Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreCanadian consumers: is the last pillar still standing?

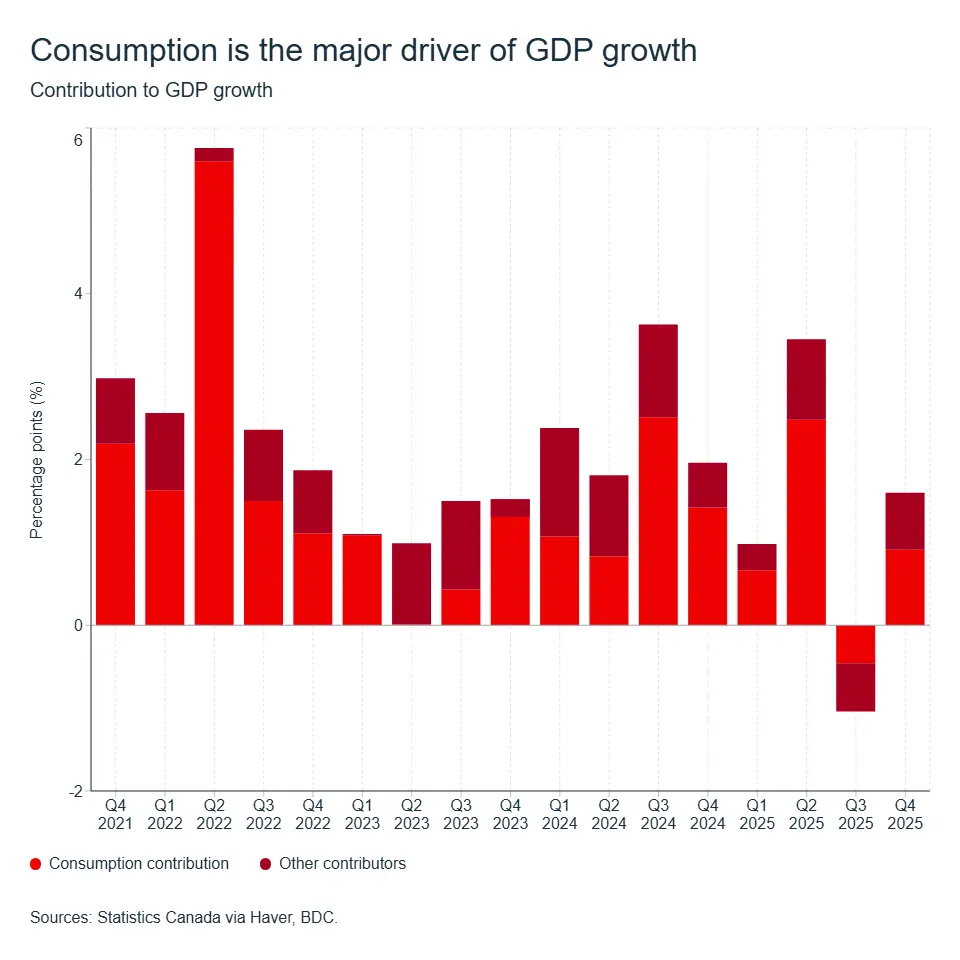

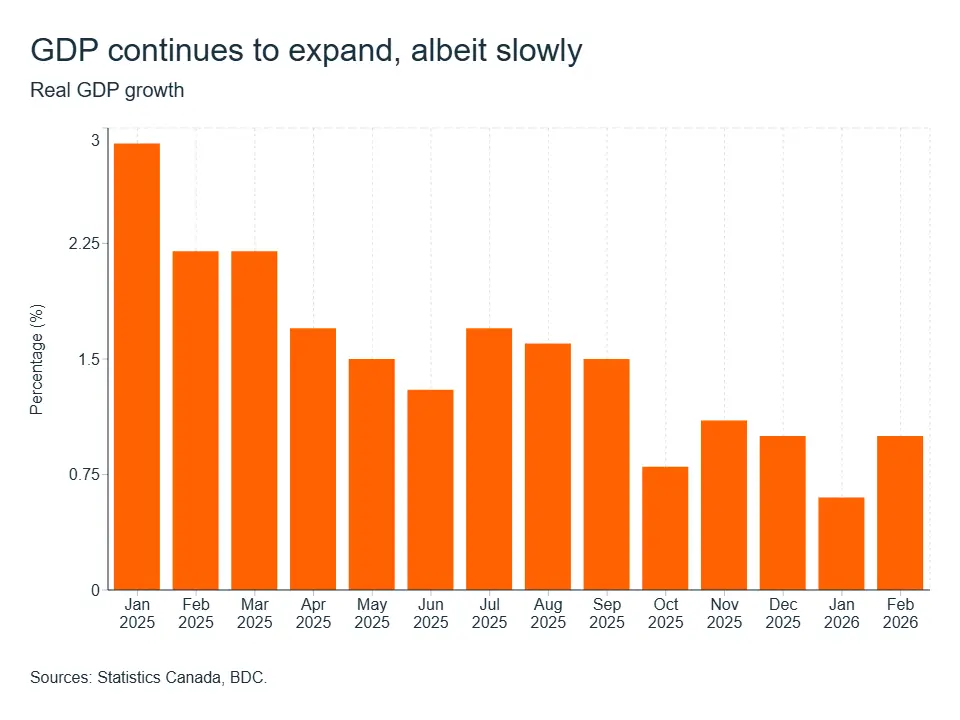

The Canadian economy is growing, but barely. GDP rose by an estimated 1.7% in 2025—the slowest annual pace since 2020—and our forecast is for just 1.0% growth in 2026. In this context, one economic actor stands out: the Canadian consumer. Year in and year out, household spending accounts for about 60% of GDP and is the main driver of growth. Can the consumer keep the economy in positive territory this year?

In 2025, household consumption alone contributed 1.4 percentage points to real GDP growth, while net exports subtracted 0.45 points and private investment remained virtually flat.

Exports continue to be hampered by U.S. tariffs. Business investment, meanwhile, remains in a wait-and-see mode. Uncertainty surrounding the USMCA review scheduled for early July, geopolitical tensions and rising input costs are all reasons for businesses to postpone their expansion plans.

These challenges are likely to persist and intensify in 2026. Consumption, therefore, won’t just be the main contributor to growth this year—it could be the only one. So, business fortunes will depend, more than ever, on households’ ability and willingness to spend.

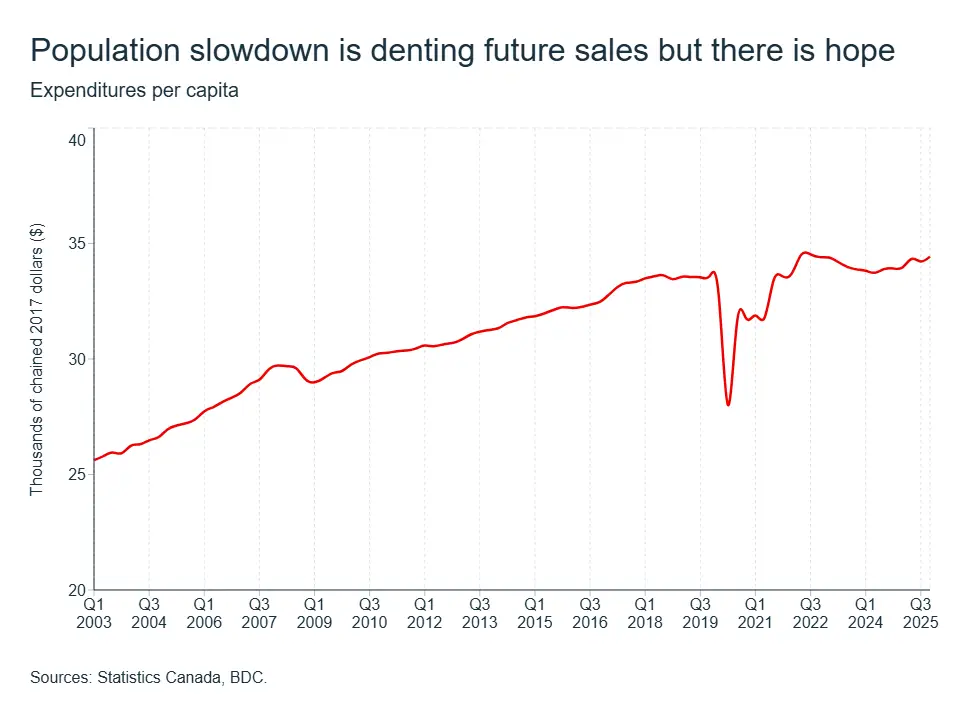

More spending per person, but fewer people

Per capita consumer spending is rebounding. After stagnating in recent years, real per capita consumption began to move higher in the second half of 2025, supported by cumulative cuts of 275 basis points to the Bank of Canada’s key interest rate since June 2024.

However, slowing population growth means the pool of potential customers is shrinking. Fewer newcomers to Canada means fewer first-time purchases of furniture, appliances and cars. Sales growth, therefore, will depend less on attracting new customers and more on increasing the value of each transaction.

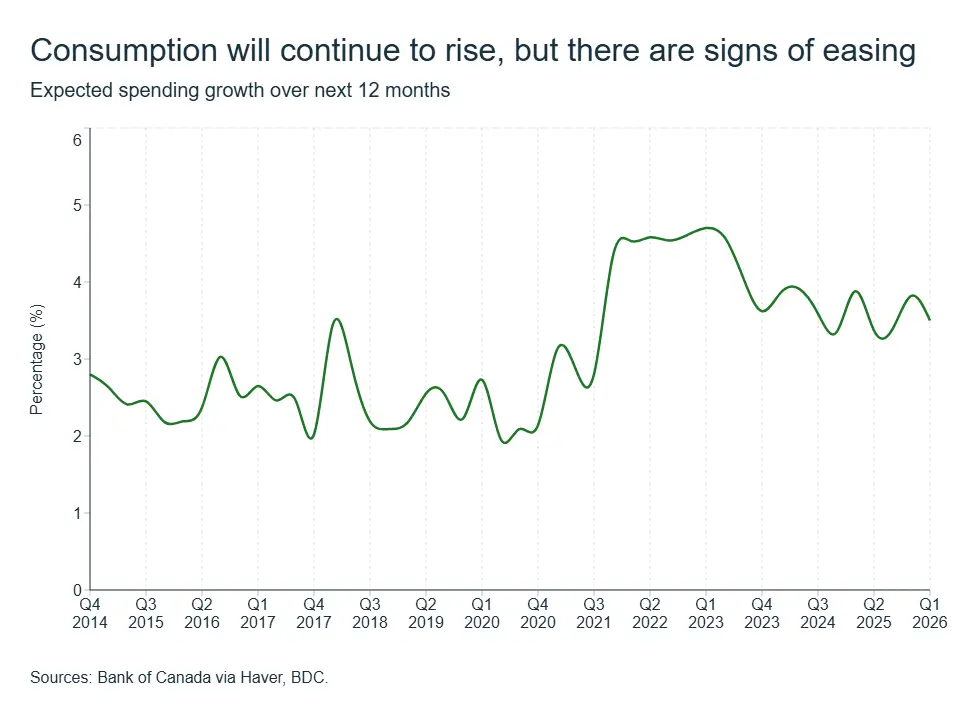

Spending is rising…but the pace is slowing

According to the Bank of Canada’s Survey of Consumer Expectations, households anticipate that their spending will increase by about 3.5% in 2026. Unfortunately, greater expected spending is likely based on the anticipation of higher prices rather than a genuine desire to spend more.

Inflation rose in March due to soaring energy prices linked to the conflict in the Middle East. Gas prices jumped 57% between February and March, while rising food prices also remain a major concern.

In general, however, purchasing power is benefitting from favorable conditions. Wages are growing by 3 to 4% year-over-year—well above inflation—and the Bank of Canada’s 2.25% policy interest rate is easing the burden of debt servicing.

Moreover, households appear to be managing a much-discussed wave of mortgage renewals better than feared—with income growth absorbing much of the shock and longer amortization periods doing the rest.

A healthy savings rate (4.4% in Q4 of 2025) suggests there remains a cushion to support consumption in the short term. However, it’s important to recall that 41% of Canadians report being $200 or less away from insolvency at the end of each month. There is room for households to spend, but the margin for error for many is essentially zero.

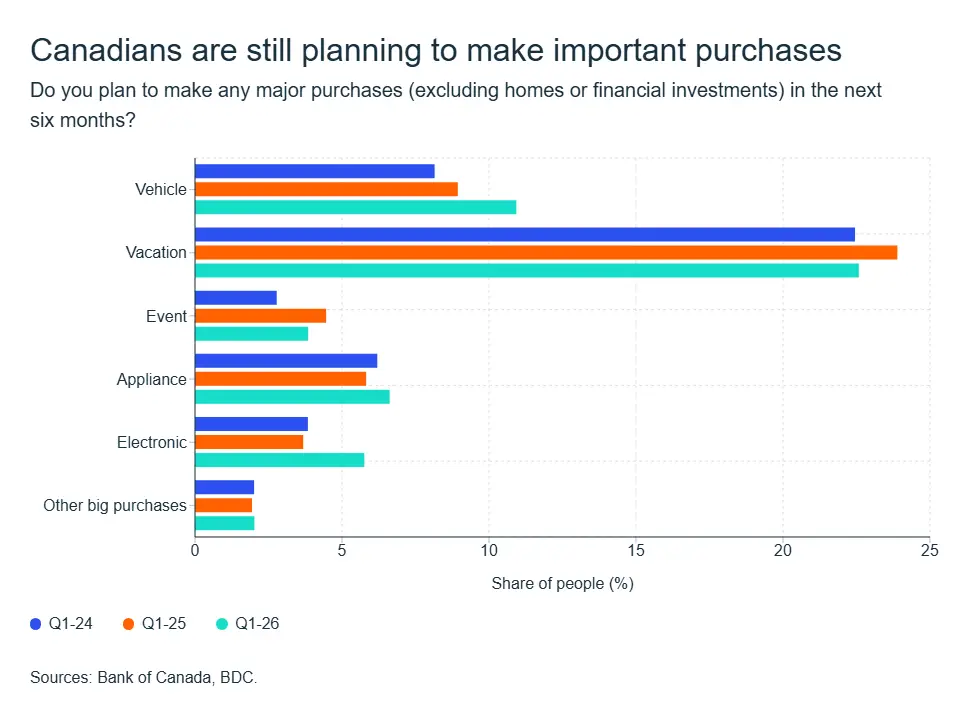

Intentions for major purchases are adjusting

Despite the prevailing uncertainty, intentions to make major purchases—vehicles, renovations, major appliances—remain relatively strong. New vehicle sales rose by 0.7% in February and used vehicle sales by 4.0%.

However, the conflict in the Middle East has likely dampened some of these intentions. This new source of stress for households is leading many to postpone or scale back large purchases, primarily due to rising transportation and energy costs.

This situation naturally creates winners and losers. According to Moneris data, grocery sales continue to rise, particularly at big-box retailers, and spending on entertainment and air travel saw significant growth early in the year.

However, about one in five people reportedly cancelled or postponed trips since the start of the conflict in the Middle East, mainly due to rising travel costs. Before the conflict, a BDC survey indicated that domestic tourism was on the rise, with 92% of Canadian travelers planning at least one trip within the country in 2026.

Where the pain is being felt most acutely is in traditional discretionary goods: clothing, household goods, building materials and gardening supplies, with the latter reflecting persistent weakness in the residential sector.

Not all consumers are facing the same pressures. The gap in disposable income between the richest 40% and the poorest 40% is widening.

Affluent households, buoyed by stock market gains, are driving high-end consumption. Conversely, households with modest incomes—which make up the customer base of many small and medium-sized businesses—are seeing their purchasing power grow, but at a much slower pace (+2.6% vs. +3.8%). Thus, consumption is increasingly taking on a K-shaped pattern, and the sales recovery will not be uniform across sectors or customer segments.

The labour market: resilient, but fragile

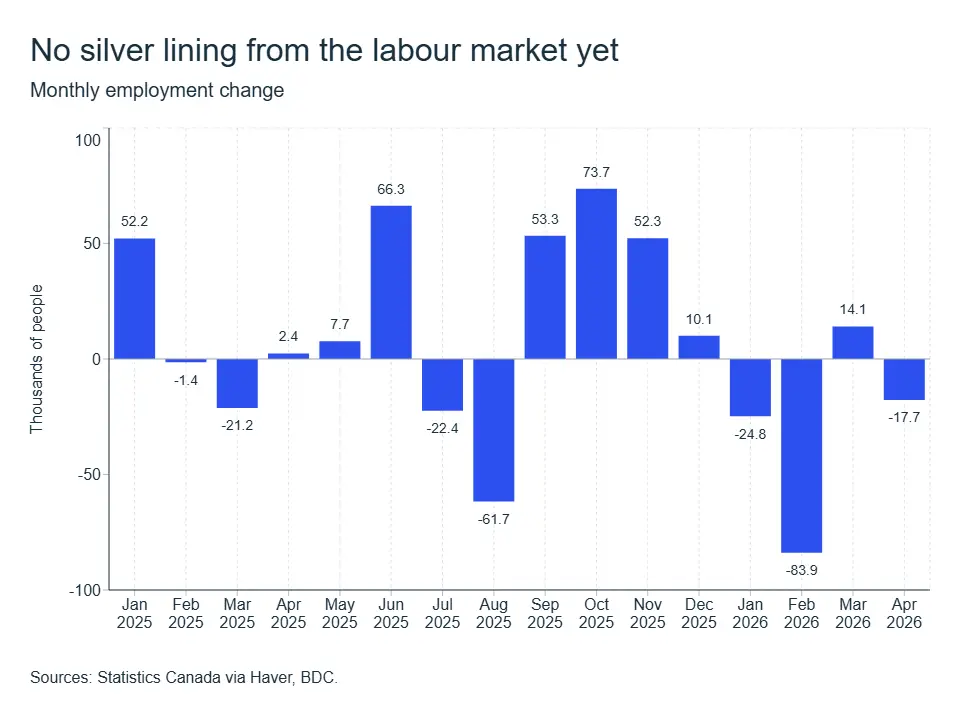

Disposable income—and the ability to consume—ultimately depends on employment. The unemployment rate rose to 6.9% in April, with 112,000 jobs lost since the start of the year, concentrated in full-time positions and the goods sector, which is most exposed to tariffs.

This is not yet a collapse: the layoff rate remains in line with pre-pandemic averages. It reflects more a freeze in hiring than waves of layoffs. And again, wages continue to grow faster than inflation, which supports the purchasing power of employed households.

But with the ratio of debt to disposable income hitting 176%, growing unemployment could push more households from spending caution to a serious pull back.

What does this mean for your business?

For businesses, just as for the economy, consumer demand continues, but it’s more prudent. Consumers aren’t radically scaling back their spending, so there’s no need to panic. It’s simply that the margin for error is getting narrower.

Consumption should, therefore, continue to support the economy and your sales in 2026. But households are reallocating their spending. They’re focused on paying for essentials and using their discretionary budget for products and experiences deemed “worth the cost.”

In a market where the customer base is shrinking and every dollar spent is scrutinized, waiting for demand to return is not a strategy. To maintain your margins, build customer loyalty, enhance your offerings and maximize value per customer through improved productivity.

Canada: Growth holds but just barely

The first quarter is expected to end on a positive note, but overall, 2026 has started off at a slow pace. BDC is maintaining its growth forecast of 1.0% for the full year, while the Bank of Canada is now projecting 1.2%. In both cases, this is significantly slower than the economy’s performance in recent years. Sources of growth are increasingly running out of steam.

Canada will avoid a technical recession

The first quarter ended on what appeared to be an encouraging note. Real GDP rose 0.2% in February—a fourth consecutive monthly increase. Estimated annualized growth for the quarter was around 1.7%, a welcome rebound from a 0.6% contraction in Q4 of 2025.

The Q1 rebound is largely attributable to strength in manufacturing (+1.8% in February, the strongest monthly gain since January 2023). Ontario’s automotive sector was particularly strong, with vehicle production surging 20.4%, following maintenance shutdowns. While this was a positive signal for the industry, it was nevertheless a one-off event, reflecting a technical recovery rather than structural momentum.

Growth in the first quarter masked a more troubling reality. GDP growth on a year-over-year basis has slowed almost continuously over the past year, dropping from nearly 2.5% at the start of 2025 to just 0.8% in Q1.

Preliminary estimates for March point to stagnation (0.0%). Gains in wholesale trade and transportation were offset by declines in retail trade and the mining and oil extraction sector, although the latter is expected to rebound as early as next month.

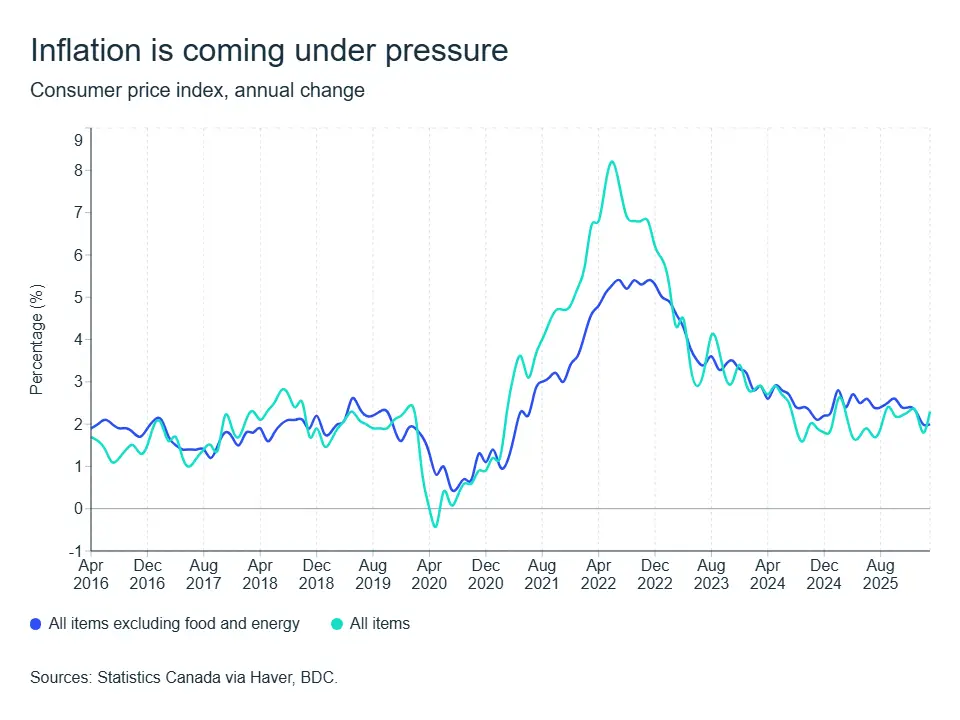

Inflation is picking up amid conflict in the Middle East

After more than a year of relative stability around the Bank of Canada’s 2% target, inflation appears to be making a comeback. The Consumer Price Index climbed to 2.4% in March, up from 1.8% in February—a sharp shift directly linked to the closure of the Strait of Hormuz, with higher energy prices being the primary driver.

Gasoline prices have surged, and while the initial shock was relatively well-absorbed by the market, each additional week without free passage through the strait clouds the longer-term inflation outlook.

Every passing day increases the risk that price hikes will be passed through various production chains—beyond just energy. Inflation for many products was well under control in Canada before the conflict erupted. But food prices had already been experiencing upward pressure and will be among the first to show the effects of rising energy costs.

Food price inflation, in fact, continued to accelerate to 4.4% in March. For consumers (as we analyze in our main article), the combination of higher energy and food costs directly squeezes budgets, reducing money available for other expenses.

For the Bank of Canada, whose role is to control inflation, important nuances must be considered. Core inflation remains contained. Excluding gasoline, the CPI actually slowed to 2.2% in March, down from 2.4% in February.

Therefore, for now, the country is experiencing a concentrated price shock rather than a widespread surge. However, the central bank won’t allow this shock to turn into persistent inflation if it sees further signs that it’s spreading in the economy.

The bank’s policy rate is expected to remain at its current level of 2.25% in June, but the prolonged closure of the strait could force it to raise rates to prevent inflation from spreading further.

Deceptive trade trends

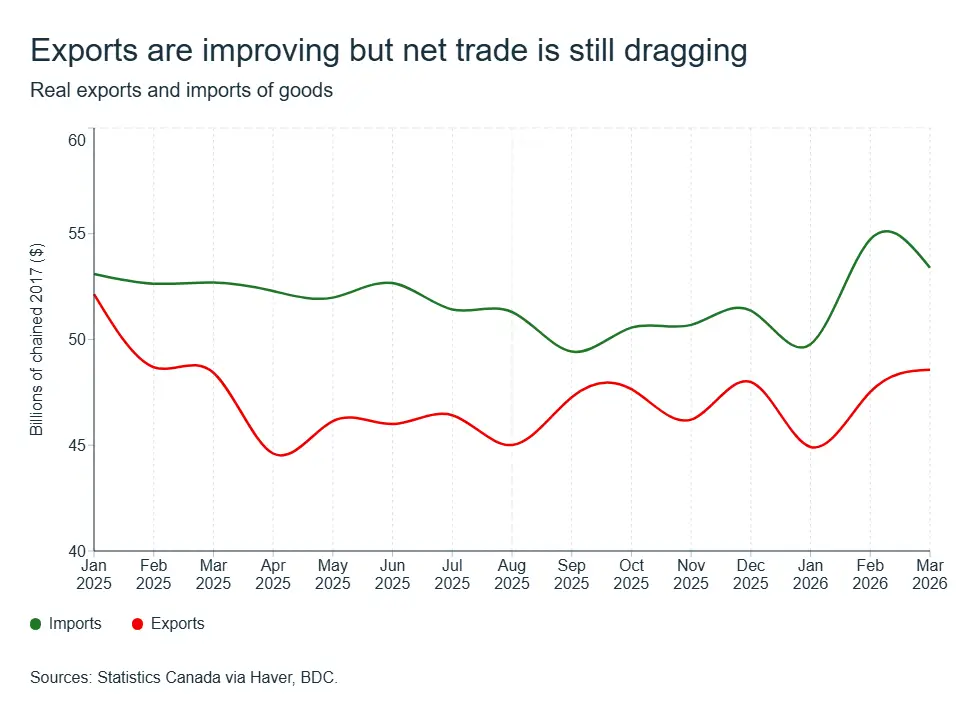

The trade balance posted a $1.8-billion surplus in March—the first since September 2025—following a $5.1-billion deficit in February. This is cause for celebration, but some caveats are in order (again!).

Renewed uncertainty at the start of the year supported markets that are important for Canadian exports, namely precious metals and petroleum products. Excluding these two categories, exports rose by only 1.1% in value in February and actually fell 0.3% in volume. Once again, what we are seeing isn’t a structural recovery in trade, but rather a one-off boost in value benefitting certain localized markets.

On the import side, spending remains high. Despite the ongoing enthusiasm for supporting Canadian purchases, a cumulative trade deficit since the start of the year points to a concerning trend—net trades are expected to contribute negatively to growth in Q1. A more significant slowdown in imports coupled with a recovery in exports will be needed to turn the situation around.

The share of exports destined for the United States fell to 66.7% in March, a historic low. While this is likely a sign that market diversification is accelerating, it also indicates that U.S. sector-specific tariffs continue to weigh on the economy. Since April 6, new tariffs have been imposed on steel, aluminum and copper products based on their total value—expanding the number of companies and industries affected.

The labour market weakens

The start of the year was difficult for employment, and the situation does not seem to be improving. After losses of 25,000 in January and 84,000 in February—the worst month since the pandemic—March offered a slight respite (+14,000), followed by another modest decline in April (−18,000). In total, Canada has lost approximately 112,000 net jobs since January, concentrated in full-time positions (−111,000).

The unemployment rate rose to 6.9% in April, and the employment rate (60.5%) returned to its recent low.

The picture is not uniformly bleak. It reflects more of a slowdown in hiring than waves of layoffs. The private-sector job vacancy rate has been stable for five quarters and, most importantly, wages are holding steady.

But the divergence between a shrinking labour market and rising wages can’t last indefinitely. If the hiring slowdown persists, consumer confidence—and their willingness to spend—will eventually suffer.

The Impact on Your Business

- The energy crisis spreads further each day that the Strait of Hormuz remains closed. Renegotiate your supplier contracts and include price adjustment clauses before your margins take a hit.

- U.S. prices are rising and will be for some time. Explore other supplier opportunities, especially if your supply chains are directly or indirectly tied to metal products.

- While hiring is on hold, wages are still rising. Make sure to include your current employees in your productivity investment plan. Focusing on retention and training costs less than replacing employees—and better positions you for a recovery.

British Columbia

The B.C. economy continued to face headwinds in early 2026, though there are signs that conditions may be stabilizing. Employment losses persisted through April, and consumer spending softened further, even as interest rate relief continues to filter through to households.

We still expect provincial growth to land near 1% this year, but the outlook remains clouded by trade uncertainty, ongoing supply chain disruptions, and lingering weakness in housing markets on both sides of the border.

The April employment losses left total employment in the province down roughly 40,000 jobs since the start of the year. While the pace of job losses moderated compared with February and March, labour market conditions remain fragile.

Recent declines were concentrated in private sector services, while construction and manufacturing posted modest gains, supported by ongoing major project activity. The unemployment rate edged up to 6.8% in April, its highest level outside of the pandemic era, underscoring the cooling in labour demand.

Consumer activity is also losing momentum. Retail sales in B.C. fell by 0.4% in February, following a flat start to the year, and remained well below the pace observed in the second half of 2025. Higher borrowing costs over the past two years continue to weigh on discretionary spending, and softer job growth is reinforcing a more cautious attitude among households.

There are, however, some offsets to the weaker near term picture. Major capital investments—particularly in LNG, utilities and public infrastructure—are supporting activity in construction, transportation and industrial services. That said, the forestry sector remains under significant strain, with mill closures, low lumber prices and U.S. trade barriers continuing to drag on output and employment. Altogether, 2026 is shaping up as a year of adjustment for the B.C. economy, with downside risks still likely to outweigh upside surprises in the near term.

Alberta

Alberta remains the province best positioned for growth in 2026. The positive forecast is driven by soaring oil prices and better-than-expected economic results in late 2025. Growth is expected to exceed 2.0% in the region in 2026, more than double the projected national rate.

The conflict in the Middle East is a major driver for Alberta’s economy. WTI neared US$110 per barrel in early May—well above the levels projected in the February provincial budget. This premium is expected to translate into a significant increase in government and corporate revenues. Oil production remains at high levels, averaging 4.2-million barrels per day in the first quarter of 2026, up 3.3% year-over-year.

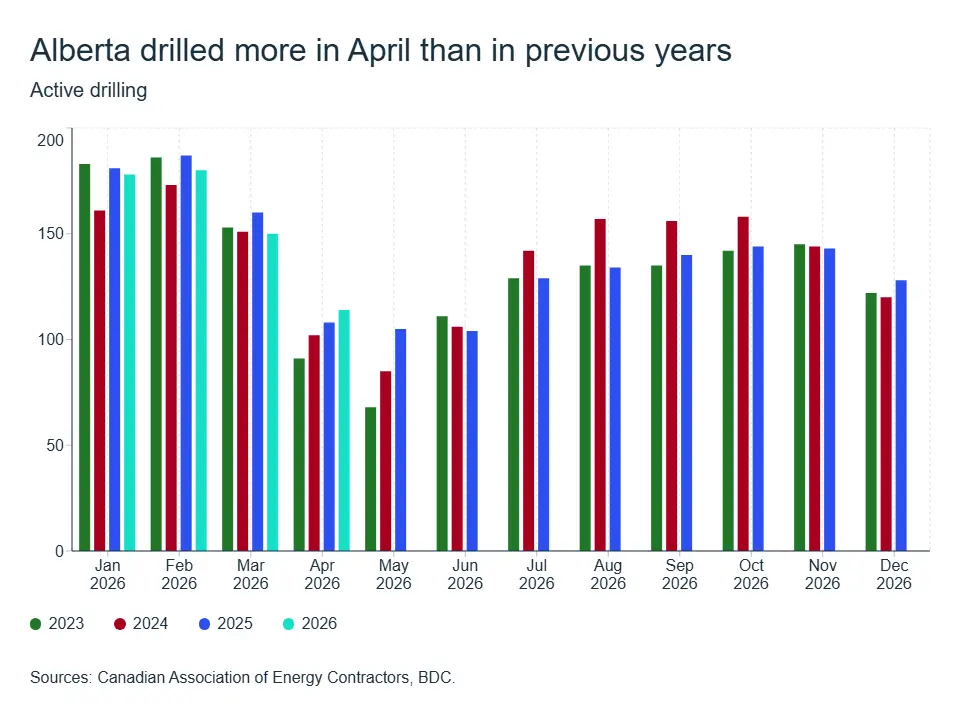

That said, the price increase is not translating into a production boom. Companies are maintaining financial discipline, keeping capital expenditures stable in the absence of clarity on how long the price surge will last. Drilling activity confirms this. The number of active rigs stood at about 125 in April, and only 41% of the drilling fleet was in operation, lower than last year, according to the Canadian Association of Energy Contractors. However, the Trans Mountain pipeline expansion is paying off, as oil exports to Asia reached a record high of over $9 billion in 2025.

The labour market lost momentum in April. Employment remained essentially stable (+1,000), but the unemployment rate jumped to 7.0%—up 0.5 percentage points—due to an influx of new job seekers into the labour force (+16,300). Since the start of the year, the province has nonetheless created about 25,900 jobs, concentrated in January. Average weekly wages are rising faster than the national average and are well above inflation. However, retail sales fell by 1.9% in February, following January’s sharp increase, a sign that Albertans are concerned about the current environment, even though it’s favorable for the economy.

Saskatchewan

As a resource-driven province, Saskatchewan’s economy is also well positioned to grow above the national average in 2026. The province’s real GDP growth could reach 2%, placing it just behind Alberta among the provinces.

The ongoing closure of the Strait of Hormuz is supporting oil and gas-producing regions like Saskatchewan as well as the mining sector. In 2025, total mineral sales reached $12.8 billion (+19%), paced by potash ($9.3 billion, +18%) and uranium ($3.2 billion, +24%, a record). The momentum continued into the new year. In February, potash sales rose by 12% and uranium sales by 8% year-over-year, while potash production surged by 19%. The planned commissioning of BHP’s Jansen mine in 2026, combined with the start of construction on NexGen’s Rook I uranium mine this summer—the largest under development in Canada—is expected to support the province’s growth in the medium term.

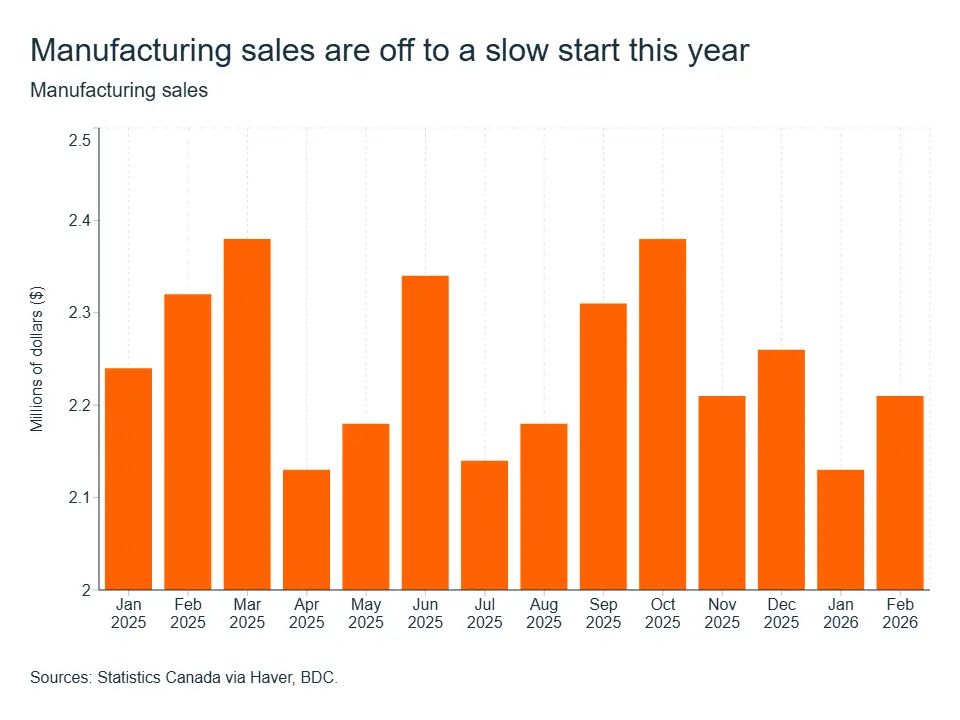

The conflict in the Middle East is benefitting potash and oil exporters. Oil prices are well above the province’s conservative budget assumption of US$59.75 per barrel for WTI. However, the war is also driving up nitrogen fertilizer costs for farmers—the price of urea has surged to about $1,200 a tonne, up from $780 last summer. The good news is that a critical mass of farmers had stocked up on fertilizer before the conflict broke out, according to the Canadian Federation of Agriculture. The downside for Saskatchewan lies more in the manufacturing sector. Manufacturing sales fell by 6.6% since the start of the year, and exports to the United States dropped by 22% in January—a reminder that U.S. tariffs are weighing even on this resource-based economy.

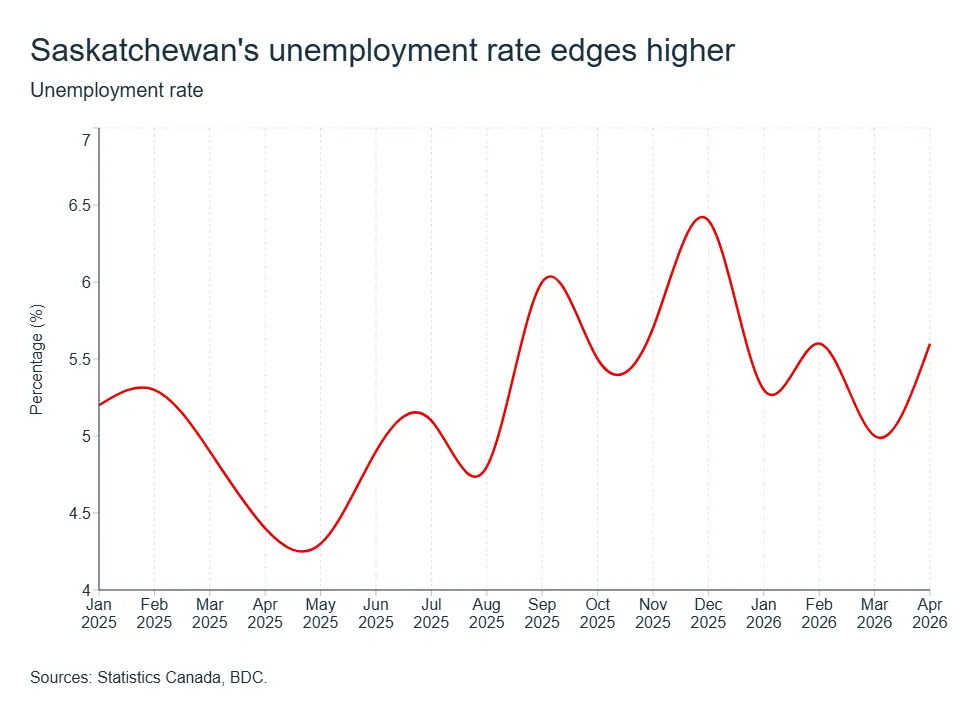

The labour market lost momentum in April. After adding 5,800 jobs in March, Saskatchewan lost 4,000 jobs in April, and the unemployment rate rose to 5.6% (+0.6 percentage points). The province nevertheless remains second among the provinces with the lowest unemployment rate, well below the national average of 6.9%. The total labour force and full-time employment reached historic highs for the month of April, two indicators that will support consumer spending.

The Canada-China agricultural trade agreement is bearing fruit. Since March 1, China has reduced its tariffs on canola seeds to approximately 15% and completely suspended tariffs on canola meal until the end of 2026. Tariffs on dry peas have also been lifted. Canola oil, however, remains subject to a 100% tariff, which limits the progress for processors.

Manitoba

Manitoba’s economy is expected to grow moderately by about 1.2% in 2026, slightly above the national average, according to the provincial budget forecast.

The budget included several measures designed to ease the burden on households and support spending. For example, the province will eliminate the 7% provincial sales tax on all grocery items sold in grocery stores starting July 1, including prepared meals, soft drinks and snacks, which were previously taxed.

Manitoba’s labour market continued to enjoy positive momentum. After a sluggish start to the year, employment rebounded in March with the creation of approximately 11,000 jobs. In April, despite a slight decline, the unemployment rate dropped to 5.0%—a notable decrease of 0.6 percentage points—placing Manitoba among the provincial leaders.

Manufacturing shipments remain under pressure. Manufacturing sales fell by 5.5% this year through February, reflecting a slowdown linked to the imposition of tariffs, primarily on agricultural products. The agri-food industry accounts for nearly one-third of the province’s total manufacturing sales. The agreement on Chinese tariffs on canola—a pillar of the industry—was welcome.

Manitoba’s international exports have fallen by 33.4% since the start of the year, with exports to the United States down by 43%—a sign that U.S. tariffs are weighing heavily on the province. High energy prices could also boost transportation costs—a key sector for the Manitoba economy, which relies heavily on domestic trade.

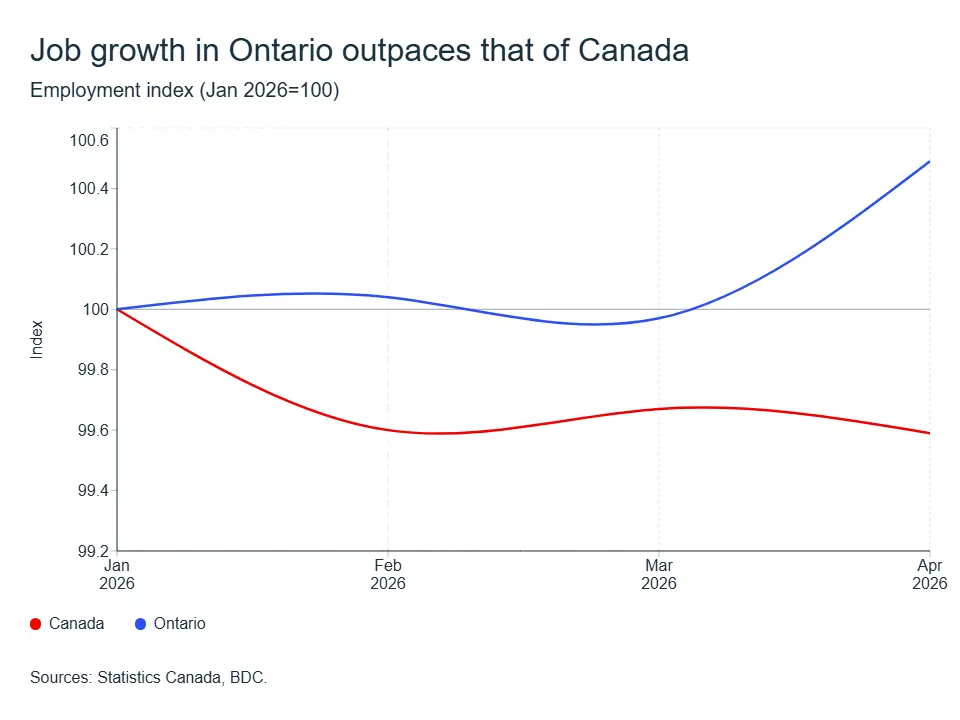

Ontario

The Ontario economy is showing encouraging signs after a slow start. The latest employment data indicate an improvement in Ontario’s economic situation.

In April, employment rose by 42,500 jobs. Following job losses in March and weak growth since the start of the year, this increase is encouraging.

This is particularly true when comparing Ontario’s results with the rest of Canada. Since the start of the year, the rest of Canada has lost 112,000 jobs, while Ontario has created 39,900.

However, the impact of tariffs continues to weigh on the economy. In addition, slowing population growth has been dampening consumer spending in recent months. Employment in the retail sector is slowing. But Ontario has fared better than the rest of Canada since the start of 2026.

Quebec

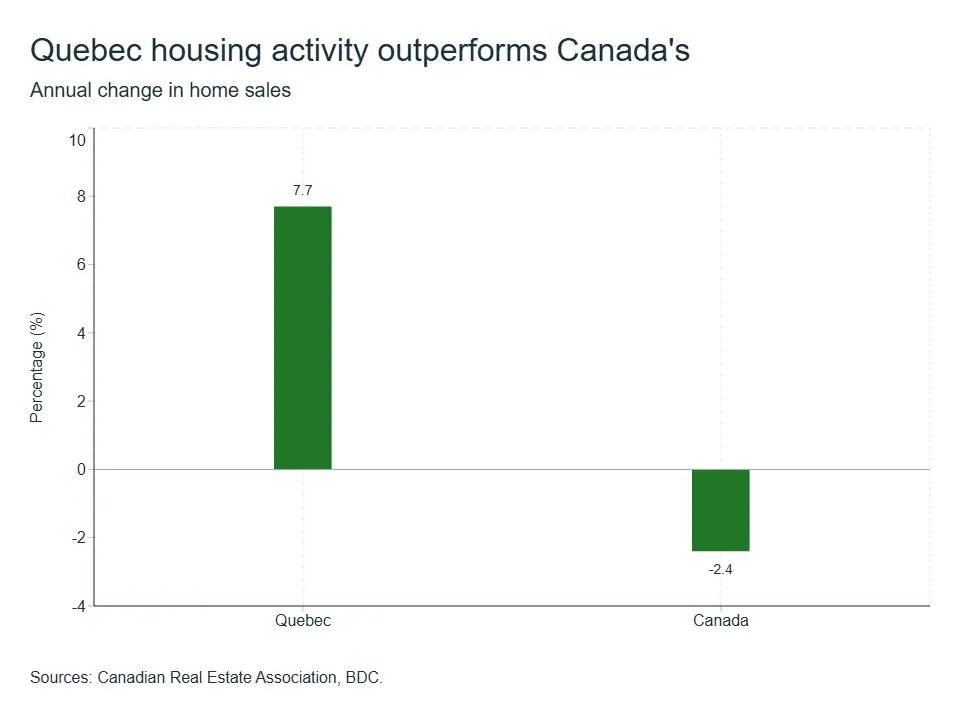

Quebecers continued to buy homes in 2025 despite an economic slowdown. Home sales rose by 7.7% last year, while the opposite trend was observed across Canada. Lower debt levels and a strong job market in 2025 supported real estate activity. Now that the job market is cooling off, we will closely monitor developments to see if this trend continues in 2026.

The job market in Quebec continued to show signs of slowing. After an encouraging March, the number of jobs fell by 43,000 in April, pushing the unemployment rate up to 6.2%. This is the highest unemployment rate seen since 2022.

Exports regained some momentum in February and even more so in March, when they increased 19%. However, trade levels remain below pre-tariff levels, and we don’t anticipate a full recovery this year.

We forecast modest growth of 0.7% for the province in 2026, held back by weaker external demand, persistent uncertainty and slower population growth.

Nova Scotia

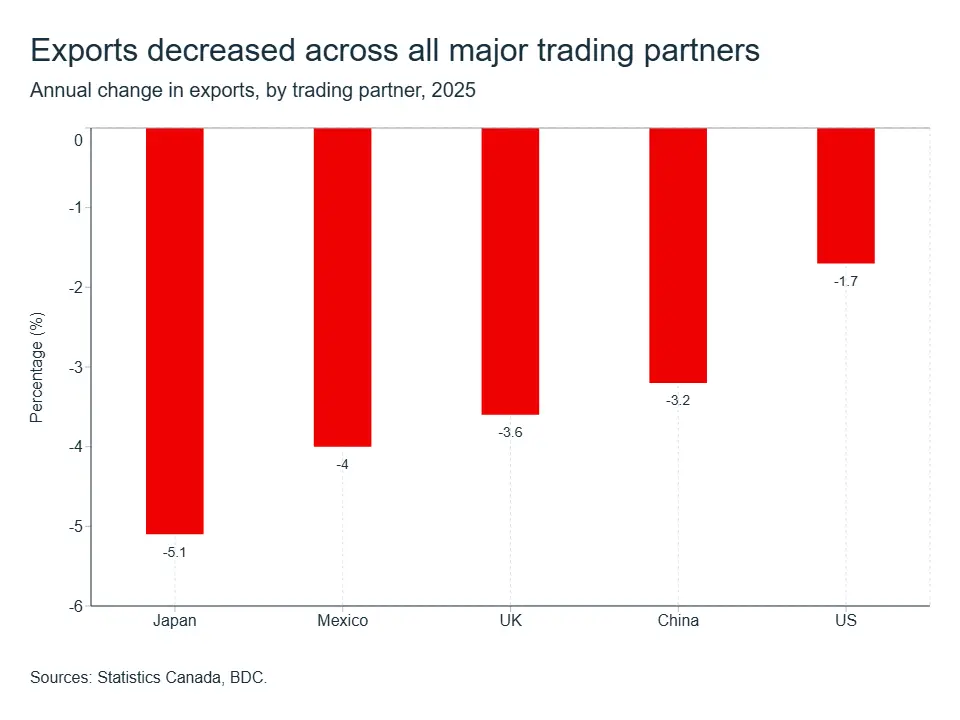

The effects of U.S. and Chinese tariffs continued to weigh on Nova Scotia’s trade. Exports declined with all major trading partners in 2025. And the first quarter remained weak compared to the fourth quarter of 2025.

Employment weakened in the first quarter, with a loss of nearly 3,000 jobs. The number of jobs continued to decline in April, reflecting the pressure that trade tensions are placing on the economy.

However, resilient consumer and government spending are expected to support growth this year. The province remains on track to post growth of about 1.2% in 2026.

New Brunswick

Exports rebounded in the first quarter thanks to a dramatic 58% increase in March. However, unresolved tensions and disputes between Canada and the United States are expected to weigh on trade in the months ahead.

The labour market resumed its decline in April, pushing the unemployment rate up by 0.2 percentage points to 7.2%.

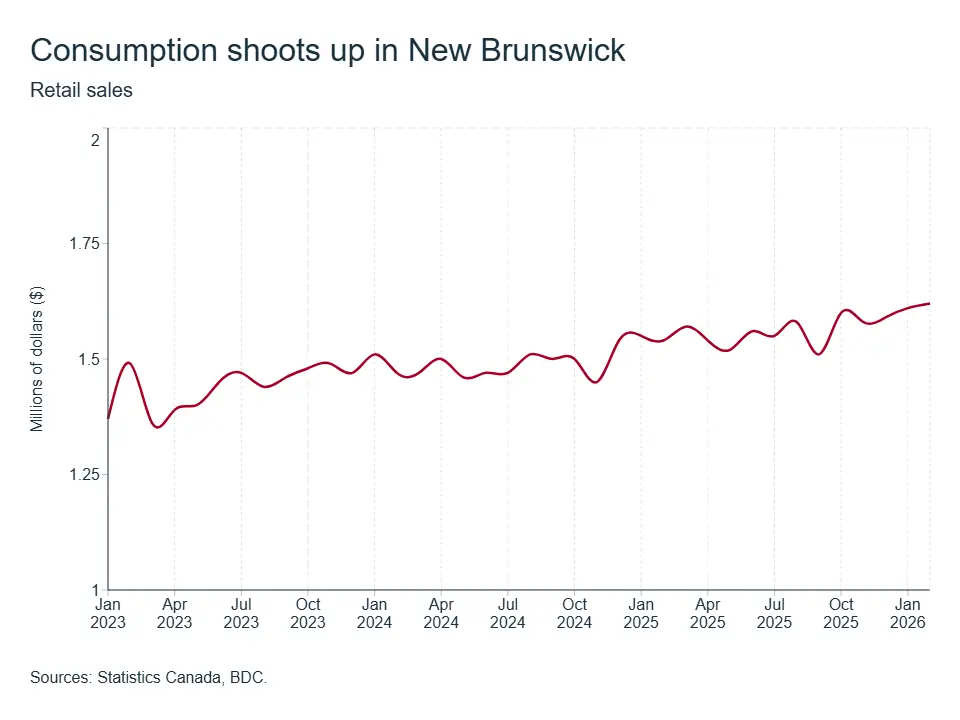

Although employment growth has stalled, overall employment levels remain satisfactory. And the unemployment rate is relatively low. Consumers have continued to support the economy. Retail sales have risen steadily since November.

The province’s economy is projected to grow by 0.9% in 2026, lagging behind its counterparts in the Atlantic region.

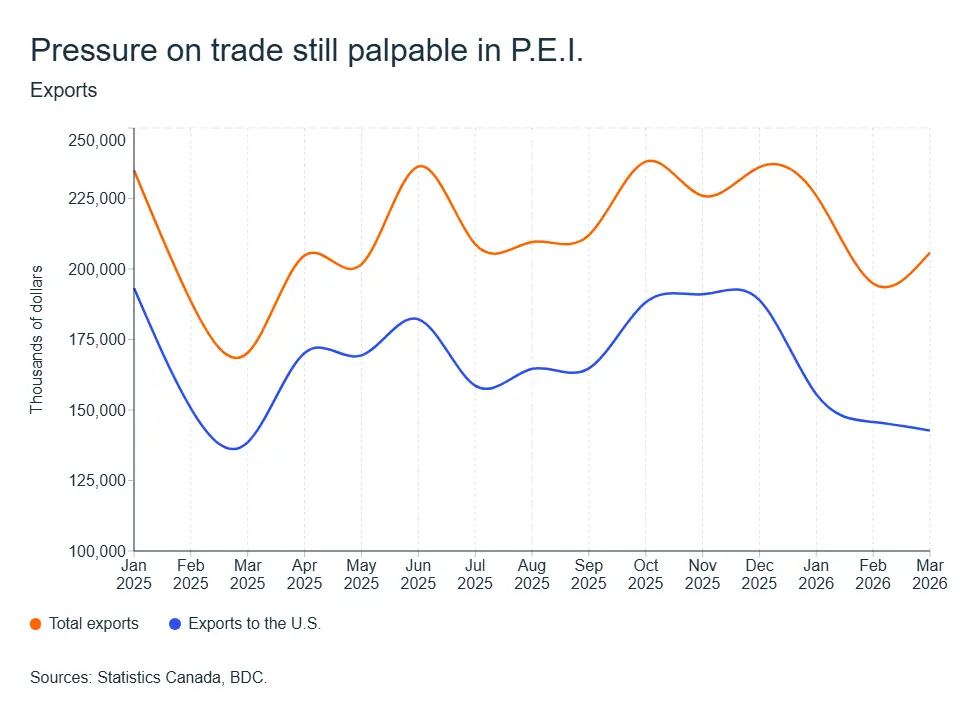

Prince Edward Island

Trade has remained under pressure in the province, with exports to the U.S. declining since the start of the year. An improvement in trade relations with the United States and China will provide much-needed relief to certain sectors of the economy.

While the province lost some jobs in March and again in April, employment levels remained positive for the first four months of the year. The unemployment rate rose slightly to 8.0%. Retail sales continued to rise in the first two months of the year, a sign that households are confident and ready to spend more throughout the year.

Despite ongoing pressure on trade, the province remains on track to grow by 1.2% in 2026, outpacing Canada’s projected growth.

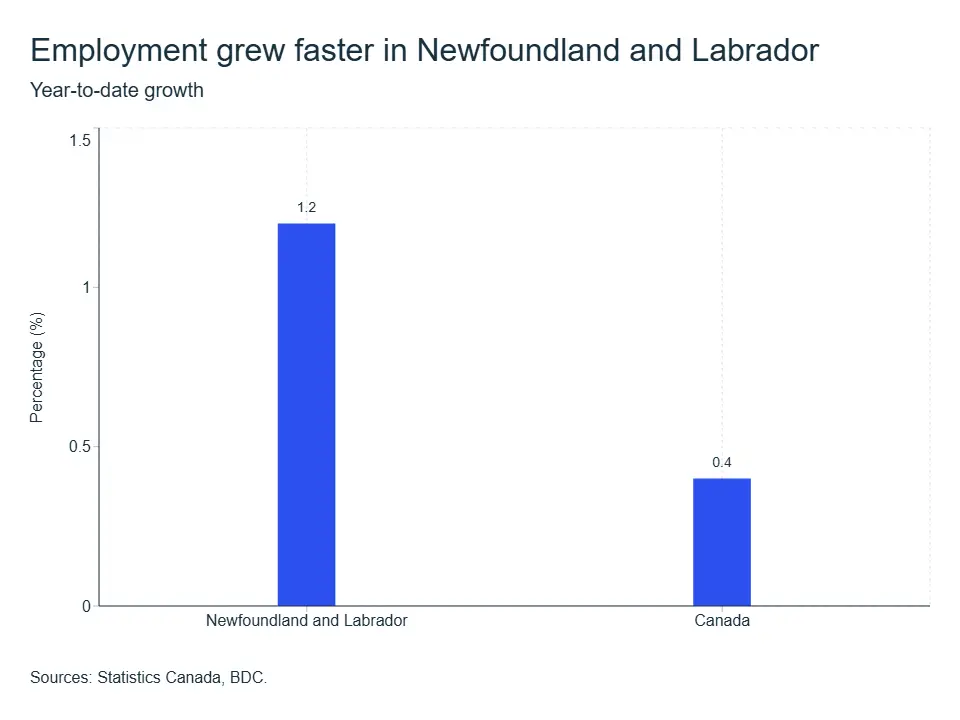

Newfoundland and Labrador

GDP is expected to grow by 1.1% this year, slightly exceeding the national average, thanks to a resilient labour market and successful diversification efforts.

The jobs market saw a slight decline in April, but the overall situation remains positive. Employment has risen by 1.2% since the start of the year, a faster pace than the national average. The healthy labour market is expected to support robust consumer spending this year.

Exports rose by 32% in the first quarter of the year, driven primarily by increased trade with European countries such as France, Germany and Spain. Trade with the United States and China declined in the first quarter, reflecting the ongoing impact of tariffs.

Oil producers continue to benefit from the price surge caused by the conflict with Iran. While negotiations between the United States and Iran continue and a ceasefire has taken effect, upward pressure on prices will persist until a formal agreement is reached and the war ends.