Monthly Economic Letter

Keep abreast of key economic indicators.

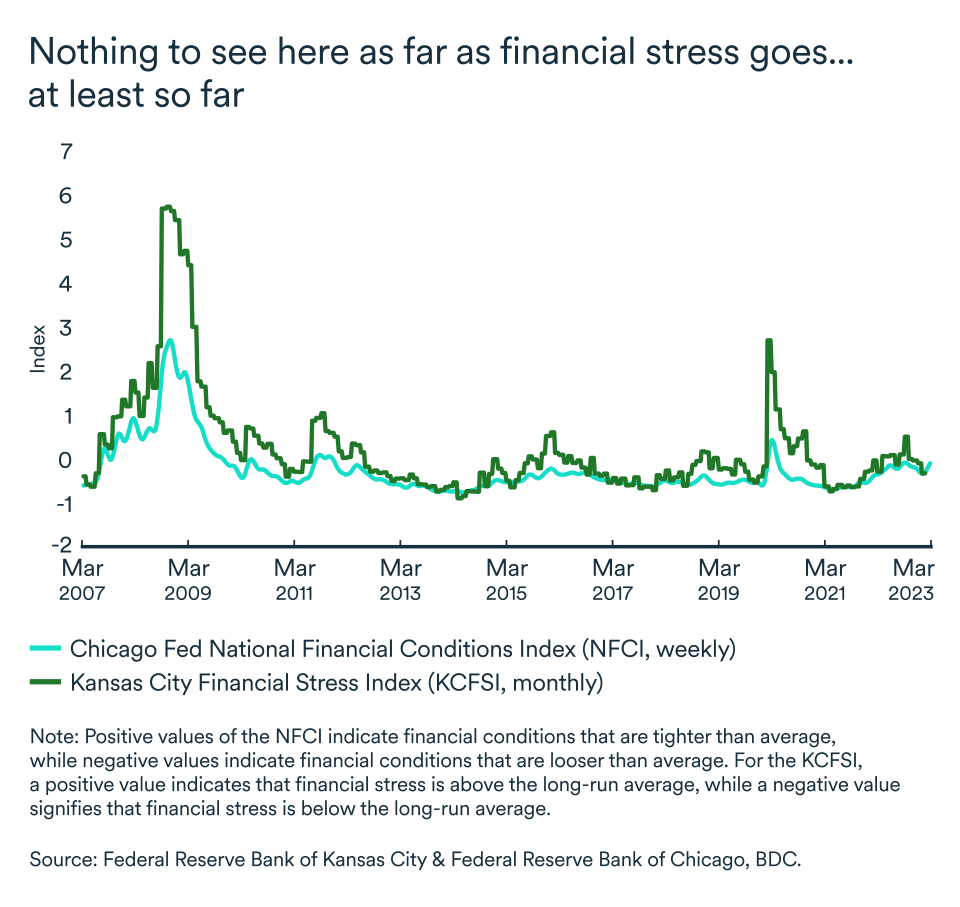

Read moreCould U.S. banking turmoil turn into a financial crisis?

In recent weeks, the failure of a pair of U.S. banks has raised concerns about the stability of the global financial system in the face of fast rising interest rates. The U.S. situation has calmed in recent weeks, but risks remain. While the Canadian system is solid thanks to its different structure and regulatory framework, a deterioration in the U.S. would obviously have a significant impact on the Canadian economy. What are the risks surrounding the banking system and what does it mean for your business?

The largest bank failure in the United States since 2008

U.S. authorities had to intervene in mid-March following the extraordinarily rapid collapse of Silicon Valley Bank (SVB). On March 10, 2023, the SVB, an important bank for American technology businesses, was unable to find new financing to meet its obligations, pushing it into bankruptcy. The news sent shockwaves through the markets, where memories of the 2008 financial crisis still linger.

Probably with the disasters of 2008 in mind, the U.S. authorities reacted quickly. The Federal Deposit Insurance Corporation (FDIC) announced that insured deposits would be available the next working day. However, the majority of SVB's deposits were uninsured due to the nature of their operations.

Shortly after, New York-based Signature Regional Bank also collapsed. To reassure depositors, and in an attempt to limit the contagion, the FDIC and other regulators announced that all deposits (insured or not) would be protected at both banks.

At the same time, Treasury Secretary Janet Yellen and the Federal Reserve announced a new measure to support failing financial institutions. The new Bank Term Funding Program (BTFP) is a 12-month loan that provides an additional source of liquidity for financial institutions.

Was crisis averted?

Calm seems to have returned, but there are risks that will need to be monitored closely to avoid a new outbreak of banking instability.

The biggest economic risk is a climate of fear that’s taken hold in the world since the bank collapses in March. The balance sheets of banks, large and small, have been put under a microscope by investors and depositors.

As a result, lenders with highly specialized clients could come under pressure, and the likelihood of other smaller financial institutions defaulting remains a threat. But the risks of broader contagion are limited for now.

Banks that are more diversified, whether in terms of business lines, customer base or geography, are better protected against deposit flight. The current issues facing banks are linked to faulty risk management and not generalized weakness in the system. However, unlike previous financial shocks (1980-86, 2001, and even 2007-09), information flows much faster nowadays and so does money (as transactions can happen in a few clicks). Small difficulties can therefore quickly escalate into big problems for the financial system.

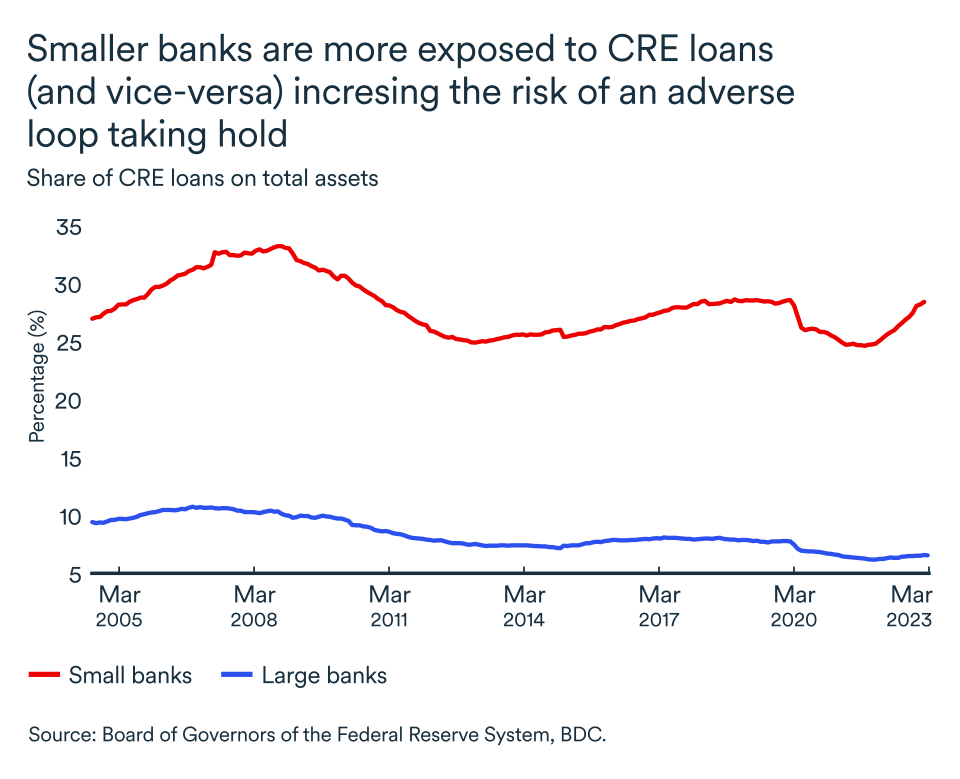

Also, the vulnerability of the U.S. regional banks has highlighted the difficulties of one sector in particular—commercial real estate. It’s no secret that since the pandemic, the commercial real estate industry has suffered, particularly companies leasing office and retail space, due to the popularity of online shopping and telecommuting.

Defaults by commercial real estate owners have been accelerating since the beginning of the year. Small U.S. banks are particularly exposed to the slump.

Small regional banks hold $1.9 trillion in outstanding commercial real estate borrowings compared to only $0.9 trillion for the large national banks. The exposure of small banks to commercial real estate could lead to a spiral of adverse effects and is therefore something to watch closely.

What does this mean for the real economy?

Banking woes in the U.S. and Europe will slow the global economy further in 2023, but we don’t expect a major financial crisis to develop. It’s much easier to contain a crisis you see coming as was the case in the U.S. as well as in Switzerland where Credit Suisse had to submit to a government-engineered takeover by rival UBS.

These developments reflect more a crisis of confidence than a financial crisis at this point. Households and businesses in Canada and the U.S. had already grown cautious about rising interest rates, but now uncertainty, and fears of recession that accompany it, will further constrain the real economy in the coming months.

The events of the last few weeks will naturally lead to tighter credit conditions without central banks having to raise rates. This will slow demand in the economy.

However, market expectations for lower interest rates this year appear premature to us. We now expect rates to remain elevated for longer than we had forecast earlier this year. (For more details, see the article on Canada).

The risk of doing too little to contain inflation is still too great to begin lowering rates, even in the current environment of financial uncertainty. We will need to see more tangible changes in the real economy before the U.S. Federal Reserve and Bank of Canada consider rate cuts.

Restoring depositor and investor confidence in the U.S. financial system is essential to avoid a recession, but getting inflation back on target will remain the priority for central banks.

The impact for your business

- There is no doubt that recent events in the financial markets have increased economic uncertainty and fears of a global recession. Global economic growth is expected to slow further in this climate and so is Canadian domestic demand (although there are no concerns about the strength of the Canadian financial system).

- While central bank rate hikes have likely hit their peak for the year, credit and financing conditions will be more challenging given recent vulnerabilities in financial systems around the world.

- With risks present in both bank balance sheets and commercial real estate, Canadian businesses will want to carefully assess their growth options in a slowing economy.

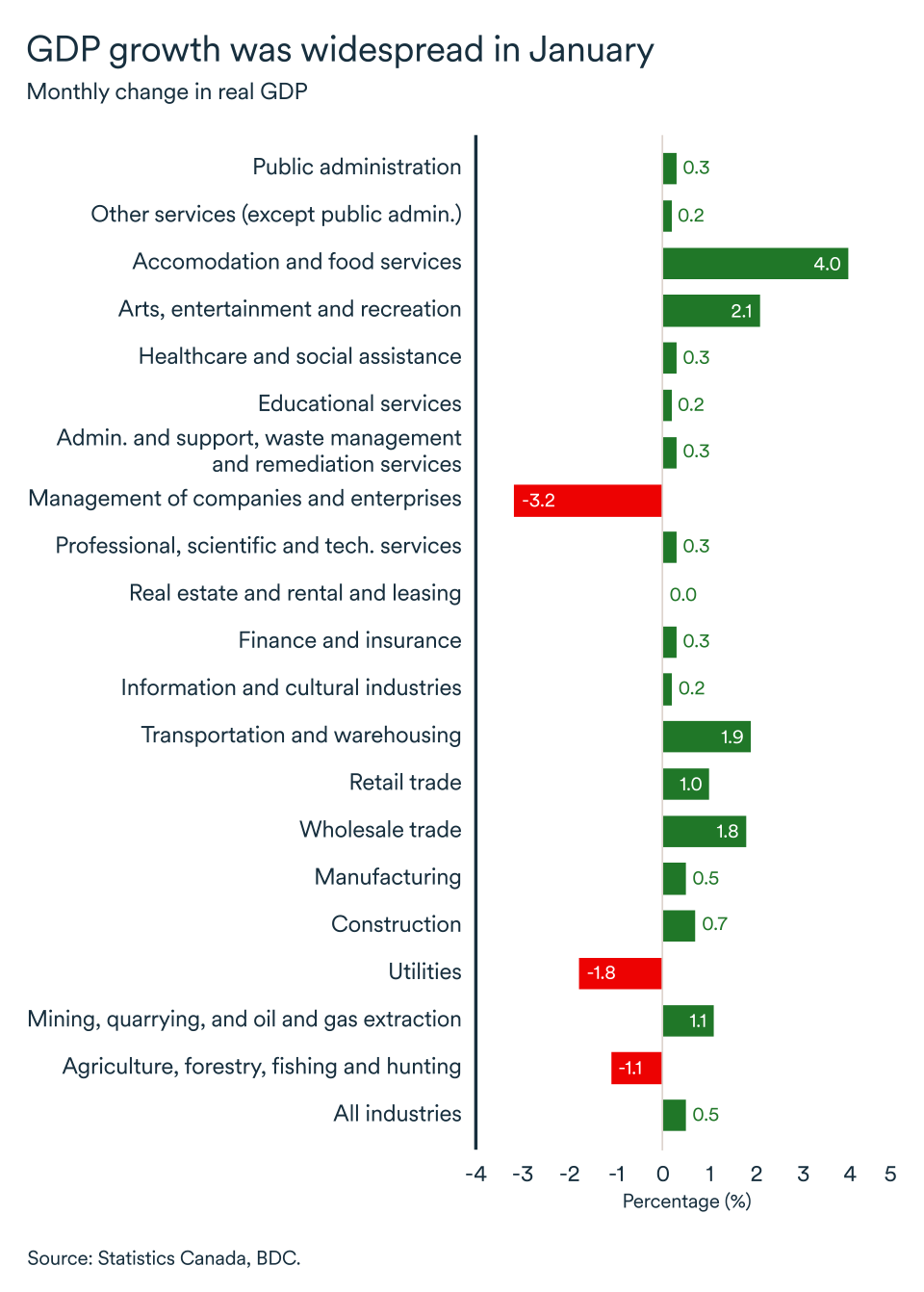

Canada's economy starts the year strongly

Canada's GDP rose a robust 0.5% in January. This is a solid rebound in economic activity from December when real GDP fell by 0.1%. Statistics Canada's preliminary estimates for February also point to significant gains, with monthly growth expected to have reached 0.3%.

January's recovery was broad-based, with gains recorded in 17 of the 20 sectors of the economy. The outlook for GDP growth in the first quarter, therefore, looks healthy and could reach around 2.5% annualized. That’s well ahead of the Bank of Canada 0.5% estimate for the period in its January report.

Canadian interest rates will be high for longer

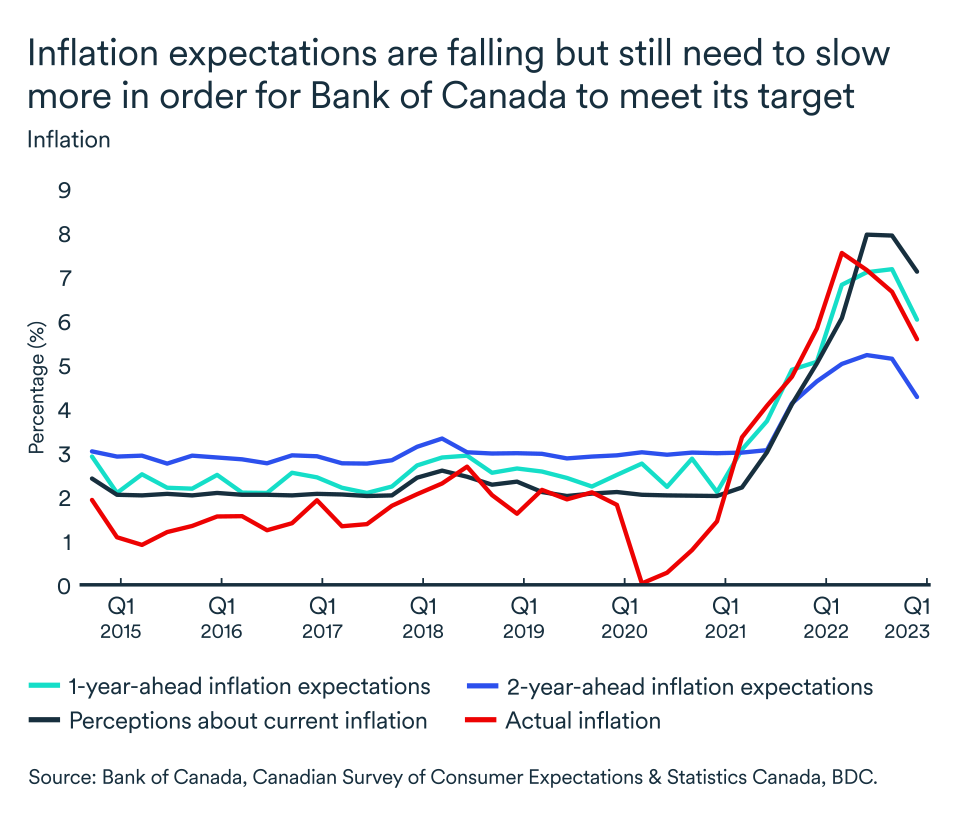

Inflation continued to decline in February to 5.2% from 5.9% in January. Favourable comparisons with a meteoric rise in many commodity prices in the spring of 2022 should push the annual change in the consumer price index down sharply again in March.

However, if the economy's momentum in the first two months of 2023 continues, it may prove more difficult for the Bank of Canada to bring inflation back to target.

At this point, the decline in inflation remains on track and is now expected to reach 3%—the upper limit of the target range—towards the end of the year. Reaching the 2% midpoint will be the real challenge for the Canadian central bank.

According to the latest Bank of Canada survey, consumers' short-term inflation expectations have declined, but remain stubbornly high for now. Canadian household inflation expectations should continue to normalize as actual inflation slows.

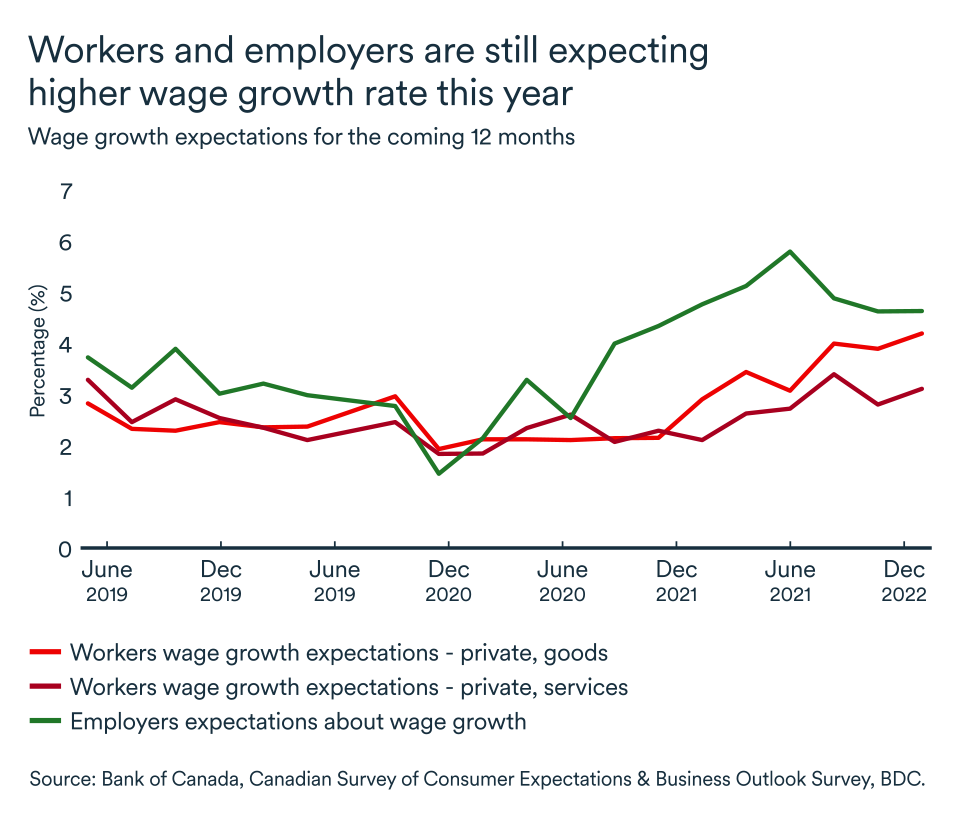

Conversely, high expectations will continue to put upward pressure on wages. On average, businesses are expecting wage increases in the range of 4.7%.

The bank will need to be patient because there’s a significant lag between rate hikes and their effects in the economy. The policy rate should remain at its current level of 4.5% for a little longer than we had estimated at the beginning of the year. We now expect a first rate cut to come in December 2023 or January 2024.

Manufacturing started to contract in March

The economic slowdown is expected to become more evident in the coming months as early indicators for March show signs of easing.

The Purchasing Managers' Index (PMI) for Canadian manufacturing reached its lowest level since June 2020 at 48.6. An index reading below 50 usually indicates a contraction in activity. The production and new orders indices also swung into contraction territory during the month.

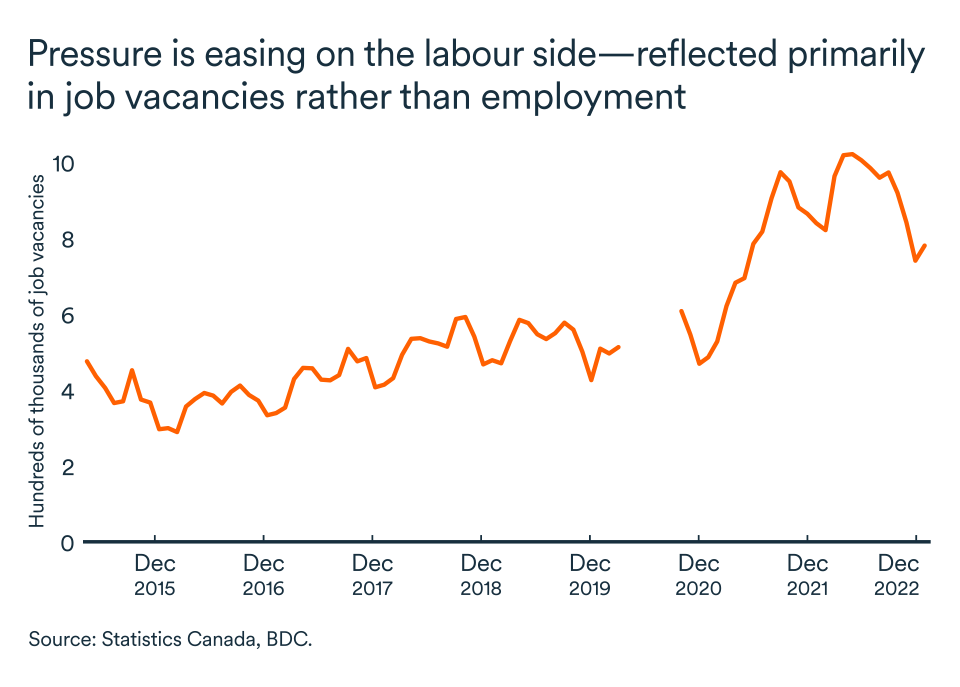

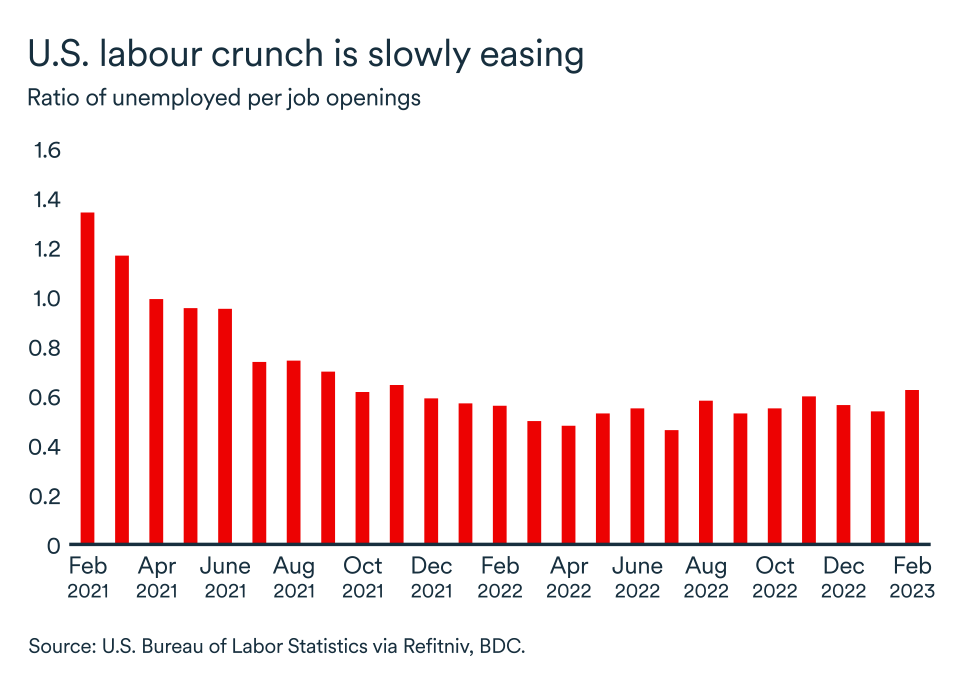

Strong labour market and low unemployment continue

Canada's labour market remains strong but is stabilizing. In March, 35,000 new jobs were created and the unemployment rate remains stable at a low 5.0%.

An expected economic slowdown has yet to appear in the labour market. It’s more likely to be reflected in a decrease in job vacancies than in job losses. Even so, more than half of the companies surveyed by the Bank of Canada in the first quarter of 2023 still intend to increase their workforce in the coming year. A strong labour market will help consumers cope with higher inflation and interest payments.

The impact on your business

- The strength of the Canadian economy continued to surprise in early 2023, but signs of a slowdown are surfacing. Make sure you have a solid plan in place to deal with the headwinds you will face in the coming months.

- So far, the Bank of Canada's monetary policy is having the desired effect of reducing inflation. However, it will take several more months before the full impact of past rate hikes is felt in the economy. Businesses and households will have to be patient in waiting for a rate cut in Canada, as the economy is still going strong.

- Wages will continue to rise at a faster rate in the coming year. If your company is experiencing labour issues and rising costs are holding you back, it may be time to explore new avenues to increase your productivity.

U.S. growth is slowed by tighter credit conditions

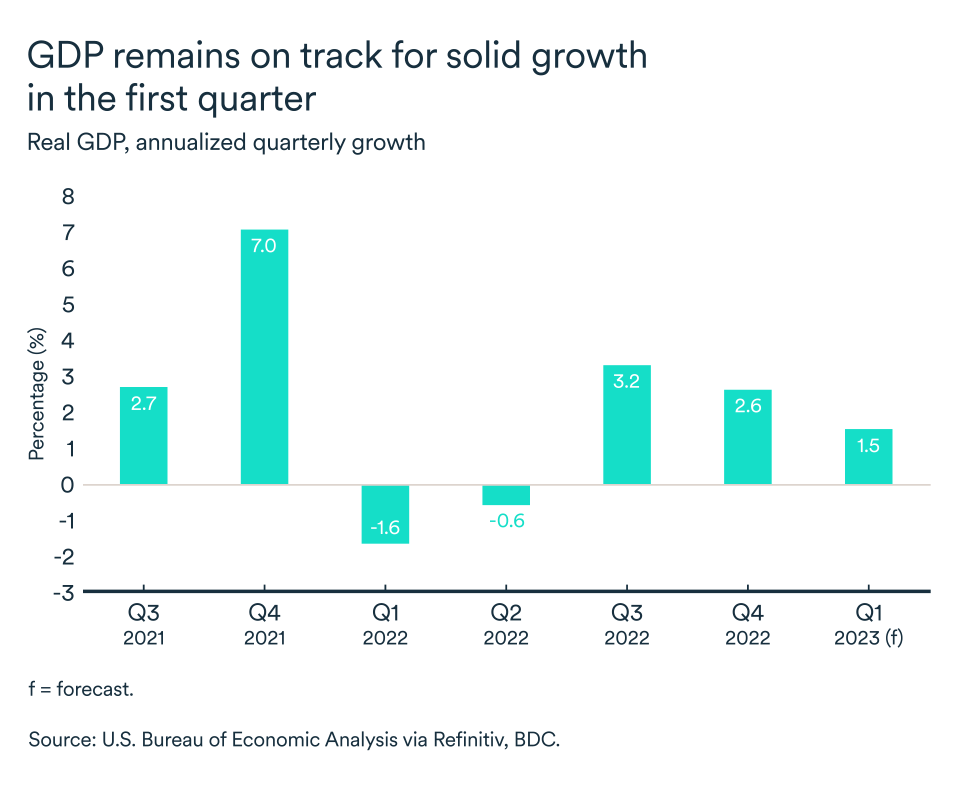

The full impact of recent U.S. bank failures on the real economy is still unknown. However, the good news is that the U.S. economy appeared to be on a solid footing in the first quarter of 2023 and the initial shock of the bank failures seems to have been contained so far.

U.S. GDP growth continually defied expectations during the last months of 2022 (+2.6% annualized growth in Q4). By contrast, growth is expected to slow to between 1.2% and 1.5% in the first quarter of 2023.

Will the Fed raise its rate one last time?

As expected and despite the banking turmoil, the Federal Reserve raised the federal funds rate by 25 basis points in its March announcement, bringing the range to 5.0% - 5.25%.

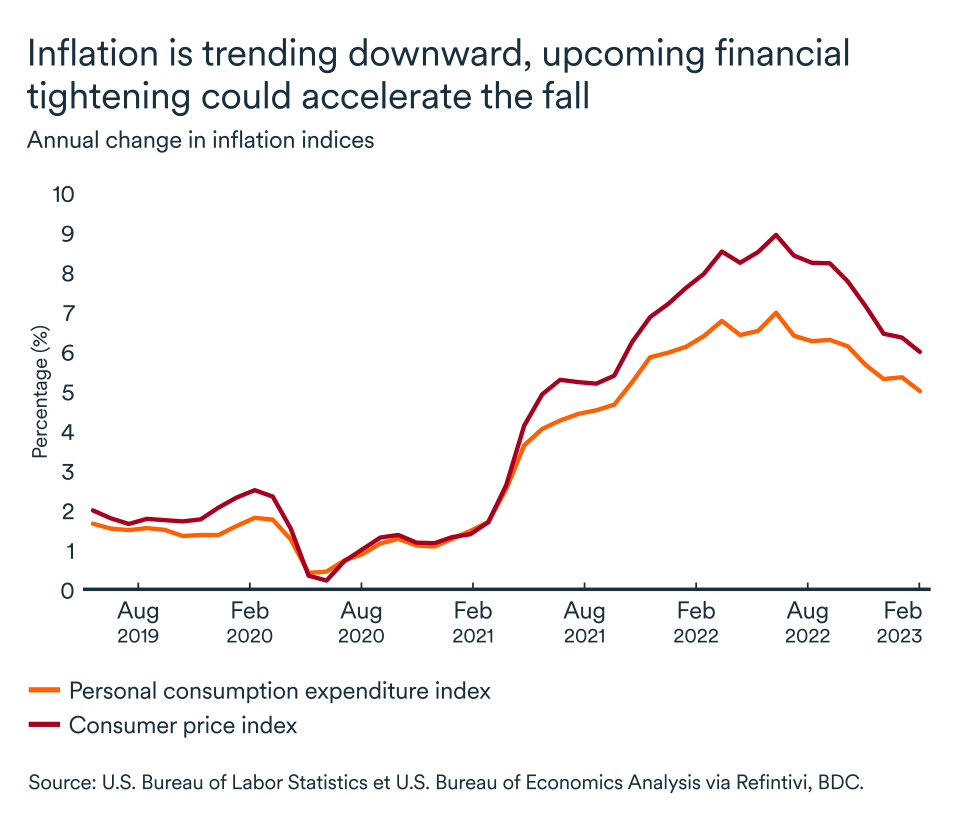

The U.S. central bank is well aware that the U.S. banking system will tighten credit conditions for businesses and households in reaction to the banking situation and this will contribute to the slowing of the economy. However, the Fed stressed once again that a further tightening of monetary policy may still be necessary to bring inflation back to 2% over time.

The consumer price index slowed further in March and thus remains on track. However, the core personal consumption expenditures index, the Federal Reserve's preferred measure of inflation, was up 4.6% in February 2023 from a year earlier, a level where it’s been for several months. In light of these developments, the Fed may very well be forced to raise the policy rate once again at its May 2-3 meeting.

Consumption fell in February, but hints at a rebound

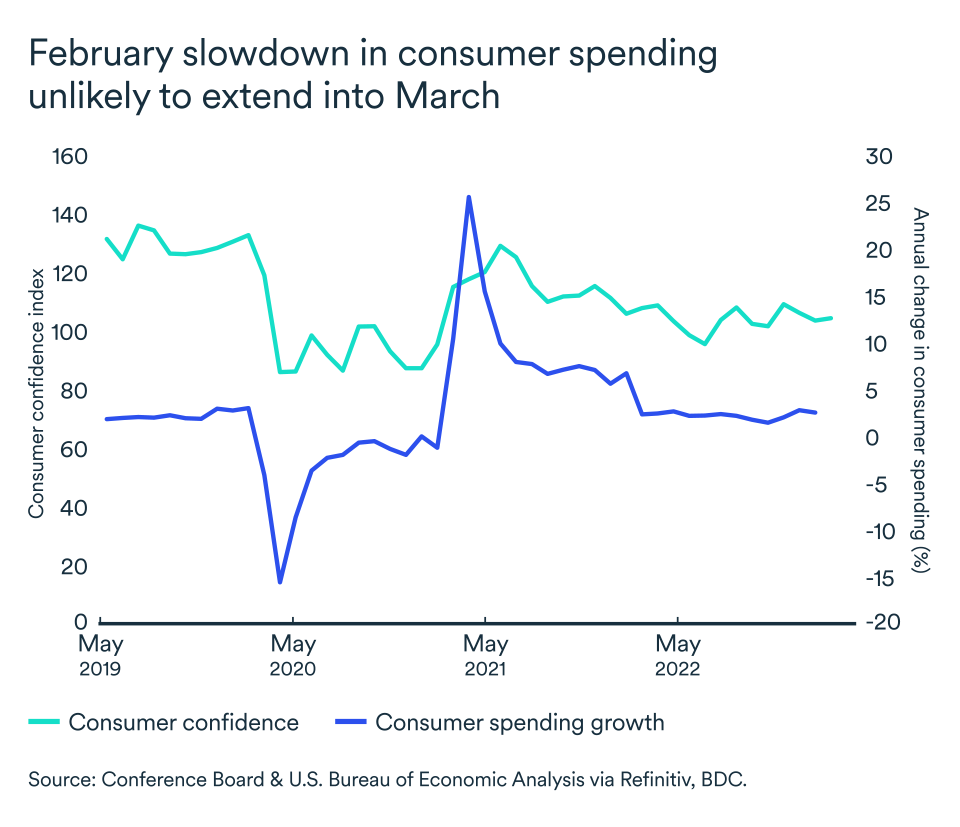

After the strong rebound in personal consumption expenditures (adjusted for inflation) in January, they declined in February. Consumption of gasoline and energy products increased during the month but did not offset a slowdown in purchases of motor vehicles and parts. Accommodation and food services also contributed to the decline in consumer spending volumes.

Consumer confidence improved in March compared to February despite the banking turmoil. The Conference Board's U.S. Consumer Confidence Survey also noted that while Americans continue to believe inflation will remain stubbornly high over the next 12 months, more households intend to spend on big ticket items, such as vehicles and appliances.

The job market is cooling down (a bit)

The number of jobs increased by 236,000 in March. This sets total job growth at over million in the first quarter of 2023 alone. The unemployment rate fell slightly after February's increase to 3.5%. Wages continue to rise, but at a slower pace, reflecting some easing of labour market pressures.

U.S. job vacancies have fallen to their lowest level in nearly two years. A decrease of 632,000 job openings, brought the total number to close to 10 million. This is a signal that demand for workers is finally slowing south of the border even though the country posted good job gains in the first quarter.

The impact on your business

- The shock to the U.S. banking system has been well contained so far, but the risk remains significant and therefore credit conditions in the U.S. will tighten further. As a result, the U.S. economy should continue to slow.

- Consumer confidence is still supported by the strength of the labour market, and U.S. households still intend to increase their spending in the near term but should turn more cautious as the rest of the year unfolds.

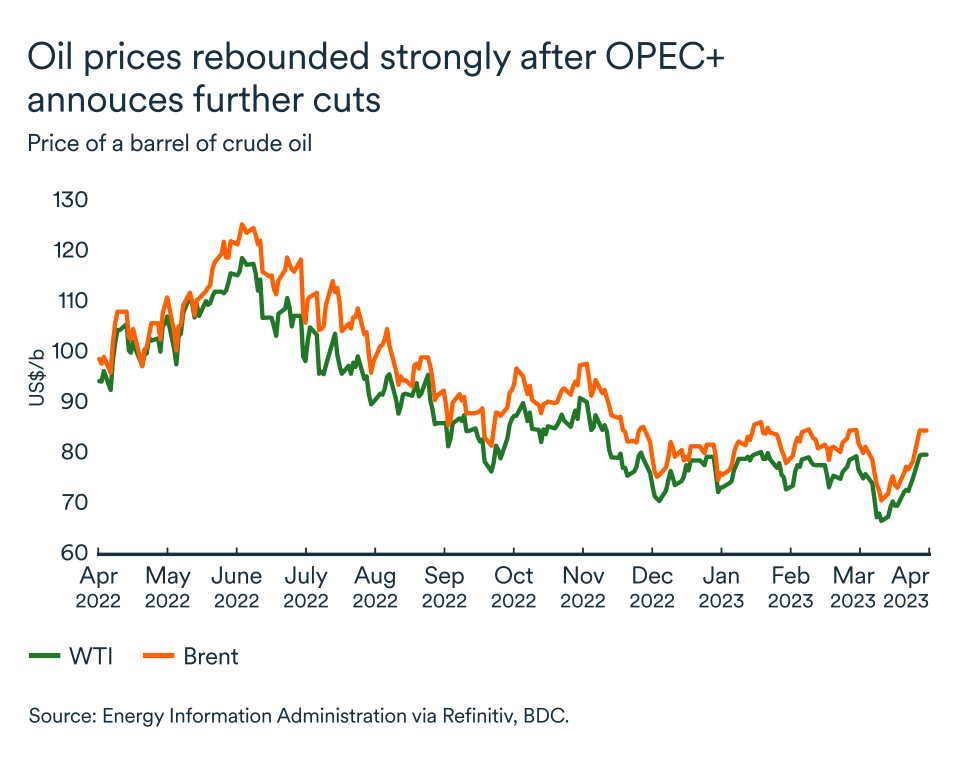

OPEC and its allies announce new production cuts

In March, Brent crude fell to US$71 per barrel and WTI to US$67, levels not seen since December 2021. Both global crude oil benchmarks, however, rebounded quickly following the announcement by the Organization of the Petroleum Exporting Countries and its allies (OPEC+) of further production cuts.

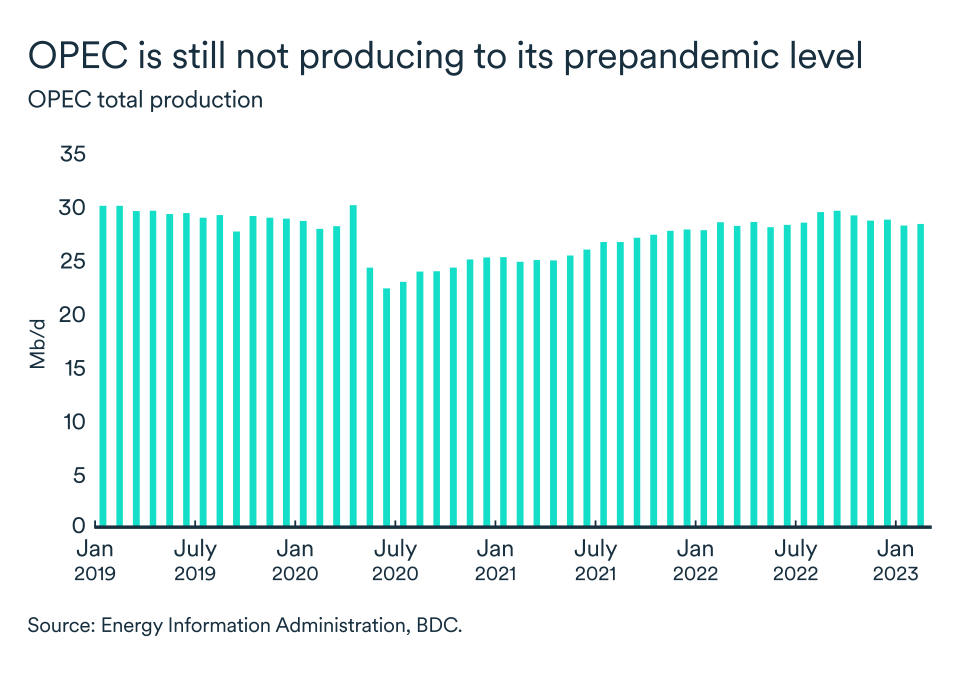

An expected economic slowdown in the U.S. and a rather modest recovery in China were enough for OPEC+ to revise its outlook for global demand in 2023. On April 2, the organization stated it intends to reduce production by an additional 1.66 million barrels per day from May until the end of 2023.

That will bring total production cuts to 3.66 million barrels per day, representing a little less than 4% of global demand.

A decision that could weigh heavily on the global economy

The decision to reduce global crude supply in the coming months was probably highly linked to the recent signs of a slowdown in global manufacturing. According to the Purchasing Managers' Index (PMI), manufacturing activity in the U.S. is already contracting. The index reached its lowest level since the start of the pandemic in March. Chinese manufacturing activity has also struggled to pick up since the end of COVID lockdowns and recorded another slow month in March.

OPEC and its allies, therefore, are betting the industrial slowdown will continue, if not worsen, in the coming months, and lead to a decline in crude demand. However, many analysts have revised their price forecasts for 2023 sharply higher, with some even predicting US$95 barrel by year end as supply would actually be lacking.

A new red flag

In the event an economic slowdown proves OPEC right, WTI is expected to hover closer to US$75 and Brent US$80. If, however, oil demand remains stronger than expected, prices will increase, fuelling inflation.

If oil prices rise too much, central banks around the world will have a harder time bringing inflation down. They will be forced to potentially raise interest rates above their desired level and increase the risk of pushing some economies, including Canada and the U.S., into recession.

Bottom line…

The news that OPEC and its allies intend to further limit global crude production in the coming months adds more uncertainty to an already volatile global market.

While the outlook for the manufacturing sector points to a slowdown in demand for crude, concerns about an unbalanced oil market pushed prices higher in early April. The impact of oil prices on the ability of central banks to bring inflation back to target while avoiding a recession will need to be watched closely. For now, oil prices remain at a sustainable level.

Canadian policy rate at 4.5%—just a little longer

The Bank of Canada announced that it was holding the policy rate at 4.5% in its latest announcement on April 12. To date, the Canadian economy has been very resilient despite past interest rate hikes. It is unlikely that the Bank of Canada will resume raising interest rates, although it still says it is open to doing so, if necessary. In our view, this will not be necessary and the next change in monetary policy is still expected to be a cut. However, we believe that the policy rate will remain at its current level longer than our forecast from last month (and market expectations too). If the economy and employment continue on their recent trends, all signs suggest that the first rate cut will not occur before December 2023.

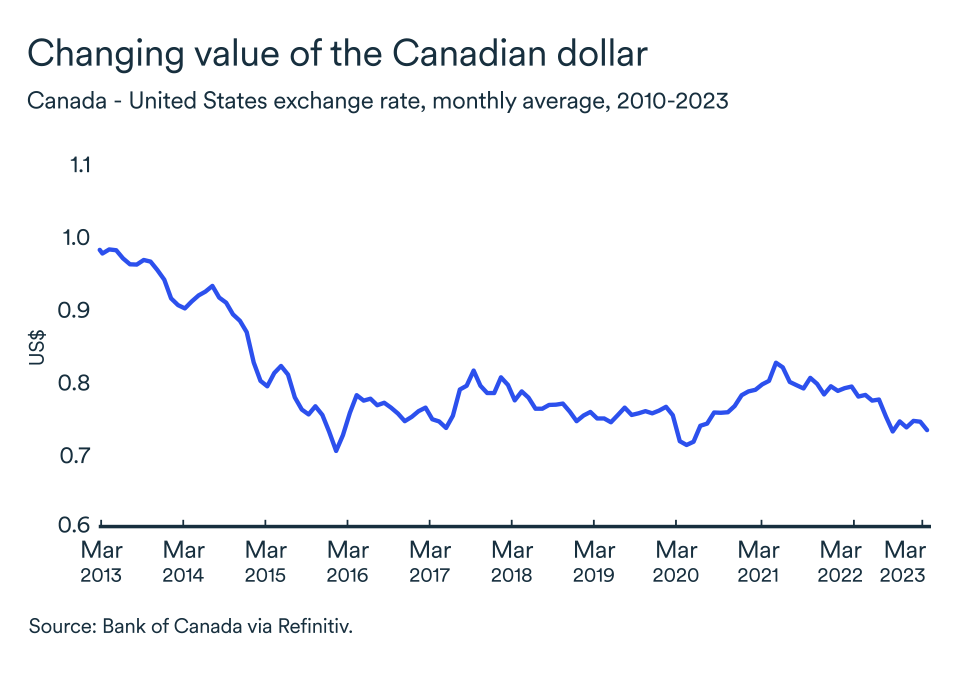

The loonie is changing rapidly

The Canadian currency plunged further in mid-March as fears of a major financial crisis pushing the global economy into recession surfaced. The loonie moved closer to the US$0.72 mark. However, the loonie gained a few cents on the back of a sharp rise in oil prices since the OPEC announcement. The Canadian dollar even reached 74.5 cents US, a two-month high. Since there is still a lot of uncertainty about the real impact of the new production cut announced by OPEC and whether the global economic slowdown forecasted a few months ago will materialize soon, the prices of many commodities (including oil) could push the loonie in either direction in the coming months. However, it would be surprising to see the loonie rise above US$75 on the long run.

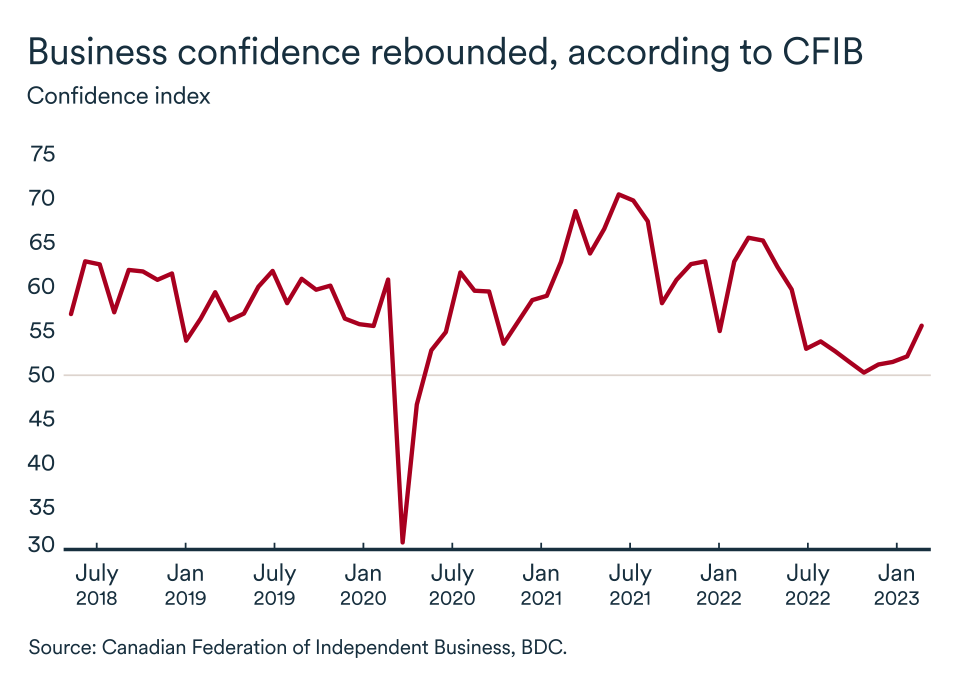

Optimism is slowly coming back among businesses

In March, the CFIB's business confidence index for the coming year rose from 51.8 to 55.3 after stagnating for the past six months. Businesses remain on edge, but the downturn in 2023 may be less severe than they anticipated in 2022. An indicator of 50 indicates that as many business managers expect the business environment to worsen as to improve over the next 12 months.