Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreWill businesses finally get a break from labour shortages and rising wages?

Some economic indicators suggest that labour market conditions have eased in recent months. If this is the case, it should be easier for businesses to find workers and pressure for higher wages should finally moderate. However, the national unemployment rate has remained stuck at 5.0% for most of 2023—a historically low level. So, are better labour conditions really in the cards for Canadian entrepreneurs?

Is Canada's great labour crunch coming to an end?

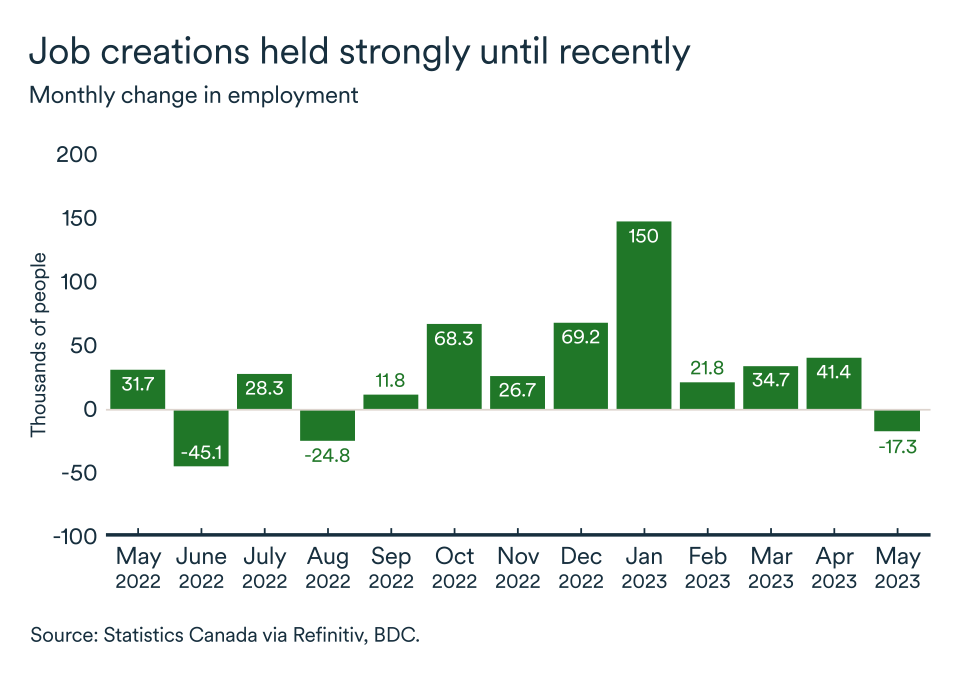

Job creation in Canada continues to be very strong. In the space of a year, 365,000 new jobs were added in the economy while the country's active population of workers—people able and available to work—increased by over 380,000. The result was a low unemployment rate. It hit 5.0% and stayed there in most of 2023. It recently ticked slightly higher in May but remains low by historical standards, at 5.2%.

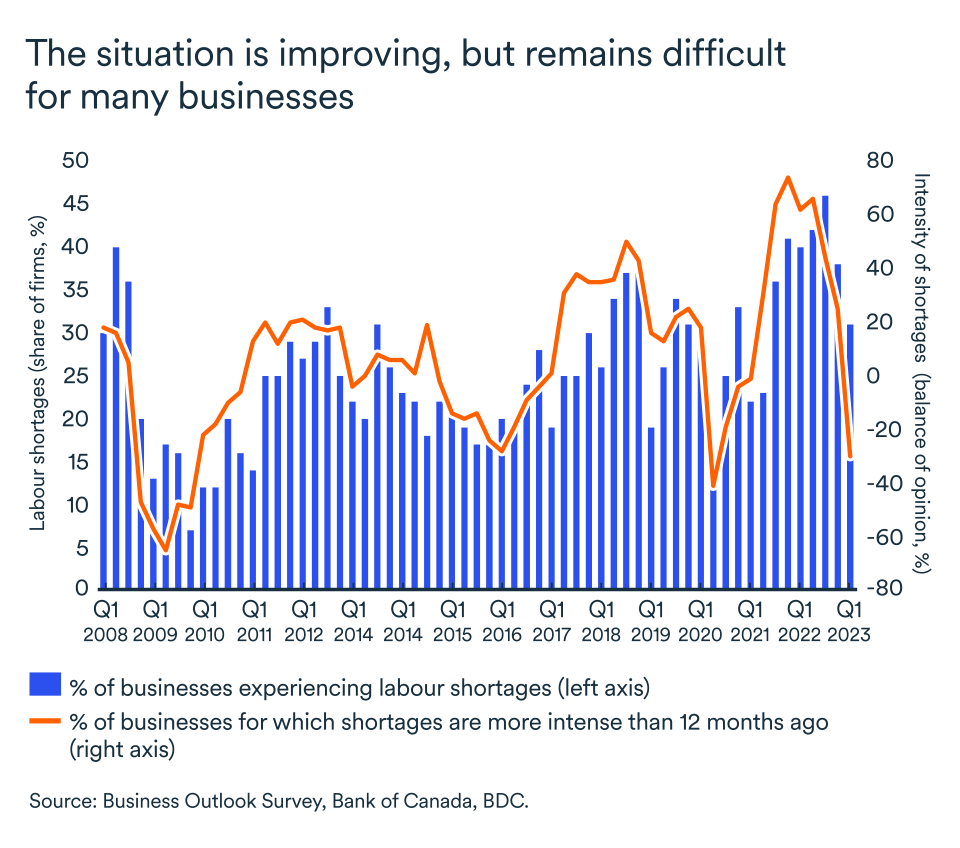

Despite the solid job gains and an increase in the number of potential workers, many companies are still struggling to fill positions. According to the Bank of Canada's latest survey, businesses continue to report labour shortages as the second most important challenge they face, after rising costs.

However, this is the first time in over two years that the labour shortage intensity indicator has been negative. This means that companies consider the current situation to be better than a year ago and that it’s easier to hire the workers they need.

There are other recent signs indicating the labour market is loosening up. For example, job vacancies have fallen by around 20% since last spring. Regardless, openings remain significantly high and nearly three out of five small and medium-sized businesses said in a recent BDC survey that they were still having difficulty hiring skilled workers.

This mixed picture suggests the labour situation has improved but remains challenging for many companies.

Can record population growth help?

In the first quarter of the year, Canada's population grew at its fastest rate ever and, in the fall, Ottawa announced new immigration targets that would see the country welcome 500,000 immigrants a year by 2025. This will no doubt help companies find workers, but the situation is more complex than it appears.

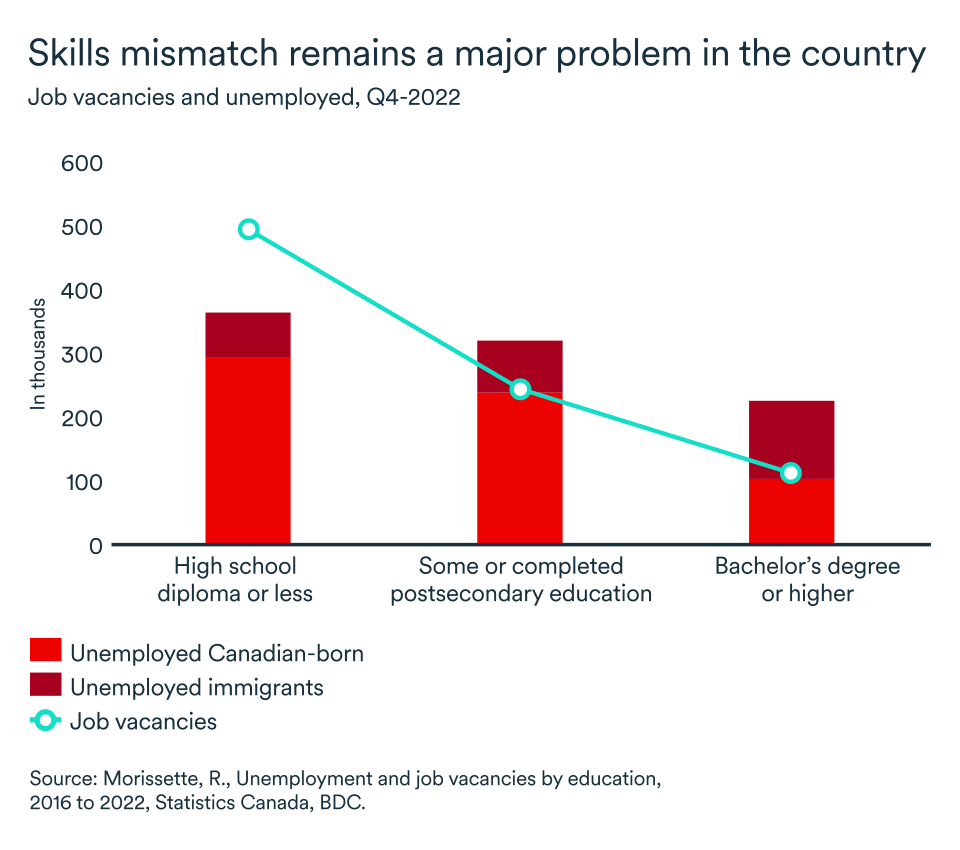

According to a recent Statistics Canada report, labour shortages vary widely according to the level of education or skill required for the job.

For jobs requiring higher education levels, there seems to be an ample supply of workers. Of course, not all diploma and training are equivalent on the job market and therefore do not meet the same needs. However, the situation is reversed for low-skill jobs. Here, there are far fewer unemployed people than vacancies for jobs that require a high school diploma or less. Indeed, even if all the available workers in that category had been instantly hired in the fourth quarter of 2022, there still would have been over 130,000 vacancies.

In the fourth quarter of 2022, 497,000 job vacancies required a high school diploma or less, but only 70,000 unemployed immigrants had this level of education. Meanwhile, job vacancies requiring a university degree numbered 113,000—10,000 fewer than the number of unemployed immigrants with these qualifications.

Geographical factors or working conditions partly explain the shortage, but the figures nevertheless show an imbalance between the skills of available workers and market needs in the country.

Is raising wages a solution?

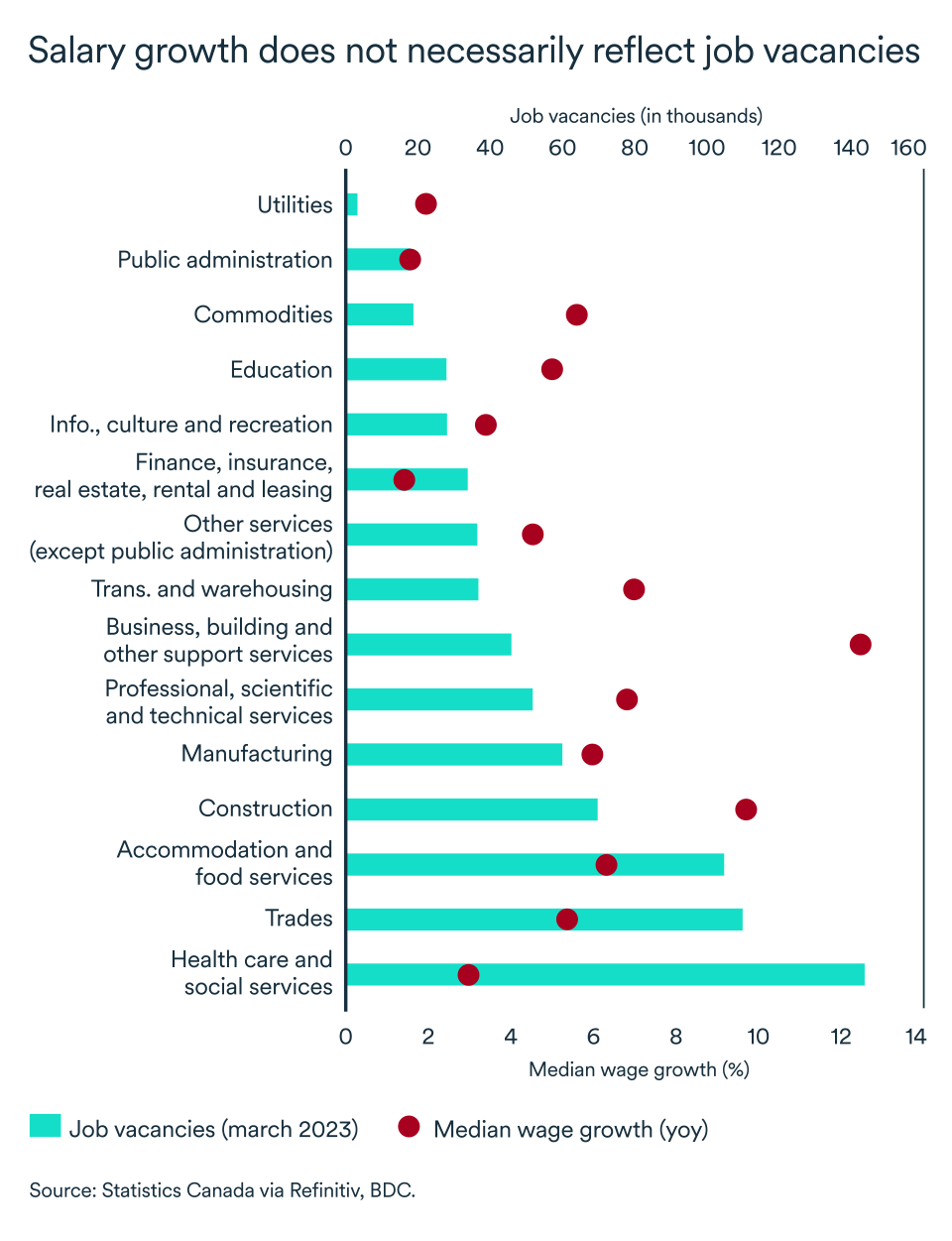

While wage growth in Canada was tepid before the pandemic, many companies have boosted salaries since the economy reopened to remain competitive in recruiting workers. The latest national employment report showed that the national average hourly wage rose by 5.1% year-over-year in May.

Going forward, companies that are losing experienced workers to retirement, or whose training and recruitment costs are high, may want to continue offering larger compensation packages to find the right workers for their long-term needs.

However, for businesses whose workforce is less specialized or prone to high turnover, further wage increases could add undue cost pressure in an uncertain economic context.

Overall, although there is some easing of labour market pressures, it is still not a generalized situation. The sector of activity and the skill requirements of each businesses will have a greater impact on the best suited strategy to help mitigate labour issues—including salary increases.

What does this mean for your business?

- The labour problems companies have been facing for the past few years will not go away entirely but the situation seems less alarming. The forecasted economic slowdown should help lift off some of the wage pressure you have been facing recently.

- While uncertainty remain high, not all sectors or regions are facing the same hiring challenges. Try to anticipate workforce issues specific to your business and prepare accordingly. For example, Technology investments can help you automate tasks, but you'll probably need a specific type of worker to operate the systems and this kind of transition takes time.

- Raising wages may be a short-term solution, but managing operating costs is already a challenge for many companies today. A good response is to improve your operational efficiency to reduce costs and maximize profits

What does Canada's latest interest rate hike mean?

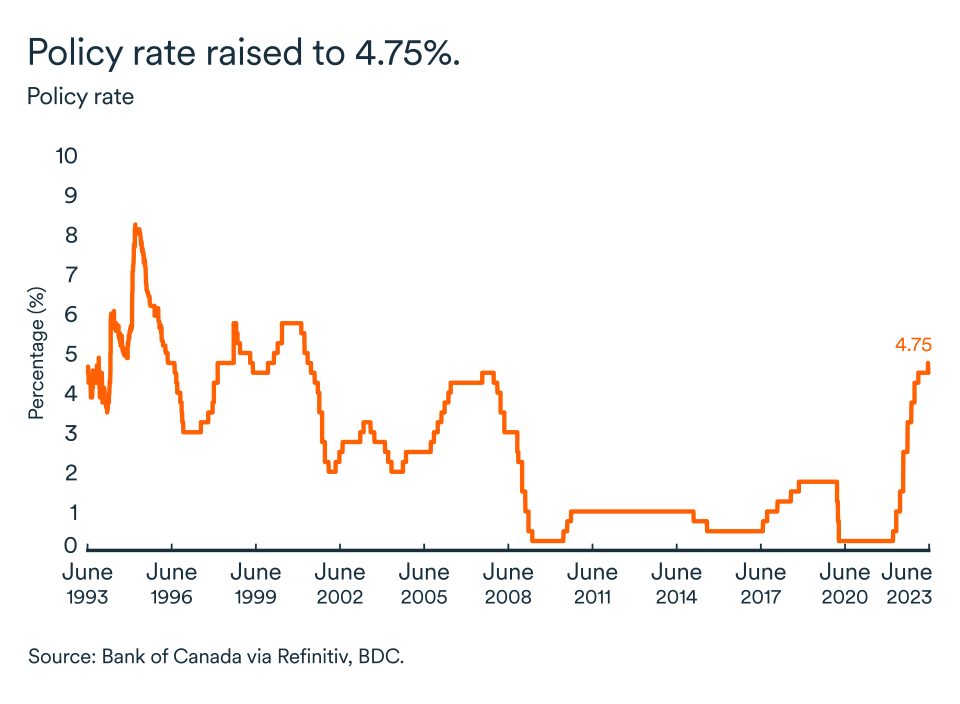

The Bank of Canada made a significant course correction when it raised its policy rate earlier this month to 4.75%, the highest it’s been in 22 years.

The 0.25% increase was a departure from Governor Tiff Macklem’s statement on January 26 when he said the bank was pausing its monetary policy tightening. That announcement had been eagerly awaited by Canadian households and businesses struggling with higher rates.

Now, the rate pause appears to have been premature. At least, that's what the state of the Canadian economy in the first quarter of 2023 suggests.

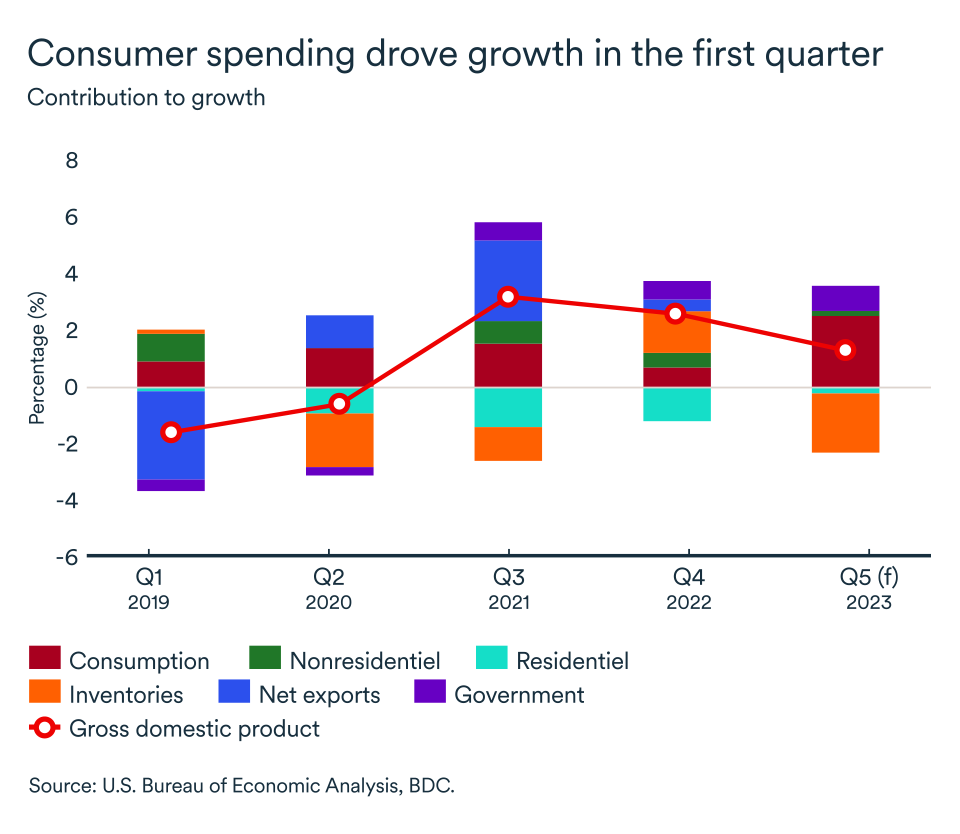

Surprisingly strong real GDP growth

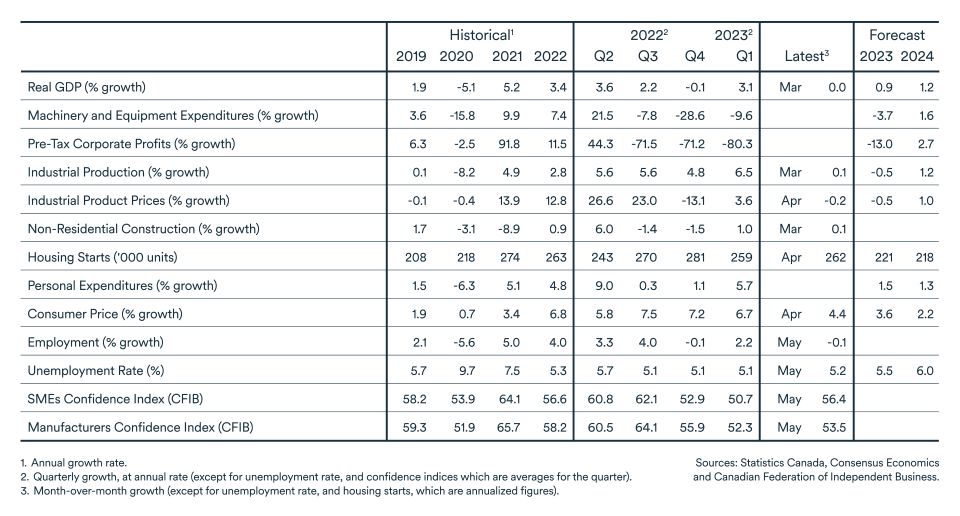

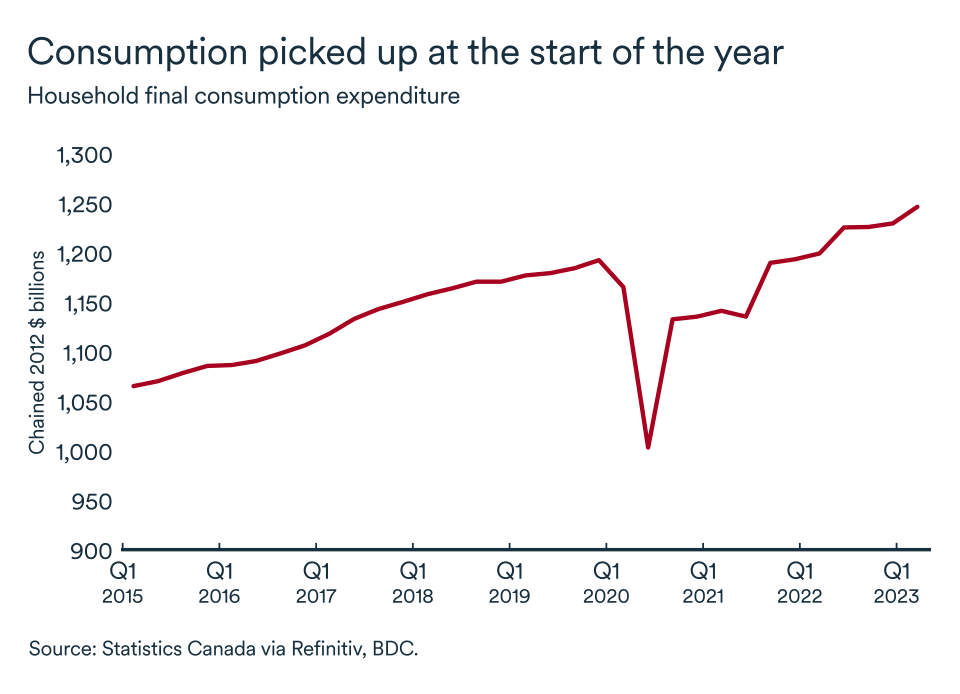

Real GDP, which measures economic activity net of inflation, grew at an annualized rate of 3.1% in the first quarter of the year, well above the Bank of Canada's estimate of 2.3%. It was the fastest quarterly growth recorded in the country since the second quarter of 2022, when many industries were recovering from the virulent COVID-19 Omicron outbreak.

Economic activity stagnated in March, but growth picked up again in April to 0.2%, according to Statistics Canada’s preliminary estimates. With rates set to remain high for some time to come, Canadian households appear to be getting used to the new reality and have adjusted their budgets accordingly.

Economic growth in March came mainly from the mining, oil and gas industry, where production picked up following unforeseen production issues in February. Manufacturing, which is closely linked to goods consumption, slowed, as did consumer discretionary service sectors (accommodation, restaurants and retail) over the same period.

Even so, consumer spending grew at a brisk 5.7% in the first quarter, a clear sign that domestic demand remains very strong in this country. In its statement accompanying this month’s rate hike, the Bank of Canada said “excess demand in the economy looks more persistent than anticipated.”

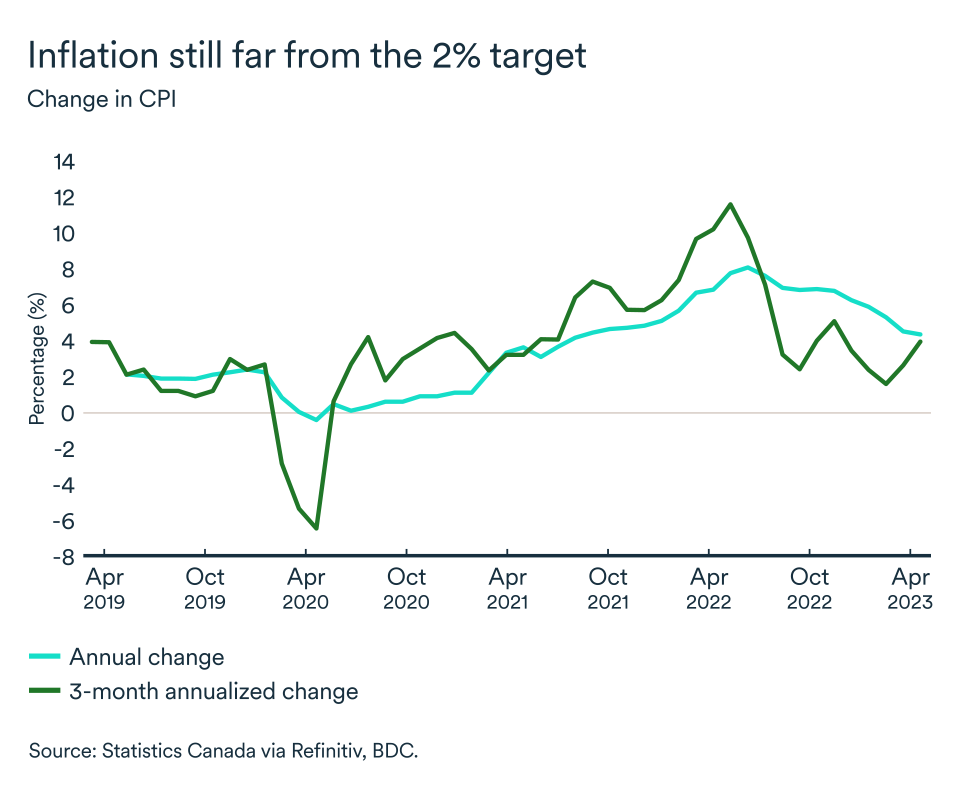

Inflation remains a concern

In April, inflation measured by the annual change in the consumer price index (CPI) rose marginally to 4.4% from 4.3% in March. Although the rise was modest, it represented an acceleration in the country's price growth, which moved away from the bank’s 2% target for the first time since June 2022.

Nevertheless, Canada's central bank tends to prefer core inflation measures to assess the underlying trend in inflation, rather than the more volatile headline CPI. In year-on-year terms, all three measures of core inflation were down in April.

On a month-over-month basis, two of three measures of core inflation that are closely monitored by the Bank of Canada rose in April. The house price index also started to rise again as some buyers return to the market to take advantage of price decline and the stabilization of rates.

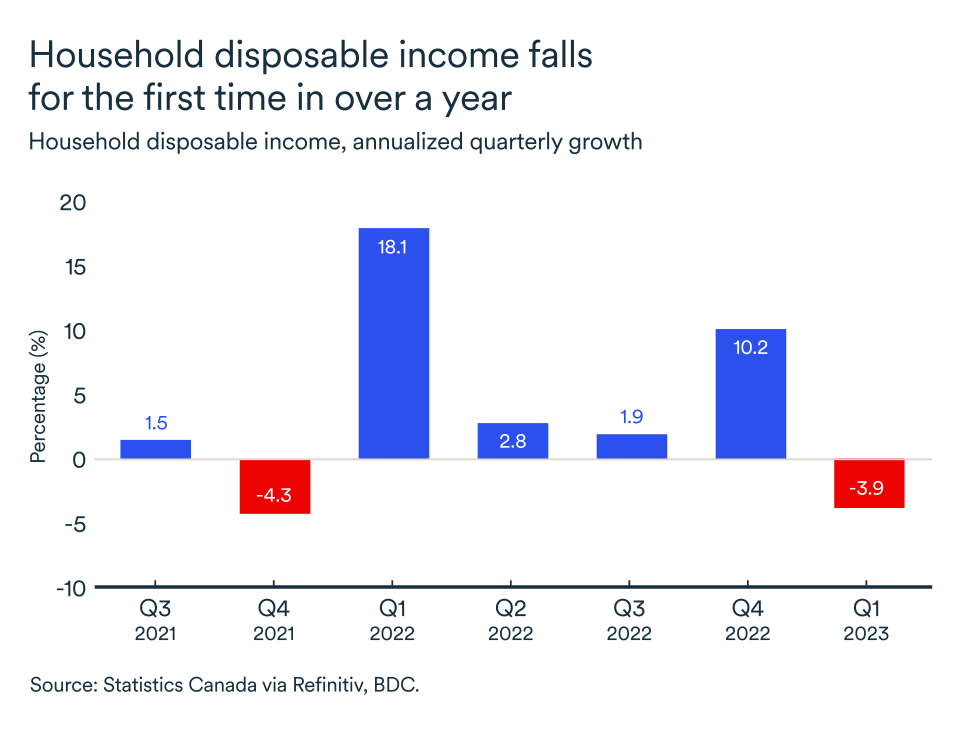

Less money to spend

Nevertheless, there are signs of an economic slowdown in the making, which will probably give the Bank of Canada some support in its fight against inflation.

During the pandemic, households benefitted from a significant increase in disposable income. Despite the strength of the labour market at the start of the year, employment decreased for the first time since September (although marginally). Moreover, disposable income for Canadian households fell by almost 4% (on an annualized basis). This was the first quarterly decline since the end of 2021. The savings rate has also fallen and is now closer to pre-pandemic levels.

Moreover, in the face of rising costs, business revenues continue to slow (-2.2% in the first quarter of 2023).

What does this mean for entrepreneurs?

- The pause in interest rates seems to have given consumers time to adjust to higher debt servicing costs and increase their spending. The Bank of Canada may raise rates again as early as July, rekindling uncertainty and caution among consumers.

- Improved growth in Canada means that higher interest rates are likely to prevail for longer, which will keep up the pressure on business costs. Find out how to manage your costs more effectively in BDC's latest study.

The Fed holds rates steady but remains under pressure

Uncertainty seems to have eased somewhat over the past month in the United States. There were no new bank failures, and a bipartisan agreement was reached in Congress to resolve the latest debt ceiling crisis. Nevertheless, the Federal Reserve remains on its toes when it comes to the state of the economy and especially where inflation is headed.

Second-quarter real GDP growth was revised slightly upwards to an annualized rate of 1.3%. Compared with the fourth quarter of 2022, this represents a significant deceleration in the pace of growth.

The slowdown was due mainly to a decline in investment in inventories and non-residential assets. It was, therefore, more evident among businesses than consumers, where demand remained strong despite higher interest rates.

Last-minute agreement on debt ceiling

To no one's surprise, the parties agreed on a bill to raise the debt ceiling. Although the agreement also limits spending and is therefore a brake on President Biden's fiscal policies, the macroeconomic impact of government spending will remain positive in 2024, just by less than initially expected.

Consumption continues to grow despite pessimism

After consumer confidence reached its lowest level in six months in April, pessimism was still being felt in May, according to the Conference Board's Consumer Confidence Index. The index was essentially unchanged in May, but remains lower than in the same period last year.

Americans' assessment of the labour market darkened, but a large proportion of households still plan to make major purchases in the next six months, such as buying a motor vehicle.

Consumer spending was revised slightly upwards in GDP estimates for the second quarter (+1.3% annualized vs. Q1 2023). It remains to be seen, however, whether the expected rise in household spending actually materializes.

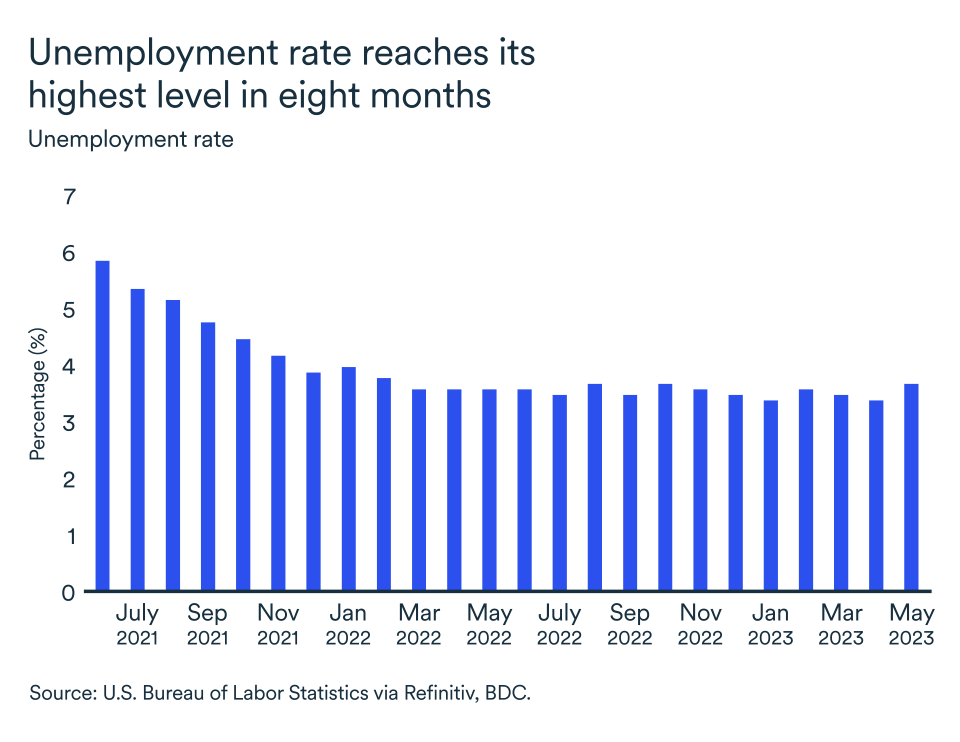

The job market remains strong

The unemployment rate rose to 3.7% in May, 0.3 points above April's level. Nevertheless, the economy added 339,000 jobs in May, according to the Bureau of Labor Statistics’ business survey, marking yet another month above expectations.

However, the Bureau’s household survey indicated that employment actually fell in May by 310,000 jobs. This is not the first time there’s been this kind of discrepancy between the two data sets. Employment measured by the household survey is typically more volatile. In fact, the May report points out that much of the decline found in the household survey was due to a reduction in self-employment.

All in all, the job market is showing signs of slowing, but the economy will have to gear down further for real signs of easing to appear. Average hourly earnings continue to climb, coming in at 4.3% year-over-year in May compared to 4.4% in April. In addition, job vacancies hit 10.1 million.

Inflation remains too high

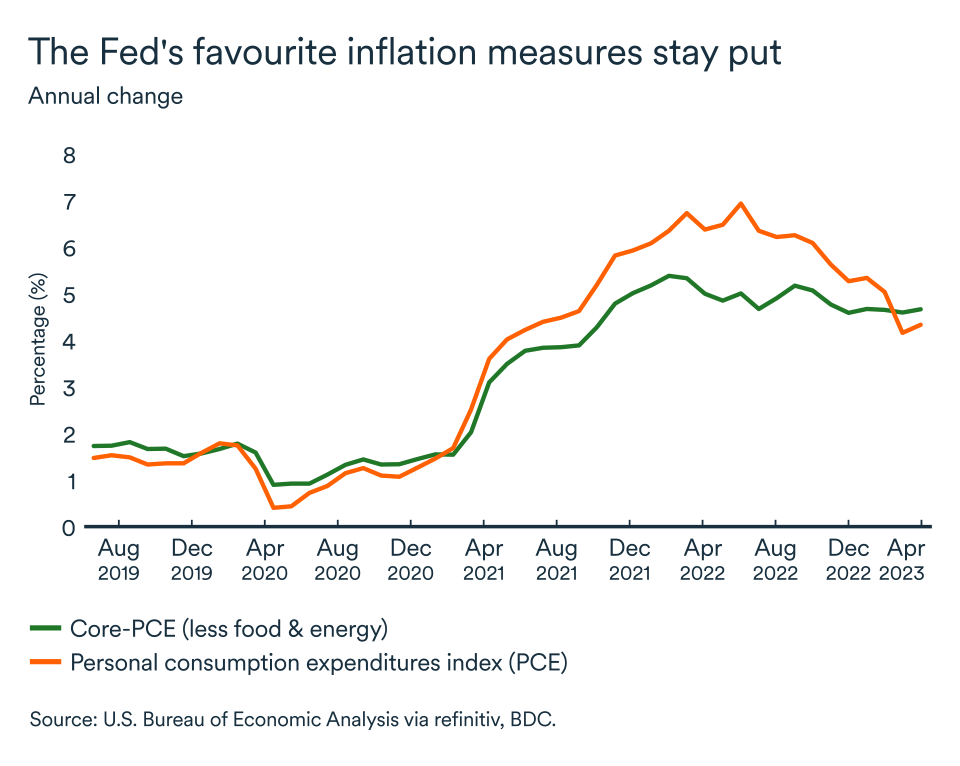

The tight labour market and wage growth kept the pressure on prices south of the border. Inflation measured by the personal expenditure (PCE) index for April was 4.4% overall and 4.7% excluding food and energy. Both measures were slightly higher than in March. On a more positive note, the Consumer Price Index (CPI) increased at a pace of 4% in May, quite down from the 4.9% of April.

The Federal Reserve generally gives greater weight to inflation as measured by the Personal Consumption Expenditure Index (PCE) than the Consumer Price Index (CPI). Moreover, Fed Chairman Jerome Powell has placed a great deal of emphasis on three specific inflation categories in his speeches in recent months: core goods inflation, core services inflation related to housing and core services inflation excluding housing.

While the first indicator shows clear signs of improvement, services inflation measures have been less responsive to monetary tightening because they are more sensitive to the labour market. Still, the Fed sets rates based on where it expects inflation is heading, not where it is now.

In the end, the Fed decided to stay on the sidelines for its June announcement, but the likelihood of at least on more rate hike still looms over the American economy.

The impact on your business

- Stable interest rates in the U.S. and a strengthening Canadian economy could lead to an appreciation of the Canadian dollar. However, the Canadian dollar remains weak for now, making the current context attractive for exports.

- Despite the recent turbulence, the U.S. economy remains strong and offers opportunities for Canadian exporters, particularly in the consumer sector, where many Americans are still planning to increase their spending in the coming months.

- Exporters of building materials, including lumber, have been struggling in the U.S. of late, as the housing market has slowed in response to higher interest rates. June's announcement to keep rates at the status quo bodes well for a slight revival in those markets.

Supply will be more constrained in the second half of the year

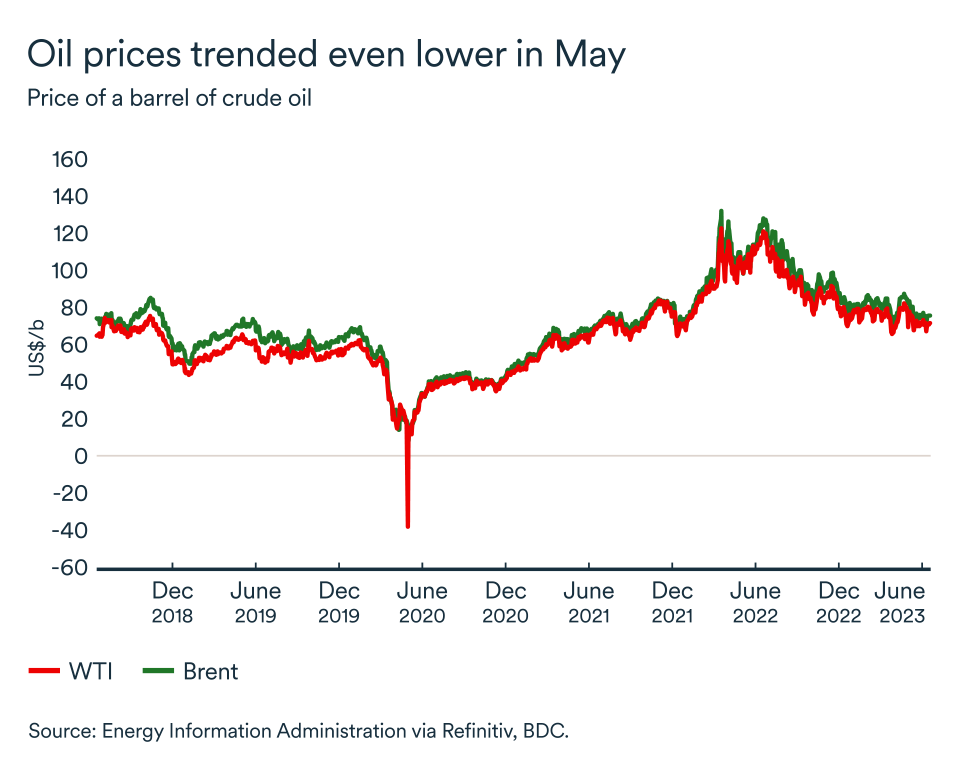

Prices for the main crude oil benchmarks fell in May with Brent averaging US$75 and WTI hovering near US$70. The Organization of the Petroleum Exporting Countries and its allies (OPEC+) opted not to further cut production at a June 5 meeting.

However, the member countries agreed to continue limiting oil supply to the market at the rate imposed almost a year ago. The exception is Saudi Arabia, which has committed to a voluntary production cut of 1 million barrels a day in July. This voluntary reduction is hardly surprising, given current price levels and the fact that Saudi Arabia needs a barrel to be at least US$80 to balance its budget.

OPEC+ maintains production target

The cartel has also agreed to maintain its current production target for 2024. The only change, other than the Saudi Arabia cut, will be the distribution of production limits between countries.

Since some African countries are already struggling to produce at their target levels, other members such as the United Arab Emirates, will be able to increase their supply to compensate, which should be enough to entice them to stay in the cartel.

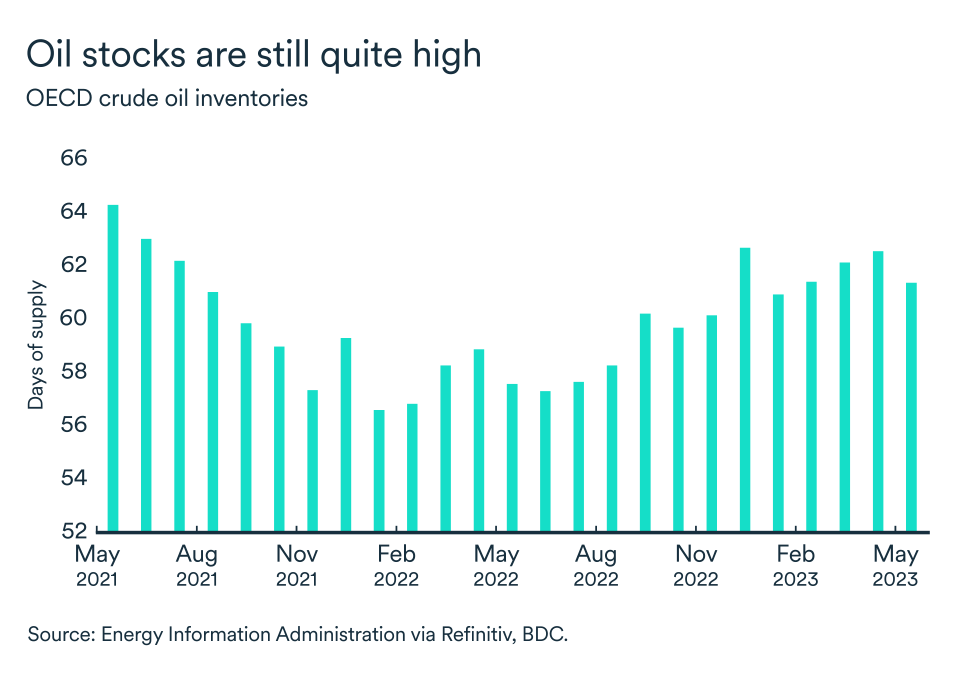

Crude oil prices are therefore set to rise in the second half of the year, but increases will likely be moderate. Inventories in OECD countries are still historically high.

For the moment, the world economy is well supplied

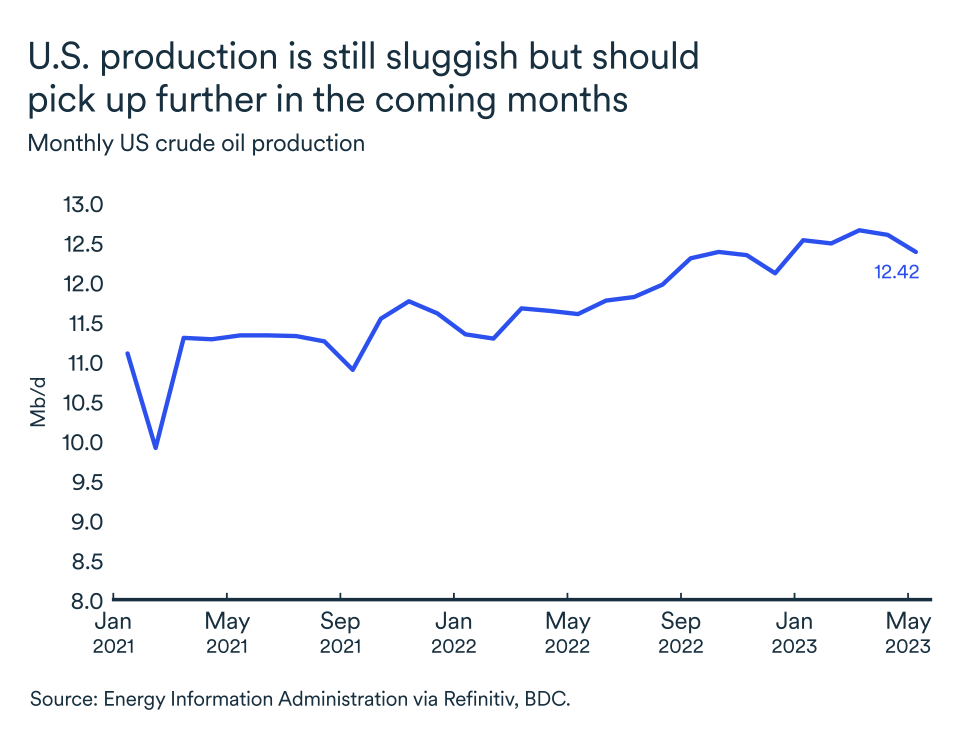

U.S. crude oil production is set to rise to 12.6 million barrels per day, according to the U.S. Energy Information Administration, an increase of 720,000 barrels per day. It remains to be seen whether this prediction will come to pass as U.S. production has yet to return to pre-pandemic levels.

Unsurprisingly, there was no discussion of the strategic winds buffeting the global oil market at the OPEC meeting. With Russian oil under embargo in Europe, U.S. exports of distillate petroleum products to Europe reached their highest level in over three years in May. The U.S. is, therefore, redirecting part of exports usually destined for Brazil to Europe, as Brazil is now getting supplies from Russia at a discount.

Elsewhere, China refined a record amount of crude oil in the first quarter of this year, with around 90% of production used domestically and the remainder exported.

Bottom line…

The extension of production restrictions by OPEC and its allies should lead to a modest increase in crude prices in the second half of the year. Saudi Arabia's additional self-imposed restrictions from July onwards could have a greater impact on the market if they continue. On the other hand, the Americans could start to increase production further and OECD inventories are still well stocked.

The Bank of Canada raises its key rate in June and will follow suit in July

The Bank of Canada raised its key rate by 25 basis points to 4.75% at its June meeting. The Canadian key rate had been at 4.5% since the end of January 2023. Canadian economic activity proved too strong in the first quarter of the year, despite past interest rate hikes. The job market continues to perform well, and inflation remains stubbornly high. It is therefore highly likely that the Bank of Canada will have to raise interest rates once again in July. The rate is now expected to peak at 5.0% this year, but more economic indicators will have to slow down to get there.

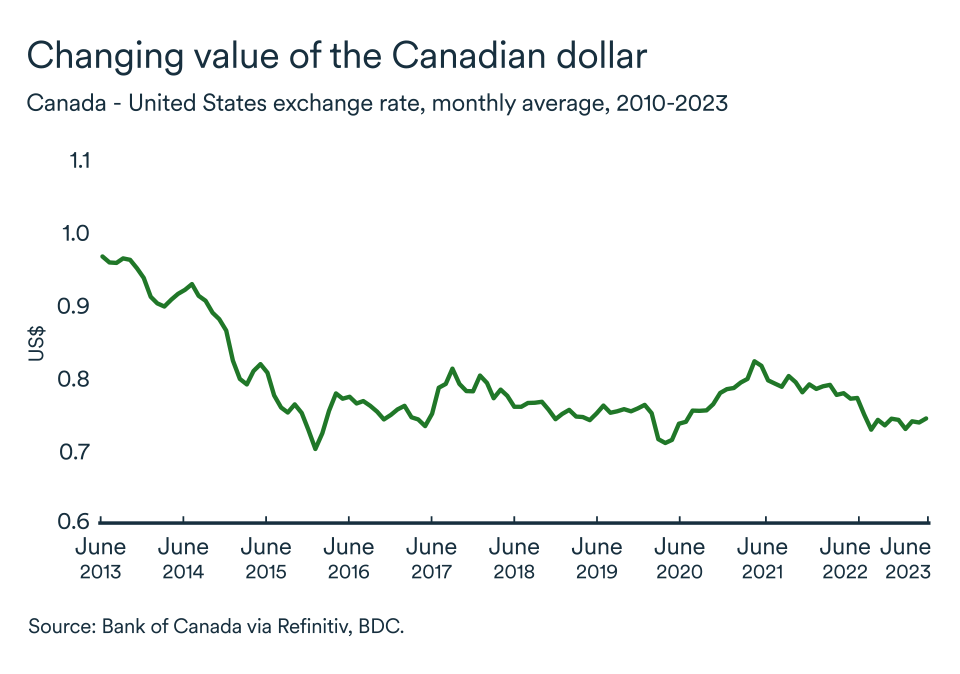

The loonie regains some lost feathers

The Canadian dollar averaged US$0.74 in April and May. However, ever since the Bank of Canada latest rate hike in early June, the Canadian currency has appreciated to US$0.75—its highest level since February 2023. The Canadian dollar should remain within this range over the next few weeks, or even appreciate slightly further. The interest rate differential between Canada and the U.S. should narrow, supporting an increase Canada’s exchange rate against the greenback.

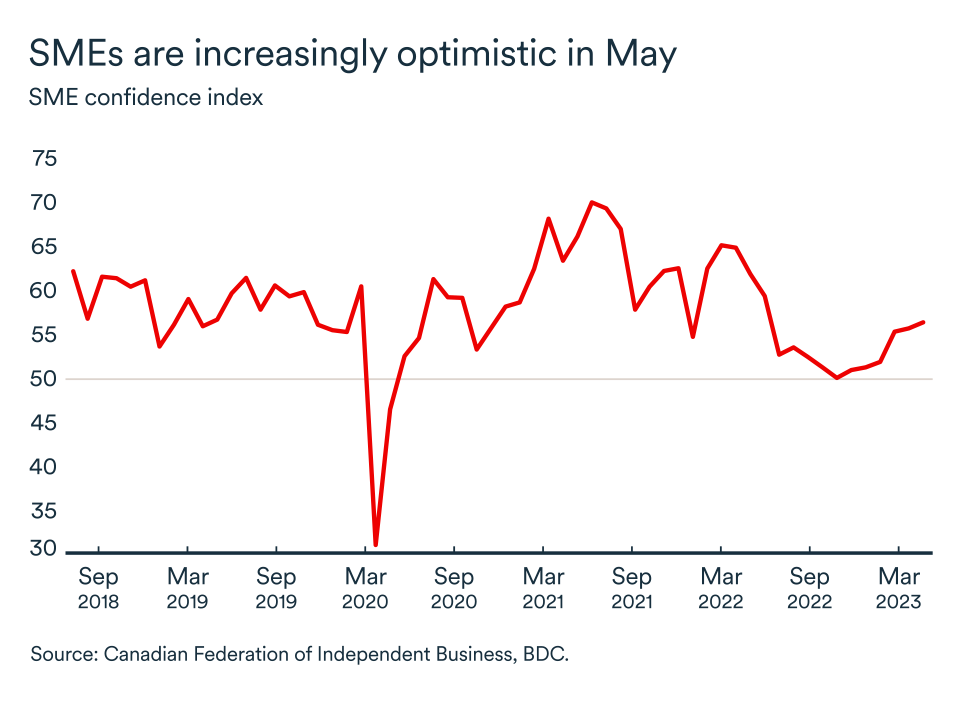

Optimism on the rise among businesses in May

In May, CFIB's business confidence index for the coming year rose again slightly, from 55.7 to 56.4. Businesses are still on edge, but the index continues to move in the right direction. The various confidence indices could, however, turn around as early as June, following the Bank of Canada's announcement to raise interest rates further.

An indicator of 50 means that as many business managers expect the business environment to worsen as those who expect it to improve over the next 12 months.