Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreEconomic outlook 2023: cause for caution, not alarm

Recovery from the short but deep recession caused by the COVID-19 pandemic is proving to be more difficult than anticipated a year ago. In 2022, the question has shifted from “is this the end of the pandemic" to "are we in a recession."

The simple answer for Canada is that we’re still not in a recession. And while the economic outlook has darkened in recent months, the economy can still avoid slipping into negative growth. The year 2023 will, however, be characterized by a slow down and a great deal of uncertainty. A slower economy is necessary to counteract inflation but will policymakers go too far?

The legacy of a turbulent year

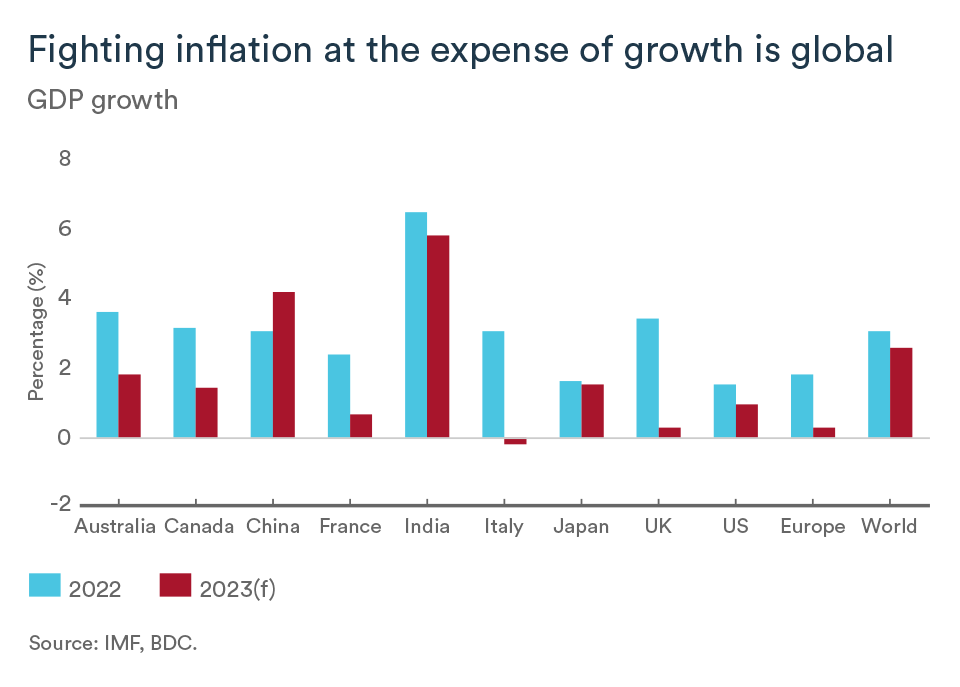

Before making predictions, it’s always important to know where we stand. It’s now clear that 2022 was a turning point for the global economy. The war in Ukraine, the resulting sanctions on Russia and a sharp slowdown in China all weighed on global growth as the year progressed. High inflation forced central banks to raise interest rates sharply to bring down inflation.

The European economy suffered a serious setback due to the invasion of Ukraine in late February 2022 and continues to face a major energy crisis. The U.S. economy, meanwhile, was hurt by consumer pessimism and caution in the face of high inflation, interest rate hikes and a declining stock market. U.S. GDP declined in the first two quarters of the year, but a rebound in the second half helped offset the earlier losses.

The Canadian economy in 2022 proved resilient despite global problems and growing uncertainty. Growth was supported by a strong recovery in the labour market, household savings, high commodity prices, increased business investment and pent-up demand for services following the end of COVID restrictions.

What can we expect in 2023?

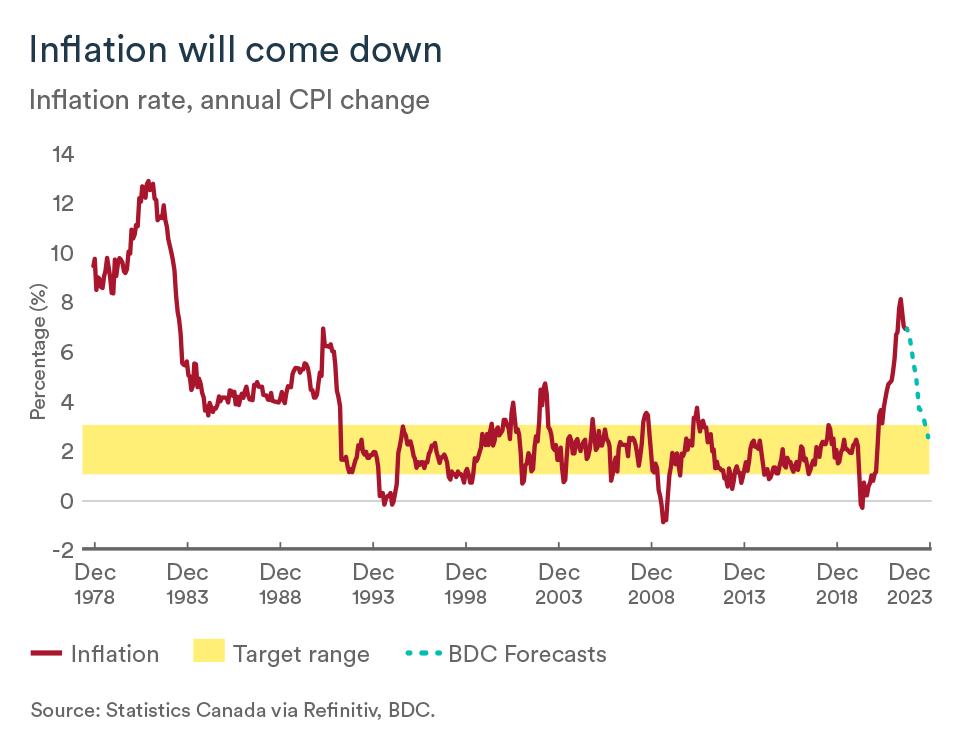

While there is some disagreement among economists about whether we are headed for a recession, there is consensus that the economy will slow in 2023. The source of the slowdown is the Bank of Canada's fight against inflation. Interest rate hikes are expected to continue in the new year, but there’s a lot of uncertainty about how much further the bank will go.

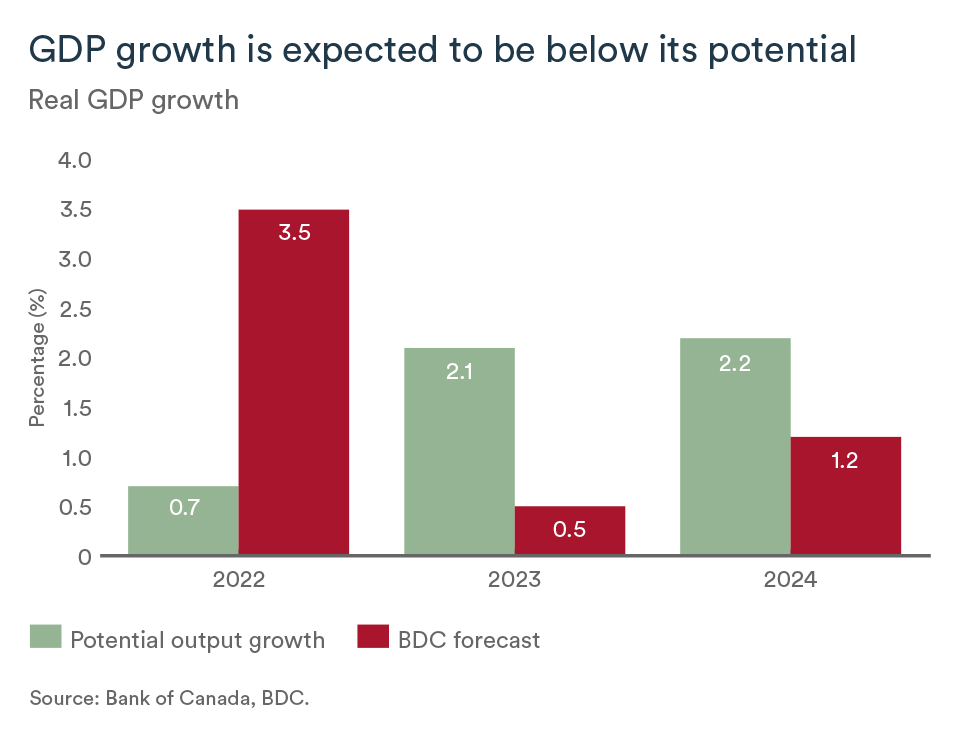

The recipe for bringing inflation back to the bank’s 1-3% target appears simple on paper—tamp down demand enough to allow for supply to catch up. This implies engineering below-potential GDP growth, estimated by the Bank of Canada to be about 2.0% in 2023 and 2024. In practice, it gets more complicated.

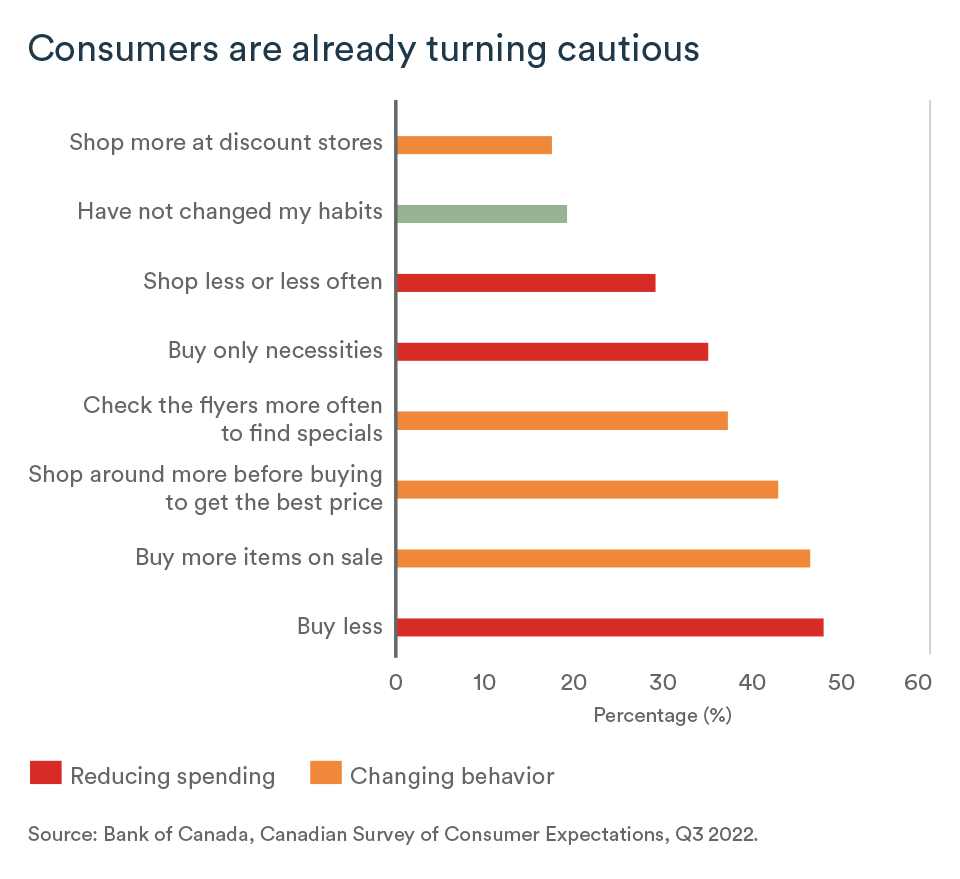

Households and businesses will be cautious

Household spending is the main engine of economic growth. While consumption typically accounts for about 60% of GDP growth, we estimate it accounted for nearly 80% in 2022.

During an economic downturn, employed individuals tend to spend less and save more for fear of layoffs. Indeed, even though household savings have slowed from their peak in 2020, they are still significantly higher than before the pandemic.

Rising interest rates have pushed down the stock market and home prices and these downturns are making people feel less wealthy and weakening their enthusiasm for spending that came with the reopening of the economy.

The slowdown will therefore hurt business sales. While most businesses are well-positioned financially and consider themselves prepared for a potential recession, the first quarter of the year will be critical for testing their resilience. A more pronounced decline than expected could lead them to cut their investment plans for the year.

Policy rate to reach 4.5%

While Canadians will be happy to see the progress made in the fight against inflation so far, there’s still a long way to go. The Bank of Canada raised its policy rate by 350 basis points in 2022 and inflation has been slowing since June.

We expect the policy rate could go as high as 4.5% next year before the central bank takes a break and allows time for past hikes to work their way through the economy. However, a change in the central bank's course could come earlier than expected in the new year.

As demand slows and core inflation stabilizes, Canada could benefit from lower interest rates before the end of 2023. However, we believe it will take another 18 months before the Bank of Canada’s policy rate return to the neutral level of 2.5%.

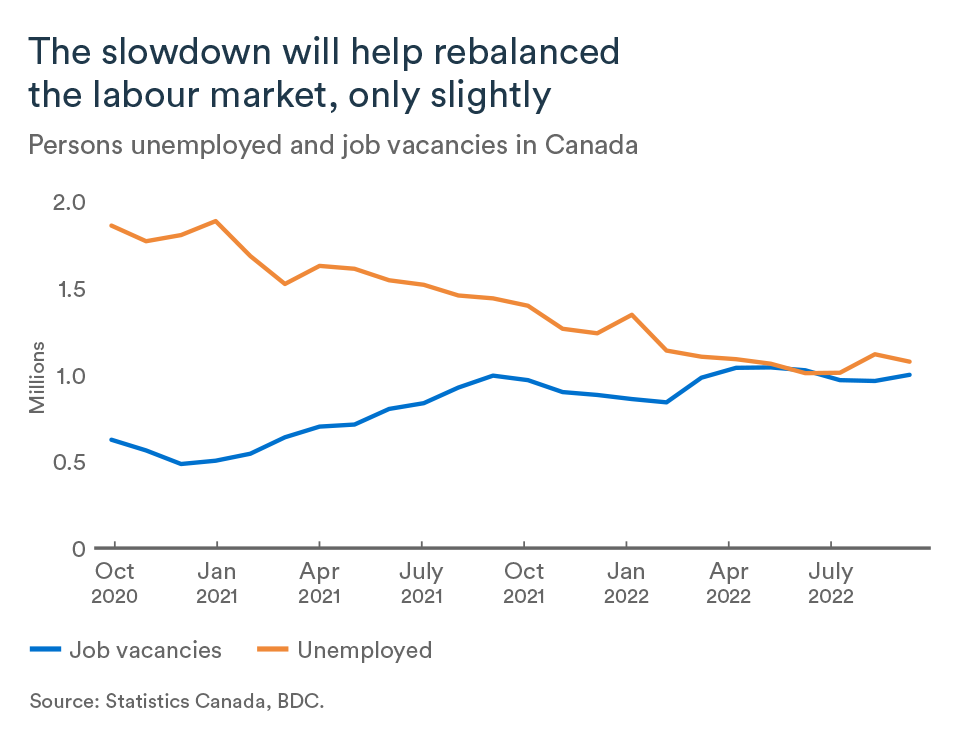

Towards a rebalancing of the labour market

Typically, an economic downturn is accompanied by an increase in the unemployment rate. Layoffs increase as companies cut back on production. However, Canada still had around 1 million job openings in September. Thus, a contraction in the labour market is more likely to translate into fewer hours worked and less demand for staff.

Since there are continuing issues of matching the skills of the available workforce with the needs of businesses, a downturn in the labour market will be less pronounced than during similar periods of economic contraction in the past.

No recession, but low growth

At BDC, we expect economic growth to stagnate, but not contract thanks to the economy’s still solid fundamentals. Therefore, our most plausible scenario for Canada is for annual GDP growth of 0.5% in 2023, including one or two negative quarters.

The slowdown will be most pronounced in residential investment and goods consumption. Energy and food prices will also continue to eat into household incomes and the pent-up demand for services left over from the pandemic will fade as the year progresses. The Canadian dollar will remain relatively weak against the U.S. dollar, which will favour exports at the expense of imports.

Since the downturn is being driven by tightening monetary policy, Canada has more control over its economic performance than in recent downturns, which were generated by external shocks such as the 2008-09 financial crisis and the pandemic.

Canada’s economic resilience continues to surprise

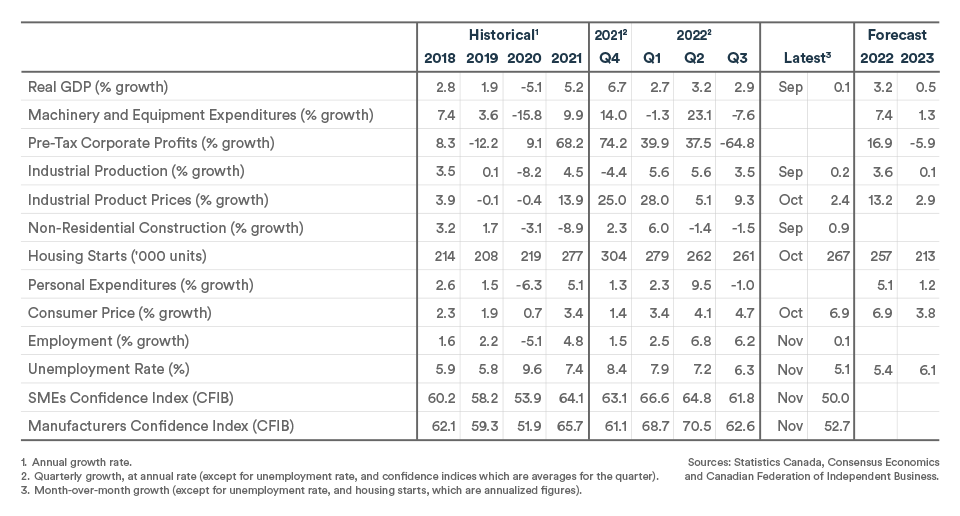

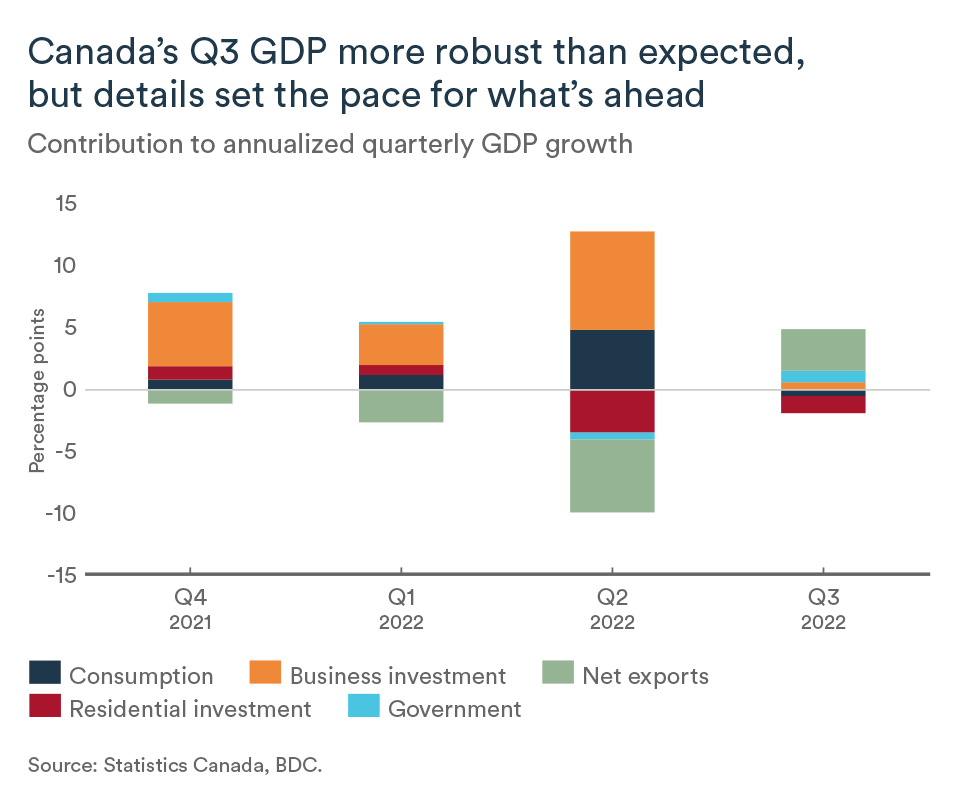

Canadian economic activity in the third quarter was significantly better than expected. GDP continued to grow at a solid pace, rising 2.9% compared to an average forecast of slightly above 1%.

The devil is in the details

Despite this impressive growth, a deeper analysis of the data points to trouble ahead. Consumer spending fell for the first time since the spring of 2021. As expected, consumers favored spending on services, while rising interest rates began to hurt goods consumption, which fell by 6.5% from the previous quarter.

Rising business inventories were another source of concern. This quarter, they were a source of GDP growth, but higher inventories also imply weaker demand going forward. Consistent with our forecast, and what one would typically expect in a rising rate environment, inventory accumulation was stronger in the manufacturing, wholesale and retail sectors.

The monthly GDP figures also indicated a loss of momentum in the economy. The level of growth slowed in September to 0.1% after increases of 0.2% and 0.3% in July and August, respectively. Preliminary estimates from Statistics Canada suggest the downward trend continued with sluggish growth in October.

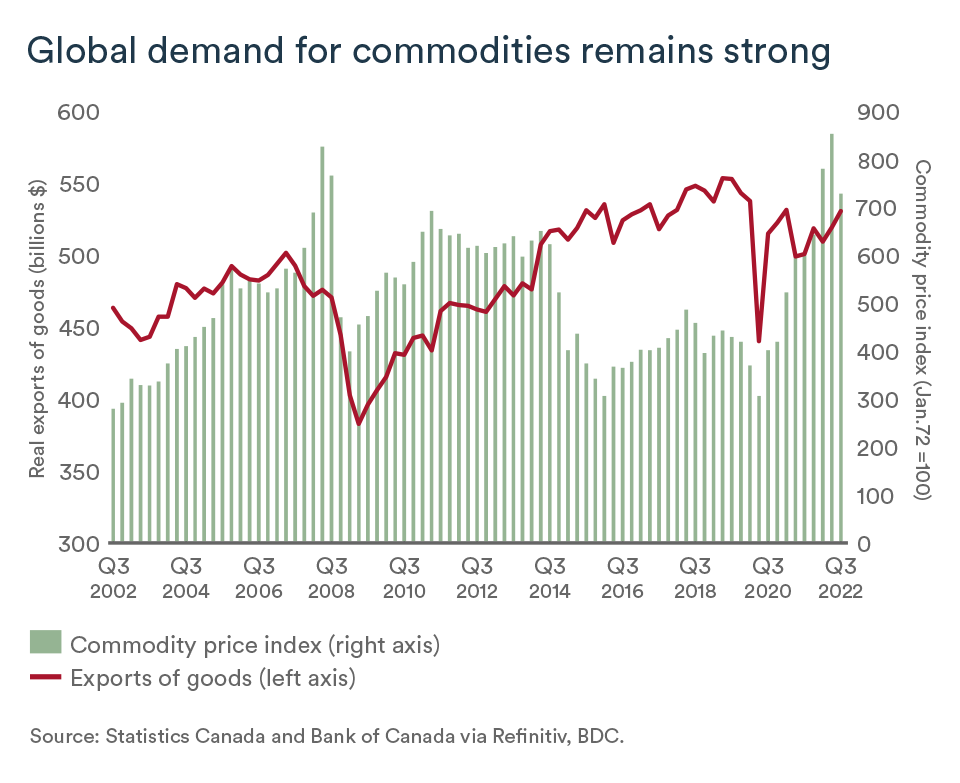

Raw materials are still in high demand

Exports accounted for much of the growth in the third quarter. Despite a drop in many commodity prices after the initial shock of the Russian invasion of Ukraine and an expected global economic slowdown, the appetite for commodities remains strong.

The main contributors to growth in real exports (controlling for price movements) were crude oil, agricultural and fish products, intermediate metal products and non-metallic minerals.

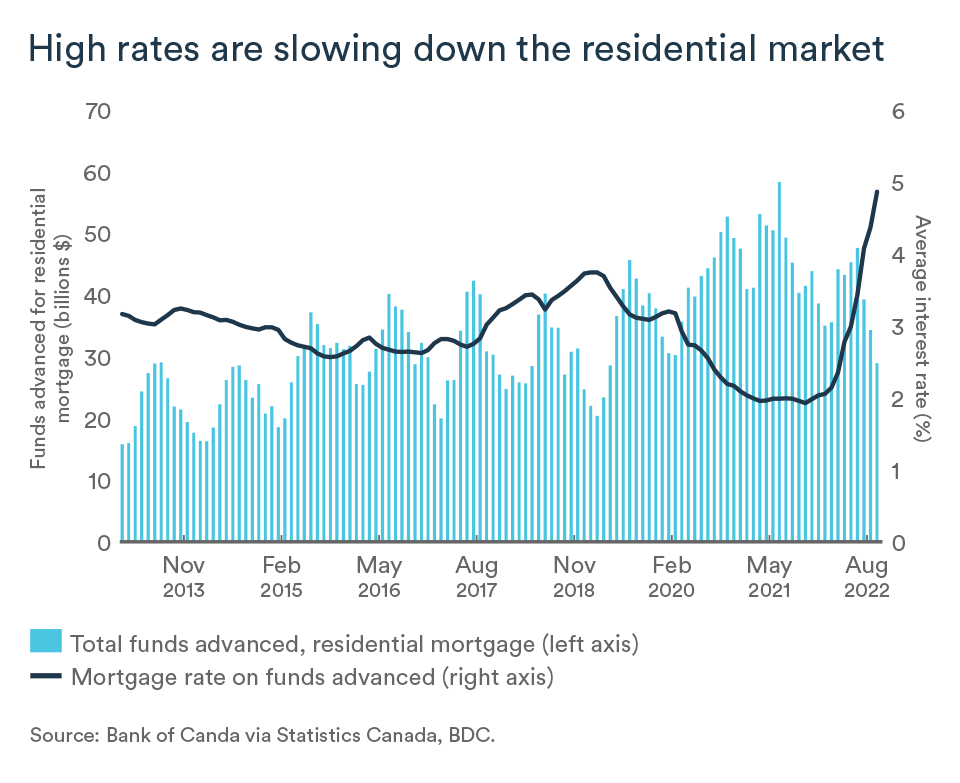

Housing sector challenges persist

The decline in real estate prices is both a cause and a consequence of the decline in residential investment (-15.4% in the third quarter). Rising interest rates have reduced demand in the resale market and led to a downward move in the average price. It has fallen by 18% compared to its level before the first rate hike in March 2022.

Inventories of existing homes could not keep up with demand during the pandemic, which led many markets to overheat. Today, the price correction is discouraging some potential sellers to put their home on the market, especially if they have to take out a new mortgage at higher rates to move.

Homeowners have also grown cautious in the face of economic uncertainty. Renovation activity declined for a second consecutive quarter.

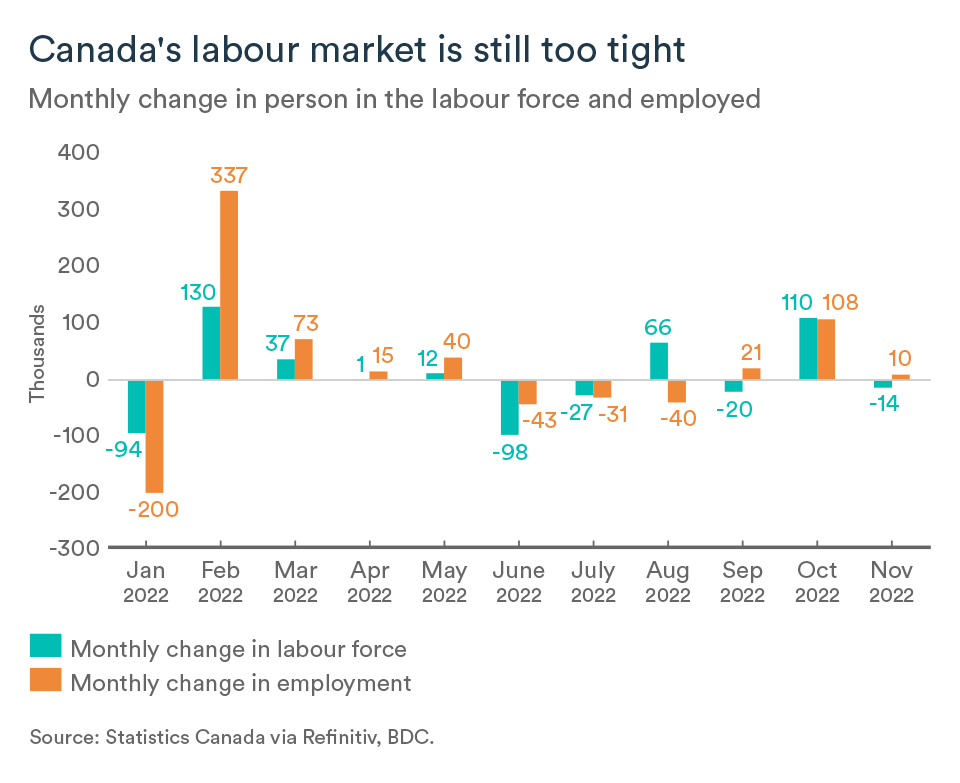

More employment gains

The Canadian economy created 10,000 jobs in November. Unsurprisingly, the pace of job creation fell from the impressive level reached in October. Labour supply declined, after growing by 110 000 in October, the labour force contracted in November with nearly 14 thousand fewer potential workers.

However, many companies are still struggling to recruit staff. In September, there were still around 1 million jobs available in Canada. A recent BDC survey found that labour shortages remain the main obstacle to the growth of Canadian businesses. The unemployment rate at 5.1% is among the lowest in Canadian history.

The impact on your business

- Despite the strong GDP growth in the third quarter, an economic slowdown is taking hold. Consumption of goods is decreasing and inventories are rising. Companies would be well-advised to optimize their inventory management and make other preparations for the slowdown.

- Employment continues to grow across the country and recruiting is still a challenge. The available workforce may not be exactly what you are looking for. Consider developing an in-house training program to bring on new employees and increase the flexibility of your current staff.

- The residential sector continues to slow due to rising rates. The longer rates stay high, the more households will have to renegotiate their mortgages, which will take a bigger bite out of their budgets. Even if your business is not directly related to the housing sector, you will feel the impact of the downturn in one way or another.

Smaller rate hike expected in December

U.S. GDP growth was revised slightly upward in the third quarter to 2.9% from an initial estimate of 2.6%. This revision is encouraging because it reflects an increase in consumer spending and non-residential investment. There was also a decline in business inventories and imports.

Will consumer resilience continue?

During the quarter, a recovery in the consumption of services was offset by a slow down in spending on goods. The acceleration of spending came as real disposable income strengthened (+0.9%) and gasoline prices fell.

Still, U.S. households began to dip into their savings to support consumption. The nation's savings rate is now lower than it was before the pandemic. While inflation is showing signs of slowing, consumer confidence remains too low and interest rates too high to expect sustained growth in consumer spending.

Moderate easing in the labour market

Job growth continued at a modest pace. Nearly 263,000 new jobs were added to U.S. payrolls in November.

The unemployment rate has remained virtually unchanged this year, from 4% in January to 3.7% in November, even though over 4.3 million jobs have been added as concerns about COVID receded and people returned to the labour market.

Unlike the Canadian job market, wage pressure had been easing in the U.S. for several months and supported the Federal Reserve’s fight against inflation, however they edge back up in November. Nonetheless, job openings and quits fell slightly in October, indicating that tightness in U.S. labour market is abating which should limit wage growth in 2023.

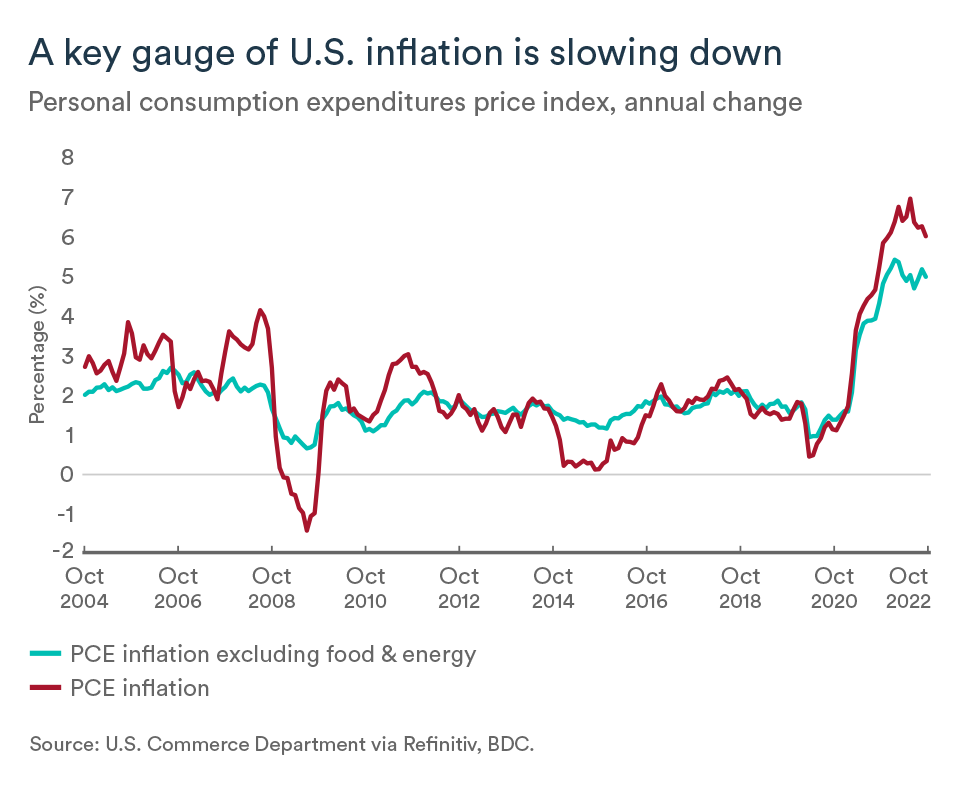

Declining inflationary pressures

U.S. inflation as measured by the Consumer Price Index (CPI) hit a record high of 9.1% in June before falling back to 7.7% in October. However, another measure, Core Personal Expenditure Price Index, fell to an annualized 5% in October.

The personal expenditure index is the Fed's preferred index because it is broader in scope and more reflective of changes in household behavior during price increases than the CPI.

The Fed is expected to slow the pace of rate hikes

Fed Chairman Jerome Powell said that size of U.S. interest rate hikes could be reduced as early as December. Therefore, most Fed watchers now expect a hike of 50 basis points at the next meeting on December 14. However, this won’t signal an end to the U.S. central bank’s tightening of monetary policy with more hikes likely to come in 2023. Interest rates are now in a range of 3.75% to 4.0%.

What this means for businesses

- While economic growth returned to the U.S. in the third quarter, economic gains for Canada will remain limited since U.S. imports decreased even more than initially estimated.

- Contrary to Canada, the U.S. labour market is showing signs of easing which should slow wage growth south of the border. Canadian businesses could find it harder to compete with U.S. businesses in 2023 as American cost pressures could be more muted than in Canada.

- U.S. inflation has been showing signs of improvement. Interest rates in the U.S. are likely to start rising slower, but they will have to stay elevated for some time once the Fed is done tightening. The Canadian dollar will likely recover some lost ground in the short run.

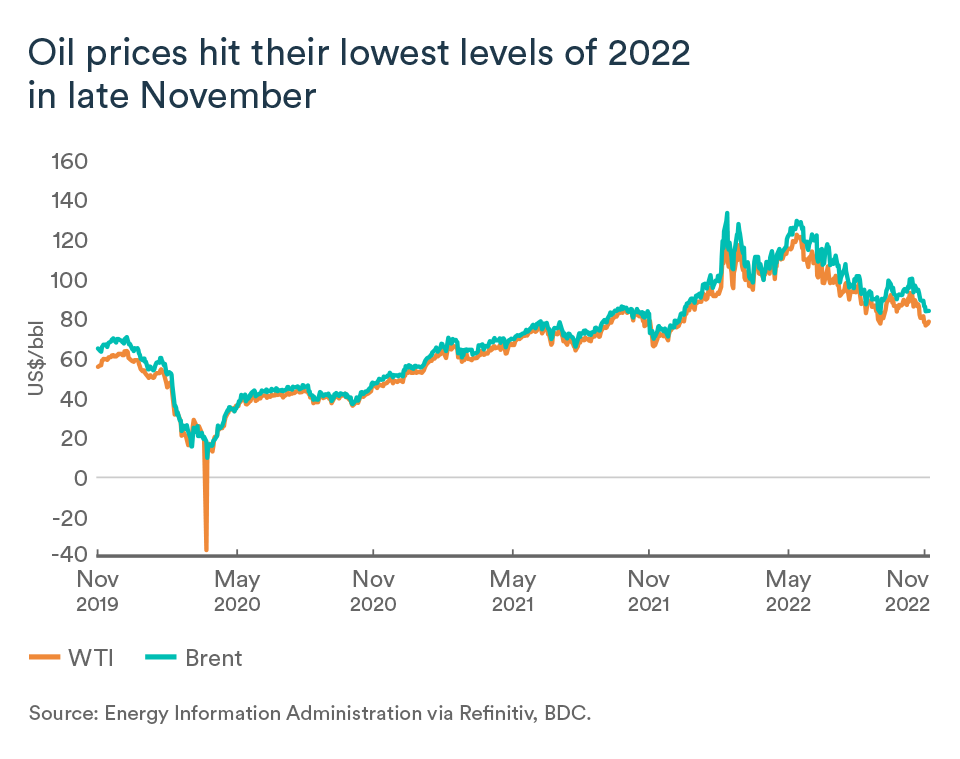

Uncertainty weighs on the oil market

The major crude oil benchmarks both ended November lower with Brent crude trading at US$88.40 per barrel and WTI at US$78 per barrel.

During the month, crude prices hit their lowest levels of the year as the market faced a lot of uncertainty on both the supply and demand sides.

Bearish factors predominated in November

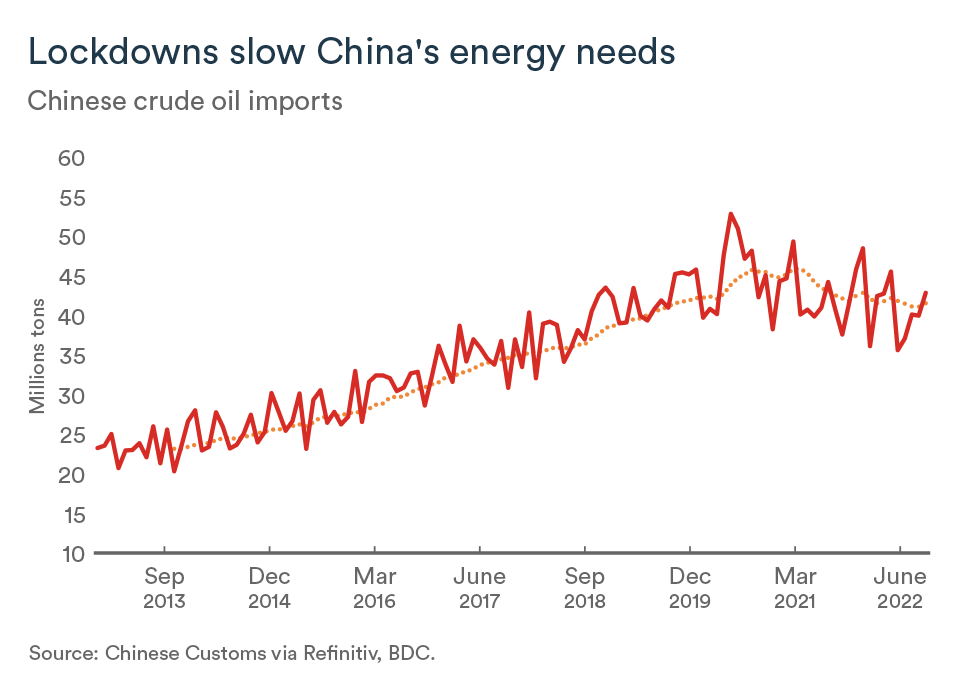

The global economy faces significant challenges. The largest economies, including the U.S., are expected to stagnate or fall into recession in 2023. In China, more than a quarter of the population is in varying degrees of lockdown to prevent the spread of COVID. In response, popular protests have erupted.

In light of these issues, global growth will likely continue to suffer, diminishing the prospects for higher demand in the oil market.

The onset of a global economic slowdown and COVID-related upheaval in China are the dominant factors behind the recent decline in crude prices. WTI was down 10% in one month and Brent 5%.

What to expect from the Russian oil price cap?

As of late November, discussions were continuing between the G7, the European Union and Australian authorities on introducing a price cap on Russian oil. According to end of November informations, the limit considered would have been between US$65 and US$70 per barrel, which is higher than the price at which the Urals (the Russian benchmark) currently trades. A week later, under pressure from some European countries, the limit imposed would be closer to US$60 a barrel.

The objective is to limit Russia’s ability to finance the war in Ukraine without creating significant supply issues in the global market. To meet this goal, the maximum price targeted will have to be below the price at which Asia is currently buying Russian oil (US$65). Therefore, the cap’s impact is not expected to have a major effect on global supply at this time.

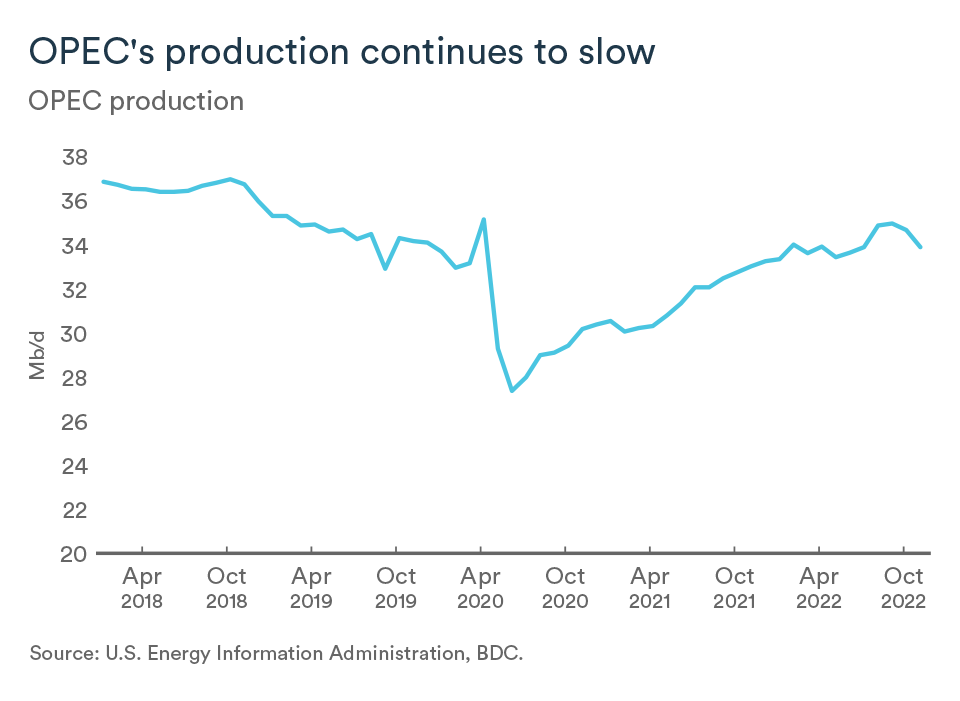

OPEC+ still anticipates an oversupplied market

The Organization of Petroleum Exporting Countries and its allies (OPEC+) had agreed to significantly reduce its production targets in November. At a December 4 meeting, members agreed to not reduce production further despite falling prices.

However, European oil inventories are now well-stocked. The announcement of an impending embargo on Russian oil will have led many refineries to fill their tanks in recent months for fear of shortages. They also appear to have diversified their crude suppliers since the invasion of Ukraine by Russia.

Bottom line…

Uncertainty remains high in the oil market and is expected to continue into 2023. Considering the cross-currents of a global economic slowdown, China's COVID difficulties, restrictive measures on Russian oil and OPEC's production restrictions, it’s difficult to predict where oil benchmarks will go next year.

If the global economic slowdown turns out to be more severe than currently anticipated, prices will fall. On the other hand, if China eases its zero-COVID policy and the economy rebounds, the opposite will be true.

For now, supplies are plentiful, driving prices to their 2022 lows. However, OPEC and its allies will adjust their production with the goal of keeping prices around US$85 to $90 per barrel.

Towards the end of rate hikes

The Bank of Canada is slowly putting the brakes on its rate hikes. After significant and historic hikes of 75 or 100 points during the summer, the pace of tightening eased in October and December to 50. The latest announcement on December 7 therefore brings the policy rate to 4.25%. We expect the rate to reach 4.5% in the first quarter of 2023, however, the central bank will be cautious, as economic uncertainty remains high and mortgage debt in the face of rising rates is a concern for an increasing number of Canadian households.

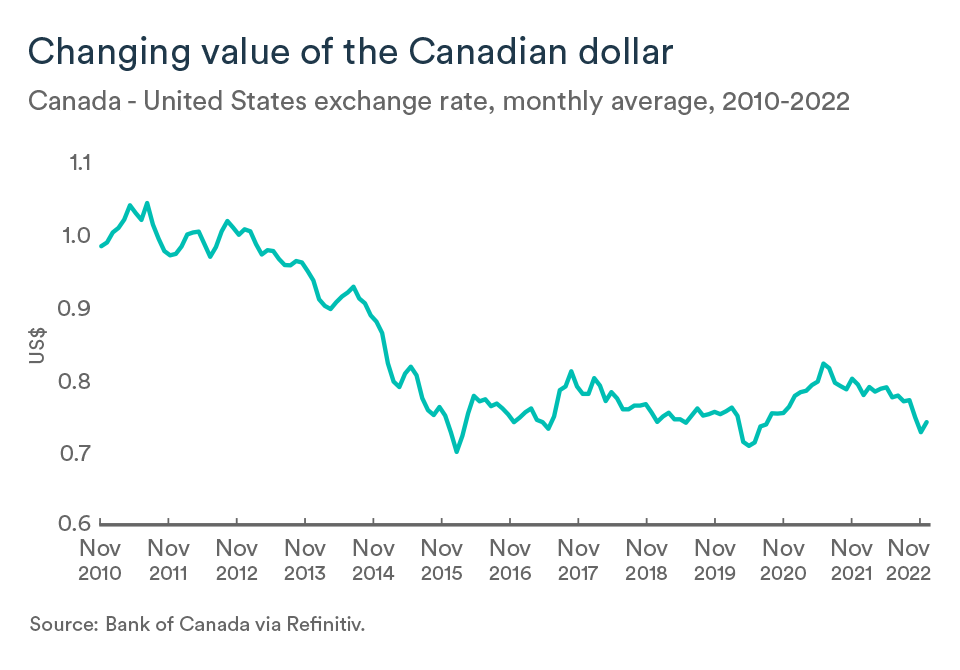

Canadian dollar rises near US$0.75

The Canadian currency had fallen to US$0.72 in October, a significant drop from its annual average. More recently, the loonie has regained some ground and is holding just below US$0.75. Lower oil prices and uncertainty surrounding a global recession are still weighing on the currency market, which will keep the Canadian dollar relatively weak against its U.S. counterpart as we head into the new year.

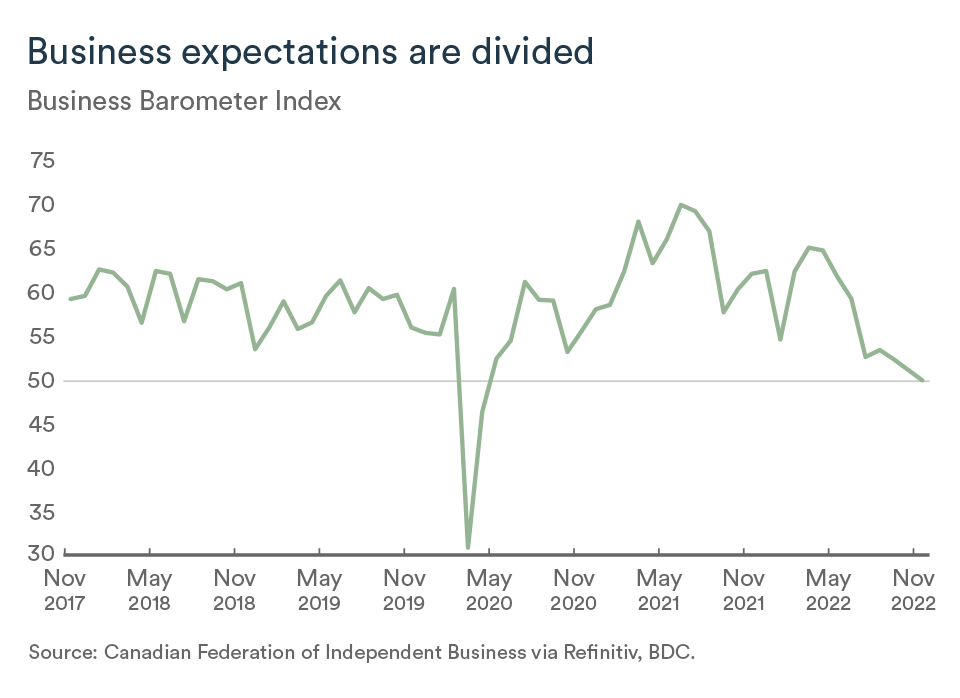

Business confidence is deteriorating

In November, the CFIB's business confidence index for the coming year dropped a few more points. Since the sharp drop that began in May, the index has been deteriorating a little more each month and stood at 50 in November. An indicator of 50 indicates that there are as many business managers expecting the business environment to worsen as those expecting it to improve over the next 12 months. However, the shorter-term indicator (next three months) dropped to 43.8 and clearly shows that the first quarter of 2023 will be critical for many small business owners.