Shareholders' equity

What is shareholders’ equity?

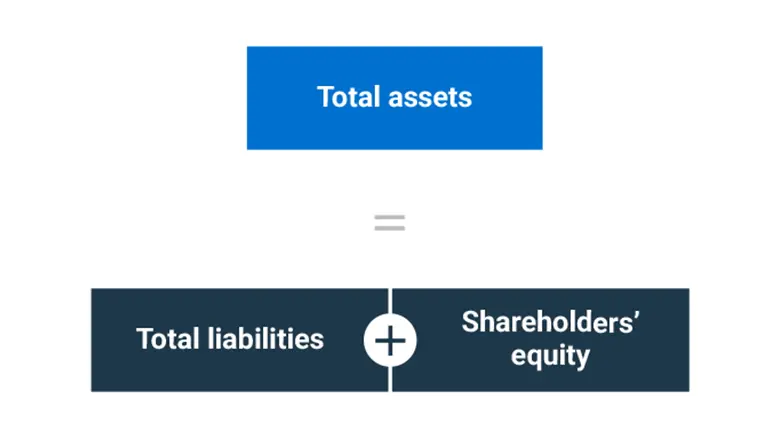

Shareholders’ equity is the value of the company’s obligation to shareholders. It appears on a company’s balance sheet, along with assets and liabilities.

What is the difference between equity and shareholders’ equity? There is no difference; they’re the same thing.

Also, shareholders’ equity is not the same thing as the company’s assets. Assets are what the business owns; they always equal liabilities plus shareholders’ equity on a balance sheet.

The four categories of Shareholders' equity

Shareholders’ equity is broken down into four categories:

- common shares

- preferred shares

- paid-in capital

- retained earnings

Shareholders’ equity formulas

There are two different formulas to use when calculating your shareholders’ equity.

Formula

Example of shareholders’ equity on a financial statement

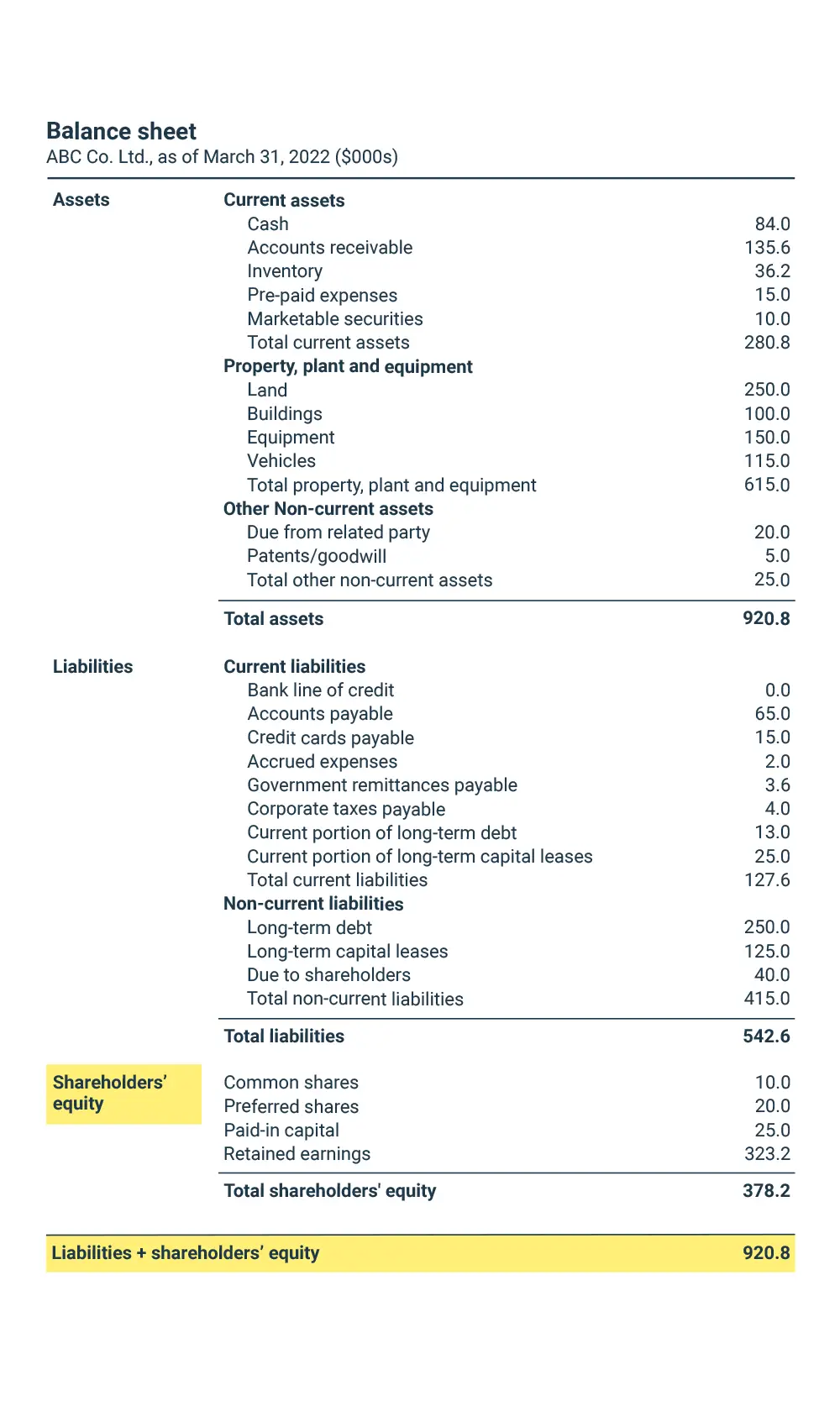

On the balance sheet below, shareholders’ equity has its own section, broken down into its four categories. When added to liabilities, the total equals the value of the company’s assets.

How shareholders’ equity helps fill out a company’s financial picture

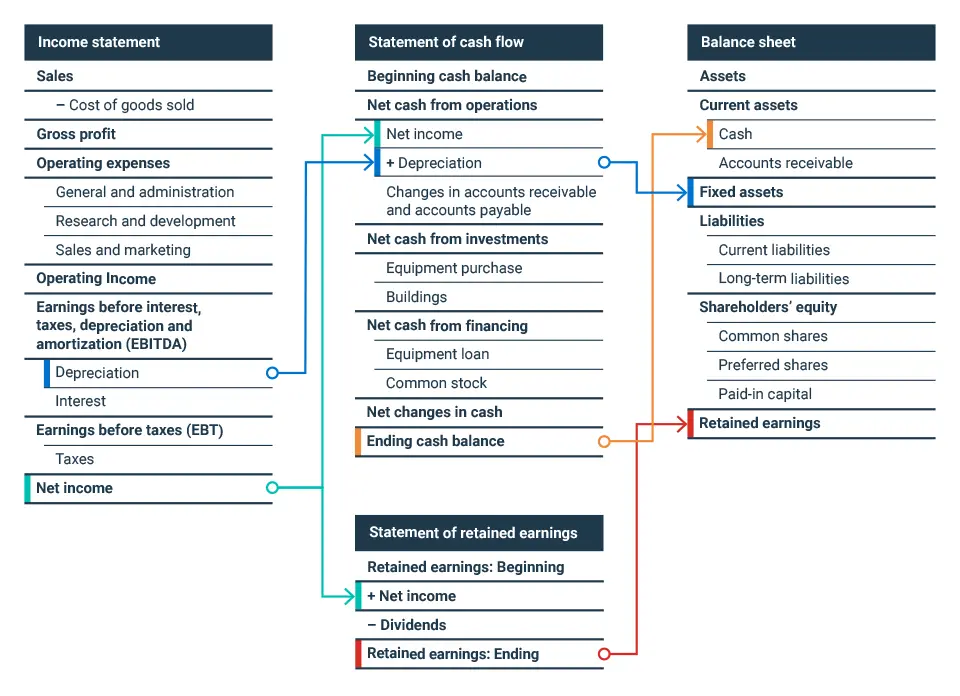

The illustration below shows how shareholders’ equity connects to the other components of a company’s finances.

For example, let’s say you generate a positive after-tax net income one year. That’s first recorded in the income statement as net income. The net income is represented in both the statement of cash flow and the statement of retained earnings. After subtracting dividends, retained earnings for the current year are stated in the final line of the statement of retained earnings and reflected in the balance sheet under shareholders’ equity.

What are the components of shareholders’ equity?

Shareholders’ equity is:

- Share capital—Which consists of common and preferred shares and paid-in capital. Paid-in capital (sometimes called contributed capital) is the amount that the company has received from owners for common shares that is in excess of the shares’ par or stated value.

- Retained earnings—Which consist of cumulative earnings from previous years plus the current year’s after-tax net income, minus dividends.

What can shareholders’ equity tell you?

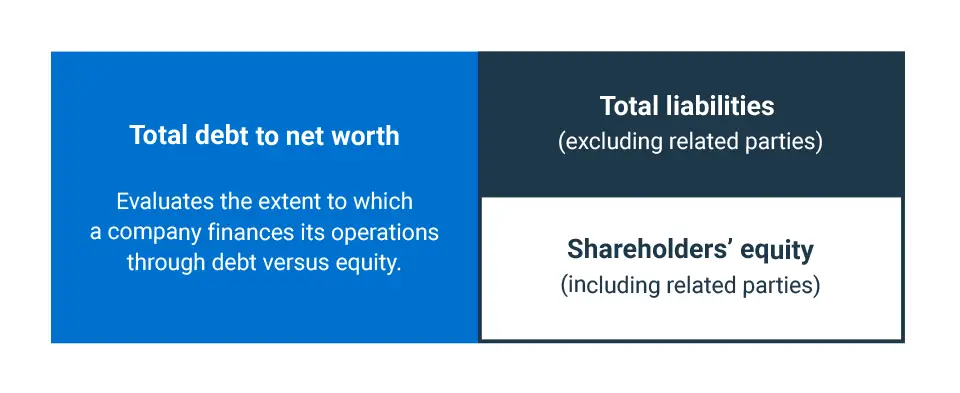

Shareholders’ equity is one of the first things bankers and other analysts look at when evaluating a company’s financial health and stability. They compare equity to liabilities to understand the company’s degree of leverage and its ability to take on more debt.

Comparing total liabilities to shareholders' equity shows the extent to which a company finances its operations through debt versus equity.

“A banker wants to know how much debt you have vis-à-vis your equity,” Sood says. “When someone asks me to review a company’s financials, I say, ‘Show me the balance sheet first.’ I look at that and can tell right away whether they’re in trouble.”

The relationship between equity, assets and liabilities also reveals:

- the company’s cumulative financial progress

- how much owners have reinvested in the business

- the owners’ long-term commitment to the company

“It tells me the owners’ attitude toward their business and how much debt they’re willing to take on,” Sood says. “Many entrepreneurs never look at their balance sheet. That’s a mistake because it’s a key component of measuring financial health. Just looking at a profit-loss statement isn’t enough. You have to look at all your financial statements together.”

It’s an opportunity for education and to find strategies to clean up the financial statements.

Alka Sood

Senior Business Advisor, BDC Advisory Services

A red flag that all might not be well is when the money with which the owners are financing the business is categorized as a loan rather than shareholders’ equity. “That tells me they may have a very short-term view,” Sood says. “They could pull that money out at any time and may not be in it for the long haul.”

Bankers also compare a company’s retained earnings to its fixed assets. “I always find it fascinating to look at retained earnings versus fixed assets,” Sood says. “It tells me how much the company is reinvesting in the business or if it’s just letting cash pile up.”

The numbers could also reveal poor accounting practices, which can in turn adversely affect how bankers and other outside analysts perceive a company’s finances. For example, owners may not be paying themselves an appropriate salary or dividends, which can skew financial results.

“It’s an opportunity for education and to find strategies to clean up the financial statements and improve your company’ financial health,” Sood says.

What does negative shareholders’ equity mean?

Negative shareholders’ equity can occur for several reasons or a combination of reasons:

- Long-term losses: The company has incurred a cumulative loss since its inception.

- Excess dividends: Owners have drawn dividends that exceeded the company’s cumulative gain.

- Share repurchase: The company or a shareholder has bought shares from other shareholders. The money for the share buyback may have come from the company’s cash and retained earnings, which would reduce assets and shareholders’ equity.

Negative shareholders’ equity is a warning sign that something may have gone awry with the company’s financial health. “If it’s negative, it’s important to figure out why and take corrective actions,” Sood says. “It could be a sign of excess dividends or a flawed business model.”

For example, a closer look may reveal that retained earnings are negative and have been in the red for several years. “Bankers like to see at least two years in a row of positive retained earnings,” Sood says. “If they don’t see that, it means you haven’t made money for a couple of years or you’ve been pulling it out of the company. It’s an absolutely crucial part of the shareholder account.”

Is shareholders’ equity an asset?

No, shareholders’ equity is an obligation to a company’s shareholders. Assets are what the business owns. Remember the formula: Assets equal liabilities plus shareholders’ equity.

What is the relation between shareholders’ equity dividends?

Dividends are included in the calculation of shareholders’ equity. They are subtracted from cumulative retained earnings and current-year net income to arrive at the retained earnings for the current year.

“Dividends are a withdrawal of money from the business,” Sood says.

What is the relation between shareholders’ equity and book value?

Book value is the recorded value of a company’s assets, whereas shareholders’ equity is the value of the assets minus liabilities.

What is the relation between shareholders’ equity and net worth?

Shareholders’ equity is sometimes also called net worth. But it’s important to recognize that net worth in this sense is an accounting measure and not the company’s valuation or what it could fetch if sold.

A company’s balance sheet reflects past business activity, whereas its valuation is typically based on what the company could earn in the future and a market-based multiple.

“Many entrepreneurs mistakenly think shareholders’ equity is what their company is worth on the market, but it’s not,” Sood says. “There’s a lot of confusion about this.”

Even a sale of the company’s assets may not yield the same amount as the balance sheet net worth after debt is paid. Asset proceeds can vary widely depending on sale conditions and how accurately asset values are represented on the balance sheet.

How do you evaluate shareholders’ equity?

You can evaluate shareholders’ equity by comparing it to liabilities. The ratio between the two is a key indicator of a company’s financial health. “Bankers like to see that liabilities are, at most, two or three times the value of shareholders’ equity,” Sood says. “That shows financial stability and that you’re not overly leveraged. If it’s over three, you want to take a closer took at what’s going on with the company.”

Next step

Download our free guide for entrepreneurs, Understand Your Financial Statements, for more financial management tips and advice to better manager your company.