Line of credit

A line of credit is convenient for bridging gaps between the points when accounts payable are settled and accounts receivable are collected.

A company must make monthly interest payments on any money it borrows through its line of credit and can pay down the balance over time out of its cash flow.

For a small business, the line of credit is simple to understand. “When you use your line of credit, there’s interest to pay. Once you’ve repaid the line of credit, there’s no interest to pay,” explains Simon Brassard, Manager, Major Accounts, BDC. “Then, you don’t have to make monthly payments to repay the principal. The company can go forward according to its capability.”

It’s more complex for larger business, because the financial institution uses collateral-based lending. “It will authorize an amount that can be quite high, but the actual amount that can be used from the line of credit each month is always adjusted according to the amount and quality of the company’s accounts receivable and inventory, which are, in fact, collateral,” says Brassard.

Often secured by inventory and accounts receivable, lines of credit are considered “demand” loans, meaning the financial institution can demand full repayment at any time. To ensure it will be repaid, the bank will often include a claim on the company’s inventory and accounts receivable as part of the loan agreement. This makes bank loans “secured” by the company’s main current assets.

How does a line of credit work?

A line of credit is convenient for financing your short-term needs. “It certainly varies depending on your business model. But typically, we’re talking about the supplies you need to make and sell your products,” says Brassard.

He gives the example of a distribution company that buys $200,000 worth of inventory. The company takes this amount from its line of credit until it receives the merchandise and sells it. Let’s say two months go by.

“The company will have paid $200,000. But depending on its profit margin, it may have gotten $250,000 by reselling the inventory,” says Brassard. “The company will therefore put $200,000 back into its line of credit and keep the $50,000 profit to pay its fixed costs and reinvest in its working capital. Its goal will be to eventually have enough working capital to buy inventory without using its line of credit.”

Mistakes to avoid when using a line of credit

You should avoid using your line of credit to finance long-term expenses, like buying a machine.

“The reason is simple,” says Brassard. “Unless you quickly resell the machine, you won’t have a quick cash inflow after the purchase to repay your line of credit. The line of credit room used up by this long-term purchase will no longer be available to finance your business operations. You’ll be stuck—which is not good. You need to keep that cash flow to support your business growth.”

The golden rule is to finance short-term expenses with short-term credit and to finance long-term assets with long-term debt.

Simon Brassard

Manager, Major Accounts, BDC

How to calculate line of credit interest rates

Interest on a line of credit is calculated on a daily basis. So if the annual posted interest rate is 5%, to find the daily rate, you need to do this calculation:

5% annual rate / 365 days in a year = 0.01369863% per day

Going back to the example of a $200,000 line of credit repaid in full 60 days later, the following calculation would tell you how much interest you’d need to pay:

$200,000 X 0.01369863% = $27.40 of interest payable each day

$27.40 X 60 days = $1,644

If you pay back half the amount after 30 days, the interest calculation should be adjusted as follows:

$200,000 X 0.01369863% = $27.40 of interest payable each day

$27.40 X 30 days = $822

+

$100,000 X 0.01369863% = $13.70 interest payable each day

$13.70 X 30 days = $411

Total interest payable for 60 days = $1,233

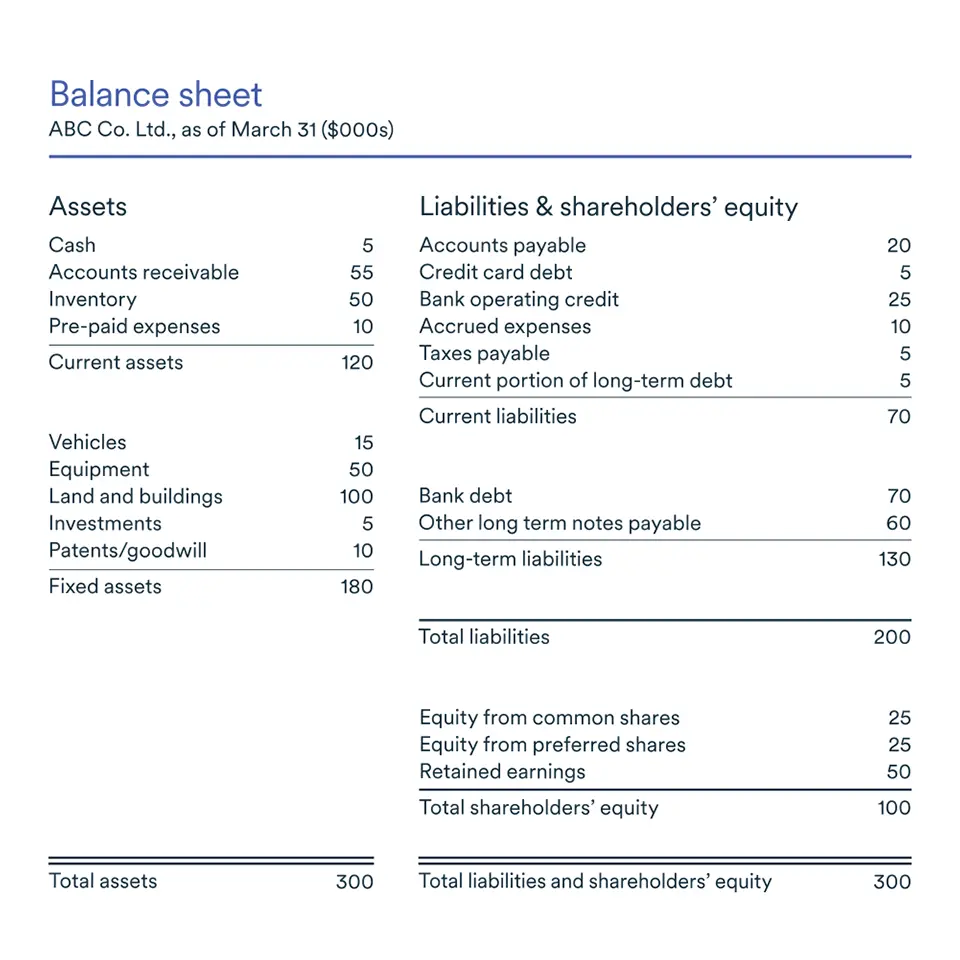

Where is the line of credit entered in the financial statements?

Lines of credit appear under liabilities on the balance sheet. They are considered current liabilities because they must be paid within the current 12-month operating cycle.

The excerpt below shows where lines of credit appear on a company’s balance sheet, along with various other current liabilities. Each type of loan or credit has its own payment terms.

How to get a line of credit?

When you start your business, you typically apply for a business credit card. Often, the bank will give you a line of credit as well.

“The bank will look at your personal credit rating and net worth to determine the line of credit amount,” says Brassard. “However, if you have a lot of debt and a bad credit rating, the financial institution may refuse to give you a line of credit.”

Subsequently, the line of credit will be increased based on the company’s performance. “The greater the company’s collateral and turnover, the more it can increase its line of credit,” says Brassard. “It certainly depends on each situation, but, as a rule, the line of credit you obtain is about 10% of revenues.”

When a company requests a very large line of credit, it can purchase a guarantee from lenders, such as Investissement Québec and Export Development Canada (EDC). This is an insurance premium that increases the interest cost of a line of credit, but allows companies to obtain larger loan amounts.

“When a bank is reluctant to grant a line of credit, it may be reassured if the company gets a guarantee for, say, 50% of the amount,” says Brassard. “It will also have the accounts receivable and inventory as collateral.”

When we’re talking about a large authorized amount, around $1 million, the actual amount of the line of credit will be readjusted each month based on its inventory and accounts receivable.

Simon Brassard

Manager, Major Accounts, BDC

What is the difference between a credit card and a line of credit?

For a small business, the two are very similar. But for a larger business, it’s a little different.

“When we’re talking about a large authorized amount, around $1 million, the actual amount of the line of credit will be readjusted each month based on its inventory and accounts receivable,” says Brassard.

There are businesses where these elements vary greatly, such as a pool store that needs to stock up on products in the winter to be ready to meet demand in the spring.

“The store may start by reinvesting its profits from the year just ended to buy new inventory. But to grow, it will need to buy more inventory,” says Brassard. “It will therefore finance this inventory through the line of credit. Previously purchased inventory will serve as collateral, and so will accounts receivable as customers purchase pools.”

For small businesses, the authorized amount does not vary from month to month, just like a credit card.

What’s the difference between a line of credit and a term loan?

A line of credit is much more flexible to use than a term loan.

Let’s take the example of a $75,000 loan amortized over five years, says Brassard. “The company will have to make payments each month to repay the principal and interest, but with the line of credit, there is no obligation to repay the principal. So the company could use $75,000 of its line of credit and just make the monthly interest payments.”

Generally, the interest rate is higher on a term loan than a line of credit. “But it still depends on the financial strength of the company and the level of risk assessed by the financial institution when granting the loan,” he says.

Sometimes, though, a line of credit is used to complement a term loan. Let’s take the example of a financial institution that grants a $350,000 term loan to a company for equipment purchasing

“If the company is $50,000 short of what it needs to buy the equipment, it could get that amount by having its line of credit increased,” says Brassard. “This isn’t too risky if the company knows that this equipment purchase will quickly generate additional revenue that will allow it to quickly repay the amount. However, it must ensure that it has sufficient room to continue purchasing inventory and pay its accounts payable.”

Since a line of credit is a flexible financing method, you should always make sure to use it wisely. When in doubt, don’t hesitate to ask experts.

How does a line of credit affect your company’s credit score?

Interest rate and credit score:

- The interest rate on a line of credit is usually variable, meaning it can fluctuate over time. Your credit score plays a role in determining the interest rate you’ll pay.

- Generally, the higher your credit score, the lower the interest rate on your line of credit.

Borrowing and repayment:

- When you use a line of credit, you’re essentially borrowing money. Any outstanding balance affects your credit utilization ratio.

- Making timely payments on your line of credit can positively impact your credit score.

- However, if you consistently carry a high balance or miss payments, it can have a negative effect.

Reporting to credit bureaus:

- Business lines of credit are typically not reported on your personal credit report. They are separate from personal credit cards or loans.

- However, some lenders may report business credit activity to commercial credit bureaus, which can indirectly affect your company’s creditworthiness.

Next step

Learn how forecasting sales and inventory and shortening customer payment terms can improve your cash conversion cycle. Download BDC’s free guide, Taking Control of Your Cash Flow.