Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreIs this the start of a new economic chapter?

After many gloomy months, interest rate cuts helped rekindle optimism among Canadian households and businesses over the summer. When confidence improves, the economy usually does too. Will it be the case this time around? What can we expect from the economy as the year draws to a close?

A slowdown created by rate hikes

Since 2023, Canada’s economy has been in a slowdown caused by tighter credit conditions. After more than a decade of low interest rates, households, businesses and governments had to relearn how to deal with much higher financing costs.

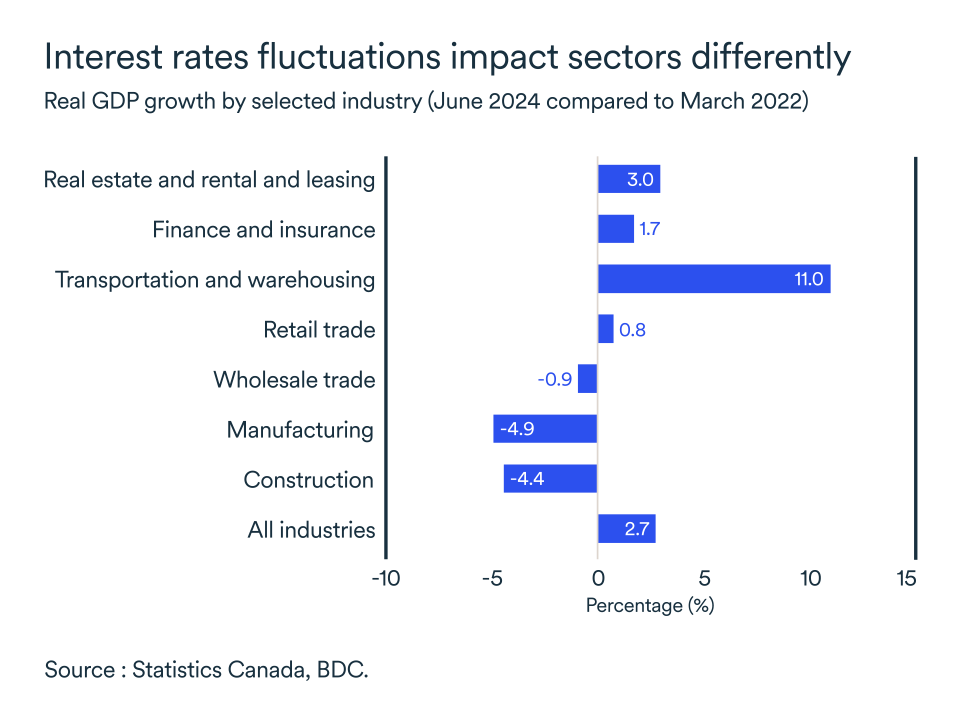

The sectors hardest hit by the slowdown have been those where activity is typically financed by borrowing (especially those linked to the real estate market and durable goods) along with ones that rely on discretionary consumer spending.

But now the tide has turned. The Bank of Canada has cut its key rate three times since June, bringing it to 4.25% from 5.0% with further cuts likely to come in the months ahead.

Naturally, we expect the sectors hardest hit by interest rate increases to benefit the most from cuts. However, regardless of the sector, consumers and businesses will have to be patient as they look for signs of an economic rebound. It will likely take several months before the economy regains momentum in the face of still high rates.

Real estate market on the mend

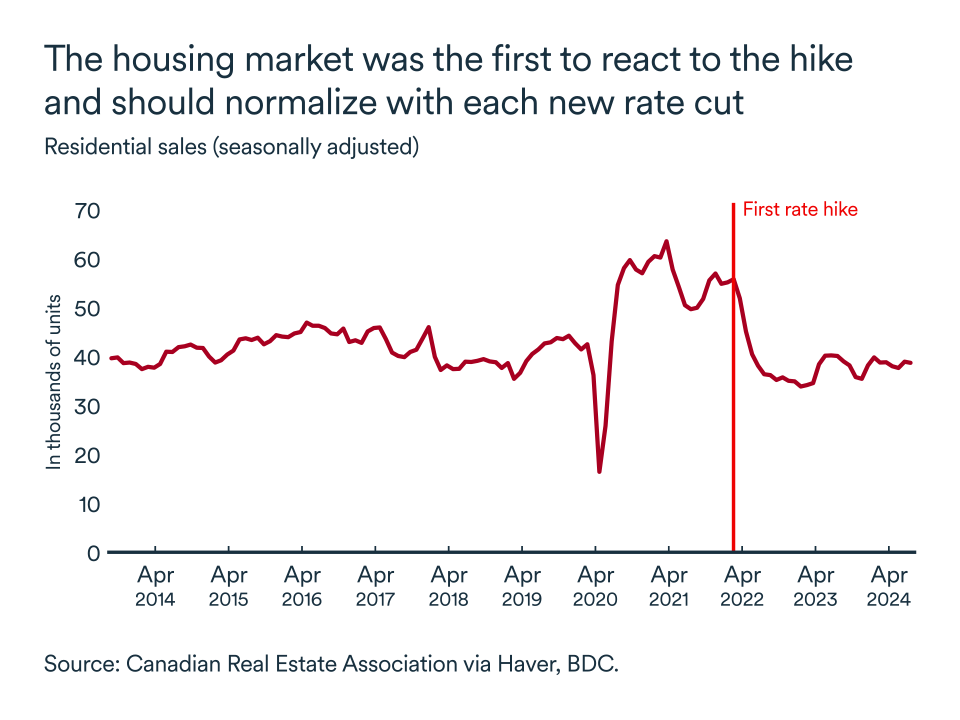

The sector that suffered the most from interest rate hikes is undoubtedly the real estate market. On the national level, higher rates brought home sales and prices down substantially in 2023.

Now, the market is on the rise again against a backdrop of strong demand for housing and limited supply. However, with today’s market being in better balance between buyers and sellers and rates still relatively high, we expect growth to be more moderate than in past years.

For the construction industry, ratcheting up activity to keep pace with record population growth is proving to be a challenge, even if overall permits and housing starts have held up well in recent months. In particular, the industry is grappling with sluggish productivity, high costs and a significant regulatory burden.

More rate cuts and a larger increase in housing starts will be needed to restore affordability in the country and ensure a sustainable recovery in the real estate sector. Since Bank of Canada rate cuts are already largely priced into five-year mortgage rates, the chances that they continue to decline significantly in 2024 is unlikely.

Household spending power improves

When it comes to discretionary spending, a host of unrelated industries depend on consumer confidence for their health. Since these sectors are non-essential, their fortunes are closely tied to the ups and downs of the economy. They include consumer durables, clothing and services such as hotels, leisure, restaurants and retailers.

With interest rates and inflation falling, household purchasing power is recovering, which should support modest growth in consumer spending. But once again, the recovery will take time. The labour market is no longer as strong as it was in recent years, which should limit wage increases and by extension, consumer spending.

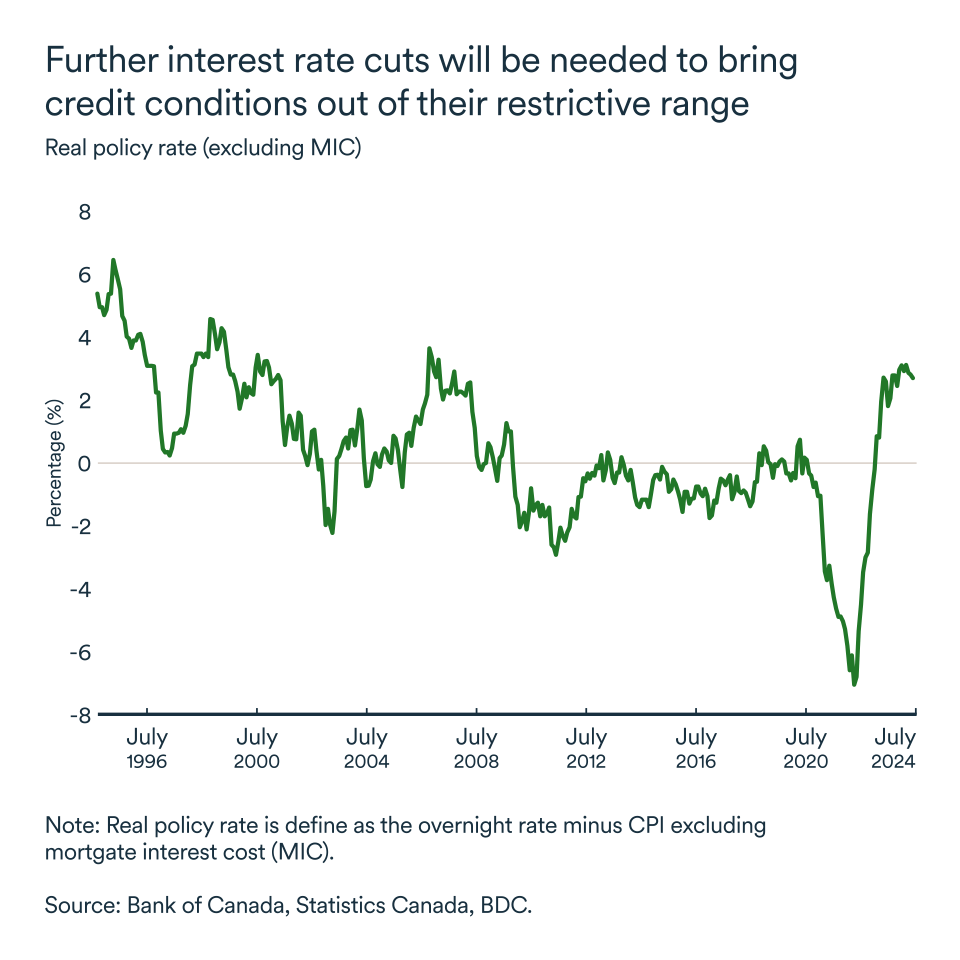

Taking these trends together, we expect economic growth in Canada to continue to be below potential, despite the rate cuts. This is because demand continues to be restrained by past rate hikes. Many mortgages have been renewed at higher levels, real interest rates are still in the restrictive zone (a level that encourages saving over borrowing), and demand for workers is waning.

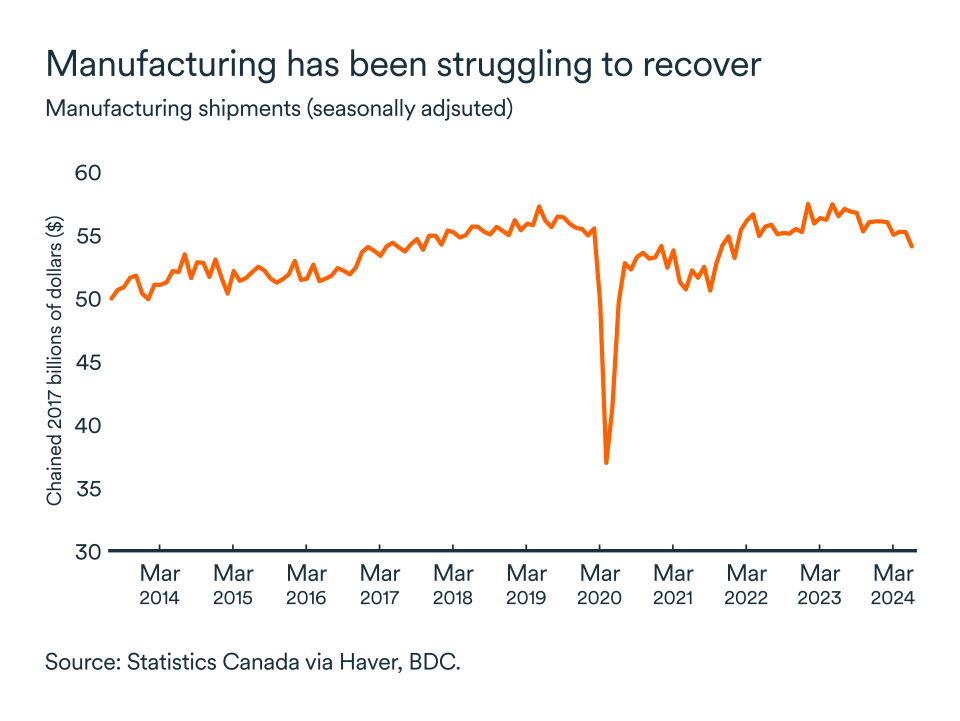

Manufacturing remains weak

One key area of concern is manufacturing. The sector never really recovered from the pandemic and activity remains sluggish by historical standards.

The sector is significantly more exposed to the U.S. economy than others, with manufactured goods accounting for 65% of all the Canadian exports of good heading south of the border, and an economic slowdown in the U.S. is currently underway.

At the same time, financing conditions are still difficult for companies, crimping investment and hurting demand for machinery and materials. Canadian manufacturers continue to report subdued demand and this is generating uncertainty and a general reluctance on the part of companies to engage in new development projects.

The impact on your business

Interest rate cuts have improved household and business confidence, which bodes well for the economy. However, businesses should remain cautious. The recovery will be gradual in the months ahead as the economy comes in for a soft landing. Full recovery will take time and sectoral challenges will persist.

Interest rate sensitive sectors: Sectors such as real estate and durable goods, which rely heavily on borrowing, should benefit from rate cuts. Companies in these sectors can look forward to improved financing conditions and demand.

Consumption as a growth driver: Consumption is a key factor for economic growth. Businesses need to monitor consumer trends and adapt their strategies accordingly. Household budgets remain tight.

Challenges in the real estate sector: While lower rates should stimulate the real estate market, challenges persist for the construction industry where companies are dealing with low productivity, high costs and restrictive regulations.

Limited impact on mortgage rates: Rate cuts are already largely reflected in five-year mortgage rates, so a further significant drop in mortgage rates in 2024 is unlikely.

Manufacturing sector in difficulty: Canada's manufacturing sector continues to face stiff headwinds. Companies in this sector must be prepared to manage slow demand and persistent uncertainty.

In short, companies need to remain vigilant and ready to adapt to changing conditions. Prepare your strategy and positioning to avoid missing out when the recovery gathers momentum next year.

Is a soft landing still achievable?

The Canadian economy is navigating a complex landscape marked by cautious optimism about a recovery on one hand and persistent challenges on the other. Both sides are pointing toward the same outcome: more interest rate cuts in the months ahead.

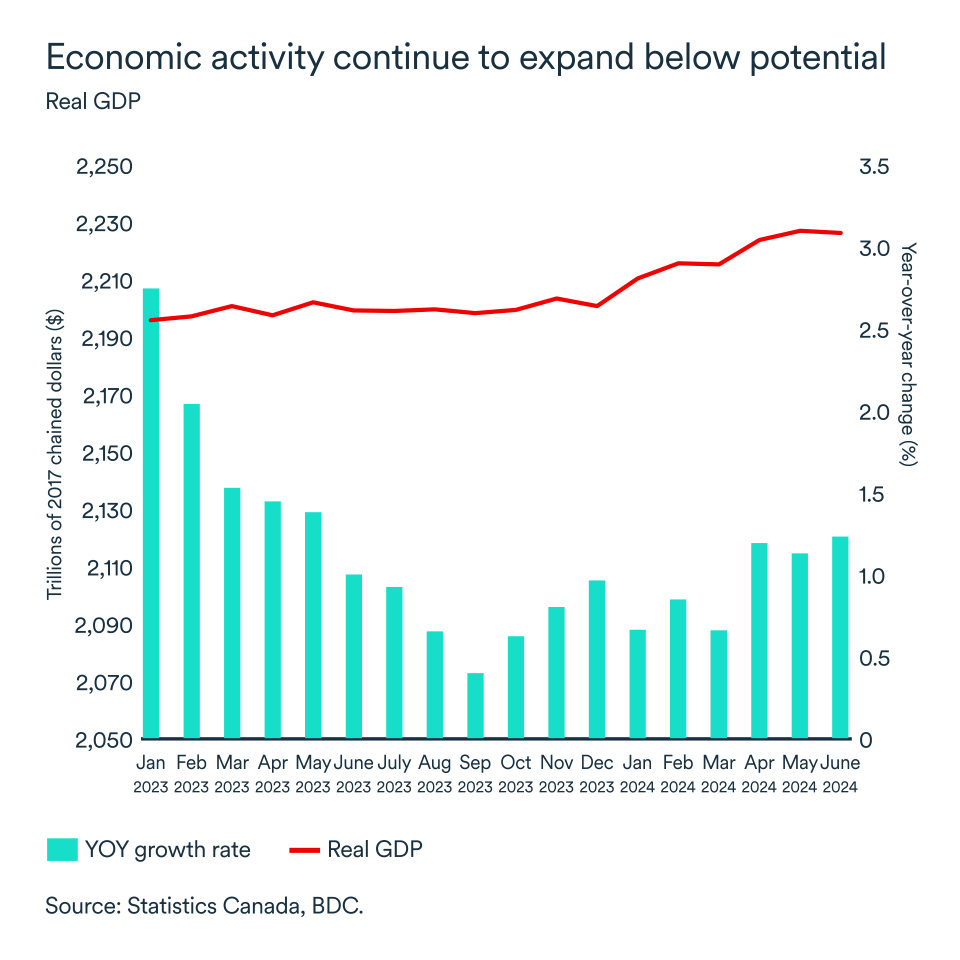

Leading indicators suggest the economy could very well continue to grow in the second half of the year, albeit at a slow pace. The economy is still grappling with the effects of high debt servicing costs. As a result, BDC Economics continues to forecast real GDP growth of just 1.0% for the whole year, reflecting an economy that’s essentially in neutral.

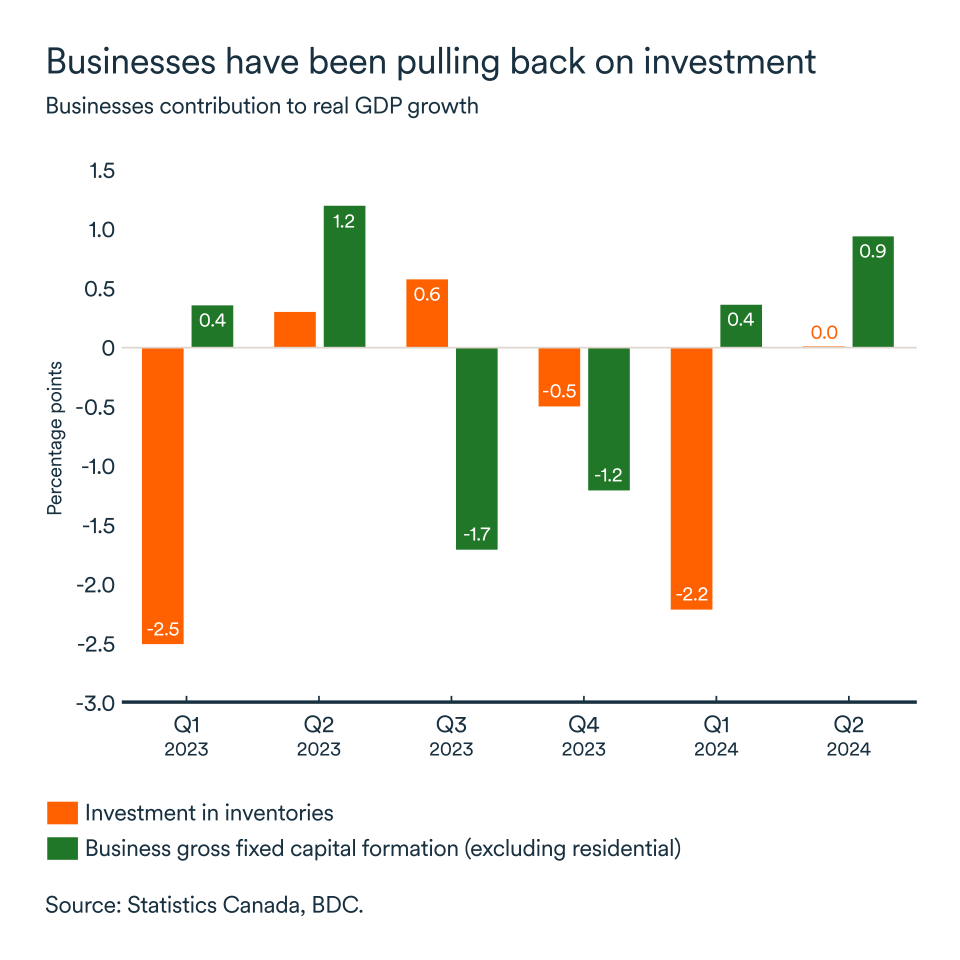

Slow business investment in the second quarter

High interest rates have produced weak demand in the economy and generated uncertainty among businesses. As a result, business investment has struggled to recover from the lows reached at the end of 2023, dampening economic momentum.

One significant factor that hurt GDP growth in early 2024 was the reduction in business inventories. Companies faced difficulties clearing excess stock accumulated in 2023, which reduced growth by 2.2 percentage points in Q1 alone.

Business investment has regained some strength since, with Q2 non-residential business investment surging 11.1% on an annualized quarterly basis. However, it will take much more growth to make up for past investment shortfalls. Lack lustre investment will reduce the ability of Canadian businesses to take advantage of the recovery when it gathers steam in late 2025.

Interest rates remain high… at least for now

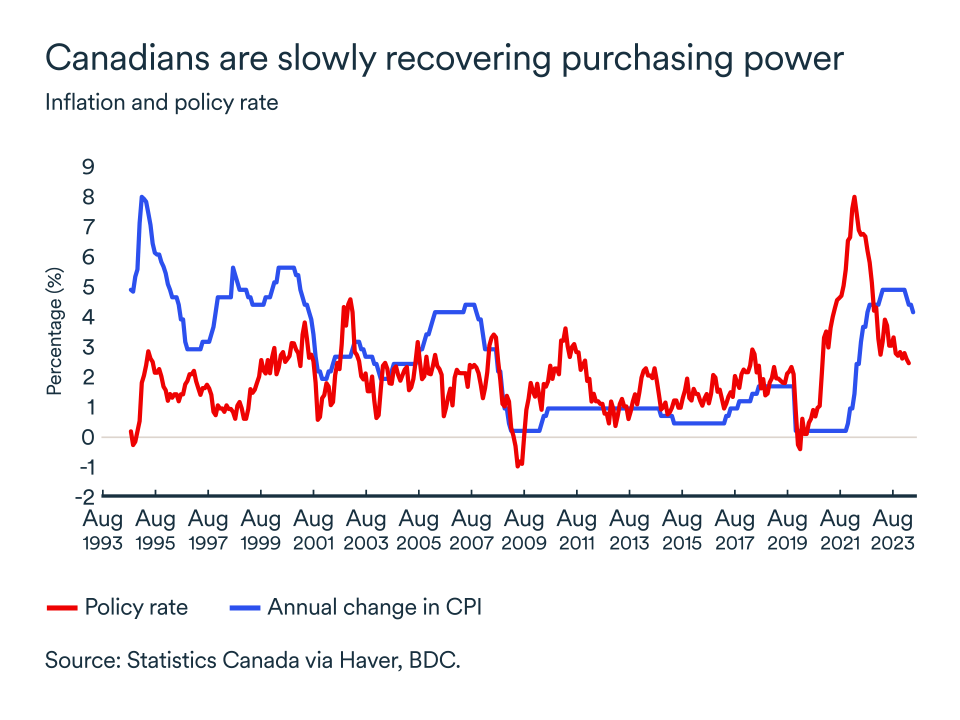

One of the most significant developments in the Canadian economic landscape has been the series of interest rate cuts enacted by the Bank of Canada. Since June, the bank has reduced its policy rate three times, bringing it down to 4.25% from 5.0%.

Further cuts are anticipated, with projections suggesting the policy rate could close 2024 at 3.75%. These rate cuts are a response to the slowdown in key economic indicators, including inflation and employment.

Inflation is the focal point of monetary policy and it continued to fall this year, reaching 2.5% in July. This progress reflects the Bank of Canada’s tight monetary policy stance and the normalization of the supply-demand balance in Canada. With inflation largely under control, the bank’s focus has now shifted to supporting economic growth and the job market in an effort to ensure sustainable price growth through lower interest rates.

Despite recent rate cuts, interest rates are still considered restrictive because at their current level they encourage saving over borrowing.

Cuts to the bank’s policy rate are typically aimed at stimulating economic activity by making borrowing cheaper for households and businesses. However, the real impact of these reductions takes time to fully materialize. (See our main article for further details.)

Households and businesses will continue to exercise caution in their spending and investment plans, awaiting more substantial rate reductions.

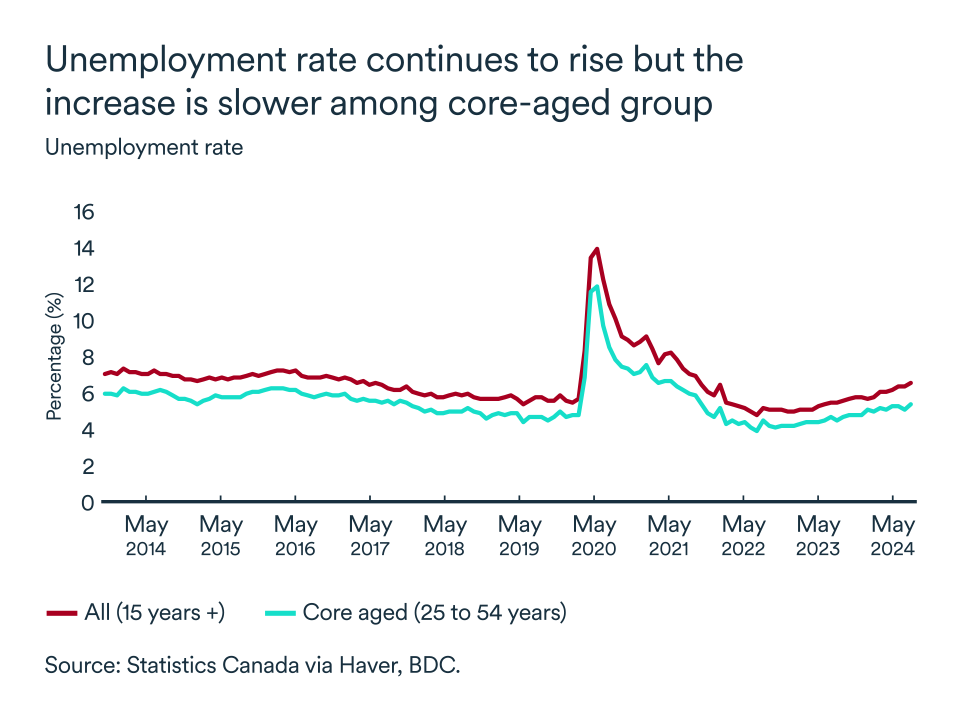

Labour market loses steam

The labour market is finally feeling the effects of high rates. While job creation was strong in the second quarter, with 115,000 new jobs, the national unemployment rate still increased to 6.4%.

While more entrants into the labour force explained part of the increase, employment gains slowed significantly in July and August. Job vacancies also took a dive.

These trends indicate that while the labour market is normalizing, it remains fragile and susceptible to economic fluctuations. Entrepreneurs should find some relief in expectations of lower wage growth in the coming months.

The impact for your business

- We still believe a soft-landing scenario is the most more likely. Therefore, businesses should expect a gradual recovery. However, high interest rates, weak demand and cautious business investment continue to weigh on economic growth.

- By contrast, positive signs such as strong government and consumer spending, along with a controlled inflation picture, are grounds for cautious optimism for business owners.

- The Bank of Canada’s continued efforts to lower interest rates will be crucial in supporting the recovery and steering the economy towards a more robust growth trajectory. Make sure your business plan is ready for takeoff as investment plans and strategic deployment don’t happen overnight.

Towards a first rate cut in September

The U.S. economy grew by 3.0% in the second quarter and the latest estimates point to more modest growth in the third quarter—around 2.0% at the time of writing (which is still solid under the circumstances).

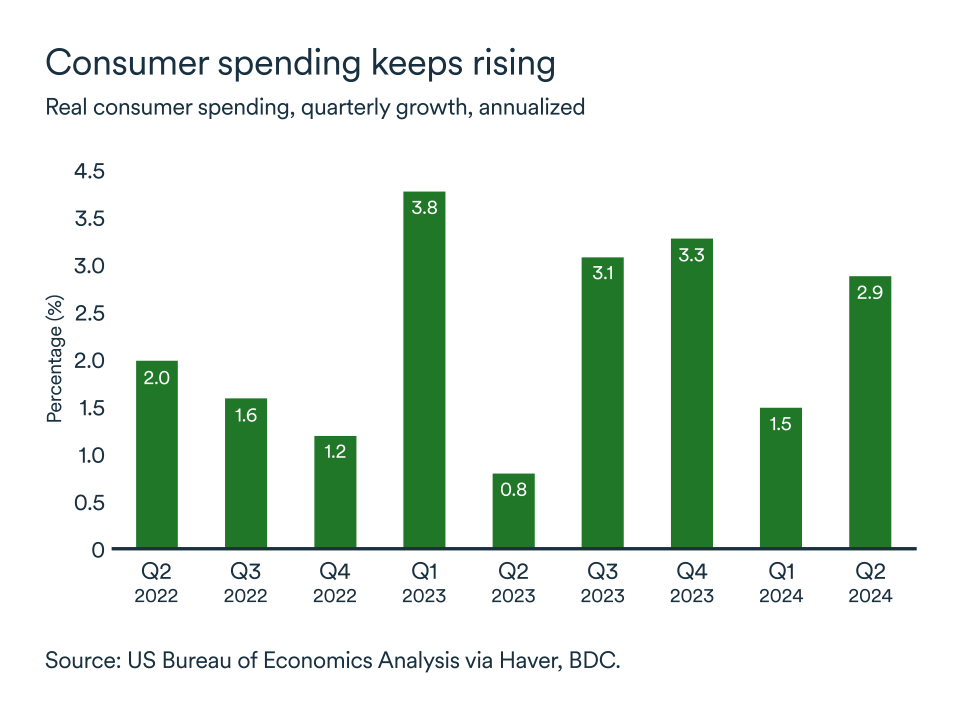

Consumer spending on the rise

Real consumer spending continued to rise in the second quarter, increasing to a rate of 2.9% compared with the first three months of the year. The U.S. economy continues to benefit strongly from household spending.

Another piece of good news was that the increase in consumption was not accompanied by a sharp rise in prices.

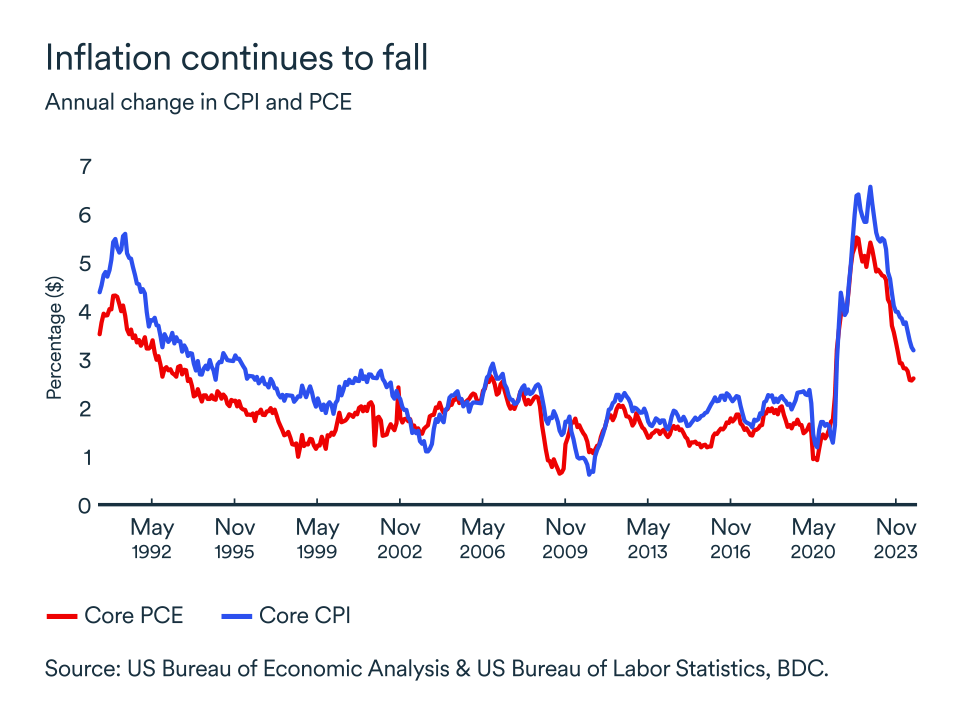

Core PCE inflation held steady at 2.6% in July, while the consumer price index continued its downward slide to 3.2%. Core PCE inflation is the Federal Reserve's preferred inflation measure in gauging progress toward its 2% target. It has held steady for the past three months, setting the stage for a first Fed rate cut this month.

The downside for households was that growth in real personal disposable income remained moderate. As a result, the savings rate fell from 3.1% to 2.9%, a new low for the U.S. economy in the current cycle. This raises the question: how much longer can households keep up their pace of spending?

Interest rates no longer need to be so high

Households may soon get help in paying down their debts since a rate cut is widely expected in the next Federal Reserve announcement in mid-September. Overnight rates could fall by 0.25 points from their current level of 5.25% to 5.50%.

Investor concerns about the health of the economy have intensified of late, contributing to a pullback in global stock markets. While stock markets are anticipating a September rate cut, some are forecasting a 50-basis-point drop, which we think may be overly optimistic. Although possible, such a large cut seems unlikely given the inflation picture.

A return to normal in the labour market

In addition to controlling inflation, the Federal Reserve's mandate includes keeping unemployment as low as possible. This is the U.S. central bank’s famous dual mandate.

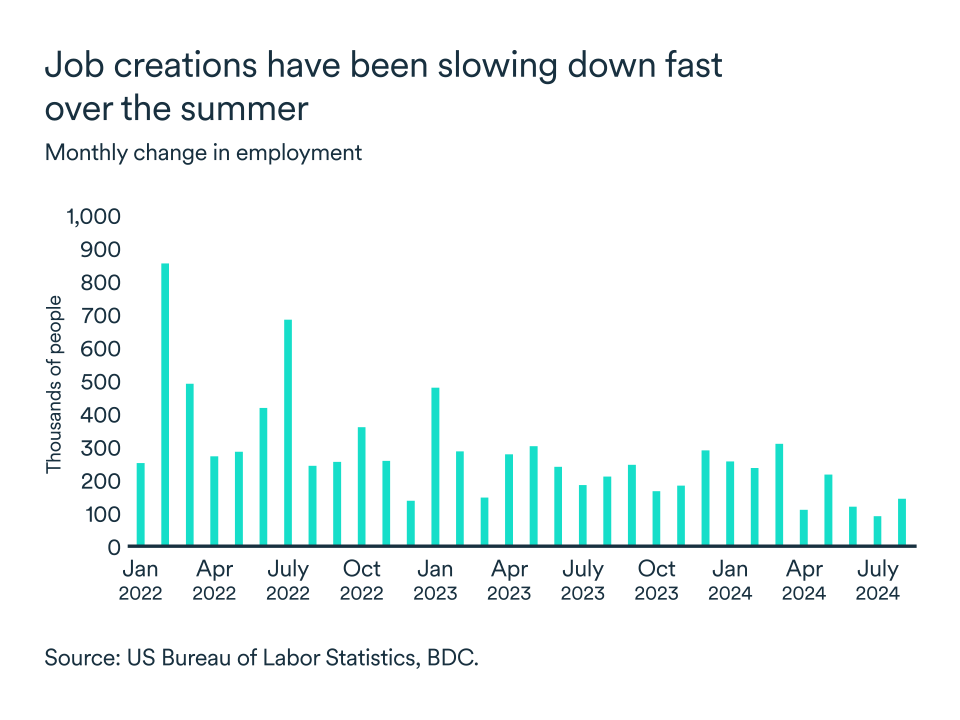

While the job market continued to perform well in August, it’s been slowing for some months now. Job creation is still positive so far in the third quarter; the 140,000 jobs added in August were in addition to 89,000 in July. Although we're still a long way from widespread layoffs, the latest employment report confirms a slowdown in the labour market. The unemployment rate rose to 4.3% in August.

Notwithstanding job vacancies falling by almost a million since the start of the year and hiring intentions easing, average hourly earnings rose by 3.8% in August compared with a year earlier—higher growth than in July. Several indicators still suggest wage growth will normalize at or above 3% by the end of the year, a return to pre-pandemic levels that are in line with inflation at 2%. However, faster wage growth in the latest employment report could dent the pace at which the Fed will decide to cut rates.

The impact on your business

- It may have taken longer in the U.S. than elsewhere, but it seems tight monetary policy is finally having an impact on the real economy. However, the slowdown hasn’t yet been felt too much by consumers, which is good news for businesses.

- The Federal Reserve held interest rates steady over the summer while credit conditions eased in Canada. This put downward pressure on the Canadian dollar, which is always good news for exports.

- U.S. employment continues to slow alongside real disposable income and household savings. A normalization of the labour market and progress on inflation should prompt the Federal Reserve to make its first rate cut in the coming weeks to support the economy.

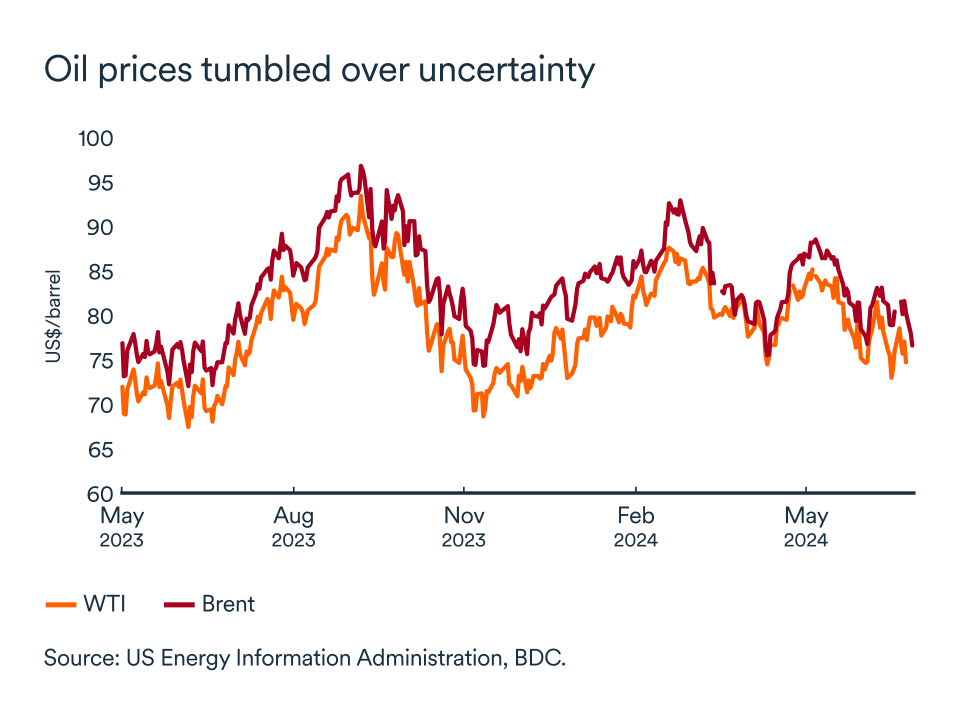

Oil prices fall amid growing concerns about a global slowdown

Crude oil benchmark prices hit their lowest level of the year in early September amid concerns about higher volumes coming to the market and signs of a global economic slowdown.

At the beginning of the month, WTI fell to US$69 and Brent to US$74. The drop in prices mainly reflected worries about an expected production increase by OPEC+ (Organization of the Petroleum Exporting Countries and its allies) as well as slower growth in the Chinese and U.S. economies.

OPEC+ considers delaying an output hike

OPEC+ is scheduled to increase output by 180,000 barrels a day in October as part of a plan to gradually unwind production cuts. However, member countries are looking at delaying the move in response to the global growth outlook and recent steep price declines.

Between January and July 2024, China's oil imports fell by over 11%. Part of this decline can be explained by the base effect since the volume of Chinese crude imports had risen to a record level in the same period the previous year.

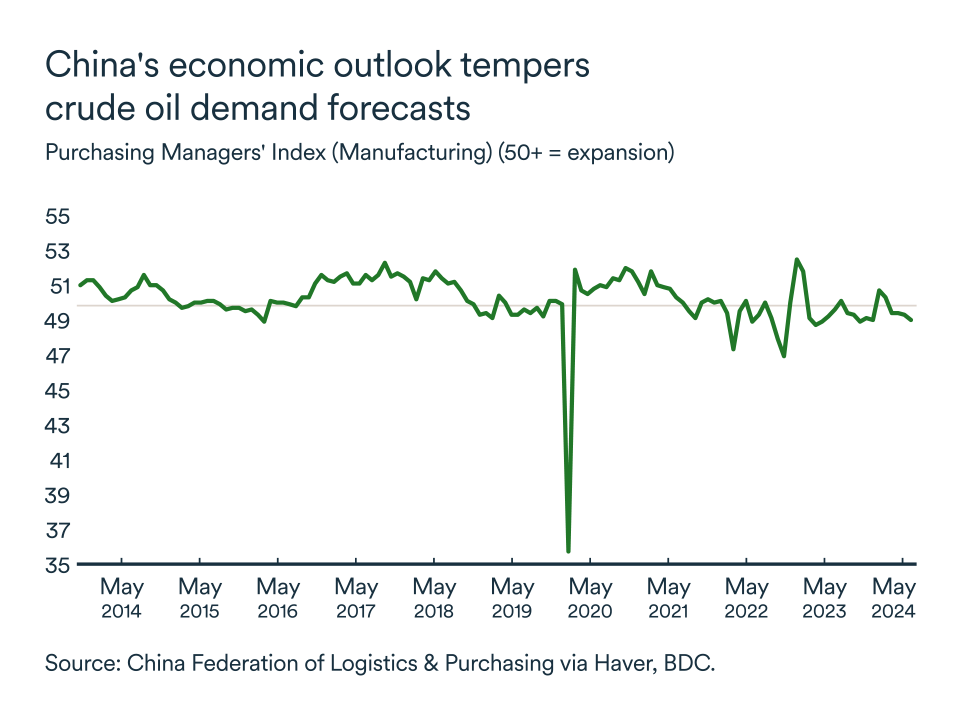

Demand weakens as the world's largest economies slow

However, China's economy has showed clear signs of slowing. The country is the world's largest importer of oil and its demand indicators are closely watched by the market. Previously rising crude prices and falling demand for refined fuels have squeezed the margins of the country's refineries and reduced the nation's energy appetite since the first half of 2024.

It’s a similar story in the United States where the world’s largest economy also appears to be gearing down. In particular, disappointing manufacturing data in both China and the U.S. are prompting observers to review demand forecasts.

The Chinese purchasing managers index has been below 50 (i.e. in contraction territory) for the past four months. The U.S. manufacturing index improved in August, but also remains in contraction territory, reflecting a drop in new orders and an increase in inventories.

This suggests that industrial activity could remain muted for some time. These two countries alone account for almost 50% of global manufacturing output.

In a nutshell...

OPEC+ has announced increases in production and exports despite continued high economic uncertainty threatening global growth, particularly in the manufacturing sector in China and U.S. Prices of the main crude benchmarks have weakened recently and may continue to fall, but a delay in OPEC+’s production hike could stabilize the market. Meanwhile, recent price declines in the oil markets could further support central banks' inflation-fighting efforts around the world and accelerate the easing of credit conditions.

Policy rate could end the year at 3.75%

The Bank of Canada lowered its key rate by yet another 25 basis points at its September meeting and is likely to do so again at its remaining two meetings of 2024. Inflation has slowed slightly since the central bank's July announcement. While the economy continues to show resilience, it has been growing below potential for over a year now. The labour market is also showing signs of easing; wage growth is still a problem, with the year-on-year change in average hourly earnings rising 5.0% in August – a slight drop compared to previous months. We expect the economy to continue to grow, but struggle on the back of still elevated interest rates and inflation continuously heading toward target. We foresee the central bank to continue cutting rate by 0.25 points throughout the year.

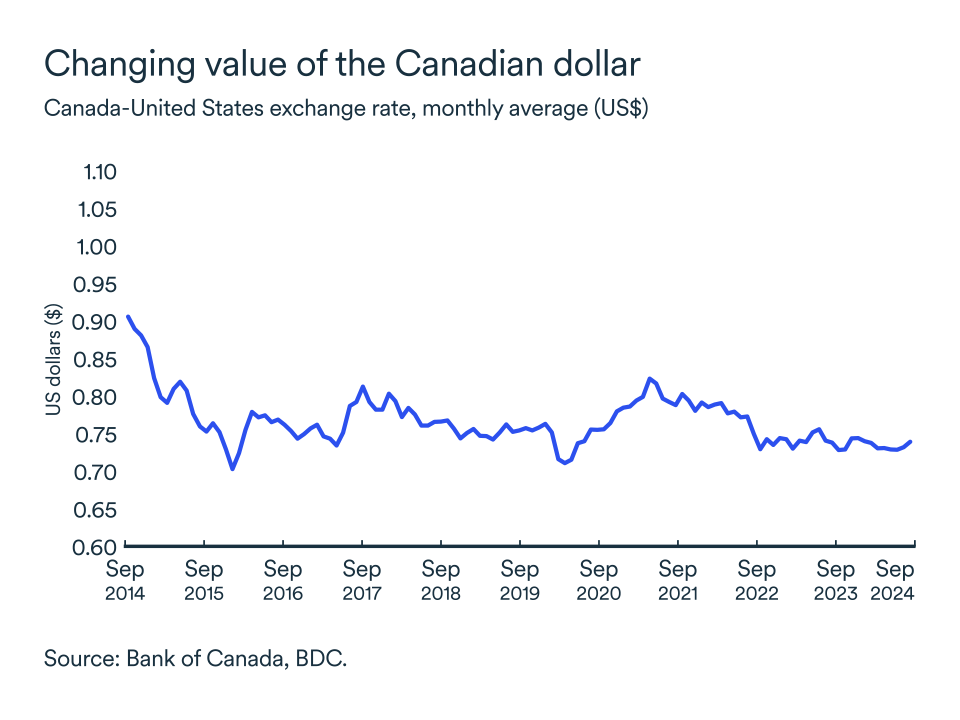

The loonie rebounds from this summer decline

The Canadian dollar has appreciated slightly since the end of August. In July, the loonie traded as low as 72 US cents at some point, but has since recovered to around US$0.74 in September. It’s the highest level we’ve seen the loonie reach in months, thanks to the expected slowdown in the United States. The Canadian currency's recent, albeit slight, improvement against the US greenback could continue but we do not expect it to gain much more strength. The Canadian dollar is expected to remain between US$0.73 and US$0.74.

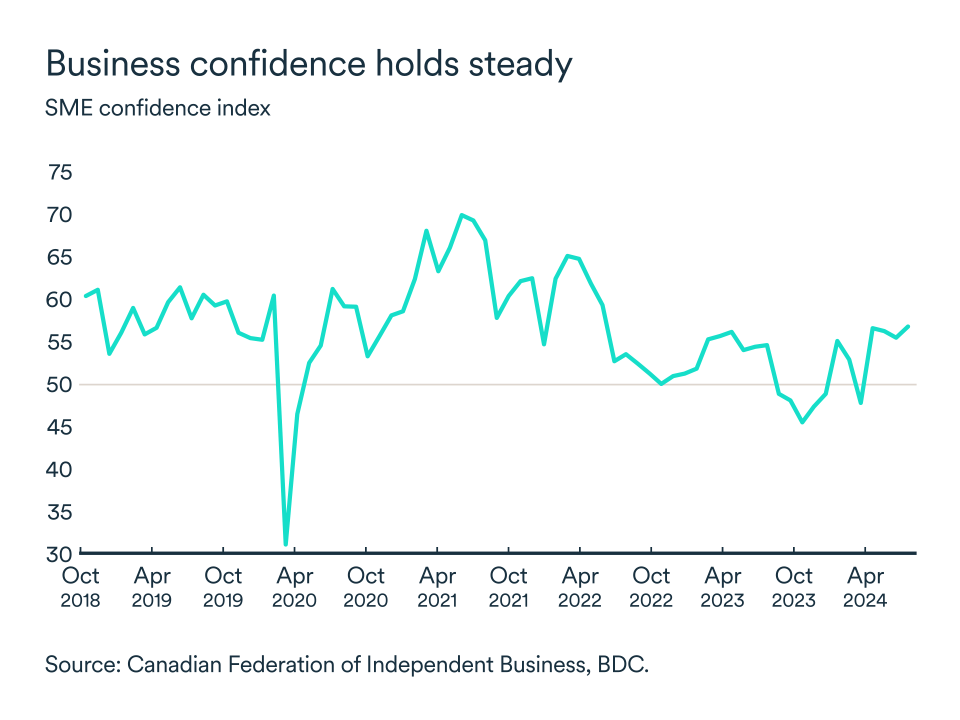

Business confidence stable

In August, the CFIB business confidence index for the coming year remained broadly unchanged compared to June’s level. The index stayed above the fateful 50 threshold, reaching 56.8, a level sufficient to recover July’s losses. Businesses remain on the lookout in the shorter term and optimism has been quite muted giving the interest rate cut experienced.

An indicator of 50 means that as many company managers expect the business environment to deteriorate versus an improvement over the period covered (either 12, or three months).