Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreYou’ve got questions. We have answers!

Many entrepreneurs are grappling with high levels of uncertainty in their business as we begin a new year. To help you gain some clarity on your most pressing concerns, this edition of the economic letter answers the top 10 questions BDC economists have been asked in recent months.

Q1. Are we heading for a recession?

Recessions are a normal part of the business cycle. A recession, in its most simplistic and widely used definition, is characterized by two consecutive quarters of declining real GDP. However, many economists, including BDC’s, prefer a less mechanical definition. We consider a widespread and significant decline in both GDP and employment to gauge whether a recession has occurred.

Our current analysis indicates the Canadian economy should experience a marked slowdown this year, but avoid a recession. However, the risk of the economy slipping into a mild recession has increased in recent months.

Q2. Should we be concerned about household finances?

Consumer spending is a key driver of economic growth and rising interest rates are causing Canadian consumers to become increasingly cautious. While household borrowing continued to increase in the latter part of 2022, the pace slowed to its lowest level since the pandemic. The ratio of household debt to disposable income rose slightly.

On the other hand, the job market and wage growth remain strong, even as spending has slowed. The result has been rapidly rising household disposable income and higher net savings.

So, it’s a mixed bag for households. Nevertheless, Canadians are facing the fastest increase in interest rates in decades (+29.6% annualized in the third quarter of 2022) and that will leave households increasingly vulnerable to financial setbacks as 2023 unfolds.

Q3. What can we expect from the Canadian housing market?

If there is one place where Canadians have seen the effects of the Bank of Canada's interest rate hikes, it’s the residential real estate market.

The volume of transactions in the resale market fell by 39% in November, compared to February 2022, just before rates began to rise. The decline in demand has also led to a significant correction in housing prices (-19%).

The number of transactions and the average price are expected to continue to fall in the first part of this year before stabilizing. We are already seeing lower effective interest rates in the government bond market, which should lead to a decline in mortgage rates. Moreover, immigration started to resume since the pandemic and shelters are still in short supply. According to CMHC, Canada still needs 3.5 million affordable housing units to be built by 2030 to help achieve housing affordability. Therefore, it wouldn’t be surprising to see the residential housing market regain some momentum by the end of 2023.

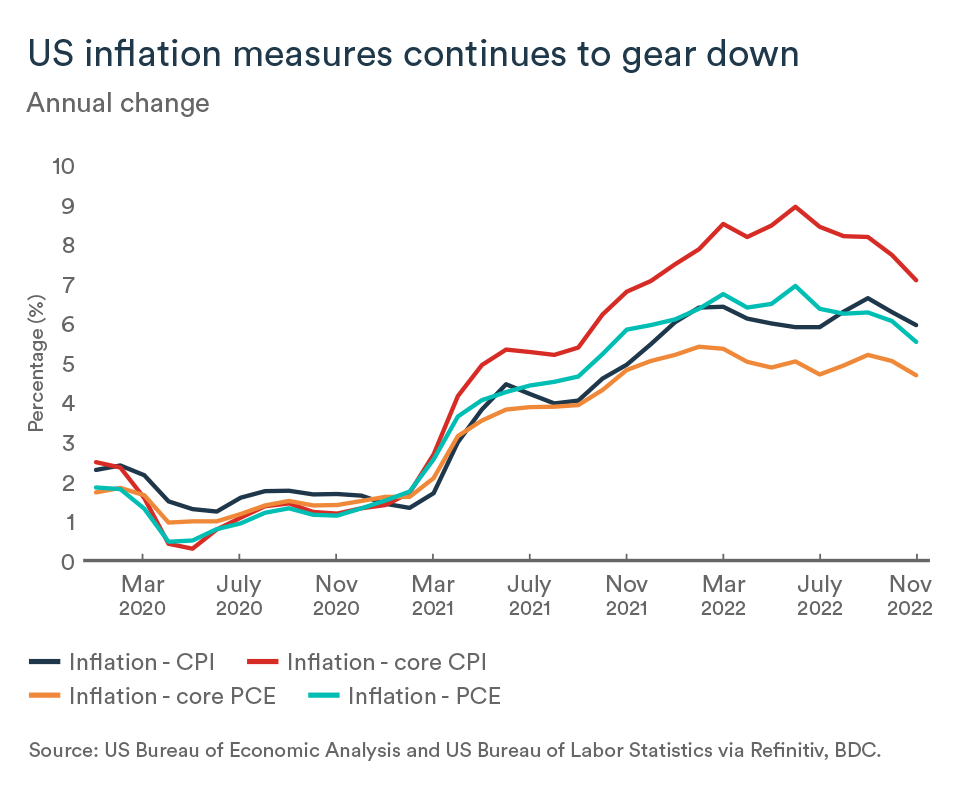

Q4. Is inflation out of control?

Much of the inflation seen in 2022 can be explained by global supply issues. The invasion of Ukraine and retaliatory sanctions against Russia pushed up commodity prices at a time when supply chains were still disrupted by pandemic-related issues.

After seven rate hikes by the Bank of Canada, there are signs inflation is moderating. However, it won’t be until the second half of the year that we will see inflation move closer to the bank’s 2% target range as higher rates bring domestic supply and demand back into balance.

Q5. Where are interest rates headed? Fixed or variable?

The Bank of Canada’s policy rate—the trendsetter for other interest rates—has risen from 0.25% to 4.25% in less than a year. We expect the rate to peak at 4.5% in the first quarter of 2023 and remain there for most of the year before starting to come down in the fourth quarter.

However, Canadians will need to be patient. We don’t expect to see the rate return to a neutral level of 2.5% for at least 18 months.

There are many factors to consider—not just rate direction expectations—when choosing between fixed and variable rate financing. There is no one-size-fits-all answer. The decision depends on the financing horizon, the structure and options of the loan, your ability to pay, anticipated changes in income and, of course, your appetite for risk.

Q6. What does this mean for the Canadian dollar?

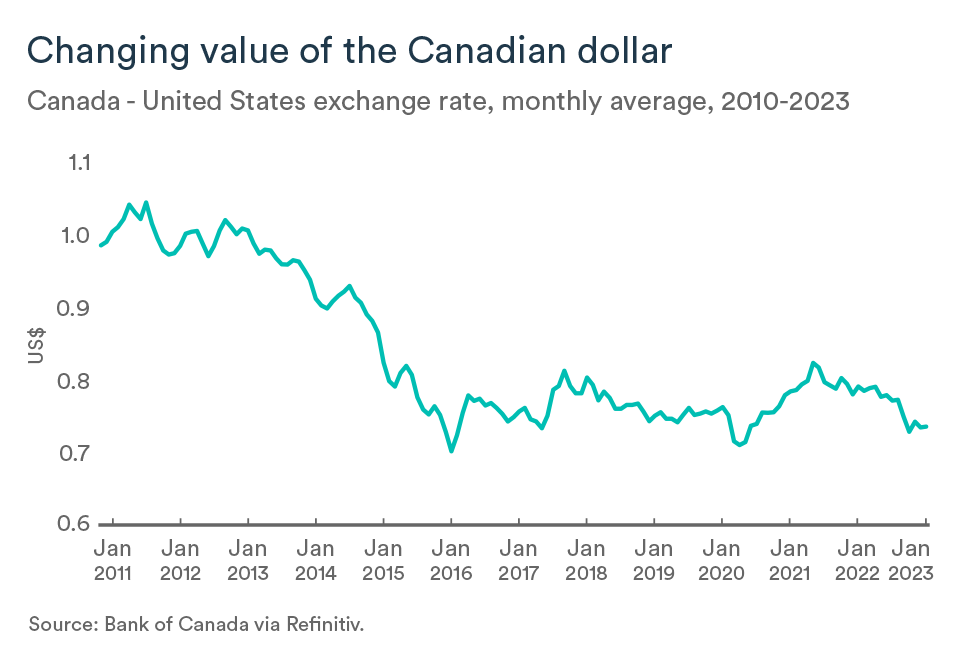

In the second half of 2022, the Canadian dollar fell versus the U.S. greenback as growing economic uncertainty took a toll. A slowdown in global demand and lower commodity prices contributed to the drop in the Canadian dollar to the current level of around US$0.74 and will continue to exert downward pressure on the loonie.

In addition to economic uncertainty and commodity prices, the short-term interest rate differential between the two countries is another factor to consider. As the cycle of interest rate hikes comes to an end in Canada, the U.S. is expected to maintain higher rates for longer. As a result, the short-term rate differential should widen, keeping the dollar weak (between US$0.72 and 0.75) in the coming months.

Q7. What are the international risks?

Economic forecasts for global growth are down sharply for 2023 and with good reason. On the one hand, inflation is a global problem, so rate tightening to contain it will weigh on growth around the world. The U.S. Federal Reserve is still not ready to end its tightening cycle, while Europe is being hit by a major energy crisis. In addition, the debt burdens of developing countries have become much heavier thanks to the strength of the U.S. dollar and rising interest rates.

A key international risk remains the economic and geopolitical situation in China. Now that the zero-COVID policy has finally been scrapped, the virus is spreading unchecked. That’s hurting the Chinese economy, which was already coping with the slump in the real estate market.

Q8. Will the prices of inputs, such as oil, continue to rise?

Many commodity prices have begun to descend in recent weeks as traders become increasingly concerned about the risk of a global recession. Price declines are likely to continue in the first quarter, as households and businesses remain cautious. Some markets, notably oil, are expected to be oversupplied in early 2023.

However, the gradual reopening of China and the end of rate hikes should give a lift to commodity markets by mid-year, leading to some price recovery.

Q9. Where are the workers I’m looking for?

In a typical economic downturn, layoffs increase. The 2023 downturn will prove different in this respect because job vacancies are still very high and retirements are at a peak. Unfortunately, Canada's labour shortages will countinue after the 2023 downturn is history. Canada's population is not getting any younger, despite significant immigration. Labour shortages were the reality before the pandemic and they will continue for many years to come.

Q10. What about wages?

Inflation, strong demand and labour shortages all contributed to robust wage growth in 2022 (+5.1% annual change in December 2022). Wages are expected to continue to rise in 2023 at a higher rate than before the pandemic, but we don’t expect the magnitude of recent increases to become the new norm.

The economic slowdown will provide some relief to businesses from wage pressures experienced in 2022 and inflation expectation should cool in the coming months. Nonetheless, wages are expected to rise by an average of 4% across the country this year.

Canada’s inflation fight proves difficult

The Canadian economy showed continuing strength early in the fourth quarter despite a series of interest rate hikes designed to cool inflation.

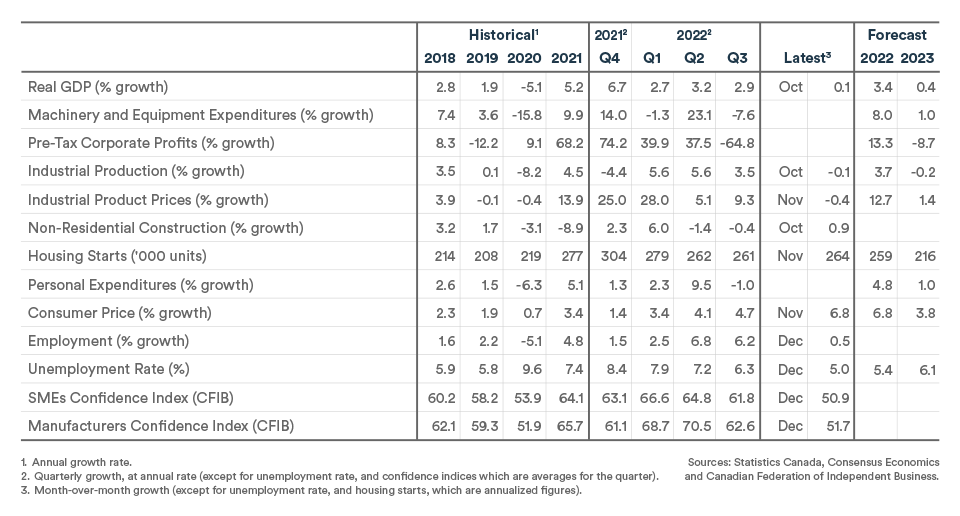

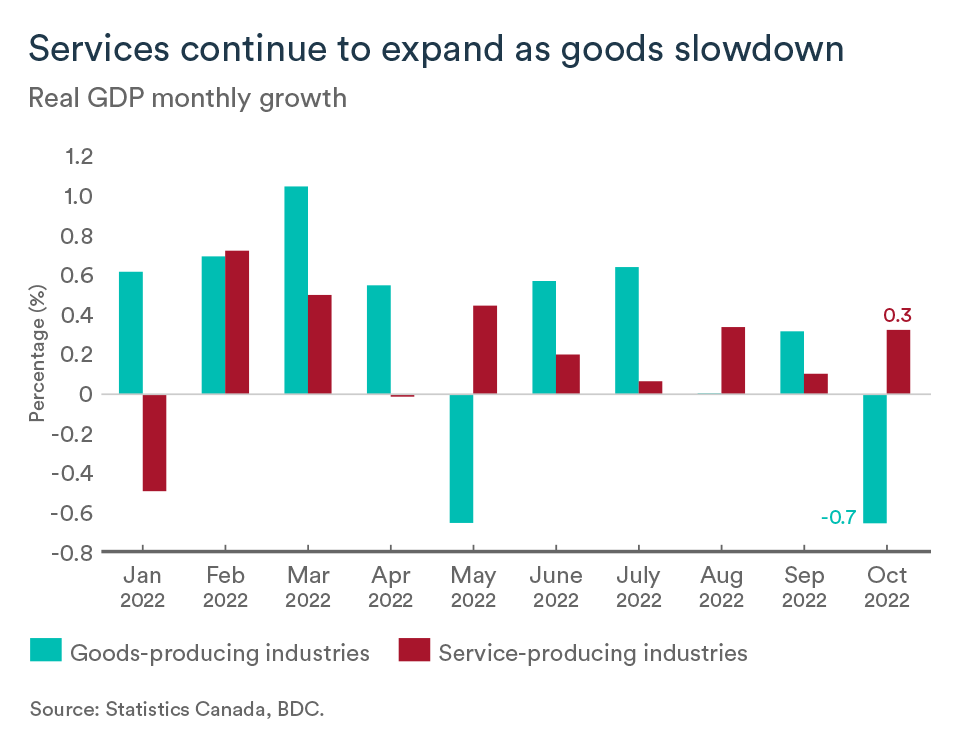

Real GDP increased by 0.1% in October compared to September. This meant the economy grew at a rate of 4.0% from January to October 2022 compared to the same period in 2021. According to Statistics Canada, preliminary information indicates that real GDP increased by another 0.1% in November.

The economy’s resilience can be mostly explained by the good performance of the services sector in October (+0.3%) while the goods sector recorded another decline (-0.7%).

Inflation persists despite Bank of Canada's efforts

All in all, growth seems to be holding up well in the face of successive interest rate hikes, at least for now. Remember, however, that it takes about 18 months for the full effect of an interest rate increase to be felt in the economy. Therefore, it’s a good bet the economy’s strong performance in 2022 will not continue in 2023.

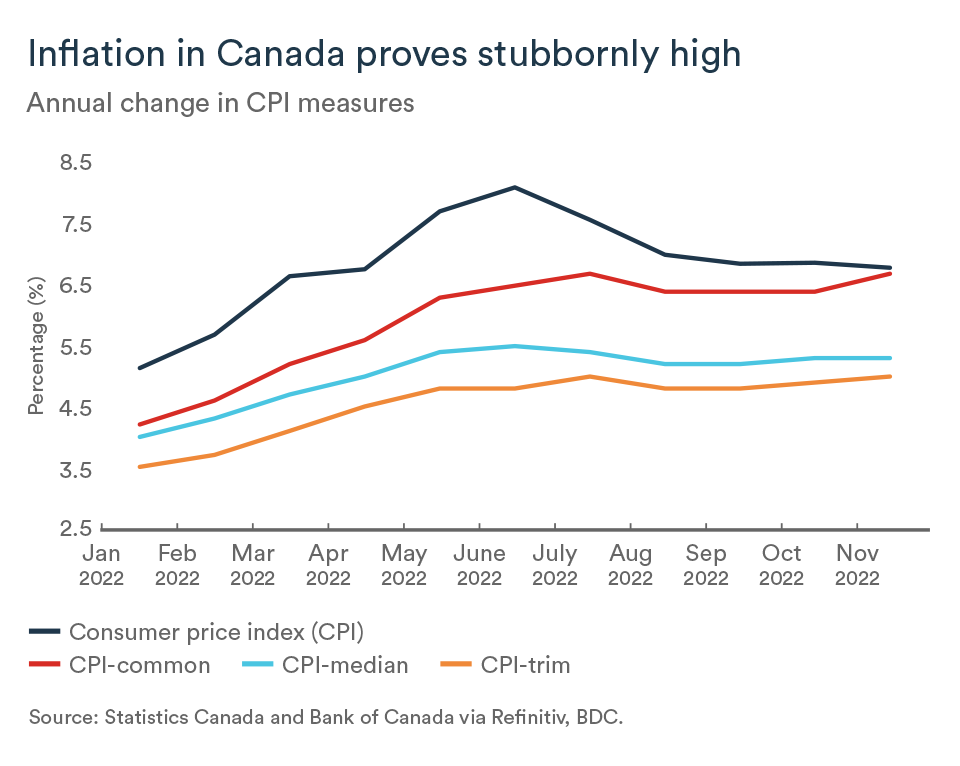

Indeed, notwithstanding the Bank of Canada's extraordinary efforts to keep inflation in check, more medicine will likely be needed. The increase in prices as measured by the annual change in the consumer price index (CPI) in November was 6.8%, just 10 basis points lower than in October.

Core inflation measures as well as short-term indicators (3-month annualized) that are favoured by the central bank were all pointing up in November. This reinforces our view that Governor Tiff Macklem will once again raise the bank’s policy rate at his next announcement on January 25.

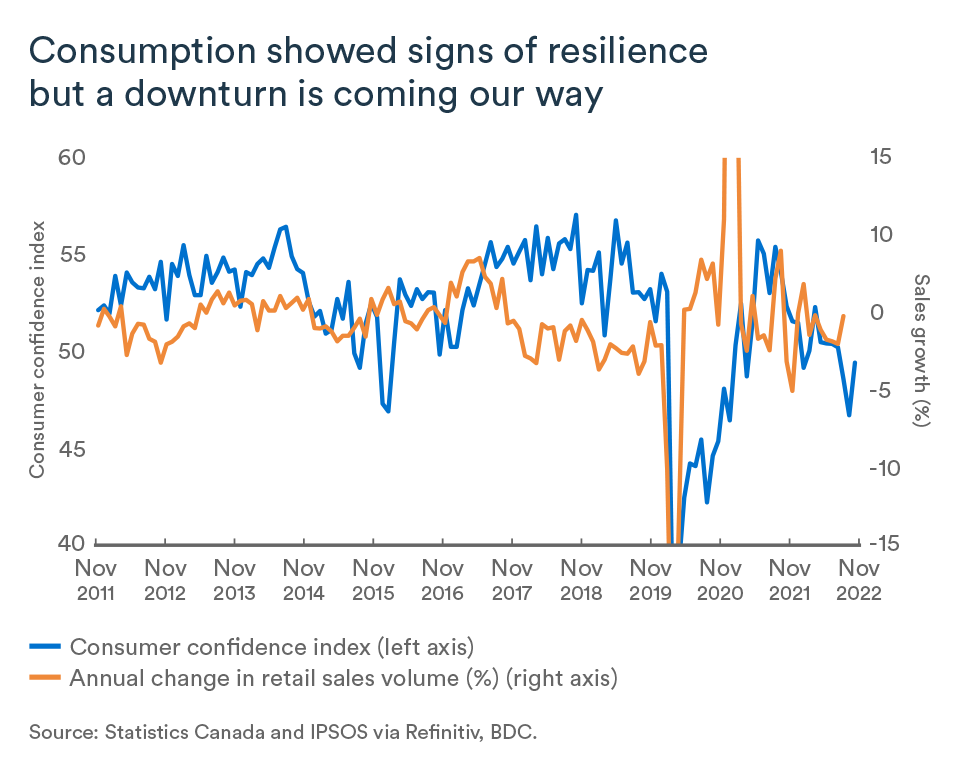

Consumption holds up

Manufacturing and retail sales volumes were flat in October. A return to normal holiday spending after two years of pandemic was likely why consumption held up better than expected in the fourth quarter, despite high inflation.

Motor vehicle sales declined again in October, but it was unclear whether this decrease was due to slowing demand in response to rising interest rates or a shortage of inventory, as manufacturers' undelivered orders increased even more during the month.

While there were still few signs of a slowdown in consumer spending last quarter, low consumer confidence, is a sign that consumption will be more subdued in the coming months.

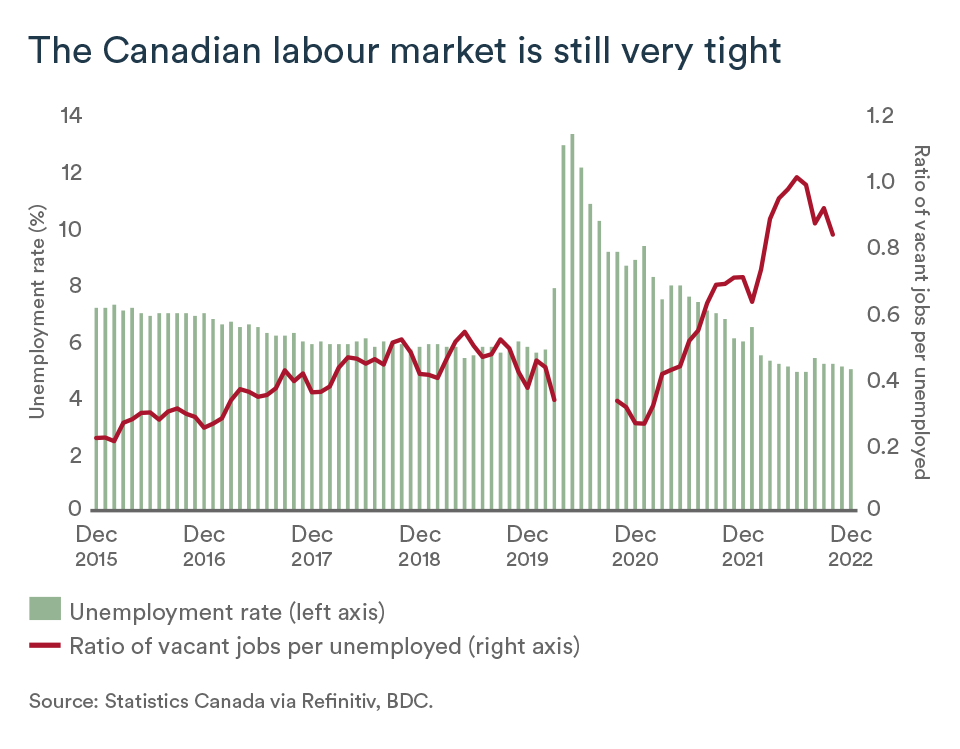

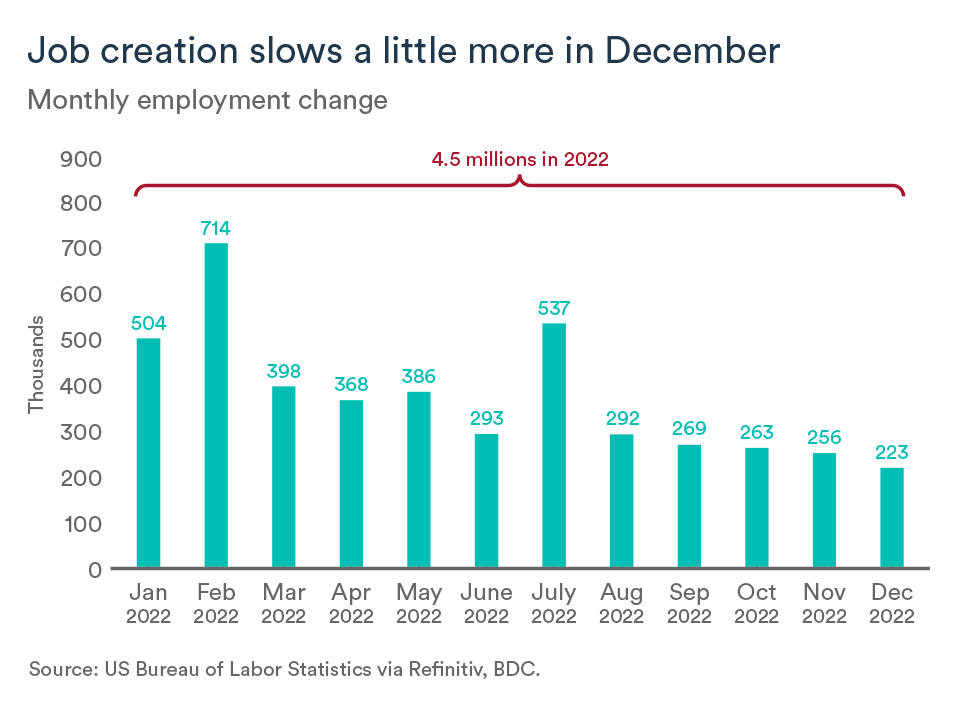

Employment rebounded in December

An economic slowdown that’s been brewing in Canada since late 2022 has yet to hit the labour market in a significant way. In December, employment increased massively, up 104,000 jobs. The unemployment rate remains historically low at 5.0%—near its all time bottom of 4.9%. More than 265,000 Canadians left their jobs for retirement during 2022.

Job vacancies have been slowly falling from the one million mark reached in the summer but were still over 900,000 across Canada in October. While labour shortages are still being felt by entrepreneurs, hiring intentions are expected to decline in the first quarter in line with a softening in overall demand in the economy.

The impact on your business

- Economic activity has so far held up well despite the many interest rate hikes in 2022. However, the next months will likely be more challenging for businesses. The usual post-holiday lull will be exacerbated this time around by economic uncertainty, continued high inflation and further interest rate increases.

- Inflation is proving to be more persistent in Canada than anticipated. Take advantage of the post-holiday slowdown to review your business. It may be time for your company to develop a new, less expensive product line, increase the quality you provide for the same price, introduce a loyalty program or improve your after-sales service.

- Hiring intentions are slowing but employment is still growing. Recruiting will remain difficult in the coming year. The economic downturn will mean less competition for workers, and this could be your opportunity to find the workers you’ve been looking for. Part-time, casual work or internships may be a good way to attract new staff for your longer-term needs.

U.S. economy starts to lose momentum

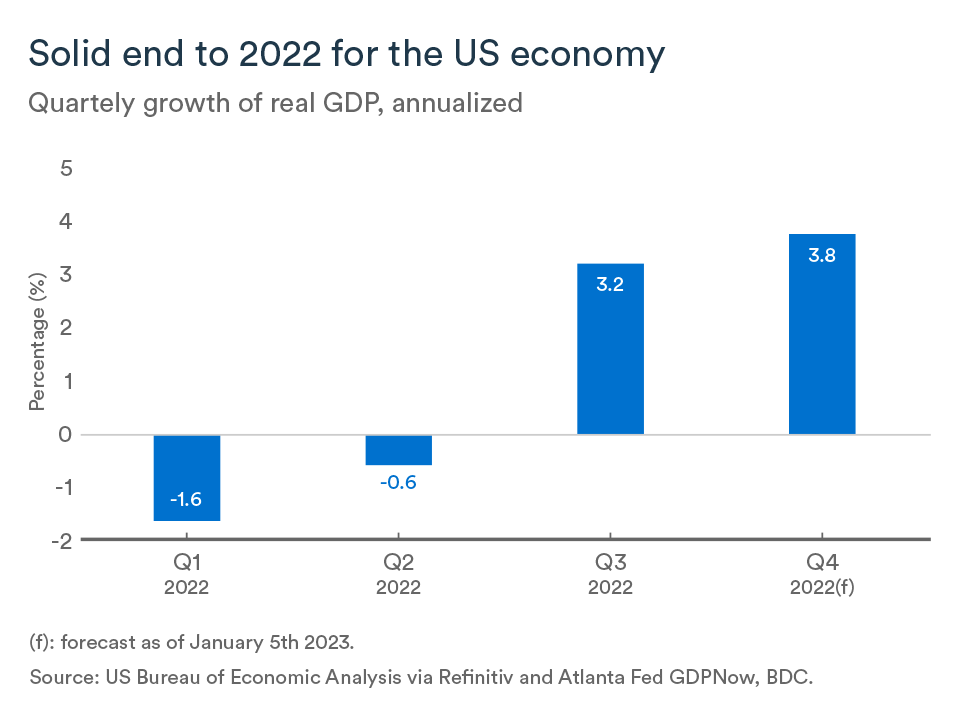

The U.S. economy likely slowed in the final quarter of 2022 after expanding by a surprisingly strong 3.2% in the third quarter.

The healthy gain in Q3 followed two straight quarters of negative growth—the technical definition of a recession—and brought growth to 2.5% for the first three quarters.

Can spending continues moving into 2023?

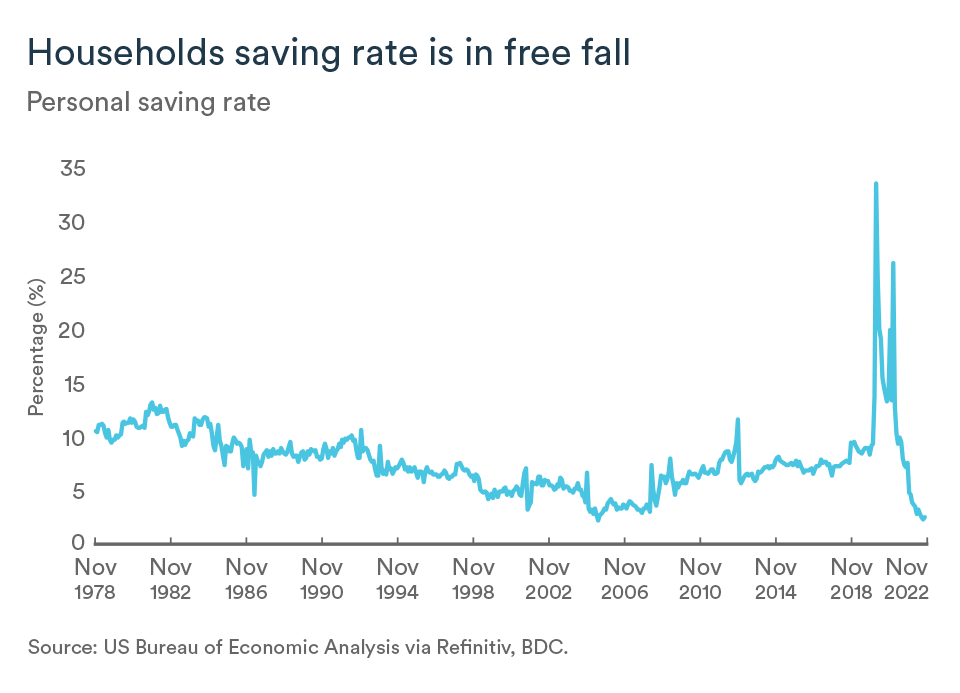

Consumer spending remained unchanged in November compared to October but could pick up in the coming months as real household disposable income grew by a solid 0.3% in the month.

That gain was supported by rising wages, particularly in the private sector. However, the savings rate relative to disposable income remains at 2.4%, among the lowest on record.

Consumer confidence also recovered in December thanks to lower prices at the pump, a decline in overall inflation and lower expectations for future inflation. Confidence was also bolstered by a solid labour market and a rebound in the stock market during the period. It remains to be seen whether the momentum will continue in 2023 in the face of rising interest rates.

The Fed has not said its last word

As expected, the Federal Reserve opted for a smaller rate hike in December, going for a 50-basis-point increase, down from the 75-point hikes it favoured earlier in the year. The Fed raised the federal funds rate to between 4.25% and 4.50%.

Inflation in the U.S. is showing definite signs of improvement. The consumer price index was at 7.1% in November, and the core measure (excluding food and energy) was at 6.0%. The price index for basic personal consumption expenditures was at 4.7%.

Despite progress on inflation, the central bank is not done tightening monetary policy as price increases are still too high. In its latest announcement, the bank warned that continued increases will be necessary.

Fewer jobs created

The labour market was strong in 2022, but fewer new jobs have been created in recent months. In December, 223,000 new workers were added to bring the total for 2022 to an impressive 4.5 million.

The unemployment rate declined to 3.5% in December, its lowest level of 2022 and in history. Despite a gloomier economic outlook, layoffs remain limited. Average hourly wage growth is also high and likely reflects a slowdown in lower-wage hiring.

The impact for your businesses

- While the U.S. returned to economic growth in late 2022, interest rate hikes will slow the economy in the coming months.

- Inflation is showing signs of improvement. Therefore, interest rates are expected to rise more slowly, but the Federal Reserve will continue its tightening in the first quarter as the speed of price growth remains too strong.

- Job creation continues but is less robust. The unemployment rate dropped to its lowest level in December. While consumption has held up so far, workers are drawing down savings to maintain spending. U.S. consumption is expected to be more subdued as the new year begins.

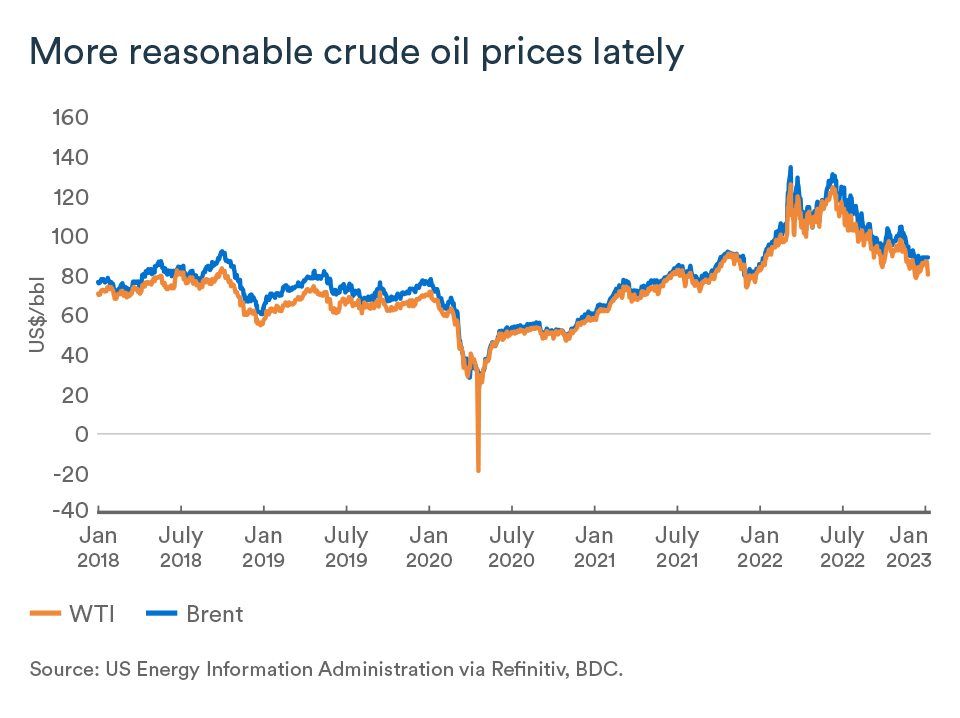

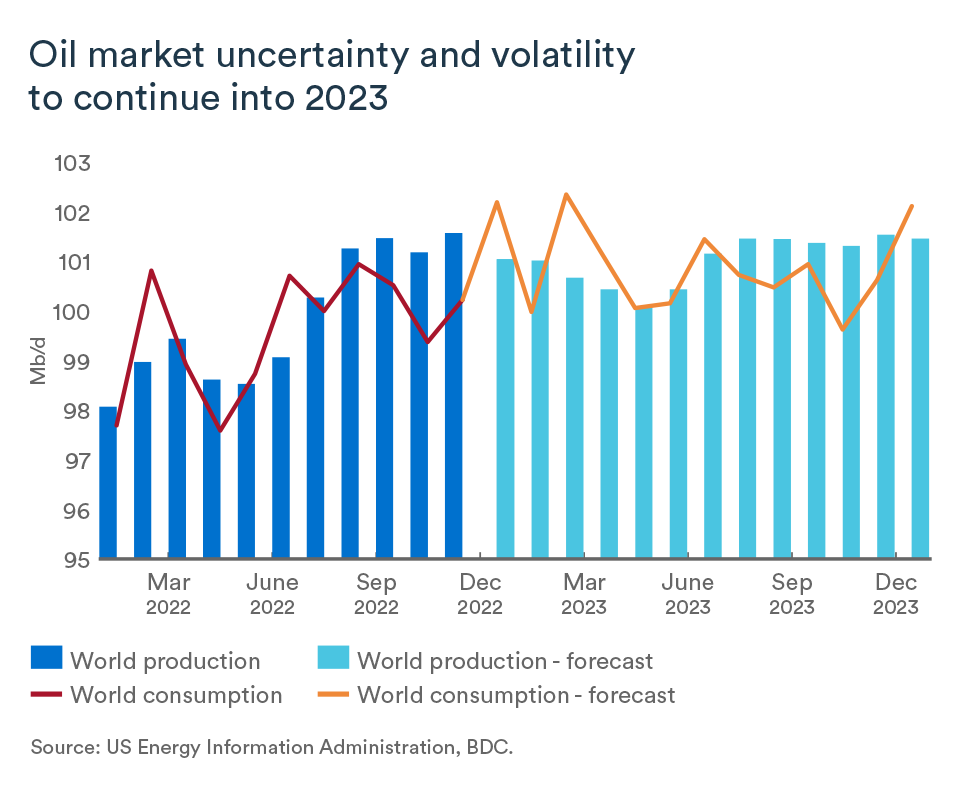

More volatility ahead in the oil market

Forecasts of simultaneous economic slowdowns in Europe, China and the United States hurt crude oil prices in the early days of the new year. Prices in early January fell to US$82 per barrel for Brent and US$73 for WTI. Those prices were down from 2022 averages of US$101 and US$95, respectively.

In the short term, prices are expected to remain around their current range, but anticipation of a recovery in global demand in the second half of the year could quickly spark a recovery.

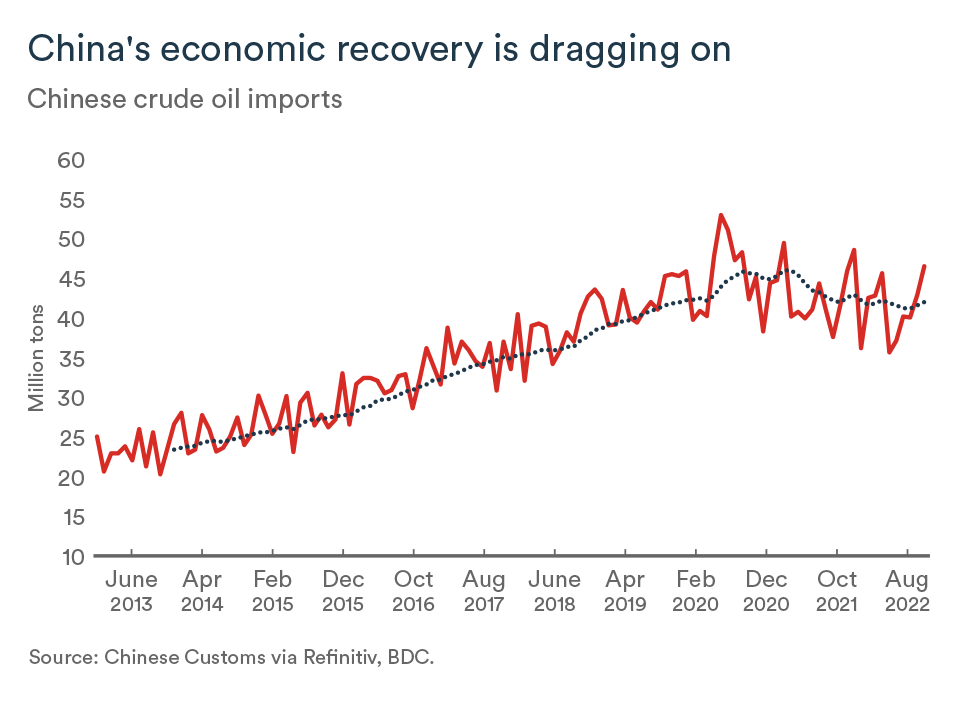

China's economy struggles with COVID

The easing of anti-COVID measures in China has produced a wave of infections and led to a contraction of manufacturing activity in the country.

It’s clear the virus will continue to disrupt production and slow domestic demand in the world's second largest economy and largest importer of crude oil. The Chinese government has increased export quotas for refined petroleum products, which is consistent with forecasts for weak domestic demand.

The first quarter will set the tone

The level of uncertainty in the global economy is such that crude oil prices will likely continue to yo-yo. After what’s expected to be a simultaneous slowdown in the major economies in the first quarter, signs of recovery should begin to be seen in the spring and several factors could push prices higher in the second half of the year.

The spread of COVID in China and a complete end of restrictions related to the virus should eventually support a resurgence of activity in that country.

In the U.S., the hundreds of billions of dollars in new subsidies and incentives contained in two federal bills—the Bipartisan Infrastructure Law and the Inflation Reduction Act—should accelerate the energy transition.

Massive government incentives flowing from these bills are diverting investment from fossil fuel projects toward renewables. Underinvestment in oil infrastructure, including for production from shale deposits, will contribute to upward pressure on prices. Meanwhile, reluctance to develop new interstate pipelines in the U.S. will limit the growth of the natural gas industry, despite strong demand from abroad as energy supply in Europe is a major issue. Embargoes against Russian energy remain in full force meaning stockpiling during the summer in anticipation of fall and winter may be more difficult in 2023 than in 2022.

Bottom line…

Crude benchmarks could recover as early as the second half of the year to the range of US$90 for WTI and US$100 for Brent. This is in line with the most recent forecasts from OPEC and its allies. OPEC+ sees oil demand increasing by 2.5% in 2023 compared to last year.

Interest rates: It's not over yet

The Bank of Canada has begun to ease up on its rate hikes, but this is still not the end of this cycle of tightening credit conditions. The latest announcement on December 7 brought the policy rate to 4.25%. We expect the rate to reach 4.5% on January 25, an increase of 25 basis points. Admittedly, the risks of a larger 50 basis points rise in January or an additional hike in March have increased. In addition to the higher core inflation data from November, the strong job gains from December and wage growth above 5% are a new source of concerns. The Bank of Canada's January Business and Consumer Outlook Survey will prove to be a key factor for what lies ahead.

Canadian dollar is fairly stable

The Canadian currency has held fairly steady since November, hovering between US$0.73 and US$0.74. However, the loonie could lose more feathers in the coming weeks as the decline in oil prices continues and fears of a global recession materializing weigh on the exchange rate. The spread between U.S. and Canadian rates is expected to widen in the first quarter of the year, which will also favour the U.S. dollar.

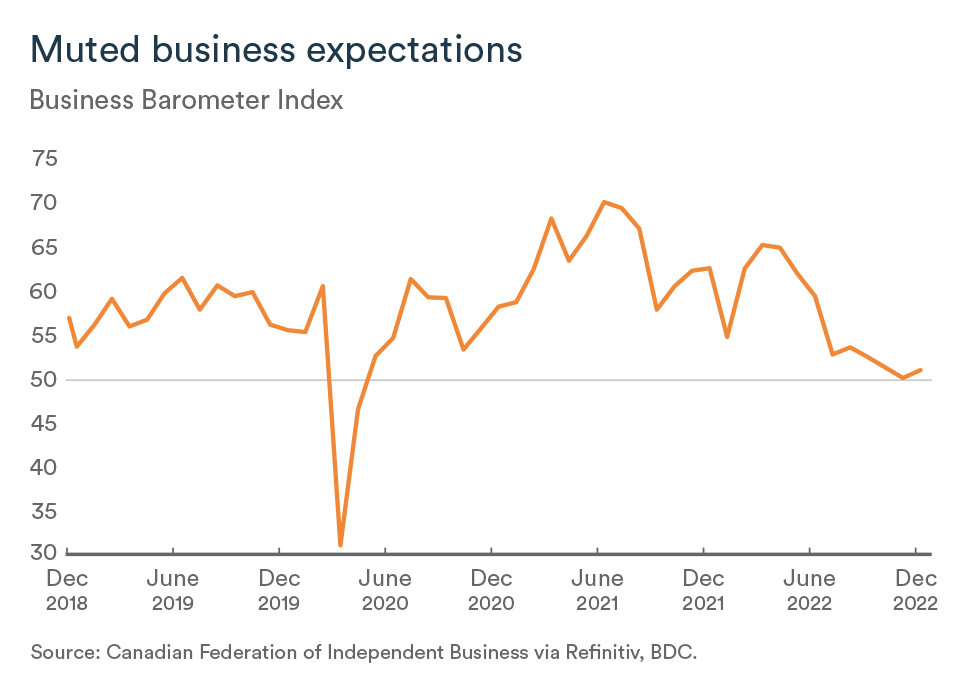

Business confidence is stalling

In December, the CFIB's business confidence index for the coming year essentially held steady, moving from 50 to 50.9. This reinforces the idea that businesses will begin 2023 on the lookout.

An indicator of 50 indicates that there is as many business managers expecting conditions to worsen over the next 12 months than there are expecting them to improve.