Monthly Economic Letter

Keep abreast of key economic indicators.

Read more3 ways Canada’s population boom is impacting the economy and your business

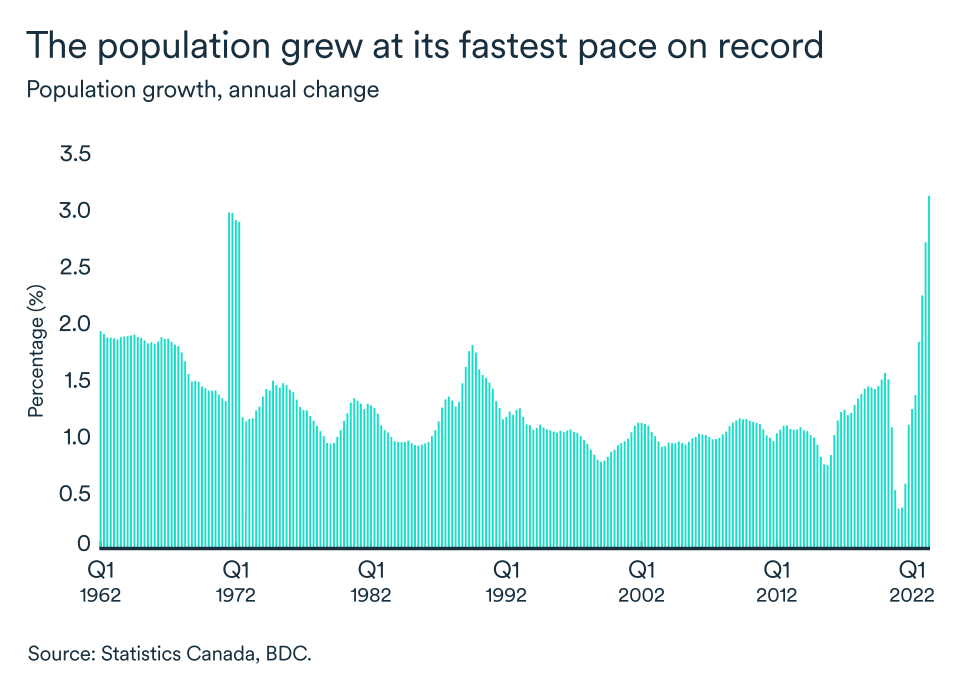

Canada's population is growing at a record pace, thanks mainly to higher levels of immigration and temporary resident arrivals. The population expanded by over 1.1 million people in 2022 and high growth is set to continue in the coming years.

This month's Economic Letter looks at how Canada's growing population is changing our economy and what it means for your business.

1. Economic growth

Despite a slight dip in the second quarter, Canadian economy has shown resilience in the face of rising interest rates and the waning of a post-pandemic spending wave. One of the factors behind this resilience is population growth.

Supply and demand are the fundamental factors driving the economy. A growing population contributes to both. On one hand, more people mean more demand for goods and services. On the other, a larger population adds workers, entrepreneurs and other supply elements to the economy.

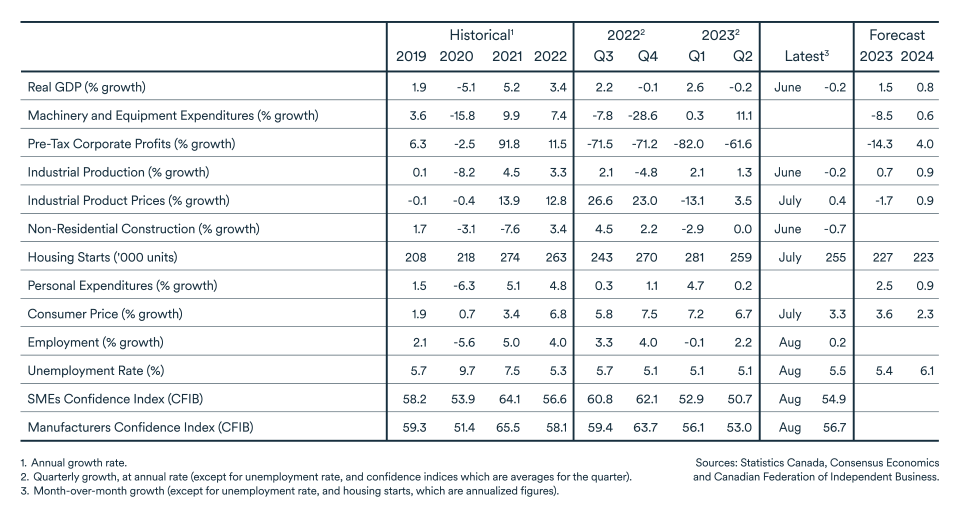

Canada’s annual population growth reached 3.1% in the second quarter of 2023. Over the same period, real GDP grew by 1.1%. Therefore, Canada’s population is growing faster than the economy meaning that the standard-of-living performance is deteriorating.

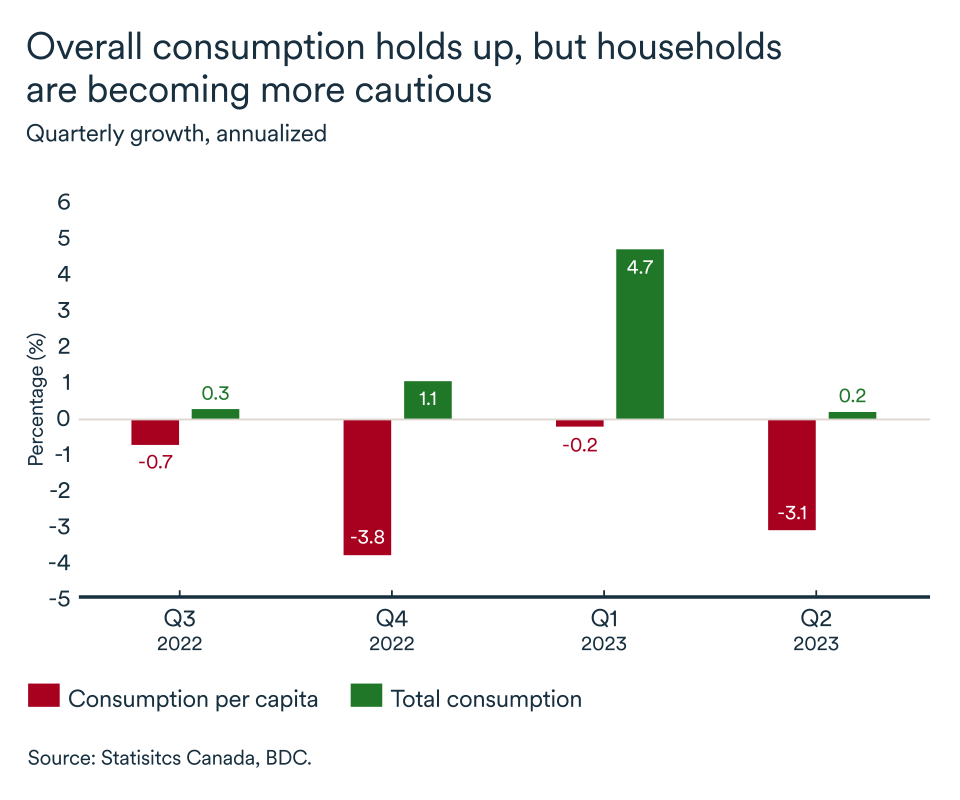

A per capita analysis of real GDP actually shows that the Canadian economy is more vulnerable than aggregate figures suggest. We tend to favour an analysis of GDP per capita to assess a nation's economic prosperity. Consumption continued to grow in the second quarter, but household spending per capita declined – a sign that consumers are becoming more cautious in the face of rising interest rates. Essentially, the Canadian economic pie is growing but the average size every Canadian is getting is shrinking. As BDC forecasts economic growth to be sluggish for the reminder of 2023 and 2024, coupled with an expected population growth of 1.4 %, this will lead to continuing lower living standards for Canadians.

2. The job market

While an economic slowdown is finally underway in Canada after a series of interest rate hikes, job creation continues to be very strong. Over the last year, 500,000 new jobs were added.

The active population, meaning available and able-bodied workers, also grew strongly, adding 577,000. Since the pool of potential workers is growing faster than the number of jobs, Canada's unemployment rate rose this year, although it remains low by historical standards.

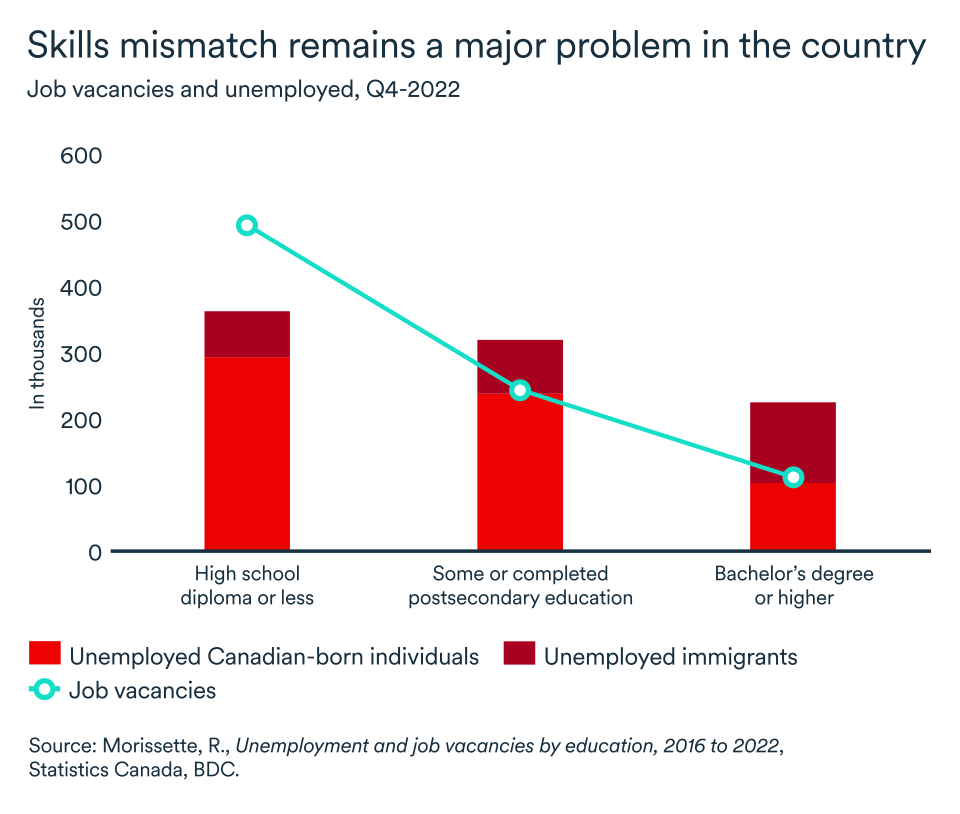

While the growing population is helping ease labour shortages, many companies are still struggling to find the qualified workers they need. Why is this?

According to a Statistics Canada study, an imbalance between the skills of available workers and the needs of employers is a key contributor to persistent labour shortages in many parts of the country.

Therefore, your ability to successfully fill positions won’t necessarily be determined by a lack of workers applying for jobs or how you cope with pressure for higher wages. Rather, it will depend on your ability to train and transfer knowledge to your new hires.

The impact of skill shortages should not be underestimated. Research has shown that hard-hit companies are more likely to experience slower growth, be less competitive and suffer a deterioration in the quality of their products and services.

3. Inflation risk

High population growth carries the risk of higher inflation as more consumers boost overall demand for goods and services. Thus, population growth could counteract the Bank of Canada’s efforts to temper demand and bring down inflation to its 2% target through interest rates hikes.

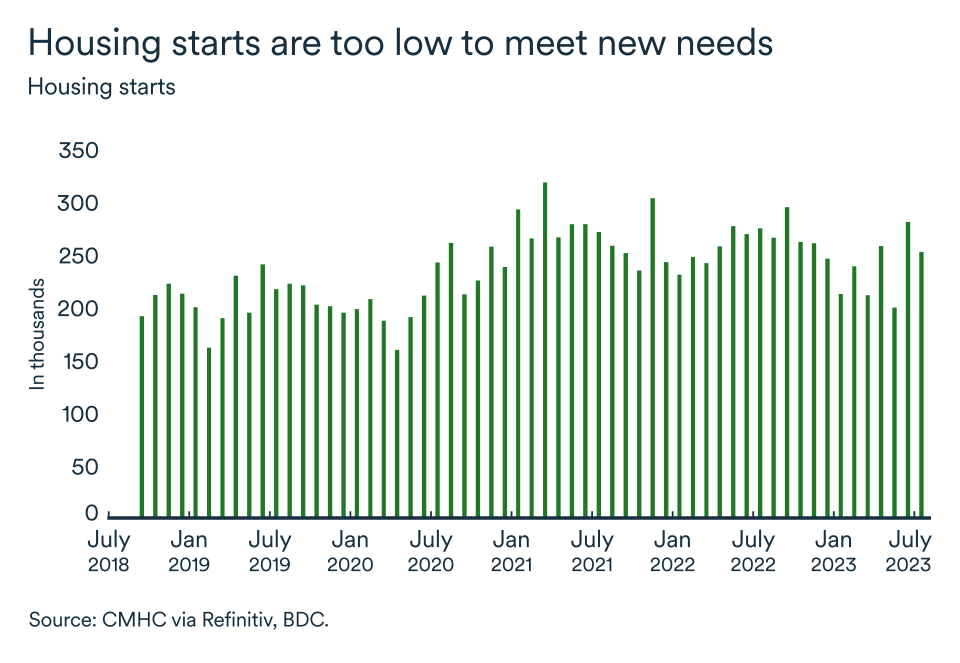

One market where this phenomenon is particularly evident is real estate. There are many housing challenges across the country, but the main issue remains a lack of supply.

Interest rate increases have slowed resale activity and housing starts. However, rental vacancy rates in major Canadian cities remain excessively low. CMHC believe that over 22 million housing units will be required by 2030 to help achieve housing affordability for everyone living in Canada. Since housing starts have not kept up with Canadian needs (so far at least), real estate price could pick up steam again and fast.

The imbalance between supply and demand could therefore widen further as the population grows, with repercussions not only for affordability, but also for the effectiveness of monetary policy in controlling inflation.

Bottom line…

Population growth presents opportunities for small and medium-sized businesses. It offers a new pool of potential consumers and workers for entrepreneurs. But you need to act now to position your business to capitalize on current demographic trends and ensure long-term growth.

The slowdown has finally begun

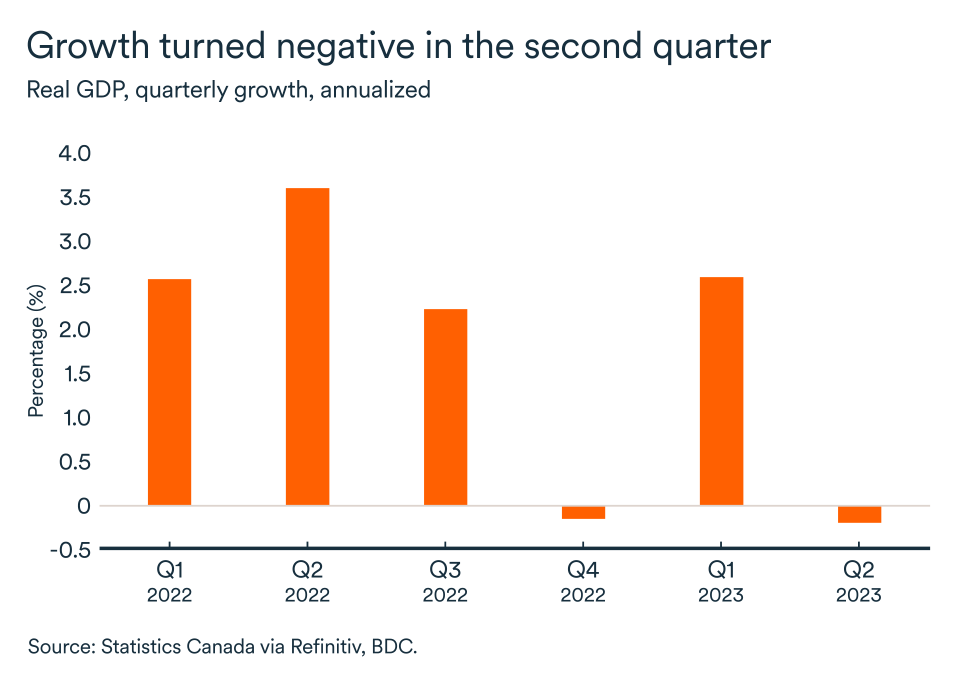

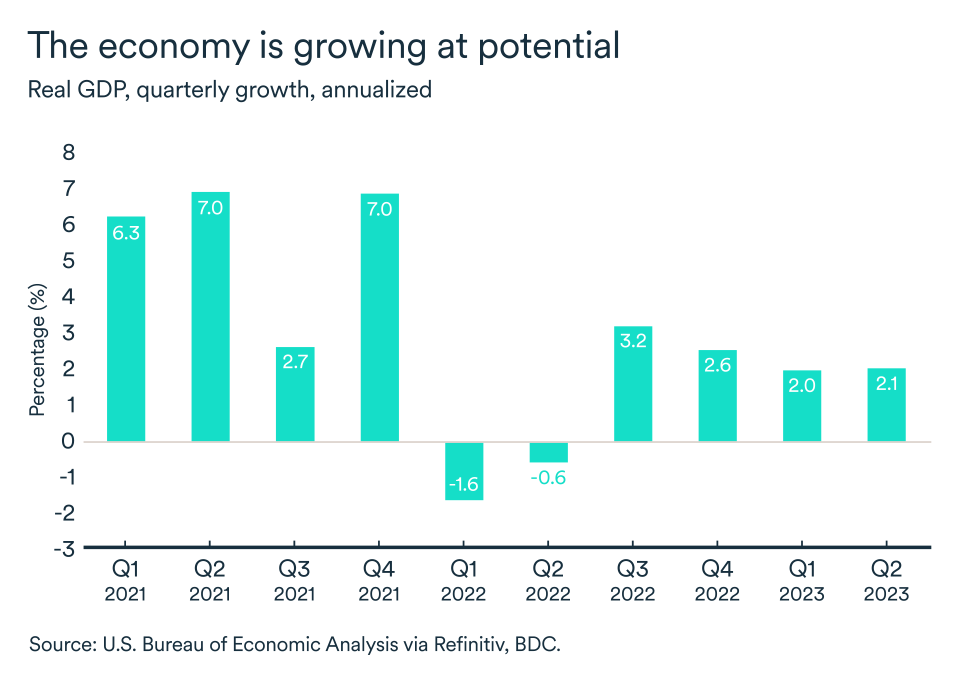

Canada’s economic data for the latest quarter contained an unexpected twist. Contrary to forecasts for slower but positive growth in the second quarter, the economy actually contracted by 0.2% annualized compared with the first quarter of 2023. Statistics Canada also revised growth downwards for the first quarter, from 3.1% to 2.6%.

Does this mean we’ve entered a recession? Not so fast! A technical recession occurs after two consecutive quarters of negative growth. Canada isn't there yet, but preliminary GDP data for July point to an economy that’s stagnating. The forest fires that struck western Canada in August are likely to hurt growth in the third quarter as well.

In fact, according to Statistics Canada, the spring forest fires were responsible for a remarkable 13% decline in the natural resources industry, a 1.4% drop in the oil and gas sector and a 6.5% decline in accommodation services. In addition to forest fires, rising interest rates are having an increasing impact on discretionary consumer spending, including home renovations and retail sales.

It’s now undeniable that the slowdown we’ve been predicting for several months has finally arrived. However, this isn’t necessarily bad news in the current context. Rather, it's a sign that monetary policy is working to counteract overheating in the economy and tamp down price and wage inflation. As a result, the Bank of Canada can likely forego more interest rates hikes.

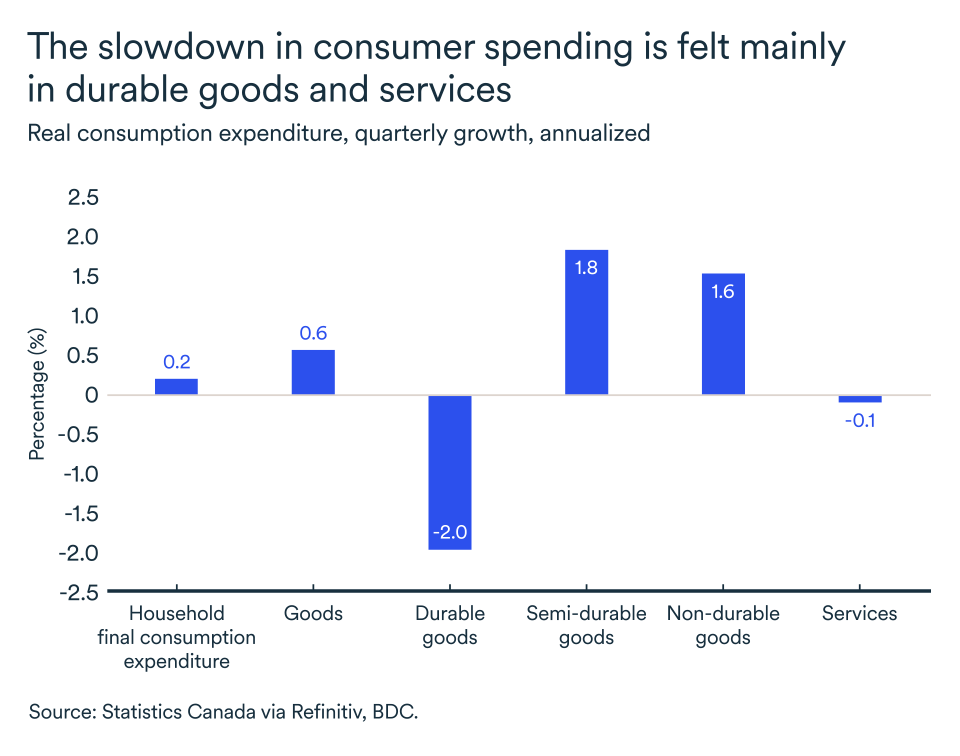

Consumer spending has fallen

Indeed, consumers continue to feel the effects of rising rates, with household spending weakening to annualized growth of 0.2% in the second quarter. This represents a significant slowdown from the 4.7% recorded in the first quarter. Unsurprisingly, consumption of durable goods slowed the most, but purchases of household services were also down slightly.

Meanwhile, households increased their savings during the quarter. In a sign of growing caution about the future, savings reached 5.1% of disposable income, compared with 3.7% in the first quarter. Healthy household income growth largely offset the rise in interest payments. However, prospects for a recovery in spending don’t look promising. Consumer confidence has remained in neutral territory since the beginning of July, according to the Nanos/Bloomberg index.

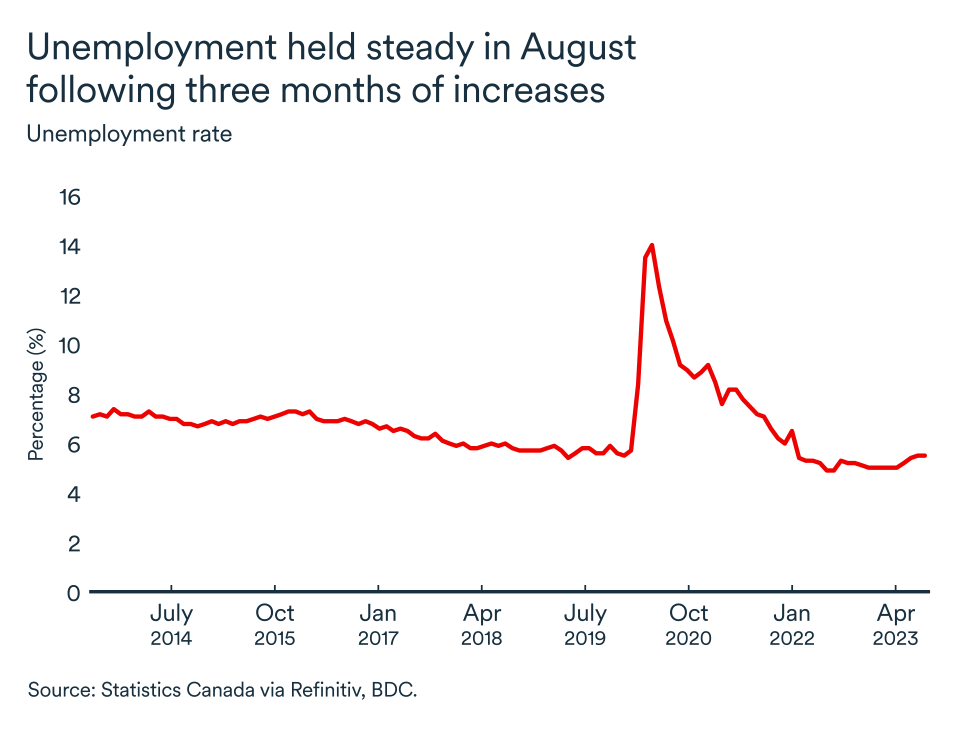

A looser labour market

We usually expect to see job losses during an economic slowdown. There were 6,400 fewer jobs in July than in June, however employment bounced back strongly in August (+40,000 jobs). While unemployment rate has risen in recent months, the increases are largely due to significant growth in the working-age population. Unemployment rate was unchanged in August at 5.5%.

The pressure on companies to raise wages is only slightly easing. The number of job vacancies continues to fall as demand for goods and services moderates. However, average hourly wage growth in Canada reached 4.9% in August, a pace similar to what was seen in recent months.

The impact on your business

- Consumers will continue to pull back on purchases of expensive or easily substitutable items. Find out how you can improve the value of your offerings to maintain sales.

- Interest rates are likely to remain at current levels for some time to come. This is a good time to review your growth plans.

- The expected economic slowdown has finally begun, but it's not too late to adopt good practices and adjust your company's finances accordingly.

The U.S. economy holds up despite higher interest rates

Real GDP growth in the United States remained above 2.0% in the second quarter. The growth mainly reflected a smaller slowdown in inventory investment than in the first quarter and a recovery in non-residential fixed investment.

Residential investment declined further, marking a ninth consecutive quarter of decline, while 30-year fixed mortgage rates jumped to 7.3%—a record in this century.

Consumers continue to spend

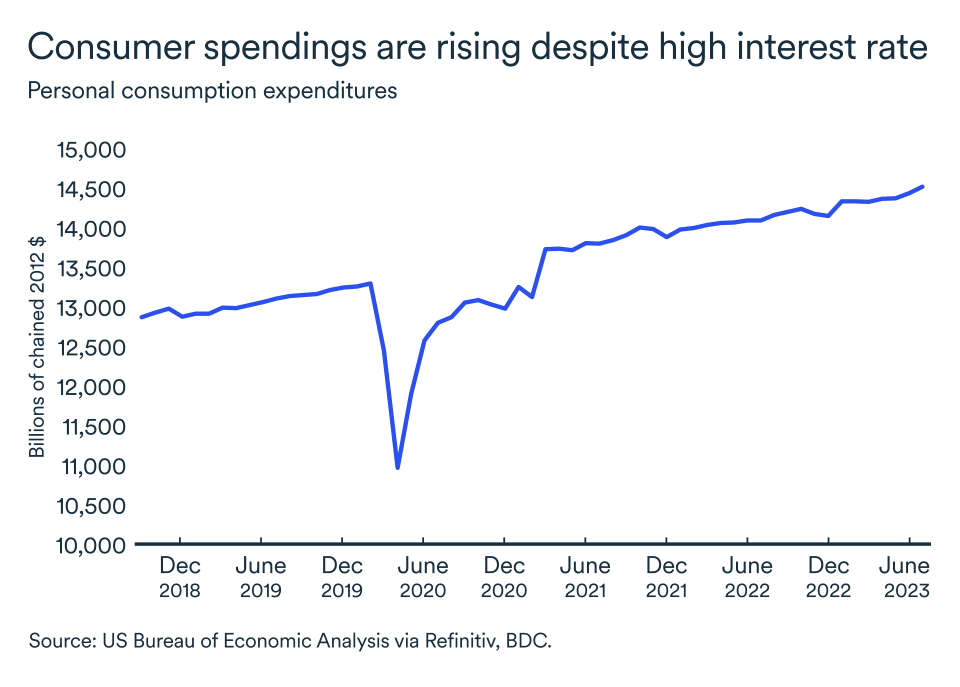

So far, American consumers are supporting the economy with their spending, offsetting the downturn in the housing market. Representing around 70% of U.S. GDP, consumer spending is an important barometer of the economy's health. In the second quarter, spending on both goods and services grew by 1.7%. Consumption in real terms (taking inflation into account) also got off to a good start in the third quarter, rising by 0.6% in July compared with June.

A solid job market is supporting consumer spending. The economy created 187,000 jobs in August, but this was not enough to fully absorb potential new workers coming onto the job market. As a result, the unemployment rate rose by 0.3 percentage points to 3.8%. Although the pace of job creation has slowed in recent months, the unemployment rate remains low.

Consumer spending should continue to support economic growth in the third quarter of 2023, but it will be more difficult for the economy to maintain its pace until the end of the year. Disposable income fell by 0.2% in July, and although average hourly wages rose by 4.3% year-over-year, wage growth is also showing signs of slowing.

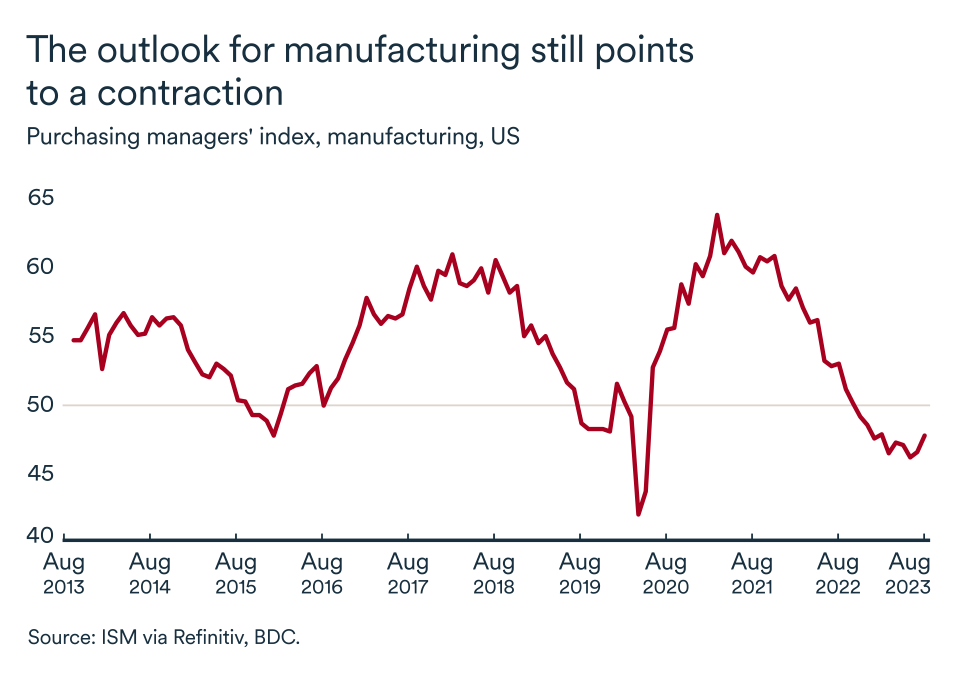

Manufacturing struggles

The manufacturing sector has been directly affected by the tightening of monetary policy worldwide. Despite slight improvements in recent months, the purchasing managers' index for the U.S. manufacturing sector remains weak. The index has been stuck below 50 since November 2022.

A reading of below 50 indicates contraction in the manufacturing sector. The new orders index also remains very weak, suggesting that a slowdown in the sector is set to continue.

Core inflation is still high

U.S. inflation accelerated slightly in July to 3.2% from 3.0% in June. This is the first increase since a peak of 9.1% was reached in June 2022. At the same time, core inflation, which excludes food and energy, fell to 4.7% from 4.8% in June.

The Federal Reserve has raised the Federal Funds Rate 11 times in its last 12 scheduled meetings and it now sits in the 5.25-5.50% range. If inflation proves more persistent than expected in August, Fed Chairman Jerome Powell will probably preside over a final rate hike at the next announcement on September 20.

What does it mean for entrepreneurs?

- Interest rates could continue to rise south of the border, which would further slow the Canadian economy. U.S. imports are already falling, and American consumers won't be able to maintain their current pace of spending for much longer.

- With U.S. manufacturing barely improving in the last 10 months, provinces that are more sensitive to the sector, notably Ontario and Quebec, remain more vulnerable to a slowdown.

- While the U.S. economy as a whole continues to show solid growth, manufacturing, residential investment and durable goods retailers are more vulnerable to rate hikes. If these are your business partners or customers, be prepared for a more pronounced slowdown in the months ahead.

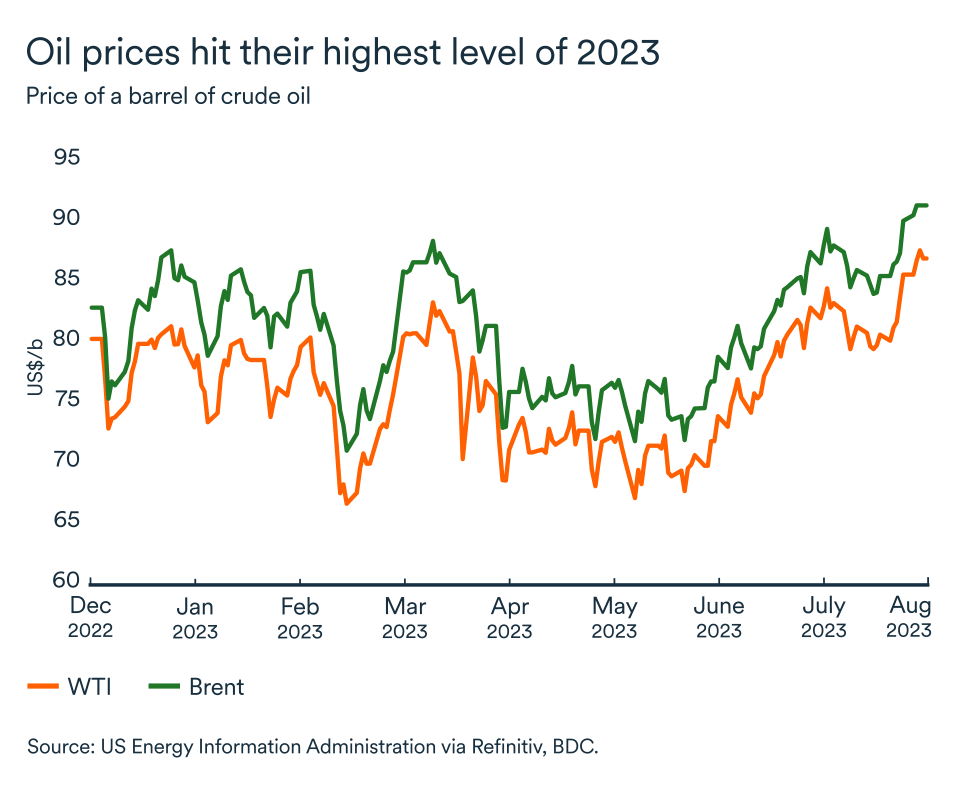

Production cuts lead to stronger oil prices despite weakness in China

The price of crude oil strengthened over the summer. By the end of August, WTI had jumped to US$87 and Brent to US$90. The price rise was mainly due to further cuts announced by the Organization of the Petroleum Exporting Countries and its allies (OPEC+).

Saudi Arabia extended its voluntary production cuts by 1 million barrels per day (mb/d) until the end of the year in response to concerns about the outlook for global economic growth. The same is true of Russia, which has pledged to reduce its crude exports by 300,000 b/d for the remainder of 2023.

Of course, these countries may revise their production plans between now and the end of the year in response to changing market conditions. But for now, planned cuts by OPEC+ amount to over 5 mb/d, or 5% of world oil production to support higher prices.

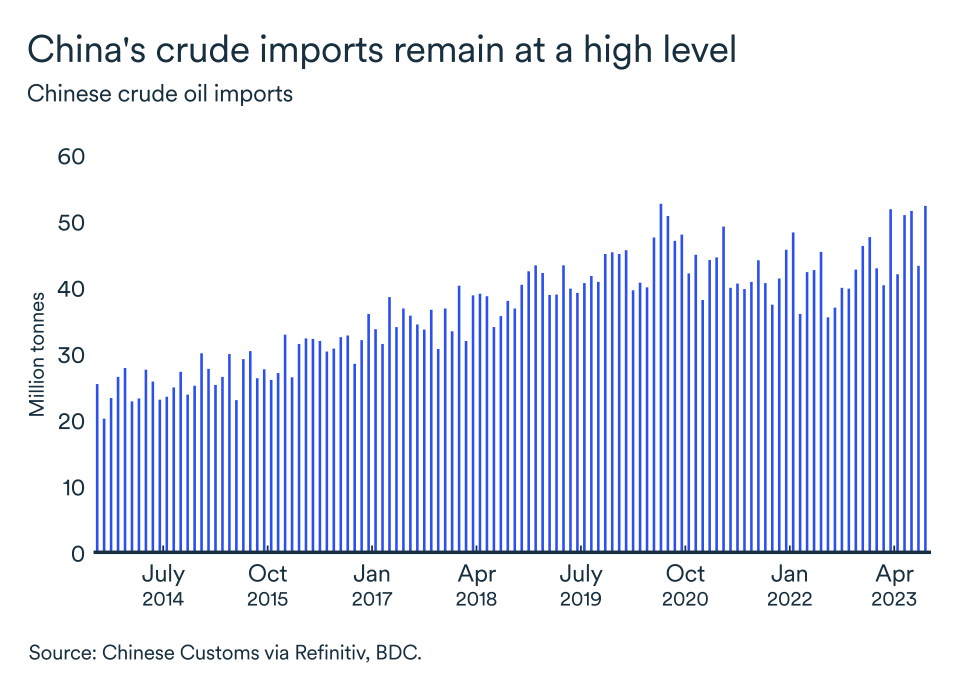

Where is Chinese demand heading?

Despite the new production reductions, crude prices are still being held back by fears about slowing Chinese economic growth.

Between January and July 2023, China's oil imports rose by over 12% thanks to the reopening of the economy and the end of anti-COVID measures. But now China is experiencing a significant slowdown, which is worrying for oil producers.

China’s purchasing managers’ index has been below 50 (in contraction territory) for the past five months. Yet, demand for oil has continued to grow. This is because China has been accumulating oil inventories during this period.

However, Chinese imports fell by 2.38 mb/d in July from 12.67 mb/d in June, reaching the lowest monthly total in 2023. Refiners even had to dip into their crude reserves in July to meet demand, a first in 33 months.

As manufacturing is also facing headwinds elsewhere in the world, the increase in demand for oil has been largely driven by a surge in international travel so far for the year.

Bottom line…

Faced with continued high economic uncertainty and rising interest rates threatening global growth, particularly in manufacturing and the Chinese economy, major OPEC+ members have announced further production and export cuts.

Prices of the main crude oil benchmarks rebounded over the summer and could continue to rise over the remainder of the year. Higher prices could stymie inflation-fighting efforts by central banks around the world.

Bank of Canada keeps key interest rate at 5.0%

The Bank of Canada decided to maintain the status quo at its September meeting. The key rate therefore remains at 5.0%. Signs of improving inflation and negative economic growth in the second quarter were enough to convince Canada's central bank that credit conditions did not need to be tightened further. This new pause will reduce uncertainty and should lead to a certain revival in business and consumer confidence. If the inflation trend continues downward, the next change in monetary policy will likely be a rate cut, as the economic slowdown has already set in over the second trimester. However, rates will not get lower until 2024.

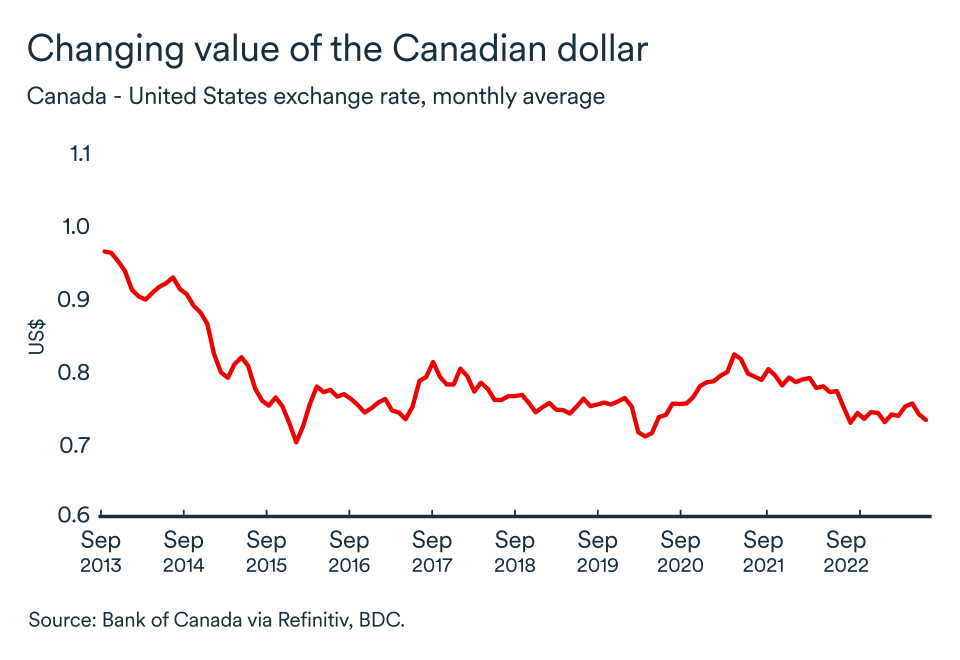

The loonie is trading lower

The Canadian dollar has depreciated over the summer, averaging US$0.74 in August and reached as low as US$0.73 in early September. This slump of the Canadian currency against the U.S. greenback is explained in part by the interest rate differential between the two nations. The Canadian outlook as turn gloomier recently when GDP posted negative growth over Q2 contrary to the U.S. who is still growing at potential. The Canadian dollar is likely to remain in this range over the coming weeks, and may appreciate slightly as oil prices increase.

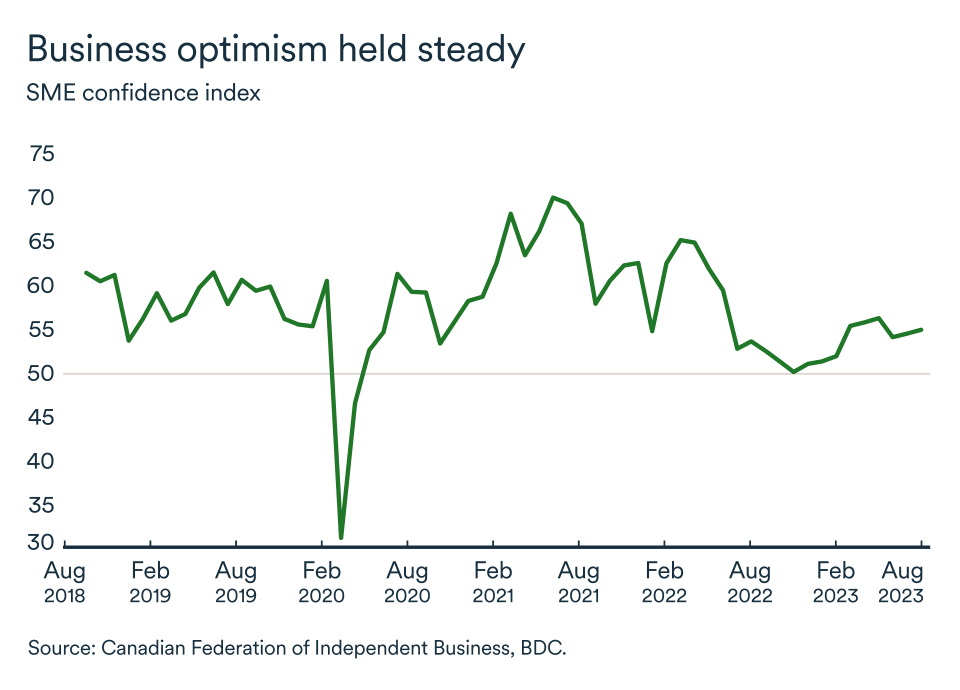

Business confidence is stalling

In July, CFIB's business confidence index for the coming year remained fairly steady. The index remains above the critical 50 mark. Moreover it increased marginally from 54.4 to 54.9 in August. Businesses remain on edge, but the Bank of Canada’s decision to stay on the sideline in September will likely bring less uncertainty and hopefully lowered fears of a more pronounced slowdown. An indicator at 50 means that as many business managers expect the business environment to worsen as to improve over the next 12 months.