Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreSoaring oil prices: What do they mean for the Canadian economy and entrepreneurs?

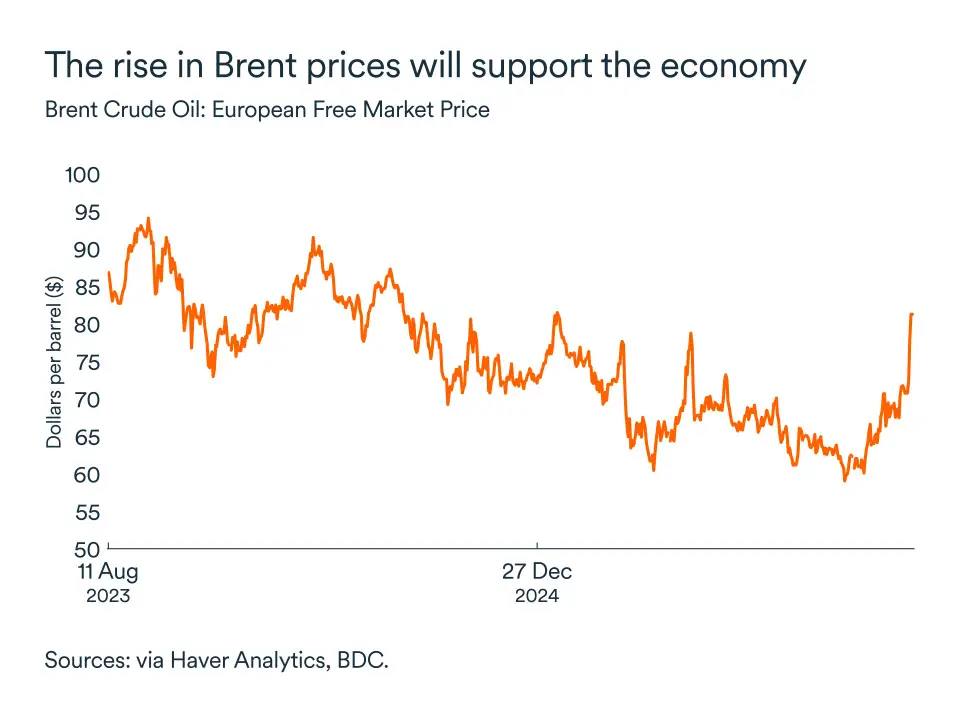

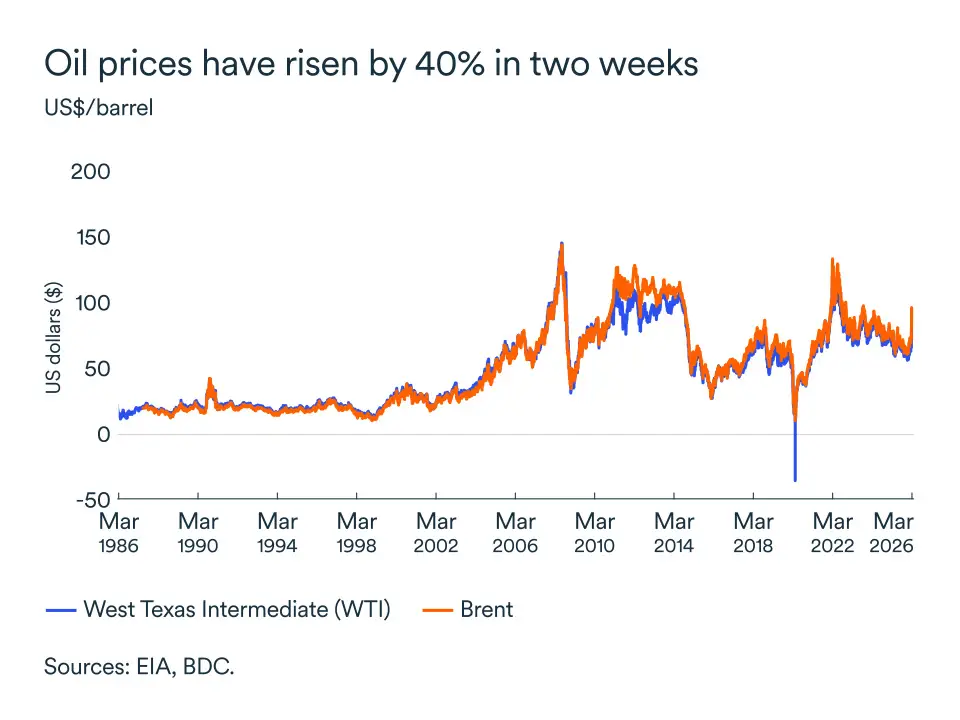

The price of crude oil has surged 40% over the past two weeks, rising from US$65 per barrel at the end of February to nearly US$95 per barrel. In response to Israeli-U.S. strikes that began on February 28, Iran has blocked the Strait of Hormuz—a key oil transit route. This has sent shockwaves through energy markets, with the price even surpassing the US$100 mark.

Prices are not expected to drop anytime soon

Last year, it was estimated that more than 20 million barrels of oil per day passed through the Strait of Hormuz, representing about 20% of the world’s oil supply.

Besides Iranian oil, energy from key member countries of the Organization of the Petroleum Exporting Countries (OPEC), including Saudi Arabia, the United Arab Emirates and Kuwait transit through the strait, destined for such major markets as China, India and Japan.

The price surge is mainly due to the risk of a massive decline in global oil supply. Producers in the region have already cut output by 10 million barrels per day, or about 10% of global production. The conflict has also led to the closing down of several refineries and gas processing facilities for security reasons.

As a result, prices could very well go much higher. When will they peak and at what level? It’s impossible to say.

What is certain is that volatility will persist beyond a ceasefire. Large quantities of oil may remain stranded in the Persian Gulf for weeks, or even months, once the war is over.

Are we heading into a recession?

Volatility in the energy markets has plunged the stock markets into turbulent waters and increased fears of a recession—or worse, the onset of a period of stagflation.

Historically, two of Canada’s last five recessions have been linked to an oil shock. Will the rapid rise in oil prices over such a short period lead to a recession this time? Probably not in Canada.

An oil shock can cause a recession by pushing up inflation and interest rates, and, in turn, depressing consumption and growth.

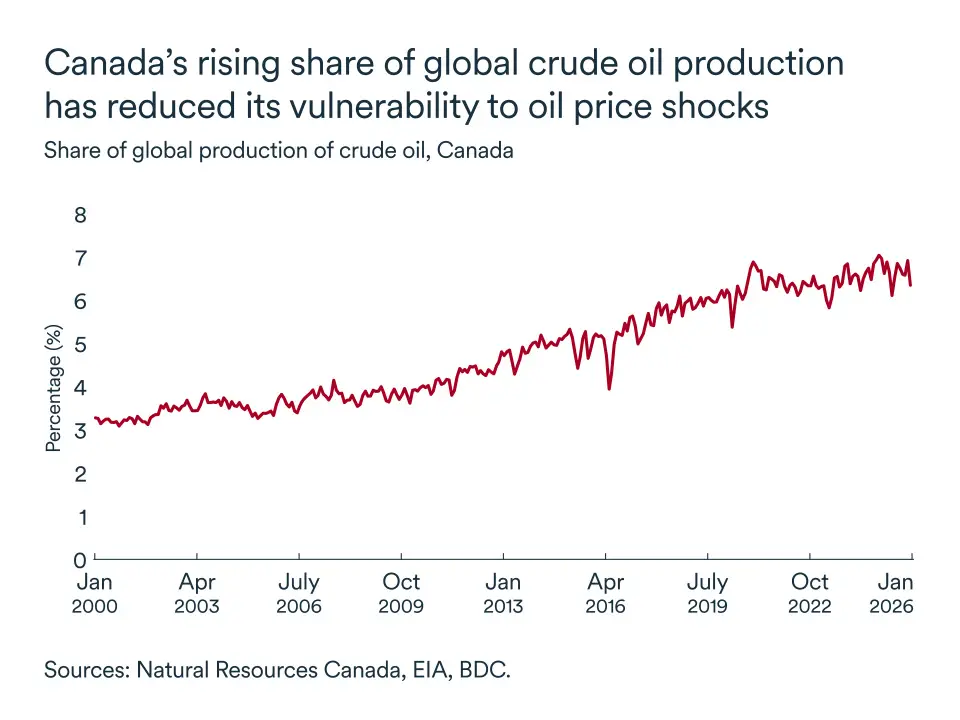

However, the economies of Canada and the United States are much less vulnerable to oil shocks than they were in the 1970s and 1980s.

While our analysis leads us to believe the risk of a recession has increased, we don’t believe one is on the horizon.

Before the conflict with Iran, we were already forecasting modest economic growth. Rising oil prices could further slow the economy, while higher prices at the pump will further limit household spending.

But it’s not all bad news for Canada. The energy sector represents a significant share of the country’s economic activity. Higher prices will benefit Canada’s energy-producing regions, which don’t face the supply constraints currently experienced by their Middle Eastern competitors.

Worse yet, stagflation?

The term stagflation is derived from the combination of stagnation and inflation. It describes a period characterized by high inflation and low (or even negative) growth.

The precise cause of stagflation remains the subject of debate among economists. However, the last two episodes—in 1974–75 and 1978–82—share distinct similarities. They both stemmed from an energy crisis and were preceded by periods of expansionary monetary policy. The latter condition isn’t the case today.

Oil prices would have to remain high for months, not just a few weeks, to have a ripple effect through global supply chains and ultimately lead to higher inflation and stagnant growth in Canada. At this point, we don’t see stagflation as a likely outcome of the Iranian conflict.

So what are the implications for the economy?

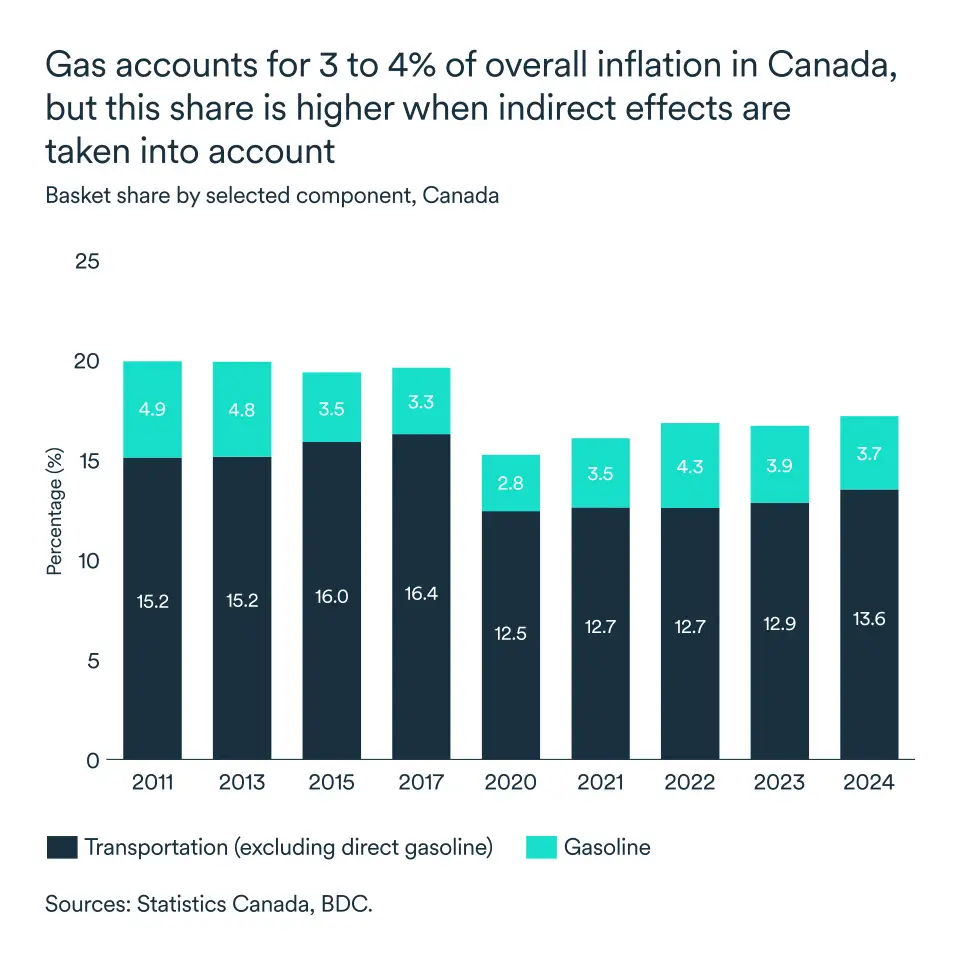

The economy was already slowing when the war started. The rise in energy prices will obviously push up inflation, but we don’t expect it to exceed 3% on a sustained basis in Canada this year.

The decline in purchasing power linked to higher spending on energy is likely to further constrain demand for other types of goods and services and could mitigate partially the effect of higher inflation.

It would be highly surprising to see any action from the Bank of Canada in this context. Our forecast still calls for the key interest rate to remain at 2.25% for the coming months.

However, even without action from central banks on either side of the Canada-U.S. border, we still expect effective interest rates for households and businesses to rise, given the prevailing uncertainty.

In short:

- inflation to increase but not sustainably above 3% in Canada

- the policy rate to remain at 2.25%

- effective interest rates to rise slightly due to the risk premium

- opposing forces on the Canadian currency to limit its volatility against the greenback

- No recession, no stagflation, but slow growth

The impact on businesses

For Canadian entrepreneurs, rising oil prices represent a new headwind to contend with in 2026.

Production costs were already a challenge for many businesses. This will intensify if crude prices remain high for a long period because price shocks will work their way through the production chain.

Meanwhile, rising prices at the pump will reduce household purchasing power, which could further slow demand for your goods and services. For non-energy producers, profit margins will be further squeezed.

In response, focus your efforts on improving profitability by:

- reviewing internal processes to eliminate inefficiencies

- automating repetitive tasks

- outsourcing non-strategic activities

- discontinuing low-margin products or services

- strengthening discipline in managing fixed costs

The Canadian economy remains resilient, but a slowdown is on the horizon

Uncertainty has increased around the world, but Canada’s economy continues to weather challenges and remains resilient in the face of trade tensions and pressure from higher energy prices.

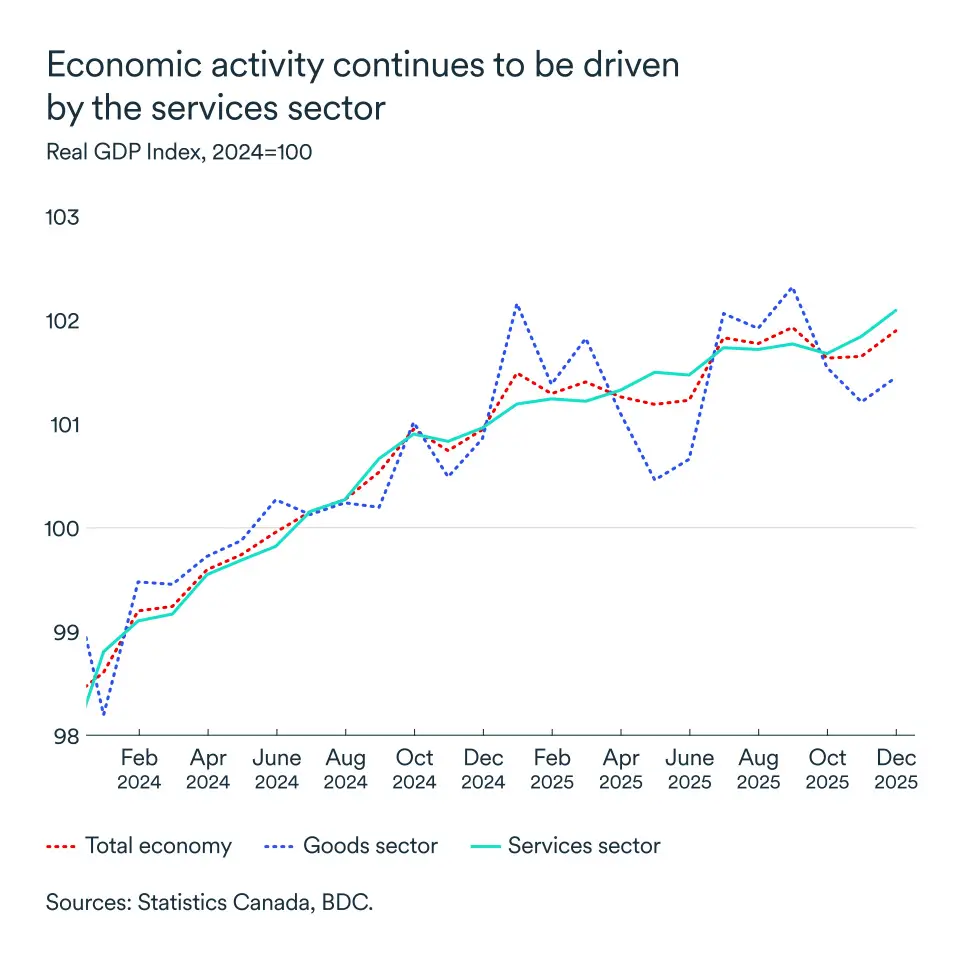

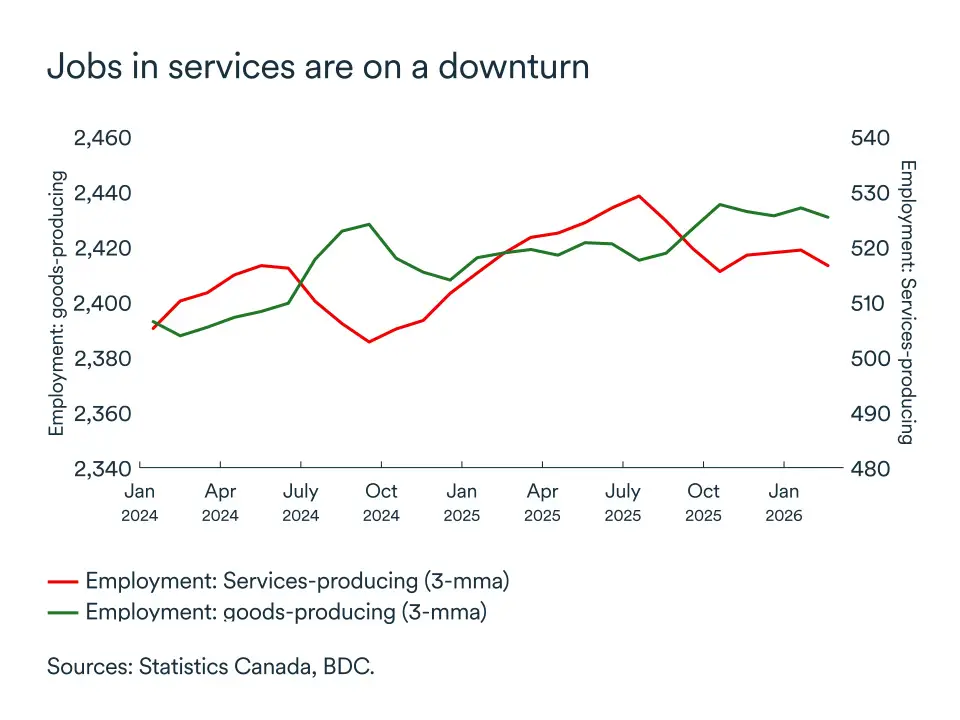

Much of the country’s economic resilience in 2025 can be attributed to the importance of the services sector in the economy.

Service industries held up well in a slowing domestic economy, even as tariffs created uncertainty and volatility in manufacturing and the overall goods sector.

In December, GDP for both the services and goods sectors rose by 0.2% compared to November. That brought Canada’s economic growth for all of 2025 to 1.7%, beating expectations.

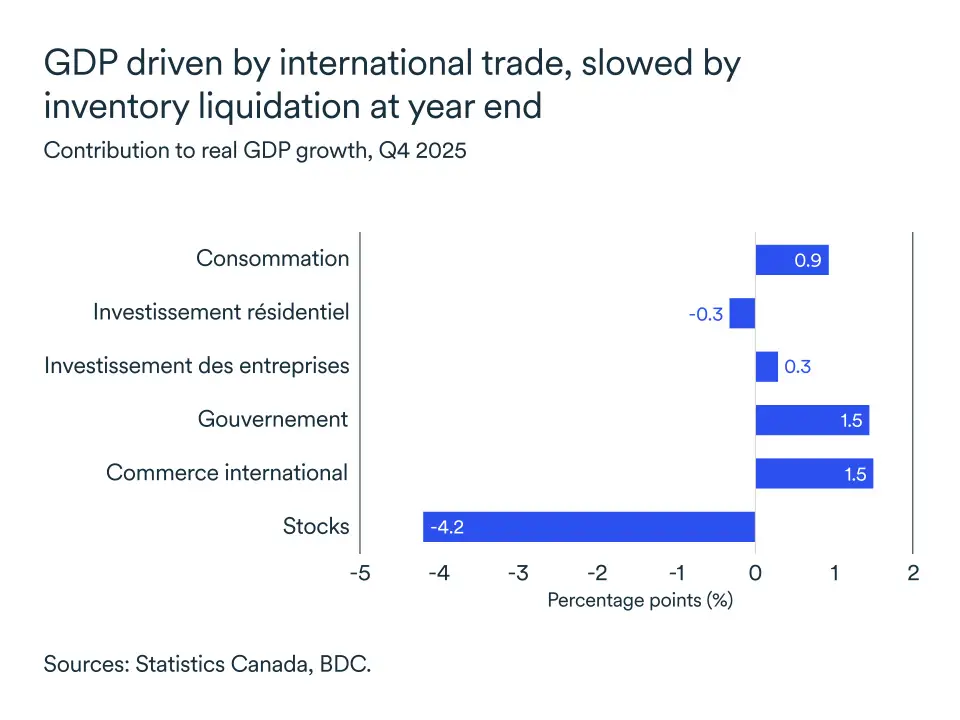

A disappointing final quarter, but it’s not all bad…

While growth in the final quarter declined by 0.6% (annualized rate), the pillars of the economy stood up.

Consumer spending and business investment (excluding residential) both contributed positively to GDP growth.

International trade was also a major and, on the whole, positive factor during the quarter. Exports of goods and services rose by 1.8%, while imports slowed further.

So what explains the decline in GDP? It can be traced to the liquidation of corporate inventories, which translates into a loss of domestic output.

However, it’s important to note that, in the context of the trade tensions during 2025, inventory reductions were more of a technical correction than a harbinger of recession. Many businesses cleared out their warehouses earlier in the year to protect themselves from tariffs. Production could therefore rebound in the coming months, even in the face of more modest demand.

Consumption remains the driver

All signs point to consumption remaining the engine of growth this year. But that engine has slowed, which will keep the country’s growth—and thus your sales outlook—on the modest side.

Inflation in February stood at 1.8%. While well-controlled inflation is welcome, it indicates slowing demand in the economy. Production costs remain under pressure, and companies don’t seem able to pass these increases on to consumers.

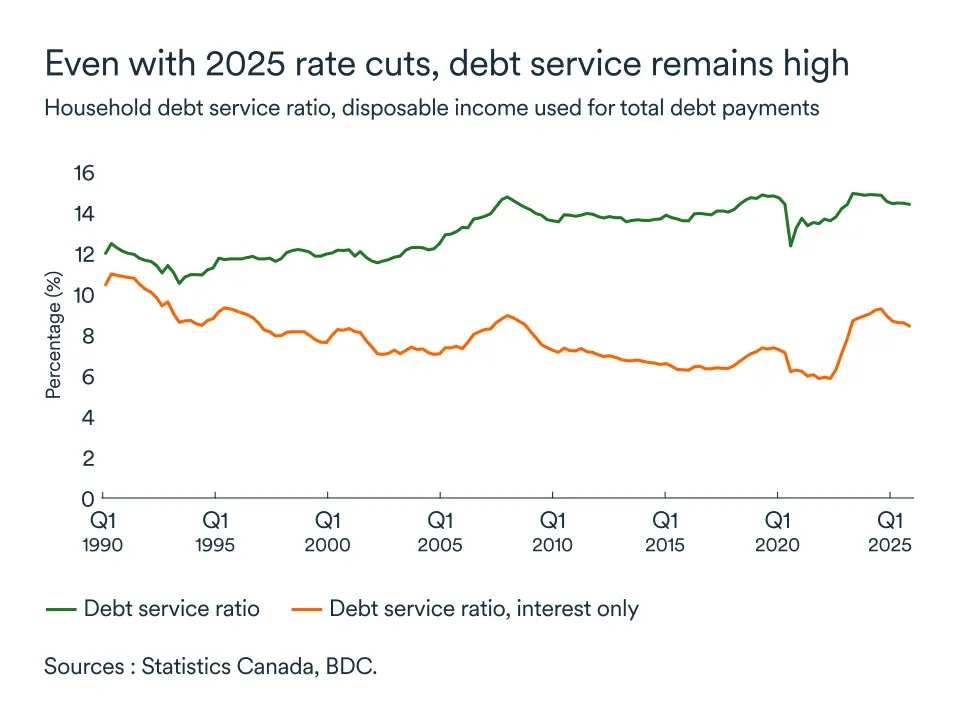

Despite rate cuts by the Bank of Canada in 2025, debt service costs—the portion of household disposable income allocated exclusively to debt repayment—remain high

More importantly, the portion of these payments dedicated exclusively to interest is declining just as slowly. Canadian household budgets are, therefore, still under pressure from high interest rates and debt repayment.

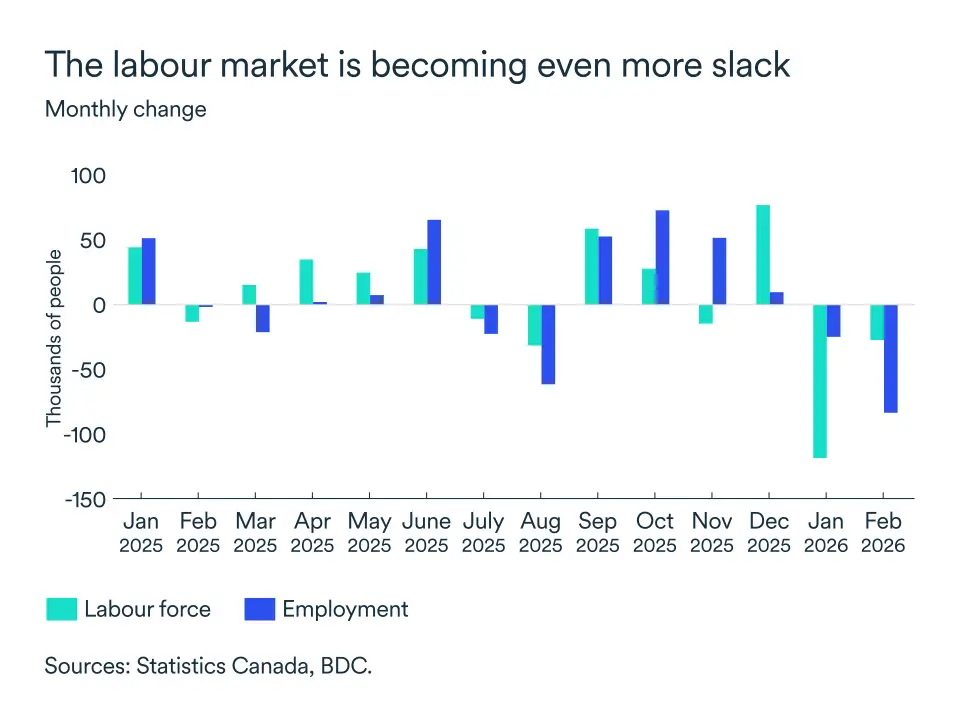

The slowdown hits the labour market hard

A significant employment correction hit the country in February. The 84,000 job losses weren’t only substantial in number but were also widespread across industries—a sign that the growth slowdown is taking hold. The unemployment rate climbed to 6.7%, a 0.2-point increase from January.

The labour market has deteriorated both in terms of the quantity and quality of jobs, with 108,000 fewer full-time positions, and 73,000 job losses in the private sector alone. When employment deteriorates, incomes erode, consumption slows and household confidence is undermined. In short, while one month does not make a trend, this is yet another sign of slowing growth in the Canadian economy.

The Impact on Businesses

- Demand will remain weak, amid income erosion, high debt and a deteriorating labour market, limiting sales despite continued consumer spending.

- Your margins will remain difficult to protect. Costs remain high while your ability to raise prices will be limited by slowing demand. The recent rise in crude oil prices is expected to exacerbate both these trends.

- Managing uncertainty remains paramount. Trade tensions and inventory adjustments are forcing businesses to plan investments and production more cautiously.

British Columbia

The economic outlook for B.C. calls for a GDP increase of 1.2% in 2026. Consumers and businesses, who were under considerable pressure when interest rates cycled higher in 2022-23, have had some relief from rate reductions that occurred in 2024-25.

Employment in February slipped by roughly 20,000 jobs. While both goods and services sectors declined by similar amounts, the level of employment in goods-producing industries has held firm above the average of 2025, whereas services industries have seen employment drop below its summer peak.

Retail sales turned marginally negative in December, slipping 0.6%. Still, retail sales increased 2.6% in 2025, which was among the strongest results in Canada. Consumption fundamentals point to a softer near-term outlook.

Exports from B.C.’s natural gas sector could see gains with the onset of the conflict in Iran, which is leading to shifts in global gas supply chains.

Alberta

Alberta’s economy, which was already on track to grow around 1.8% in 2026, will get a boost from soaring oil prices, positioning it to continue outperforming many other provinces.

Employment was roughly stable in February as the province added 25,400 part-time jobs while losing 17,000 full-time positions. The result was a net loss of less than 2,000. The unemployment rate dropped further to 6.3%.

Retail sales fell in December, the latest month for which data is available. The province encountered the largest monthly decline among Canadian provinces in the period.

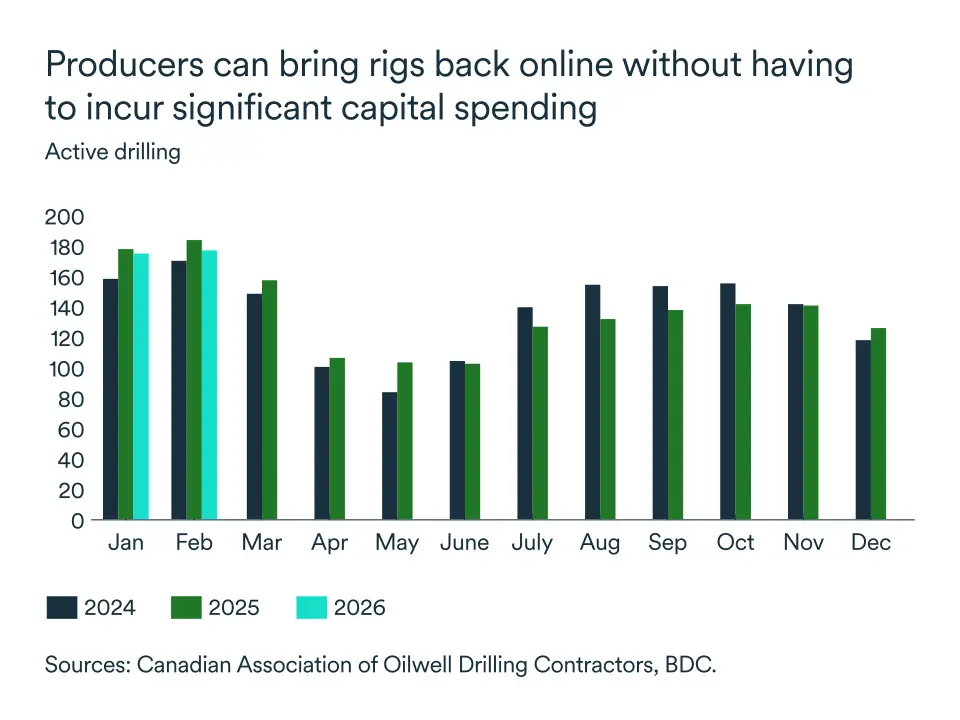

Oil production continues at strong levels. WTI prices rose dramatically to US$95-$100 a barrel at the beginning of March. Although the gap between WTI and WCS, the Canadian benchmark, widened slightly to around US$13.50, the price surge should support Alberta’s economy.

Drilling activity was marginally lower in the first two months of 2026, compared to 2025, signalling modest, but ongoing investment and field operations. As Middle East tensions escalate, Alberta producers are well-positioned to increase production to benefit from recent higher prices.

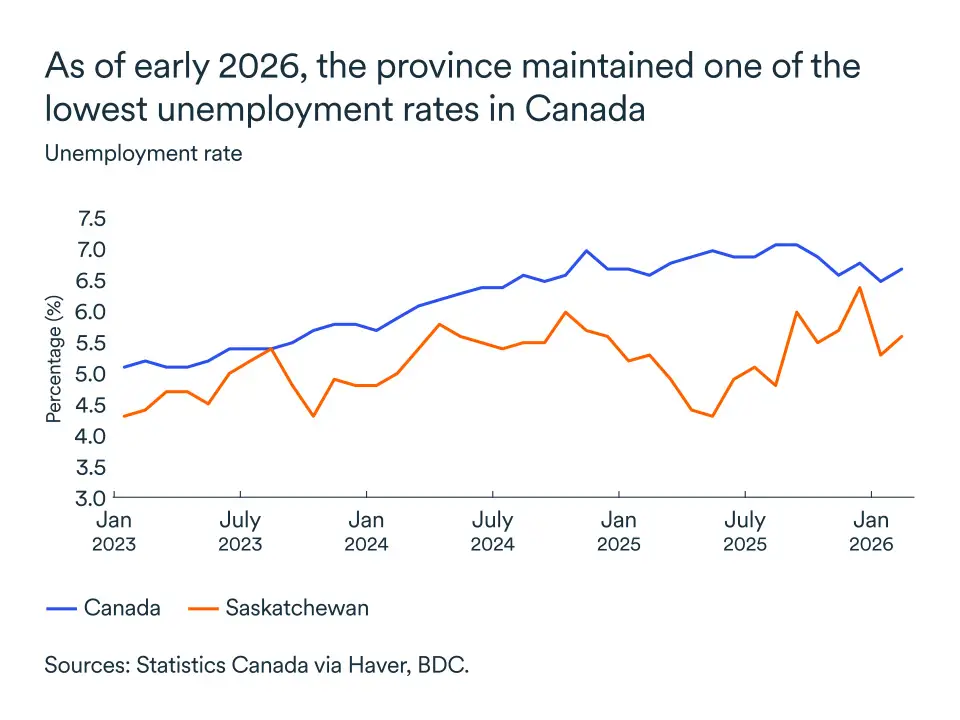

Saskatchewan

Saskatchewan’s economy is projected to grow around 1.7% in 2026, maintaining its position among Canada’s top-performing provinces. In the wake of a Canada-China agreement to lower tariffs on canola and other agricultural goods, we expect momentum to build in Saskatchewan’s economy.

The labour market eased in February with the net loss of 5,500 jobs. Unemployment rate rose to 5.6% but remain among the lowest in the country. Statistics Canada reported that southeast Saskatchewan reported a remarkably low unemployment rate of 2.7%.

Exports should pick up somewhat in the province, thanks to the deal with China. Exports to China dropped by around 40% at the end of 2025.

Manitoba

Manitoba’s economy is forecast to grow modestly by around 1.0% in 2026, on par with the national average.

The Manitoba labour picture was mixed in February. While employment dropped by 4,000 jobs, the unemployment rate declined to 5.7%, a significant 0.6-point decrease from January, attributable to fewer people actively seeking employment.

Manufacturing shipments continue to slow, reaching their lowest level in over two years. Manufacturing sales were down 8 % in January, compared to last year.

The weakness reflected an economic slowdown that hit the province following the imposition of tariffs mainly on agricultural goods. Food manufacturing accounts for almost a third of the province’s total manufacturing sales.

Lower Chinese duties represent a positive development, pointing to a pickup in 2026. However, caution is warranted, given the uncertain trade situation and high energy prices, which could hurt transport costs.

Ontario

Employment stabilized in Ontario in February. Following a big loss of 66,500 jobs in January, the province added 3,300 jobs. However, since this increase was smaller than the growth in the labour force, the unemployment rate rose to 7.6% from 7.3%. These figures confirm a difficult start to 2026 for the Ontario economy.

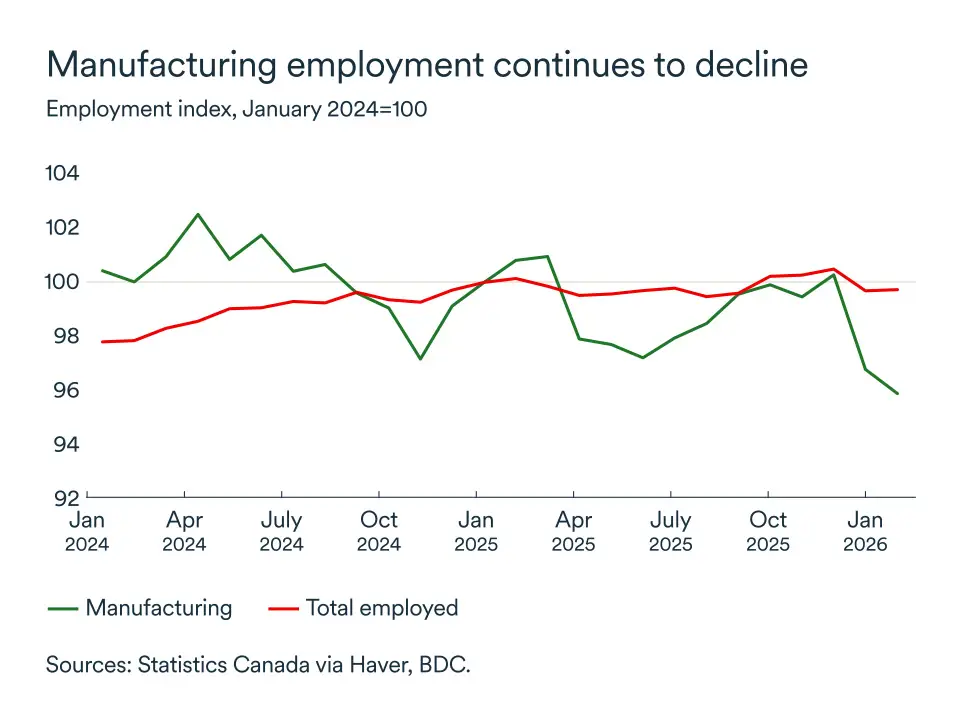

Manufacturing remains under pressure. Employment in the sector declined again in February, bringing total job losses to about 36,800 since the start of the year, completely erasing gains last fall.

The automotive sector has been particularly hard hit. Vehicle exports declined in January and production is down. Part of this decline is due to extended shutdowns at certain plants that are linked to maintenance work and complex adjustments in the context of U.S. tariffs.

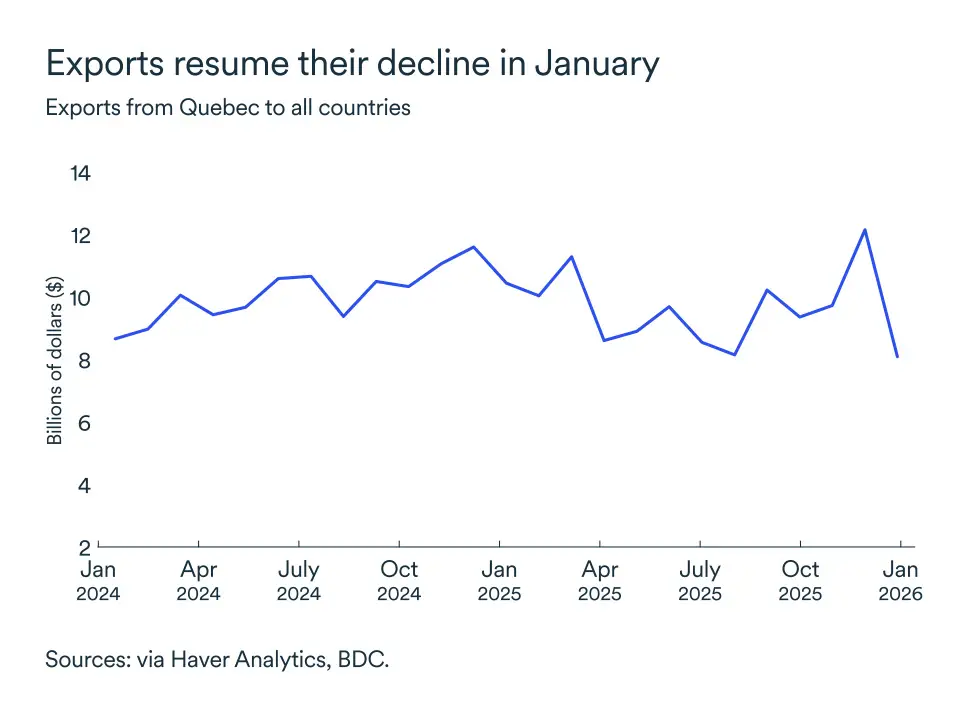

Quebec

Recent data suggest Quebec is off to a weak start to the year. However, we’re waiting for the publication of several indicators that will confirm the province’s economic performance so far this year. We expect the province to grow a modest 0.8% in 2026.

Exports declined in January, after increasing steadily in the last quarter of 2025. While this data doesn’t confirm a trend, it indicates that trade tensions with the U.S. continue to put pressure on the economy.

Employment also struggled in February. The province lost 57,000 jobs, raising the unemployment rate to 5.9% from 5.2% in January. This marks the first significant decline in employment since 2022.

Housing activity was also under pressure. Home sales decreased in both December and January. However, prices remained strong, increasing 5.8% in January versus the same month a year earlier.

Nova Scotia

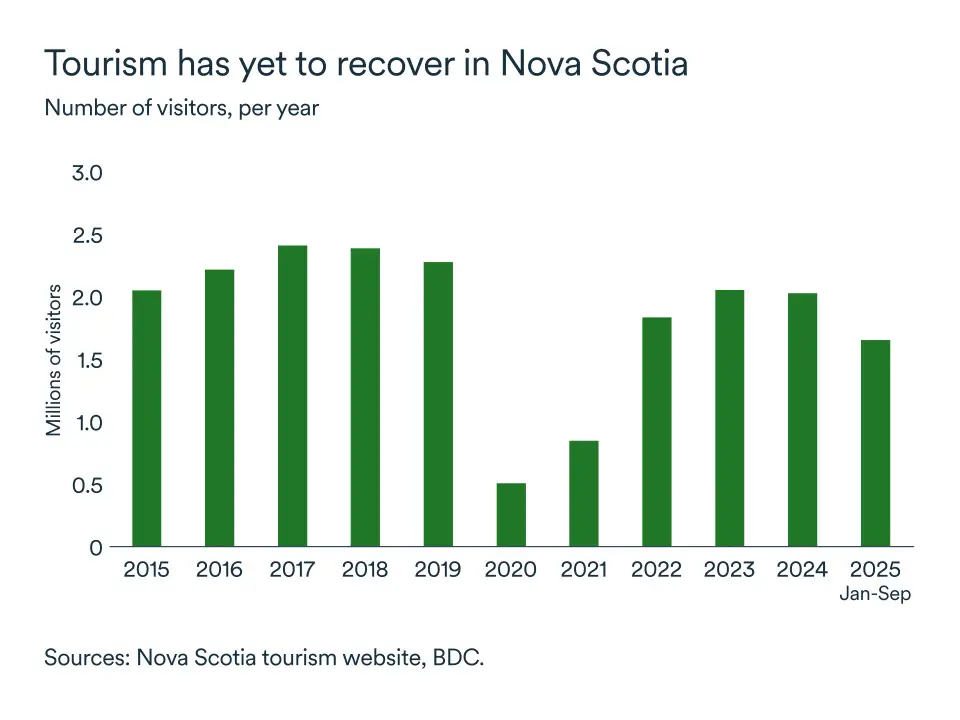

The number of visitors to the province has continued to increase since 2022 and now hovers close to pre-pandemic levels. Given the importance of the tourism sector, the government has put in place a strategy for the next five years to boost the number of visitors year round.

Exports continued to decrease at the start of the year, showing the persistent effects of U.S. and Chinese tariffs on the province.

Employment weakened slightly in February, pushing the unemployment rate to 7.2%. However, employment remained higher than the average level in 2025, and losses in February were much lower than those suffered nationally.

Retail sales growth stayed positive (+3.3%) in 2025 as employment stabilized. While choppy performance is expected to continue, trade talks with China should boost trade and retail trade. The province is on track to grow around 1.2% in 2026, slightly exceeding the national average.

New Brunswick

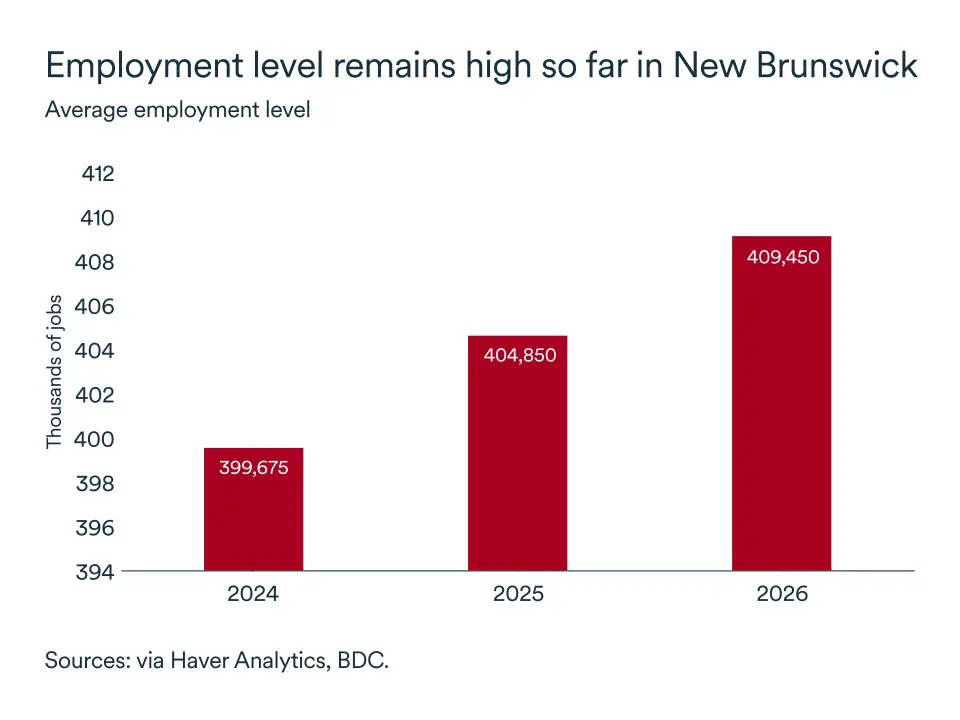

Exports remained under pressure in New Brunswick, declining significantly at the start of the year (-11%). Continued trade weakness is expected to keep the manufacturing sector under pressure. Flat employment figures in manufacturing also indicate continued weakness.

The job market softened slightly in February with most losses coming in the transportation and warehousing sector, as well as in accommodation and food services. However, the employment level remains relatively high, keeping the economy on solid footing despite recent declines.

Retail sales increased by a decent 4.8% in 2025. A stable labour market will support consumer spending this year. The province’s economy is expected to grow 0.9% in 2026, lagging its peers in the Atlantic.

Prince Edward Island

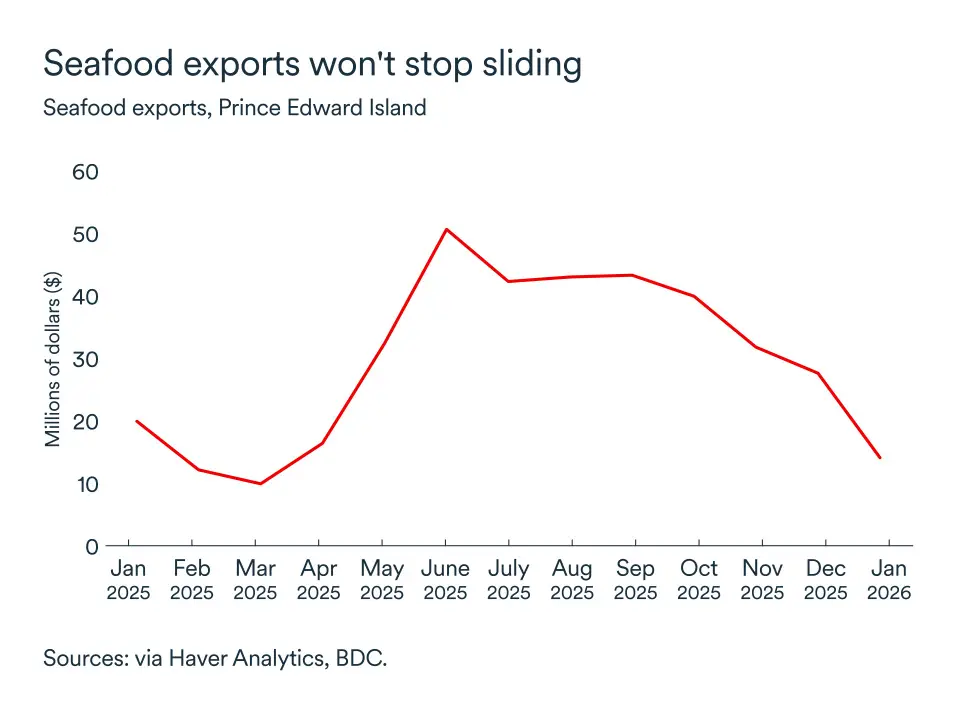

Tariffs from China and the U.S. kept exports under pressure in the province. The sharpest decline was seen in seafood exports. However, the island remains on track to grow 1.2% in 2026.

The job market was strong in 2025 and started this year on a solid footing, with two months of job gains. The unemployment rate dropped to 7.2% in February, down from 7.9% in same period last year.

Consumers continued to spend despite trade tensions. While retail sales were choppy in 2025, they still increased by 2.9%. Faster population growth and a resilient job market should support consumer spending this year, as well as housing activity in the province.

Newfoundland and Labrador

The Middle East war has driven oil prices to new highs. They are expected to drop sharply once the conflict is resolved, but, in the meantime, oil producers in the province will benefit.

The job market strengthened in February, adding 2,100 jobs. This marks the second consecutive month of job gains.

Consumers slowly increased their spending in the last months of 2025, with total retail sales increasing by 3.8% on average in 2025. Positive numbers in the job market will continue to ease pressure on households and support consumer spending. GDP is expected to grow 1.1% this year, slightly outperforming the national average.