Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreWhere are interest rates headed?

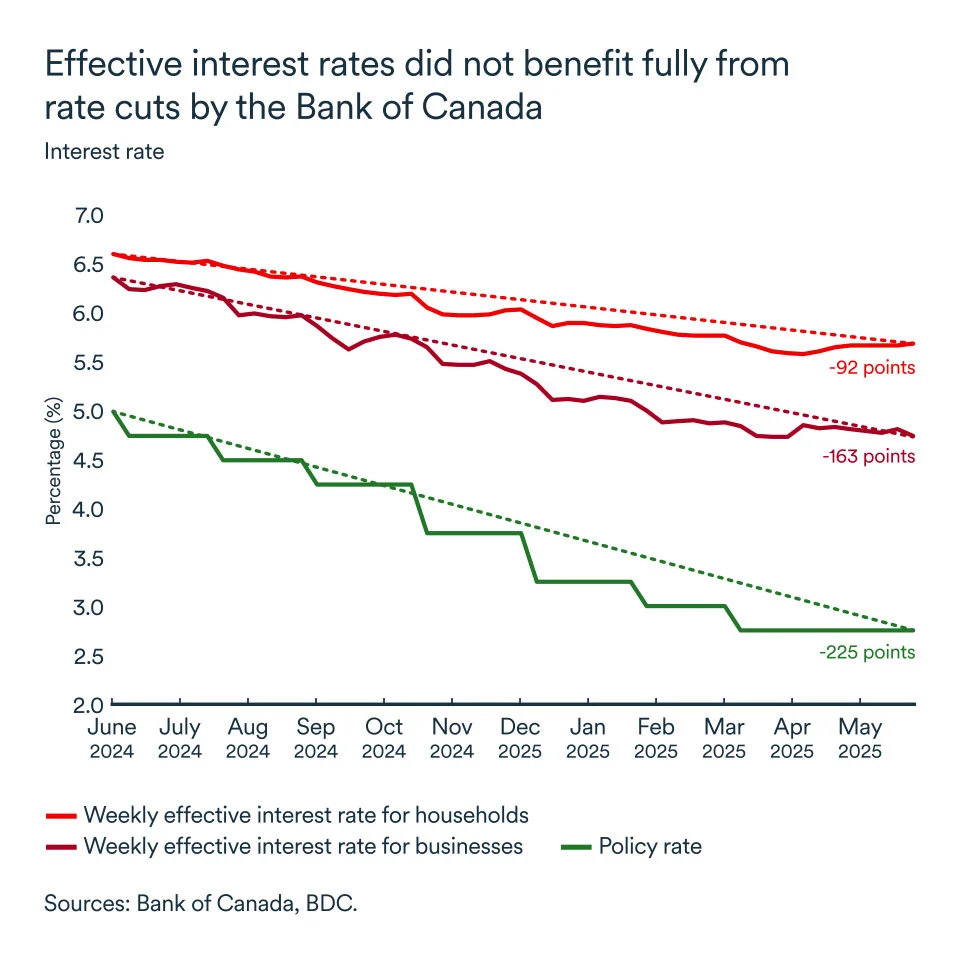

Over the past year, the Bank of Canada has lowered its key interest rate by 2.25% in an effort to bring down borrowing costs and stimulate the economy. But even as the bank’s rate dropped from 5.0% to 2.75%, interest rates for consumers and businesses have remained stubbornly high.

For households, rates have fallen by less than 1%, while for businesses, the drop has been a little greater at 1.63%.

Why haven’t they fallen further? It’s because rates for longer-term loans for such things as mortgages and car purchases are mostly influenced by what’s happening in the gigantic bond market.

Interest rates for bonds—their yield—are decided by investors and they don't just look at what central banks are doing. They also observe the state of the economy, future risks and the inflation outlook.

This has meant, for example, that the rate for a five-year fixed mortgage rate in Canada has fallen by just .75% over the past year and has actually risen in recent weeks, despite the Bank of Canada’s rate cuts.

U.S. rates lead Canadian rates

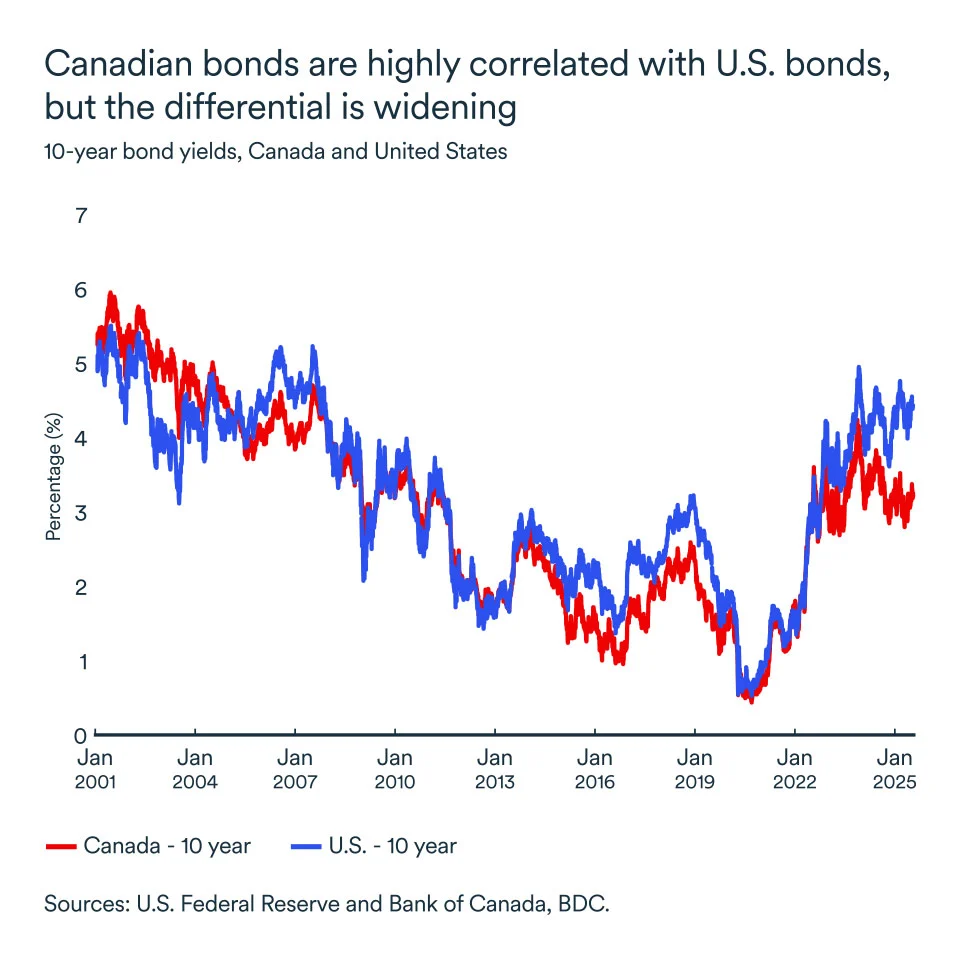

To understand where Canadian interest rates are headed, we need to look at what's happening in the United States.

U.S. rates have a major influence on Canadian ones, since international investors are constantly comparing bond yields in the two countries. If U.S. bonds offer a higher yield, capital will leave Canada, forcing Canadian rates to adjust upwards to remain competitive.

Recently, U.S. bond yields have started to rise again due to a number of concerns, including persistently high inflation, a large and potentially growing federal budget deficit and an economy that remains surprisingly robust. Taken together, these factors have led investors to seek a better return on their bond holdings.

High interest rates reflect a tense climate

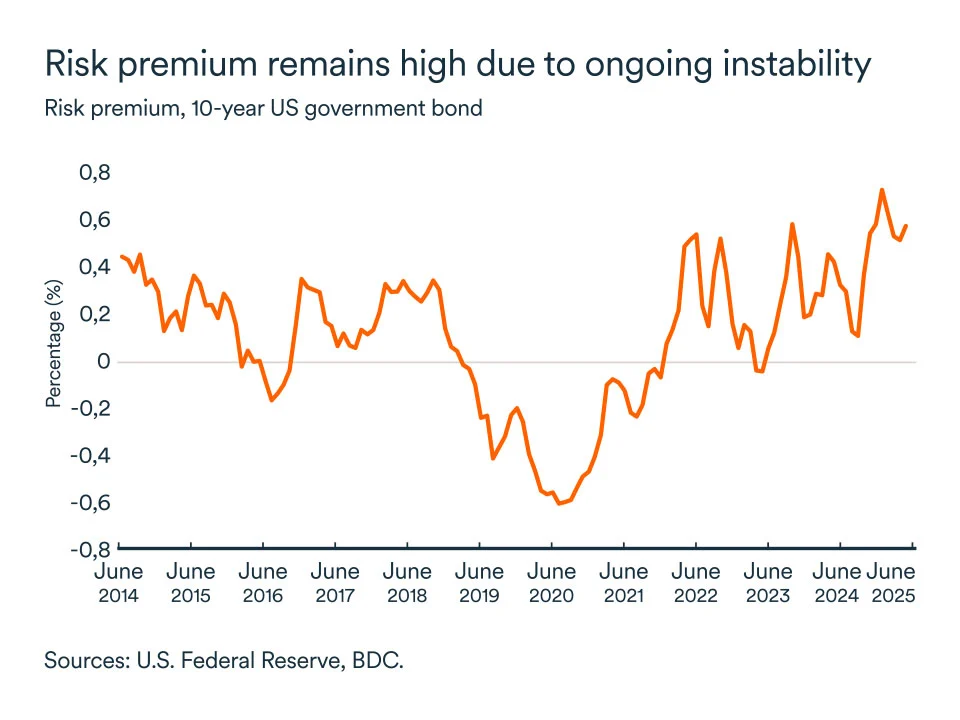

What’s more, something surprising is happening in the U.S. bond market. Normally, when investors sense uncertainty in the economy, they look for safe havens, including U.S. bonds. This pushes up bond prices and pushes down yields (since the two move inversely).

But right now, the opposite is happening. Despite heightened uncertainty, yields are rising.

Instead of rushing into U.S. bonds for safety, investors are demanding a higher risk premium on those investments. In other words, they want to be paid more for lending their money in an unstable environment. In fact, the premium has reached a 10-year high. This dynamic can be explained by three factors:

- As trade tensions intensify around the world, bond yields have started to rise, especially in the U.S. As well, Inflation concerns are putting upward pressure on interest rates in response to the U.S. economy’s continued strong performance.

- Foreign central banks are diversifying their reserves away from the U.S. dollar and investors are reducing their exposure to the U.S. economy.

- To finance its large deficit, the U.S. government has had to issue more debt. To convince investors to buy this debt, it has to offer higher interest rates.

It all points to one conclusion. Interest rates in the United States are likely to remain high for some time to come.

What is the impact on Canadian businesses?

Canadian markets generally move in tandem with U.S. markets. So, credit conditions in Canada could tighten and interest rates for longer-term loans could rise (or at least remain high). If you have investment projects to finance in the coming months, you might want to lock in your rate soon.

However, the gap between the Bank of Canada’s key rate and effective rates in the bond market seems to be more pronounced for household loans than for business financing. While that’s positive news for businesses seeking financing, it also means tighter credit conditions for households. This could hurt demand for products and services for businesses that serve a consumer market.

Much of what drives bond yields is investor expectations. Over time, trade tensions may ease or investors may get used to living with the discomfort of trade conflict. If this is the case, the risk premium built into current interest rates could decline, providing relief to borrowers.

Nevertheless, patience will be required. It would be surprising to see interest rates fall significantly before 2026.

Is Canada on the verge of a recession?

Canadian entrepreneurs have their eye on several economic indicators that are flashing yellow about the potential for a recession this year. A slowdown in economic growth, rising unemployment and a number of ailing sectors are all worrisome signs. However, we still expect Canada to avoid a recession in 2025.

Canada is not currently in a recession and our forecast calls for modest growth of 0.8% for the year. But the risk of one or two quarters of declining GDP remains.

Growth surprises to the upside in Q1

Although many consumers and businesses might have the impression the economy is already in recession, recent data has shown unexpectedly strong growth.

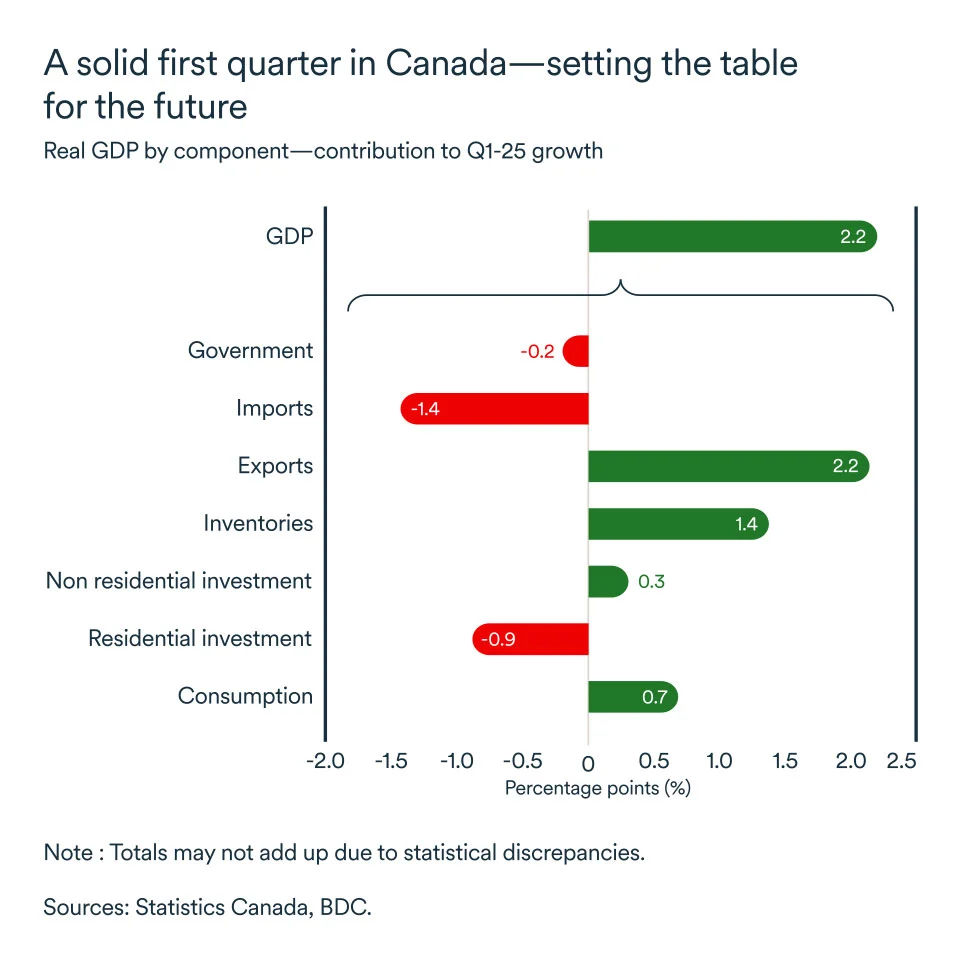

Canadian real GDP grew at a rate of 2.2% in the first quarter. It would be surprising, however, to see this strength continue in the balance of the year as trade conflict takes an ever greater toll on the economy.

Consumption and business investment, key pillars of economic growth, were positive in the first quarter, contributing 0.7 and 0.3 percentage points to GDP, respectively. But this was a subpar performance as uncertainty prompted many businesses and consumers to remain cautious.

Non-residential investment had regained some momentum at the end of 2024, thanks to interest rate cuts, but is once again suffering in the current economic climate.

Rising inventories and exports: Ominous signals

The uncertainty surrounding U.S. trade actions led to higher inventories, imports and exports as businesses and consumers rushed to get ahead of the imposition of tariffs on both sides of the border. It’s unlikely the economy will benefit from a similar boost in the coming months.

In fact, Canadian exports to the U.S. have already slowed significantly—falling by over 15% in April. By contrast, exports to the rest of the world rose by 2.9%, but this wasn’t enough to maintain overall trade growth.

The increase in business inventories is likely to come up against slower demand and this could be another drag on the economy this year.

Bank of Canada maintains key interest rate

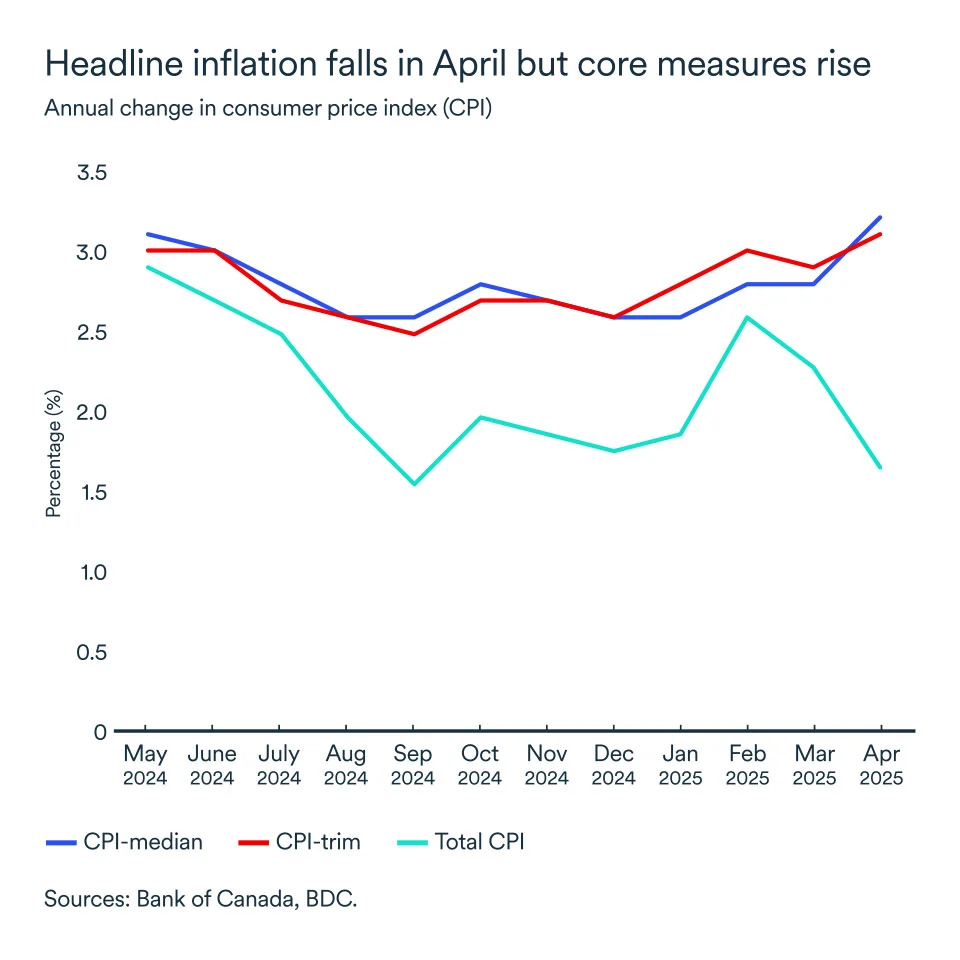

The Bank of Canada maintained its key rate at 2.75% in its June 4 announcement. Headline inflation, as measured by the annual change in the consumer price index, slowed to 1.7% in April. But core inflation measures, which the Bank of Canada favours, picked up again, all exceeding 3%.

At this stage, the key interest rate is within the so-called "neutral" range. A rate between 2.25% and 3.25% corresponds to a monetary policy that allows the economy to run smoothly—neither too fast, nor too slow.

However, the economic slowdown that is underway could prompt the bank to cut its rate further, especially if it judges that inflation resulting from tariffs will be temporary.

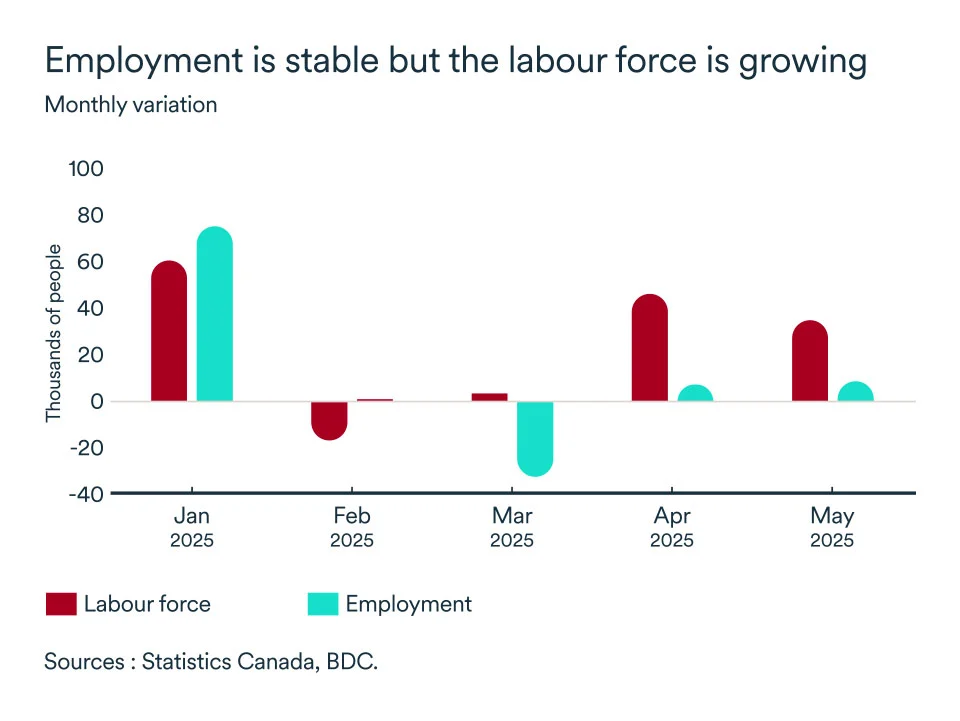

Unemployment rate rises

The country's unemployment rate increased again in May. Despite positive job gains during the month, the labour force—the number of people available and ready to work—grew by a much larger margin. (+35,300 available workers versus 9,000 jobs created.)

In a positive sign for the economy, private sector employment rose for the first time since January, jumping by almost 61,000 positions. Layoffs were stable compared with the same period last year.

There were job losses in sectors that are more vulnerable to tariffs, such as manufacturing (-12,200), construction (-7,400) and transport and warehousing (-15,500).

The impact on your business

- Trade negotiations with Washington are continuing and the situation is evolving by the day. Until an agreement is reached, consumers will remain cautious and companies will continue to want to reduce the inventories accumulated in Q1.

- In the face of trade uncertainty, the Bank of Canada is being patient in making further rate cuts, despite a slower economy. It's still a good time to review your investment projects and develop your growth plans.

- The economic slowdown is concentrated in certain sectors, particularly those affected by U.S. tariffs and Canadian retaliatory levies. If your company operates in these sectors, or if your supply chains are impacted, BDC can help you stay on track.

- Even if you’re not directly affected by trade turbulence, it's worth assessing how your company needs to adapt to a wider slowdown in the economy. While we expect slower growth ahead, we’re not forecasting a recession at this stage.

Ontario’s economy bears the brunt of trade tension

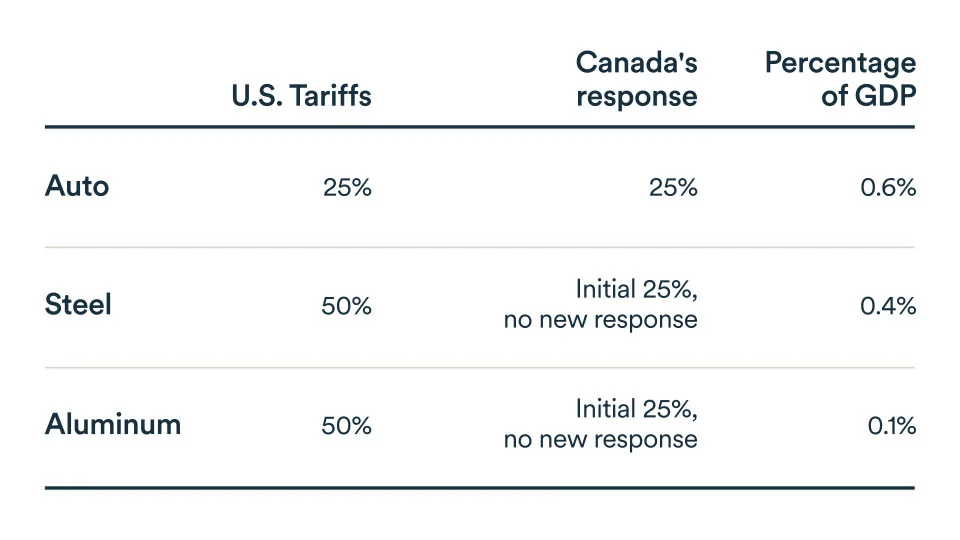

So far, the U.S. has backtracked on its intention to impose sweeping tariffs on all Canadians goods but gone ahead with duties on the auto, steel and aluminum industries.

While Canada seems to have avoided the worse case scenario of across-the-board tariffs, the sectoral ones have hit Ontario the hardest among the provinces.

While autos, aluminum and steel account for a little over 1% of Ontario’s GDP, they represent around a third of the province's exports. As a result, southern Ontario, where these industries are concentrated, will experience a significant slowdown this year, while other regions of the province should see modest growth.

Overall, given the high level of economic uncertainty and the disproportionate effect of U.S. protectionism on the province, we expect Ontario’s growth to be a weak 0.6% this year.

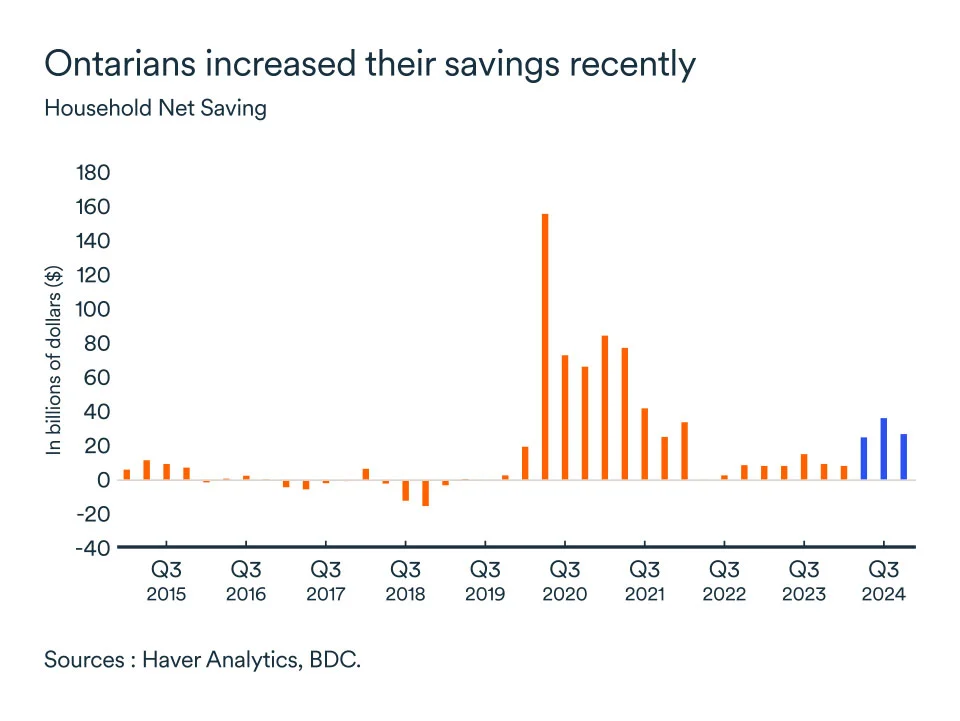

Job market weakens, but households have rebuilt their savings

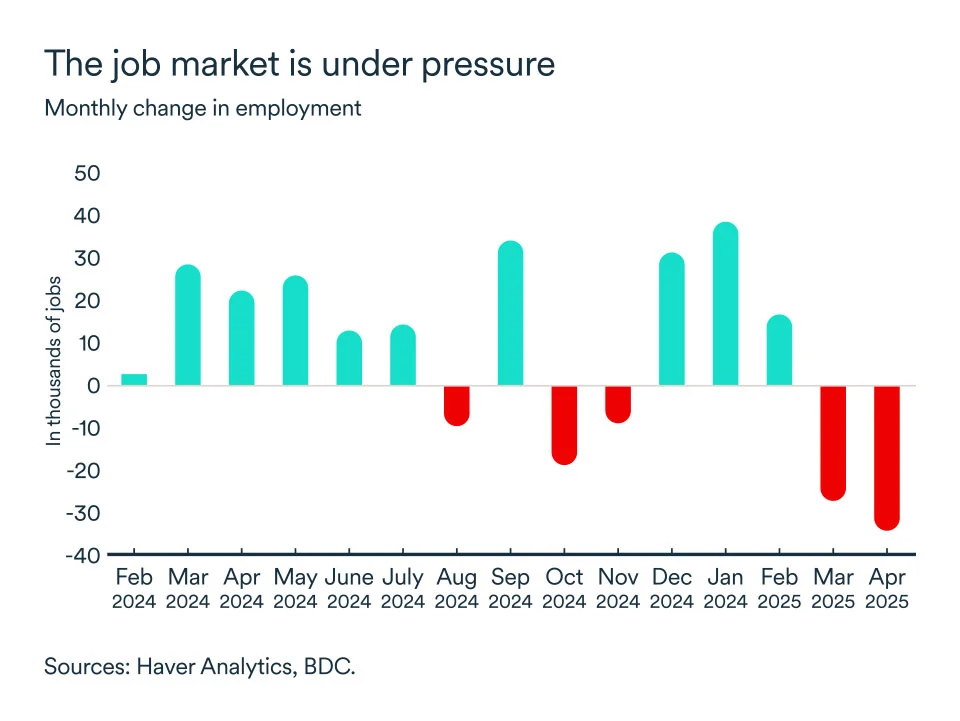

Businesses in Ontario are feeling the heat of tariffs and uncertainty. Hiring in the targeted sectors fell significantly in recent months with employment in manufacturing declining for three consecutive months since March.

Sectors indirectly affected by the tariffs, such as construction and accommodation and food services, have also experienced job losses. Although the overall unemployment rate in Ontario was little changed in May, variations in regional unemployment were substantial. For example, the unemployment rate in Windsor increased at a significantly faster pace (+1.5) than in Toronto (+0.3) over the past two months.

As long as trade talks continue between Canada and the U.S. without agreement, the job market is expected to remain under pressure, weighing on the confidence of Ontario consumers.

Households are expected to remain cautious with their spending and continue to increase their savings ahead of mortgage renewals and in response to the continued uncertainty.

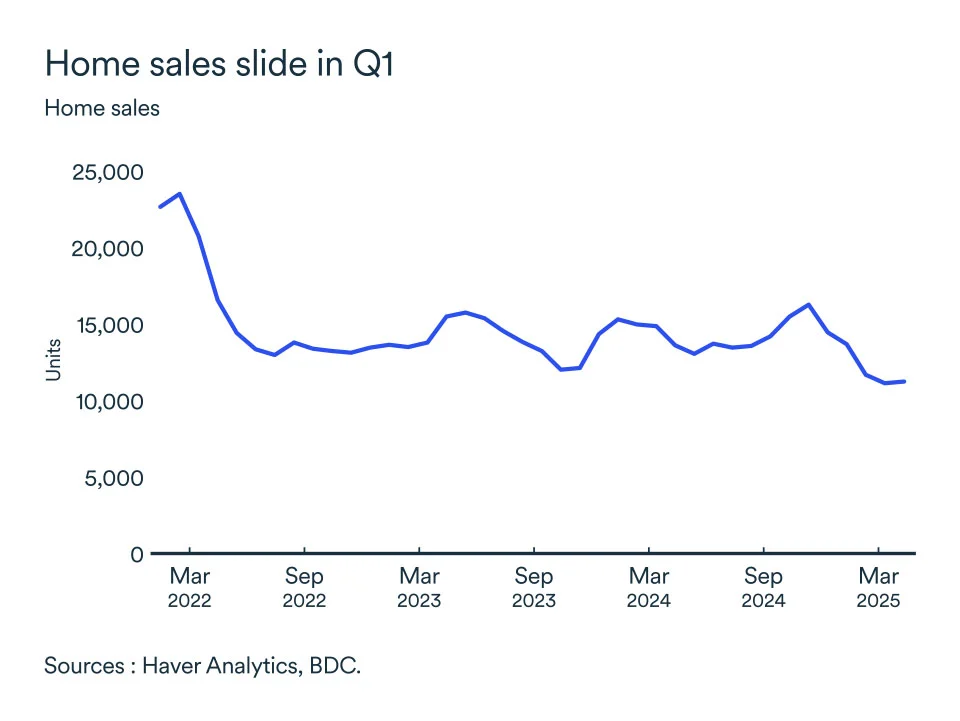

Housing market recovery cut short by trade tension

The housing market quickly deteriorated as trade tension escalated this year. Home sales declined by 21% in the first quarter 2025.

Despite lower interest rates, households remained cautious due to declining confidence in the economic outlook and concerns about job security. April saw lack-lustre home sales as economic uncertainty likely deterred potential buyers.

Growth to continue this year but with downside risks

After rising sharply in the first quarter, automotive exports fell significantly in April, as the province's automakers reduced production capacity in response to the tariffs. Exports will remain under pressure in the months ahead. Continued tariffs are likely to lead to further cuts in production by Ontario automakers, further weighing on growth.

However, the budgetary measures announced by the government will provide support to affected industries and households. The infrastructure investments planned for 2025-2026 will also stimulate the economy and pave the way for a revival in interprovincial trade.

Overall, Ontario is facing a challenging year, but as uncertainty subsides and a deal is negotiated, business and consumer confidence will slowly recover, leading to a stabilization of the job market, real estate activity and exports.

The impact on your business

- Pricing can have a significant impact on your business, depending on your industry. There are tools that can help you deal with this situation.

- With credit conditions tighter than in previous quarters, it's important to assess your financial situation and position yourself favorably when applying for financing.