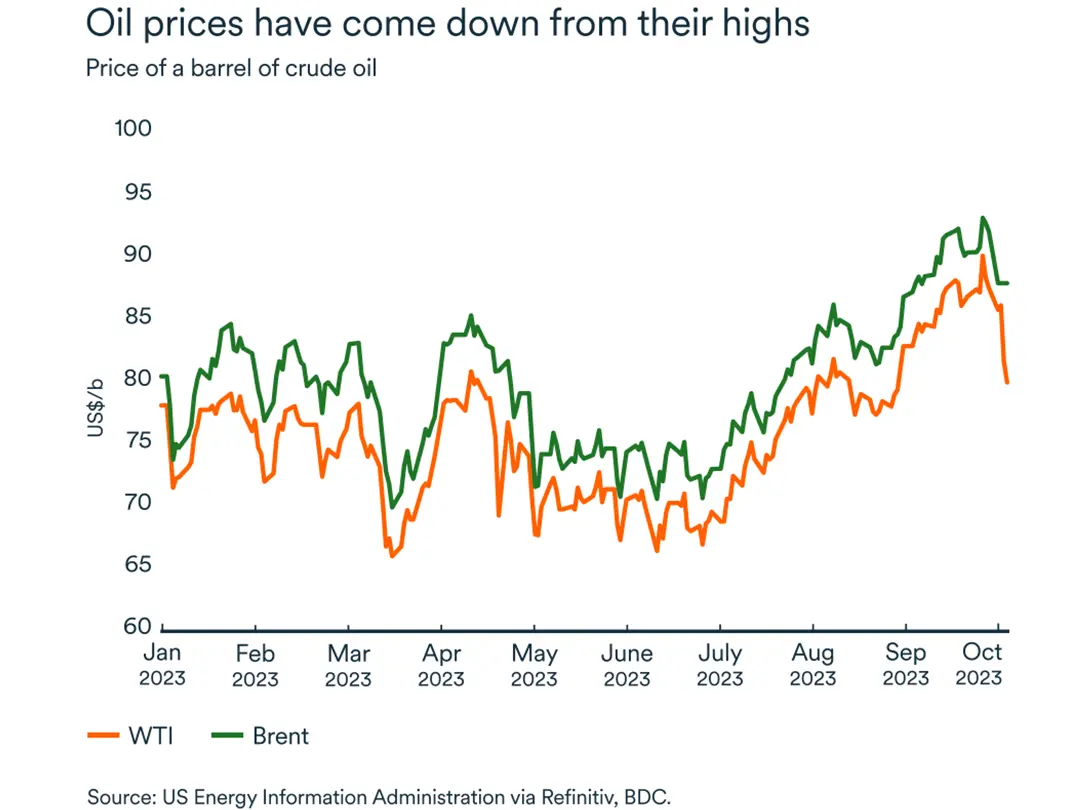

At the time of writing, WTI was trading at US$85, while Brent was at US$88. That’s well off the marks reached at the time of last month’s Economic Letter. Back then, the main crude oil benchmarks had reached $93 and $95 per barrel, respectively.

There are currently opposing forces at work in the oil market, causing big price swings. On the one hand, there are supply cuts from the OPEC+ group of producers that will continue into the autumn. Those cuts put upward pressure on prices last month.

On the other hand, concerns about a global economic slowdown as well as inventory drawdowns have brought prices down from their highs. With so much uncertainty, volatility will continue to dominate the crude oil market this autumn. More recently, the main source of price movement have been the attacks on Israel.

OPEC+ expectations push up prices

In early October, OPEC+ confirmed its members would be sticking to production caps that prevailed this summer. Separately, Saudi Arabia and Russia also declared they would maintain their voluntary cuts into November. These decisions were largely based on forecasts for sluggish global oil demand.

The resilience of many of the world's leading economies over the past three months, combined with supply constraints imposed by OPEC+, have pushed the price of oil up by 17% since the start of the year. Now, an economic slowdown is taking hold around the world (including in Canada, but more importantly for oil, in China). At the time the OPEC+ cuts were announced, the economic headwinds weren’t as pronounced.

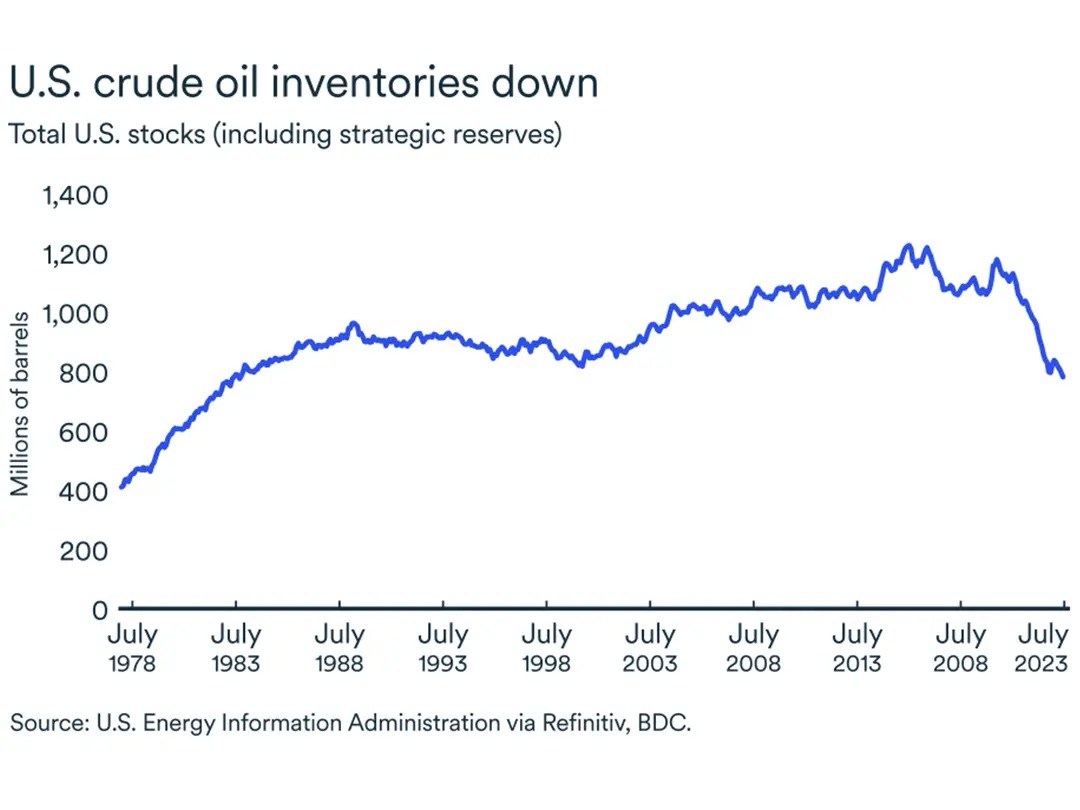

U.S. inventories drop

U.S. crude inventories recently fell to their lowest level of the year. This was due to strong foreign demand, which supported exports. Conversely, gasoline inventories rose much more than the markets had expected due to weak domestic demand, a reflection of a slowing U.S. economy.

Crude inventories fell by 2.2 million barrels in the week to September 29 to 414.1 million barrels, their lowest level since December 2022. This reduction was five times greater than analysts had expected.

Notwithstanding the strength of crude exports, oil prices plummeted after the release of the U.S. inventory data. Markets are particularly concerned about weak gasoline demand south of the border.

Bottom line…

The recent slide in oil prices could reverse again in the fourth quarter. If a feared recession fails to materialize in the coming months, and demand for oil remains buoyant, the prices of the main benchmark indices could rise rapidly and move even closer to the US$100/barrel mark. For the time being, however, the correction in oil prices remains driven by pessimism about the global economic outlook.

Bank of Canada to remain on the sidelines

The Bank of Canada is expected to maintain the status quo at its October meeting, having done the same in September. The key rate would therefore remain at 5.0% following the October 25 meeting of the Governing Council. Although signs of improvement in inflation have turned around recently, and the job market is not losing as much strength as anticipated, the economy is indeed showing signs of softening. At the time of writing, some of the key data that will guide the Bank of Canada's future decision remain unknown, namely the September inflation report and the results of the Business and Consumer Outlook survey. If September inflation rises above 4% and inflation expectations remain too high, the central bank could be forced to raise the policy rate once again.

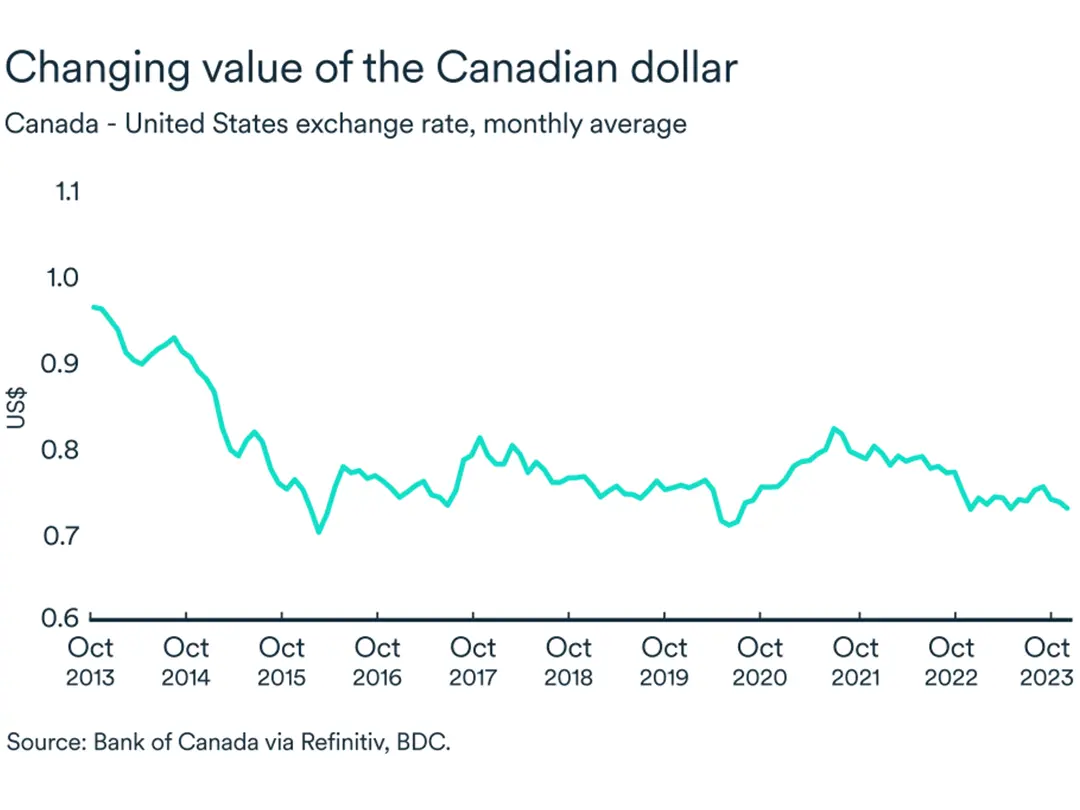

The loonie continues to fall

The Canadian dollar depreciated even further at the start of the fall, averaging just under US$0.74 in September and getting very near US$0.72 since the beginning of October. The Canadian dollar's slide against the US greenback is partly explained by the interest rate differential between the two countries. The Canadian outlook was clouded recently by negative GDP growth in the second quarter, in contrast to the US, which continues to grow at potential. The Canadian dollar is likely to remain weak, fluctuating between US$0.73 and US$0.72 over the coming weeks.

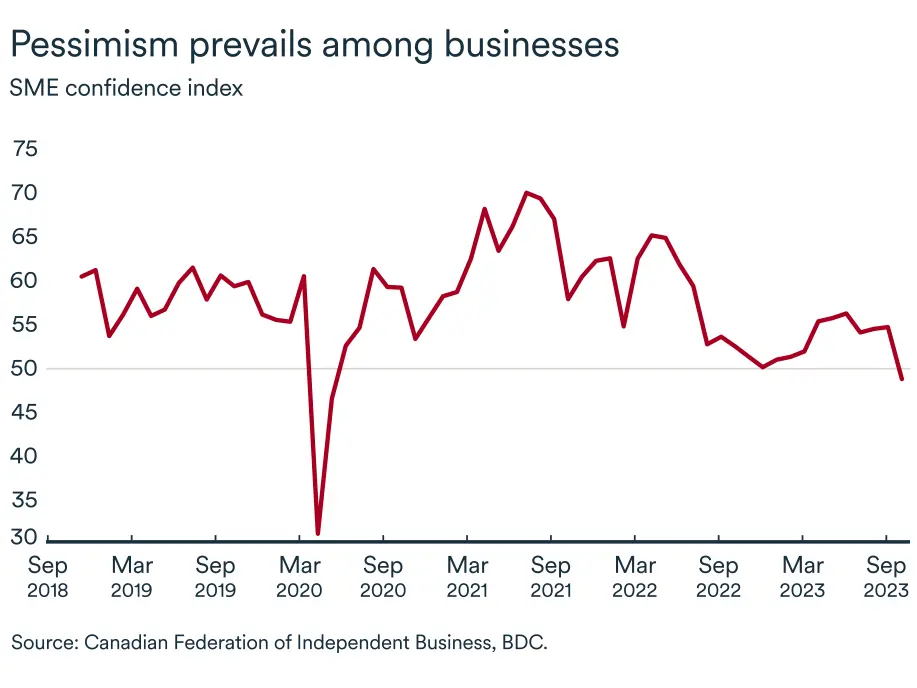

Pessimism grips business leaders

CFIB's business confidence index for the year ahead fell below the critical 50 mark in September, reaching a level close to the trough that prevailed in April 2020, at the height of the COVID-19 pandemic. The index fell from 54.6 to 48.7 between August and September. This suggests that companies are becoming increasingly fearful of the future, with the majority anticipating a deterioration in their activities over the coming months.