How to manage rising inventory levels in your business

Business inventory levels are rising, according to recent Canadian data. The situation that led to this can be traced back to the pandemic.

During the pandemic, businesses were unable to access everything they needed. As a result, they have been rethinking the way they do business with their suppliers.

While businesses typically try to keep three months of inventory on hand, they have taken to stockpiling so as to not be caught off guard by supply issues. In some cases, we’ve seen businesses accumulating more than a year’s worth of inventory!

To what extent are business inventories increasing?

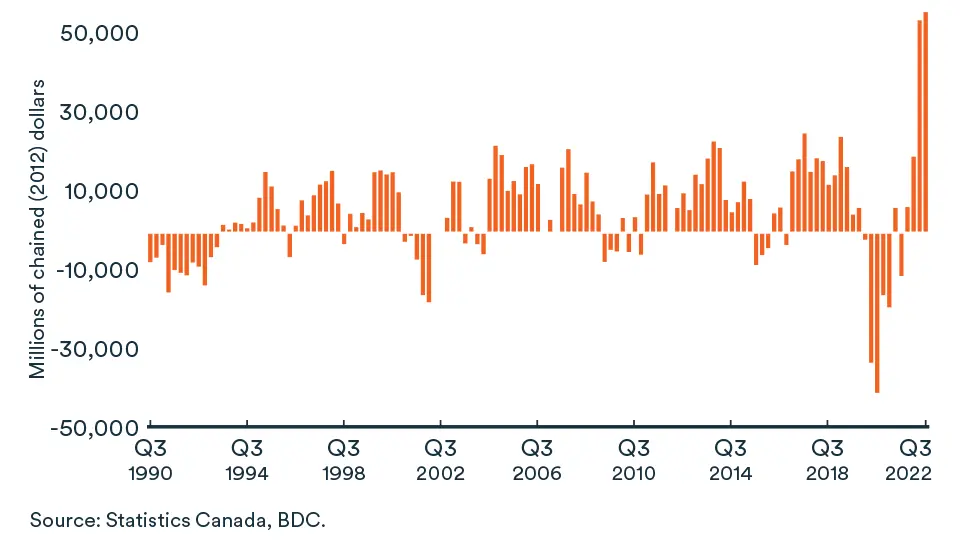

During the second and third quarters of 2022, inventories in Canada began to rise at a rapid pace and reached historic highs—despite certain sectors still experiencing difficulties with supplies.

As illustrated below, inventories are at their highest levels since 1961, the year Canada began collecting this type of data.

Business investment in inventories, Canada, Q3 1990 to Q3 2022, millions of chained (2012) dollars

Source: Statistics Canada, BDC

Why control your inventory during an economic downturn

Normally, businesses reduce how much inventory they buy based on projected sales. But because of recent market uncertainty, they have continued to build up inventory.

The issue is that if during the pandemic you increased your inventory to meet possible supply problems, you were creating an additional risk: the possibility that you might not be able to liquidate your inventory at a reasonable price in the event of an economic downturn.

The risks associated with holding onto lots of inventory can be further exacerbated by labour shortages or other external socio-economic factors.

How rising inventory impacts your business

Carrying lots of inventory can impact a business in several ways. Most importantly, the merchandise is generally not fully paid for because it is financed.

If you end up making fewer sales than expected, holding inventory that’s been financed puts pressure on your short-term credit, which may force you to take out a bigger line of credit. However, in an environment where interest rates are rising, this credit becomes even harder to shoulder.

There is also a limit to how much debt you can take on to finance inventory. While limits vary by industry, banks generally provide 90 days of financing for 50% of the inventory’s value.

If your business is feeling financial pressure from additional inventory, it could find itself compromising on plans for short- and medium-term investment and procurement. Unless, of course, your business has a very low debt ratio, can properly sustain the inventory increase and has the chance to seize a good business opportunity that could have short- and medium-term impacts on results. In addition, you’ll need to ensure that the return on investment will be attractive in spite of higher interest rates.

5 tips for lowering your inventory levels

1. Get the right information

Before taking any action, make sure you know how much inventory you’re holding, how much higher it is than usual, and which items are liquidating slowly. You will then know which goods you can focus on and eventually return to a sustainable level.

2. Find new markets for your inventory

Trying to acquire new customers is always in your best interest. That’s even truer when your warehouse holds a lot of inventory to be liquidated.

You’ll also need to think about your current customers. For example, some businesses are constantly struggling to meet demand. If you inform customers that you have a lot of inventory available, they may see this as an opportunity to increase their production.

3. Consider giving discounts

Having excess inventory means paying more interest to finance it, as well as for storage and handling.

It may be more lucrative to sell your inventory at, say, a 5% discount than to pay interest on a line of credit, plus all the costs associated with storing that inventory—not to mention the risk that the inventory becomes obsolete.

4. Negotiate with your suppliers

During an economic downturn, it’s important to take some time to discuss potential arrangements with your suppliers. You may be able, for example, to delay a payment. Also, sharing your purchasing projections with your suppliers will help them better plan their operations. For all you know, they may be in the same situation as you.

5. Adjust your production

If your inventory levels are already high, make sure you analyze the current needs of your market. Try to avoid overproducing and ending up with more finished product than you can sell.

This means listening to your customers and, when necessary, adjusting your pace.

This is also the time to take a second look at the manufacturing and distribution of products with low profit margins. We sometimes see businesses hold on to unprofitable products to maintain good relationships with certain customers. But if that practice no longer remains viable, it should be further looked at.

Quieter production periods are a good time for training staff, something that busy production periods leave little time for.

You may also want to use that time to give your employees extra time off or special leave for extended absences.

Long-term inventory management

The pandemic and other events in recent years have shown that supply management is a complex function.

Yet, many businesses are very reactionary when it comes to their inventory. They could benefit from a bit more awareness and agility. They need to adopt better planning and keep an eye on the true cost of their purchases, accounting for inventory management.

It’s not wrong to consider hiring people to keep a continuous watch on inventory. These employees will not be able to predict everything; but they will be able to catch certain issues before they become a problem.

For example, procurement specialists can implement strategies and consider alternative purchases in the event of supplier issues.

All businesses need to find ways to be more resilient to the fluctuations caused by external factors. Making supply management a priority will do just that and set you apart from businesses that are choosing to not invest in it.

Learn how to improve your inventory management

Discover how to set key performance targets, ensure you always have the right amount of inventory on hand to meet supply and demand, and improve your company’s cash flow by downloading our free guide for entrepreneurs: Inventory Management.