Monthly Economic Letter

Keep abreast of key economic indicators.

Read more2024: The economy slips into neutral

Many Canadians will probably be happy to see the end of another year of economic uncertainty, but can we expect better in 2024?

Time for a review

The news was generally better than expected for the Canadian economy in 2023, despite persistently high inflation and further interest rate hikes.

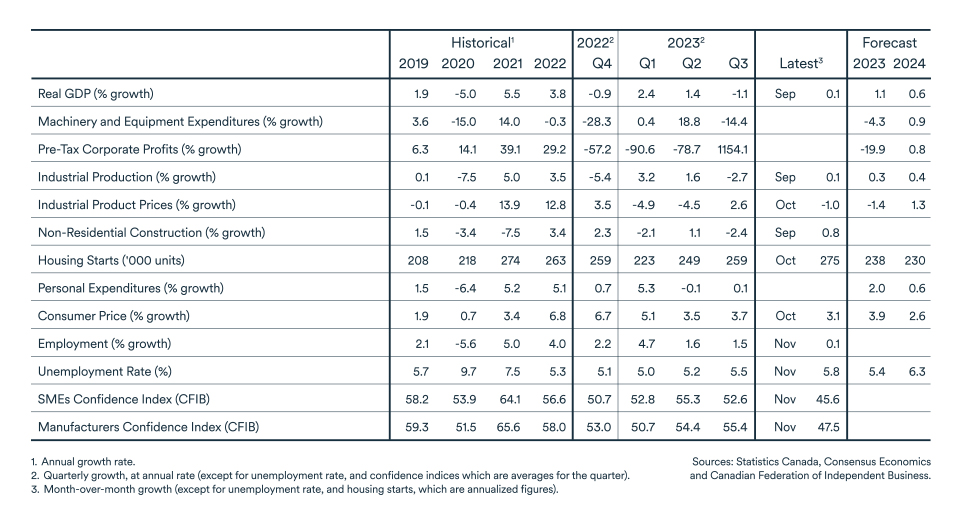

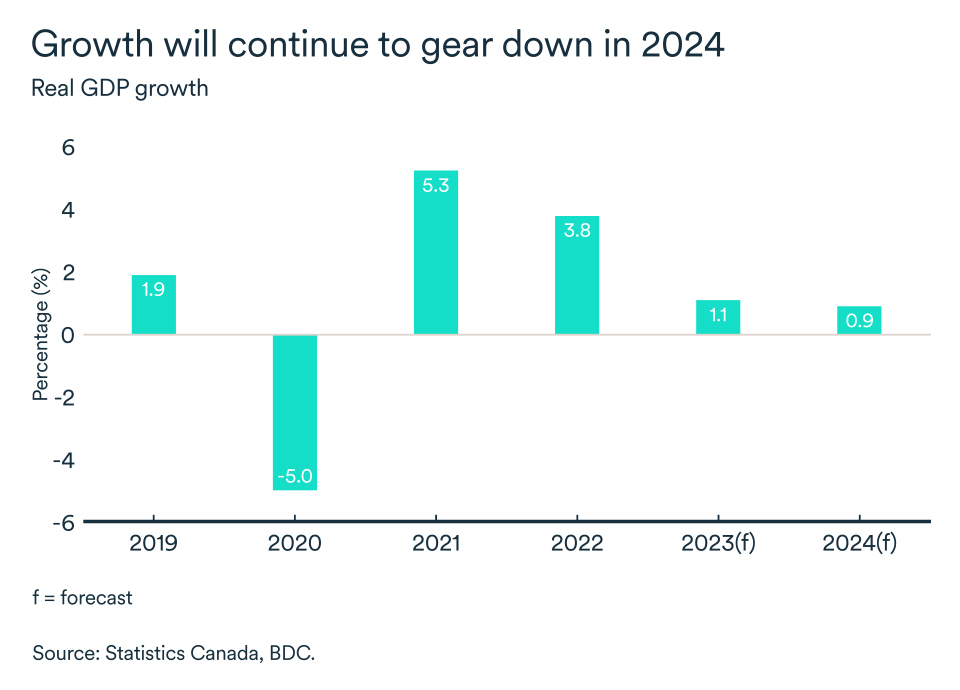

At this time last year, many economists were wondering whether it was possible to stop the overheating of the economy without causing a recession. Today, estimates point to Canadian economic growth of 1.1% in 2023, slightly slower than the economy’s 2% potential but still higher than the initial forecasts of most economists.

Strong population growth was largely responsible for the vigorous demand that supported the Canadian economy in 2023. In turn, the economy's performance helped sustain the labour market.

While the unemployment rate rose in the second half of the year, this was because the active working population grew. About 430,000 jobs were created between January and November 2023.

The resilience of the Canadian economy prompted the Bank of Canada to raise its key rate further during the year, increasing it by 75 basis points to its current level of 5.0%.

As a result, growth was uneven in 2023, with sectors such as housing that are particularly sensitive to interest rates experiencing marked slowdowns. The residential market has mostly stabilized, but remains in a slump. Canadian households are spending less, and the slowdown in the global economy will have led to a deceleration in business investment and exports in the second half of the year.

Canadian economic growth is expected to be anemic in 2024

Canada's economy should avoid recession again next year, but growth will still be elusive. So, while 2024 will probably prove less tumultuous than 2023, growth will continue to slow against a backdrop of high interest rates. The growth will also be tempered by both international and domestic factors.

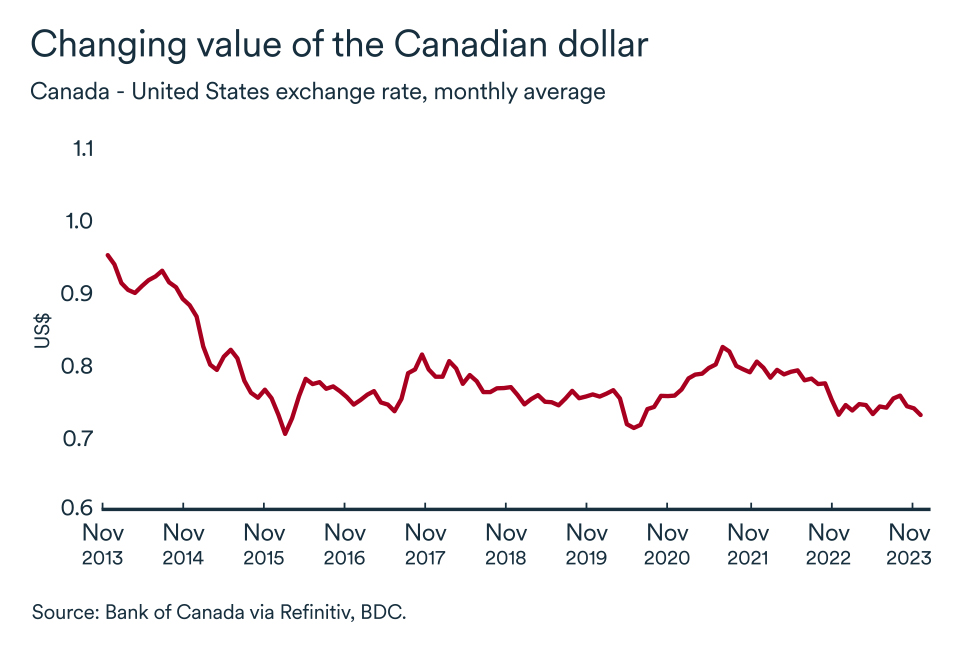

The U.S. will likely continue to outpace other major economies. As a result, the U.S. dollar will remain strong against most other currencies, including the Canadian dollar. Overall, we don’t expect the loonie to drop much more against the greenback, fluctuating between 72 and 75 cents in 2024. A weak loonie has its advantages. It makes Canadian exports cheaper and is more attractive for tourists.

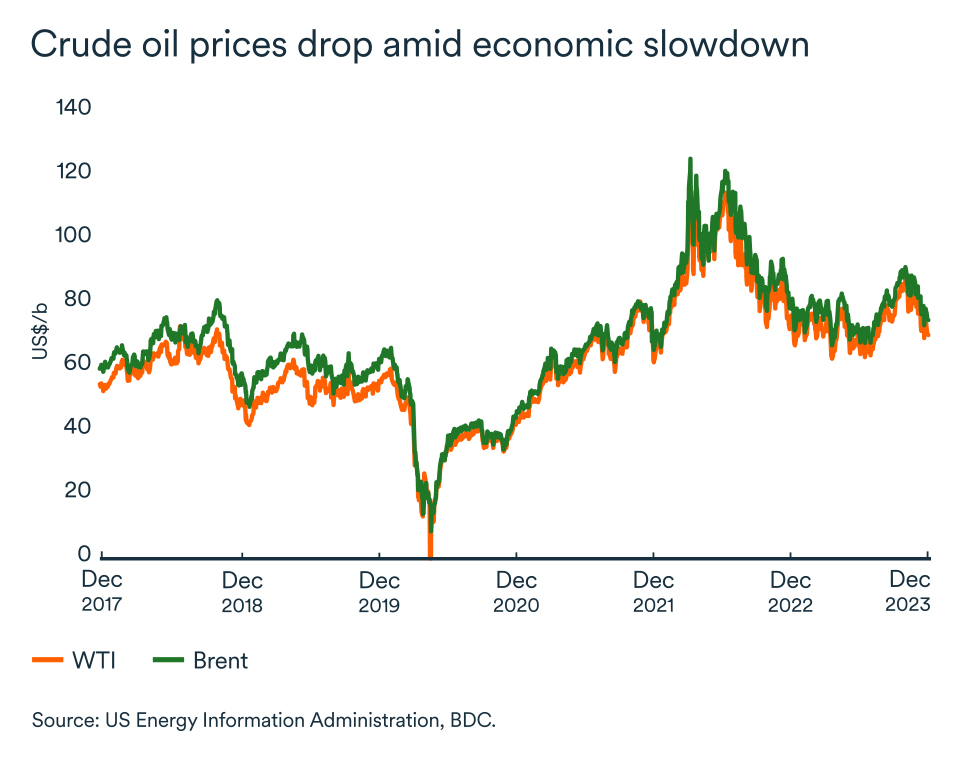

Global oil prices are expected to range between US$70 and US$80 per barrel for WTI and US$75 and US$85 for Brent. Crude prices look set to decline in early 2024 in reaction to a small surplus.

The driving force behind the foreseen 2024 economic slowdown remains high interest rates. Therefore, the Canadian economy is more vulnerable to a deeper slowdown than other countries because of its debt level. We expect Canadian real GDP to grow by a meagre 0.9% in 2024, with one or two quarters of negative growth early in the year. However, there should be an upturn in activity in the second half of the year.

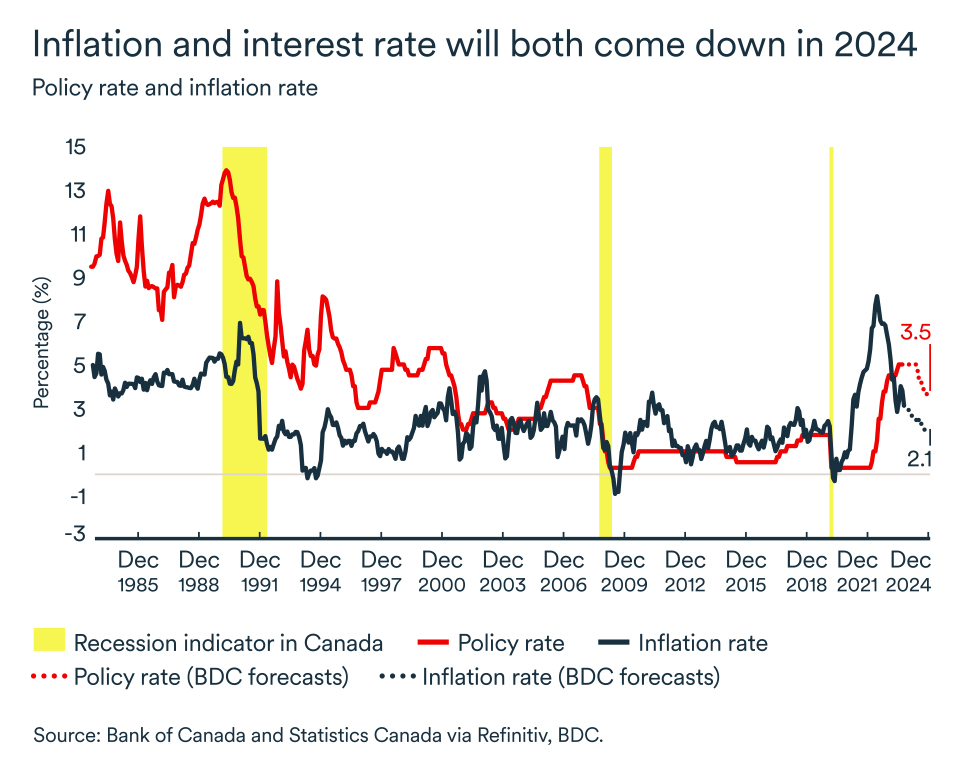

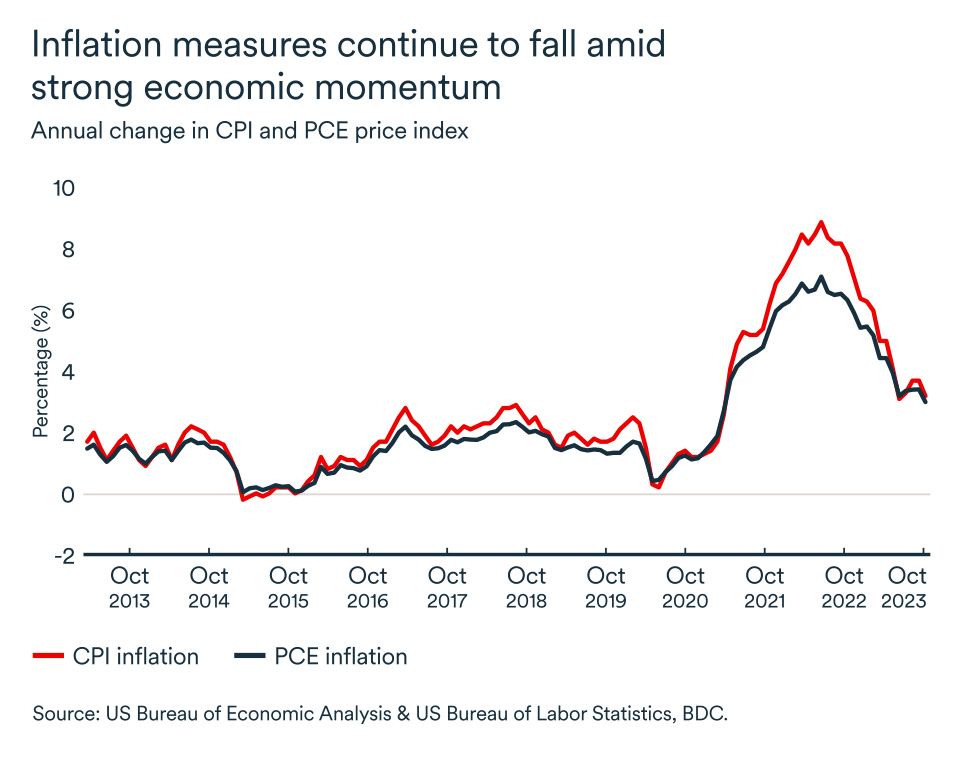

We're not done talking about inflation

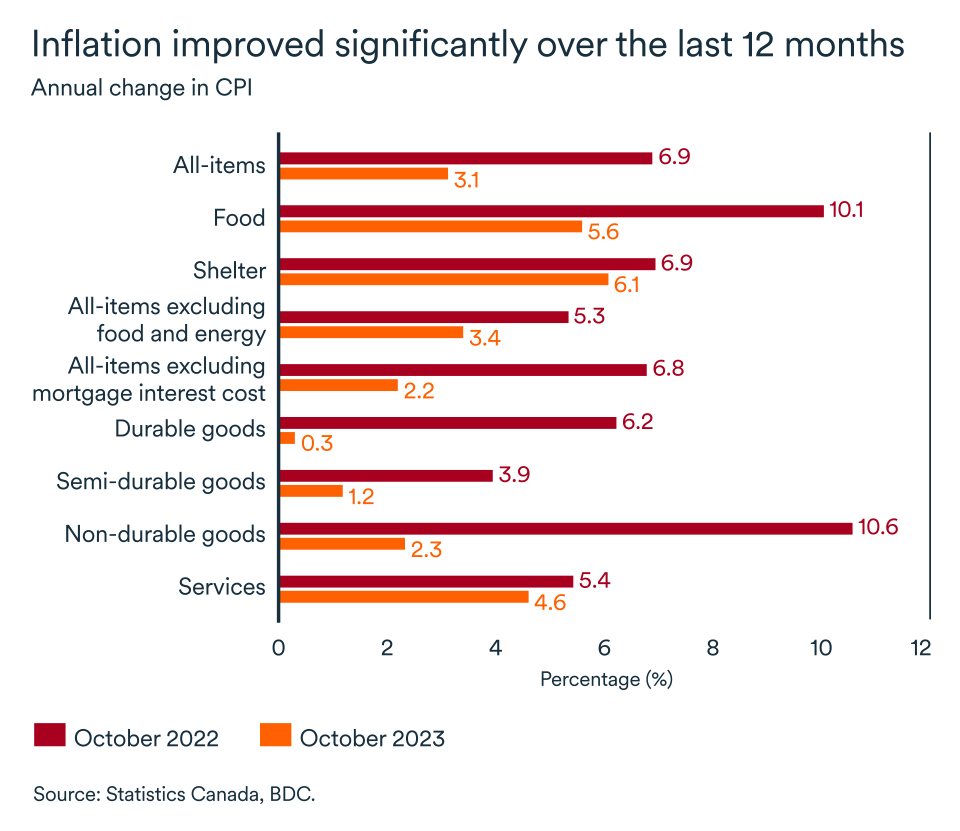

Over the past 30 years, inflation in Canada has remained relatively stable at around 2% per year. However, in the 1970s and 1980s, it was customary to see prices rise by around 8% a year and go as high as 13%. Inflation can have a significant impact on a company's profitability, so it's important for businesses to keep a close eye on it and find coping strategies.

Next year, we expect inflation to continue on its downward slope, oscillating between 2% and 3%, but we don’t foresee a stable and sustainable 2% being achieved until the end of 2024.

While we expect inflation to be lower than what we've experienced over the past two years, price increases for certain budget items will remain stubbornly high for Canadians, including the important categories of food and lodging.

Food price inflation is expected to hover around 4-5% over the coming months. Many foodstuffs are traded on world markets and the weakness of the Canadian dollar against the U.S. greenback will help to push prices higher. Elsewhere, housing-related expenses, notably rent and mortgage interest costs, will also continue to rise faster than the Bank of Canada’s 2% inflation target, particularly in the first half of the year.

The direction of central bank rate policy becomes clearer

Probably the best news for 2024 is that the uncertainty surrounding the direction of interest rates has been significantly reduced. After two years of rate hikes, Canadians should find some comfort in the fact that the most aggressive tightening cycle in 40 years is likely over. Past rate hikes will continue to weigh on economic growth, but the bulk of the slowdown has likely already taken place.

We anticipate a first downward revision in the Bank of Canada’s key rate from the current 5.0% as early as June. However, the bank is unlikely to bring the rate down to 2.5%, the neutral level, before 2025. Rates will therefore remain higher than those to which Canadians have become accustomed over the past 15 years. However, Canadian households and businesses have so far shown an impressive capacity to adapt to this new, higher-rate environment.

Challenges and opportunities for entrepreneurs

Despite the many challenges that lie ahead for entrepreneurs, economic expansion is expected to continue in Canada in 2024, albeit at a modest pace.

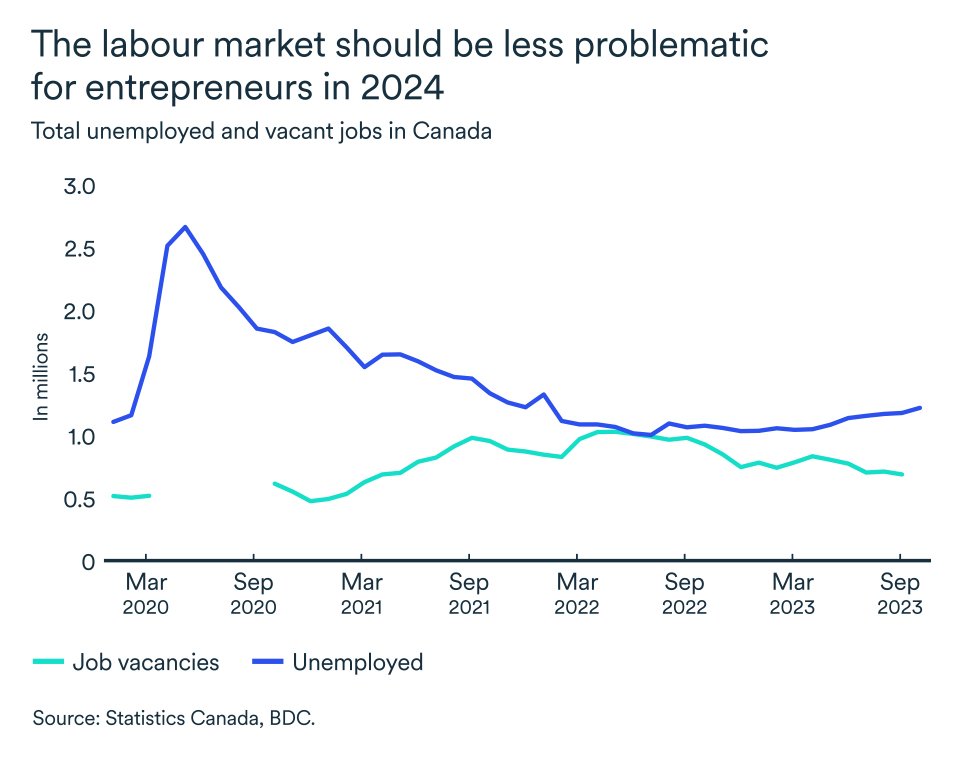

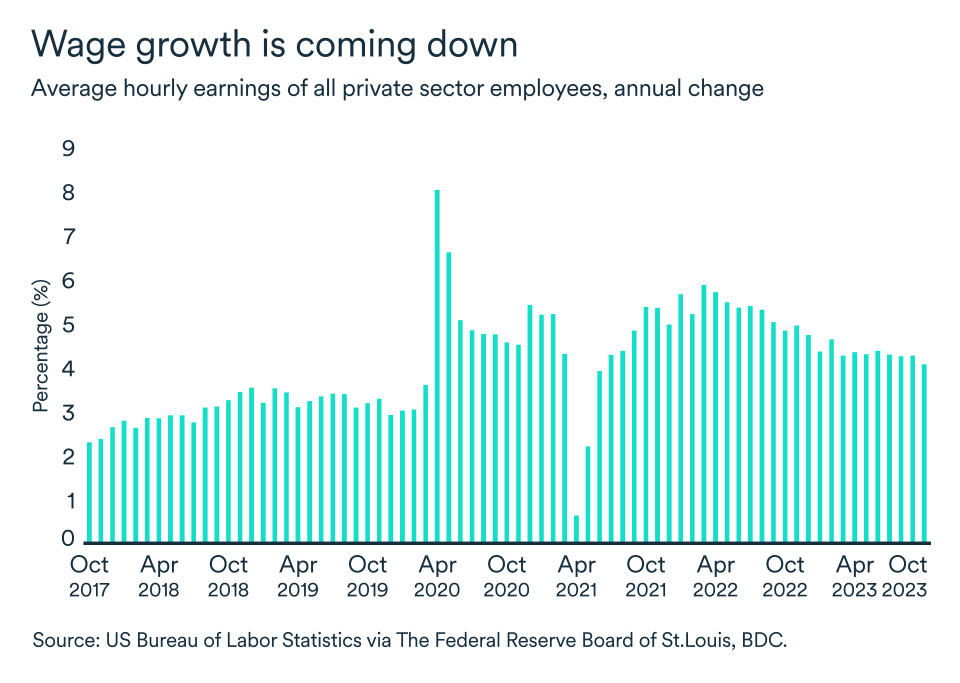

Companies will need to focus on maintaining sound management of human resources. Although the aging of the population will have an impact on the labour market for several years to come, the economic slowdown and population growth will made it easier for businesses to find workers than in recent years. Wage growth should return to a more sustainable pace in 2024 as pressure eases on the labour market.

With interest rates remaining high and demand slowing, entrepreneurs will need to be nimble and strive to maintain the financial health of their businesses. Adopting more technology can help by boosting productivity and improve competitiveness. Business owners who act now will be in a better position to capitalize when the economy takes off again.

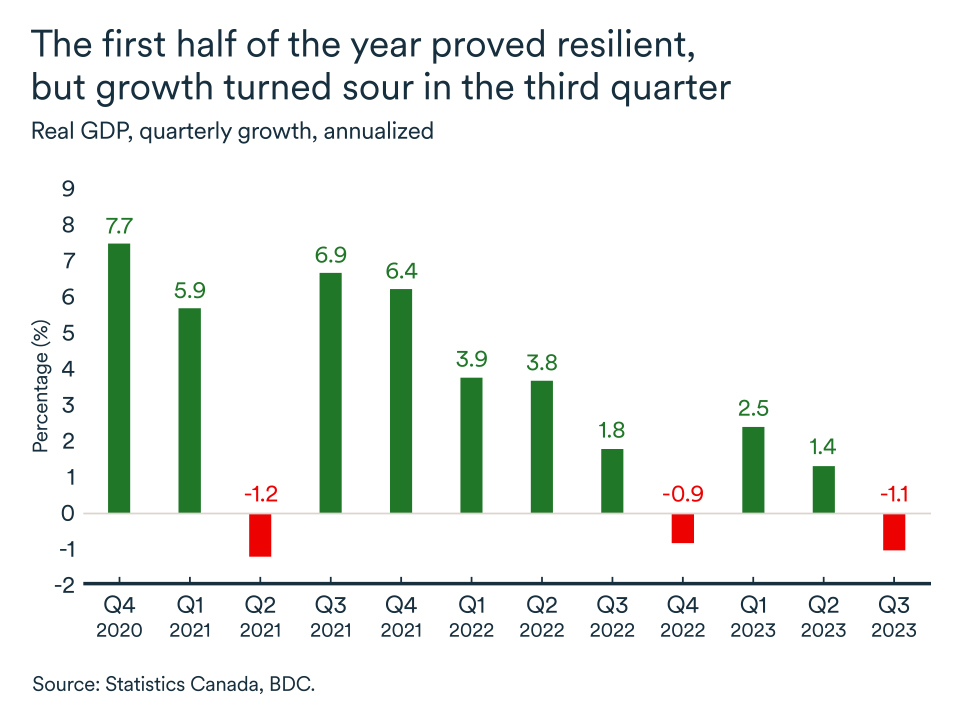

Still not in recession

Economic activity in Canada slowed sharply in the third quarter, contracting at an annualized rate of 1.1%. At the same time, Statistics Canada revised its GDP data for the second quarter upward to a positive 1.4% from an initially reported decline of 0.2%.

Taken together with preliminary data for the fourth quarter, these readings indicate the economy has slowed considerably but is still not in recession.

GDP growth was positive in September, and preliminary estimates point to an encouraging start to the fourth quarter as well. Growth is estimated to have reached 0.2% in October compared to September, pointing to growth of 1.4% for the first ten months of the year, compared to the same period in 2022.

Nevertheless, the poor performance in the third quarter reinforces our view that the next move by the Bank of Canada will be a rate cut in mid-2024.

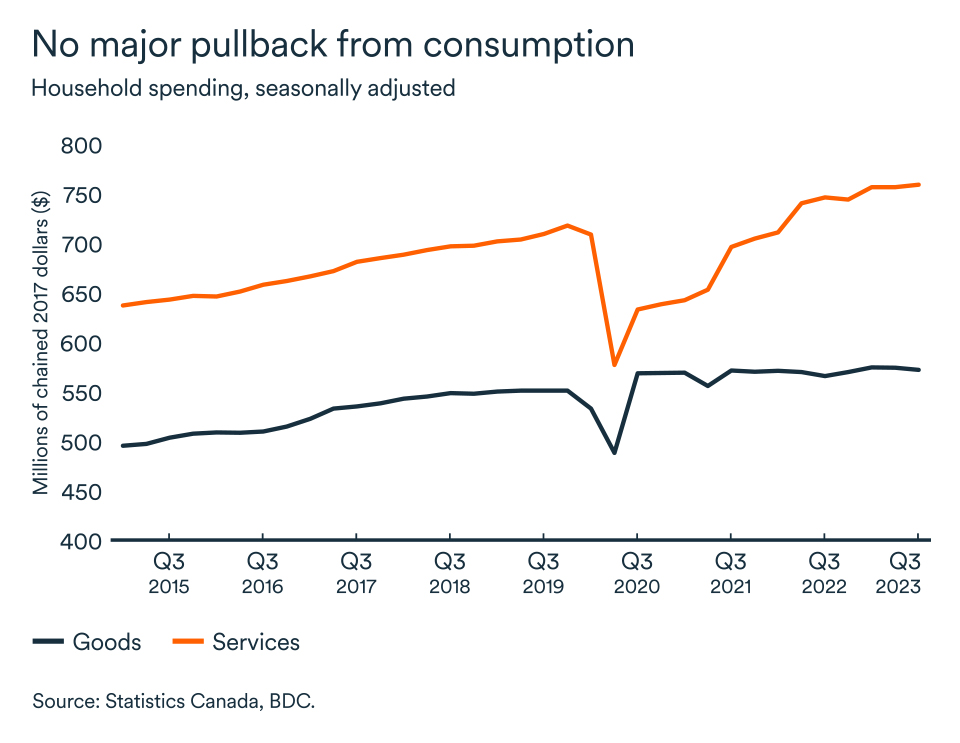

Households continue to somewhat support the economy

Positive contributions to GDP in the third quarter came primarily from government spending, but consumer spending and residential investment also helped, despite high interest rates.

Residential investment rose for the first time in almost a year and a half. The upturn was entirely due to new construction, as ownership transfers were on the decline. While consumption was only barely positive, there is still no massive pullback in spending neither on goods nor services.

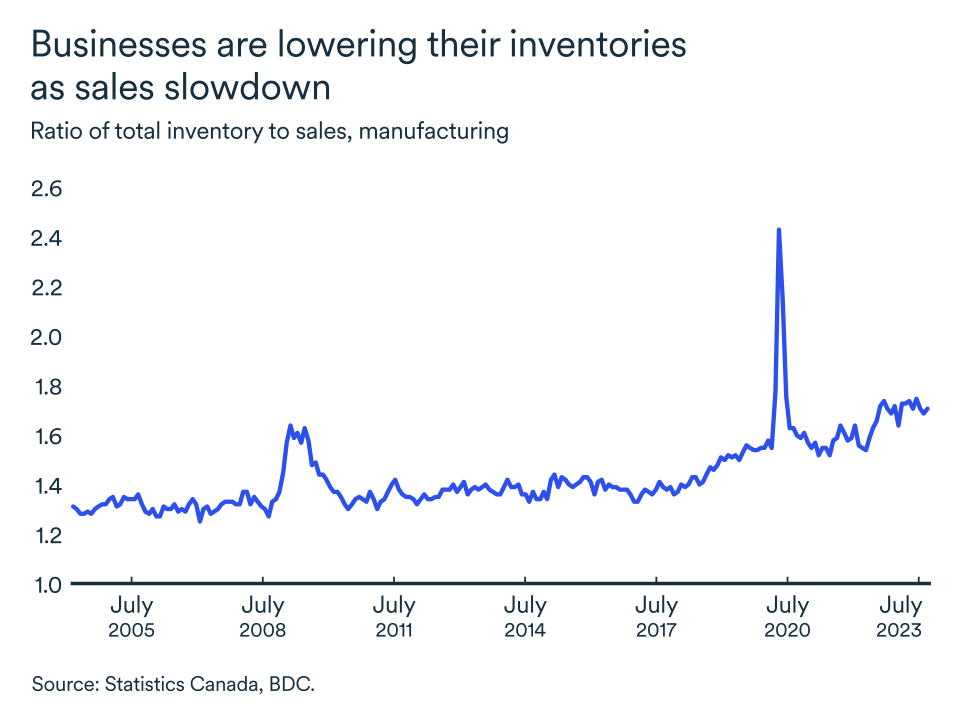

Businesses are increasingly worried

Unsurprisingly, business investment is slowing and companies remain cautious on their outlook for the coming months. On the one hand, the economic slowdown is starting to show up in their order books, while, on the other hand, many are reporting overcapacity.

As a result, businesses are paying more attention to inventory management. For the country as a whole, inventories accumulated at the slowest pace in two years in the third quarter, subtracting almost a full percentage point from real GDP.

High interest rates are also acting as a brake on investment projects for many companies, which prefer to put them on hold until uncertainty about the future direction of rates subsides.

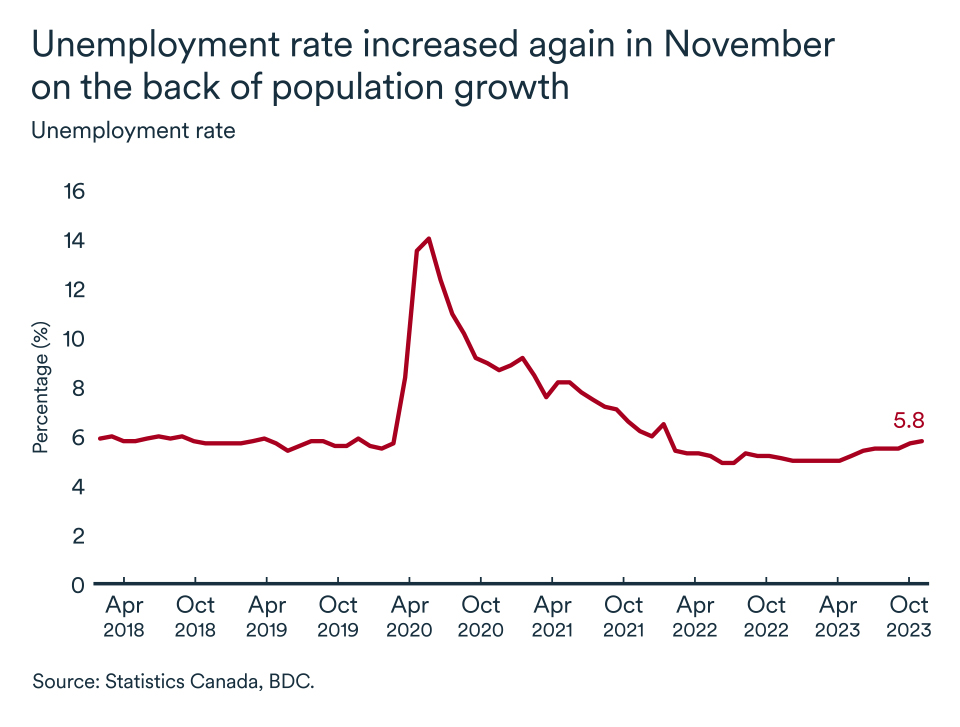

More job gains

The Canadian economy added a meagre 25,000 jobs in November as the pace of job creation in the country continued to slow. At the same time, the unemployment rate rose again, to 5.8% from 5.7% in October. This is still low by historical standards.

The unemployment rate is rising despite the employment gains because the pool of potential workers continues to grow rapidly (+36,000 between October and November alone). In fact, the number of people unemployed has risen by 16% in one year.

Despite this labour force growth, many companies are still struggling to fill positions—there were over 630,000 job openings in Canada in September. However, it’s a mixed picture across the economy—some sectors continue to have difficulty finding workers while others have made significant layoffs.

The impact on your business

- The weak GDP performance in the third quarter confirms the economic slowdown has taken hold, but Canada is not yet in recession. Population growth is once again mitigating the impact of high interest rates by helping maintain household consumption and residential investment.

- The Bank of Canada has probably finished raising its policy rate for this cycle as demand in the economy has finally softened, reducing inflationary pressures. The next change in monetary policy is likely to be a rate cut, but that is still some way off. Until then, economic activity is likely to be increasingly subdued.

- Businesses are becoming more cautious in their hiring, inventory management, spending and investment. So, no matter where your company is in the production chain, you're going to feel the effects of the slowdown.

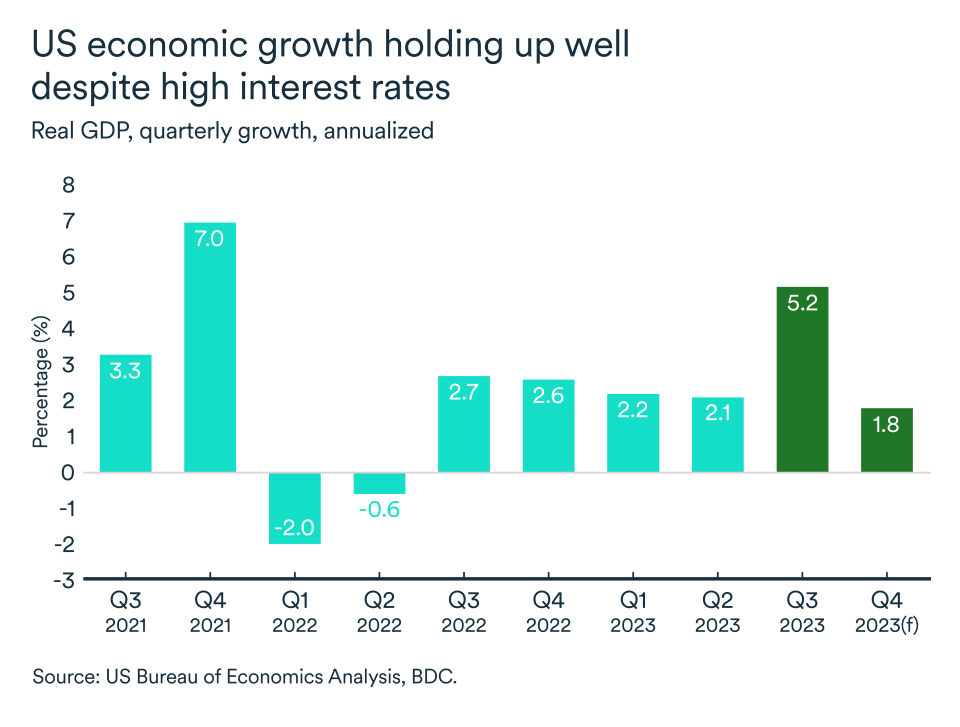

U.S. growth holds up

Despite the uncertainty created by inflation and high interest rates, the U.S. economy has weathered the many ups and downs of 2023. Even a couple of bank failures did not shake the economy. Real GDP is estimated to have grown 2.1% over the past year.

We believe that the U.S. economy is still on track for another year of growth in 2024, especially with inflation coming down. Nevertheless, we expect growth to slow to 1.3% next year. This would still be a solid performance in an environment where volatility remains high.

Consumption is still resilient

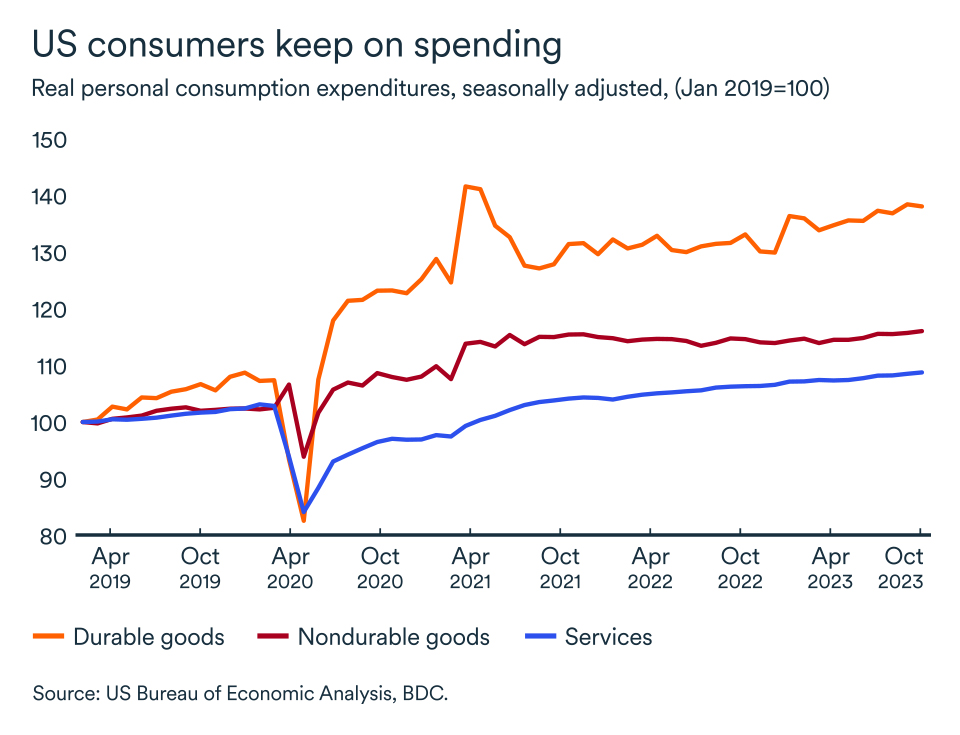

For the time being, economic growth continues to be vigorous. In fact, third-quarter growth came in at 5.2% (annualized), with consumer spending offsetting the effects of slowing investment and high uncertainty. Consumers have been the engine of economic growth and are expected to maintain relatively high spending levels next year, although the strength of spending should wane somewhat. In the third quarter, households spent at an annualized rate of 4%, which is unsustainable in the current context and what awaits the U.S. in 2024.

Disposable household income has fallen in recent months, forcing Americans to dip into their savings to cover their spending. The situation should reverse somewhat in the coming months as inflation slows. However, wage gains have already begun to decline, which should continue into 2024 as the labour market stabilizes. At the same time, interest rates will remain high, limiting purchases that require financing.

Volatility to be felt for some months yet

Following Federal Reserve Chairman Jerome Powell’s latest comments, expectations of interest rate changes for the coming year have been revised downwards. Fed observers believe the possibility of further increases is becoming less and less likely because inflation is approaching the Fed’s target more quickly than forecast.

While uncertainty remains, the economy has shown itself to be highly resilient in the face of what’s been an aggressive cycle of credit tightening.

Still, Federal Reserve decision-makers have repeatedly warned that lasting signs of a slowdown in demand must be observed before they claim victory over inflation.

For this reason, policymakers prefer to analyze core inflation measures, which exclude the notoriously volatile food and energy categories. Thus, while overall inflation reached 3.2% annualized in October, when food and energy are excluded, it was around 4%.

Pressure on the job market eases further

Job growth in the U.S. is set to continue to moderate. Nearly 150,000 new jobs were added in October, and a similar number are expected in November. Unemployment rate could climb back to the 4% mark as more workers entered the job market. That’s a level not seen since January 2022, when the economy was caught up in the Omicron variant, the most virulent of the pandemic.

In contrast to the Canadian labour market, wage pressure has been slowing in the U.S. for several months. This will continue to support the Fed in its fight against inflation in 2024. Job vacancies and voluntary departures continue to decline. Pressure on the U.S. labour market is therefore showing signs of easing, which should limit wage growth even further in the months ahead.

The impact on your business

- Stronger growth in the U.S. than in Canada means a weaker loonie. Canadians exporting to the U.S. will be more competitive, but Canadian companies will face higher costs when importing goods and services from the U.S. or trading on international markets.

- Canadian entrepreneurs who are selling into the U.S. should be prepared for a slowdown in consumption south of the border in the coming months.

- With interest rates still high and the country entering a fraught election year, U.S. businesses will be dealing with an uncertain economic environment and could delay their investment projects.

Slowing demand pushes oil prices down

Many consumers, entrepreneurs and central bankers will be pleased to see crude prices on a downward slope. Worries about weaker global economic growth are increasingly pointing to a crude surplus in 2024.

Signs of oversupply drive prices down

As we await a decision from OPEC+ on future production levels, the main crude oil benchmarks continue to fall. An economic slowdown in China and elsewhere in the world is the overriding factors behind the recent drop in prices. WTI and Brent have both fallen by around 3.5% in the space of a month.

Brent futures were trading at US$83 a barrel and WTI at US$78 at the end of November. This represents a decline of about 3.5% for Brent, compared with the same period last year, while WTI was trading at about the same level as last year.

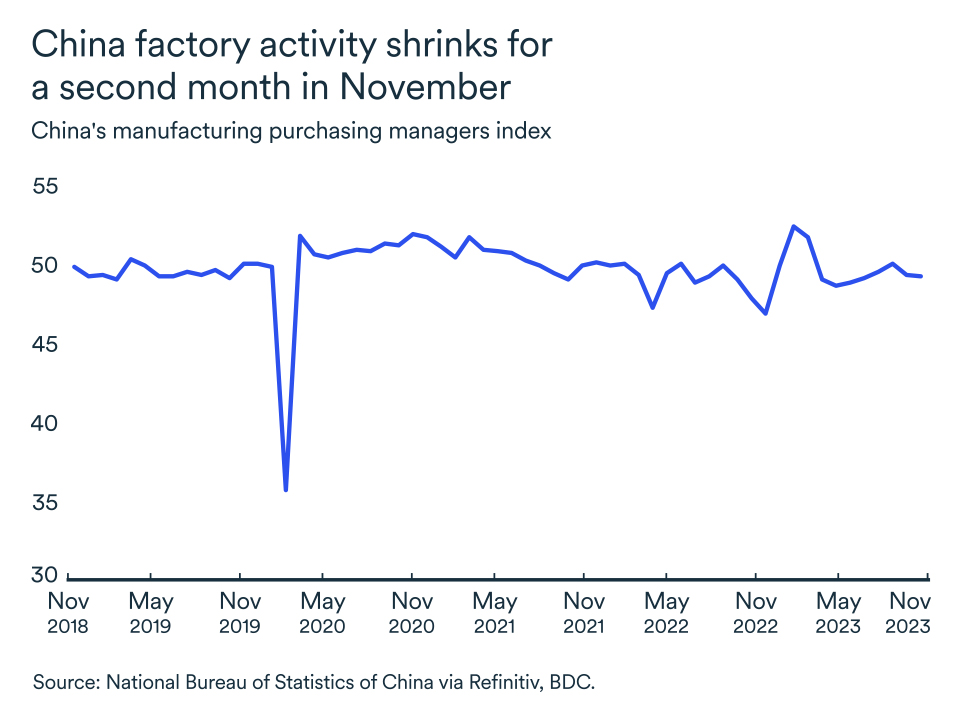

The global economy continues to face major challenges. Some countries in Europe are likely to fall into recession, while other major economies will continue to slow down. In China, the economy has underperformed expectations since its full reopening from the pandemic earlier this year.

Indeed, Chinese manufacturing activity contracted for a second consecutive month in November and did so even faster than expected. China is the world's largest importer of oil, and its manufacturing sector is one of its biggest consumers. On the other side of the globe, U.S. oil and gasoline inventories are on the rise—another sign of slowing demand.

OPEC decision could boost prices

Bearish factors dominate for now and uncertainty looms as OPEC+ just announced further production cuts for the first quarter of 2024. However, the cartel is finding it increasingly difficult to agree on strategy. At a June meeting, member countries agreed to extend cuts in place until 2024, while granting a quota increase for the United Arab Emirates. Barely 24 hours after the announcement of new cuts coming into place next year, some cartel members are planning to break their quotas.

If we add up all the reductions put in place since the end of 2022, Saudi Arabia, Russia and other OPEC+ members have already committed to cutting total oil production by around 5 million barrels per day (mb/d), including a voluntary 1 mb/d reduction by Saudi Arabia and 300,000 b/d by Russia, both of which expire at the end of December. As a result of the most recent meeting, the Saudi and Russian voluntary cuts will be extended. In the end, an additional 900,000 barrels per day will be taking off the market compared with what was in place at the end of December.

OPEC and its allies supply over 40% of the world's oil. The cuts in place until the end of 2023 represent around 5% of global demand.

Bottom line…

Uncertainty is rife in the oil market and will continue into 2024. If the economic slowdown proves more severe than currently anticipated, prices will fall further. However, OPEC and its allies will adjust their output in line with global economic developments, in an attempt to keep prices at the desired level of around US$85-90 a barrel.

Bank of Canada remains on hold

The Bank of Canada ended the year without raising rates, signaling a tone of confidence that our economy is not overheating anymore. Inflation cooled to 3.1% in October from 3.8% in September. Lower oil prices helped bring inflation closer to target. While goods inflation fell to 1.7%, services inflation was at 4.6% in October 2023 (an increase from 3.9% in September).

Inflation should continue to trend lower in the new year, clearing part of the uncertainty. Canada’s policy rate is most likely going to stay at 5% as the Bank of Canada waits to see further easing in core inflation measures. Before thinking of bringing the policy rate down the central bank will need to feel confident that inflation is on track to reach the 2% target and stay there.

The loonie stabilizes in November

The Canadian dollar was stable in November, averaging the same level as in October at US$0.73. While the currency has gained some strength towards the end of November, the long-term outlook remains muted.

In 2024, the greenback will remain strong as the U.S. economy outperforms its major trading partners. Therefore, the Canadian dollar is expected to remain weak, fluctuating between US$0.72 and US$0.75.

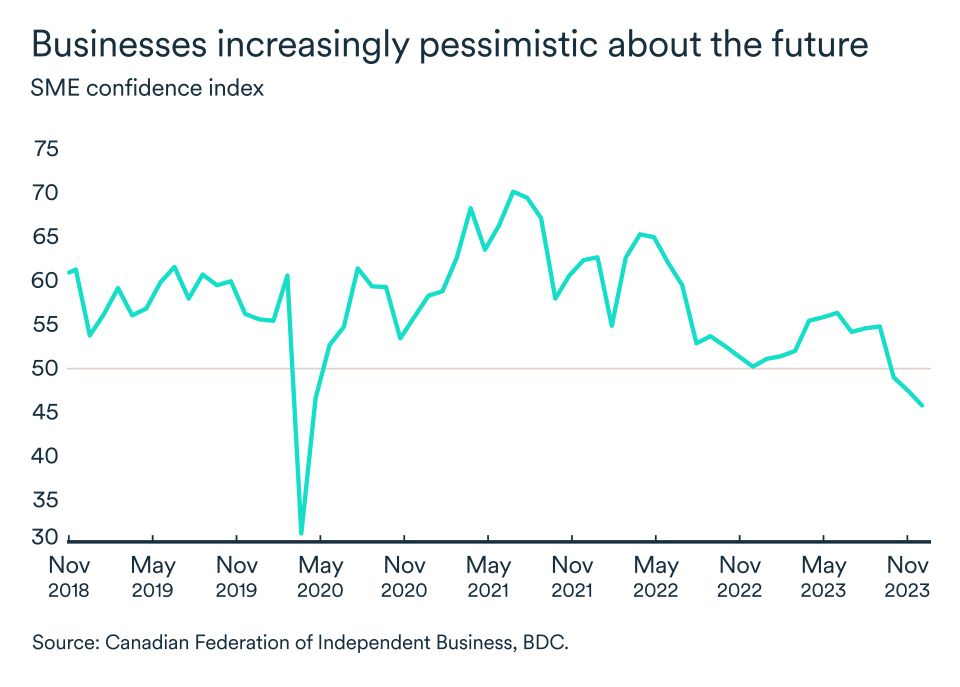

Pessimism intensifies among business leaders

The CFIB's confidence index for the year ahead continued to fall below the critical 50 mark, from 47.2 to 45.6 between October and November. Optimism continued to decline in nearly every province. Among the provinces, confidence was lowest in Ontario and Quebec, at 45.2 and 42, respectively.

A slowing economy combined with tight credit conditions has weighed heavily on business confidence.