Revolutionize your business model with a digital plan

Embracing digital technology and a digital culture, with a focus on your customers, processes, technology, and data-driven thinking, allows you to:

- leverage and enrich your corporate intelligence

- predict trends

- streamline operations

- reduce costs

- innovate your products and services

- generate new revenue streams

“Digital goes beyond adopting technology or optimizing operations. It's about reimagining your business model to explore how data, technologies and processes can revolutionize how you create value,” says Rene Vargas, Senior Business Advisor and Business Model Innovation Lead at BDC Advisory Services.

Businesses that fail to evolve and embrace digital risk falling behind their competitors—or worse, disappear altogether, Vargas warns. “It’s a question of embracing change, innovating, and staying relevant. A digital plan can help you stay competitive and can transform businesses, no matter how large they are or what sector they’re in.”

You can take your company to a new level by building a culture of creativity.

Rene Vargas

Senior Business Advisor and Business Model Innovation Lead, BDC Advisory Services

What is digital technology?

Digital technology encompasses all tools and processes that enable the creation, collection, management and use of data. These tools can be customer-facing, such as:

- e-commerce sites

- mobile point of sale (mPOS)

- social media

- digital signage

- digital kiosks

- online banking

- multimedia displays

- mobile apps

- portals

- surveys

- search engines

- chat boxes

- smart wearables

- medical devices

They can also be technologies that improve your operations, such as:

- enterprise resource planning (ERP) systems

- Web content management (WCM) systems

- transportation management systems (TMS)

- smart factories

- Industry 4.0 technologies

In addition, digital tools include:

- cloud-based applications

- artificial intelligence

- analytics

- data storage solutions

- sensors

- robots

- industrial Internet of things (IIoT)

3 steps to transform your business model with digital technology

“By following these three steps, you can leverage digital technology to stay ahead of the competition, drive innovation and growth, and take your business to new heights,” explains Vargas.

1. Plan your digital technology investments

To transform your business model with digital technology, the first step is to strategically plan your digital technology investments using a digital strategy or digital roadmap. This involves taking a 360-degree view of your enterprise by sitting down with key employees to review your business goals and strategic plan.

“It is crucial to document and understand your business objectives to prioritize your digital investments,” says Vargas.

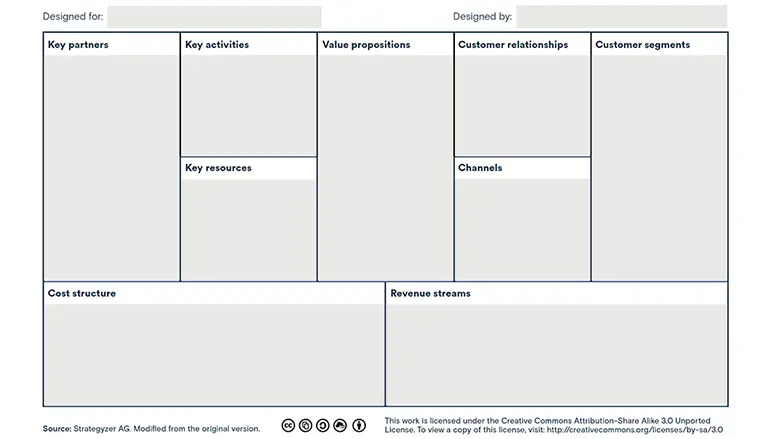

You can use the business model canvas to identify the nine essential components of your business model. It is a commonly used tool to break down and visualize the profit mechanism and how revenue comes into the company. It is a simple one-page chart that depicts your business model using nine essential components:

- key partners

- key activities or operations

- key resources

- value propositions

- cost structure

- customer relationships

- channels

- customer segments

- revenue streams

Business model canvas

You can download a business model canvas here.

For each of the nine components, review your current digital capabilities with your team. Then discuss and explore how you can leverage technology, processes and data in these areas:

- key goals and bottlenecks you could address with data, processes and technology

- important technology trends that employees and stakeholders see happening in the industry

- what you’re hearing from competitors, start-ups (new players), customers and partners

- new must-have and nice-to-have tools, the return for each and how they’d change your business model over the next several years

- your corporate culture and the decision-making process to enable digital and innovation

- customer interactions, expectations and journeys, including the systems, processes and data being used and exchanged

- where is your competition, who they are, where they are going, how they are innovating

Ask yourself if making new digital investments could help you:

- deepen your relationship with your clients and partners

- become a data-driven company and improve the decision-making process

- introduce a culture of innovation and change

- use resources more efficiently to improve the supply chain

- increase product and service value to your customers

- make operations more efficient and productive

- achieve your business objectives

- be agile in the event of market changes

- make your company more attractive to employees and future investors

“It's important to ideate and discuss how your data, processes and new technologies can help you achieve your strategic goals and allow you to innovate,” says Vargas.

Evaluate how your products or services can be enhanced using data and digital technologies. Consider what unique benefits your business can offer your target audience that your competitors cannot.

2. Adopt digital technology with a strategic approach

The second step is to prioritize your projects and select initiatives with the best potential return. You can use tools like pareto analysis to identify the projects that will have the greatest impact on your business. Consider developing different scenarios with various combinations of projects to determine the ones with the best probability of success. Ensure that you align every opportunity with your strategic objectives.

It’s important not to wait. You can test new processes or systems on a small scale, in small batches or with a lab-like approach.

Rene Vargas

Senior Business Advisor and Business Model Innovation Lead, BDC Advisory Services

Identify inefficiencies in your current operations and explore how data, processes and digital technologies can streamline and automate them. This could include automating repetitive tasks with artificial intelligence or machine learning, such as invoice processing or the quotation process, or automating inventory management.

Finally, don't wait to implement your new processes or systems. Start by testing them on a small scale, in small batches, or with a lab-like approach. This will enable you to identify any issues or challenges early on and make necessary adjustments before scaling up.

You can follow these steps to avoid making mistakes while preparing for a major tech purchase:

- establish a project team or a steering committee with success indicators and accountability

- conduct a functional requirements analysis to determine what features and capabilities you need

- develop a vendor list and rate each solution based on its features, benefits and total cost

- be wary of hidden expenses and implementation challenges that could derail your plans

3. Transform and innovate through digital

Moving forward with digital transformation is more than just purchasing a new system. It's about transforming your entire business model by leveraging data, processes and people. To truly transform your business, you need to cultivate a culture of innovation and creativity. Encourage employees to leverage data and share their ideas, experiment with new digital tools and processes, and embrace a growth mindset. Don't be afraid to test things on a small scale and learn from your mistakes.

Observe and adjust as you go, ramping up your efforts when they show signs of success. Innovation relies heavily on not being afraid to make mistakes and embracing slip-ups as part of your learning curve.

“Rather than following what other companies are doing, build a culture of creativity and innovation that leverages digital to transform your business model. By doing so, you can take your company to a new level and stay ahead of the competition,” says Vargas.