Are Canadian businesses reshoring their production?

Reshoring is a hot topic in the business news these days. This is the trend of North American manufacturing companies returning production back home from offshore locations.

It’s a reversal of the long-standing phenomenon of offshoring, in which manufacturing has been moving out of the country to lower-cost areas, such as China and the ASEAN region.

A lot of talk surrounding reshoring appears to be motivated by recent supply chain disruptions due to the pandemic.

There are also signs that the cost advantage of offshore locations could be declining. Labour costs are rising quickly in China, for instance, while they’ve remained stagnant in the U.S. Other drivers of reshoring include:

- lower energy prices in the U.S.

- rising shipping costs

- lack of intellectual property rights in China

- protectionism and trade disputes

First Canadian data on reshoring

But how commonplace is reshoring, particularly in Canada? It’s an important question because the answers help Canadians understand and be ready for secular shifts in the global economy and future trends.

Until now, however, solid data has been scarce. It’s often hard to tell why a company has decided to relocate production. The pandemic has further confused the picture and whipsawed historic trends.

To fill the data gap, BDC asked Deloitte Economic Advisory to study reshoring. Deloitte’s report provides the first data on the phenomenon in Canada and sheds light on specific industries.

To determine whether reshoring was happening, the report looked at three indicators:

- the ratio of imports to domestic production

- domestic production

- investments in the industry

If production and investment in Canada are rising, and the ratio of imports to domestic production is falling, that is strong evidence for reshoring. The contrary would be evidence of offshoring.

Trend weaker here than in U.S.

Deloitte’s conclusion: Some reshoring does appear to be occurring in a few Canadian sectors, but the trend isn’t as strong here as in the U.S.

South of the border, an estimated 628,000 manufacturing jobs were reshored from 2010 to 2019, according to a study by the Reshoring Initiative. That figure represented 44% of the total 1.4 million gain in U.S. manufacturing jobs during the same period.

Comparable employment impacts aren’t available for Canada. But the report did find that the bulk of Canadian manufacturing industries are headed in the opposite direction: They remain in a long-term trend of imports outpacing domestic production, as opposed to reshoring.

Imports outpacing domestic production

The report finds that the ratio of imports to domestic production has been increasing across most manufacturing industries over the last decade. If reshoring of manufacturing capacity back to Canada is occurring, a reversal or at least some slowing in this trend would be expected.

However, in most industries, there are few signs of reshoring. Production has generally been slow to recover after large declines in output during the recession of 2008-09. On the other hand, imports have generally fared better as imports rebounded relatively quickly after the 2008-09 recession.

Why isn’t Canada experiencing the same level of reshoring as the U.S.? The chief culprits seem to be Canada's stagnant industrial production and lagging productivity.

Machinery manufacturing is reshoring bright spot

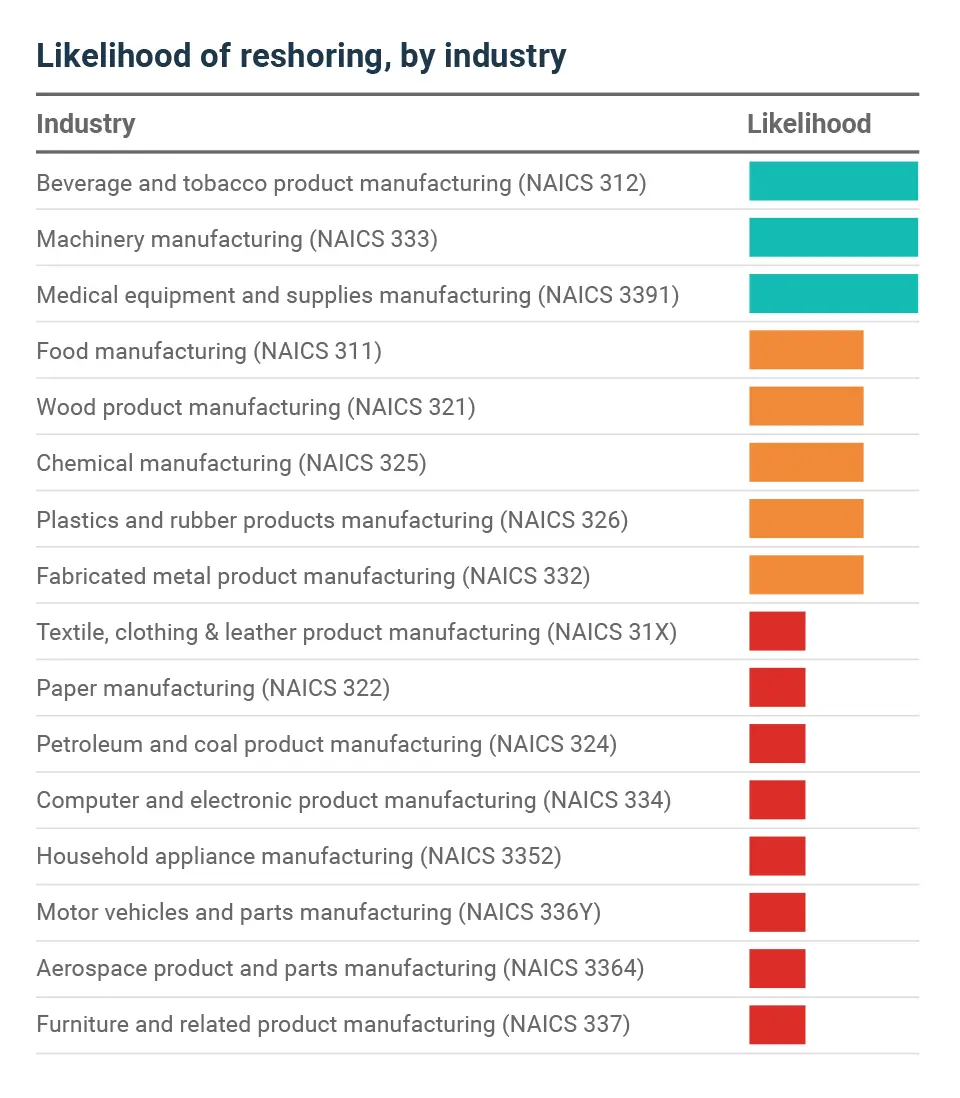

Only three of 16 Canadian industries examined show strong evidence of reshoring:

- machinery manufacturing

- medical equipment and supplies manufacturing

- beverage and tobacco product manufacturing

In all three of these industries, the ratio of imports to domestic production is steadily declining, while output and investment are rising strongly. Together these factors are solid evidence of reshoring.

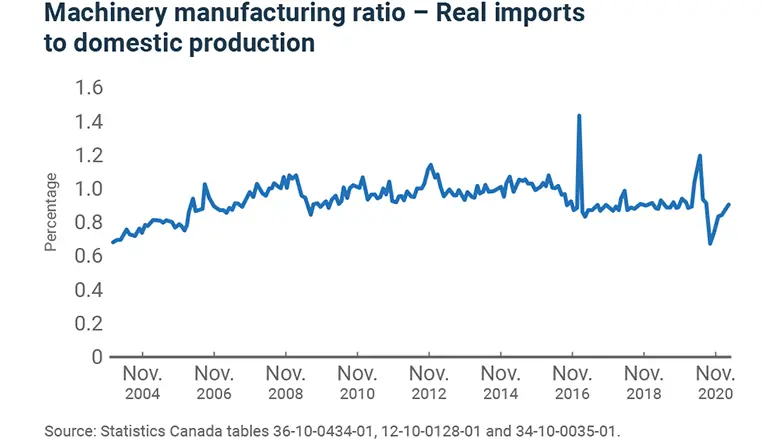

Machinery manufacturing, for example, is a Canadian reshoring poster boy. The ratio of imports to domestic production has declined since 2010, while production, investment and employment have all steadily gone up.

Another bright spot is medical equipment manufacturing. The sector’s strength started long before the pandemic. It has experienced growth for the past 20 years, including especially rapid expansion since 2015. The ratio of imports to domestic production has been declining since 2014.

Food and wood products see “modest” reshoring

A few manufacturing industries show what the report calls a “modest likelihood of reshoring”:

- food

- wood products

- chemical manufacturing

- plastics and rubber products

- fabricated metal products

These industries have seen slight declines in imports vs domestic production ratios and/or moderate output and investment gains.

Food production, for one, has seen years of steady growth in domestic production, boosted by Canadian trade deals with the European Union and Pacific Rim countries. The industry saw a decline in the import-to-domestic production ratio from 2016 to 2018, but the ratio then reversed course and has fluctuated significantly during the pandemic.

Wood product manufacturing also presents an unclear picture. Reshoring appears to have occurred in the 2010-2016 period, but the trend reversed in 2017. Imports then started to decline again during the pandemic, but investment has been stagnant and is forecast to remain so in 2021.

Few supply chain impacts seen

Deloitte also studied impacts of reshoring on North American supply chains. If U.S. supply chains are reshoring, how is this impacting Canadian imports? Is Canada turning more to the U.S. for imports as opposed to China and the ASEAN region?

The report found little evidence of such a phenomenon in most industries. Of 16 industries, only two—beverage and tobacco products, and petroleum and coal products—showed strong evidence of both increased U.S. imports and declining imports from China and the ASEAN region.

One other industry—motor vehicles and parts—did show evidence of a parallel phenomenon called “nearshoring.” This is the trend of bringing production closer home to a nearby country, such as Mexico.

Canada’s motor vehicles and parts industry doesn’t show any evidence of reshoring, as the ratio of imports has steadily gone up for years versus domestic production. But Canada is increasingly getting those imports from Mexico, while imports from the U.S. show no clear trend. This is a sign of nearshoring.

Future of reshoring unclear

Much about the future of reshoring in Canada remains uncertain. Some factors behind the trend may be transitory, such as lower U.S. energy costs. The pandemic’s still-unclear impacts on the economy further cloud the picture. But other drivers will likely keep providing a tailwind for reshoring, namely increasing wages and lower productivity growth in developing countries.

Close attention is warranted to monitor the trends of both reshoring and offshoring in Canadian manufacturing, especially as the impacts of the pandemic and other shifts in the economic landscape become clearer.