Canadian Small Business Health Index

The Canadian Small Business Health Index combines survey data collected by BDC, Equifax credit bureau data and macroeconomic data from Statistics Canada and the Bank of Canada. The index complements existing indices and provides a novel perspective on Canadian business health. The index can inform business decisions about strategy and investments.

2026 started on a positive note, with returned optimism and improved expectations despite the lingering uncertainty that surrounds the Canada-United States-Mexico Agreement (CUSMA) renegotiations.

However, the situation shifted quickly with the outbreak of the conflict in the Middle East, which brought back inflationary pressures as key commodity prices surged. Although economic fundamentals held strong in 2025, some cracks began to show in early 2026. The unemployment rate rose in Q1, and slowing population growth is expected to weigh on the economy's growth potential in the quarters ahead. Consumer spending, however, remained a bright spot. Retail trade continued to increase through January and February 2026, providing some support even as labour market conditions softened.

These crosscurrents are likely to weigh on the index in the coming quarters.

Results by region

May 2026

Canada: Optimism returns for now

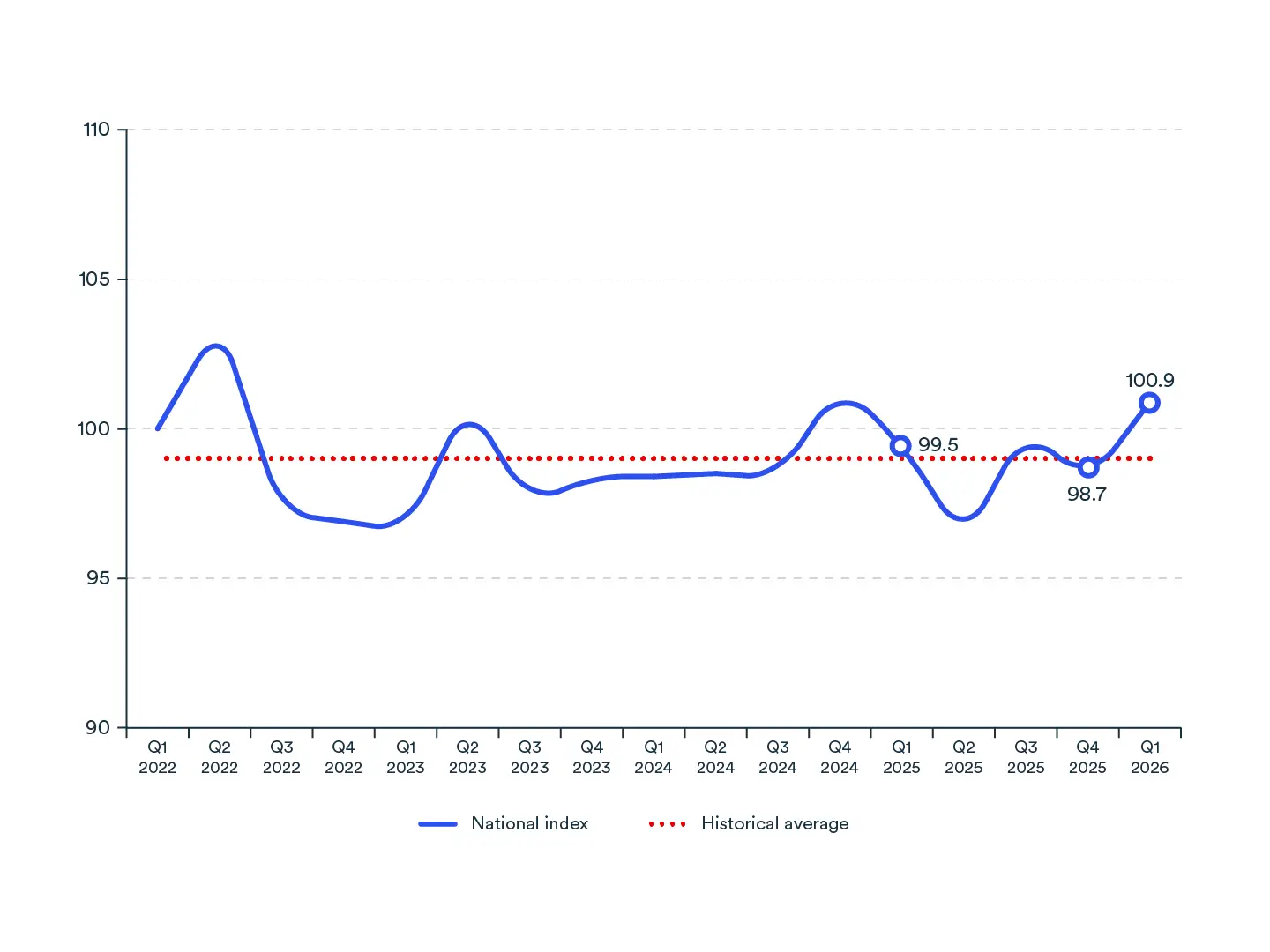

Canadian Small Business Health Index, Q1 2026

100.9

Year-over-year difference

1.5%

Difference over the previous quarter

2.3%

Small Business Health Index, Canada

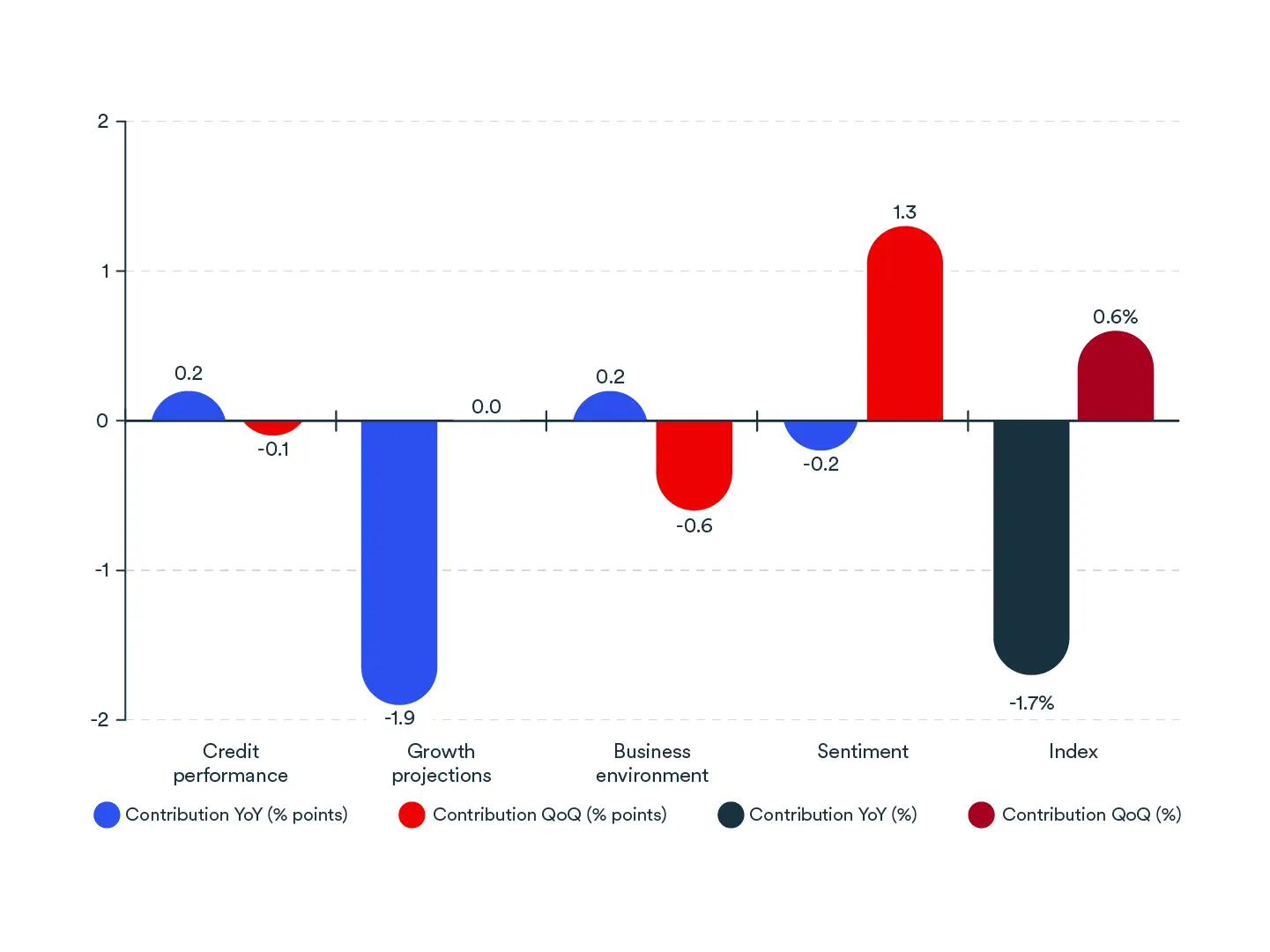

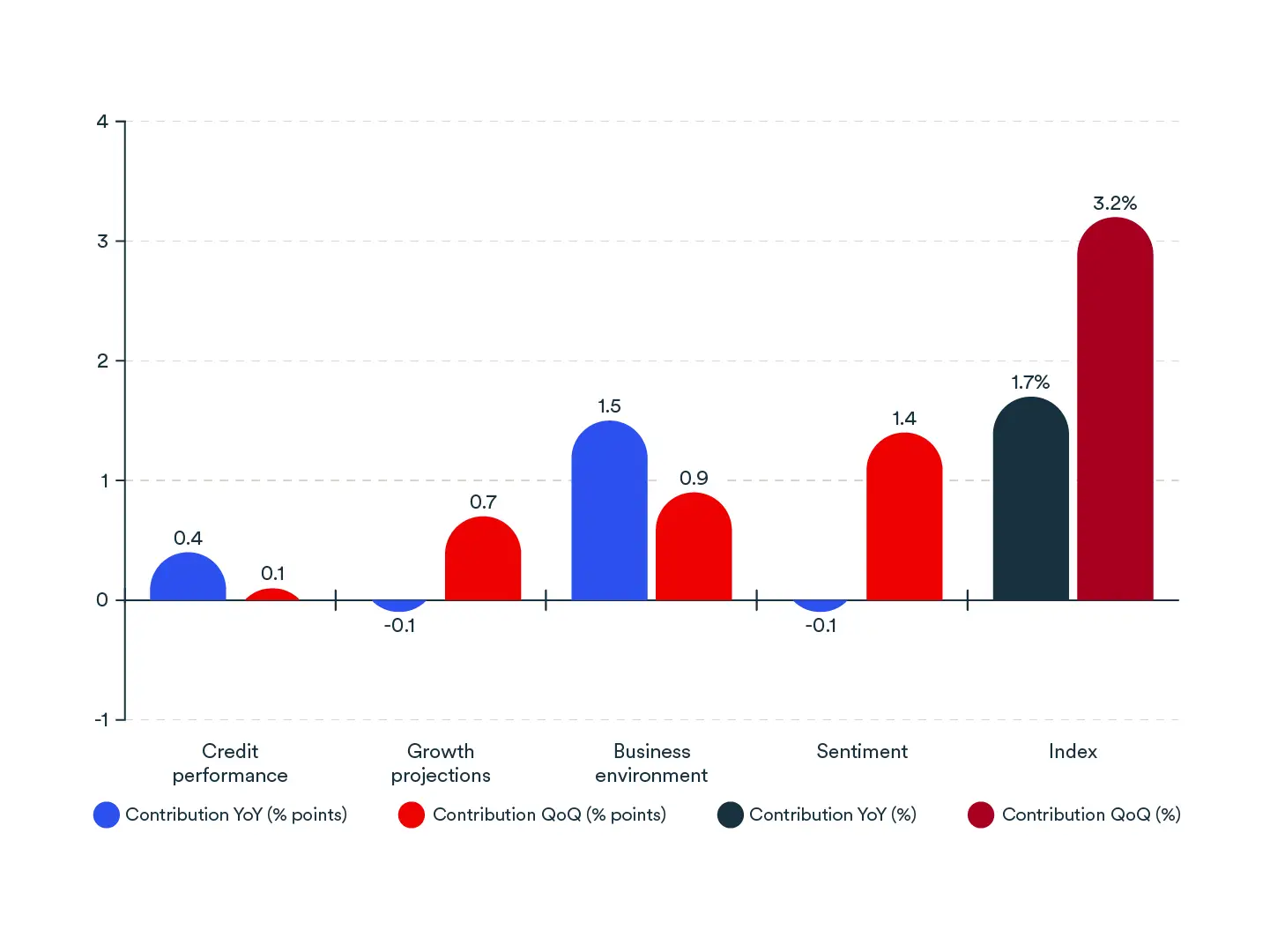

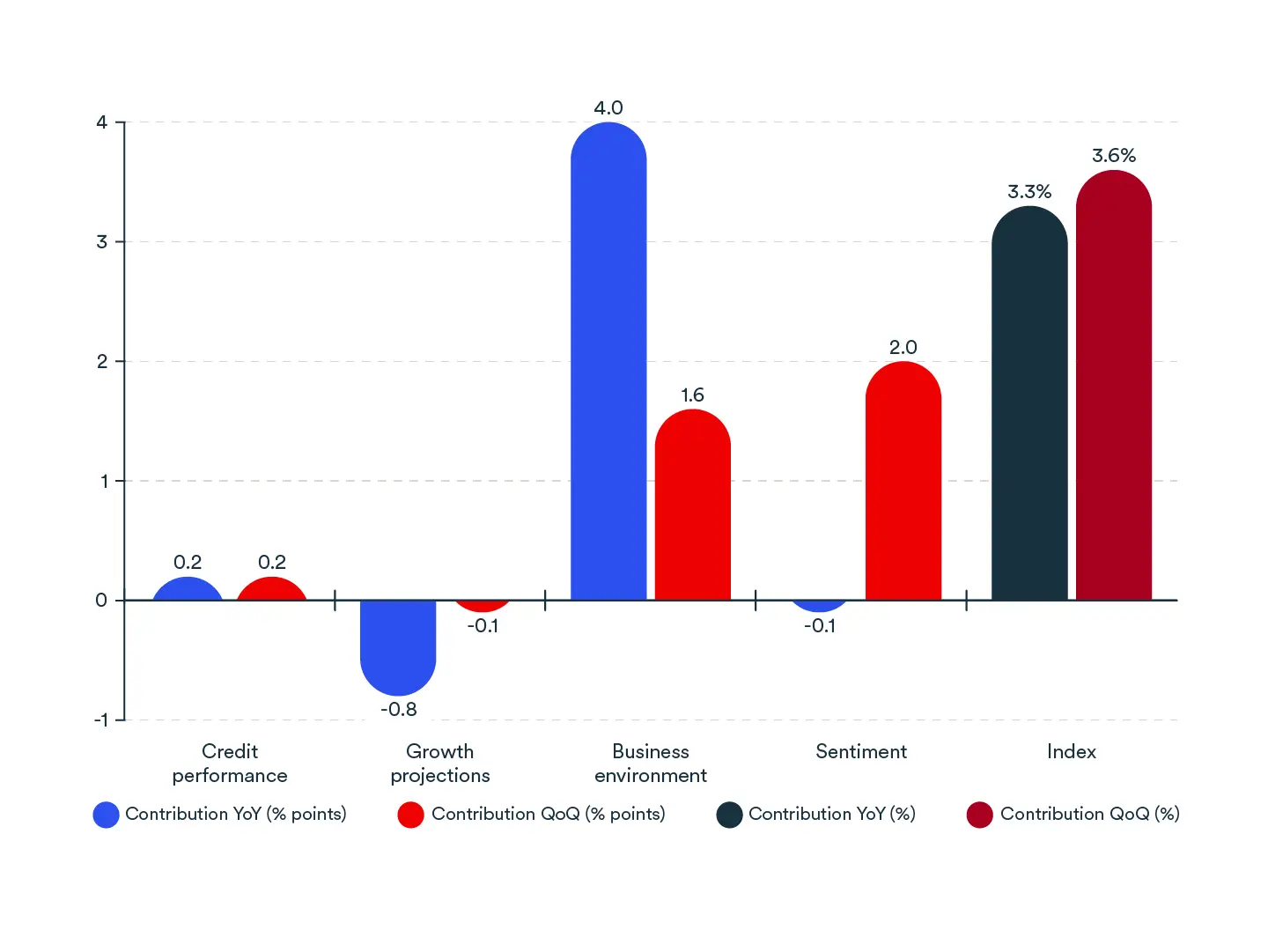

The national index rebounded in Q1 2026, rising to 100.9, a 2.3% quarterly increase and 1.5% gain year-over-year, and returned above its historical average for the first time since Q1 2025.

The recovery was primarily driven by improving sentiment, and this contributed more than half of the quarterly gain. Cash flow expectations improved markedly: 32% of SMEs anticipated an improvement in the next 12 months, up from 26% in Q4 2025. Those expecting deterioration fell from 20% to 14%. Economic pessimism eased somewhat, though it remains elevated: 49% expected worse conditions ahead, down from 55%.

However, this improved sentiment may prove short-lived. The outbreak of the conflict in the Middle East and resulting surge in commodity prices, which occurred after the Q1 2026 survey, are likely to weigh on business confidence in the coming quarter, potentially reversing some of the gains observed in early 2026.

The business environment component continued to strengthen, driven primarily by rising wages and favourable financial conditions, even as employment edged lower on a quarterly basis.

Growth projections improved modestly, though they remain below last year’s levels as reduced business openings and slightly lower credit inquiries were offset by improving expectations for investment, sales and hiring. Credit performance showed a slight increase: improvements in 30+ day past-due supplier credit and lower bankruptcies were muted by a rise in 90+ day past-due financial credit. This indicates that some SMEs continue to face deeper financial difficulties.

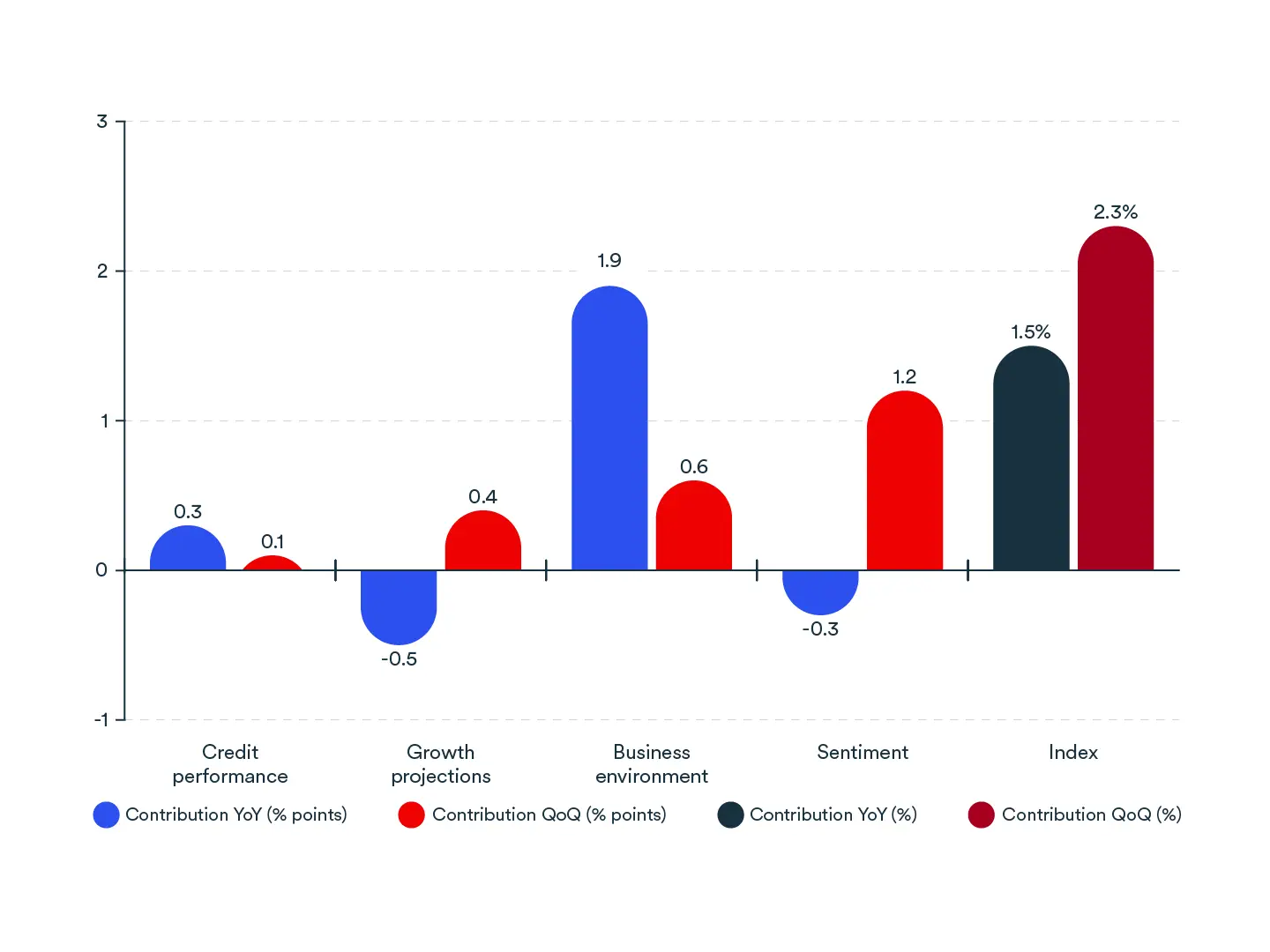

Component contribution to the growth of the Small Business Health Index for all of Canada, Q1 2026, percentage points

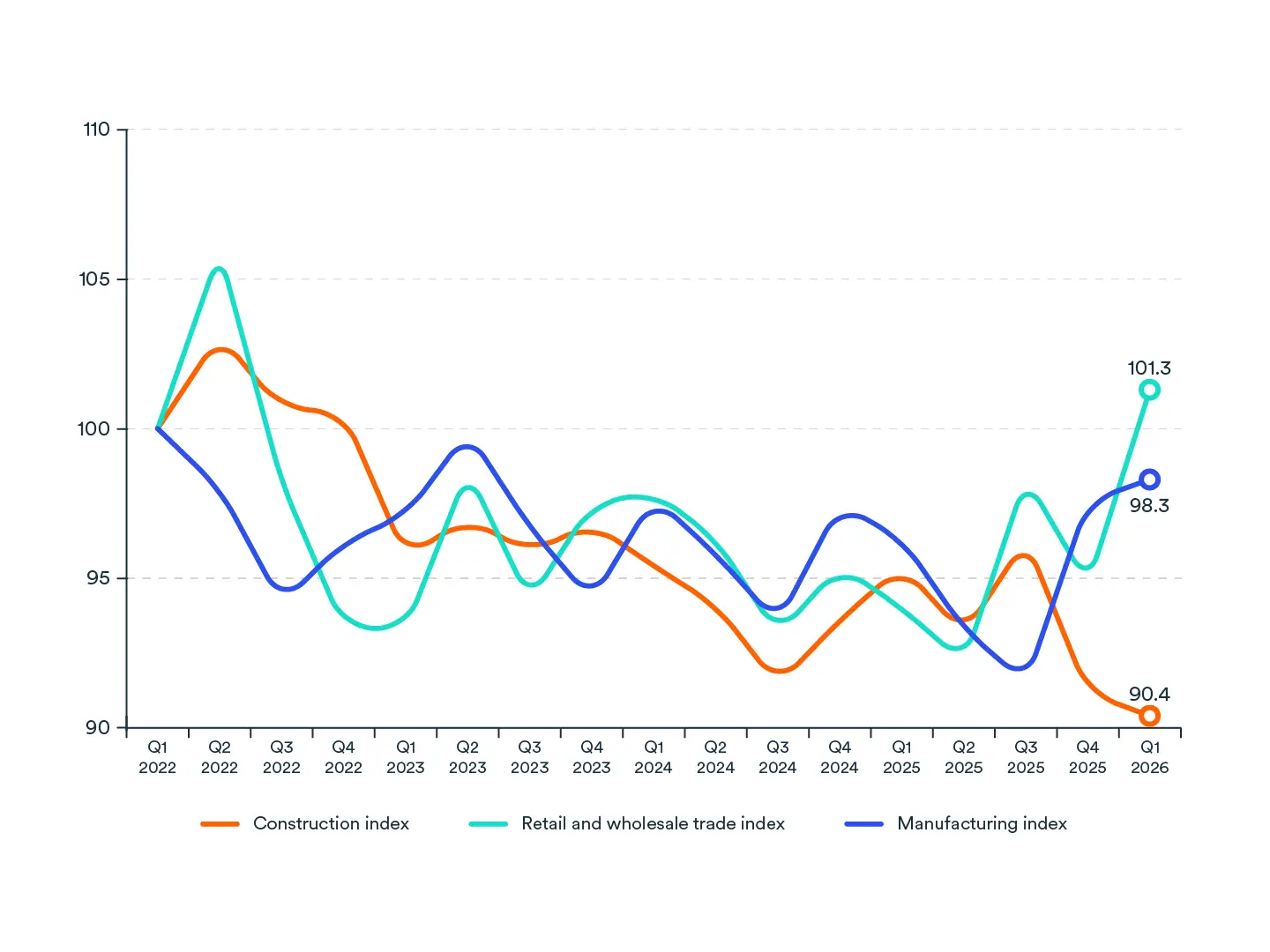

Retail leads the recovery as construction reaches new lows

The retail and wholesale trade index delivered the strongest performance this quarter, surging 6.2% from the previous quarter to 101.3, its highest level since Q2 2022. The recovery was broad-based, driven by strong gains in both the business environment and sentiment components. The share of SMEs expecting worse economic conditions fell sharply, from 58% to 34%, while credit conditions improved, supported by lower delinquency rates and reduced utilization.

The manufacturing index increased modestly, edging up 0.9% to 98.3 and extending the strong rebound seen in Q4 2025. Growth projections were the primary driver, supported by stable business openings and trade activity, alongside improved sales and hiring expectations. Financial access also strengthened, with 57% of manufacturers reporting that their financing needs were fully met, up from 44% the previous quarter. Despite these improvements, economic pessimism continued to weigh on the sector and, amid rising commodity prices, it is unlikely to ease in the coming months.

In contrast, the construction index fell to a new record low of 90.4, declining 1.0% from the previous quarter and 4.9% from a year earlier. Credit performance worsened further, reflecting rising bankruptcies and higher late delinquencies. Economic pessimism deepened significantly, and a growing share of SMEs reported that debt repayment constraints limited their activities. Although sales expectations rebounded from last quarter’s lows, overall conditions point to persistent challenges ahead.

Small Business Health Index, Industries

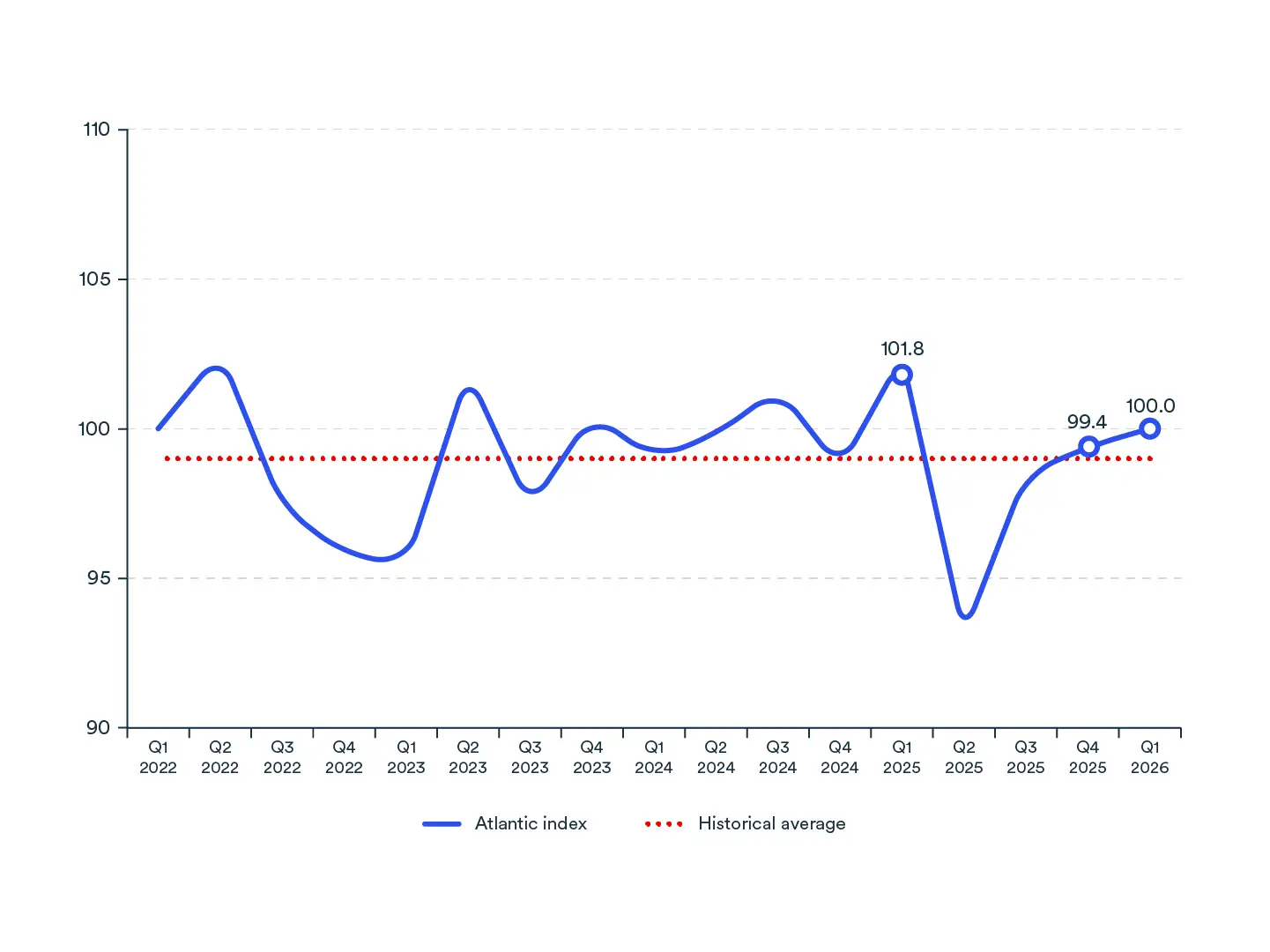

Atlantic: Optimism improves but SMEs stay defensive

Atlantic SMEs began 2026 with a more optimistic outlook, even as business conditions remained weaker than a year earlier. In Q1 2026, the regional index edged up to 100.0—slightly above its historical average—marking a tentative improvement after the sharp downturn in mid-2025.

The improvement was driven mainly by stronger confidence. SMEs reported a more favourable cash-flow position and economic outlook, suggesting that sentiment began to stabilize after several quarters of heightened uncertainty.

Despite this renewed optimism, growth plans remained cautious. The business environment continued to weigh on the index, while declining business and financial trade openings restrained growth projections, which remained well below last year’s levels. Rising credit utilization also weighed modestly on credit performance, as financial conditions had yet to fully normalized.

Although the removal of Chinese tariffs on Canadian seafood products was not reflected in the Q1 data, it is expected to support activity in the coming quarters. This is a welcome development amid ongoing uncertainty related to global trade conditions and volatile oil prices.

Component contribution to the growth of the Small Business Health Index for Atlantic provinces, Q1 2026, percentage points

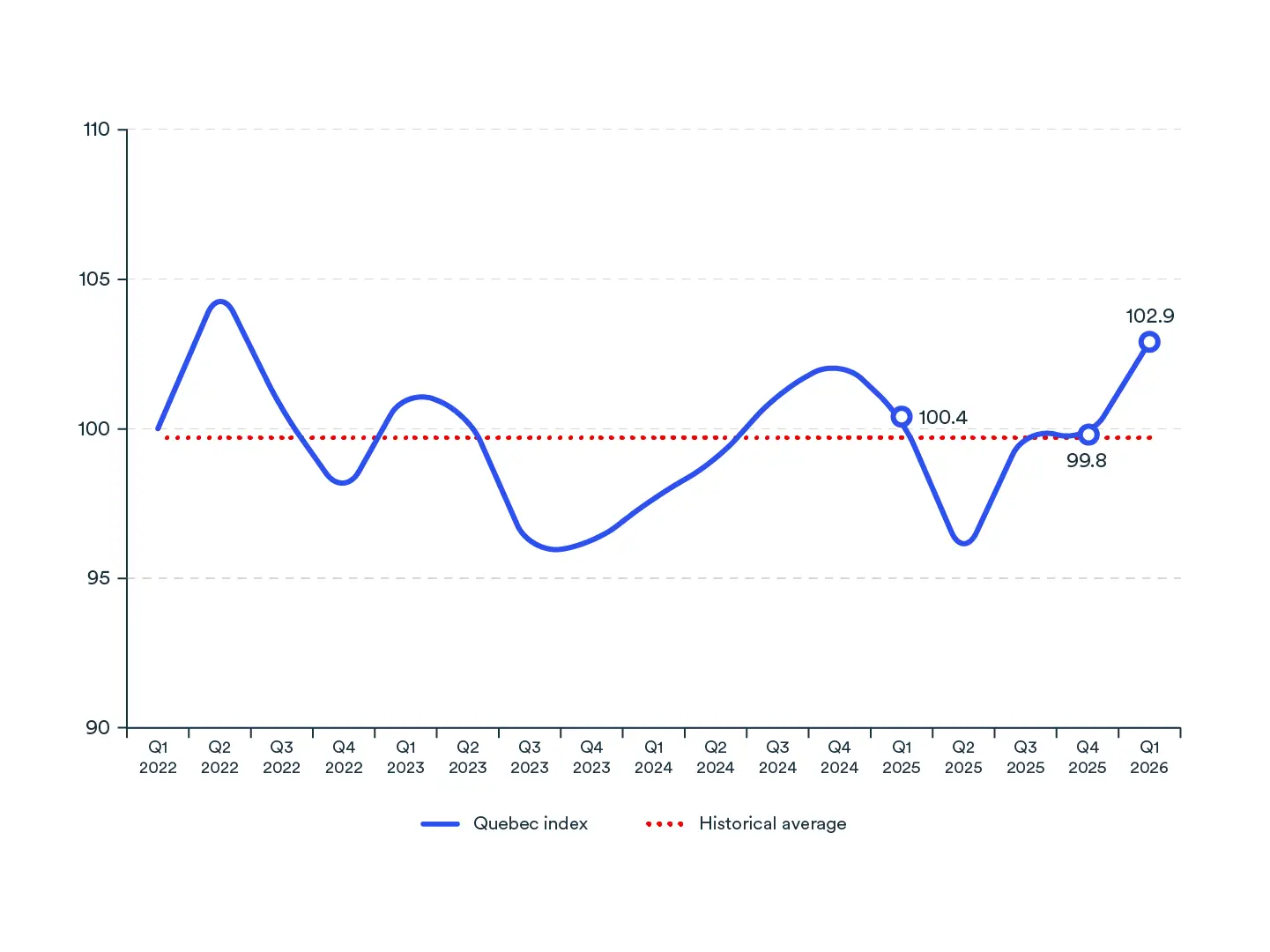

Quebec: SMEs regain their footing in early 2026

Quebec SMEs began 2026 on firmer ground, supported by renewed confidence. The regional index climbed to 102.9, well above its historical average and its highest level in more than three years.

The improvement was driven by two forces moving in tandem. Sentiment rebounded sharply from the steep decline experienced in Q2 2025, when trade tensions weighed heavily on expectations. As the economic impact of tariffs proved more limited than initially anticipated, SMEs reported stronger cash-flow expectations and a more optimistic outlook for the economy. The business environment also contributed positively, supported by firmer wage growth.

Despite these broad-based gains, growth projections remained the main area of weakness. Investment intentions and hiring expectations stayed subdued, suggesting that many Quebec SMEs had yet to translate their improved confidence into concrete expansion plans.

With trade uncertainty still present and volatile oil prices continuing to cloud the outlook, the durability of this recovery remains to be confirmed.

Small Business Health Index, Quebec

Component contribution to the growth of the Small Business Health Index for Quebec, Q1 2026, percentage points

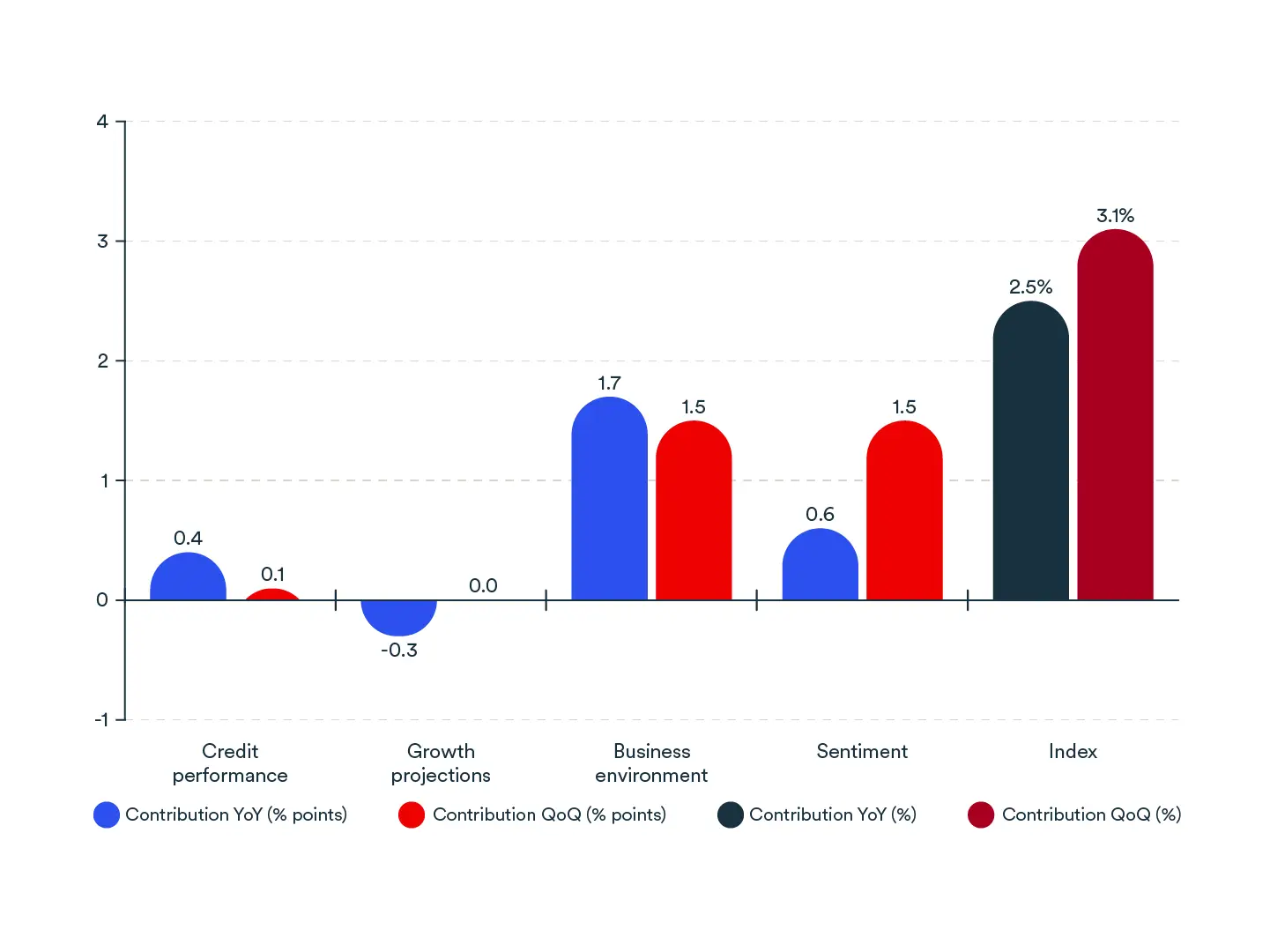

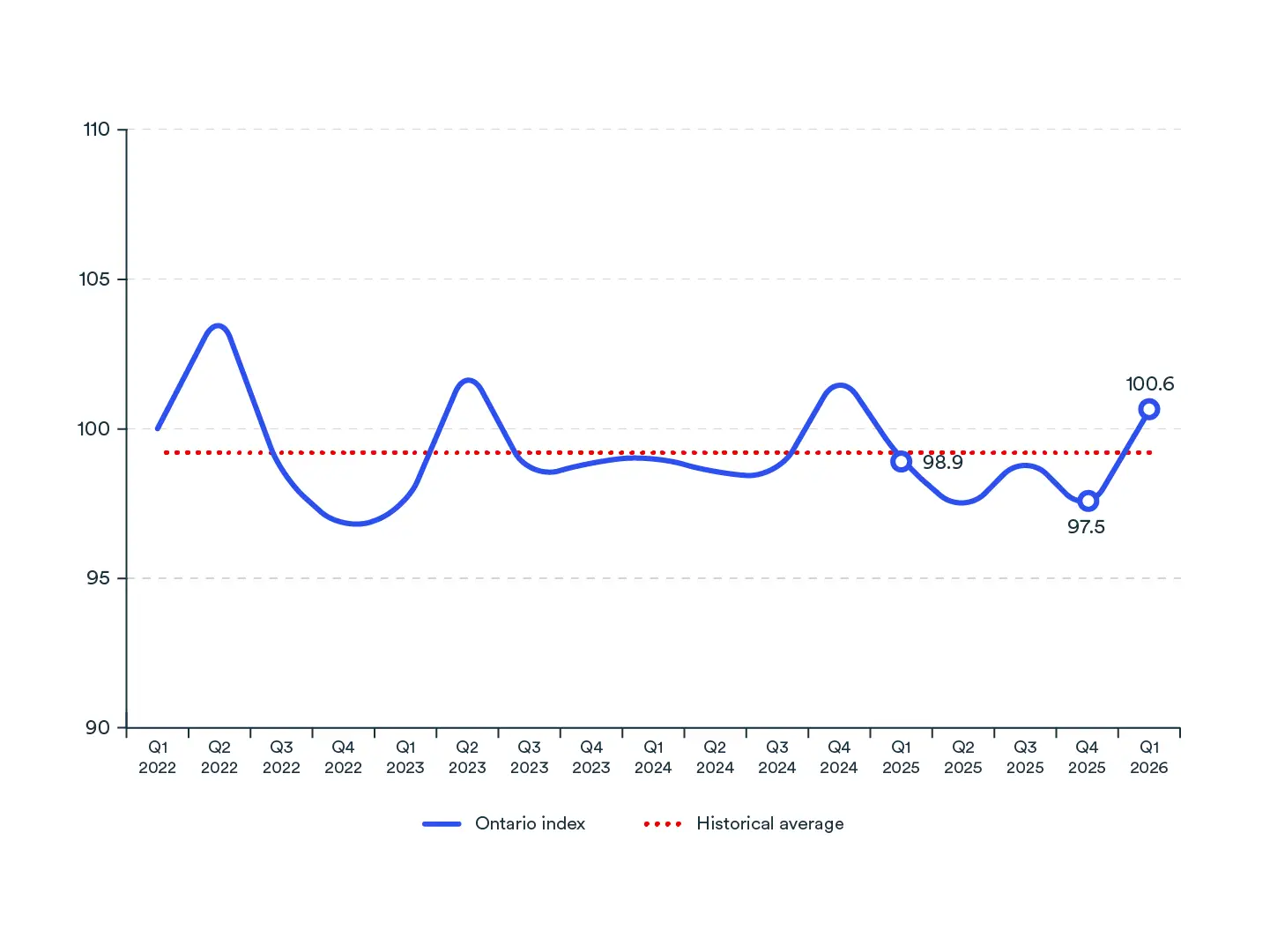

Ontario: A broad-based rebound to start the year

Ontario's index rose to 100.6 in Q1 2026, up 3.2% from the previous quarter and 1.7% from a year earlier, pushing it back above its historical average of 99.2.

The recovery was broad-based, with all four components improving on a quarterly basis. Sentiment led the rebound as SMEs reported stronger cash-flow conditions, supported by continued growth in consumption in 2025, alongside improving economic expectations following the sharp decline in late 2025.

The business environment and growth projections also contributed to the upturn, while credit performance improved modestly. On a year-over-year basis, the business environment stood out as a key source of strength, while growth projections and sentiment remained slight drags. This suggests that confidence has not yet fully returned to early-2025 levels.

Ontario avoided the worst in 2025, supported by several measures that helped sustain growth and allowed businesses to adapt to their new context. However, uncertainty remains elevated, and new headwinds have emerged, dampening the improvement seen at the start of the year.

Small Business Health Index, Ontario

Component contribution to the growth of the Small Business Health Index for Ontario, Q1 2026, percentage points

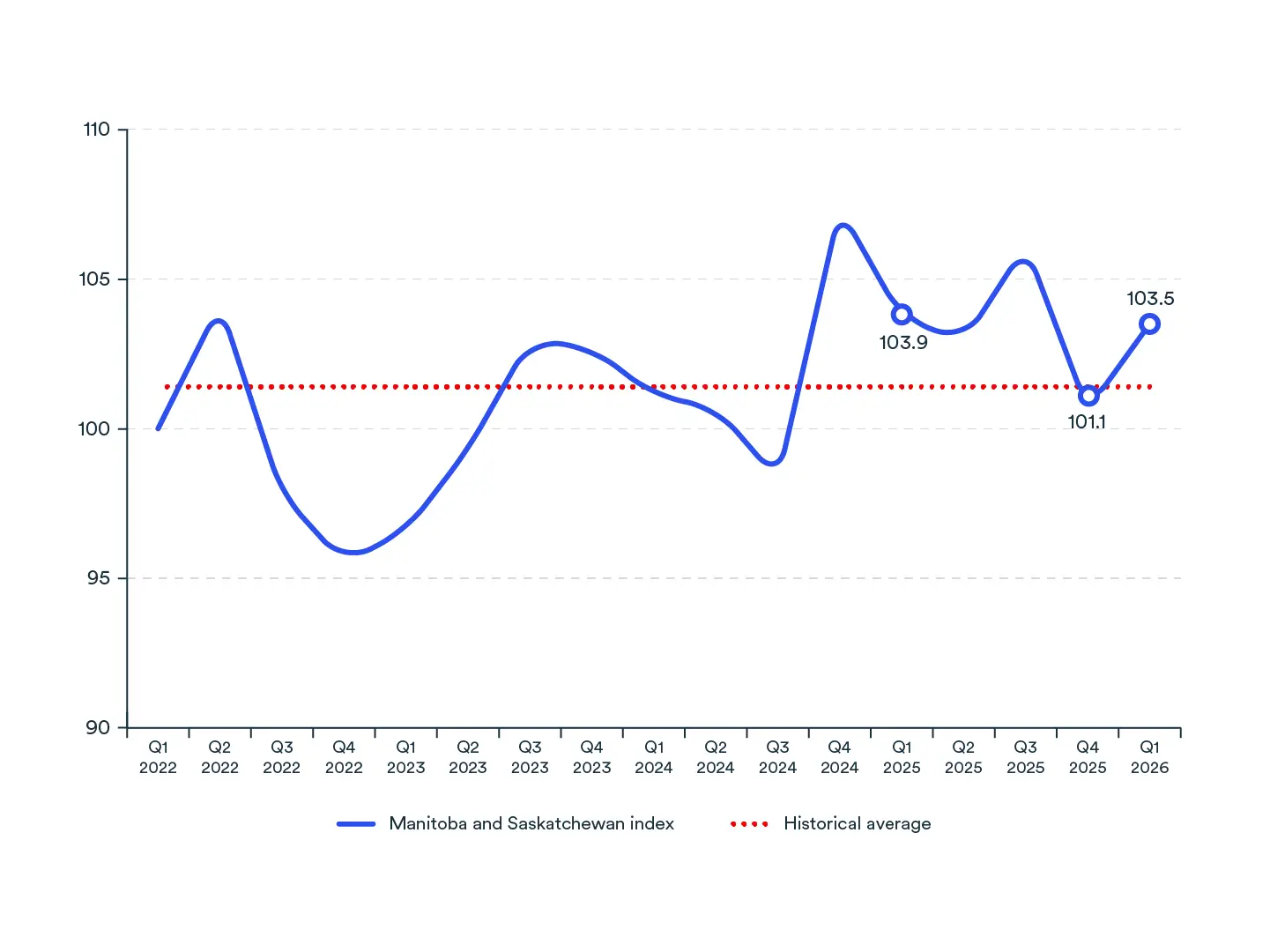

Manitoba and Saskatchewan: Momentum resumes after a year-end pause

SMEs in Manitoba and Saskatchewan began 2026 positively, as the regional index rose to 103.5, above its historical average and among the highest readings across all regions. Sentiment and growth projections both rebounded from their year-end pullback, while stronger financial trade openings and business openings pointed to improving activity on the ground.

The region's resilience continued to be underpinned by a a solid business environment, supported by employment and wage growth in both provinces. This provided a steady anchor following a challenging year in 2025. Despite the encouraging quarterly rebound, sentiment remained below last year’s level, indicating that uncertainty had not fully dissipated heading into the new year.

Small Business Health Index, Manitoba and Saskatchewan

Component contribution to the growth of the Small Business Health Index for Manitoba and Saskatchewan, Q1 2026, percentage points

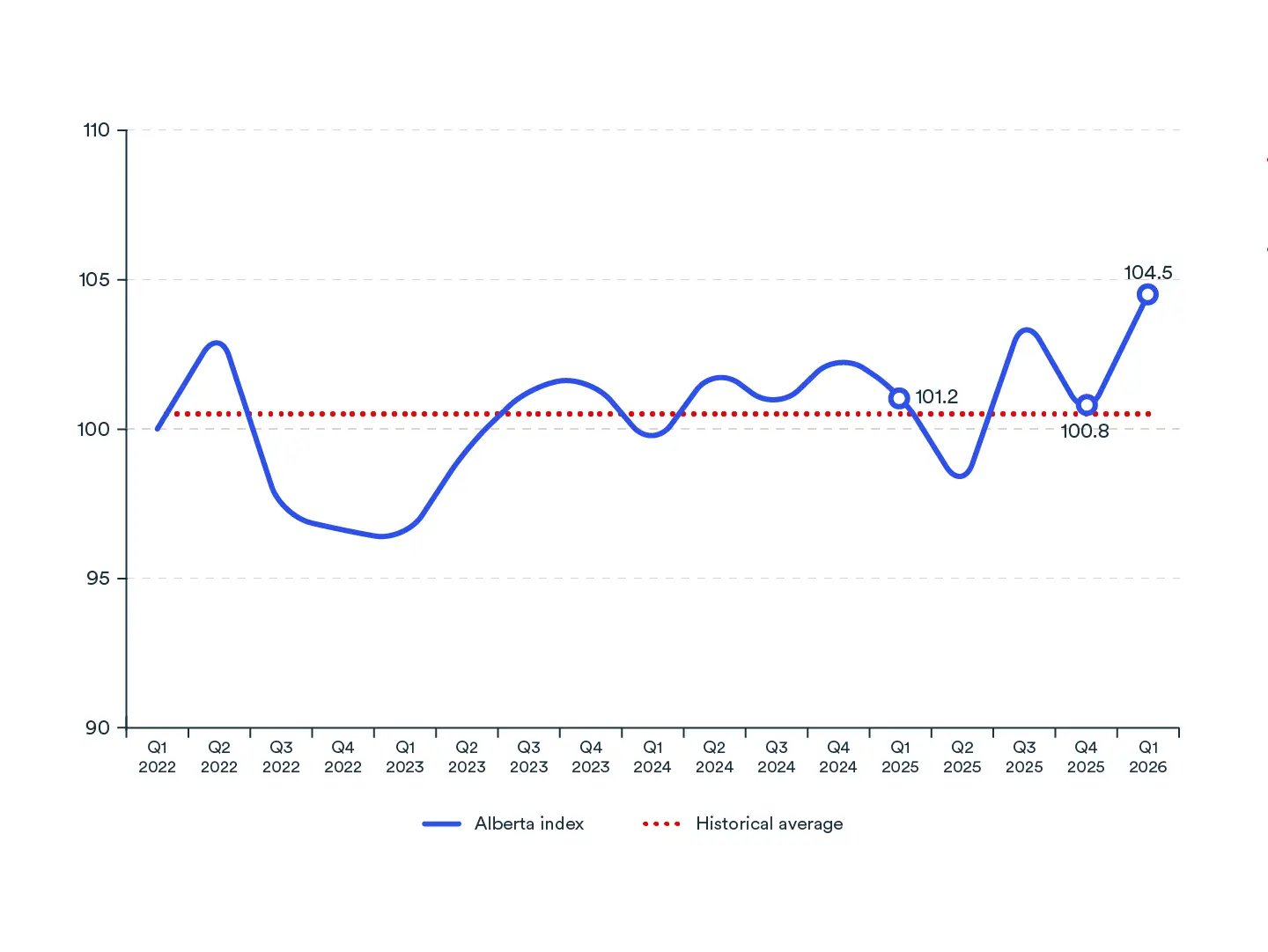

Alberta: A bright spot amid national uncertainty

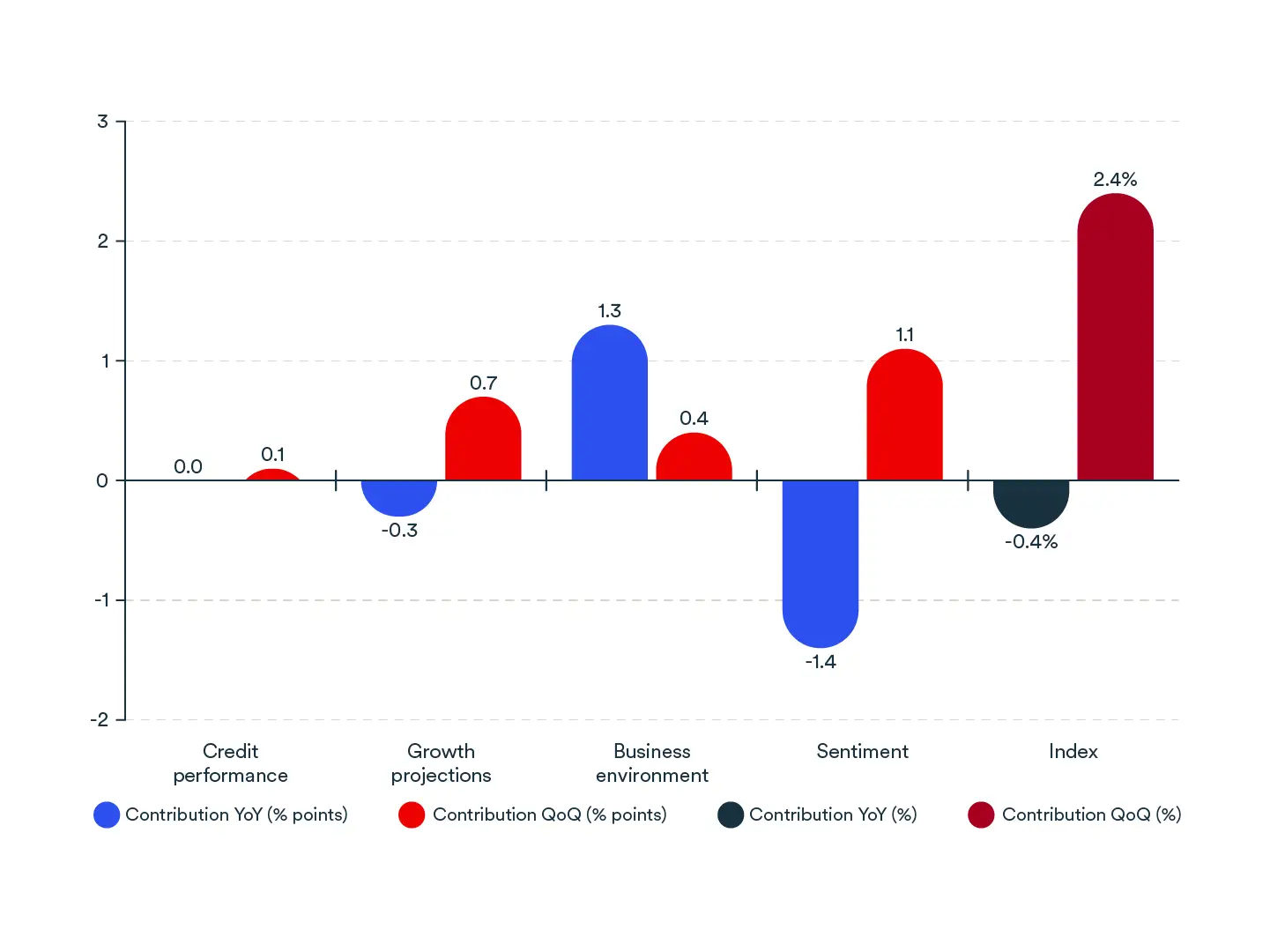

Alberta SMEs began 2026 with the strongest index reading across all regions, as the overall index rose to 104.5, its highest level since the series began. The quarter was marked by a sharp rebound in sentiment, alongside a business environment that continued to strengthen. Persistent employment and wage growth helped set Alberta apart from the rest of the country.

Growth projections, however, remained a key area of weakness. Lower business openings, along with declining investment and hiring intentions, weighed on expectation. This suggests that Alberta SMEs, even with their strong footing, remained cautious about expanding in the near term.

Despite the encouraging quarterly rebound, sentiment remained essentially unchanged from a year earlier, indicating that uncertainty had not fully lifted. As a major oil-producing province, Alberta could nonetheless benefit from recently rising oil prices, which may provide a potential tailwind as the year unfolds.

Small Business Health Index, Alberta

Component contribution to the growth of the Small Business Health Index for Alberta, Q1 2026, percentage points

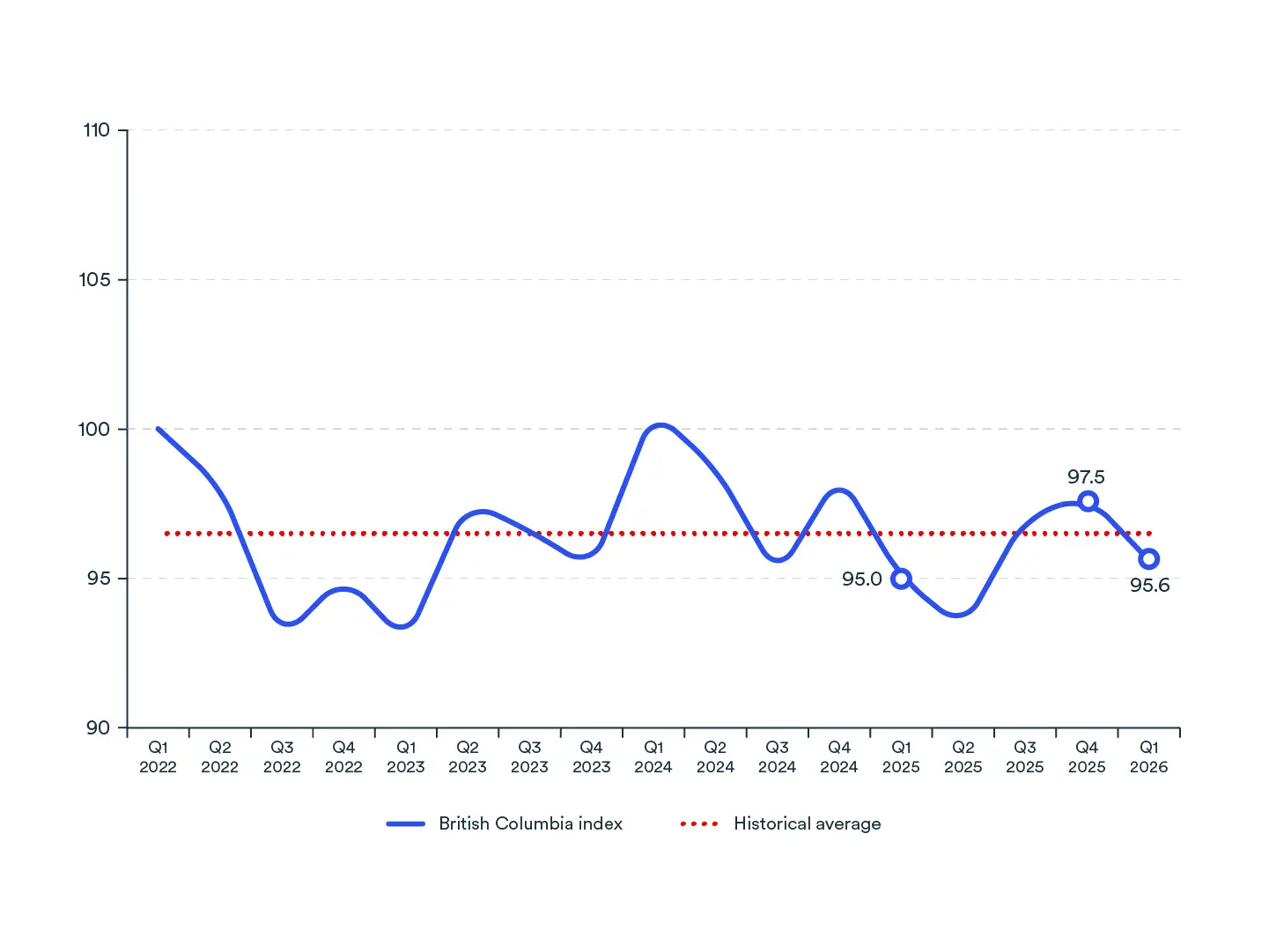

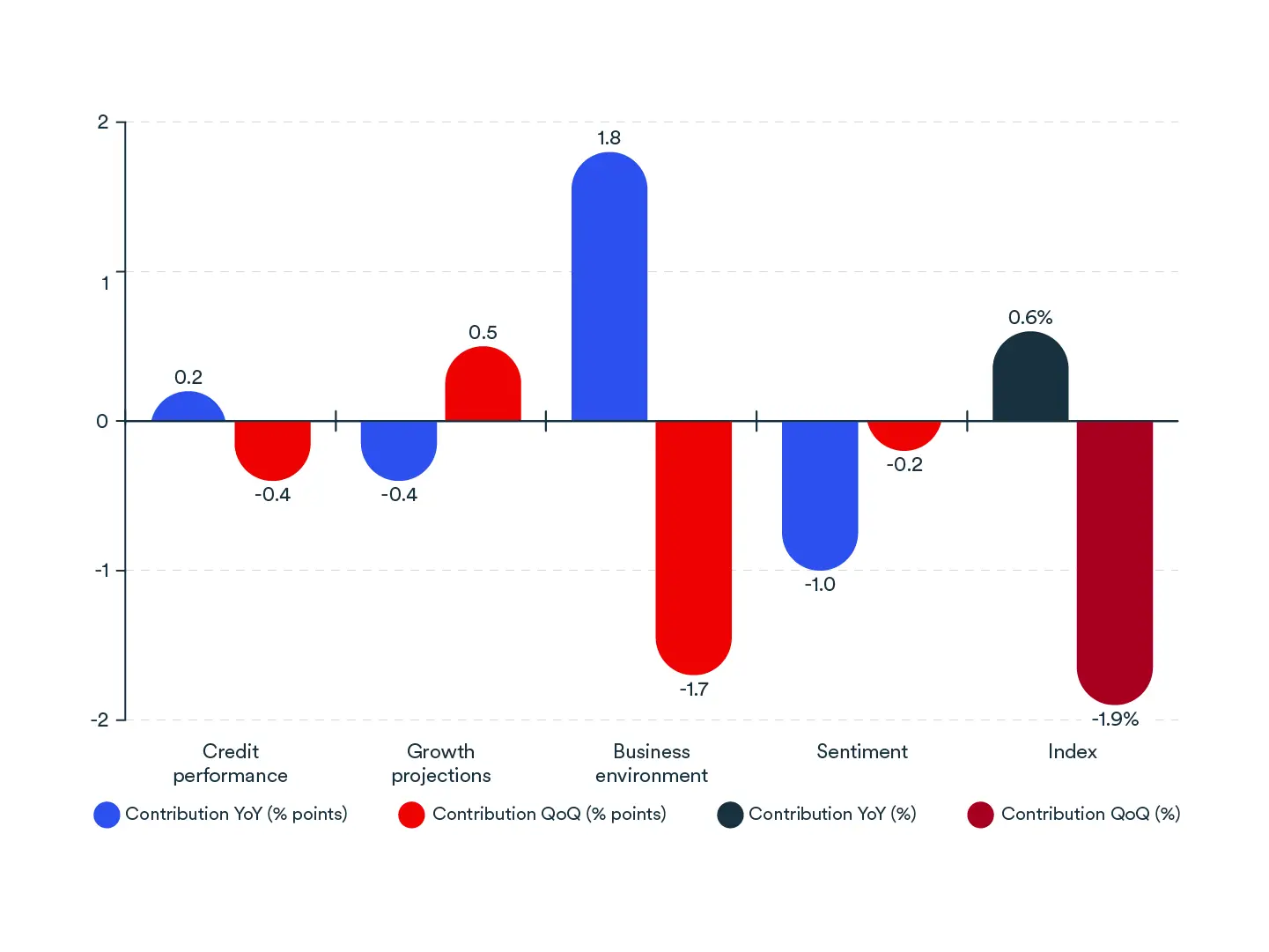

British Columbia: A contained decline and mounting pressure

British Columbia SMEs faced a more challenging environment in Q1 2026, as the regional index slipped to 95.6, making it the only region to fall below its historical average. The quarterly decline was driven mainly by a weakening business environment, reflecting job losses and slower wage growth.

Sentiment also remained subdued, staying below its 2025 level as SMEs continued to report cautious expectations for both cash flow and the broader economic outlook. On the credit side, rising bankruptcies and higher supplier trade delinquencies added further pressure, pointing to gradually tightening financial conditions.

Growth projections provided a modest offset, improving on the quarter, though lower business openings limited the overall gain. Despite the difficult quarter, the index remained slightly above its level a year earlier, suggesting that the deterioration, while meaningful, has not yet reversed the gradual recovery seen through 2025.

Small Business Health Index, British Columbia

Component contribution to the growth of the Small Business Health Index for British Columbia, Q1 2026, percentage points

For additional information on the methodology, please consult this document.