Preparing your finances for an economic slowdown

As an entrepreneur, you probably look at the news differently than do most people.

You are probably able to spot business opportunities where others only see headlines. And when something bad is being forecasted, you likely think about how these changes could affect your business.

Whether it’s inflation and rising interest rates, or global events that risk disrupting your supply chain, you need to do more than just react, you need to prepare proactively.

So, let’s look at what you can do to ready your business for an economic slowdown.

Start with the big picture

There are a couple of actions any business owner should take as soon as they feel the economic winds are turning.

Understand how your clients and suppliers are affected

In a time of uncertainty, it’s crucial to take the needs of your clients and partners to heart. This doesn’t have to be complicated; it can be as simple as a phone call to your most important clients. These conversations will help you understand how the market for your goods or services is changing, and how you need to react.

Do your best to answer these questions:

- Are clients changing or reducing their orders?

- Should you be exploring new markets?

- Will your suppliers be affected in a way that might disturb your purchases?

Review your production plan and focus on efficiency

These conversations should lead you to review your production plan to make sure the goods or services you are producing will find a buyer on the market.

The other key thing on the production side is to maximize output while limiting unneeded expenses. Measure your performance to evaluate how you’re doing compared to internal goals or benchmarks, such as industry averages. You can then start improving your results by limiting delays, improving quality and cutting down on other forms of waste.

Focus on financial management

Finally, a key area of focus in a slowing economy should be your finances. Take a full measure of your financials.

So, let’s dive in to see how you can do that.

Get your financial processes up to speed

In a time of economic stress, it’s important to have a clear understanding of how your business is performing at any given time. This shouldn’t be based on a guess or a gut feeling. You need actual data and a process to know how your results fluctuate over time so you can monitor your company’s financial performance and potential issues to address.

Ensure the quality of financial data

Every company has to do bookkeeping—it’s the minimum that’s required to, for example, file your company’s annual corporate tax report or your GST/HST filings. You probably have a bookkeeper or maybe an accountant that’s helping you collect that basic financial information.

A first step is to make sure you are collecting:

- relevant and reliable information

- at the source

- when needed

This financial data will not only be used to prepare your financial statements but also to review your progress to reach your financial objectives.

You should also make sure you are using an accounting system that is properly set up. Your general ledger accounts should be well structured and organized, allowing you to capture the financial data in a way that reflects your operations. The better your accounts will be structured and organized, the more the financial data will be useful to make decisions.

Create a budget and financial projections

The next step from that is to use the data you are collecting to create a forecast.

Putting together a complete annual budget, prepared monthly, is a core component of sound financial management practices.

What do I mean by “complete?” Your budget has to include:

- an income statement

- a cash flow statement

- a balance sheet

And all three statements have to be interconnected.

Unlike financial statements, which look at what has already happened, your projections are forecasts of future income, cash flows and financial position.

They will act as an early warning system, helping you to plan for cash flow dips, potential reductions in investments or operating costs, or additional financing needs.

Most importantly, preparing an initial budget is an opportunity to examine the impacts of potential scenarios on your business, from best to worst, and plan for strategies you could use in such cases.

Especially in a slowing economy, you want to be able to plan and compare against that plan.

Work with your team

When it’s properly done, preparing a budget is a great way to bring the operational and financial side of the business together to set priorities for the year and get everyone working in the right direction.

We often meet with businesses where one person prepares a budget alone in an office with nothing contributed from the other key people in charge of sales or operations in the company. That’s a recipe for failure.

Financial management is like building a house: You need multiple expertise working together, all dependent on one another. You need to get your whole team around the table, from sales and marketing to HR and operations.

Measure your current financial health

To face economic uncertainty, you have to know where you are starting from. This means you need to measure your company’s financial health.

This is typically done using financial ratios, which fall into four different categories:

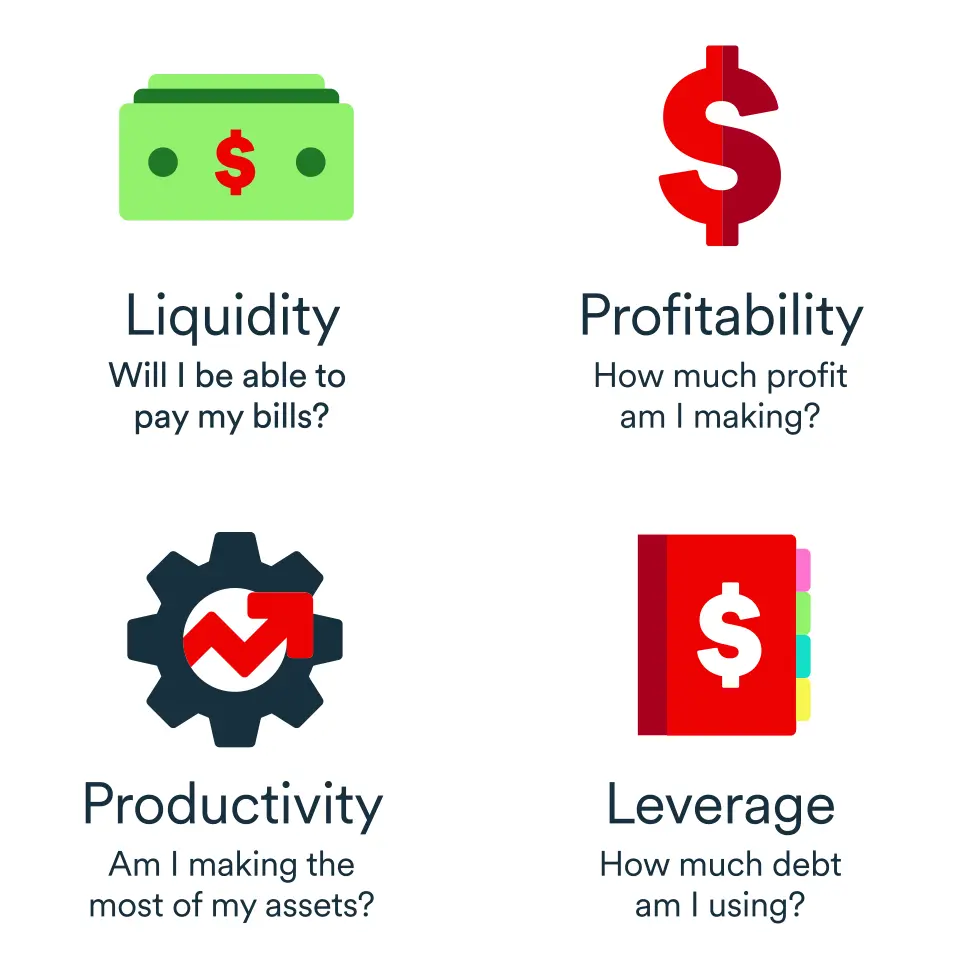

4 types of financial ratios to measure financial health

Liquidity

Is your company able to pay its upcoming bills? Bankers and investors consider this angle when evaluating a company’s short-term viability.

Profitability

How much profit is your business making—or losing? It’s what’s left of your revenue after paying for costs.

Productivity (or efficiency)

How long will you need to convert your production into cash? This period is commonly called the cash conversion cycle. The shorter the conversion cycle, the more your liquidity will improve.

Leverage

How extensively are you using debt in your operations? Profitable doesn’t always mean financially healthy. Your company may be highly leveraged and struggling with short-term cash issues.

Track your performance

So now you’ve prepared your budget and you’ve measured your financial health. The next thing you’ll want to do is compare your actual results with your budget.

Management reports and performance dashboards tools are designed to help you do just that.

They’re prepared under different formats and help you:

- compare actual financial statements with the budget in order to know whether you are on track with your plan

- integrate operating activities and non-financial results with financial information. (The purpose of dashboards is to represent, at a glance, key measures that are essential for the performance of your business.)

- calculate financial ratios to measure and monitor your financial health

When building your dashboard or management reports, choose quality over quantity—use the information that is most relevant for your business so you’re not overwhelmed by data.

Management reports are usually prepared monthly, but some can be prepared daily or weekly (daily or monthly “flash reports”) depending on what they track and how quickly you need the information.

Once you have your management reporting set up and begin to review them regularly, you will have clarity on how your business is performing and what adjustments you can make.

Example of a dashboard

Bringing it all together

Having these tools and processes in place will allow you to react to changes in your business proactively so you can stay ahead of potential issues.

Let’s say one of your customers starts cutting down on their orders, while others are paying you more slowly, which increases your number of days to collect sales. At the same time, you have to pay suppliers more quickly. And to top it off, your inventory is being used at a slower pace.

These negative developments will be tracked using your productivity ratios and they will have an impact on your liquidity ratios. Eventually, you will have less cash on hand to pay your bills, your rent or mortgage as well as wages.

As a result, you may need to take out a loan to finance a working capital shortfall, which will affect your leverage ratios. The increased debt will then impact your profitability because you’re using your operating profits to pay back additional interest costs.

Such a bad-news scenario can be avoided if you track and monitor all your indicators regularly, including some that may seem unimportant, like the time it takes for customers to pay you.

Financial management is an ongoing process

As you meet with your team and see that some objectives are lagging behind, you may need to take action.

Let’s go back to the example where one of your key clients is slowing down their orders.

You’ll evaluate the impacts on your profitability, working capital needs and future cash flows. Then, based on your evaluation, you might need to set new financial objectives that will be supported by a revised budget. This revised budget will then serve as your new benchmark for reporting purposes.

And, once again, the wheel will turn every time a new significant event occurs, positive or negative.

Based on that principle, it’s important that your priorities and objectives be constantly challenged depending on the results achieved and their alignment with your financial plan.

Financial management cycle

What to do if you get in trouble

I’ve given you a few tools to better prepare your company for economic uncertainty. But what should you do if your company is facing severe short-term cash issues?

In this type of situation, the main objective is to preserve your cash for as long as possible.

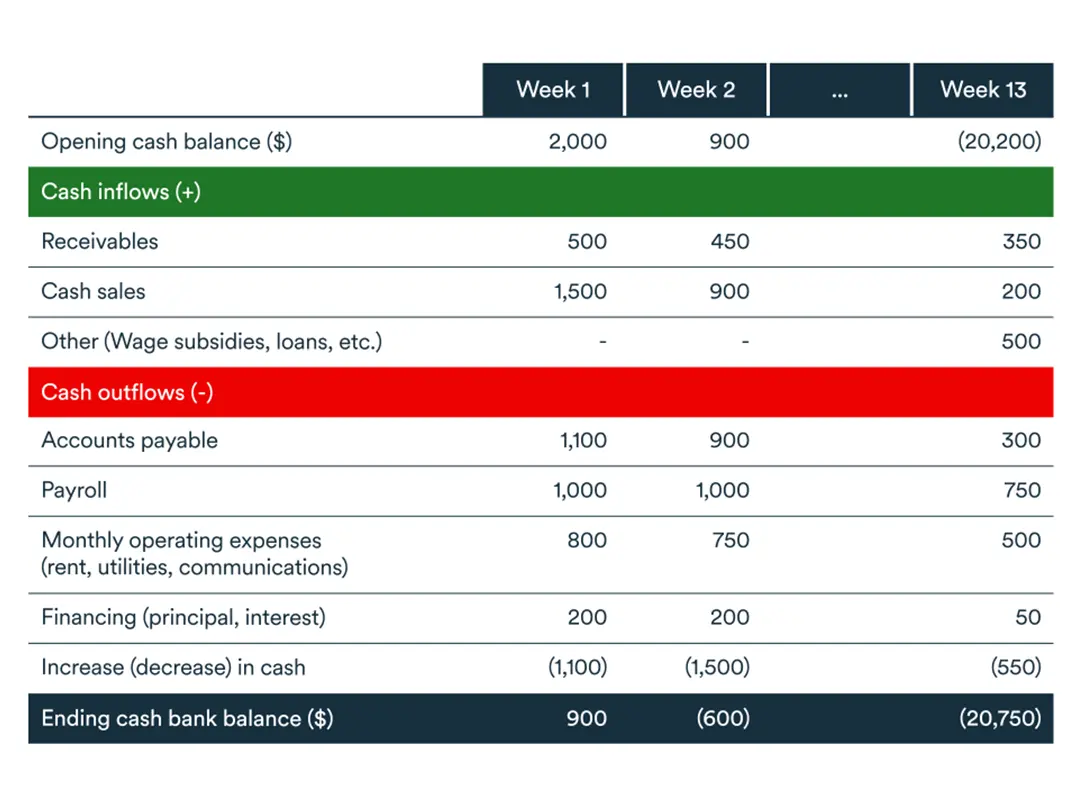

A simple and effective tool for implementing this is a 13-week rolling cash flow forecast. Having a three-month window and updating it at the beginning of every week will provide much tighter visibility on your cash compared to the cash flow that’s part of your monthly budget.

The tool’s two main sections allow you to see:

- how much cash (not sales) to collect in the next 13 weeks from your receivables, including from cash sales or any other type of cash inflow such as new loans, tax refunds, capital injection or subsidies.

- how much cash (not purchases) you’ll need for things that include paying your suppliers, salaries, operating expenses and loans.

You’ll need to prepare both best- and worst-case scenarios.

Know your cash burn rate

You’ll also need to know your cash burn rate. That’s the speed at which you are regularly using up cash. A tool like the 13-week rolling cash flow will help you evaluate how quickly you are spending money and what kind of window, or runway, you have before you run out of cash.

Be prudent with investments

If you are unsure about your financial health, don’t start a major investment project, especially with a coming economic downturn. Use what you need to run your business.

And if you decide to invest, make sure you’ve prepared scenarios showing how you can absorb the cost, even with delays in additional revenue or return on investment.

Stay close to your lenders

If you think you might need a new loan or a larger line of credit to get you through the slowdown, it’s best to contact your lenders as early as possible—they generally don’t like surprises.

Are you ready for a downturn?

How comfortable are you with the quality of your financial data? Are you confident it can help you make the right business decisions in a slowing economy?

If the answer is no, then you need to start making changes right away to make sure you have data you can trust to help weather more difficult economic times.

Next step

Discover how to use financial ratios and set KPIs for your business to track and analyze data and take the guesswork out of business planning. Download the free guide, Monitoring Your Business Performance.