Deep tech valuations: How they compare to software start-ups

Since the launch of our first-ever $200 million Deep Tech Venture Fund last year, it’s become very clear that deep tech investing is extremely different from investing in software start-ups.

Most venture capital funds (VCs) tend to invest in software start-ups building new apps that are highly scalable and relatively inexpensive to create. Generally, the biggest risk with software start-ups is market adoption—some apps just never get picked up by their target market. Investors call this “market risk.” Well known successes include Facebook, Square and Uber.

Deep tech companies, on the other hand, build novel products that are often expensive to produce and difficult to scale. They tend to occupy sectors such as quantum computing, AI, hardware, blockchain, cybersecurity, electronics, advanced materials and biotech1. Not only is there market risk for these companies, but there is also the added risk that the end product never gets built. This is called “technical risk.” Well known successes include Tesla, NVIDIA and Moderna.

Most VC investors tend to shy away from deep tech start-ups because of the added technical risk. Our fund however, one of the only pure deep tech funds in Canada, sees this gap as an opportunity.

Our team consists of people with a science and engineering background, alongside others who have a business and finance background. As a result, we are able to dissect both the technical and market risks of a deep tech start-up, and have no shortage of great investing opportunities.

In this post, we will focus on how fundraising and valuations differ between software and deep tech start-ups. The data revealed should prove useful to all types of entrepreneurs and VC investors.

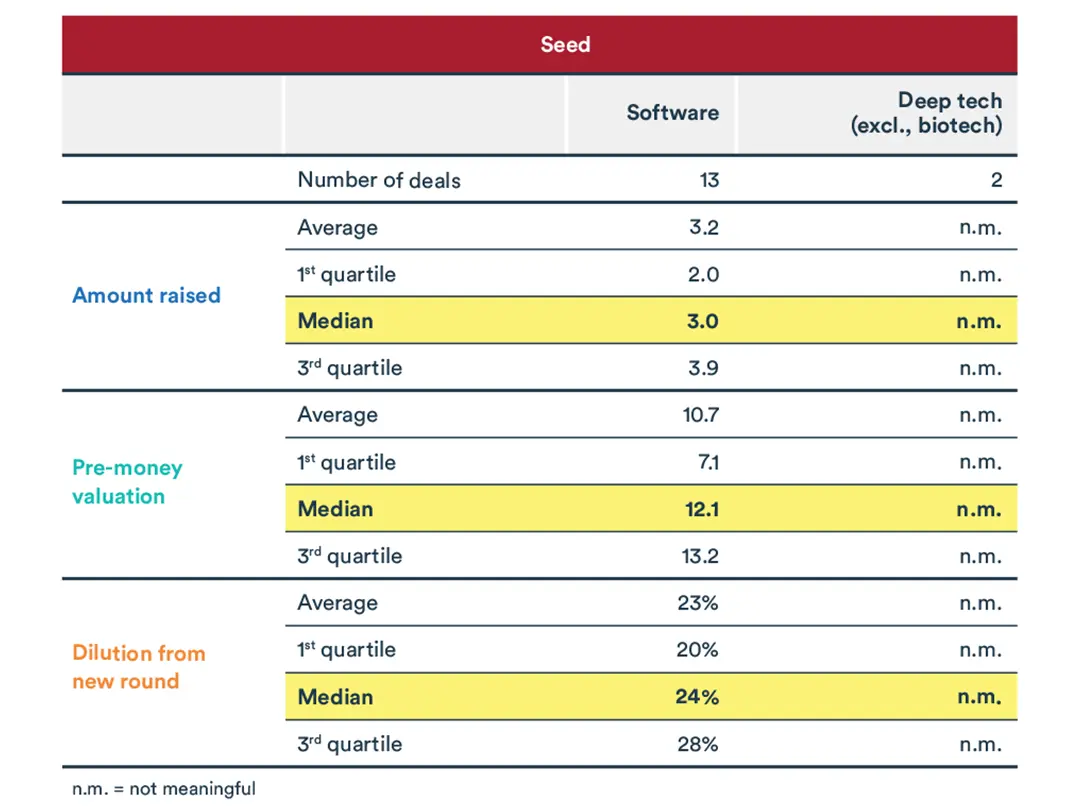

Valuation metrics for early-stage deep tech and software companies

BDC Capital is the most active VC investor in Canada. With over 300 companies in our direct investing portfolio, we have access to proprietary data on a large segment of the Canadian VC ecosystem.

In the table below, we chart capital raised, pre-money valuations and dilution across various stages, comparing software to deep tech start-ups. We examined deals closed since the start of 2019, primarily to ensure a meaningful amount of data.

It also allows us to limit our analysis to a defining period in Canadian VC. A recent study by BDC Capital shows that total VC investment in Canada doubled in 2019 from the prior year and has continued to grow rapidly ever since. VC investment in the 2016–2018 period on the other hand was relatively stable.

Early-stage software and deep tech valuations in Canada, 2019-2022

Note: The deals considered here only include those for which BDC has complete data and may not be representative of all the deals BDC Capital has closed over the given period. For example, if BDC completed a deal but the stage of the deal was not documented, the deal was removed from the analysis. Given that data omissions are random, the data is still representative of the VC ecosystem.

Canadian entrepreneurs can use this table as a reference when planning their next fundraising round, as it provides guidance on amounts raised, valuations, and expected dilution on any given deal compared to the average, the median, and the 1st and 3rd quartiles. We have noticed, for example, that amounts raised and valuations were generally closer to the 3rd quartile throughout 2021. However, we have seen them shift closer to the median over the past three months due to market conditions. For this reason, you may hear some VC investors arguing that valuations are not crashing, they are just returning to normalcy.

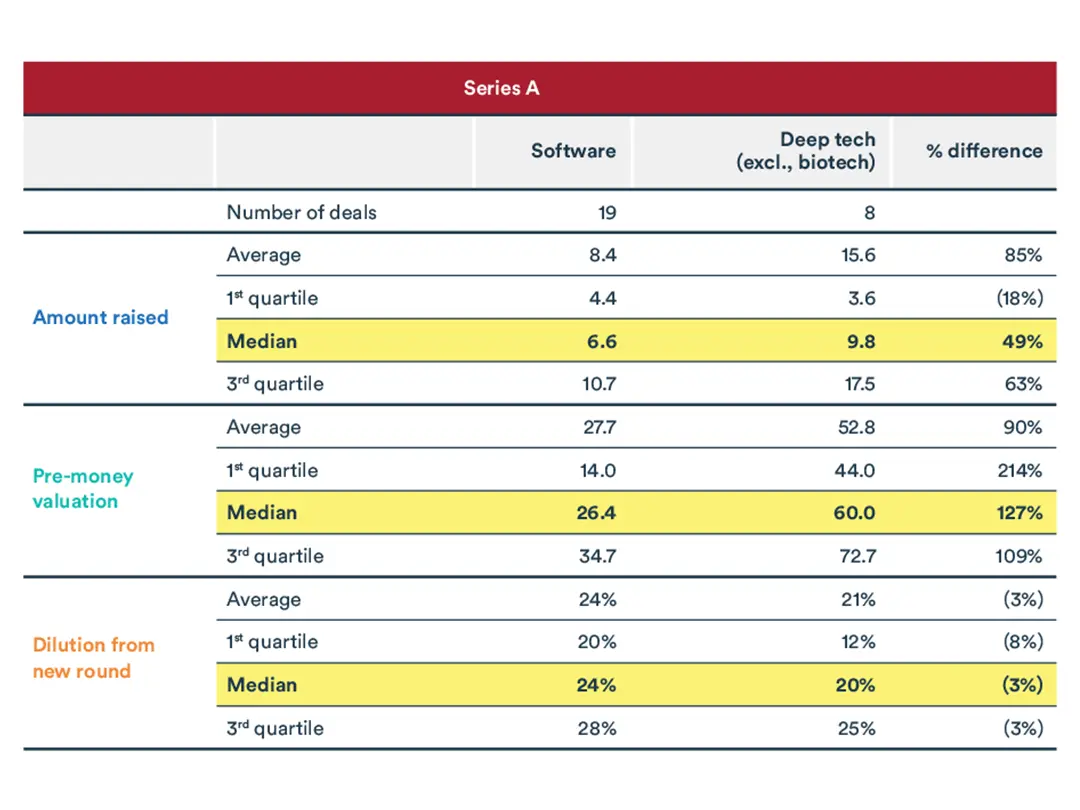

Deep tech start-ups require more capital in the early stages

One result that sticks out is that, in Series A, the median deep tech start-up raised around 50% more capital than the median software start-up. Deep tech valuations also tend to be 127% higher, resulting in 3% less dilution for existing shareholders.

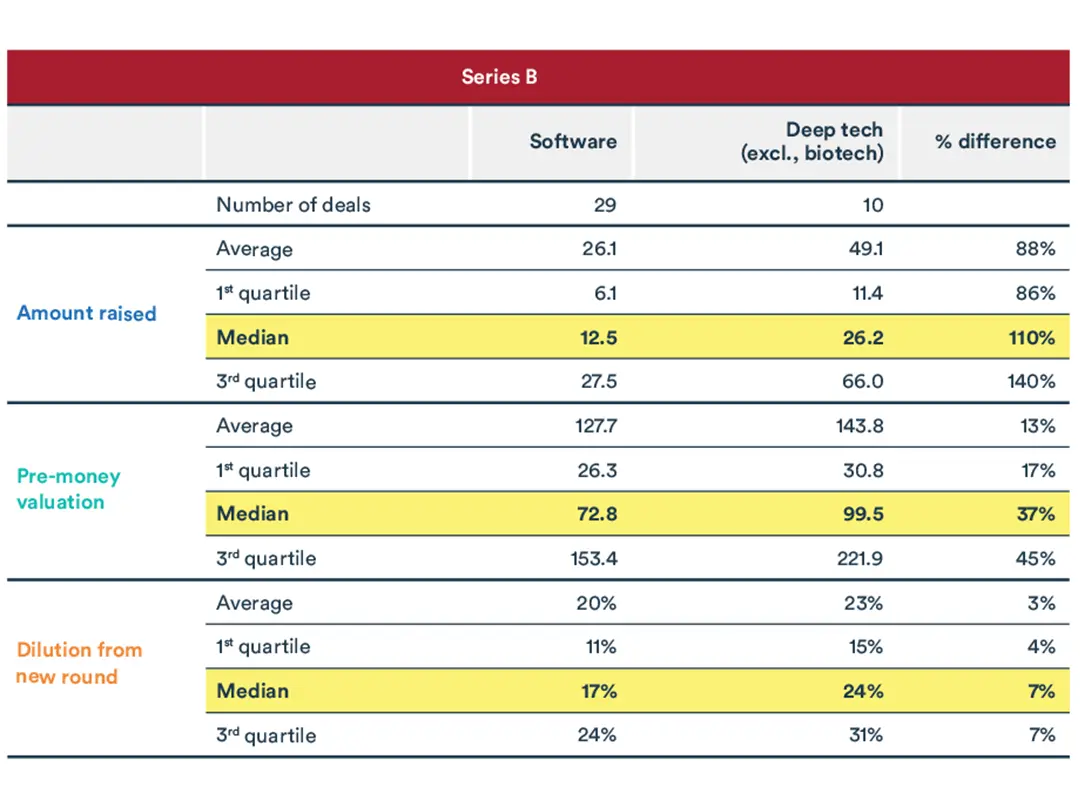

The same result persists in Series B, to a degree. Deep tech companies tend to raise 110% more than software companies at the Series B stage. While valuations at this stage are higher, they do not compensate for the larger raise, resulting in 7% more dilution to existing deep tech shareholders.

At these early stages, valuations are usually dictated by capital needs rather than any fundamental metric such as revenues, number of clients, etc. Clearly, more capital is required for deep tech companies building the first iteration of their product.

We also see more corporate investors in early-stage deep tech ventures. When making investments, corporates generally prioritize bolstering their own innovation efforts over seeking high returns. They are therefore less valuation-sensitive than the typical VC investing in software start-ups. Consequently, valuations are higher for deep tech start-ups.

Valuation metrics for later stage deep tech and software companies

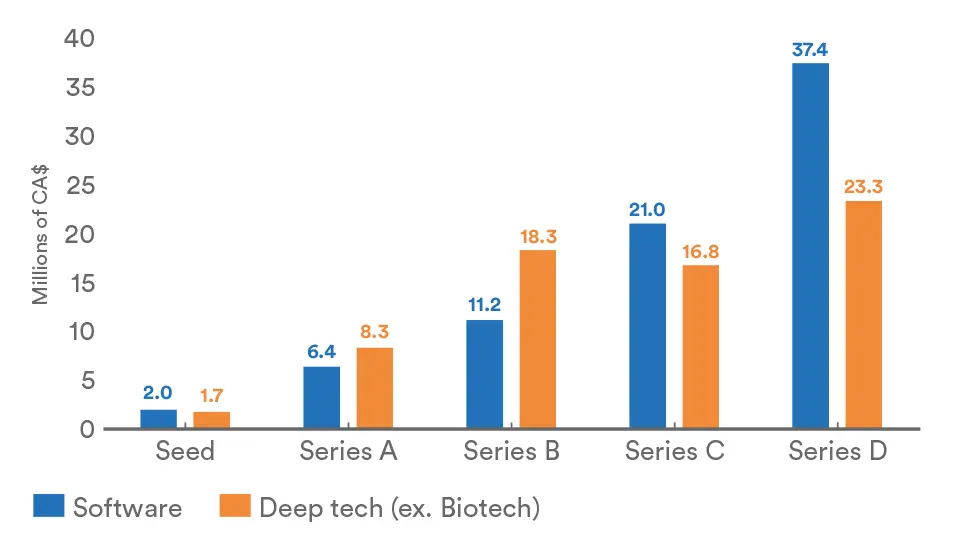

We did not have enough data in the 2019–2022 period to test whether these trends continued in later stages, so we broadened our time horizon to include the last seven years, from 2016 to 2022. The results are surprising!

While deep tech companies tend to require more VC capital than software companies at the Series A and B stages, they generally require significantly less VC capital at the Series C and D stages.

Median amount raised by deep tech and software companies in Canada, by stage, 2016-2022 (C$M)

Boston Consulting Group and Hello Tomorrow also came across the same result in their own analysis of deep tech start-ups across the globe and provided the following explanation:

“On the one hand, SaaS ventures typically have low early-stage equity needs but for some of them it can blitzscale due to high cash burn rate as they go to market, acquire and retain customers below the cost of delivering services to them (e.g., Uber, WeWork, Palantir). On the other hand, successful deep tech ventures require higher early-stage equity funding but once their deep tech product has been effectively de-risked and designed to value and cost, equity needs on average are controlled over time. As confirmed by several ventures interviewed, ‘once running, the need for outside capital will decrease.’ Also, revenues from the first commercialized product enable a shift to project financing.”2

In other words, deep tech ventures create their moat during the early stages by building their product and overcoming any technical risks. Software start-ups, on the other hand, tend to create their moat through branding, by building a network, or by being first to market.

It costs less for software start-ups to build their product during the early stages, but it costs them significantly more in marketing spend to maintain their edge during the later stages. In addition, because deep tech start-ups have a tangible product often yielding revenues once built, it tends to be easier for them to attract non-equity financing as they scale.

Deep tech: A strong, defensible moat

While deep tech start-ups have an added layer of technical risk at the early stage, overcoming this risk can quickly turn into a competitive advantage, leading to a lessened need for capital at later stages.

There are several other nuances between investing in deep tech and software companies, ranging from the IP ownership to the role of the Chief Science Officer. Once investors get comfortable with these nuances, they too will see plenty of great investing opportunities in deep tech. Canada, in particular, has long been regarded as a source of world-class research in deep tech domains, yet commercialization efforts have lagged.

As we continue to better understand how to support and nurture deep tech startups, we see no reason why the next Tesla, NVIDIA or Moderna cannot be Canadian.

Don’t hesitate to contact us if you’d like to learn more.

1The BDC Deep Tech Venture Fund invests in all these sectors except for biotech. The biotech space requires a unique skillset and expertise, and is more suitable for funds specializing in healthcare.

2BCG and Hello Tomorrow. “The Deep Tech Investment Paradox,” p. 21-22, March 2021.