Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreThe end of interest rate hikes: What does it mean?

The Bank of Canada raised its trend-setting interest rate last month for what is likely to be the last time in this cycle of rate hikes. What does this mean for inflation this year? When could the first rate cut occur? What are the risks?

Where we are now

The Bank of Canada's monetary policy appears to be unfolding as predicted. Although it will take several more months to see the full impact of rate hikes over the past year, demand is slowing. This is particularly true in the more interest rate sensitive sectors such as consumer discretionary, durable goods, real estate and construction.

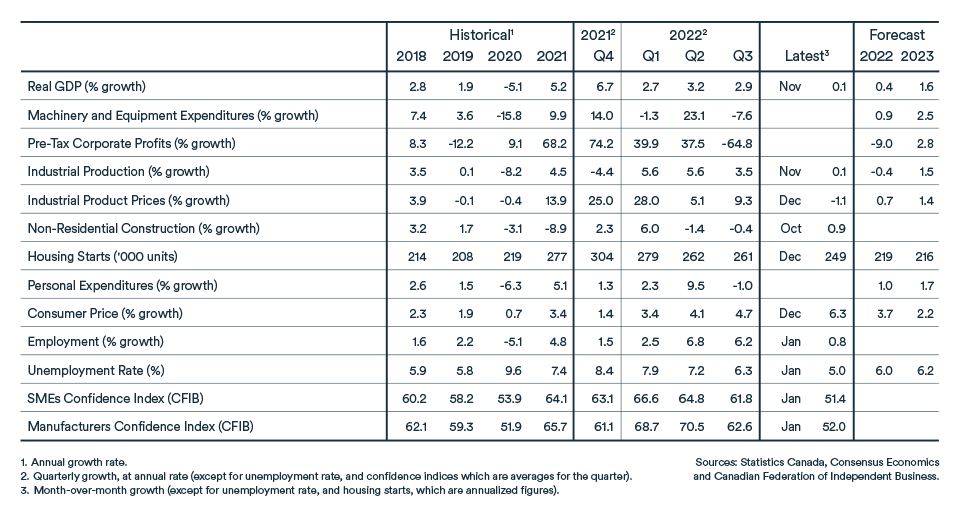

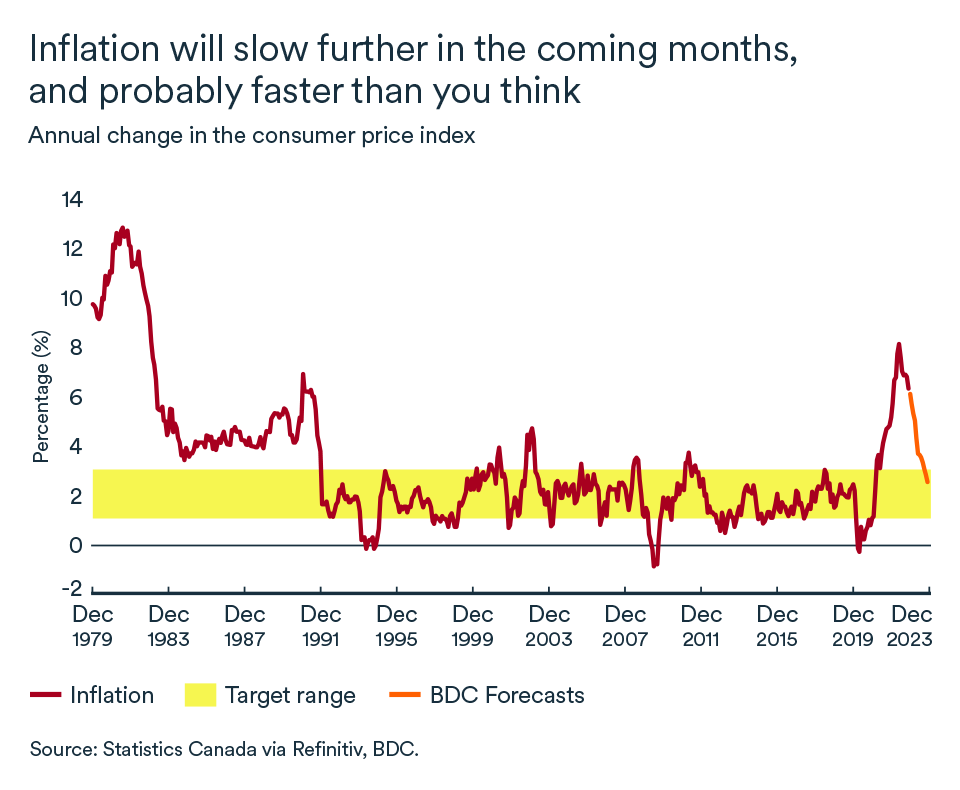

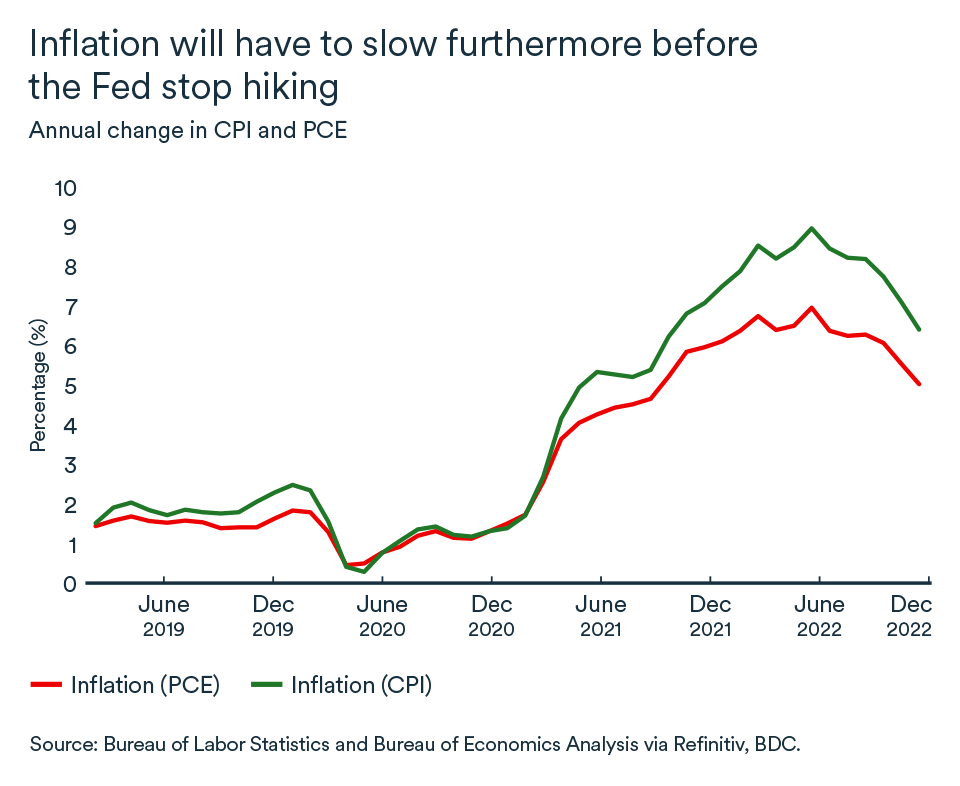

Despite the rapid pace of rate increases (a total of 4.25 percentage points in 10 months), inflation remained stubbornly high in 2022. However, the growth rate of the consumer price index started to fall at the end of the year, hitting 6.3% in December from a peak of 8.1% in June.

When volatile components such as energy and food were stripped out, core inflation indices hovered around 5%, which is still much too high. However, the central bank could take comfort from the progress made in slowing growth in wages and services prices.

Inflation will continue on its downward path

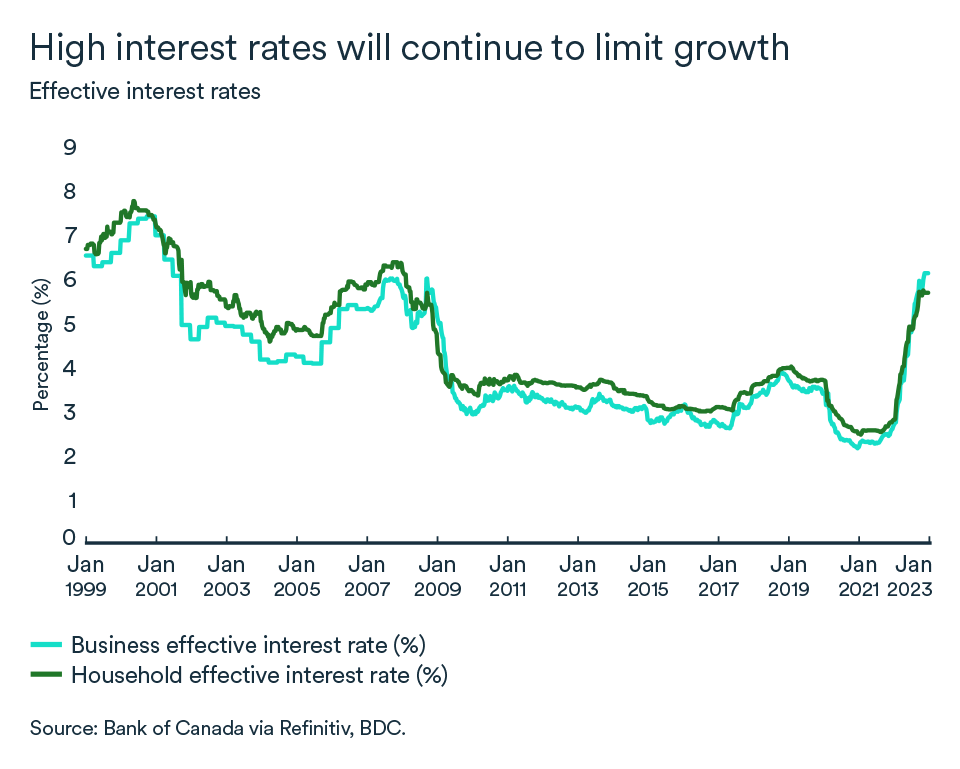

While the current level of interest rates are a source of concern for many households and businesses, the Bank of Canada’s current policy rate of 4.5% is designed to restore balance between supply and demand in the economy and bring inflation down to a sustainable level for the the long term.

Our forecast is for inflation to continue to fall in the coming months and it may be faster than you expect. Tighter credit conditions and the reallocation of household budgets to debt payments will further slow demand for goods and services. Other factors will also support lower inflation.

One of these is lower commodity prices. They’ve come down from the highs reached during the Russian invasion of Ukraine in February 2022. The commodity price index fell by 30% between March 2022 and January and continues to drop. This will help price comparison in the coming months.

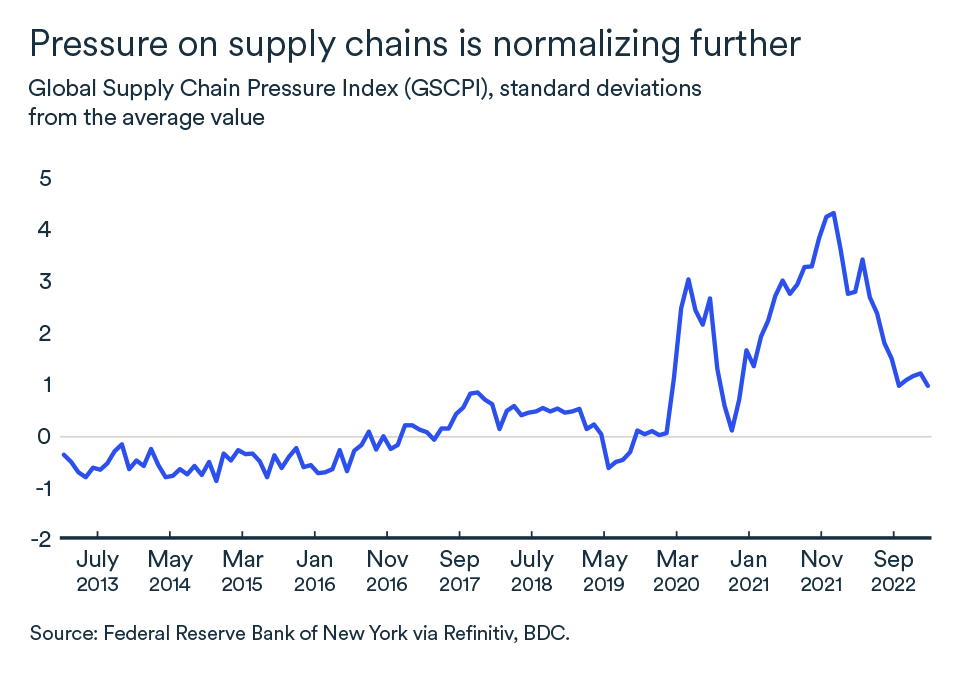

More downward pressure on inflation will come from the easing of supply chain disruptions and liquidation of inventories accumulated by companies in the second half of 2022. Additionally, the economic slowdown taking place in the world’s major economies, including Canada, will temper competition for available labour and discourage workers from changing jobs, taking pressure off wages.

We expect inflation to approach the upper end of the Bank of Canada's target range of 3% by the third quarter. At that point, the central bank will be in a good position to lower its policy rate.

Risks still remain

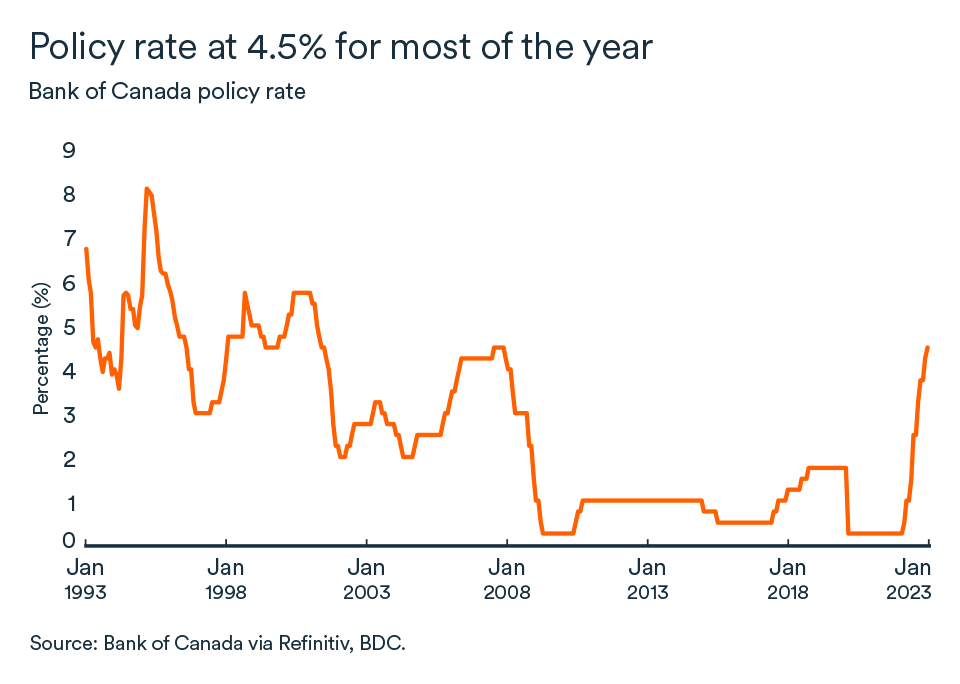

While the Bank of Canada’s rate may well have peaked at 4.5% and likely stay there for most of the year, there are risks for this forecast.

First, while we expect wage pressure to be less severe in 2023 than in 2022, the level of job vacancies and job creation is still too great to allow for a significant easing. More and more baby-boomers are retiring and it would be surprising to see productivity gains help ease the labour market because business investment is slowing.

In its January Monetary Policy Report, the Bank of Canada noted that 4-5% wage growth is not consistent with 2% inflation. In January, average hourly wages rose at a rate of 4.5%. Inflation in the service industries may, therefore, prove to be persistent. Services excluding housing account for nearly a quarter of the consumer price index.

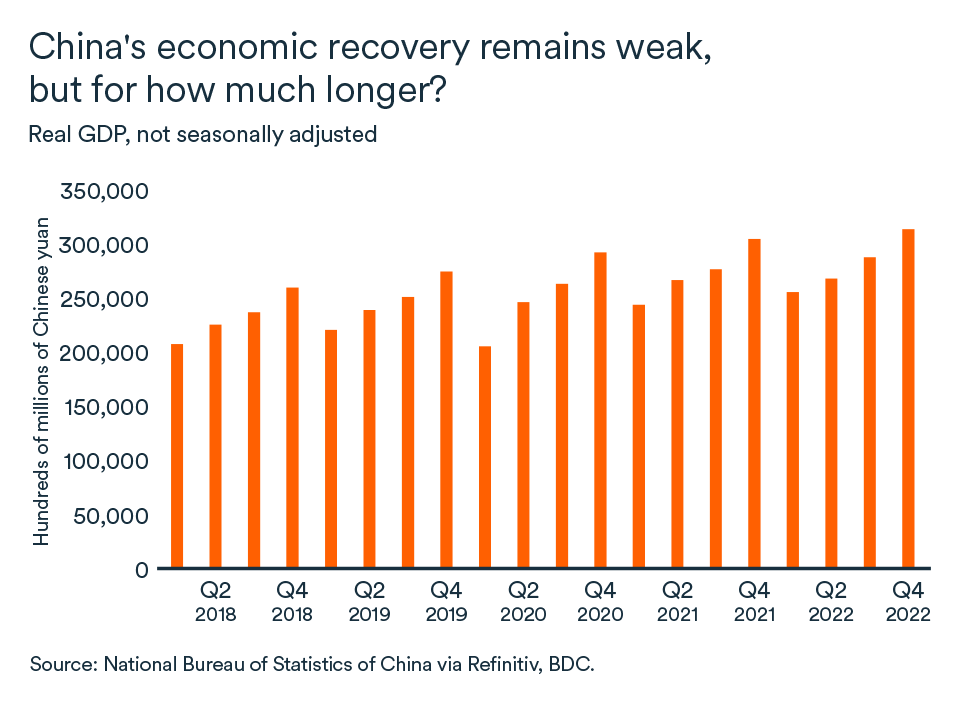

Second, the easing of health restrictions and the full reopening of the Chinese economy could revive global demand for commodities, especially energy. So far, despite the end of COVID restrictions, a strong rebound has not materialized.

Once the Chinese economy fully recovers from spike in COVID infections following the withdrawal of restrictions, demand for resources, especially oil, may pick up quickly, causing another surge in inflation. Another risk to the energy market is the geopolitical uncertainty that still remains as retaliatory measures against Russia continue to emerge.

Finally, in the most recent State of the Union speech, U.S. President Joe Biden announced new standards for construction materials used in federal infrastructure projects that could affect inflation on both sides of the border. The materials used, such as lumber, glass, drywall and fibre-optic cables, must be manufactured in the United States. At the time of writing, there is still a lot of uncertainty surrounding the application and the actual shape of this policy, particularly in terms of how it fits into the Canada-U.S.-Mexico Agreement (CUMA). It should be noted that the U.S. recently lost a dispute settlement panel on the calculation of allowable foreign content in U.S. vehicles.

In short...

- We expect the Bank of Canada’s policy rate will remain at 4.5% for most of the year, but the first reduction could come as early as fall 2023.

- Inflation will come down relatively quickly in the coming months, but we don’t expect it to reach the midpoint of the bank’s target range of 2% until 2024.

- We don’t see the Bank of Canada bringing its policy rate back to 2.5%, the neutral rate, until mid-2024. Therefore, rates will remain higher than what Canadians had grown accustomed to since the financial crisis of 2008. Wage growth will be something to watch as it could prove to be a key issue influencing the evolution of monetary policy.

Canada’s economy continues to show resilience

Real gross domestic product grew by 0.1% in November, similar to October's growth. November's gains came mostly from the service industry, where activity continues to hold up well. However, preliminary data from Statistics Canada points to sluggish growth in December (0.0%), even though retail sales benefitted from a more normal holiday season in 2022.

Policy rate peaks at 4.5%

After raising its key rate by an additional 25 basis points at the end of January, the Bank of Canada hinted this hike would be the last in this tightening cycle.

The policy rate would therefore peak at 4.5%. However, there are risks that could lead the Canadian central bank to revise its stance in the coming months. (See this month's main article for a complete picture on inflation and monetary policy.) Regardless of what moves are made by the bank in the months ahead, the effects of hikes over the past year will continue to temper economic growth.

Households readjust their budgets

The sectors that slowed in the last quarter of 2022 are those that are typically most sensitive to interest rates—construction, manufacturing, retail trade, and accommodation and food services. Together, these four sectors lowered growth by 0.12% in November, limiting overall economic growth.

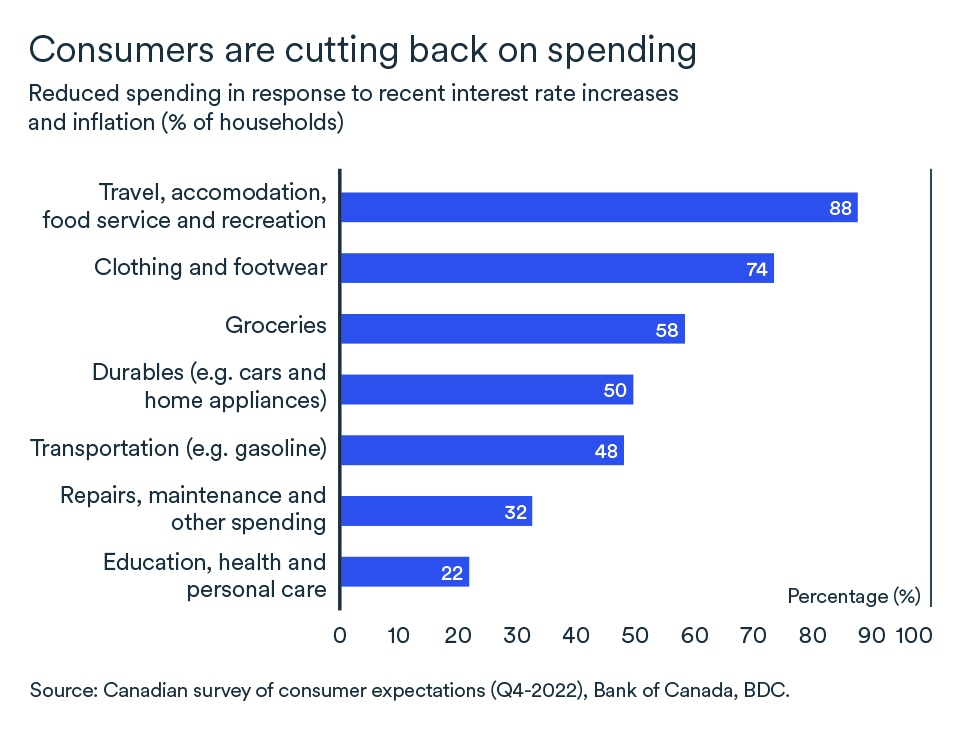

The slowdown in the more interest rate sensitive sectors is consistent with consumers pulling back on their spending in the face of rising interest rates. Obviously, discretionary consumption is the most affected by this readjustment. Nearly 88% of households have cut back on travel, dining and entertainment, followed by 74% who have reduced clothing purchases, according to the Bank of Canada.

Canadians are also changing the contents of their grocery baskets in response to high food inflation. And they’ve further slowed their pace of borrowing in the consumer credit market (+0.3% in November).

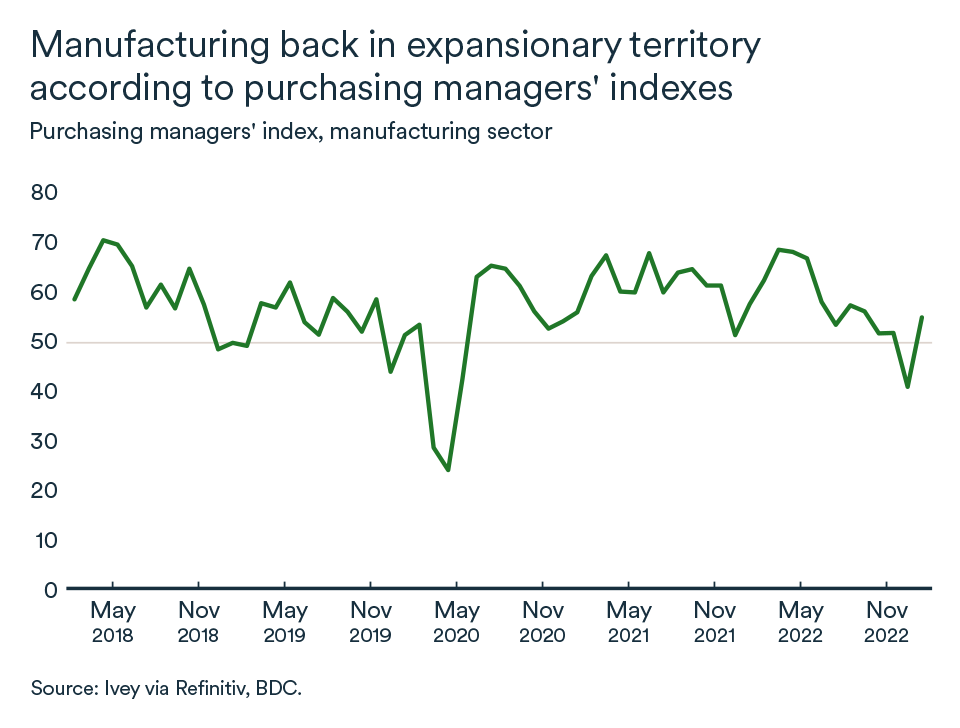

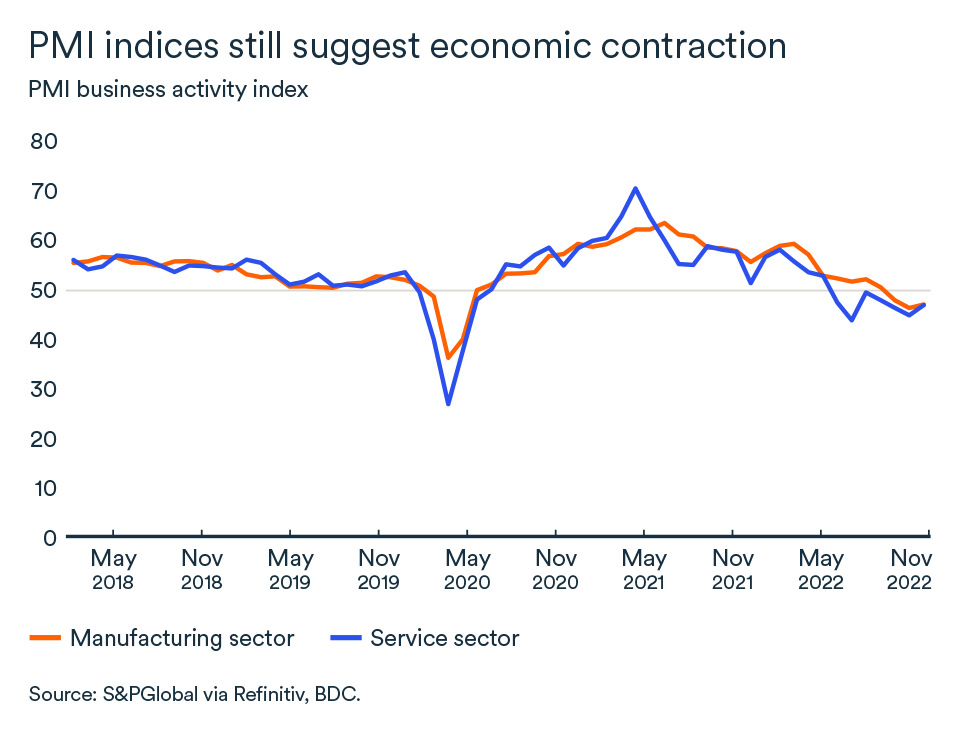

A recovery in Canadian manufacturing in January?

The Canadian Manufacturing Purchasing Managers' Index rebounded in January. After dipping below the 50 mark (which usually indicates a contraction in the sector) in December, the S&P index rose to 51 at the start of the year and the Ivey index to 54.7.

This modest improvement was supported by gains in production and stronger order books. The rebound is entirely attributable to demand in the domestic market since export orders fell for the eighth consecutive month.

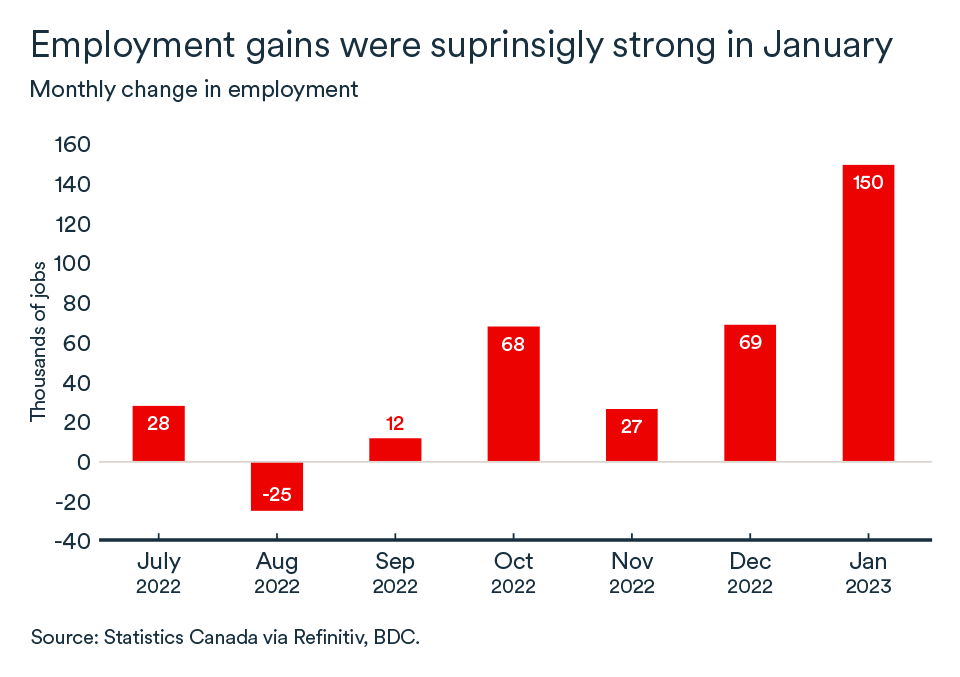

Towards a more sustainable labour market

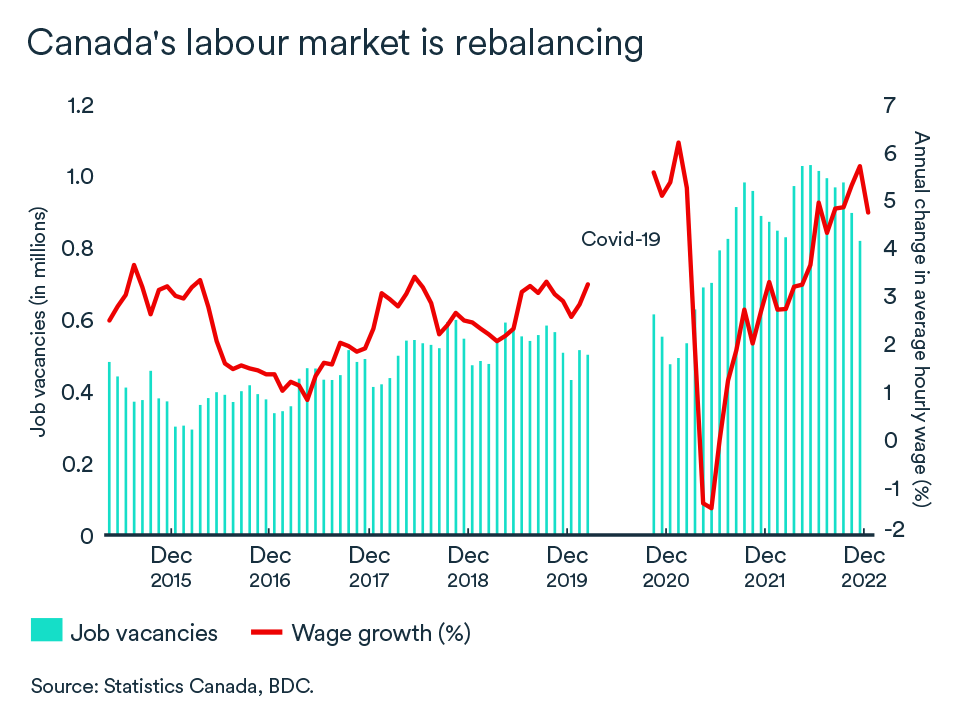

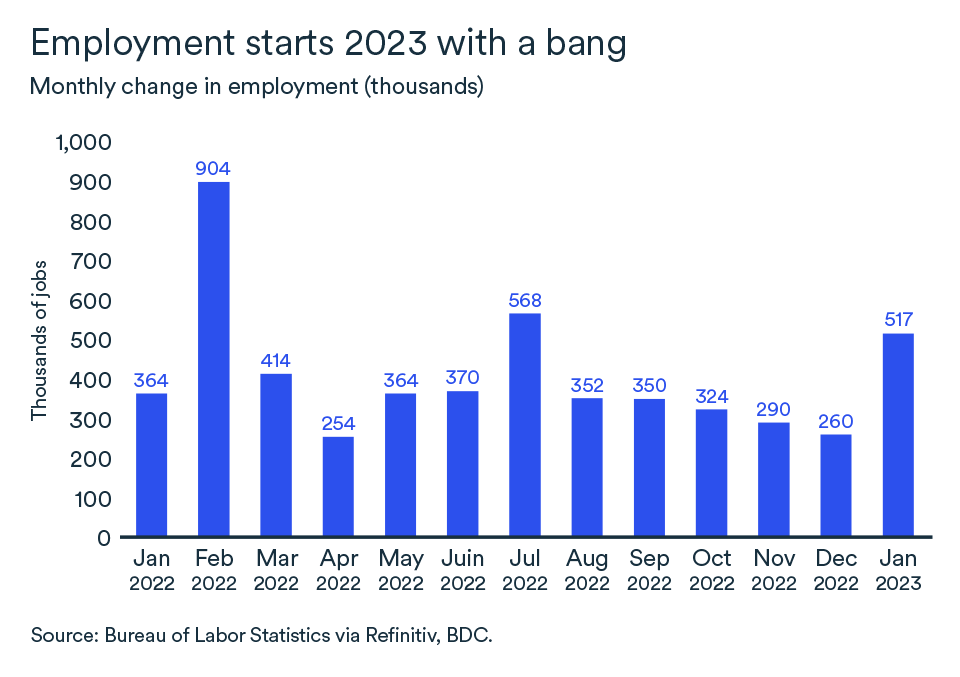

The Canadian economy added an impressive 150,000 jobs in January. While the unemployment rate remained at a low 5.0%, labour market pressures are showing signs of easing.

The number of job vacancies in the country has fallen rapidly. It dropped from 1 million to 850,000 positions over just two months in the fall of 2022. While the current level is still high, the speed at which job opportunities are disappearing points to an easing of competition for workers.

Amid high economic uncertainty, companies expect to hire fewer workers in 2023 and employees will be less likely to change jobs. The result appears to be somewhat of a rebalancing of the Canadian labour market, even though retirements remain high at more than 263,000 new departures in the last year.

These factors resulted in wage growth of 4.5% between January 2022 and January 2023, a slower pace than in recent months despite the impressive level of jobs added in January.

The impact on your business

- Despite an expected pause in Bank of Canada rate increases, Canadian household debt payments will continue to slow domestic demand. Consumers are still coming to grips with higher interest rates and more sectors will experience slower demand as households reallocate their budgets. Growth will be more challenging in the early part of the year and businesses should pay close attention to their inventories in the current environment.

- The Canadian labour market remains strong, which should temper recession fears. Household savings are still above their pre-pandemic trend and wage growth is strong. Households, therefore, still have a good cushion to absorb interest rate shocks and inflation, but they’re being more cautious in their spending.

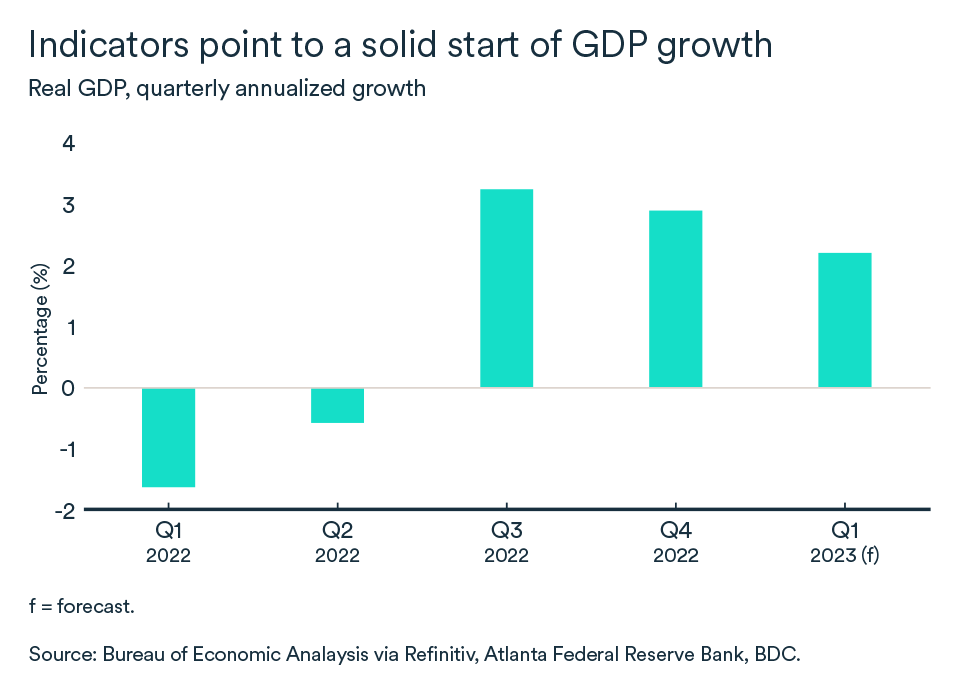

The U.S. economy looks headed for a soft landing

The U.S. economy does not appear to have lost as much momentum with the data currently pointing to 2.2% growth in the first quarter of 2023.

However, more rate hikes are coming as the labour market remains strong. Overall, signs still point to a soft landing for the economy, not a recession.

Manufacturing & services are both losing ground

New orders for U.S. manufacturers slowed further in January. The manufacturing new orders index plunged to 42.5 last month. This is the lowest level ever reached without a recession ensuing.

The service sector, which accounts for more than two-thirds of U.S. economic activity, has also lost strength and is expected to temper expected economic growth in the first quarter.

More rate hikes on the way for Americans

The U.S. Federal Reserve raised its policy rate once again on February 1. The 25-basis-point increase was the smallest by the U.S. central bank during this tightening cycle. However, the tone of the announcement tempered expectations of a reversal in course.

The wording of the statement maintained the language that "continued increases" in rates would be required. It was a clear signal that the U.S. overnight rate will exceed 5% this year. It currently sits between 4.50 and 4.75%.

Thus, lower inflation readings from the consumer price index and the personal expenditure index were not enough to convince the central bank that prices were indeed on a sustained downward slope.

Over half a million new jobs

By the last business day of December, the number of job openings had increased slightly to 11 million and job creation was strong as the new year started. The U.S. economy added nearly 520,000 jobs in January, including 443,000 in the private sector. At 3.4%, the unemployment rate is now the lowest since 1969.

Wage growth has slowed, but remains elevated at 4.4%. Therefore, while most economists expect inflation to continue to decline in the coming months, the strong employment gains likely support the Federal Reserve's guidance that further rate hikes will be needed to rebalance the U.S. economy over the longer term.

The impact on your business

- The U.S. economy appears to be off to a respectable start to 2023, but gains for Canadian businesses will be modest. U.S. growth will be weak in the coming months and will be driven entirely by service sectors.

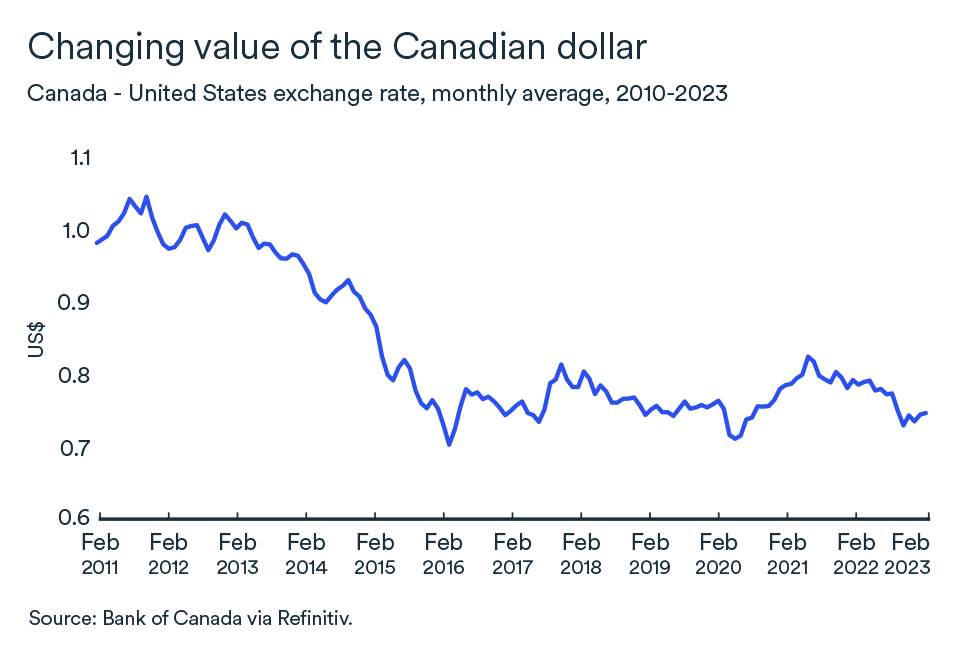

- In contrast to the Bank of Canada, which has hinted it will hold its rate at the current 4.5%, the U.S. Federal Reserve intends to continue its tightening cycle a little further. The widening spread between U.S. and Canadian rates will add downward pressure on the Canadian dollar. A weaker loonie relative to the U.S. dollar tends to favour Canadian exports. On the other hand, it will cost more for Canadian companies that rely on imports denominated in U.S. dollars.

- Strong U.S. labour market gains and an export-friendly exchange rate should support U.S. consumption, which could help mitigate a demand slowdown taking place in Canada.

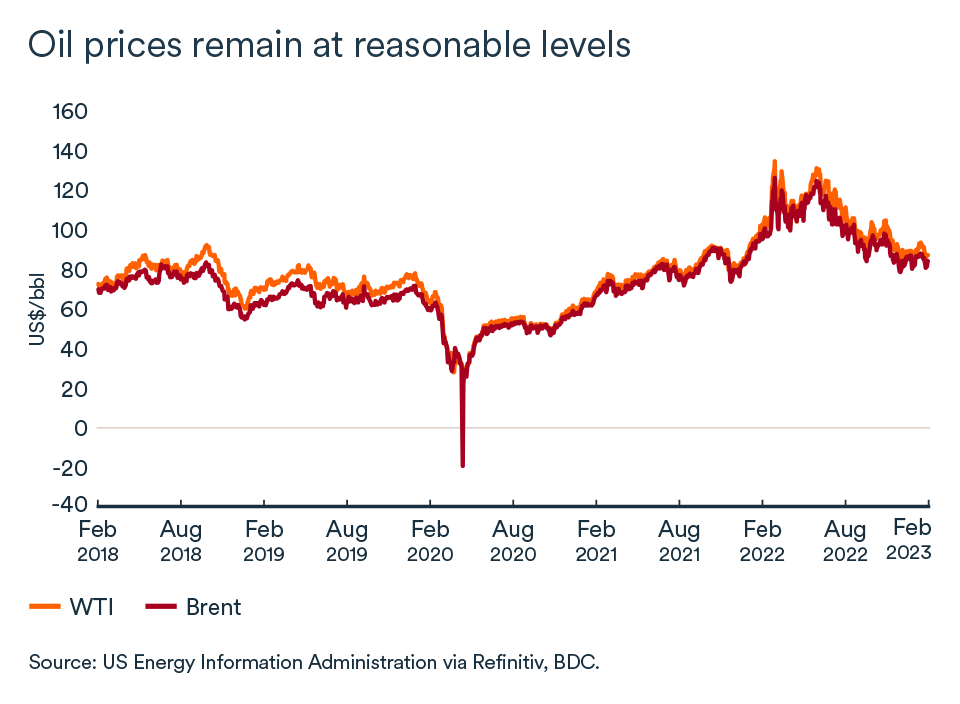

Crude oil prices fall further

The decline in crude oil prices that began in late 2022 continued into the new year. Brent and WTI futures were trading at US$80 per barrel and US$73 per barrel, respectively, in early February, down 10% and 16% year-over-year.

New sanctions against Russia

In December 2022, the G7 set a cap on the price of Russian crude at US$60 per barrel to limit the financing of its war in Ukraine. Now a new sanction has been added to the list against Russian oil. The European Union has introduced a cap of $100 per barrel on products that trade at a higher price than crude, mainly diesel, and $45 per barrel for products that trade at a lower price, including fuel oil.

Uncertainty related to geopolitical tensions with Russia will continue to create turmoil in the oil market this year.

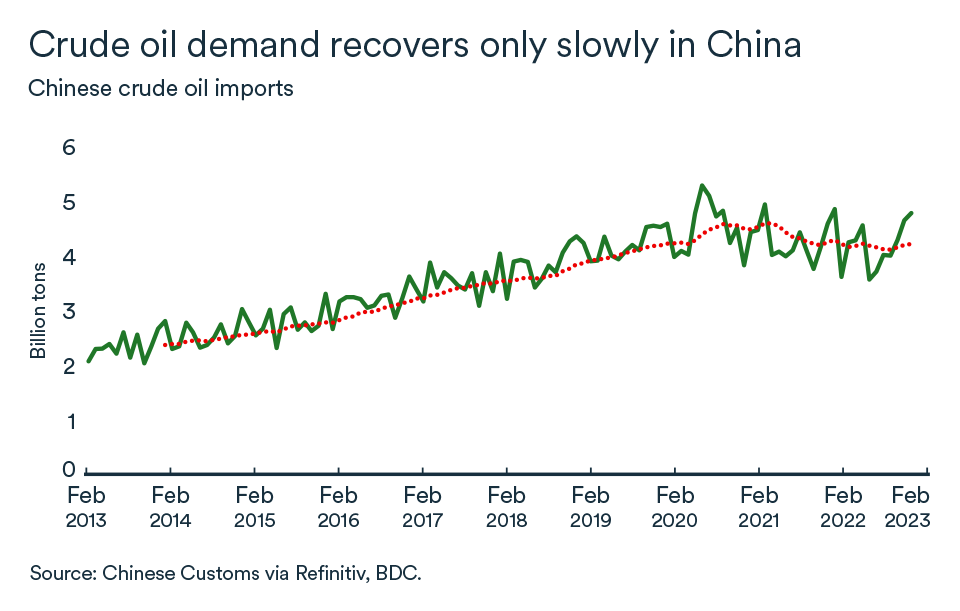

Chinese growth will be a key factor in 2023

The global recession fears that have led to lower crude prices could quickly be offset by a recovery in the Chinese economy. While economic activity has remained subdued in China since the end of health restrictions that led to a wave of COVID infections, a rebound in the world's second largest economy and largest importer of crude is expected to increase energy demand in the coming months. The International Energy Agency expects half of this year's global oil demand growth to come from China.

The U.S. economy is also in the spotlight

One factor that could moderate price pressure from China is developments in the U.S. The decision and tone of the U.S. Federal Reserve announcement on February 1 to hike its benchmark interest rate once again, along with gains in U.S. employment, led crude benchmarks to close the first week of February lower.

This was because higher interest rates bolster the U.S. dollar and a stronger dollar generally reduces demand for oil from buyers paying with other currencies. Rising rates also dampen price increases because they are designed to slow economic growth, which lowers demand for crude.

Bottom line…

Uncertainty remains high in the oil market. Hard to predict factors such as the rebound in the Chinese economy, interest rates movements and the course of the U.S. dollar are creating cross-currents in oil markets. Geopolitical tension and sanctions against Russia will also continue to weigh.

The markets will therefore continue to adjust according to short-term information, which increases the risk of price volatility in 2023. Major oil benchmarks may decline further in February and March, but we expect prices to recover before the end of the second quarter.

Interest rate at 4.5% for a while

The Bank of Canada implied that the 25 basis point increase on January 25 would most likely be the last in this cycle of tightening credit conditions. The latest announcement on January 25 will have confirmed our expectations – the policy rate in Canada will peak at 4.5%. For now, the risks that could push the Bank of Canada towards a further increase remain strong and represent a great source of uncertainty. See this month's lead article for more information on this topic.

Exchange rate is steady

The Canadian currency has held fairly steady since November. However, the loonie moved closer to the US$0.75 mark after the release of January's employment figures further tempered the risks of a recession. While the Bank of Canada was suggesting that it was done with rate hikes, the Federal Reserve warned that more rate hikes were in the cards (plural: more). The spread between U.S. and Canadian rates should therefore increase in the first quarter of the year, which will also favour the U.S. dollar at the expense of the Canadian currency.

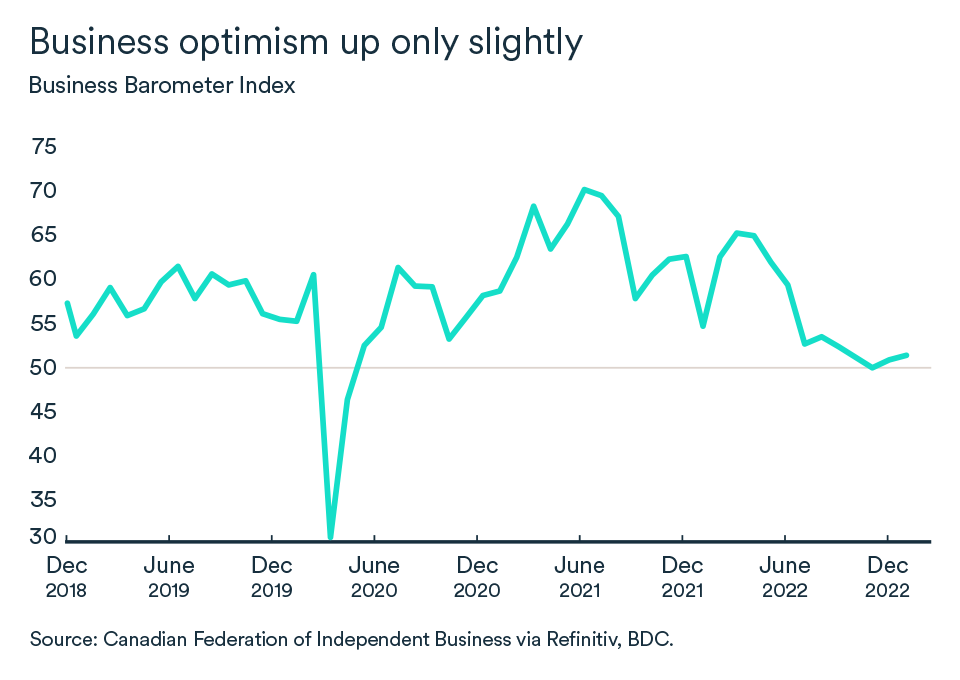

Business confidence improves slightly

In January, the CFIB's business confidence index for the coming year essentially held steady at 51.4, up from 50.9. Still, the index has improved over the past two months. Businesses remain on the lookout, but the downturn in 2023 may be less severe than they anticipated back in 2022. An indicator of 50 means that as many business managers expect the business environment to worsen than there are expecting them to improve over the next 12 months.