Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreWhat do Canadian consumers have in store for entrepreneurs in 2024?

Consumer spending is the engine of Canada’s economic growth, accounting for some 60% of GDP. As consumers increasingly cut back on spending in response to inflation and high interest rates, a growing number of companies are worried about slowing sales in the coming months. This edition of the Economic Letter looks at the state of consumer spending in Canada, what to expect from consumers in the coming months, and above all, how companies can capitalize on emerging trends to grow their sales.

Worried consumers pull back on spending

During an economic slowdown, workers tend to spend less and save more for fear they may be laid off. We see this phenomenon playing out in Canada. While household savings are down from their peak in 2020, they remain significantly higher than before the pandemic.

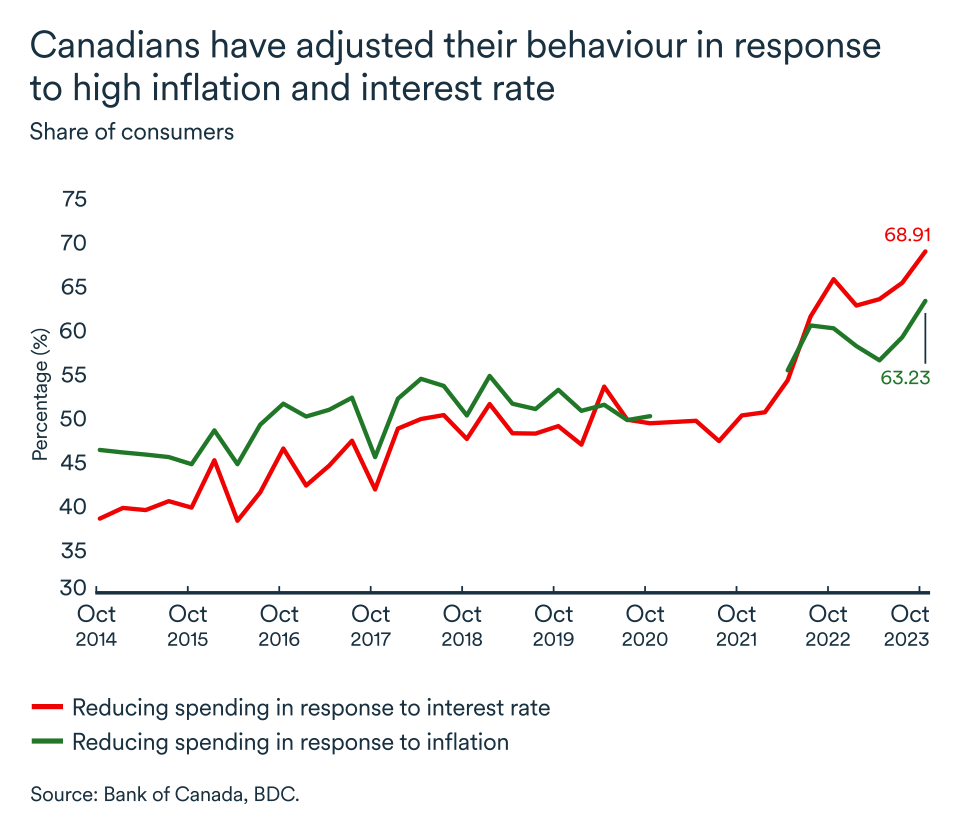

During the pandemic it was difficult to spend on many discretionary items, but today Canadians are cutting back by choice to build up a savings cushion. Nearly two-thirds of consumers say they have reduced their spending because of interest rate expectations, and more than six out of 10 because of inflation.

As a result, 39% of Canadian companies have seen their sales decline over the past year, according to a survey by the Bank of Canada. Sales have been particularly hard hit for items where substitutes are available or that are debt-financed. A slowdown in demand has also been felt more acutely in the clothing, footwear and accessories industry.

Elsewhere, stores linked to home renovation and furnishings are suffering from weakness in the residential market brought on by high interest rates.

While the slowdown is impacting many industries, a rebound in retail sales that began in October is providing hope for a better year in 2024.

Will the resilience of late 2023 last?

According to the Bank of Canada's survey of consumer expectations, consumption is set to slow further, especially early in the year. Canadians plan to reduce their spending even more, particularly on big-ticket items. They also say they’re more likely to shop around for bargains to meet their basic needs.

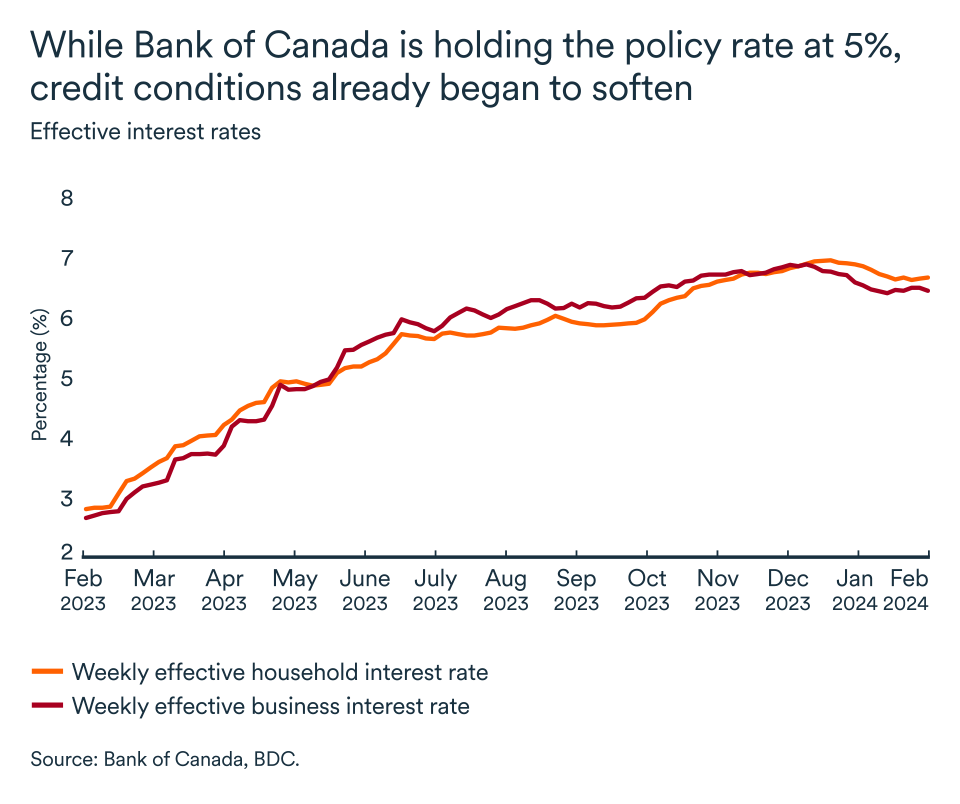

However, there is evidence that consumers have adjusted to higher interest rates and are encouraged by hopes that the rate hiking cycle is over and cuts are coming. The Bank of Canada remains coy about when it will finally decide to lower its key interest rate, but we continue to believe that consumers will benefit from lower interest rates over the second half of the year. An easing of credit conditions has actually already started as effective rates started to go down.

Given the high level of savings in the country, Canadians have the liquidity they need to support the economy once they are convinced rate hikes are a thing of the past. However, businesses may still take longer to recover their sales levels as interest rates will remain in restrictive territory. As well, inflation will continue to hurt certain sectors more than others, namely shelter and food retailers.

On the other hand, strong population growth will support spending, particularly expenditures tied to housing. Thus, the residential market (and related sectors) could rebound rapidly. According to the Bank of Canada, almost 40% of newcomers plan to buy a home within the next year.

How can your company adapt to the current environment?

Whether your company does business with other companies (B2B) or directly with the consumer (B2C), the slowdown in consumer demand will have an impact on your sales. However, capitalizing on emerging consumer trends could help your company stand out from the crowd.

- It can be very useful to take a generational approach to understanding your customers. Each generation has different needs and expectations. Assessing the characteristics of the generations your company serves will help you to better meet their needs, increase your relevance to them and enhance your competitiveness.

- Focus on delivering a complete customer experience. The vast majority of consumers (over 90%) agree that an easy, satisfying experience from the moment of purchase through to ownership and use of the product is fundamental to a good relationship with a company.

- Gaining a better understanding of your customers will allow you identify what’s most important to them when making a purchase. Are your customers more likely to be on the lookout for deals because they’re on a tight budget? Or will they spend on products that are aligned with their values, such as a concern about the environment?

- Today, more than ever, consumers want companies to act as model corporate citizens. Diversity and inclusion, greenhouse gas reduction, ethical and transparent business practices have become an integral part of the business landscape and are likely to remain so over time. Canadian SMEs should seize the opportunity to appeal to new generations of customers by improving their business practices.

Read this report for more details on the best strategies for capitalizing on these trends.

In a nutshell...

Consumption will remain sluggish well into 2024. Sales at many companies are likely to slow, but strong population growth should help moderate the trend. Consumers have enough liquidity to ensure their spending picks up pace in the second half of the year when rates cuts should begin.

Stimulating sales growth in the current economic climate isn’t easy, but companies can still capitalize on emerging trends specific to their customer base to sustain their businesses until the economy picks up again.

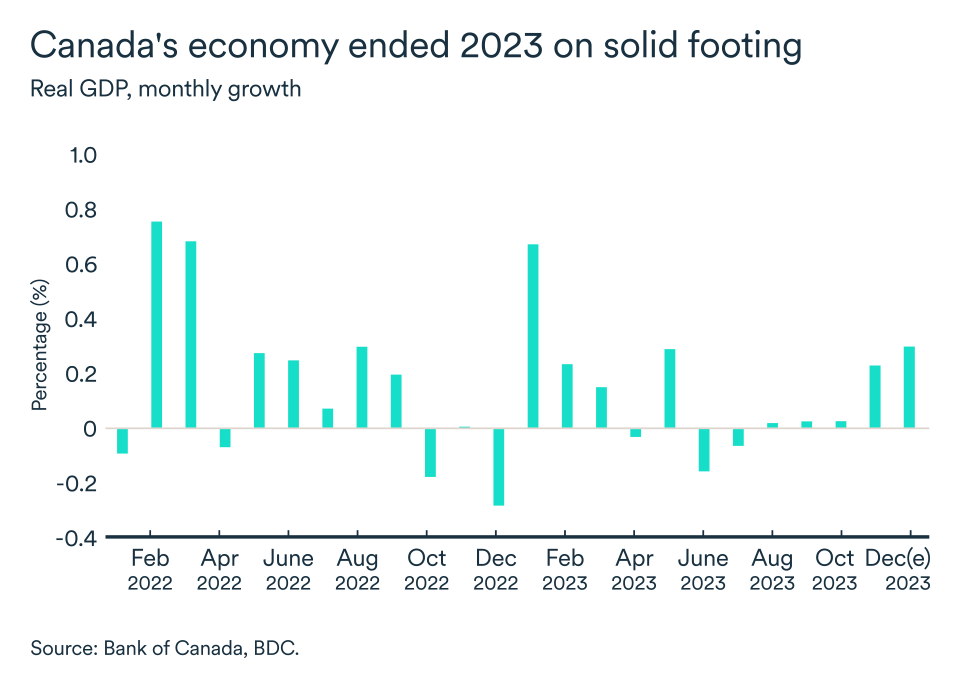

The economy slows, but growth continues

Real gross domestic product rose by 0.2% in November, a significant improvement over October. Most of this gain came from the goods industry, where activity rebounded 0.6%. Overall economic growth was also solid in December (0.3%), according to preliminary data from Statistics Canada.

Despite this modest improvement in the fourth quarter, high interest rates continue to take a toll on the economy, and we expect GDP and employment to stagnate over the coming quarters.

BoC’s key interest rate remains at 5%

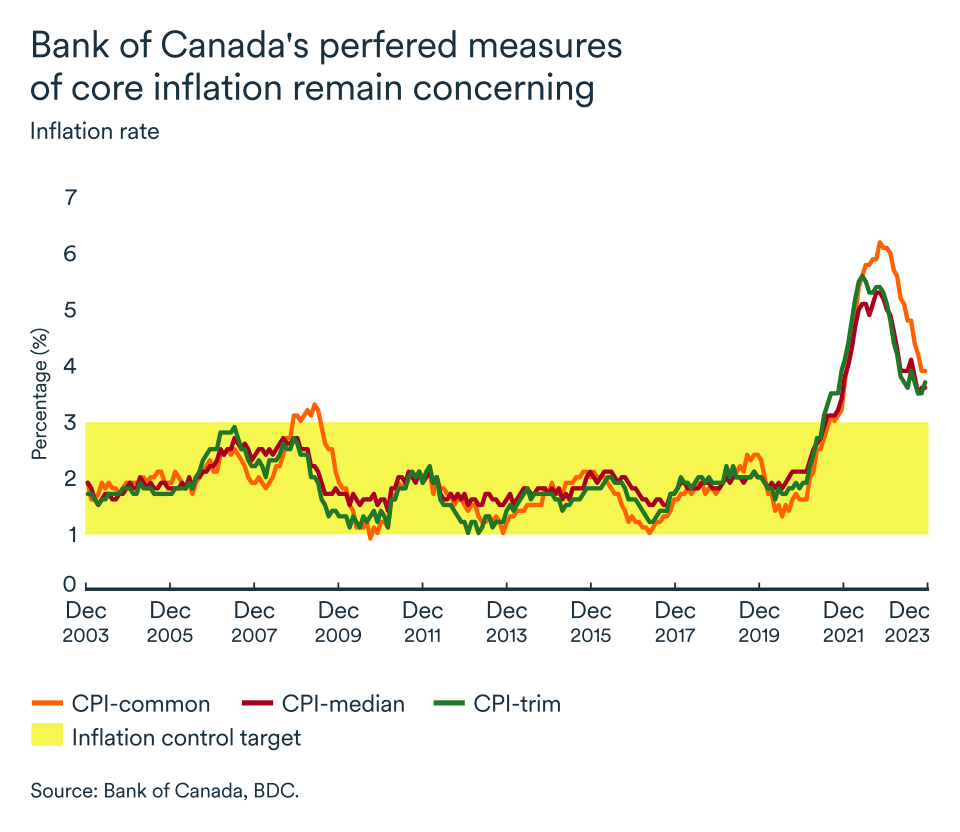

After leaving its key rate unchanged for the fourth time in a row at the end of January, the Bank of Canada suggested rate cuts are on the way but not in the immediate future. The bank is still concerned about inflationary pressures. Price increases for many services have also accelerated recently, but the central bank considers these to be temporary.

Notwithstanding the ongoing pause on rate action, the effects of past hikes will continue to temper economic growth in the months ahead. We continue to believe the first interest rate cut will come at the bank’s mid-year meeting.

Job market firmed up at the start of the year

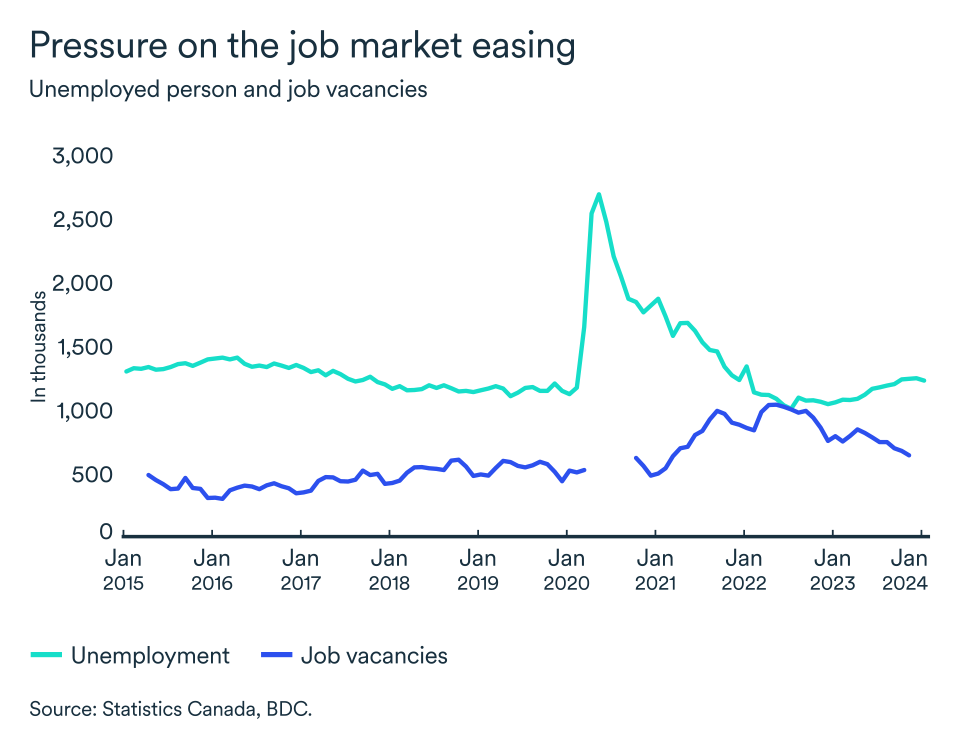

Employment is still growing in the country, surprisingly fast enough to prevent a rise in the unemployment rate this time around. 37,000 jobs were created in January (+0.2%), but that was once again outpaced by the growth rate of the population (+0.4%). The unemployment rate slowed to 5.7% in January. While this mark the first decline in unemployment rate since December 2022 it is still almost a full percentage point higher than a year ago.

Employment is set to slow in the coming months as the economy remains sluggish. Hiring intentions are down, with only 37% of companies expecting to hire new staff in 2024 according to Bank of Canada’s survey. Job vacancies also continue to decline significantly.

Since peaking at 1 million in mid-2022, the number of jobs available in Canada fell to 637,000 in November. Hours worked were also down in the fourth quarter. This decline, combined with the expected increase in real GDP, could have resulted in Canada finally seeing productivity gains at the end of 2023.

These various factors resulted in wage growth of 5.3% between January 2023 and January 2024, not a significantly slower pace than in recent months and still well above the historical norm.

Confidence slowly returning to the country

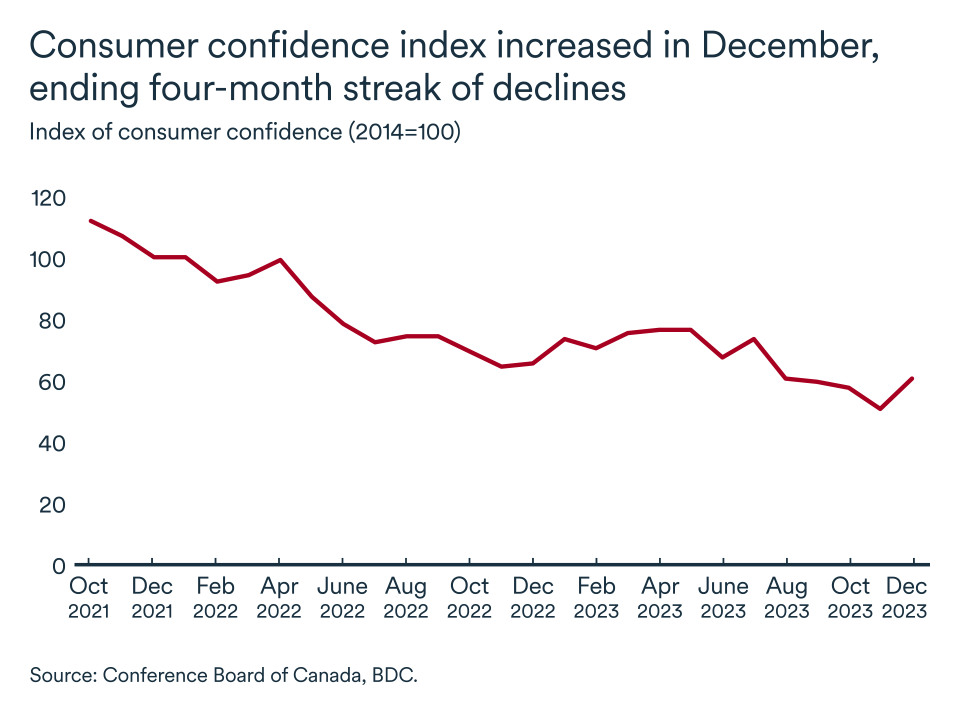

Consumers were pessimistic and anxious about the future at the end of 2023 and these trends were still firmly entrenched at the start of the new year. However, the prospect of rate cuts this year appears to be improving the mood of households. Various confidence indices have begun to rise, with the Nanos Bloomberg index even moving into positive territory in January. Similarly, the Conference Board of Canada's consumer confidence index rose by 9.6 points to 61.1 in December, ending a four-month slide.

The past performance of these same indices leads us to believe that economic activity was stable (or only slightly down) at the start of the year. With the economy having avoided a recession in 2023 and the possibility of interest rate cuts becoming more real, consumer confidence should continue to recover in the coming months. In the meantime, consumers will remain cautious.

The impact on your business

- Interest rates are expected to remain stable over the coming months, as the Bank of Canada continues to assess the impact of past increases on the economy and concerns about a surge in inflation. We still expect a first rate cut in mid-2024.

- Growth appears to be sluggish at the beginning of the year, and the slowdown should lead companies to pay particular attention to their inventory levels. Learn how to improve your inventory management here.

- The Canadian labour market remains solid, which should continue to temper recession fears. Household savings are above their pre-pandemic trend, and wage growth is still strong. Households therefore are still in a good financial position to absorb past interest rate hikes and persistent inflation. Still, they are being more cautious in their spending. See this month's main article to learn how to cope with a slowdown in demand for your products.

U.S. economy still holding its own

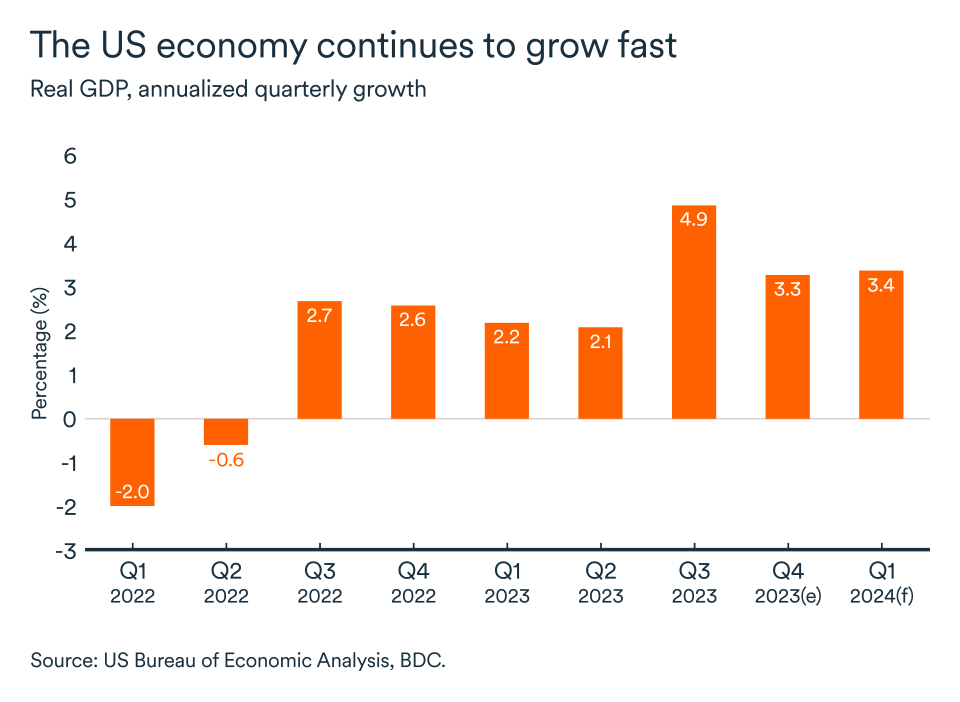

The U.S. economy ended 2023 on a high note and likely continued on a roll in the early part of this year, with forecasts pointing to 3.4% growth in the first quarter. Barely halfway through the quarter, it’s far from certain growth will actually reach such a high rate, but the bullish forecasts are another indicator that the U.S. economy remains strong.

According to preliminary data, real GDP growth came in at 3.3% in the final quarter of 2023. That was down from a robust 4.9% in the third quarter but still healthy.

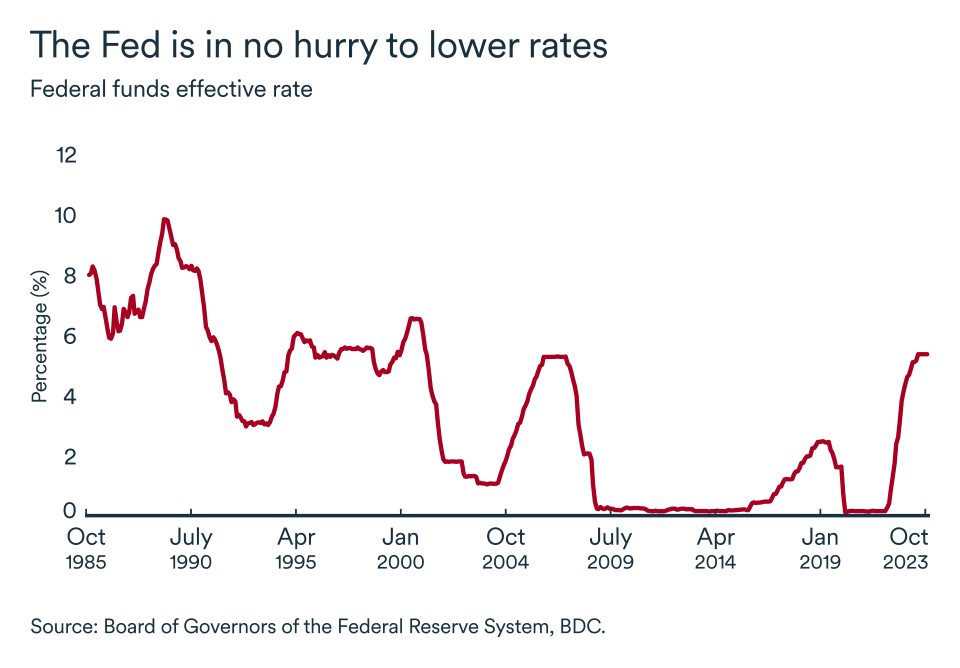

High interest rates have failed to dent either economic growth or the job market. So, even if inflation looks to be increasingly under control, it won't be enough for the Federal Reserve to change course and begin cutting interest rates in the short term. The Fed will likely prove more patient than the financial market is anticipating but could start cutting rates early in the summer.

Job market maintains momentum

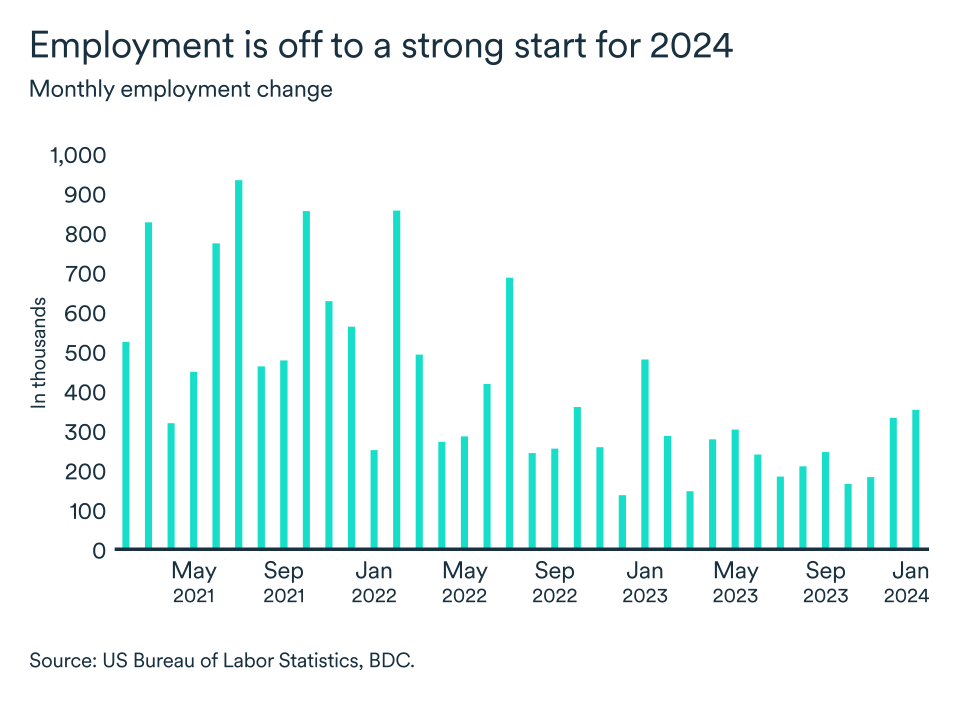

Job creation in the U.S. has started the new year with a bang. The economy added over 350,000 jobs in January, on top of a significant upward revision to December's numbers. At 3.7%, the unemployment rate remains among the lowest on record.

By the end of December, the number of job vacancies had risen slightly to over 9 million. The ratio of unemployed workers to job vacancies remained at 0.7. (A ratio of less than 1 implies there are not enough workers available to fill all the vacancies in the country). As a result, wage growth remains strong at 4.5%.

Households continue to spend

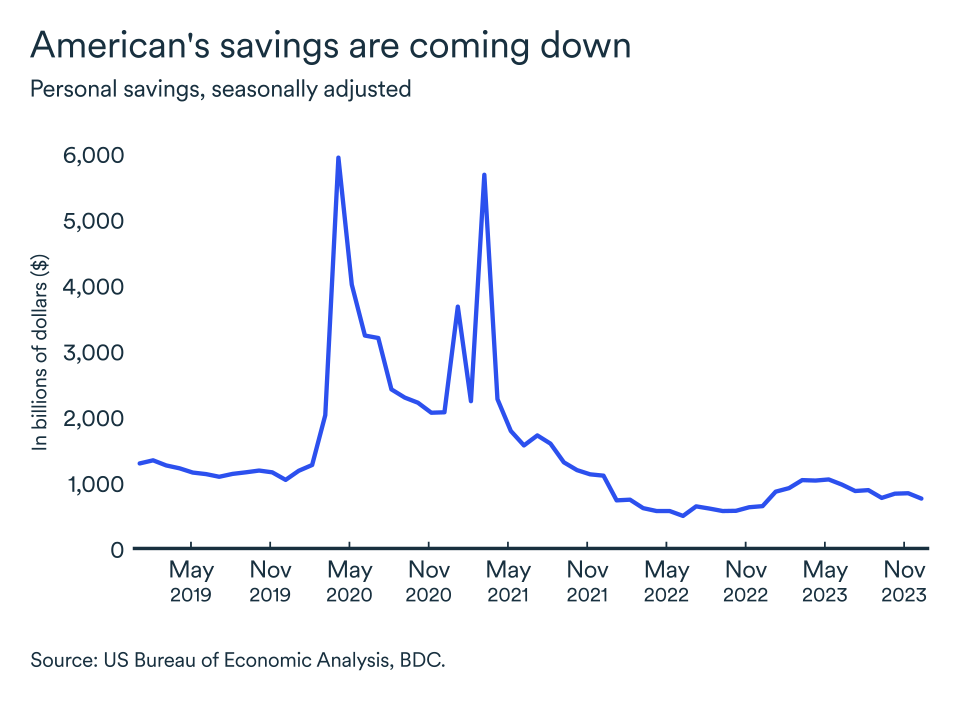

The strength of the labour market continued to support growth in consumer spending, the economy’s engine in 2023. Americans increased real spending by 2.8% in the fourth quarter, in spite of high interest rates. Household debt south of the border is dominated by long-term, fixed-rate borrowing, which means the cost of servicing remains moderate. To keep up the pace of spending, Americans seem to be increasingly dipping into their savings built up during the pandemic.

The recovery in residential investment that began in the third quarter may be faltering. November's sharp rise in housing starts was reversed in December (-4.3%). A drop in new home sales also suggests that residential investment could fall back in the coming months, especially with no clear sign of an upcoming rate cut.

The Federal Reserve sees no immediate need to cut rates

The Fed left interest rates unchanged at its meeting at the end of January, but Chairman Jerome Powell declared that rates had peaked. Since March 2022, the central bank has raised its key rate by 525 basis points to the current range of 5.25% to 5.50%.

Inflation should continue to fall in coming months, but solid employment gains and continued robust economic growth are likely to support the Federal Reserve's guidance that rate cuts are not yet necessary.

The impact on your business

- The U.S. economy has shown continuing strength in the new year. Although the benefits for Canadian companies will be modest, the strong growth should help to mitigate a slowdown on this side of the border. In particular, it should help goods-producing industries such as manufacturing and wholesaling.

- The timing of the Federal Reserve's rate cut remains a source of uncertainty and will influence the Canada-U.S. exchange rate. If the Bank of Canada were to make rate cuts more quickly than the Fed, the loonie would probably fall. A weaker Canadian dollar tends to favour Canadian exports. On the other hand, it increases costs for Canadian companies that depend on inputs traded on world markets or are sourced from the United States.

- Solid gains in the U.S. labour market and a favorable exchange rate for exports should support U.S. imports at the start of the year. This should mitigate the sales slowdown currently being experienced by Canadian companies at least in the short term.

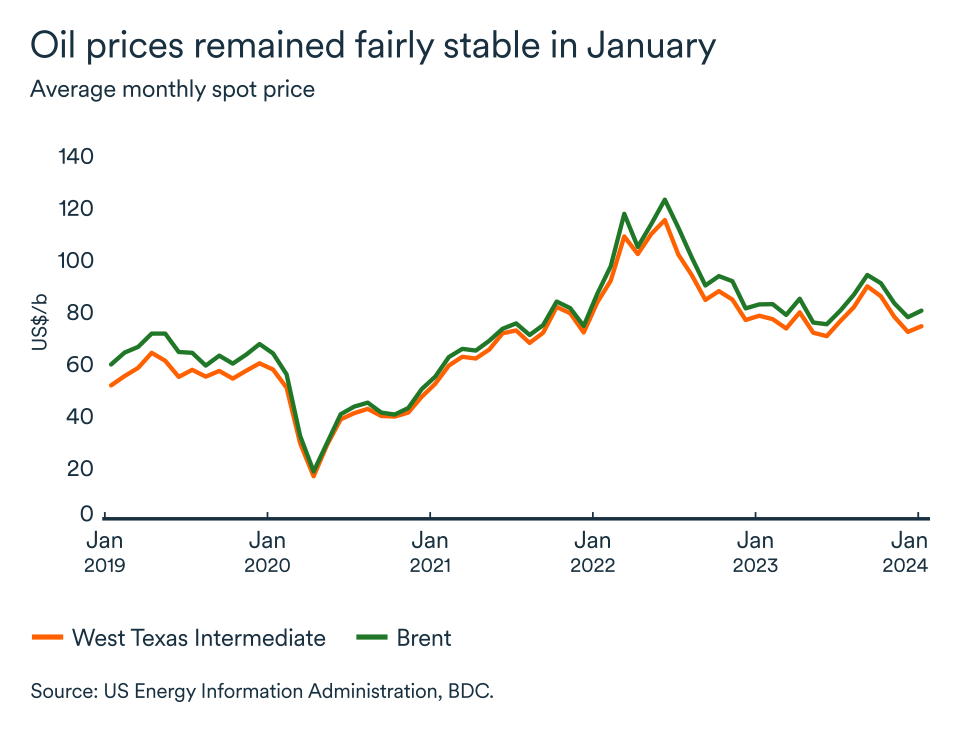

Crude oil prices steady despite global tensions

Crude oil prices remained steady at the beginning of February with Brent at just around $78 a barrel and WTI around $73. However, uncertainty continued to weigh on the market with conflict in the Middle East, uncertainty about the direction of U.S. interest rates and ongoing fears of an abrupt slowdown in Chinese demand.

Waiting for the U.S. rate cuts...

Federal Reserve Chairman Jerome Powell cooled enthusiasm for an early rate cut and markets turned from risky bets towards safe-haven assets, including the U.S. dollar, which reached its highest level in three months.

A stronger U.S. dollar exerts downward pressure on crude oil prices. The main crude indices fell by almost 1% after Powell’s comments. Indeed, uncertainty over U.S. rates was enough to counteract upward pressure on crude prices that would normally have been seen in response to U.S. strikes against the Houthi rebels in Yemen.

Oil prices have risen in reaction to longer shipping times required to avoid the Red Sea route. Escalating tensions between the United States and Iran have been another key factor influencing the oil market of late.

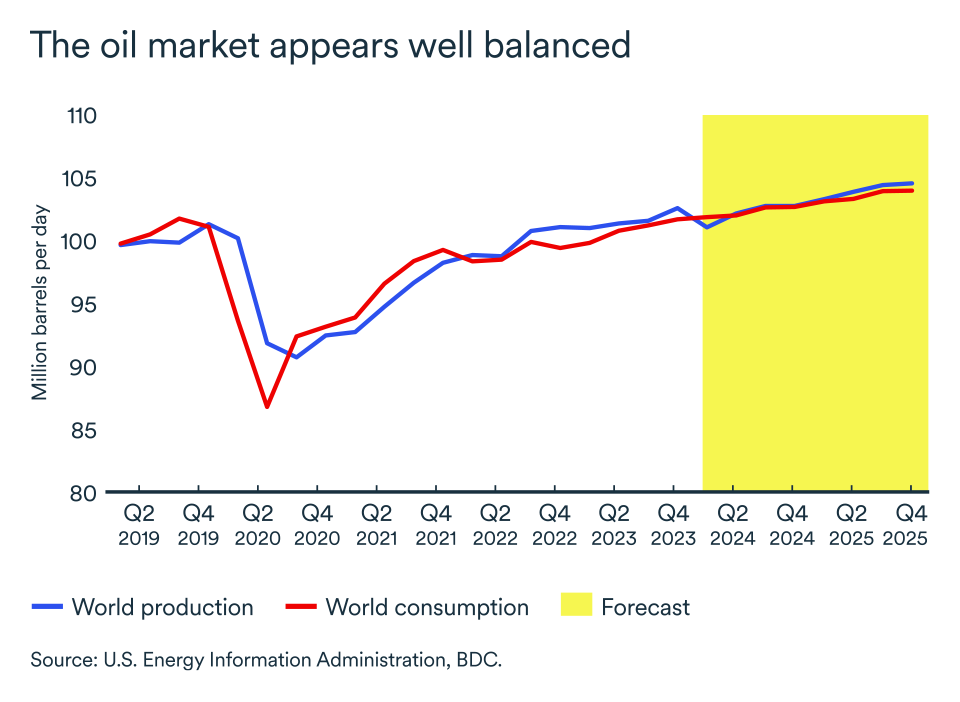

No major market imbalances for the moment, just risks

Oil demand has remained resilient. A global economic slowdown brought on by high interest rates around the world along with fears of a more abrupt slowdown in Chinese demand are helping to keep crude prices within their recent ranges. Manufacturing activity in China, the world's second-largest economy and consumer of oil, contracted for the fourth consecutive month in January.

Crude oil supply remained robust at the start of the year. Despite prolonged production restrictions by the Organization of the Petroleum Exporting Countries and its allies (OPEC+), output from non-OPEC countries is still rising at a healthy pace.

At the February meeting, OPEC+ ministers made no changes to the oil production levels agreed to in November. The 2.2 million b/d cut (led by Saudi Arabia, which renewed a voluntary 1 mb/d reduction), could be renewed beyond the first quarter (as currently agreed), when ministers meet in early March.

In a nutshell...

Opposing forces have created a degree of price stability in the markets of late. Despite the heightened risks associated with shipping in the Red Sea and other factors, abundant global supply has substantially offset the geopolitical risk premium on crude oil. The uncertainty surrounding these many factors will keep the price of a barrel between US$70 and US$90 during the year, an acceptable level for both OPEC+ and non-OPEC producers.

The Bank of Canada kept its key rate unchanged but dropped its tightening bias

The Bank of Canada decided to keep its trendsetting rate at 5.0% in January. It also reduced its outlook for GDP growth by 0.1% to 0.8% for 2024. In previous statements, the bank had specified there might be a need for more tightening in the future. This time around, it was comfortable enough with the inflation picture to remove this tightening bias. However, the bank acknowledged it still has concerns about upside risks to its inflation outlook stemming from higher energy prices, shipment costs or high wage inflation.

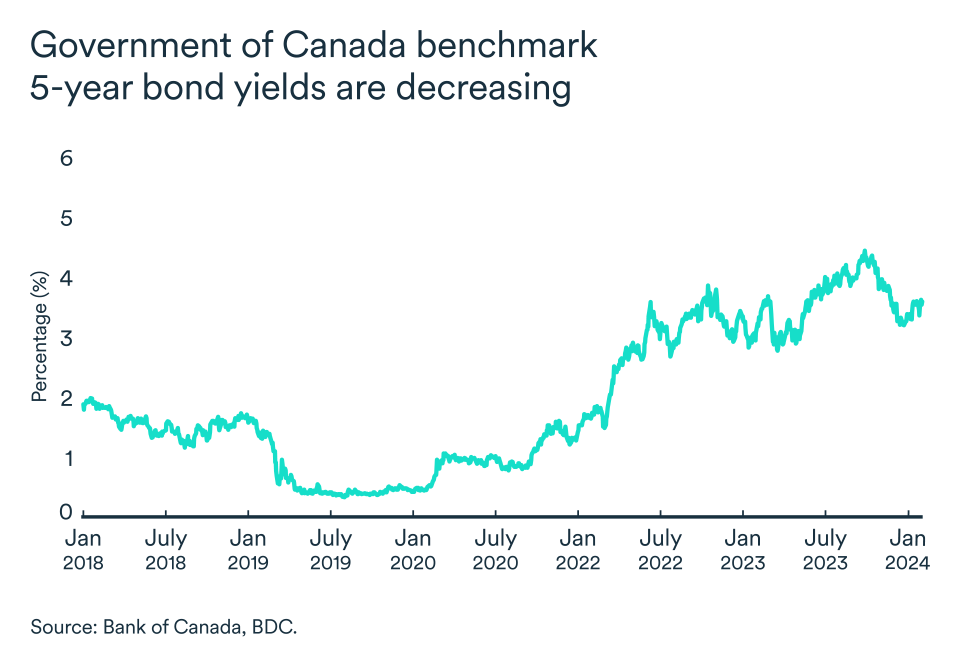

Markets have already priced in a rate cut for June 2024. We believe that, provided a sustained easing in inflation pressure, the bank should start lowering interest rates at that time, bringing them down to close to 3.5% by year-end.

Financial conditions start to ease

Financial conditions began easing in mid-October 2023, even though the Bank of Canada held its rate steady. In the bond market, long-term government yields have fallen and financial institutions have followed suit, lowering their mortgage rates.

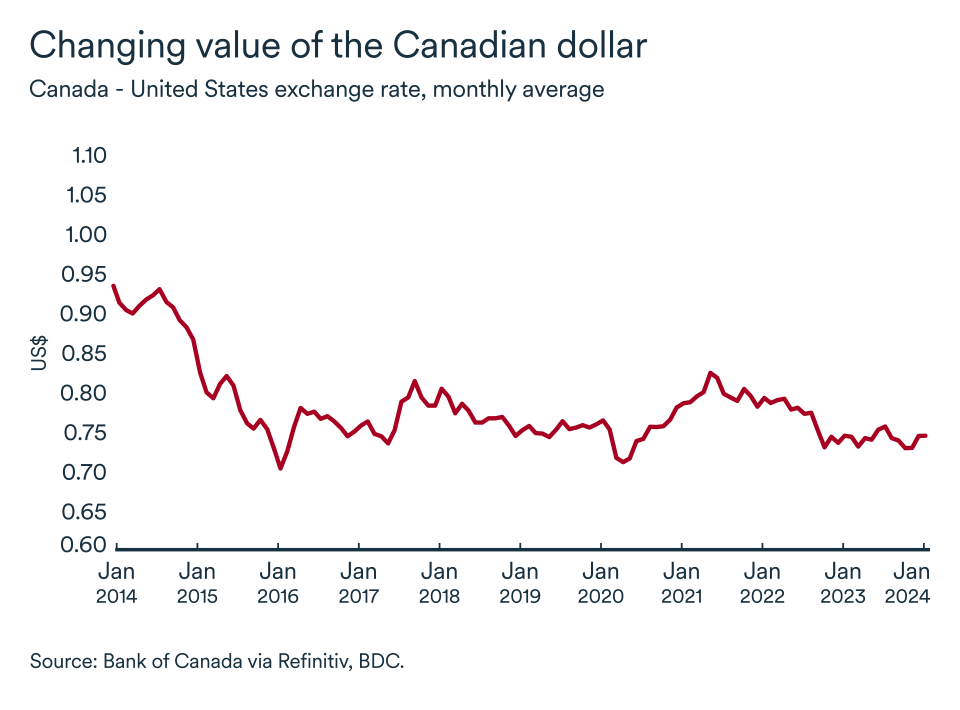

The loonie stabilizes in January

The Canadian dollar remained stable in January, averaging US$0.74. The long-term outlook continues to be muted for the Canadian dollar. The U.S. economy is heading toward a soft landing with growth expected to reach about 2% in 2024, outperforming the U.S.’s major trading partners. We expect the exchange rate to fluctuate between US$0.72 and US$0.75.

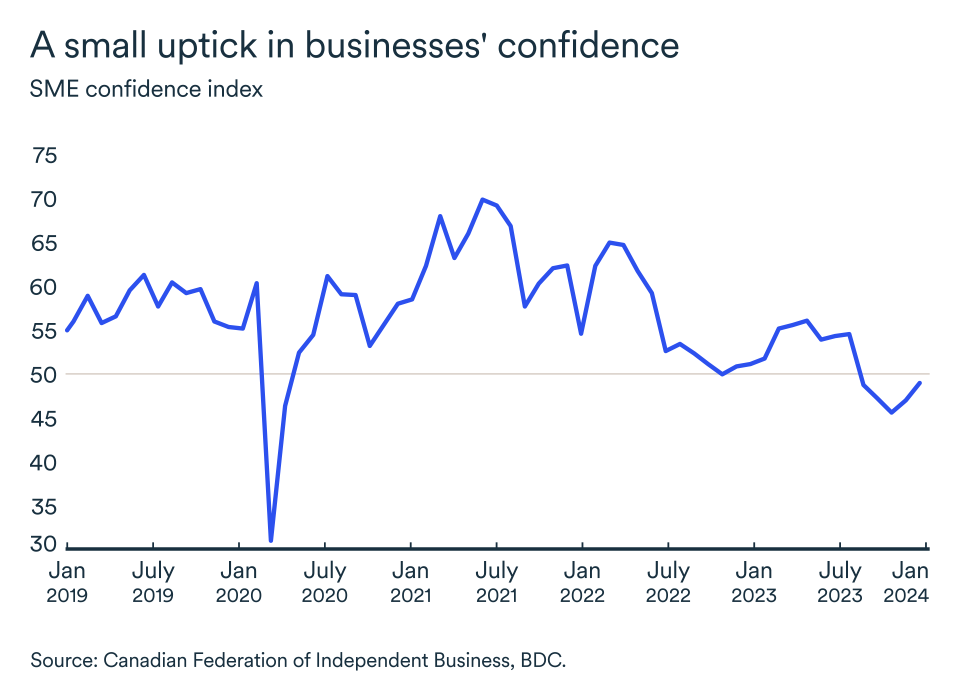

Business leaders slowly regaining confidence

The CFIB's confidence index for the year ahead remained below the critical 50 mark. However, confidence is improving among business leaders. Optimism increased from 47 to 49 between December and January. Some provinces were more optimistic than others: Prince Edward Island, Newfoundland and Labrador, Saskatchewan and Manitoba were among the most optimistic, at 50 and above.