Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreCan Canadian households afford to keep spending?

While there are many factors to consider when analyzing business cycles, one reality remains constant—the importance of consumer spending. In Canada, as in other countries, consumption is the main driver of the economy, accounting for nearly 60% of GDP.

In addition to the important role household spending plays in fuelling economic growth, changing consumer behaviours also force businesses to adapt and innovate. In the face of inflation and rising interest rates over the past year, can Canadian consumers afford to spend more on what your business offers?

Household finances are holding up for now

Household debt has increased rapidly in Canada in recent years. Borrowing accelerated since the pandemic, making the economy more vulnerable to financial disruption at a time when interest rates have risen at a historic pace.

Household credit market debt as a share of disposable income drop slightly to 180.5% in the final quarter of 2022, down from 184.3% in the third quarter. This means households had $1.80 of debt for every $1 of disposable income.

In other words, the average household would need almost twice its annual income to pay off all its debt. However, even these figures don’t provide an adequate picture of the risk facing households.

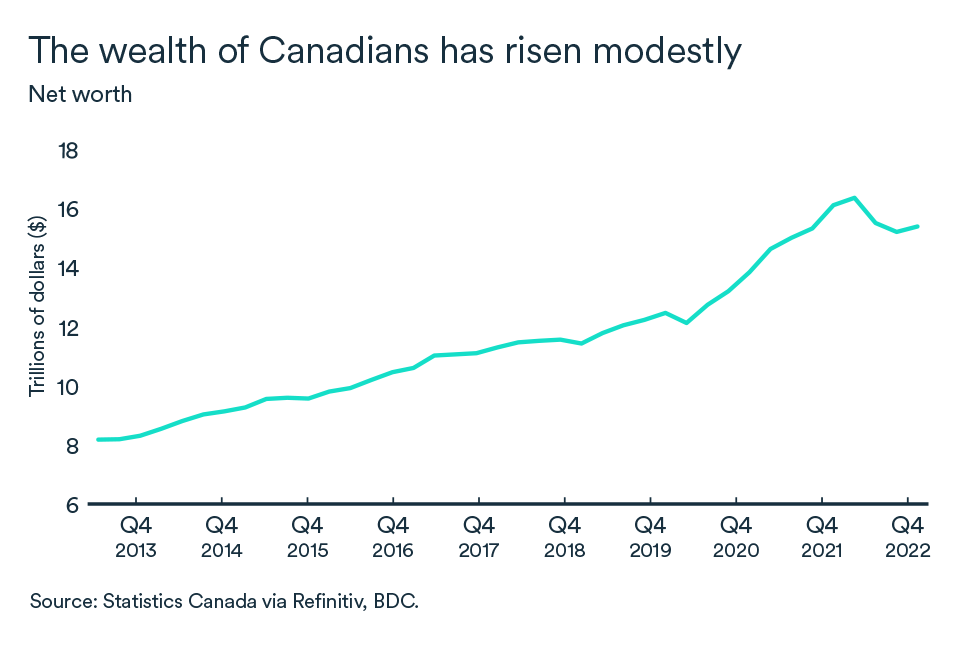

Canadians are taking on more debt at a time when their wealth is also experiencing headwinds. Real estate prices have corrected in several regions and stock market returns have fallen. The result is that consumers are more indebted and less wealthy.

Do households have the capacity to spend more?

For businesses, what’s important is whether consumers will continue to spend in the coming months. Here, there’s some positive news to report. Not only are more Canadians employed, but wages have also increased rapidly since the economic recovery began.

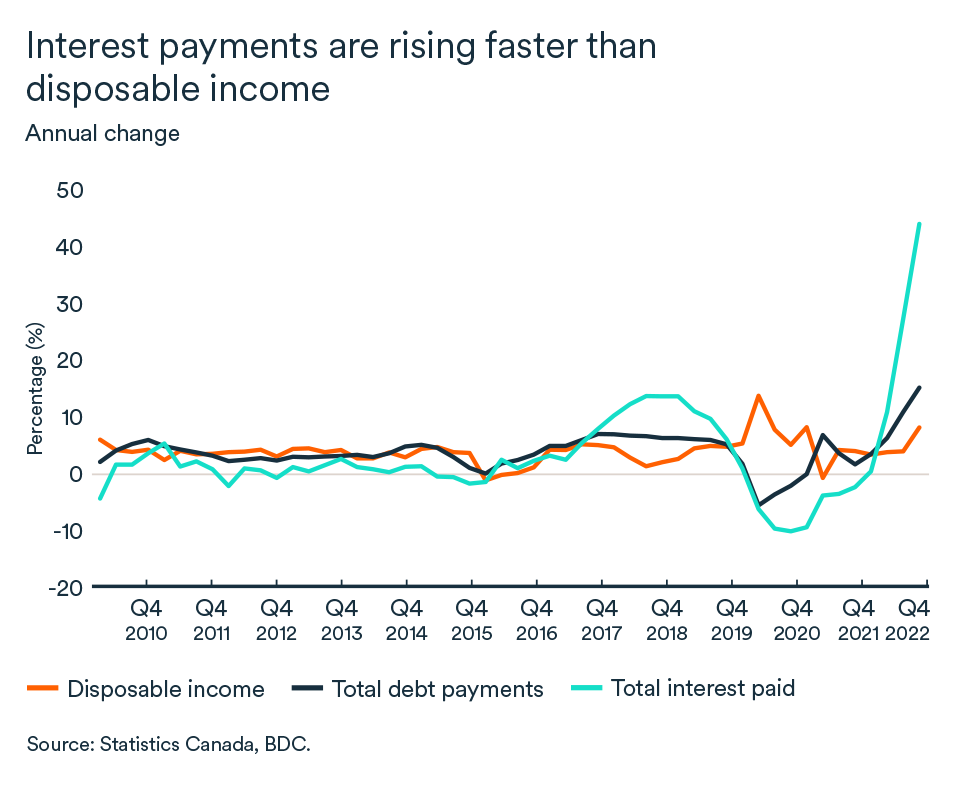

Disposable income (before interest payments) increased at a 10.7% pace in the fourth quarter of 2022 compared to the same period the year before while total debt payments increased by 15.7%. Interest-only payments accelerated even more at the end of 2022, at a rate of 45%! However, the debt service ratio remains lower than it was pre-pandemic at 14.3% (compared to 15.0% in 2019). This measures debt obligations as a percentage of a household's disposable income, which is a better indicator of ability to pay.

Are your clients more at risk?

Last month, Statistics Canada reported that one in four Canadians couldn’t afford an unexpected $500 expense and that more than one-third of Canadians found it difficult to meet their financial needs. This is likely an indication of the toll higher inflation is taking, but the rising cost of living doesn’t affect all households equally.

StatsCan data indicate that younger adults are having more difficulty meeting their financial obligations, while some racialized groups are harder hit by rising housing costs. Overall, the financial situation of Canadian households poses a growing risk to economic prosperity with some groups being in a particularly difficult situation, notably youth and low-income households.

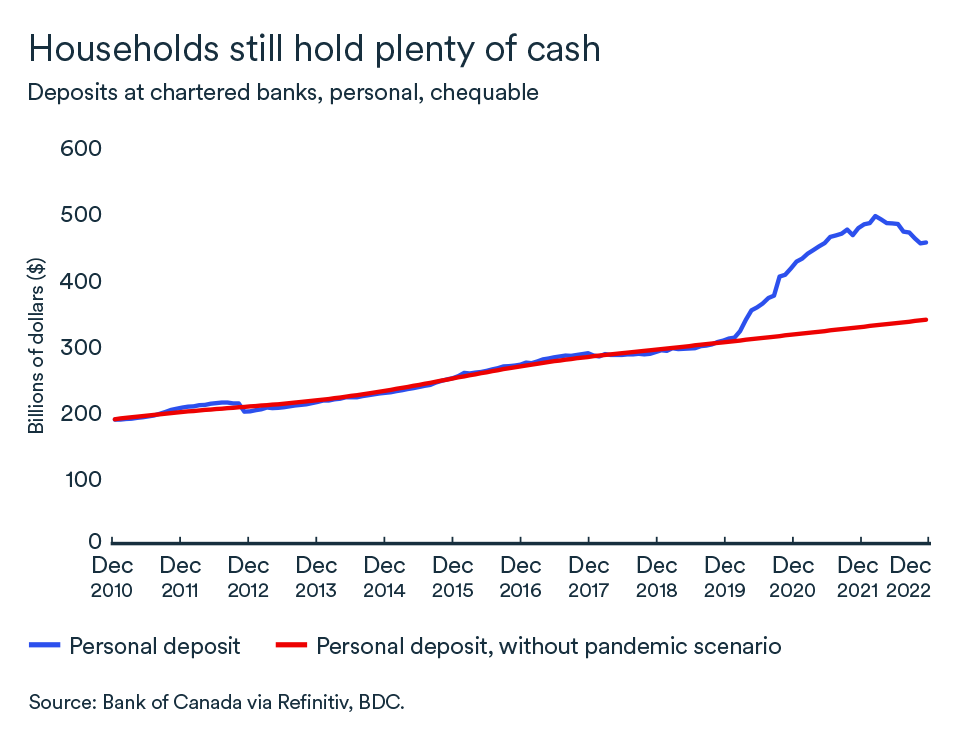

Canadians still clinging to their savings

If there was one positive economic outcome from the pandemic in Canada, it was a sharp increase in household savings. And Canadians appear to be holding onto the money they accumulated.

Savings reached about $350 billion above pre-pandemic levels in the fourth quarter of 2022. Deposits at chartered banks (which allow for immediate withdrawals) have begun to decline but are being directed more into term deposits than into consumption. Therefore, it seems the bulk of consumption has been backed-up by employment income not savings.

Again, there is disparity among income groups. The savings of the lowest 40% of income earners, which were already low at the beginning of 2020, continued to decline in 2022 under pressure from the rising cost of living. By contrast, the savings of the top 40% of income earners jumped by 28%.

The impact on your business

- Overall, the financial situation of Canadian households poses an increasing risk to economic prosperity. Certain groups are more at risk, including youth and low-income households. If your customer base is more heavily weighted towards these groups, you may experience a greater slowdown in demand.

- Rising interest rates and a sharp correction in the real estate market are also risks for indebted households. Higher rates cause households to spend more of their income on debt repayment, and real estate correction decreases the value of the assets they hold as collateral for debt. When consumers see the value of their assets decline, they feel less wealthy and will tend to be more cautious in their spending—regardless of their income class.

- Sales prospects for businesses are down, even if savings remain high. Businesses dealing with the consumer directly, particularly those related to housing or discretionary spending, should expect a more significant slowdown.

A soft landing for Canada? So far, so good

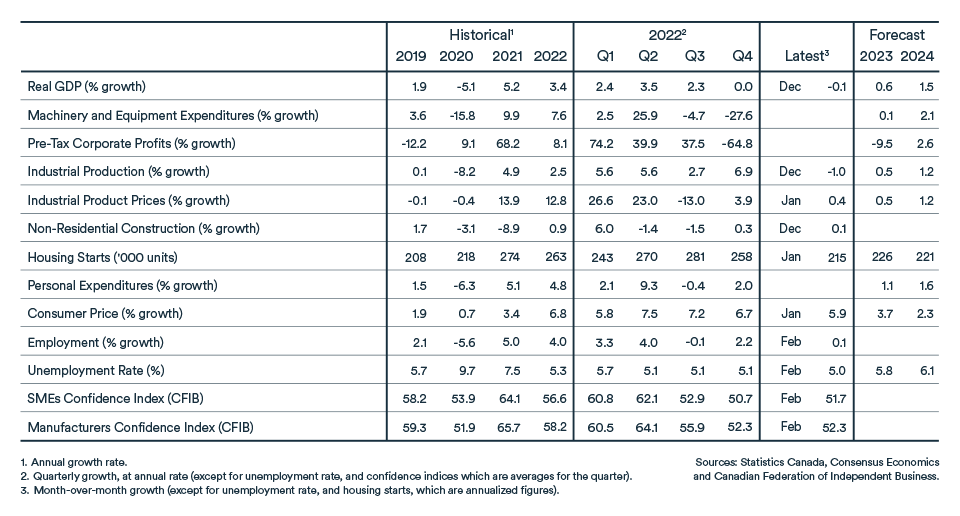

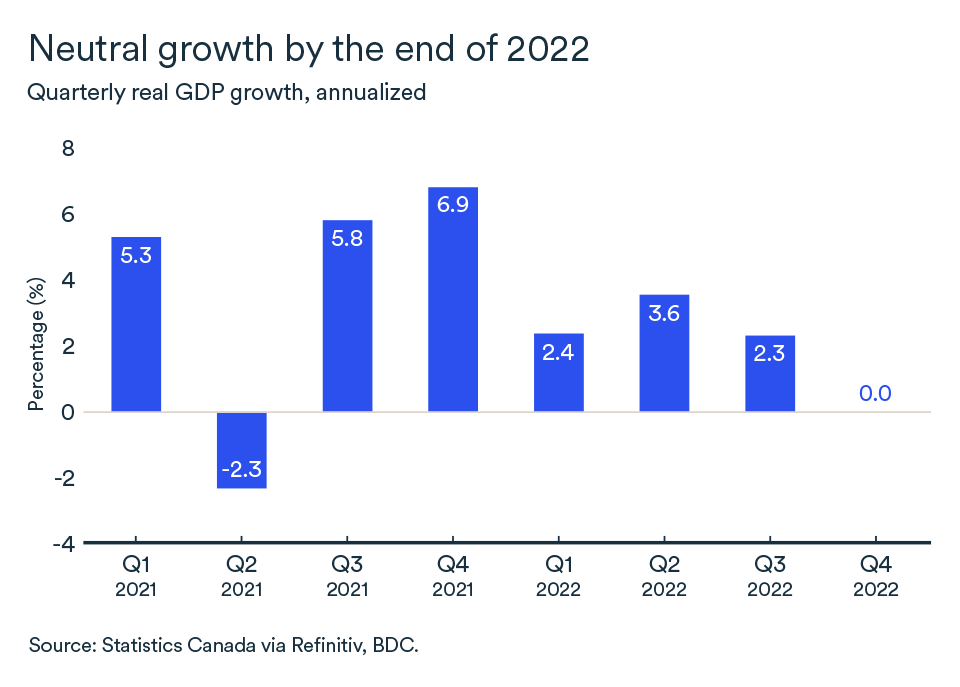

Data for the last quarter of 2022 supports a decision by the Bank of Canad this year to pause interest rate hikes. Canadian real GDP stalled in the last quarter of 2022 (+0.0% from Q3) bringing Canada’s growth for all of 2022 to 3.4%.

Canadian real GDP growth reached 0.3% in January, reversing a 0.4% decline in December, according to Statistics Canada’s preliminary estimate. The rebound in growth and continuing strong labour market raised hopes among analysts that the country could avoid a recession.

Bank of Canada keeps policy rate on hold

Despite interest rate hikes on the horizon in the U.S., the Bank of Canada is unlikely to raise interest rates again. At the last rate announcement on March 8, it held the policy rate at 4.5%.

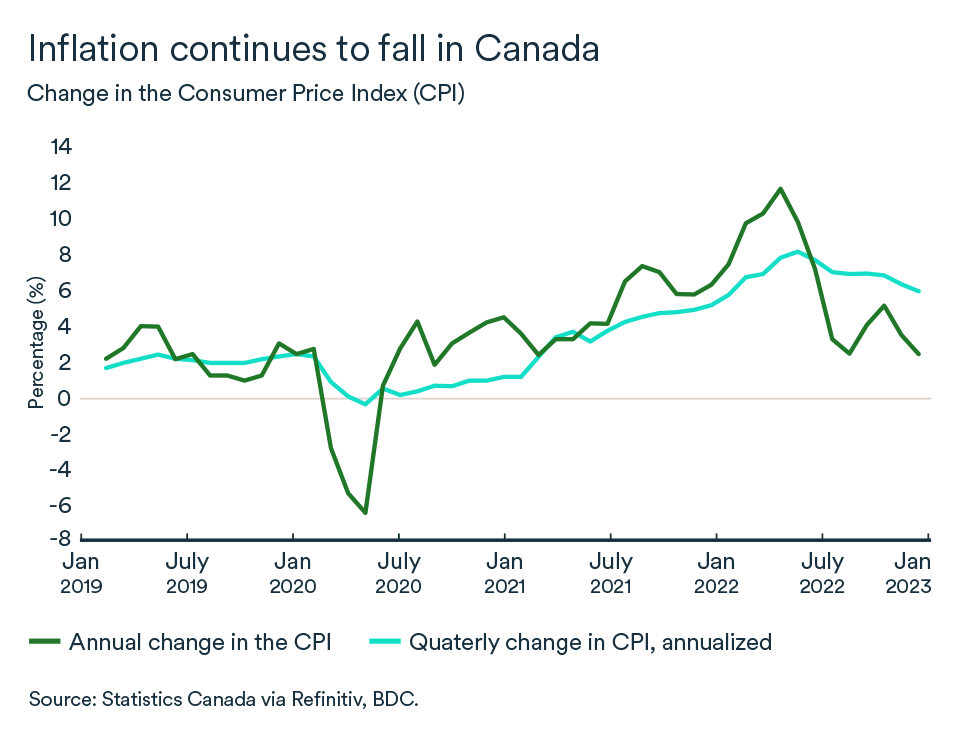

January inflation came in at 5.9%, which was actually lower than many forecasters, including the central bank, had expected. Core inflation measures, which are favoured by the bank because they’re less volatile, also came in lower. The increase in the consumer price index over three months fell below 3%.

This downward trend should continue in the coming months, which would temper Canadians' expectations for price and wage growth in the coming year.

Consumption picked up, but let’s not get too excited

Households started spending again in the last three months of 2022. After a decline over the summer, consumption has recovered to an annualized rate of 2.0%. Spending on services continued to support the economy but began to slow in favour of a rebound in purchases of durable goods.

The easing of supply difficulties at long last in the vehicle market allowed manufacturers to meet consumer demand. Despite rising interest rates, vehicle purchases soared in the fourth quarter, reflecting pent-up demand not a long-term trend.

Consumer spending on goods and services is expected to slow in the coming months.

Businesses are still holding-off

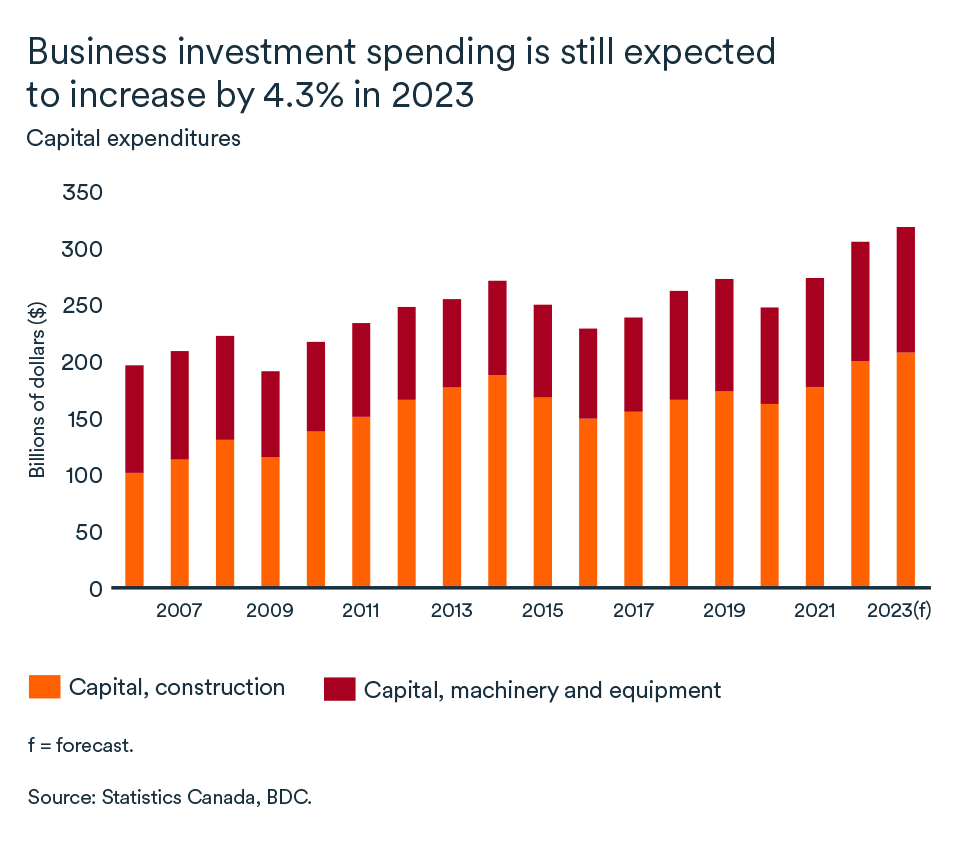

While businesses will have benefitted from the rebound in consumer spending, investment slowed in the final quarter of 2022. Investment in machinery, equipment, commercial buildings and intellectual property slowed for the first time since the second quarter of 2020, the heart of the first wave of COVID-19.

Overall for 2022, business investment grew by a solid 6.4%. According to the latest data from Statistics Canada, Canadian businesses as a whole are still planning to increase their spending on physical capital (construction, machinery and equipment) in 2023, but at a slower pace—4.3%.

Another piece of good news was a decline in inventories. After two consecutive quarters of inventory accumulation at record levels, inventories were revised downward before year-end.

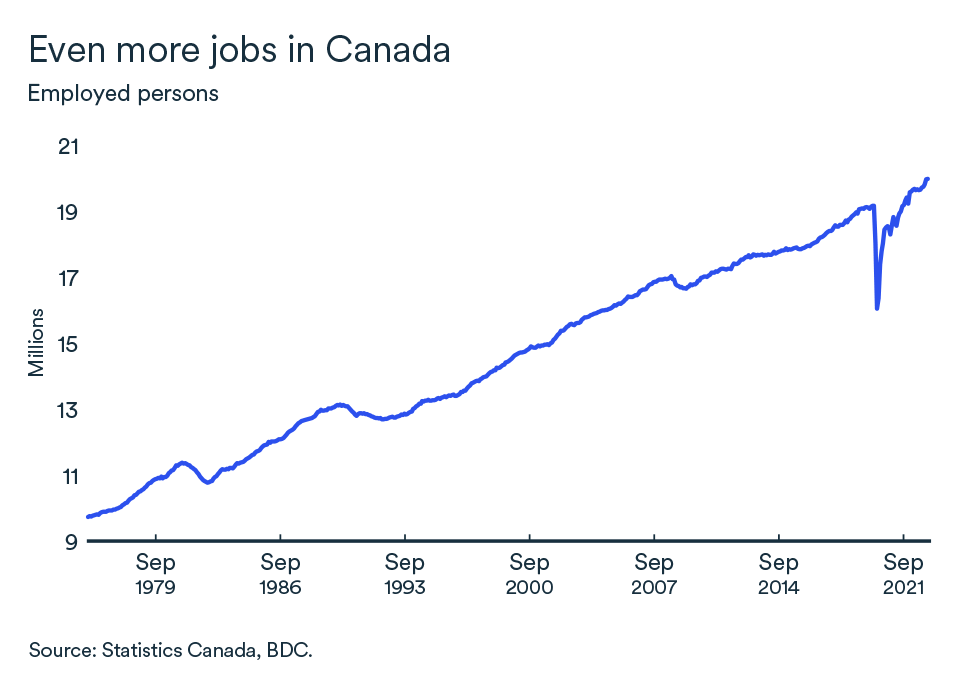

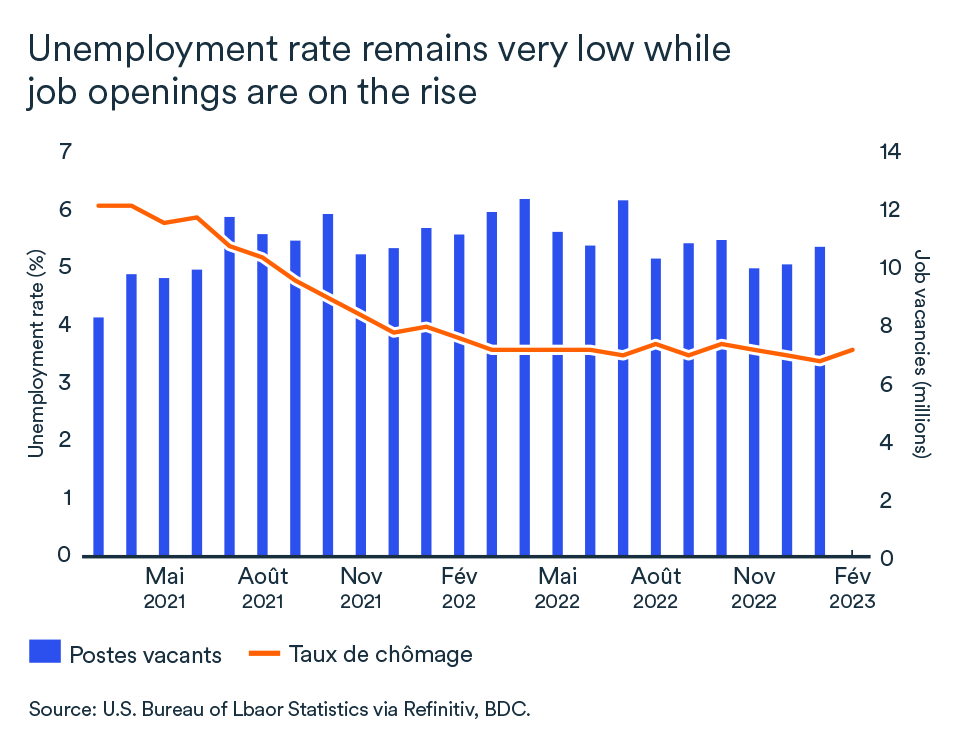

Employment is slowing

Employment growth in Canada continued in February, albeit at a modest pace. Last month, 22,000 new jobs were added, keeping the unemployment rate at a very low 5.0%.

Job vacancies were still high in December at around 850,000. The economic slowdown should reduce job openings despite a continued high rate of retirements. (Almost 265,000 Canadians left the labour market for retirement between February 2022 and February 2023.)

The latest employment slowdown and declining inflation data should start to ease wage pressure in Canada in coming months. However, for now, annual growth in average Canadian hourly earnings rose to 5.0% in February.

The impact for your business

- It’s unlikely the Bank of Canada will raise the policy rate this year, although it remains a possibility. Despite this, the slowdown in demand will continue in the coming months. Households and businesses will feel the impact of past rate hikes because it takes about 18 months for them to work their way through the economy.

- The Canadian labour market continued to show solid growth in early 2023, which should further dampen recession fears. Total compensation continues to grow in Canada and domestic demand rebounded in the last quarter of 2022.

- Most Canadian companies are still well positioned to weather the expected slowdown. Despite tighter credit conditions, investment is expected to increase this year but at a slower pace than in past years. Focusing on productivity through investment is beneficial to businesses through all economic cycles.

Interest rate hikes will continue in the U.S.

The U.S. economy is likely not slowing enough for the Federal Reserve to pause interest rate hikes with inflation and employment remaining stubbornly strong in the opening months of 2023.

As a result, an additional 25-basis-point increase on top of the current overnight rate of 4.50 to 4.75% is all but guaranteed for March 21, even taking into account the latest shock to the financial markets, namely the collapse of Silicon Valley Bank. In theory, the U.S. financial system should prove to be more resilient than in 2008. Maintaining confidence of depositors and investors will be essential to avoid a financial led recession.

Inflation remains hot

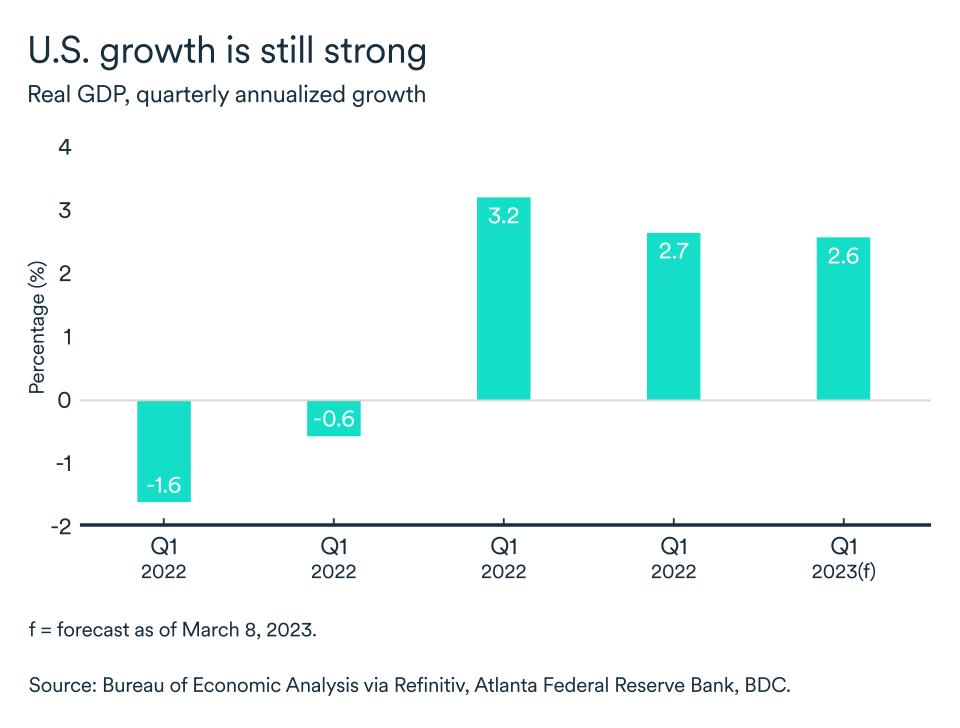

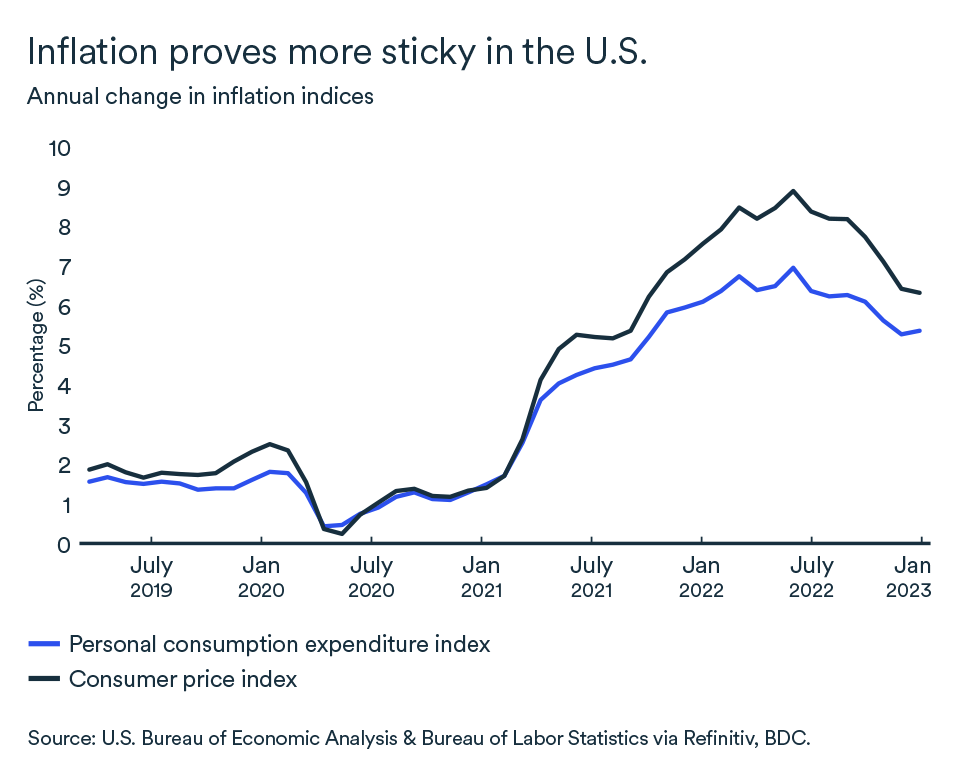

Based on the most recent economic data, real GDP growth is expected to be over 2.0% annualized in the first quarter. In addition, the inflation rate is not slowing as much as expected. In January, the increase in the consumer price index came in at 6.4% annualized from 6.5% in December.

Another inflation measure—the personal expenditure price index—actually rose to 5.4% in January from 5.3% in December. Even excluding food and energy, this index increased. It’s broader in scope than the traditional CPI and more reflective of changes in household behavior in response to recent price increases.

Americans are still spending heavily

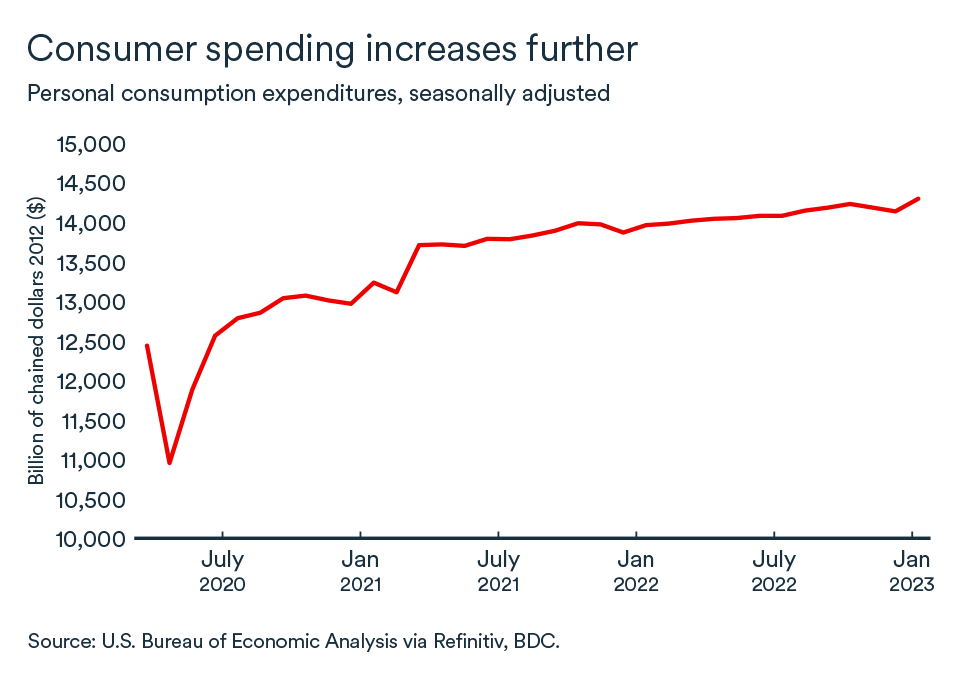

U.S. household consumption expenditures increased by 1.1% in real terms (taking inflation into account) in January. This is the strongest monthly growth since March 2021. Most of the increase at the beginning of the year was due to higher consumption of durable goods, led by purchases of motor vehicles and parts, as well as home furnishings and equipment. Americans also spent more on dining out and entertainment. The latter budget items are typically the most affected by tighter credit conditions, as they are largely financed by debt or easily avoided in the case of dining out.

The growth in consumer spending in January was supported by a 0.9% jump in earnings. Moreover, disposable household income adjusted for inflation increased by 1.4%, which will have allowed Americans to increase their savings while also boosting spending.

Job growth slows

The U.S. economy created 311,000 jobs in February, a healthy number while below the average monthly gain of 343,000 over the prior six months and significantly lower than January’s blow-out performance. January data was only slightly revised downward from 517,000 to 504,000.

The unemployment rate rose back at 3.6% in February. In the current economic context, this rise in unemployment rate is actually good news. Over the past year, average hourly earnings have increased by 4.6%.

The impact on your business

- U.S. inflation looks harder to contain than in Canada. Interest rates in the U.S. will likely rise faster, which should put additional downward pressure on the Canadian dollar and ultimately benefit Canadian exports.

- While we expect the Bank of Canada to keep its policy rate at the current level of 4.5% for most of the year, federal funds rate hikes could tighten credit further here as Canadian financial institutions also tap into the U.S. market.

- U.S. households have started spending again. Wage growth and total compensation in the U.S. remain strong and the labour market had another solid performance in February. Households should therefore continue to support U.S. economic growth in the coming months.

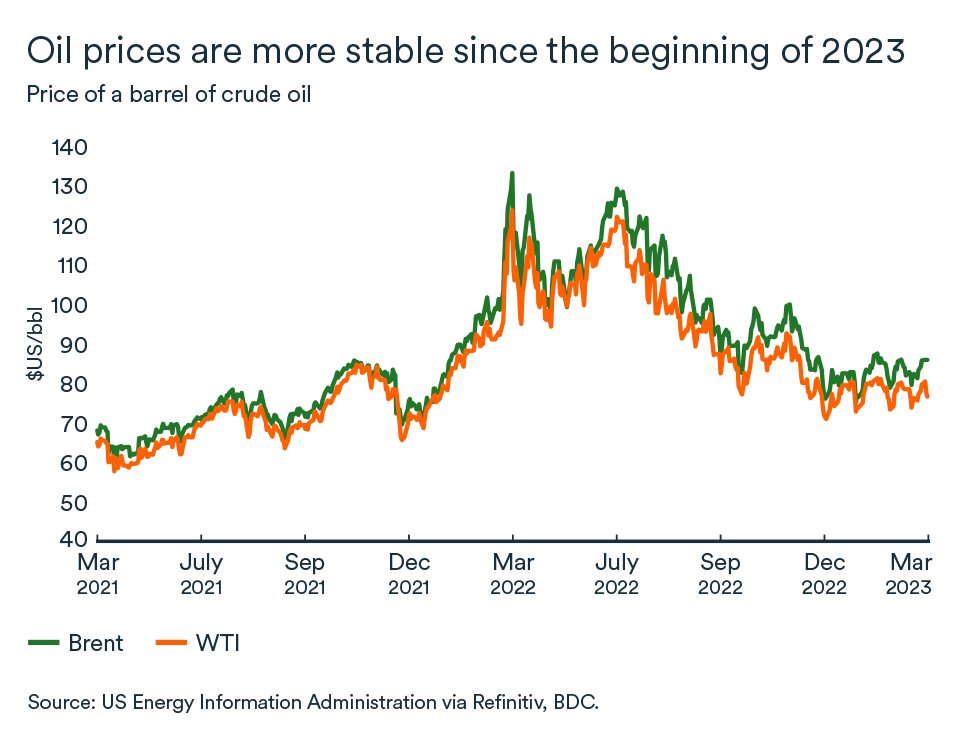

Crude oil prices could fall further in the coming weeks

Oil prices have remained at much more reasonable levels since the beginning of 2023. In early March, the main benchmarks reached US$82 per barrel for Brent and US$80 for WTI. Crude oil could fall further in the first half of the year.

The Federal Reserve's tone worries the market

After a presentation to Congress by Federal Reserve Chairman Jerome Powell on March 7, oil lost ground on concerns that more interest rate hikes are ahead.

U.S. economic data at the beginning of the year has come in too hot for the Fed to stop its tightening cycle and it will likely have to raise the federal funds rate more than is currently priced into crude.

Higher interest rates to slow the U.S. economy will put further downward pressure on the price of oil. On the other hand, the U.S. dollar has appreciated significantly against other currencies, making oil (denominated in U.S. dollars on the world market) more expensive for international buyers.

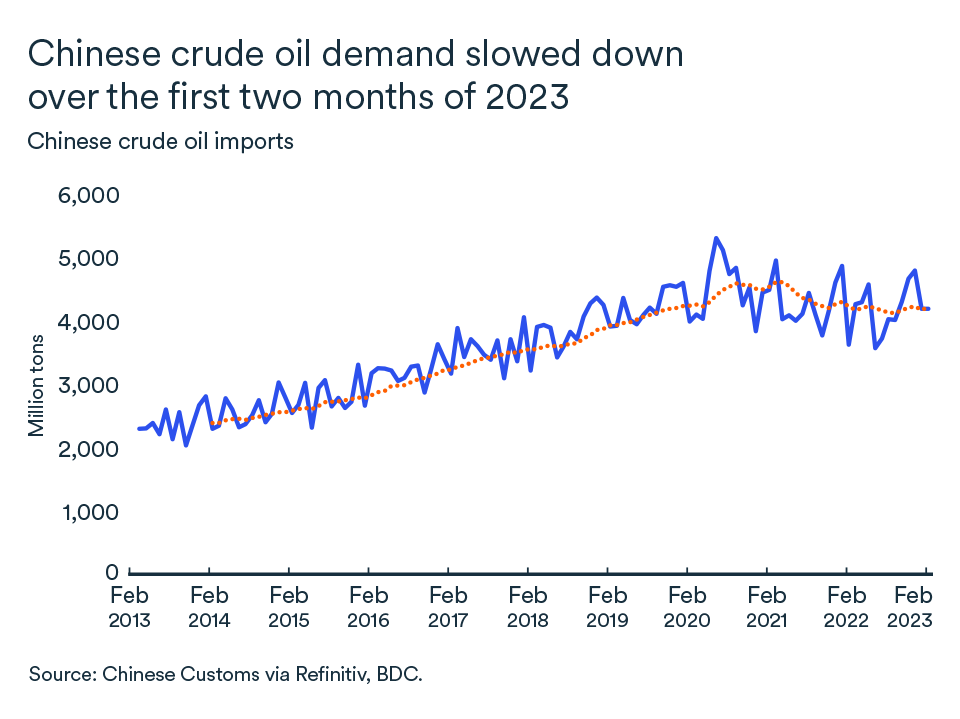

The Chinese economy is slowing

China has set its economic growth target for 2023 at just 5%, the lowest level in recent history, with the exception of the COVID year of 2020. Last year, China grew by just 3%.

It appears the decision to abandon the zero-COVID policy will not be enough to restore the country's pre-pandemic momentum in the face of slowing global demand, rising geopolitical tensions and a housing market crisis.

Chinese oil imports fell 1.3% in January-February 2023 from a year ago despite the reopening of the economy. This news from the world’s largest crude importing economy did nothing to improve the outlook for oil demand growth in 2023.

Prices should recover in the second half of the year

Short-term trends, therefore, point to price levels similar to what we are seeing now, but the outlook is brighter for a recovery before the end of 2023. The Organization of Petroleum Exporting Countries is aiming to keep production levels unchanged for the rest of the year. The cartel will likely have helped rebalance the market since the end of 2022.

As the year progresses, supply issues could push prices back up and remain a serious risk. Inventories could fall quickly as a lack of investment is already limiting production capacity in some countries. For example, Angola and Niger are still unable to meet their production quotas.

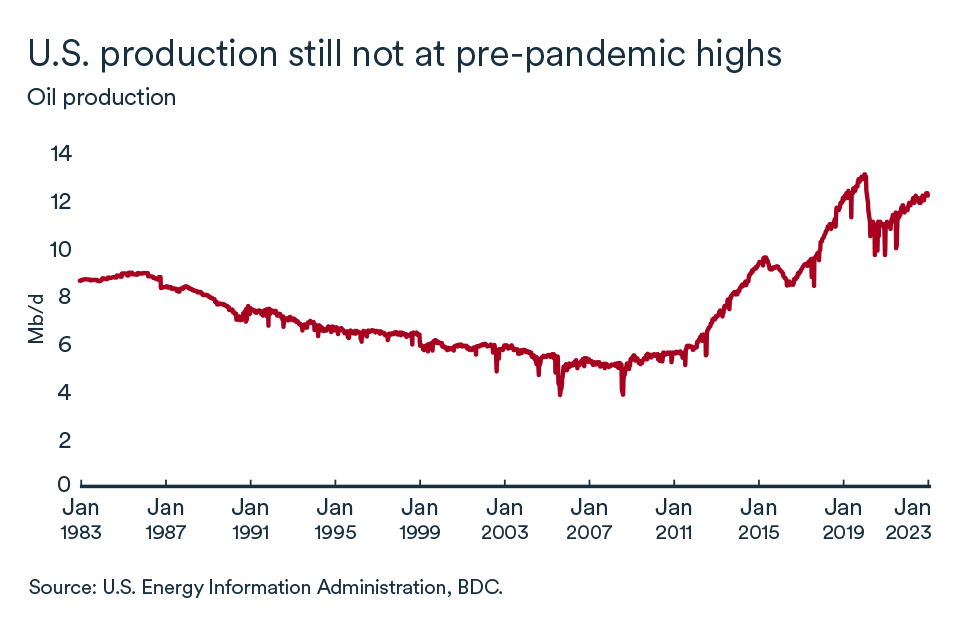

U.S. production accounts for about 10% of global oil supply but is still recovering slowly from the pandemic. The U.S. is producing at a rate of 12.3 mb/d which is still below the pre-pandemic level of 13.1 mb/d. And leading shale company executives expect future growth to be much slower, reaching a plateau in the coming years.

Bottom line…

Slowing global economic demand factors in the near term will contribute to oil prices falling further in the coming months, or at least remaining near their current levels. However, the longer-term crude market outlook will be dominated by supply issues. Prices could rise quickly in the last few months of the year.

Interest rates at 4.5% in Canada despite the Fed

The Bank of Canada announced that it was holding the policy rate at 4.5% in its last announcement on March 8. Despite the interest rate hikes in the U.S. that will continue, it is unlikely that the Bank of Canada will start raising interest rates again, although it says it is open to doing so, if necessary. In our view, it will not be necessary and the next change in monetary policy is still expected to be a cut, which could occur in late 2023. It is not uncommon to see a differential between U.S. and Canadian rates. In the current inflationary environment, it is true that the downward pressure this differential will put on the exchange rate could temper the fight against inflation in Canada, but the biggest risk that could force the Bank of Canada's hand to raise the policy rate remains Canadian economic data, including wage growth, not U.S. monetary policy.

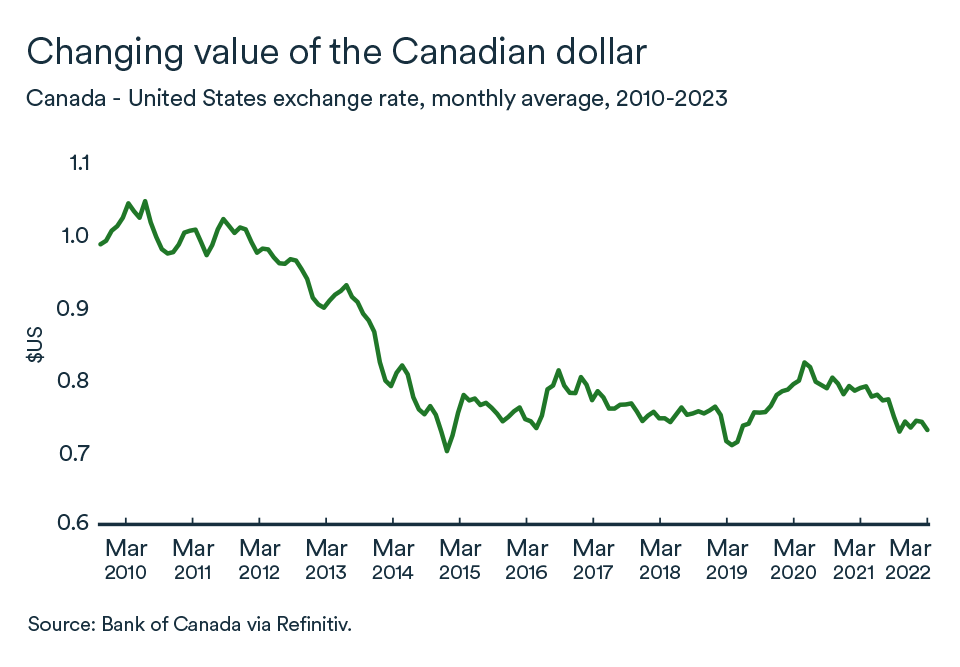

The exchange rate is falling

The Canadian currency began to fall further in March as the divergence between Canadian and U.S. monetary policies became more apparent. The loonie moved closer to US$0.72 and will have regained some strength after the release of the February employment numbers. Much of the rate differential has already been anticipated in the currency market, but it would not be surprising to see the loonie move closer to US$0.70 in the coming weeks as commodity prices (another important factor to consider when analyzing changes in the Canadian exchange rate) will also be down in the short-term.

A weaker Canadian dollar tends to benefit exports at the expense of imports. It should be noted that the Bank of Canada does not have a mandate to ensure the performance of the dollar and will not intervene to support the exchange rate (unless there is a force majeure event—and we are far from it).

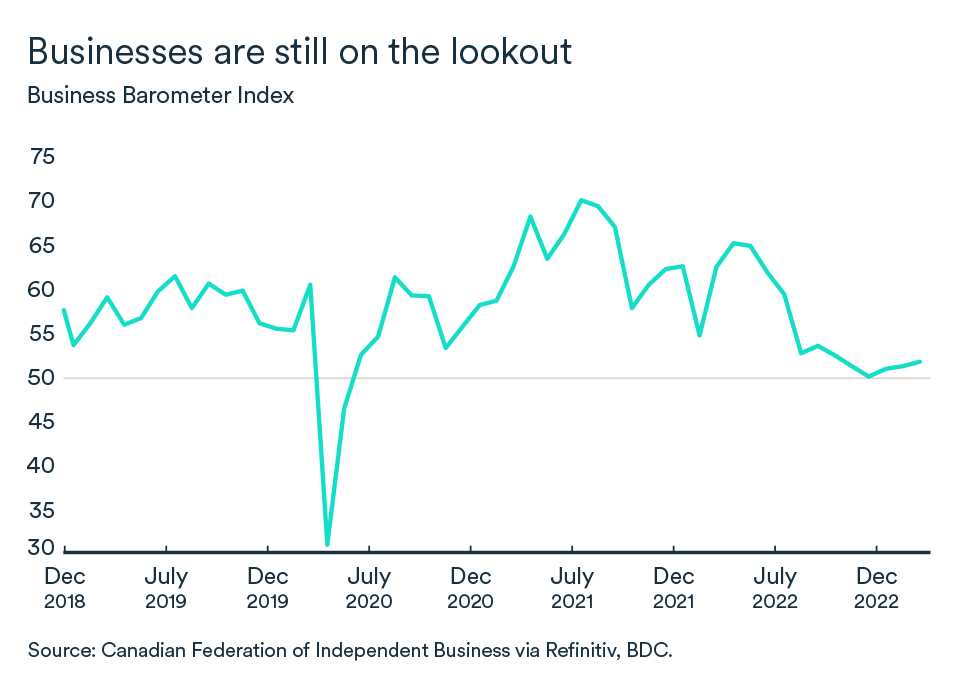

Businesses are still on the lookout

In February, the CFIB's business confidence index for the coming year essentially held steady at 51.7, up from 51.4. Even so, the index has continued to improve over the past three months. Businesses remain on edge, but the downturn in 2023 may be less severe than they anticipated in 2022. An indicator of 50 indicates that as many business managers expect the business environment to worsen than improve over the next 12 months.