Working capital

Understanding how much working capital you have on hand to pay bills as they come due is critical to the success of an organization. Focusing only on profit does not necessarily result in a healthy balance sheet.

“A healthy balance sheet will mean that you’re going to have a healthy company,” says Nicolas Fontaine, Senior Business Advisor, BDC Advisory Services. “Not managing your balance sheet, or not managing your working capital, will catch up with you. Not having access to working capital will impact your ability to grow your company.”

How do you calculate working capital?

As a dollar figure, working capital is calculated using the following formula:

Working capital = current assets—current liabilities

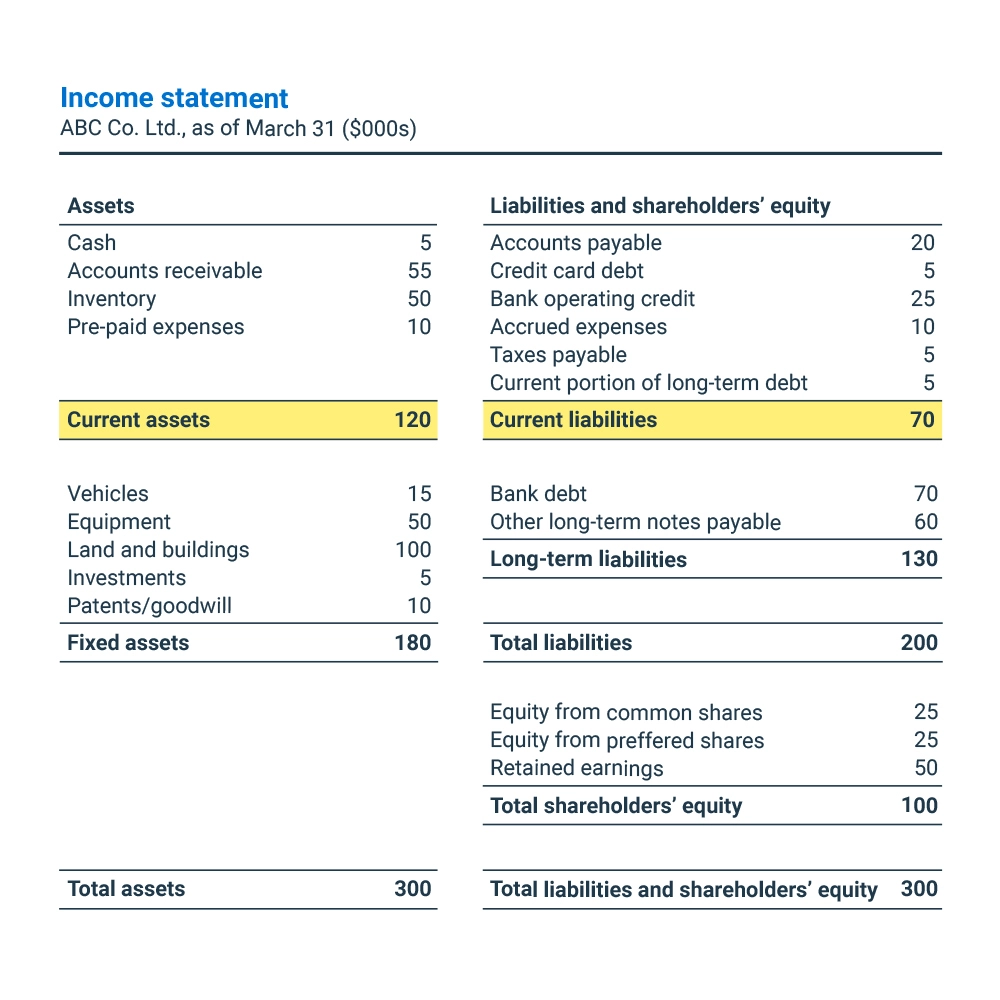

Using figures from the balance sheet below, ABC Co.’s would have:

$120,000 in current assets - $70,000 in current liabilities = $50,000 in working capital

What is the working capital ratio?

Figuring out the right amount of working capital your business needs involves calculating your working capital ratio, also called the current ratio.

The working capital ratio shows how much working capital is available for every dollar of current liabilities.

“Ideally, you want your working capital ratio to be over 1.5, and closer to 2, to give you some room. A higher working capital ratio usually demonstrates a healthier financial position and a better capacity to repay short-term liabilities with short-term assets. Working capital is always about the same principle: how you will service your current liabilities with your current assets,” says Fontaine.

Working capital ratio formula

You can calculate the working capital ratio using the following formula:

Working capital ratio =

current assets

current liabilities

Using our example above, the working capital ratio would be as follows:

Working capital ratio = $120,000 ÷ $70.000 = 1.7 (rounded)

With $1.70 of current assets available for every $1 of current liabilities, ABC Co. has a healthy working capital ratio.

Fontaine urges companies with high inventory to also calculate their working capital ratio excluding inventory in their calculations.

“Inventory is your less liquid current assets compared to cash and accounts receivable. So, if your working capital is 3 to 1, but it’s composed mainly of inventory, I’d be concerned because that means that somehow your inventory may not be turning quickly enough. If it was 3 to 1 but all cash, and quality accounts receivable—that’s what you want,” he says.

It’s important to understand that just having enough to pay the bills is not enough—this is true for new, as well as growing companies.

Nicolas Fontaine

Senior Business Advisor, BDC Advisory Services

Working capital ratio examples

- If Company A has current assets of $150,000 and current liabilities of $120,000, then the company’s working capital is $30,000.

- If, however, Company A has current assets of $120,000 and current liabilities of $150,000, the company’s working capital is –$30,000.

If the working capital ratio is negative, it means the company does not have sufficient liquidity and current assets to service its current liabilities. The more positive the number, the more ability there will be to service those liabilities.

Ideally you want your working capital ratio to be over 1.5, and closer to 2.

Nicolas Fontaine

Senior Business Advisor, BDC Advisory Services

What does the working capital ratio tell you?

The working capital ratio gives you insight on your company’s ability to pay its operating expenses. It also tells you about the general health of the company. A ratio of 1 or lower suggests the company will be challenged to pay its current liabilities.

What is a good working capital ratio?

Companies typically target a working capital ratio of between $1.50 and $1.75 for every $1 of current liabilities. A higher ratio usually demonstrates a healthier financial position and a better capacity to repay short liabilities using short-term assets. “It’s important to understand that just having enough to pay the bills is not enough—this is true for new, as well as growing companies,” says Fontaine.

“Growth is expensive. Growth means that you will need to fund your revenue. In an ideal world, you would sell your goods, get your revenue from those sales and then pay your bills. However, in reality, it’s rare that you are able to access your revenue before you need to pay your bills. Often, small companies think they can manage their business by just using profit and loss, but that doesn’t take into account the need to create cash,” says Fontaine.

Is a high working capital ratio good?

A positive working capital ratio is important for a business to be able to operate effectively. It means that the business has the ability to repay more than the total value of its current liabilities. The higher the working capital ratio, the greater the ability of the company to pay its liabilities.

What is negative working capital?

If your working capital is negative, or very limited, it means you’re not generating enough cash through your operations to pay your current liabilities. In the long run, businesses with negative working capital will struggle to survive.

If your company has negative working capital, it’s important to understand why you’re not generating enough assets to cover your liabilities.

How do you increase your working capital?

The first thing you should do to increase your working capital is look for the root cause of issues within your operations.

- Are your margins too low?

- Are your fixed costs too high for your sales volume?

- Is it a combination of both?

Since working capital is based on your assets and liabilities, improving it involves either increasing your current assets or decreasing your liabilities.

What is a working capital loan?

A working capital loan, also known as a cash flow loan , can be used to increase your working capital when you are looking to finance growth projects, or to help your business tide over cash shortfalls.

Financial institutions usually grant working capital loans based primarily on past and forecasted cash flow. These loans are usually amortized for a relatively short duration, ranging from four to eight years.

A working capital loan may be useful if:

- your business has a history of positive cash flow but now you’re nearing the limit of your credit line

- you’re growing rapidly or developing a new product, but it’ll take time for sales growth to recoup the cost of investments in marketing, new hires or R&D

- you want to take advantage of supplier volume discounts without straining cash flow

- you need to buy inventory to meet a sudden spike in demand

- your top customers are taking a bit longer to pay their invoices

A healthy balance sheet will mean that you’re going to have a healthy company. Not managing your balance sheet or not managing your working capital will catch up with you when you want to grow.

Nicolas Fontaine

Senior Business Advisor, BDC Advisory Services

What is the working capital cycle?

The working capital cycle, also called operating cycle or cash conversion cycle, is the period of time (in days) required for a business to convert net current assets and current liabilities into cash. It measures how much time goes by from the time you pay for goods to the time you receive payment from customers. Having a long operating cycle means your cash will be tied up for a longer time without earning a return. The four key elements of a working capital cycle are

- Cash

- Receivables (money owed to the company by customers)

- Payables (money your company owes to suppliers)

- Inventory

Working capital cycle

In an ideal business, you would want to use your customers’ money to pay your suppliers. The shorter the cycle, the better access you will have to those liquidities.

Nicolas Fontaine

Senior Business Advisor, BDC Advisory Services

How important is the length of the working capital cycle?

The length of the cycle is very important. A long cycle will pressure a company who may not have enough cash on hand to pay bills as they come due.

Companies can reduce the cycle by working to extend payment terms with suppliers and limiting payment terms for their customers. The goal should be to balance the time it takes for the cash to go out of the company with the time it takes for the cash to come in from sales.

“If you give 90-day payment terms to your customers because you want to please them, but your suppliers are requiring payment in 30 days, you have to finance that 60-day gap (because you’re paying for goods before collecting payment from your customers). In an ideal business, you would want to use your customers’ money to pay your suppliers. The shorter the cycle, the better access you will have to those liquidities,” says Fontaine.

What is the most important part of the working capital cycle?

According to Fontaine, inventory management is the most critical part of the cycle. Many companies carry inventory they don’t use to avoid the risk of running out. However, the decision to carry inventory can have a large impact on the bottom line.

“Don’t fall in love with your inventory! I look at it as ice cream, and ice cream eventually melts,” he says. “If you have a lot of inventory that doesn’t turn, you are going to have to decide whether to increase the length of your working capital cycle, or to focus on liquidity by selling inventory at a reduced rate to recoup your cash.”

Current ratio vs. working capital

The current ratio is another name for the working capital ratio. It is a measure of liquidity. It identifies the business’s ability to meet its payment obligations as they come due.

What is the quick ratio?

The quick ratio (or acid test ratio) is a measure that identifies an organization’s ability to meet immediate financial demands by using its most liquid assets. These assets can be cash or items that can be quickly converted into cash, such as temporary investments. Because it excludes inventories and items that cannot be quickly converted into cash, the quick ratio gives a more realistic picture of a company’s ability to repay current obligations.

A quick ratio that’s below 1 can mean your organization is unable to pay current liabilities and will miss out on opportunities that require access to cash. This ratio can be improved by making changes such as:

- Paying off liabilities

- Delaying purchases

- Reducing customers’ payment terms

A higher ratio can offer the opportunity to invest in innovation and other initiatives that drive growth, potentially benefitting the company.

How do you calculate the quick ratio?

The quick ratio is calculated by dividing your company’s quick, or liquid, assets by its current liabilities.

Quick ratio formula

Quick ratio =

Quick assets (cash + stock investments + accounts receivables)

current liabilities

or

Quick ratio =

Quick assets (current assets – inventory – prepaid expenses)

current liabilities

“It’s really an acid test for the quality of your working capital. It helps you ask questions like: ‘Do I have immediate access to those current assets? Is it liquid working capital or is it more passive, and is it mostly inventory?’ The quick ratio really offers a deeper view into the working capital ratio and tells you how healthy it is,” says Fontaine.

How many types of working capital are there?

There are several types of working capital, which are used for different purposes.

1. Permanent working capital

Permanent working capital is the capital required to make liability payments before the company is able to convert assets or client invoice payments into cash. It is the minimum capital required to enable the company to function smoothly.

2. Temporary working capital

Temporary working capital is capital that is required by the business during some specific times of the year or for some specific initiative. This requirement is considered temporary and changes with the business’ operations and market situations. It may also mean the company will require short-term loans, which will be repaid once the initiative begins to generate cash.

3. Gross and net working capital

Gross working capital represents the company’s entire current assets. These are assets that can be converted into cash within one year. It typically includes:

- Cash

- Accounts receivable

- Marketable securities (such as stocks)

- Short-term investments

Net working capital is the difference between gross working capital and current liabilities.

4. Negative working capital

Negative working capital can lead to a potential shortfall of cash. It results from your current liabilities exceeding your current assets, and means your company has greater short-term debts than short-term assets.

5. Reserve working capital

Reserve working capital is used for unexpected situations such as fluctuating markets. The reserve working capital refers to the short-term financial arrangement made by the business to take on any big change or deal with uncertainty.

6. Regular working capital

Regular working capital is the minimum amount of capital required by a business to carry out its day-to-day operations.

7. Seasonal working capital

Seasonal working capital is the amount of money a business needs during its peak season. Businesses with seasonal demands require additional working capital, usually on a temporary basis when customer demand is high. This becomes no longer necessary once cash has been collected through sales.

8. Special working capital

Special working capital is required for a special occasion such as once-yearly concerts, unexpected events and advertising campaigns. It is held by a company to pay for the special programs’ expenses.

Discover easy steps to manage your cash flow

Learn how forecasting sales and inventory and shortening customer payment terms can improve your cash conversion cycle. Download Taking Control of Your Cash Flow, our free guide for entrepreneurs.