Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreWill a new round of interest rate hikes trigger a recession?

Central banks have had to face the risk of causing a recession as they raised interest rates over the last year and a half. But so far, the "R-word" has referred more to resilience than recession in Canada. Now, the Bank of Canada has raised rates again after a lengthy pause, rekindling concerns about a recession. Can the Canadian economy still come in for a soft landing?

The challenge faced by central banks

Monetary policy decisions are never easy, and the current economic environment is proving to be a major headache for central banks around the world. Inflation has remained stubbornly high in many countries, amid economic and geopolitical turbulence.

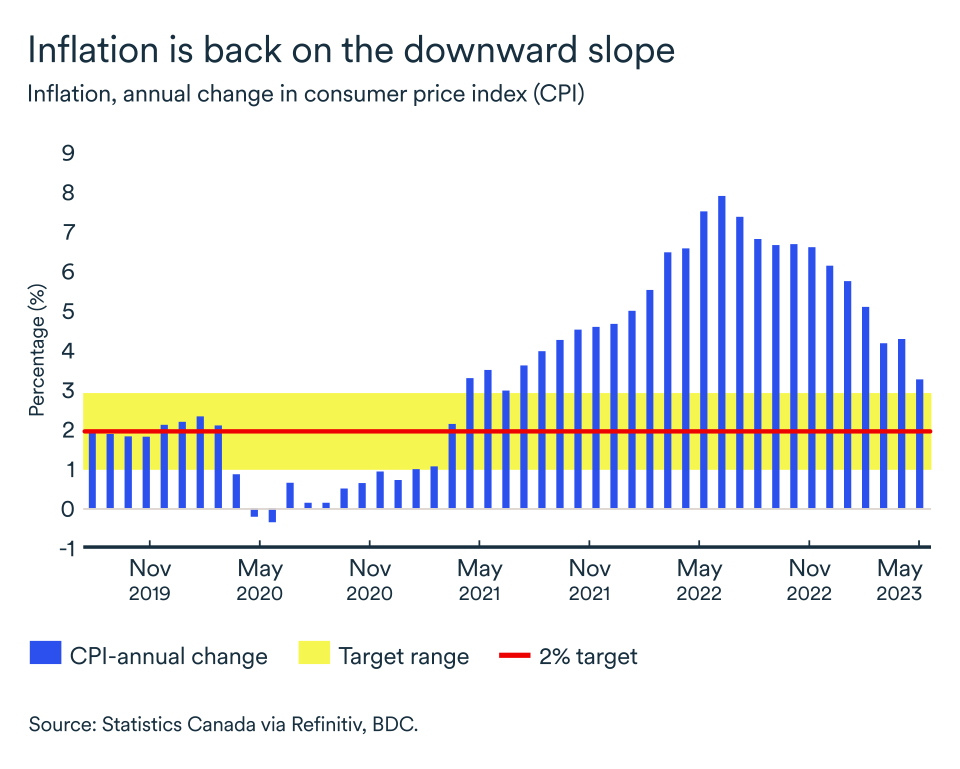

In Canada, the inflation picture has improved markedly, but there is still work to be done to get the rate down to the Bank of Canada’s 2% target.

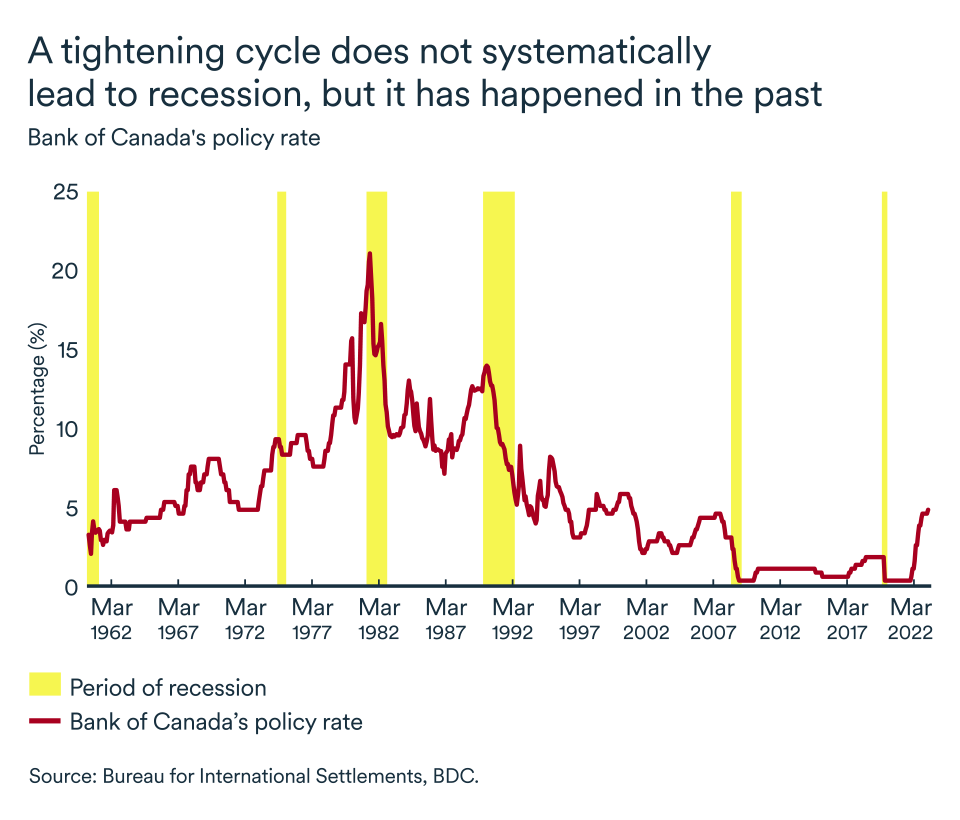

The good news is that GDP and employment have continued to grow despite one of the fastest periods of credit tightening in decades. The bank raised its trend-setting policy rate by 475 basis points in just 18 months.

However, the full effect of rate hikes isn’t felt for several months so there could be more slowing to come from the increases already announced. Tightening cycles have historically tended to end in recession and that’s why each new rate increase has been met with growing concern.

Can the Canadian economy absorb the latest rate hike?

The Bank of Canada did it again on July 12. It raised its trend-setting rate by a further 25 basis points to 5.0%—a level not seen in Canada since 2001.

In doing so, the bank hopes to bring inflation closer to its target range of between 1% and 3%, with 2% being the mid-point. It's important to remember that the bank’s mandate is to control inflation, not support economic growth, per se.

Inflation, as measured by the annual change in the consumer price index, fell rapidly in May to 3.4% from 4.4% in April. Inflation is, therefore, very close to the upper limit of the Bank of Canada’s target range.

The much-vaunted fight against inflation is likely to subside, however, after the July announcement, as previous rate hikes affect a few more households and businesses each month, and should therefore prove sufficient to bring price stability back to Canada.

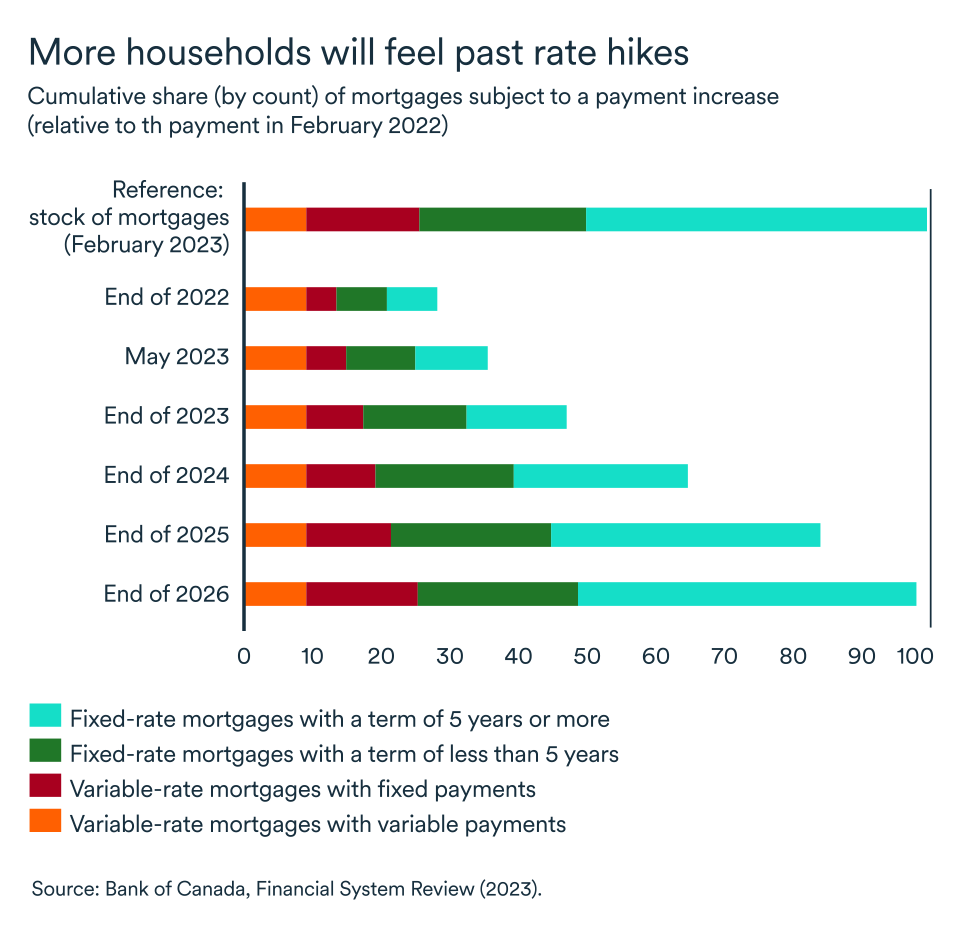

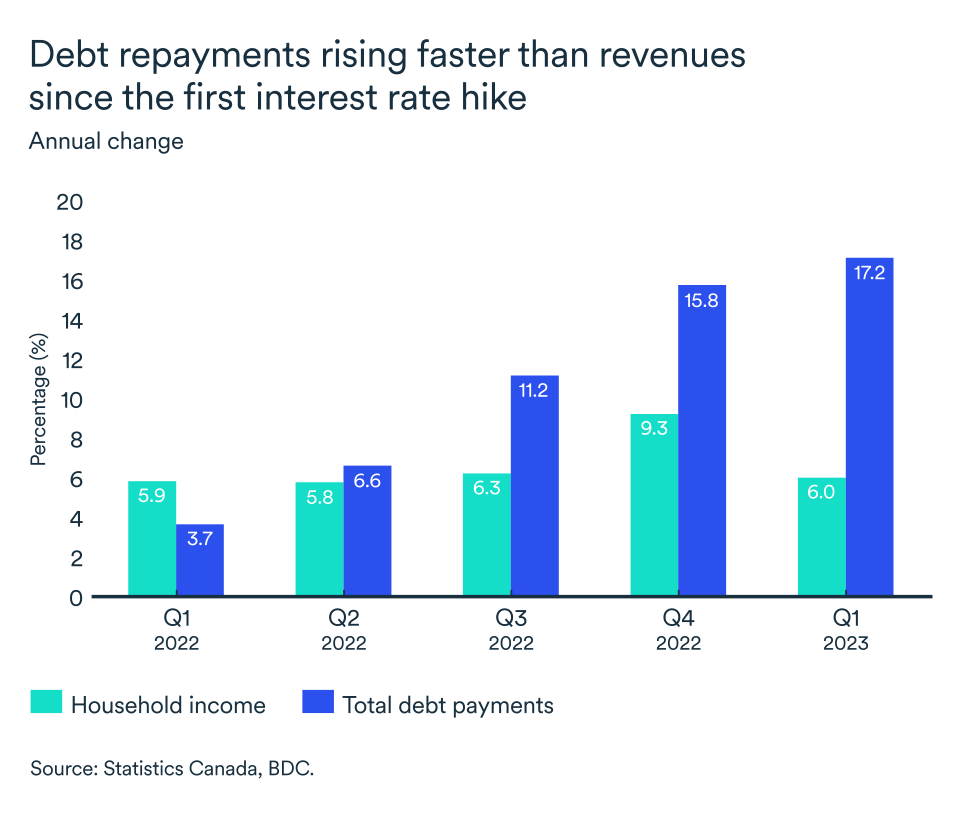

For now, only a third of mortgages have been affected by rising interest rates. This ratio will reach 50% by the end of the year, and the median increase in payments over the 2023-26 period will be around 20%, according to the Bank of Canada. Canadian households are highly indebted, so their ability to meet their financial obligations will become increasingly difficult. On average, Canadians owe $1.85 for every dollar of disposable income.

While there’s a risk the Bank of Canada and the U.S. Federal Reserve will push their respective economies into recession, this is not our base-case scenario in the short term.

Multiple factors threaten growth

However, the economic outlook remains uncertain. Structural upheaval is threatening the relative stability to which Canadians had become accustomed in recent years.

A series of factors are hampering growth and increasing business costs. These include the end of major gains from globalization, the decarbonization of economic activity, the growing impact of natural disasters and labour force problems caused by an aging population.

In this environment, we expect inflation to return to 3% by the end of the year, but getting it down to 2% will take longer. While we don’t expect more rate increases in Canada in this cycle, the Bank of Canada is unlikely to start reducing rates until 2024. Out-of-control inflation would be more damaging in the long term than a recession.

No collapse, but a slowdown

Ultimately, despite persistently higher interest rates, most consumers are still able to meet their financial obligations while maintaining enough new spending for now.

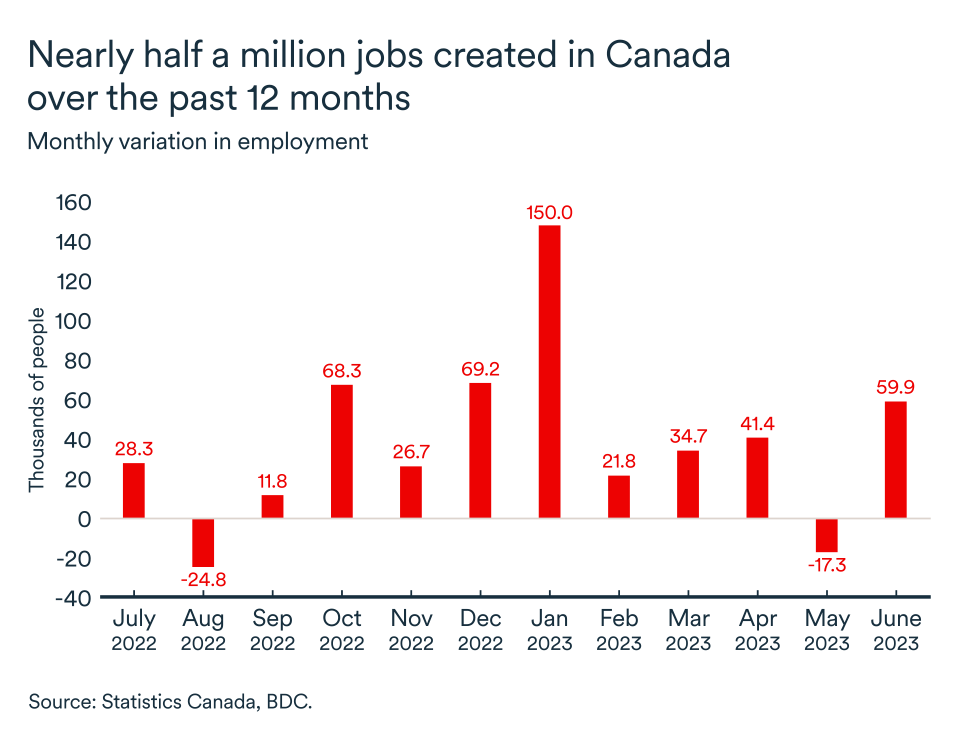

The reason for our cautious optimism lies mainly in the labour market, which continues to perform well overall. Employment is up by almost half a million in a year, and household disposable income is still robust. Government spending and investment will also support economic growth, which will nonetheless remain modest over the next twelve months.

The advantage of a slowdown generated by tighter credit conditions is the Bank of Canada will have more leeway to lower rates to head off a more serious economic deceleration.

What it means for your business

- The latest interest rate hike by the Bank of Canada has rekindled fears that the economy could fall into recession. While we remain optimistic a recession will be avoided, the hike will slow demand for business as consumers return to a cautious stance.

- The hike should be sufficient to bring inflation back into the target range, but interest rates will not start to come down for several months. Economic growth will be modest in 2024 as well.

- Higher interest rates will affect more and more households over the next few years. While cost pressures continue to pose a major challenge for businesses, it will be increasingly difficult for them to pass the bill on to cash-strapped customers. Companies therefore have every interest in optimizing their operations today. Discover innovative and successful operational efficiency solutions here.

The road to economic stability continues

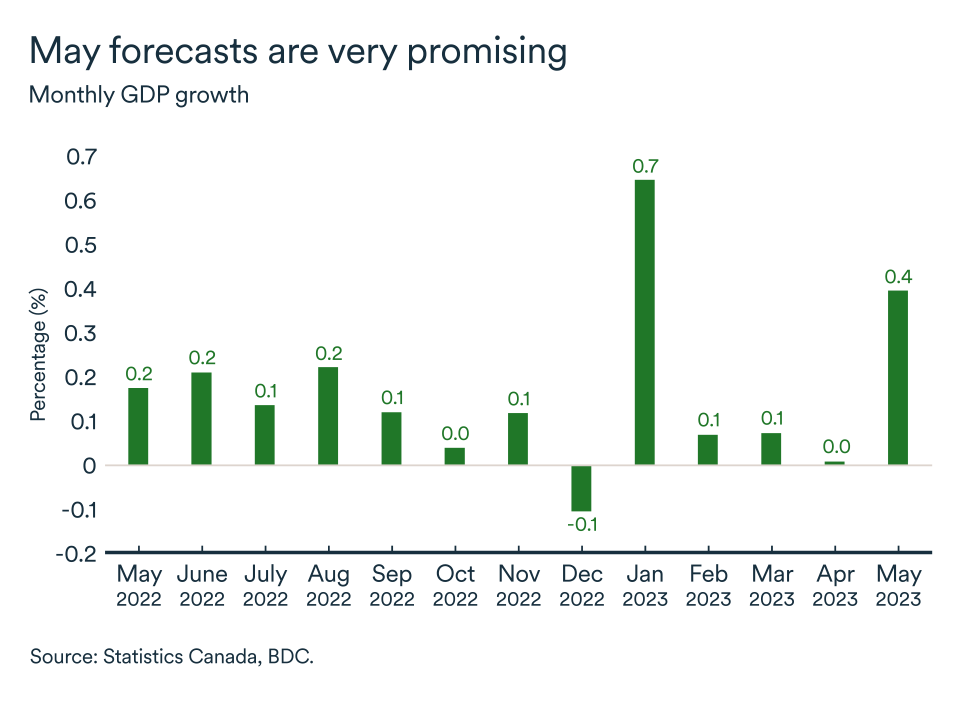

Economic growth in Canada see-sawed during the spring months as a series of interest rate hikes did their intended job of cooling inflation in the country.

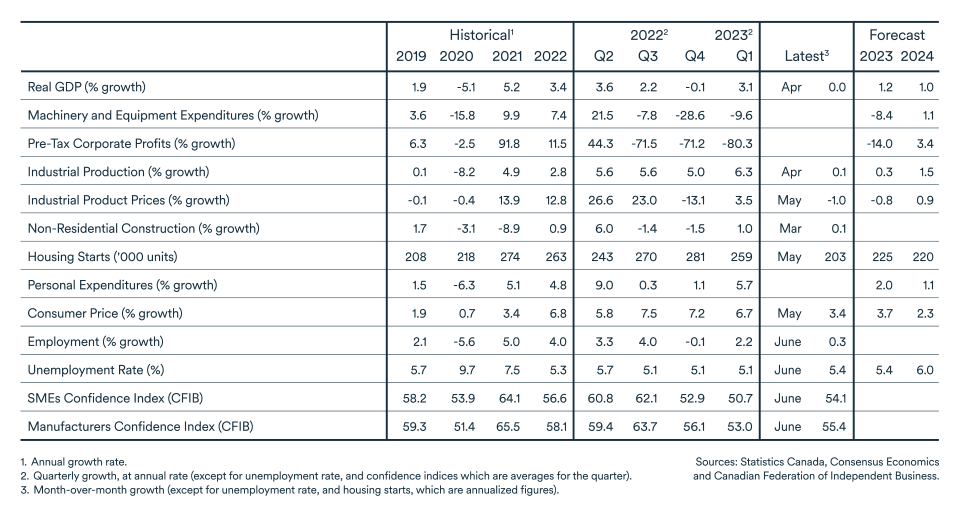

Growth was revised upwards to 0.1% in March but stagnated in April (0.0%). Half of the sectors covered by Statistics Canada recorded gains in April led by the construction industry, the real estate market and retail. By contrast, slowing hit the wholesale and manufacturing, which experienced its first monthly growth decline of 2023.

StatsCan's initial estimates for May were positive. According to its preliminary report, GDP rose by 0.4% during the month with much of the growth coming from sectors that experienced slowing in April (manufacturing and wholesale). If confirmed, these gains would offset April’s slowdown. But much of the rebound is due to thousands of federal civil servants returning to work, following a strike in April.

Significant improvements in inflation readings

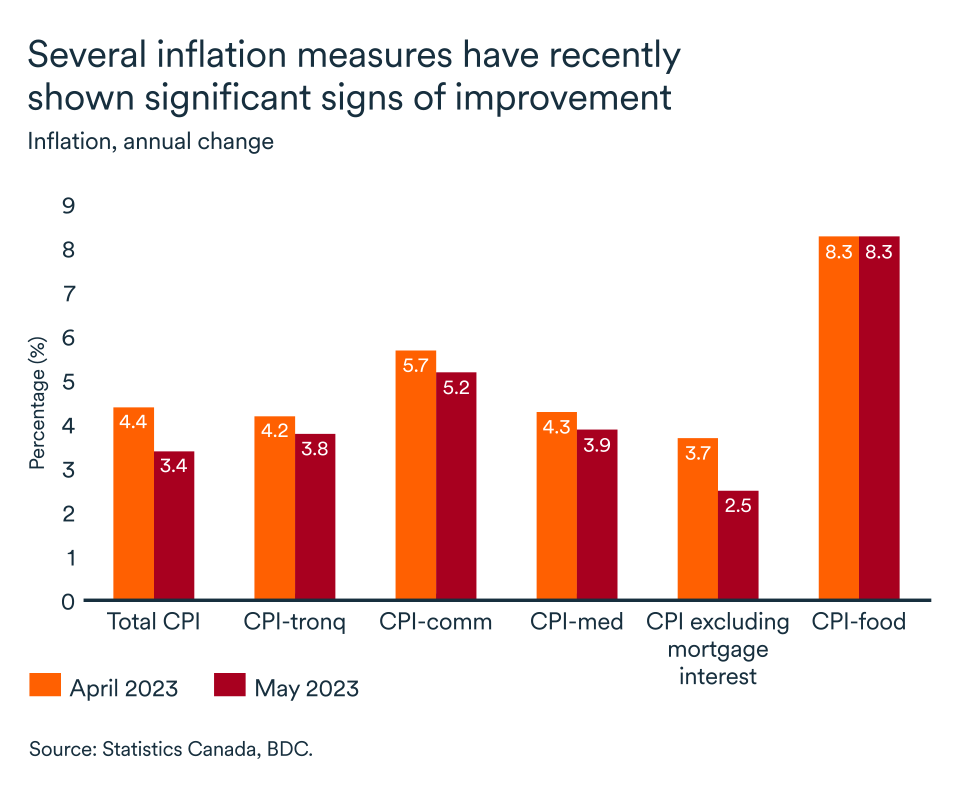

Good news was to be found in the inflation figures. In annual variation, the Consumer Price Index (CPI) rose by 3.4% in May. This represents a significant decline from April's 4.4%.

More important than this drop in overall CPI growth was an improvement in core inflation measures (favoured by the Bank of Canada). They were also approaching the Bank of Canada's target range for inflation of between 1% and 3%.

Canada's central bank is likely to have found even more comfort in another inflation measure—CPI excluding mortgage interest costs. It rose by just 2.5% year-over-year.

One dark cloud was food price growth. Here, inflation remained stubbornly high at 8.3%. The Bank of Canada's monetary policy has less impact on these prices because foodstuffs are more dependent on global market conditions.

Against this backdrop, we believe the most recent rate increase by the Bank of Canada is likely to be the last if the favourable inflation trend continues.

First rate cut not expected before 2024

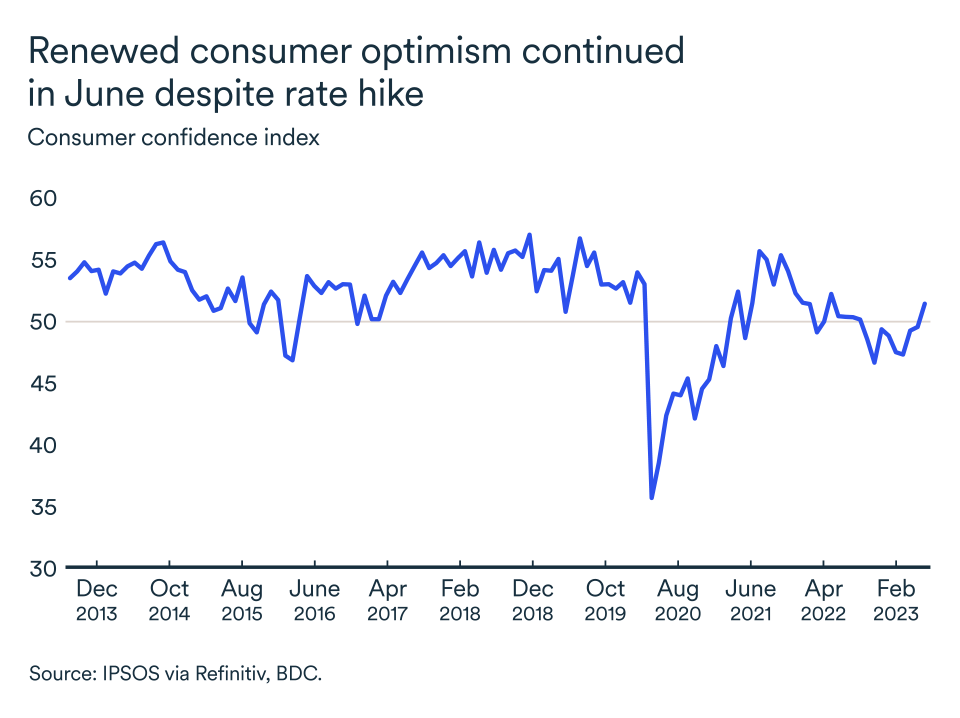

The progress on inflation does not mean, however, that the bank will cut rates any time soon. The reaction of Canadian households and businesses to the bank’s rate pause announcement in January demonstrated the extent to which uncertainty and expectations can affect the real economy.

Consumer confidence and business optimism rebounded strongly following the pause announcement, driving consumption, hiring and wages higher. The residential resale market also regained vigour, which along with population growth, supported domestic demand. With inflation heating up again, the Bank of Canada had to step in to cool the enthusiasm with a 25 basis point increase in June.

The strong positive reaction to the pause announcement from businesses and consumers will likely lead the Bank of Canada to be cautious about reigniting inflation pressures when announcing rate reductions. Therefore, we don’t expect easing to begin until the first half of 2024 with the bank’s key rate declining to 3% by year end from the current 5.0%.

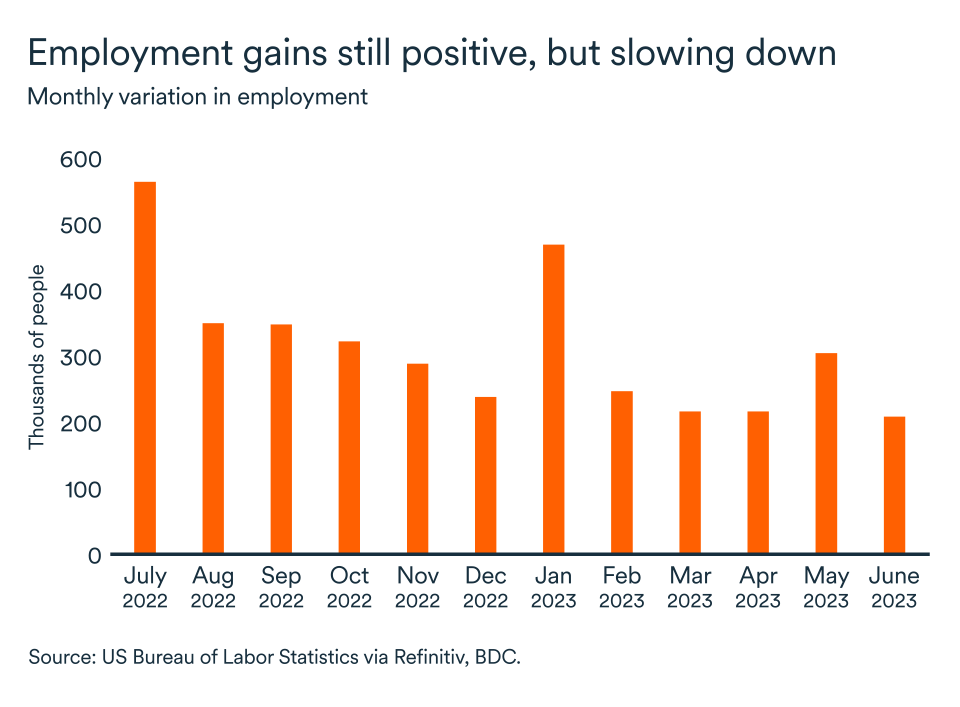

Employment slows but remains strong

Some 60,000 jobs were created in June. This marks a rebound in employment after the losses incurred in May. According to the Bank of Canada's Business Outlook Survey, the pace of hiring is set to continue to slow in Canada and more job losses are therefore to be expected in the coming months. However, employment losses will remain low since 30% of companies are still having difficulty hiring or retaining workers.

There were almost 820,000 job vacancies in the country in April. Population growth should help companies to meet these labour needs, but unemployment could rise again because the process of hiring immigrants is cumbersome, according to companies surveyed by the Bank of Canada. The national unemployment rate rose from 5.2% in May to 5.4% in June.

The impact on your business

- Despite ongoing economic uncertainty, the Canadian economy remains well-positioned for continued growth. Nevertheless, businesses should expect (and prepare for) a slowdown that will last for several months.

- With inflation falling, the Bank of Canada's monetary policy is having its desired effect. However, it will be several months before the full impact of past rate hikes is felt in the economy. Rates are unlikely to rise further, but businesses and households will have to be patient in waiting for a rate cut in Canada.

- Wages and the business costs will continue to rise. If your business is struggling with rising costs, it may be time to explore how you can boost efficiency and productivity because it will be less easy to pass on cost increases to consumers in the coming months.

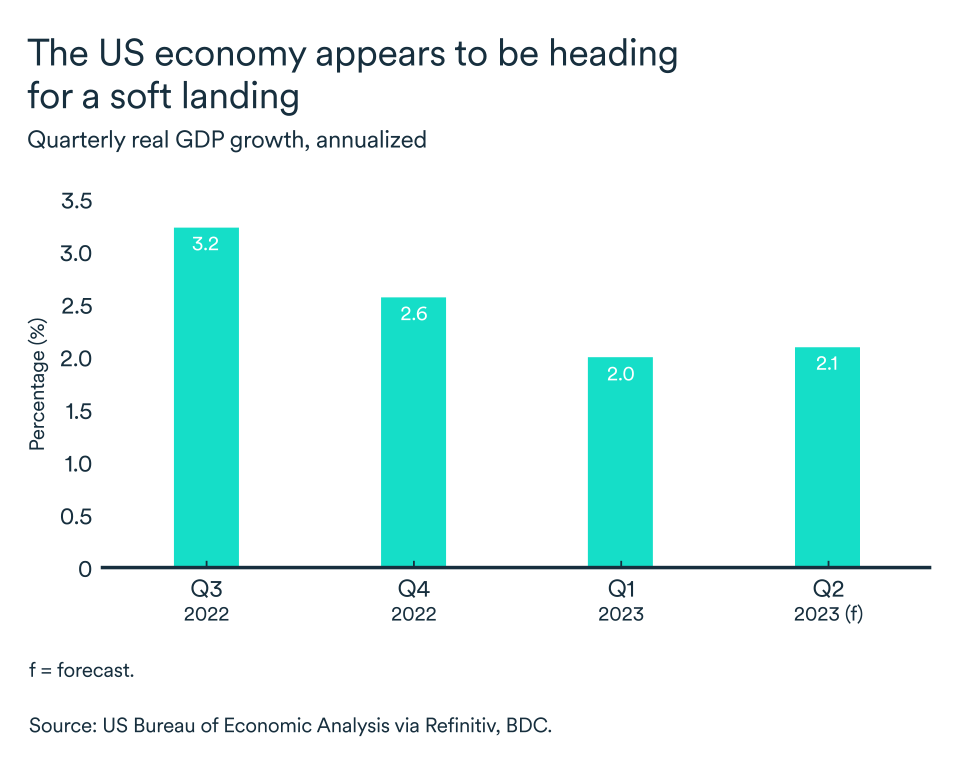

Positive growth data ease recession concerns

The latest indicators suggest the U.S. Federal Reserve has succeeded in slowing the economy to bring down inflation without tipping the country into recession. Of course, a soft landing for the U.S. economy is still not guaranteed, especially because the Fed is likely to raise interest rates once or twice more between now and the end of the year.

Economy continues to grow

U.S. real GDP growth came in at 2.0% for the first quarter—a significant improvement over a preliminary estimate of 1.3%. The upward revision is attributable to higher exports and lower imports than initially anticipated.

Consumer spending also grew faster than estimated at 4.2%. While the news on consumer spending was good for the first quarter, monthly data pointed to a slowdown since then. However, overall GDP should continue to grow around 2% in Q2 as well.

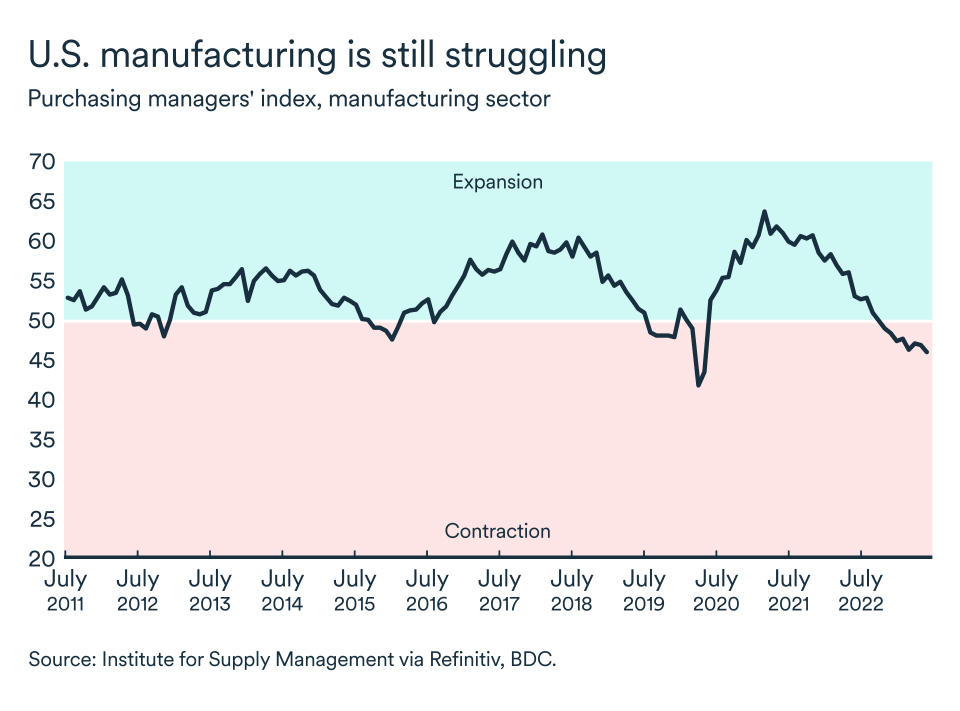

Manufacturing pulls back

The purchasing managers' index for the U.S. manufacturing sector declined further in June. The index fell to 46, its lowest level since May 2020 when the global economy was on pause due to the pandemic. This is the eigth consecutive month with the index below the 50 mark, signalling a contraction in production.

These data are consistent with a reallocation of household spending towards services from credit-financed goods in response to the 500 basis point increase in interest rates orchestrated by the Fed over the past year and a half. Businesses are sensitive to a downturn in demand and are reducing inventory.

Employment growth slows

More jobs are still being created than lost in the United States. However, the pace of growth slowed further in June to 225,000 jobs. The gains were sufficient to bring the unemployment rate down to 3.6%.

However, labour market pressure seems to be easing south of the border. The annual growth rate in average hourly earnings slowed again but remains too high at 4.35%.

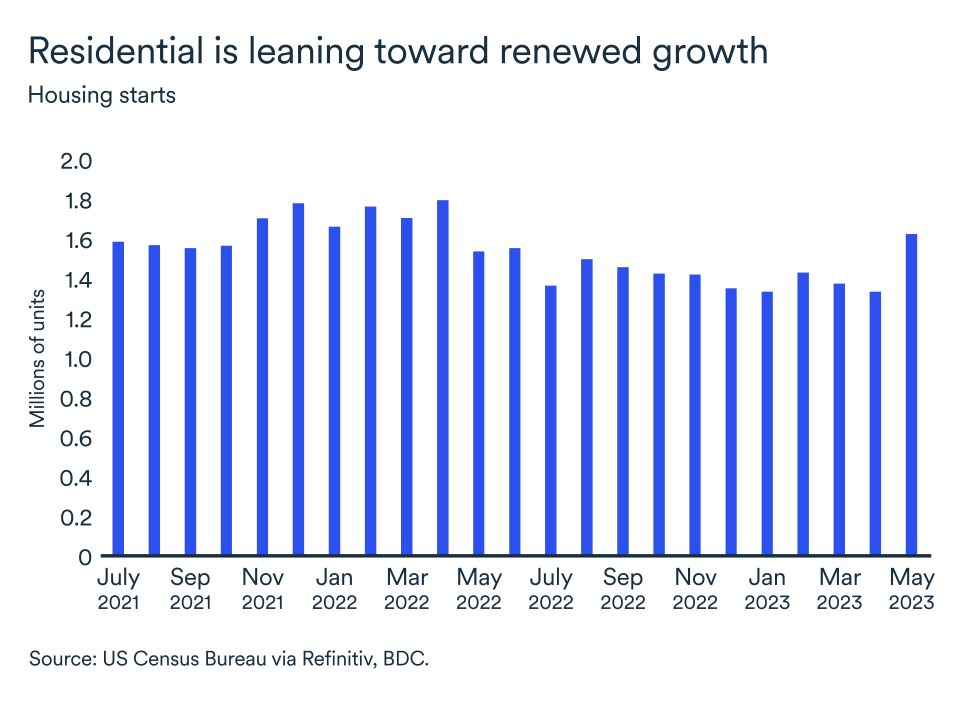

The residential market is slowly recovering

The residential construction sector appears to be benefitting from a modest upturn in demand. Spending on residential construction rebounded by 2.2% in May, after falling by 0.9% the previous month. Much of this growth came from increased investment in single-family housing projects.

Meanwhile, U.S. housing starts surged by almost 22% to reach an annualized rate of 1.6 million in May 2023, the highest level since interest rates began to rise. Even if a setback were to materialize in June, the second quarter of 2023 should see some growth in residential investment, which would be its best performance in two years.

Inflation finally dips below the 4% mark

Inflation measured by the consumer price index rose from 4.0% in May to 3.0% in June. More importantly, inflation measured by the Personal Consumption Expenditure (PCE) price index in May came in at 3.8%. However, the annual variation in the index that excludes food and energy has remained unchanged since the beginning of 2023 at 4.6%.

The Federal Reserve is expected to increase its trend-setting federal funds rate by 25 basis points at its July 25-26 meeting, moving it to 5.5%.

The impact on your business

- Even if economic growth continues in the U.S., gains for Canadian companies will likely be limited. Demand for goods continues to slow, and Canadian exports to the U.S. are largely dependent on manufacturing, raw materials, and retail and wholesale trade.

- A tepid recovery in the construction and residential real estate industries in the U.S. should benefit Canadian companies. However, Canadian exports to the U.S. will be hurt by adverse U.S. trade policies and lumber supply problems following sawmill closures caused by forest fires. Canadian companies may, therefore, find it harder to capitalize on renewed growth south of the border.

- U.S. inflation still seems harder to contain than in Canada. Interest rates in the U.S. will remain higher than in Canada, which should keep the Canadian dollar at its current level, a plus for exports.

More production cuts to come

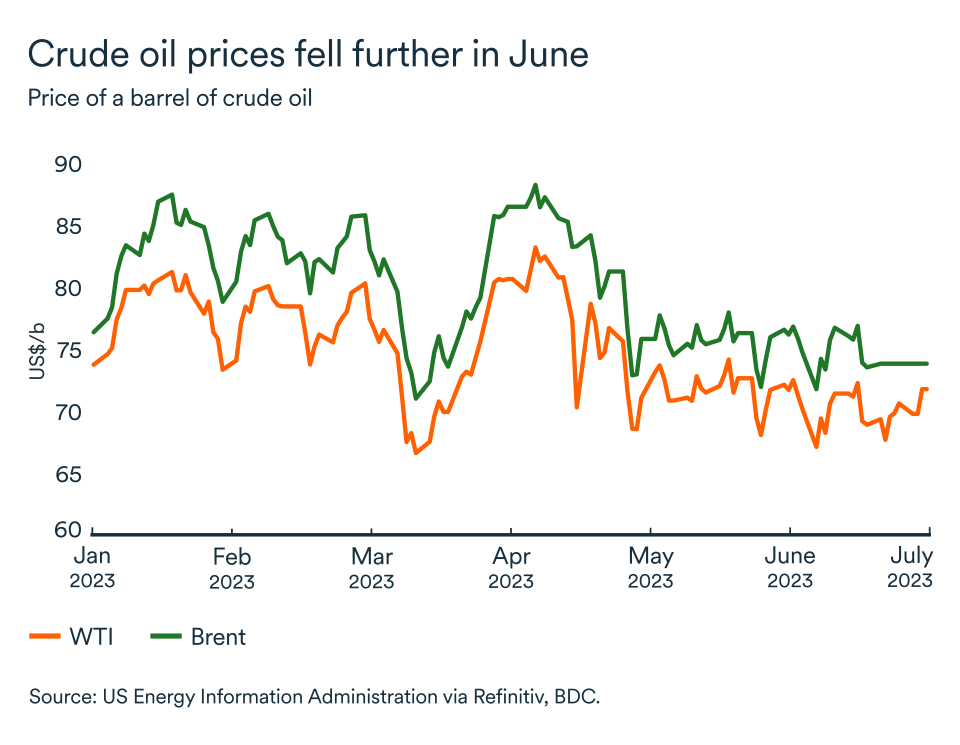

Crude benchmark prices fell further in June. WTI fell below US$70 and Brent below US$75. The main reason for the price declines is a global economic slowdown taking shape in response to tightening credit conditions worldwide.

New cutbacks

Faced with recent price weakness, exporters have announced further production cuts for August. Saudi Arabia will extend July's voluntary cuts into August to the tune of 1 million barrels per day (mb/d). Other countries have joined the initiative. Russia and Algeria have pledged to cut their production and exports by 500,000 and 20,000 barrels a day, respectively.

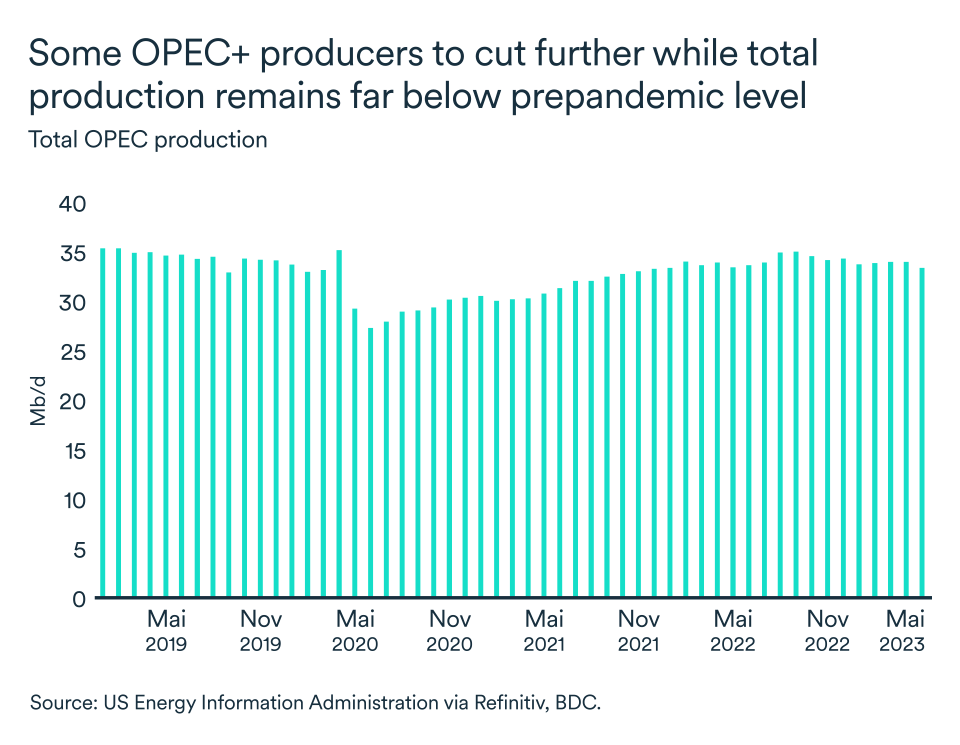

The cuts planned by the Organization of the Petroleum Exporting Countries and its allies (OPEC+) now amount to over 5 mb/d, or 5% of world oil production.

Uncertainty should keep prices low

Despite the planned new production cuts, crude oil prices are unlikely to appreciate much further. Prices rose in reaction to the announcement of new cuts but quickly returned to their previous levels.

The price weakness reflects an uncertain global economic outlook and persistent fears of recession with the European Union and the United States both expected to raise interest rates further this summer. The manufacturing sector continues to be in difficulty amid sluggish Chinese and European demand.

China could change course quickly

China's economic recovery has been disappointing since COVID restrictions were lifted at the end of December. Yet crude oil imports have grown by a surprisingly strong 6.2%. The trend continued in June, with Refinitiv estimating that imports reached 12.5 mb/d, the third highest level ever recorded.

This indicates that Chinese refiners are taking advantage of low prices in the oil market. However, they have a tendency to quickly restrict imports when prices rise. The country could adopt this strategy without creating major supply distortions, since China has significantly replenished its oil inventories.

Bottom line…

Faced with economic uncertainty and rising interest rates threatening global growth, particularly in the manufacturing sector, the prices of the main crude benchmarks fell even further at the beginning of the summer.

These price declines prompted major exporters to further voluntarily limit their production. These efforts may prove futile, however, as China could rapidly reduce its crude oil imports without harming the country's energy needs.

Bank of Canada raises key interest rate to 5.0%

The Bank of Canada raised its key rate by 25 basis points at the June meeting, and did so again on July 12, bringing the rate to 5.0%. Despite signs of improvement in inflation, Canada's central bank felt that demand was still too strong in the country, and that credit conditions needed to be tightened a little further. The rate is now expected to peak at 5.0% this year, meaning that the Board of Governors is done with rate hikes and that the next change in monetary policy will be a rate cut. Of course, more economic indicators will have to slow down to get to that point.

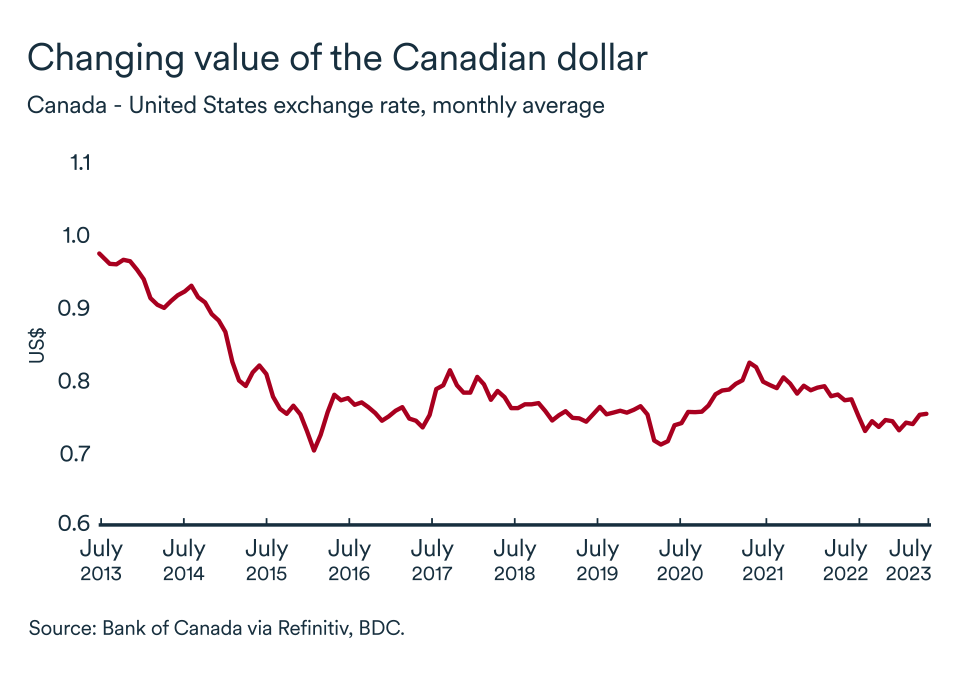

The loonie at US$0.75

The Canadian dollar has appreciated slightly recently, averaging US$0.75 in June and early July. This rebound of the Canadian currency against the U.S. greenback is explained by the interest rate differential between the two nations. While the Bank of Canada raised its rate in June, the Federal Reserve preferred to maintain the status quo that month. The Canadian dollar is likely to remain in this range over the coming weeks, and may even appreciate slightly further after the July rate hike.

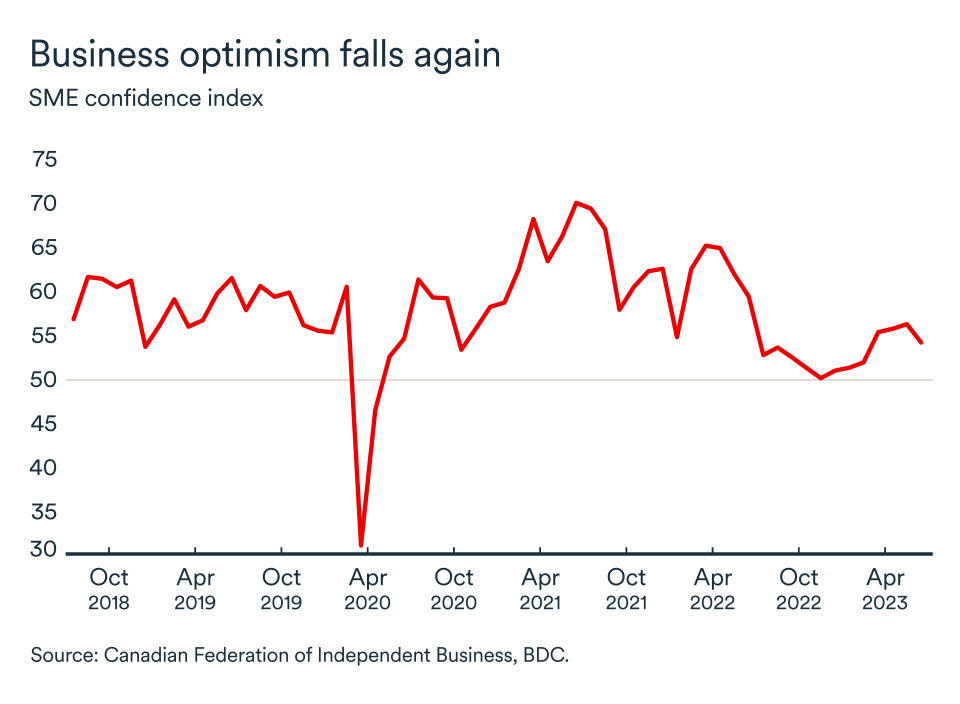

Business confidence falls in June

In June, CFIB's business confidence index for the coming year fell by two points. This is the first monthly decline in the index since November 2022. The index remains above the critical 50 mark, having fallen from 56.2 to 54.1. Businesses remain on edge, and recent rate hike announcement is likely to have rekindled fears of a more pronounced slowdown among many companies. An indicator at 50 means that as many business managers expect the business environment to worsen as to improve over the next 12 months.