Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreWhat would a new Trump mandate mean for Canada’s economy?

The next U.S. election is still four months away, but in the wake of the first presidential debate, many Canadian entrepreneurs are wondering what impact a new Trump administration would have on our economy. Unsurprisingly, their main concern is the toll heightened trade tensions could have on Canada.

While Biden’s administration hasn’t shied away from protectionism, notably through the Inflation Reduction Act, a second Trump presidency is expected to have a much greater impact on U.S./Canada trade relations.

Canadian economy vulnerable to rising protectionism

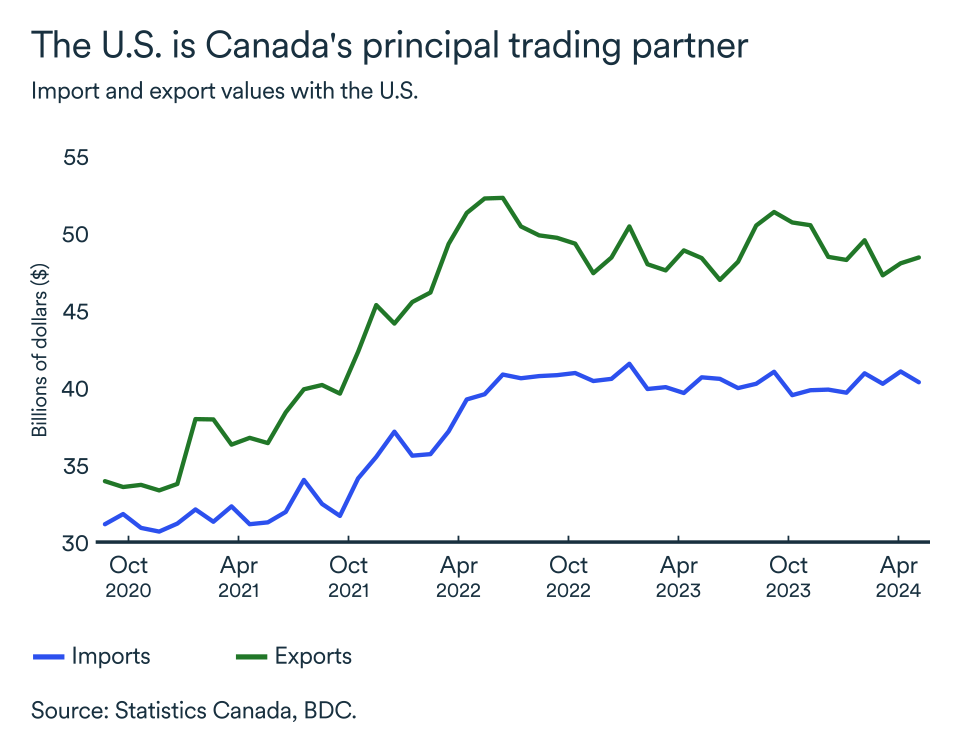

International trade remains crucial for the Canadian economy, with exports accounting for just over 30% of GDP. In April, Canada exported some $65 billion worth of goods, including nearly $50 billion to the United States alone.

Year in, year out, Canada exports 75% of its goods and services to the U.S. and is particularly vulnerable to any move by the U.S. towards protectionism. Donald Trump has said he wants to impose a 10% tariff on all U.S. imports, regardless of their country of origin.

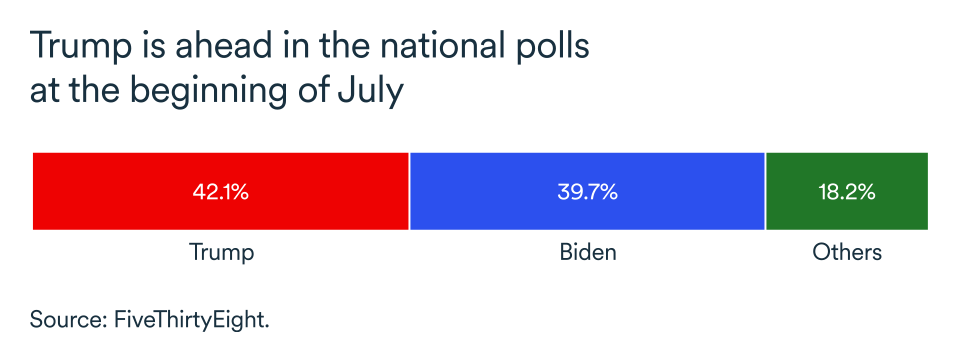

With Republicans ahead of Democrats in the latest polls for the November election, the eventual imposition of those tariffs on Canadian imports is a real possibility. After all, Trump brought in stiff tariff hikes on certain Canadian products, notably steel and aluminum, during his first presidential term.

Canadian growth would be affected

According to our models, a 10% tariff on exports to the U.S. would subtract $7 billion from Canadian GDP in the year of implementation, representing a 0.3% decline from the base scenario. This drop-in economic activity would translate into the loss of around 20,000 jobs in Canada.

In the short term, the impact on Canadian exports would be limited because American customers wouldn’t be able to replace all Canadian imports overnight. The main drag on GDP would come from a significant drop in Canadian business investment, as the imposition of tariffs would cause investor confidence to plummet.

Regardless of whether Biden or Trump wins the election, however, we expect relations between the U.S. and China to remain tense, posing a risk to the global economy and even more so for exporting economies like Canada.

A possible resurgence of inflation

The U.S. economy is still coping with above-target inflation. With unemployment at a low 4.1%, job creation has held steady and wages have risen. The economy is running at or near full capacity.

Consequently, a new economic stimulus plan under a Trump administration would likely fuel inflation, forcing the U.S. Federal Reserve to raise interest rates at a time when the world's other major economies have begun easing credit conditions. What’s more, the imposition of tariffs would also be inflationary in the U.S.

A divergence in interest rate trajectories between Canada and the U.S. already poses a major risk for the Canadian dollar.

In the past, an interest rate differential has weighed on the Canadian dollar and led to higher inflation on this side of the border. However, a shift towards more consumption of domestic services has reduced the inflationary impact of a weaker Canadian dollar.

This should limit the importance the differential plays in influencing the Bank of Canada's monetary policy in the period ahead.

The impact on your business

- Strong U.S. economic growth tends to favour consumption and therefore usually benefits Canadian exporters. In a context where a stimulus plan was accompanied by tariffs to restrict foreign imports, Canadian economic growth could be slowed by a new Trump administration.

- Higher interest rates south of the border could reduce the speed at which the Bank of Canada lowers rates.

- Regardless of the outcome of the election, companies doing business in the U.S. market will have to learn to deal with a shift in U.S. policy changes. However, the uncertain times and geopolitical climate of recent years mean that companies are already better prepared for change. Canada's business owners must continue to invest in their companies to maintain their competitiveness and seek export opportunities in the U.S., as well as elsewhere in the world.

Canada's economy slows but remains in positive territory

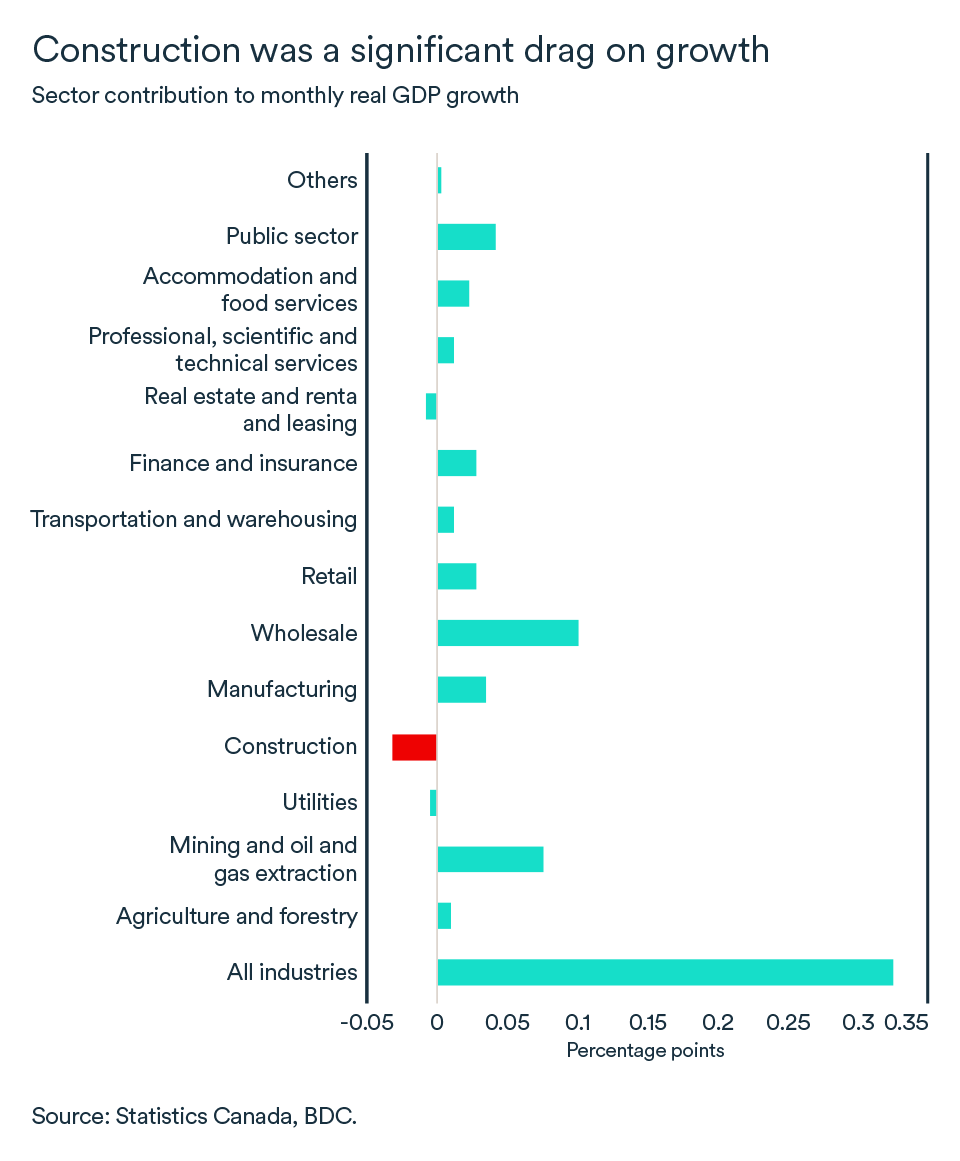

After a decent performance in March, many sectors of the Canadian economy picked up in April. Monthly growth of 0.3% was fairly widespread, with 15 of the 20 sectors covered by Statistics Canada reporting gains.

Preliminary estimates suggest that growth continued in May at a rate of 0.1% compared with April.

A slowing construction sector hurts Q2 growth

A nascent recovery in the construction sector turned out to be short-lived. After a strong March—during which construction reached its highest rate in 18 months—activity slowed again in April.

The downturn was felt mostly in residential construction, a sector where the country is in dire need of growth to address its housing challenges. Activity in the sector is still 24% below the peak reached in April 2021. The industry was expected to recover somewhat in May, with housing starts up 10% over April.

Residential construction has faced its share of issues in recent years. Rising material costs and higher interest rates have hurt the profitability of projects despite the growing need for housing across Canada.

The most recent interest rate cut, and subsequent ones expected in the coming year, should bring some respite to the industry. However, labour issues will continue to impact the sector, whose productivity has been declining for some years now.

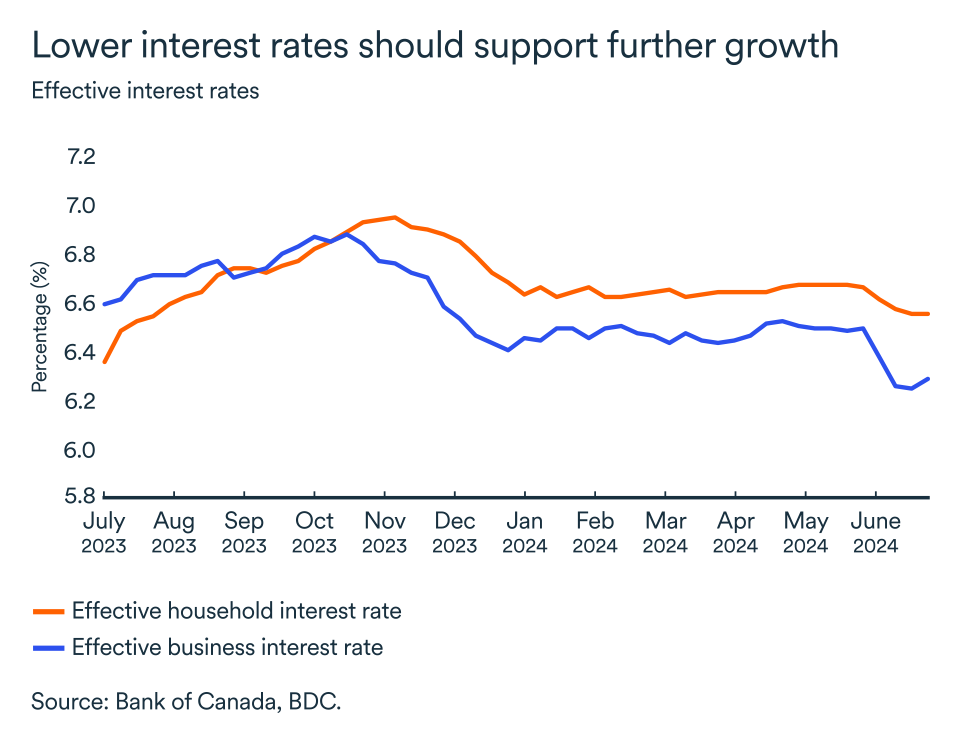

Household finances continue to improve

With the Bank of Canada’s final interest rate hike a year ago now, households seem to have adapted their budgets to a higher rate environment. This is evidenced by the household debt service ratio. This ratio measures the share of disposable income needed to pay current and future debts. It has fallen modestly in 2024, standing at 14.9% in the first quarter.

This means that, even without any change in the Bank of Canada's monetary policy, a smaller proportion of household disposable income is being devoted to debt servicing. Thus, a larger share can be allocated to other spending in the economy. The decline remains small but is nevertheless encouraging because the data dates from before the recent interest rate cut.

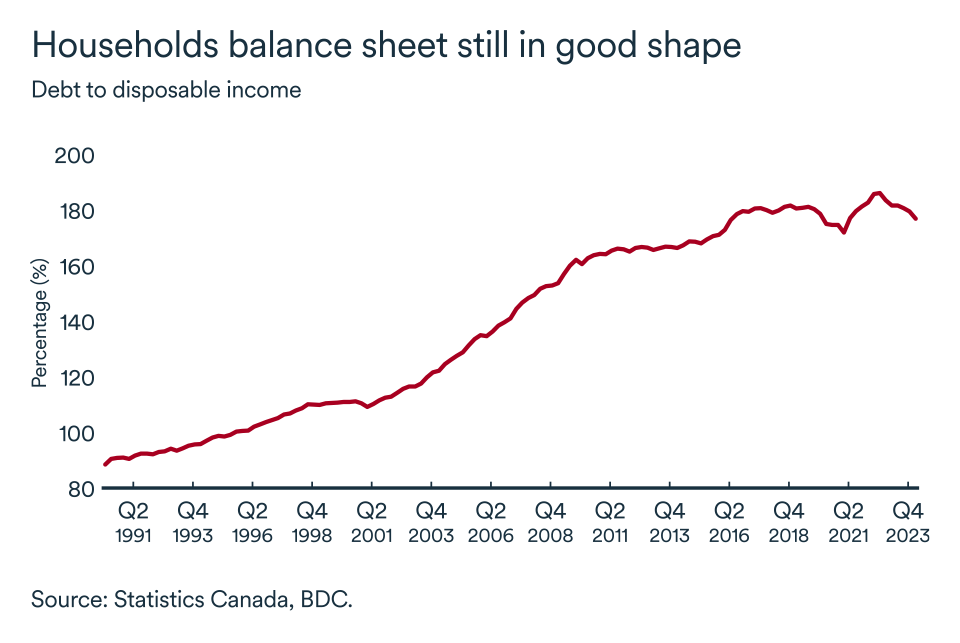

Household debt as a proportion of disposable income has also fallen steadily over the past year. For every dollar of disposable income, Canadian households owed $1.83 at the start of 2023, compared with $1.76 recently.

First rate cut should stimulate growth

Consumer spending is the engine of economic growth in Canada, accounting for around 60% of GDP. The Bank of Canada lowered its key rate by 25 basis points in early June and the market expects further cuts in the second half of 2024.

However, we believe that the Board of Governors will be cautious, evaluating the impact of the first cut before announcing further reductions. Although still small, the first cut should nonetheless support growth in the months ahead.

According to the Nanos-Bloomberg survey, consumer confidence has improved markedly since the rate cut. While confidence is still low by historical standards, it’s currently at a two-year high and should encourage greater spending by Canadians.

A rising real estate market is also likely to help dispel pessimism across the country. Although the increase was not reflected in all markets, the average selling price of homes on the resale market exceeded $700,000 in March for the first time since June 2023.

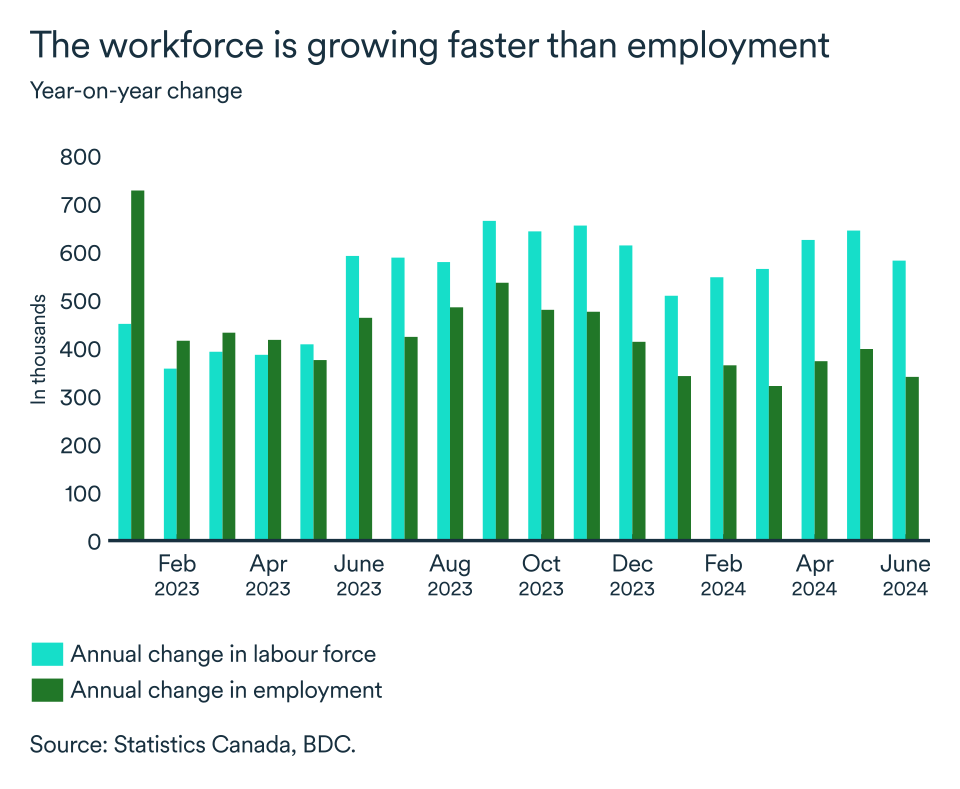

The labour market remains solid but easing continues

Employment remained steady between May and June. With more than 340,000 jobs created in the 12 months to June the labour market remain on solid footing. The unemployment rate increased slightly again in June at 6.4%, 0.2 points above May’s reading.

While job growth is certainly supporting consumer confidence, declining vacancies and a stable unemployment rate signal that the labour market is softening. Nevertheless, strong wage growth continues.

In June, national wage growth was 5,4% higher than the previous year. Pay in service industries is growing faster than goods-producing industries. This indicates that the pace of wage increases continues to pose a risk of rekindling inflation.

The impact on your business?

- Interest rates are set to come down again in the second half of the year, but the Bank of Canada will be cautious and assess the impact of the first cut on the economy before announcing a new one.

- Consumers are regaining confidence in the economy, which should be reflected in their spending. Retailers will feel positive effects, but rates are still high. Wherever possible, differentiate your products to attract the most budget-conscious consumers.

- A further slowdown in residential construction in April, coupled with rising prices on the resale market, risk fuelling more housing inflation. The construction situation is likely to improve as the Bank of Canada lowers rates but could have the opposite effect on the resale market.

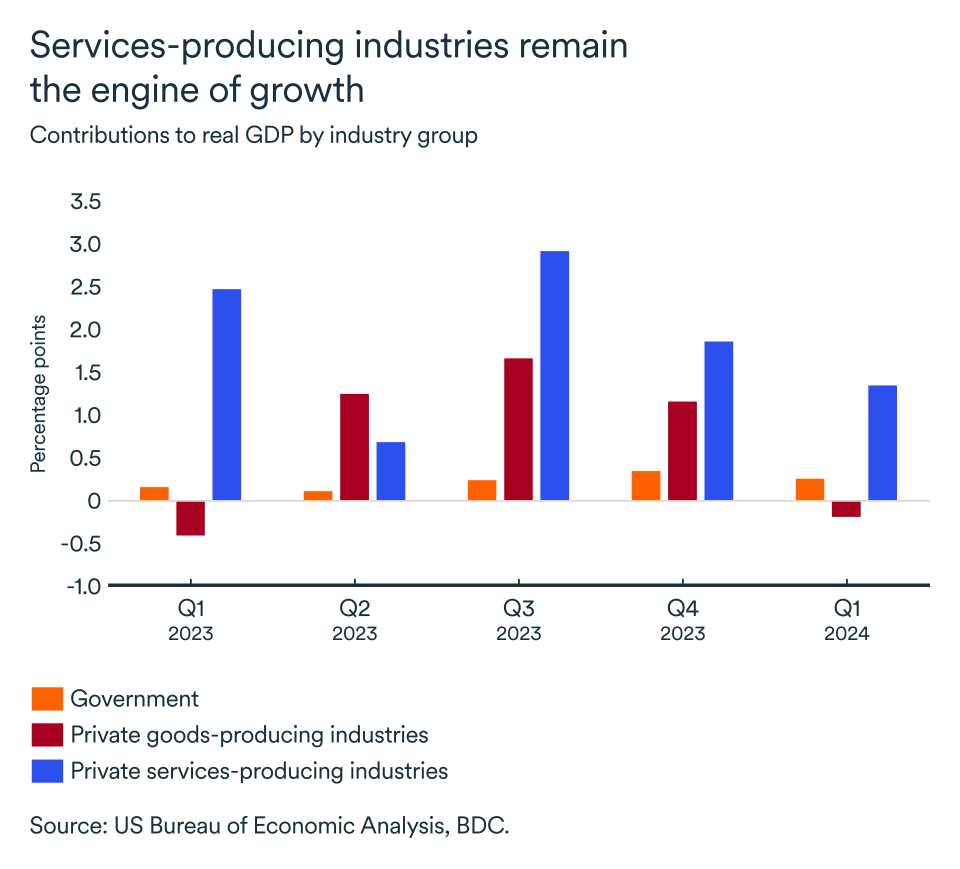

GDP growth moderates further

The U.S. economy grew by 1.4% in the first quarter and, according to the latest estimates, continued to expand at a similar pace in the second quarter—around 1.5%.

After months of surprisingly vigorous growth, it appears the U.S. economy is running out of steam, particularly in goods-producing industries. First quarter GDP declines were seen in durable goods manufacturing (particularly primary metals) and non-durable goods manufacturing (mainly petroleum and coal products).

Gains in the construction sector weren’t sufficient to offset the losses in the manufacturing sector. Goods-producing industries as a whole declined by 1.1% in the first quarter.

The main growth drivers were service industries, with growth of 1.9%, particularly retail trade (driven by motor vehicle and parts dealers), finance and insurance (including activities related to banks and credit intermediation), and health care and social assistance (with ambulatory health care services leading the way). Public spending also made a significant contribution to growth in the first quarter, increasing by 2.2%.

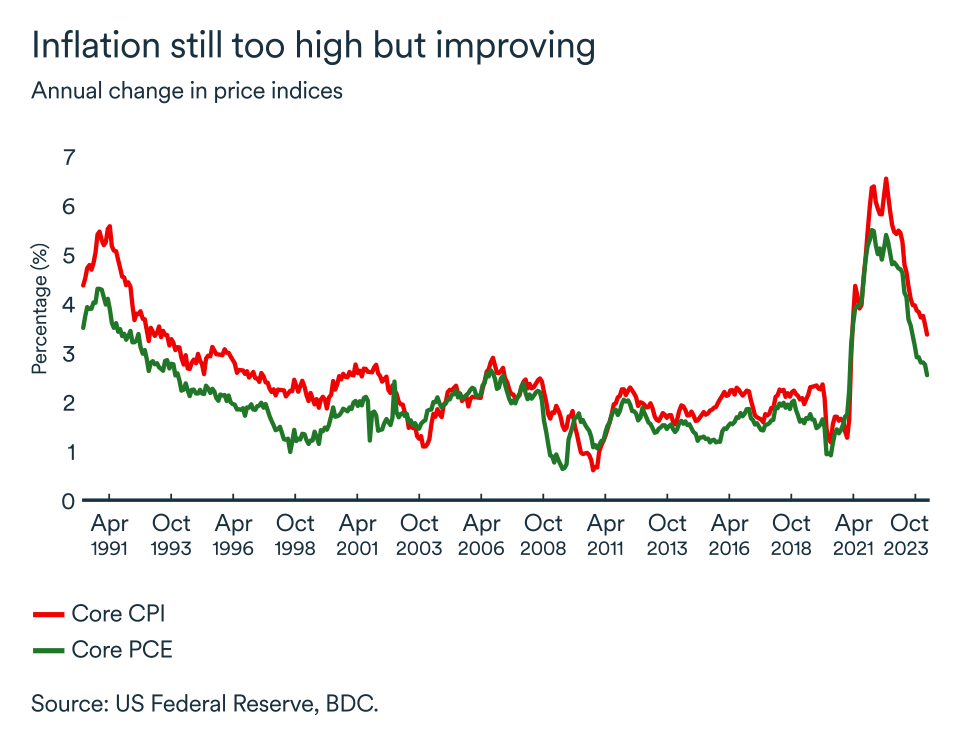

Inflation is slow to come down

Inflation remains stubbornly above the Federal Reserve’s 2% target and it seems it will take a much more pronounced slowdown in spending to bring it back to that level. The underlying inflation figures monitored by the Fed are all still more than 0.50 points above 2%.

Inflation as measured by the core Personal Consumption Expenditure Price Index (PCE), the measure on which the Federal Reserve bases its target, stood at 2.6% in May.

The core Consumer Price Index (CPI) stood at 3.4% in May, down from 3.6% the previous month. The Fed generally gives more weight to the PCE index than to the CPI. Housing accounts for a larger share of the CPI basket, and this category of expenditure is subject to more persistent inflation.

Labour market rebalancing underway

The job market continued to perform well in June with the economy creating 206,000 new jobs. The unemployment rate increased slightly from 4.0% to 4.1%, while the size of the labour force declined, reflecting the aging population.

Slower wage growth is another sign that the U.S. economy is returning to pre-pandemic normal. As job vacancies decline and hiring intentions ease, average hourly earnings still rose by 3.9% in June compared with a year earlier. Several indicators support wage growth at 3% in the coming months, a return to a pre-pandemic level that is in line with inflation at 2%.

The Federal Reserve will remain cautious

The economic picture in the U.S. has not changed sufficiently for us to alter our monetary policy forecast. We still believe it’s unlikely the Federal Reserve will cut interest rates before September.

At the most recent meeting of Fed officials, a small majority of decision-makers admitted that they expected only one rate cut, if any, this year. The overnight rate could therefore remain at its current level—between 5.25% and 5.50%—for the rest of the year. The Federal Reserve, while independent of politics, will also be paying closer attention to the direction inflation may take following the November election.

The impact on your business

- It may have taken longer in the U.S. than elsewhere, but it seems that monetary policy tightening is finally squeezing the real economy. The slowdown is being felt in goods consumption and business investment. If the U.S. is an important market for your company, you may soon feel the impact.

- Stable U.S. interest rates and a slowing Canadian economy could push the Canadian dollar lower, which is always good for exports, but makes imports from the U.S. more expensive.

- Employment continues to perform well but is slowing down. The healthy state of the labour market will help sustain consumption in the months ahead, despite persistently high interest rates.

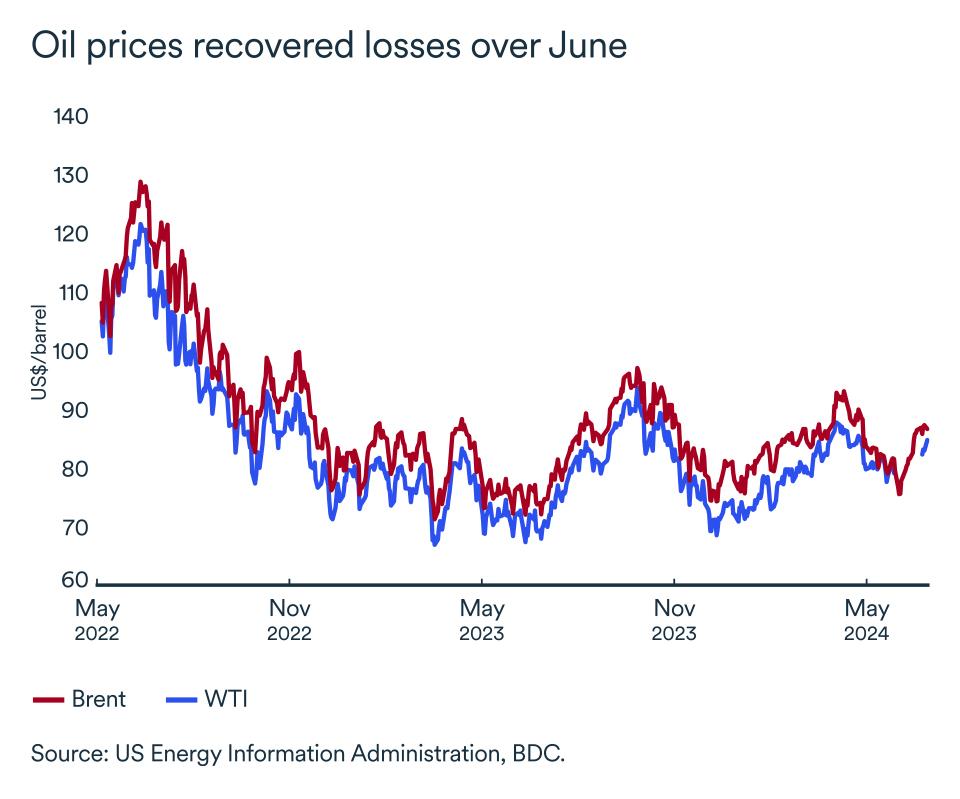

Crude oil prices rebound in early summer

The main crude oil price benchmarks rallied in June. Brent rose to $85 a barrel at the beginning of July after hitting a low near US$75 in early June, its lowest level since February. It was the same story for WTI, which recovered to US$83.20 from US$73 in the period.

OPEC+ members are already exceeding production limits

The Organization of the Petroleum Exporting Countries and its allies (OPEC+) decided in early June to extend production cuts to 2025. However, despite quotas imposed by the cartel on its members, OPEC+ oil production has continued to rise in recent months.

According to Reuters, OPEC's 12 producers pumped 26.7 million barrels per day (b/d) of crude in June, 70,000 b/d more than in May.

Overall, member countries produced 280,000 b/d over target. Iraq's production continued to account for the largest volumes in excess of OPEC+ targets. For its part, Iran saw its production rise to 3.2 million b/d in June, equalling the five-year record last achieved in November 2023. However, Iran is exempt from the cartel production agreement.

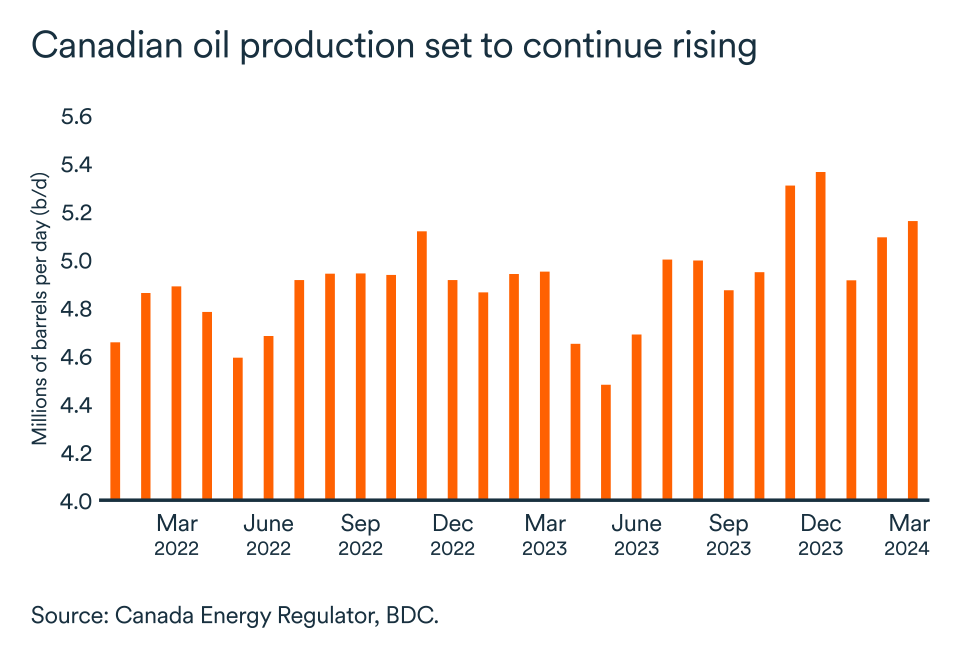

Canada's oil industry cashes in on new pipeline volume

Canadian producers are benefitting not only from the recent rise in crude oil prices but also the opening of the Trans Mountain pipeline expansion.

For several months now, the spread between Western Canada Select (WCS) and West Texas Intermediate (WTI) has been narrowing, a boon for Canadian oil companies. By early April 2024, the spread had narrowed to less than US$13, compared with around US$18.50 at the start of the year.

Canadian producers had increased production in anticipation of the Trans Mountain pipeline expansion start-up in the first half of 2024.

The new pipeline represents approximately 17% of total Canadian crude oil export capacity by pipeline. In anticipation of its completion, Canadian oil companies expanded their operational oil sands projects at the beginning of the year. This contributed to an increase in production without the need for major investments.

Alongside the U.S., Guyana and Brazil, Canada will be a key player in the growth of world oil supply for the rest of the year. Some analysts believe that Canada could even be the biggest source of global oil supply growth this year.

Bottom line...

After bottoming out in early June, Brent and West Texas Intermediate (WTI) prices have rebounded. OPEC+ extended production cuts until 2025, but oil production by member countries continued to rise, even exceeding imposed quotas.

Canadian producers have benefitted from higher prices and a narrowing spread between Western Canada Select (WCS) and WTI since the expansion of the Trans Mountain pipeline. Canada could play a key role in global oil supply growth in 2024.

Policy rate likely to remain at 4.75% this summer

The Bank of Canada lowered its key rate by 25 basis points at its June meeting, but is unlikely to do so again on July 24. Inflation has risen slightly since the central bank's last announcement, while the economy continues to show resilience.

Although the labour market is showing signs of easing, wage growth is still a problem, with the year-on-year change in average hourly earnings rising to 5.4% in June. This pace is far too high to match the 2% inflation target. The key rate is now expected to remain at 4.75% this summer, meaning that the Board of Governors will take a break in July to see how the economy is evolving ever since the June cut. The next rate cut could be announced as early as September if inflation turns around.

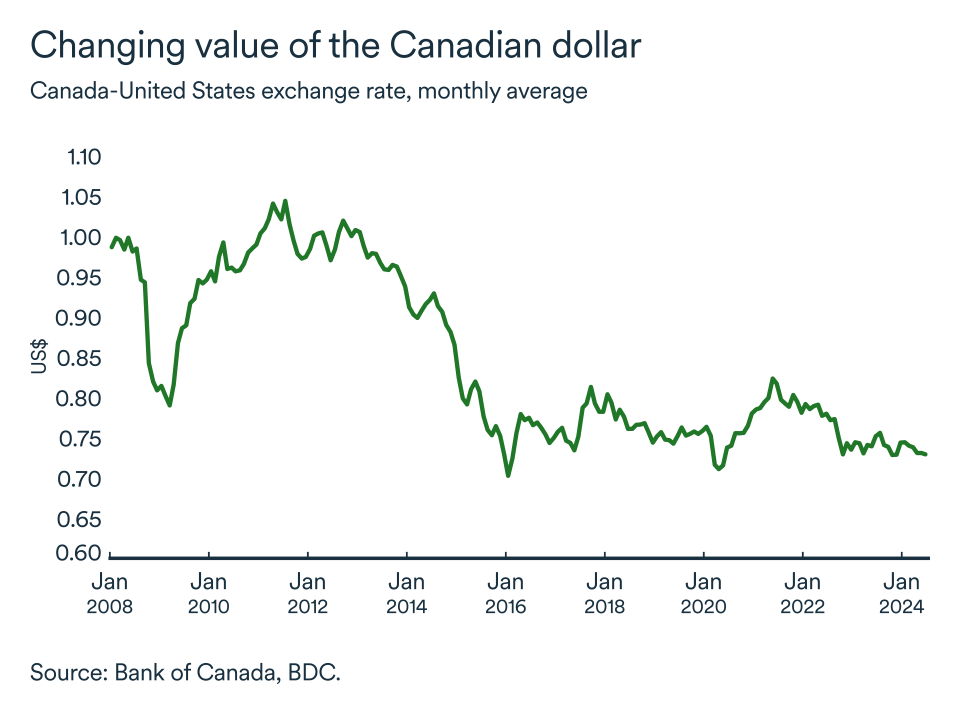

The loonie rebounds from June's decline

The Canadian dollar has appreciated slightly since the beginning of July. In June, the loonie traded at 72.6 US cents, but closed the month higher (above US$0.73).

The Canadian currency's recent, albeit slight, improvement against the US greenback is unlikely to continue for much longer nor gain significant strength. The Canadian dollar is expected to remain between US$0.72 and US$0.74.

Business confidence stable

In June, the CFIB business confidence index for the coming year remained unchanged. The index stayed above the fateful 50 threshold, reaching 56.3. Businesses remain on their toes in the shorter term, as the three-month index recorded a marginal decline of 0.9 points.

An indicator of 50 means that as many company managers expect the business environment to deteriorate as to improve over the period covered (either 12, or three months).