Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreShould we worry about the One Big Beautiful Bill?

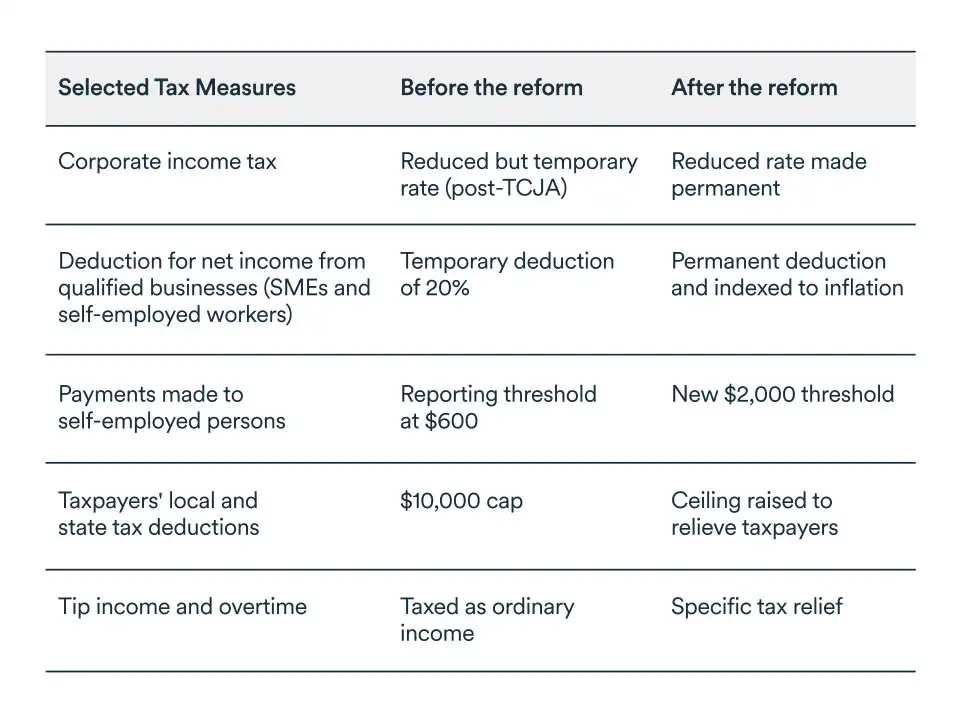

Economic uncertainty remains high in Canada and around the world as shifting U.S. tariff policy disrupts trading relationships. However, one element of the U.S. economic agenda was recently clarified. The One Big Beautiful Bill was signed into law by President Trump on July 4. What does the new law, with its sweeping tax changes, mean for your company? What does it mean for the Canadian economy?

What’s in the law?

The new law includes hundreds of tax changes that will be felt well beyond U.S. borders. This is particularly true for Canada because of the close economic and fiscal ties with its neighbours to the south.

However, most of the measures will have little direct impact on Canadian businesses. Several are a continuation of a tax reform enacted by the first Trump administration. This is notably the case for a reduction of the federal corporate income tax rate from 35% to 21% that came into effect on January 1, 2018. It had been due to expire at the end of this year but was extended in the new law.

Higher growth for Canada?

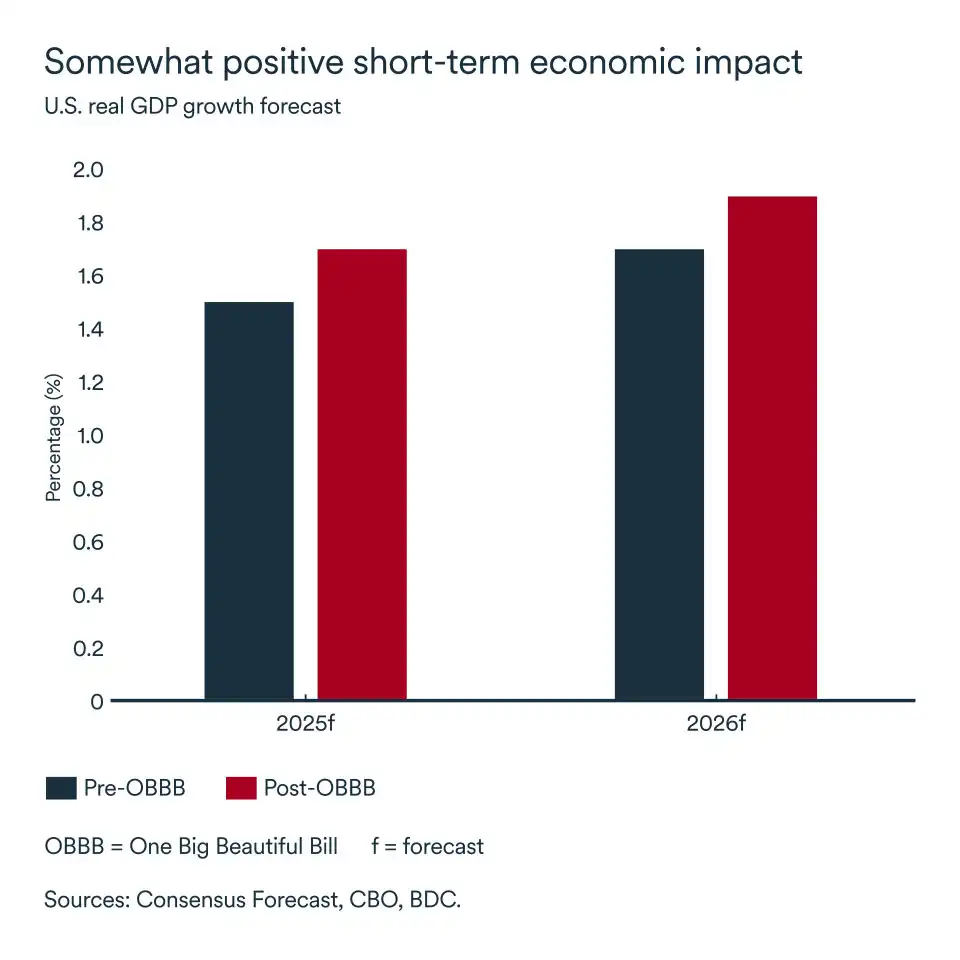

Tax cuts contained in the law should improve U.S. economic growth in the short term, but they will also create downside risks in the longer term.

Before passage of the bill, economists expected the U.S. to grow by 1.5% in 2025 and 1.7% in 2026. Tax cuts are likely to stimulate U.S. demand, boosting consumption and investment in the short term. This could add an extra 0.2% to real GDP growth per year.

Normally, stronger U.S. growth would stimulate Canadian exports. However, trade tensions between the two countries throw this equation into doubt.

In the longer term, the high and growing U.S. national debt could mean higher interest rates for consumers.

And many of the new tax breaks for individuals are scheduled to expire as early as 2028.

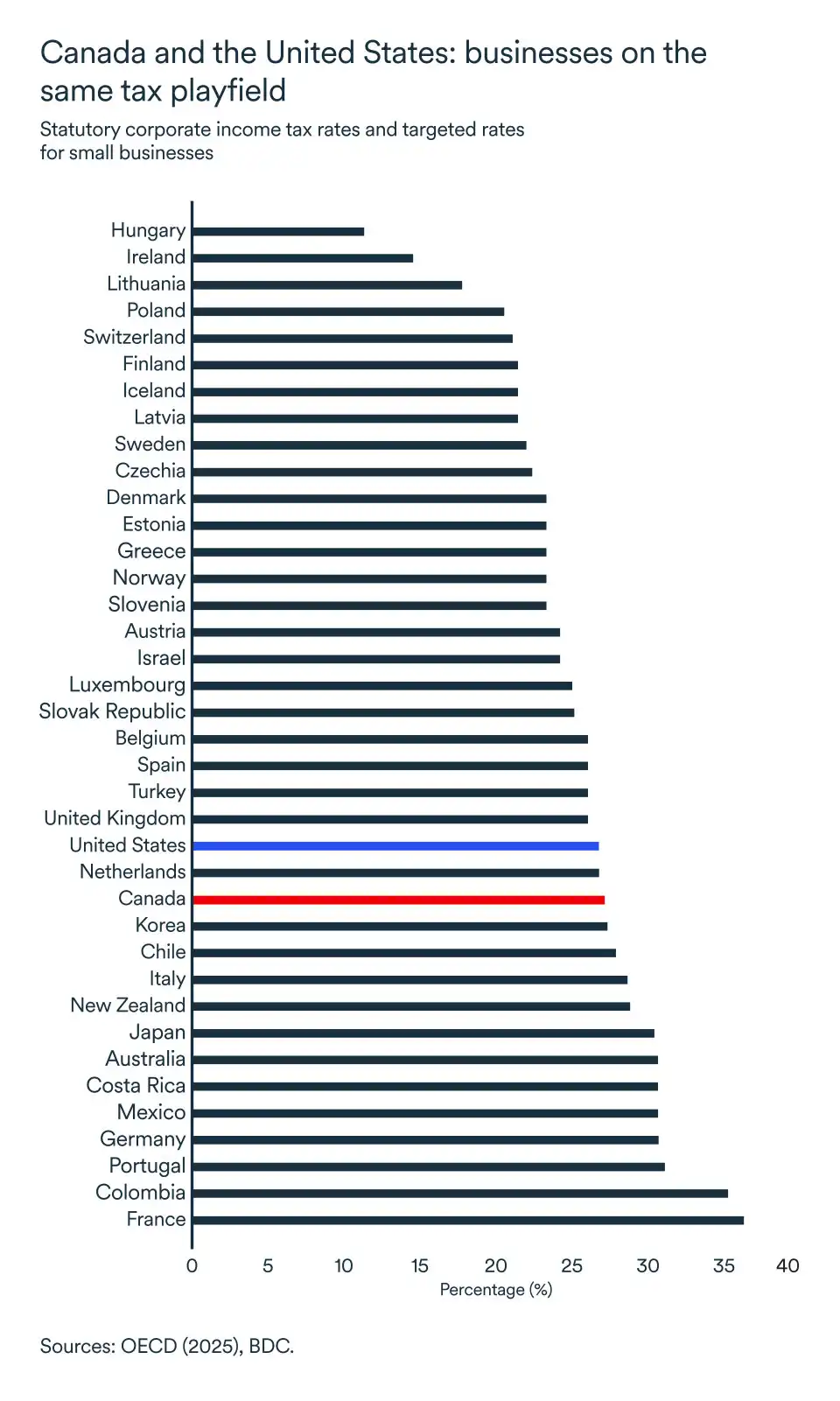

Canada-U.S. corporate tax gap disappears

By contrast, corporate tax cuts and investment incentives in the law are permanent. According to the OECD, before the adoption of the 2018 U.S. tax reform, the corporate tax rate (including national and sub-national governments) was 38.9% in the U.S. compared with 26.7% in Canada. Today, the U.S. rate has fallen to 25.6%.

The elimination of Canada's corporate tax advantage has led some observers to fear the country will lose investment to the U.S.

However, Canada remains an attractive investment location for many companies. A rich pool of well-trained workers, public services and stability just some of the advantages companies consider when planning investments.

What's more, uncertainty has reached an unprecedented level in the United States. Investors prefer stability to volatility. Research has shown a positive correlation between open trade relationships and political stability, on one hand, and foreign direct investment, on the other.

Law could benefit some Canadian sectors

The new U.S. law could prove a boon for certain sectors in which Canada has the potential to enhance its strategic position on the world stage.

One important example is the defence sector. Military spending is set to rise in Canada, but the build-up here will be dwarfed by the one in the U.S. where the new legislation aims to deploy an additional $150 billion for defence. Canadian defence contractors should benefit from higher spending on both sides of the border and around the world.

Elsewhere, the new law is expected to reduce U.S. renewable energy production and research—a sector where Canada could step in to carve out a global niche. However, the abolition of tax credits for the purchase of electric vehicles, along with the recent decline in interest in this type of vehicle, will clearly be detrimental to the clean energy sector.

What does this mean for entrepreneurs?

- We can expect U.S. growth to remain solid, at least over the next few quarters. Beyond boosting growth south of the border in the short term, Canadian entrepreneurs need not be overly concerned about the tax changes contained in the new law.

- The Federal Reserve should resume its easing cycle towards the end of the year, probably cutting interest rates by 25 basis points in Q4. The Bank of Canada, meanwhile, is likely to keep its rate steady in the coming months. This will narrow the interest rate differential, giving support to the Canadian dollar.

- Even if the loonie rises, it remains at a level favourable to exports, and with strong U.S. growth, Canadian exporters can take advantage of an expanding market thanks to the competitive edge offered by a weaker currency.

Canadian economy learns to cope with U.S. tariffs

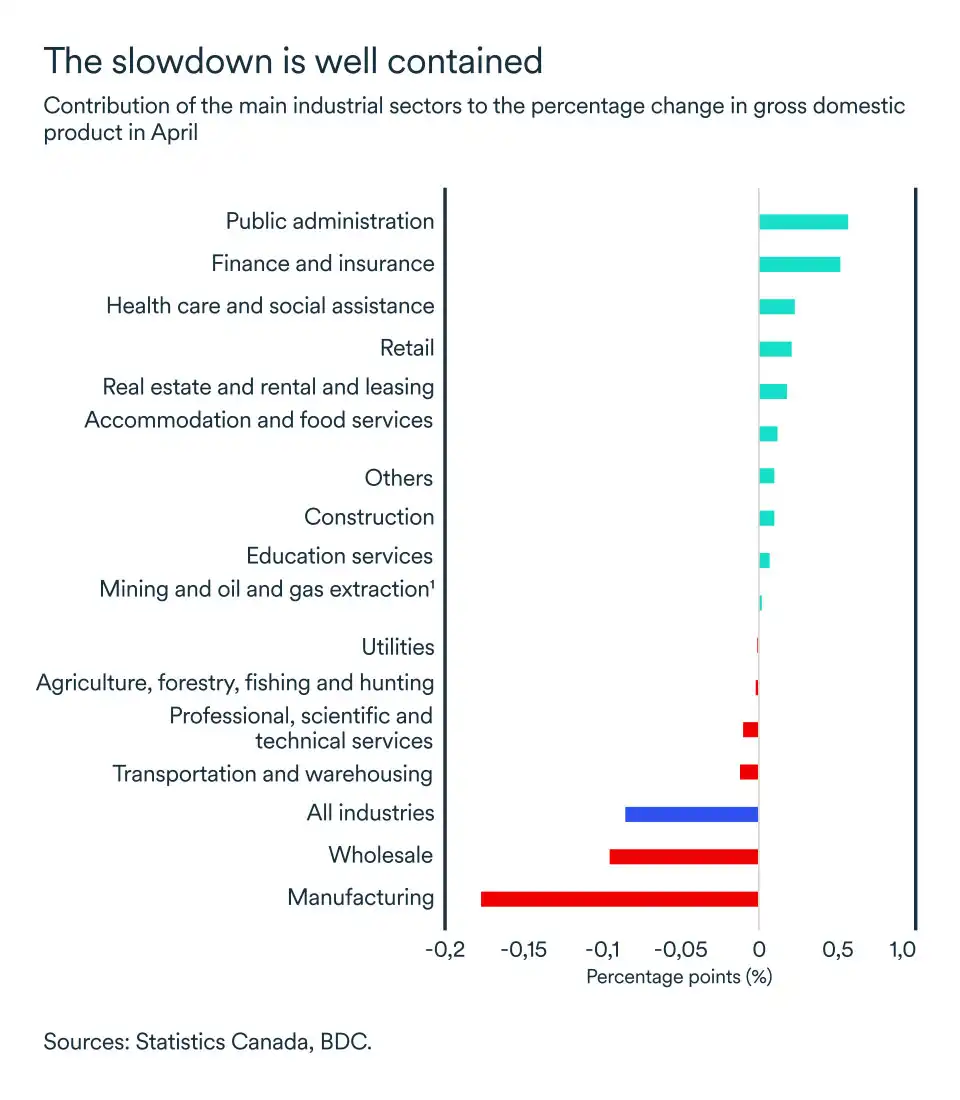

Despite ongoing trade tensions with the U.S., the Canadian economy has held up fairly well this year, but industries on the front lines showed clear signs of slowing down in the second quarter.

Unsurprisingly, Canadian GDP fell in April. The monthly drop of 0.1% compared with March brought annual growth for 2025 to 1.8% compared with the same period last year.

In April, goods-producing industries saw activity decline by 0.6%, reflecting a slowdown in manufacturing (-1.9%). Wholesale trade also recorded a significant drop of -1.9%, but other service industries saw growth that more than offset the losses. Services continued to grow in April.

While services dominate domestic economic activity, they account for a relatively small share of Canada's exports. As a result, it’s the goods-producing industries that have borne the brunt of the recent turbulence in international trade.

However, domestic economic data suggest that the negative effects have so far remained contained to the most vulnerable sectors. Still, we don’t expect a significant economic rebound in the months ahead because uncertainty remains too great.

Preliminary indicators suggest a further 0.1% decline in May, according to Statistics Canada.

U.S. keeps up the pressure

The U.S. Administration has threatened to impose 35% tariffs on Canadian products not complying with the CUSMA free-trade agreement on August 1, and copper is the latest material to be slapped with worldwide duties.

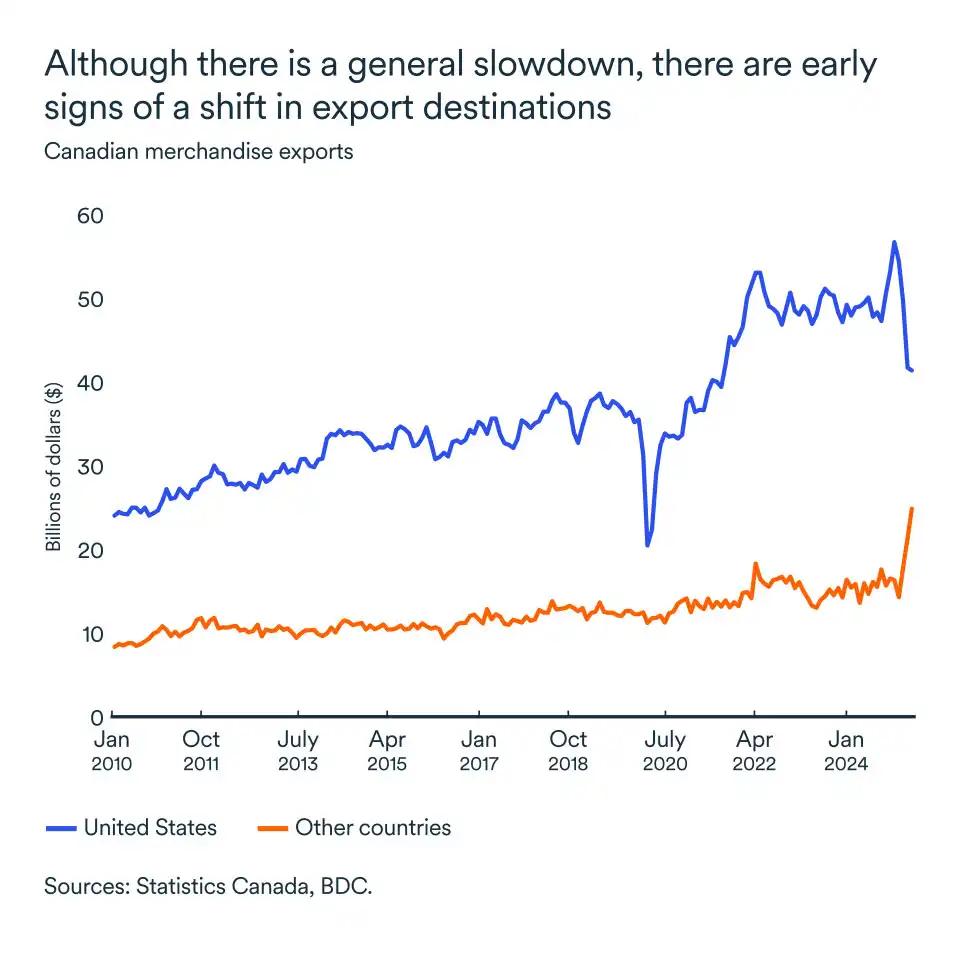

Tensions between Canada and the U.S. appears to be creating change in Canada’s trading relationships.

On one hand, goods exports have taken a hit. While they rose by 1.1% in May, this was far from enough to compensate for April's 11.0% decline. On the other hand, there were signs that Canadian trade is diversifying. While exports to the U.S. slowed since the start of the second quarter, sales to other countries picked up sufficiently in May (+16.6%) to counteract the U.S. decline.

Meanwhile, Canadians are curtailing their purchases of foreign goods. Imports are down, particularly from the United States. In a BDC survey conducted in April, half of consumers said they intended to reduce their spending on American products, and 58% said they intended to purchase more local products.

If recent declines in imports reflect these sentiments, they could prove beneficial for the country's economy. This would be particularly true if purchases that would have otherwise gone to U.S. suppliers are being redirected to Canadian companies, rather than simply being cancelled.

Even so, merchandise exports are expected to hold back GDP performance in the second quarter, as the slowdown in exports has been greater than that in imports.

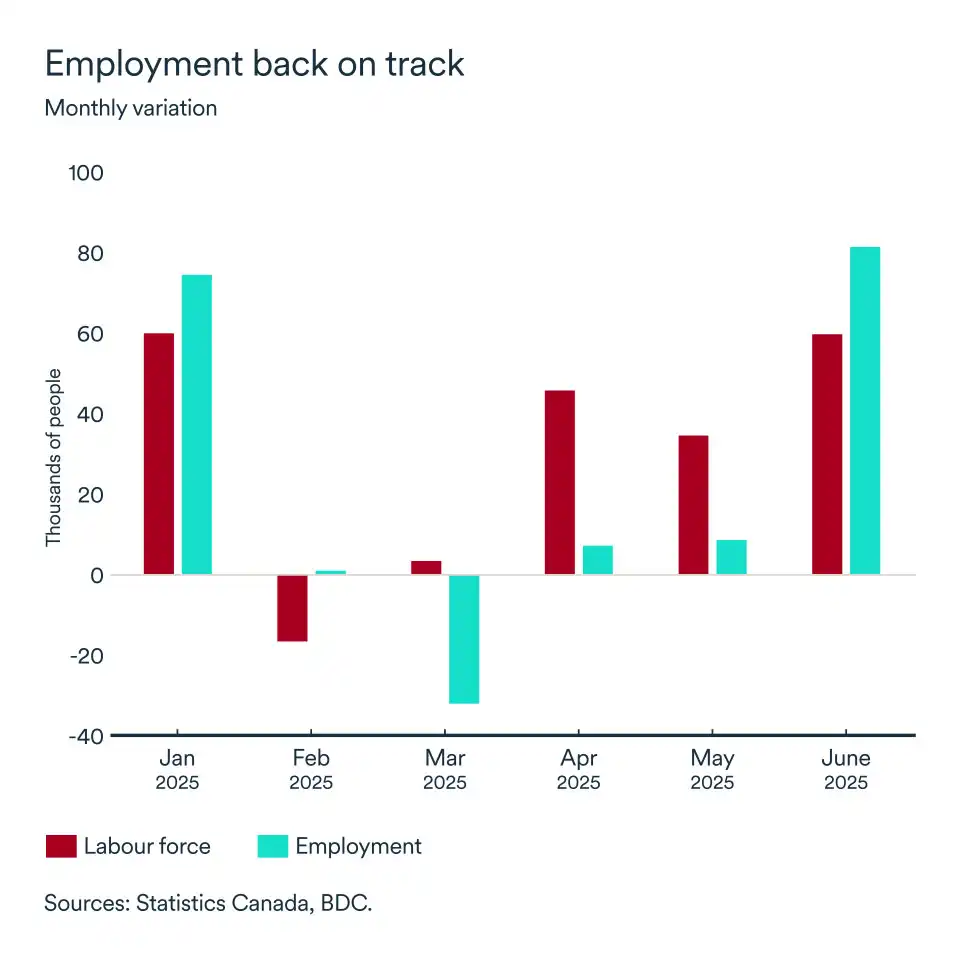

The labour market returns to growth

After holding steady in April and May, employment ended the second quarter on a strong note. In June, 83,000 new jobs were added to the economy, bringing the unemployment rate down to 6.9%. Most of these jobs, however, were part-time.

In June, job gains were more concentrated in retail and wholesale trade (+33,600), but even manufacturing (+10,500) recovered some of the jobs lost since the start of the year.

The upturn in employment is another sign that the Canadian economy is increasingly learning to cope with uncertainty. This should lead to higher consumer spending in the months ahead, helping to support GDP growth.

In another positive sign for the economy, inflation remains under control with tariffs seeming to have had a limited effect on prices so far. The Bank of Canada will most likely maintain its key rate at the current level of 2.75% in July. Recall that, at this level, Canada's monetary policy is in the neutral zone, i.e. neither stimulating nor unduly restricting the economy.

The impact on your business

- Be prepared for possible increases in the cost of materials over the summer, particularly for copper, due to new 50% U.S. tariffs. Find out if and how this could affect your business.

- Canada's renewed effort to diversify its export markets seems to be off to a good start. The country looks to be increasing trade with countries other than the U.S. At the same time, the craze for buying Canadian and local products continues. Make sure your company has a strategy to capitalize on these trends.

- The likelihood that the Bank of Canada will hold its key rate steady at 2.75% offers monetary stability for businesses. The rate cuts over the past year (-225 basis points) combined with reduced economic volatility could lead to lower effective interest rates for businesses and households. This, combined with the upturn in employment in June, could revive demand for goods and services even further.

Quebec’s economy shows resilience despite trade headwinds

Among Canada’s provinces, Quebec has been the second hardest hit by U.S. tariffs, after Ontario. Steel and aluminium are among Quebec’s top exports and 50% tariffs imposed on those industries have not only taken a toll on producers, but also on businesses and regions that benefit from them.

However, Quebec has a diverse economy, producing and exporting many other goods that are exempt from tariffs, reducing the impact of trade tensions on the province. Overall, we expect Quebec to show resilience this year, but see economic growth that’s below potential at 1.0 %.

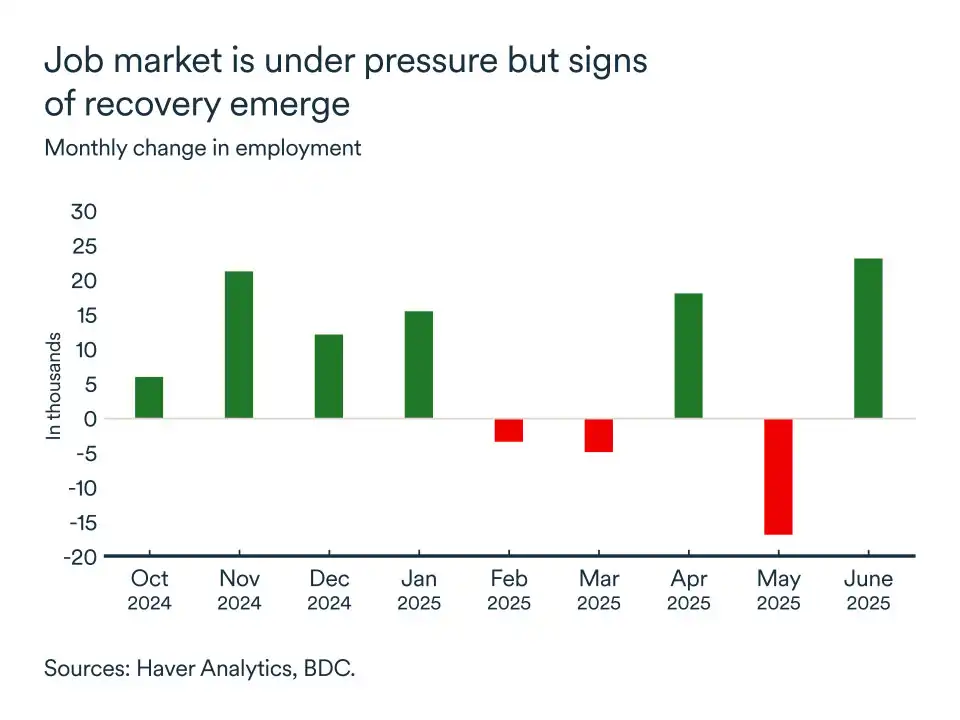

Job losses in targeted industries are offset by gains elsewhere

Sectors directly affected by tariffs have experienced job losses since the start of the year, weighing on employment growth. Some 49,000 jobs were lost from January to May in the construction and manufacturing sectors. However, most of these losses were offset by gains in service industries. And June data showed signs of recovery, with goods-producing sectors adding 6,000 net new jobs, including in construction and manufacturing.

At the same time, service sectors continued to add jobs at a strong pace, confirming the limited impact of U.S. tariffs on Quebec’s job market so far. However, as long as trade talks between Canada and the U.S. fail to produce a deal, the job market is likely to remain under pressure in the affected industries.

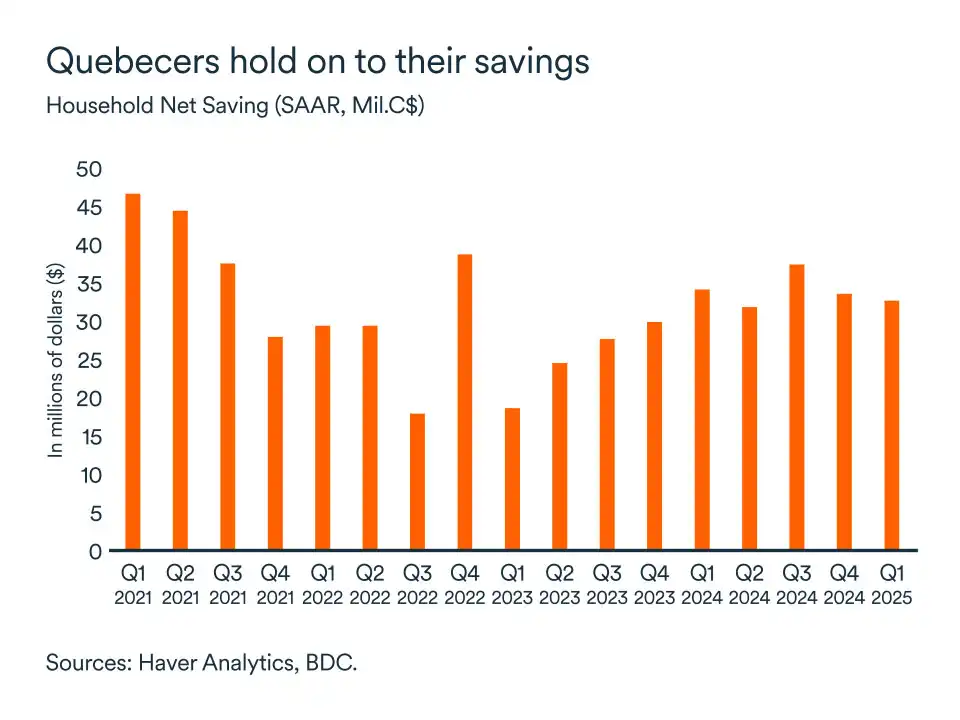

Faced with heightened uncertainty, Quebecers kept a tight grip on their savings in the first quarter.

Quebecers in turn are holding on to their savings. They reduced their spending in Q1, but early indicators show regained confidence and a recovery in consumer spending since then. In fact, households are well positioned to benefit from better conditions in the future thanks to their low indebtedness and high savings levels.

However, there were early indications of a rebound in consumer confidence and spending in the second quarter. Households are well-positioned to benefit from better conditions in future months, thanks to their low indebtedness and high savings levels.

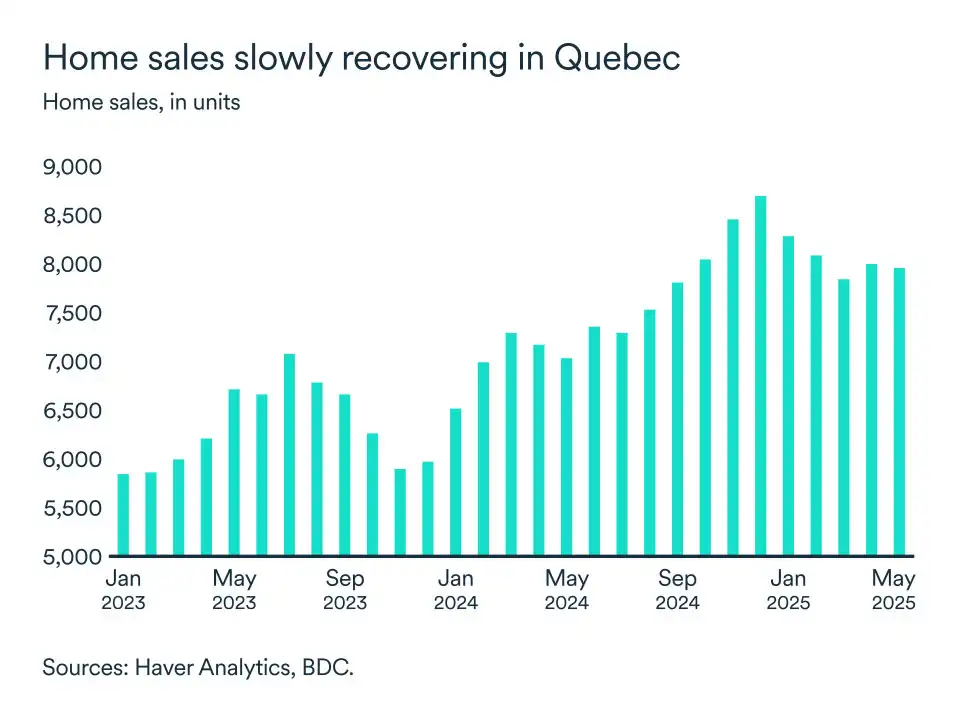

Housing market stabilizes

housing market lost momentum earlier this year as trade tensions escalated. Home sales declined by 4% in the first quarter, but the market bounced back and stabilized in April and May.

We expect lower interest rates to encourage new home buyers to enter the market as trade tensions ease and consumer confidence increases, leading to a slow recovery in the Quebec housing market.

A bumpy ride expected in the quarters ahead

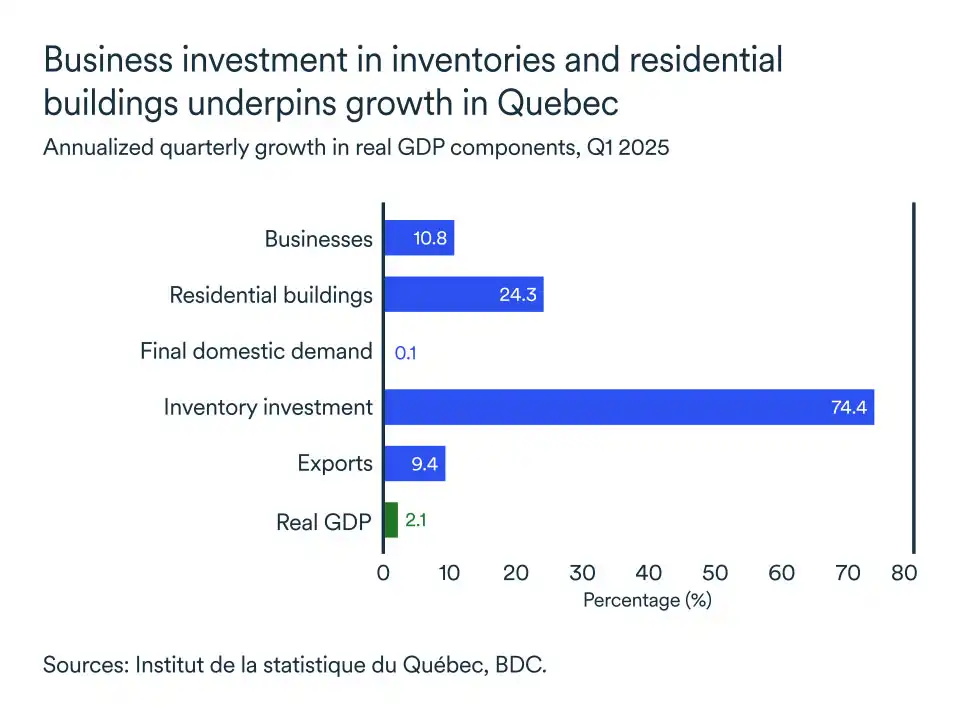

Economic growth in the first quarter was supported by robust business activity and strong exports. Real GDP increased by 2.1%.

The expansion was primarily driven by substantial business investment, particularly in residential construction. As well, there was a notable rise in exports, resulting from U.S. businesses accelerating orders ahead of impending tariffs. However, exports fell sharply in April, followed by another lacklustre month of May, fuelling expectations of more setbacks ahead.

The good news is that housing starts and building permit data remained solid in April and May, indicating continued strength in residential investment in the coming quarters. Additionally, electricity production has slowly recovered since the start of the year and is set to contribute to growth. Infrastructure spending and targeted fiscal measures aimed at sectors affected by tariffs will play a key role in offsetting the shock of trade disruption.

While we still expect Quebec’s economy to grow this year, albeit at a modest rate, progress is likely to be uneven in the coming months.

The impact on your business

- Depending on your industry, tariffs can have a significant impact on your business. BDC offers free tools to help you weather the storm.

- Credit conditions are tighter than in previous quarters. It’s important to assess your financial situation and to carefully prepare your financing request.