Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreGold volatility: What it says about the economy...and what it means for Canadian entrepreneurs

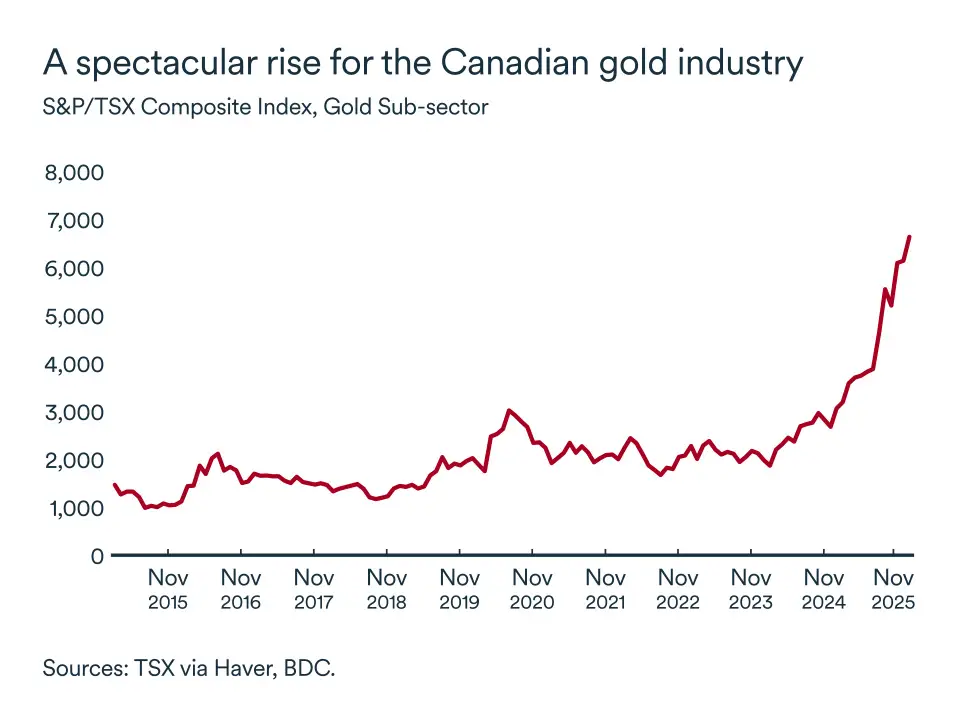

In recent months, the price of gold has been on a wild run. In January, it reached an all-time high of over US$5,500 per ounce before falling sharply—by about 10%—in a single session, its biggest daily drop since 1983. Over the past six months, the price surged more than 40%, while the last few weeks saw a correction of around 15% to 20%. In short, gold is going through a period of exceptional volatility—movements that speak volumes about the state of the global economy and the business environment for Canadian entrepreneurs.

A signal to watch

Gold is often perceived as a safe-haven asset, but its role goes far beyond this traditional image. Historically, rapid increases in the price of gold have reflected a more uncertain economic climate.

Four main factors explain gold volatility.

- Economic uncertainty, which drives investors to seek safe havens. .

- Geopolitical tensions, including regional conflicts, trade tensions or diplomatic rifts.

- Changes in monetary policy, particularly those affecting real interest rates and their anticipated direction.

- Increased volatility in financial markets, which encourages investors to turn to assets perceived as more stable.

While stock markets have performed very well in recent years, fears of a correction are growing. This has pushed investors to diversify their asset mix. In addition, many central banks have sold off their gold reserves, which has also contributed to the price volatility.

In general, when the economic system sends signals of nervousness, gold reacts—sometimes violently. The recent price surge reflects a global context marked by multiple risks: prolonged monetary tightening in the U.S. in particular, recurring geopolitical tensions, trade fragmentation and political uncertainty.

A strategic indicator for Canada

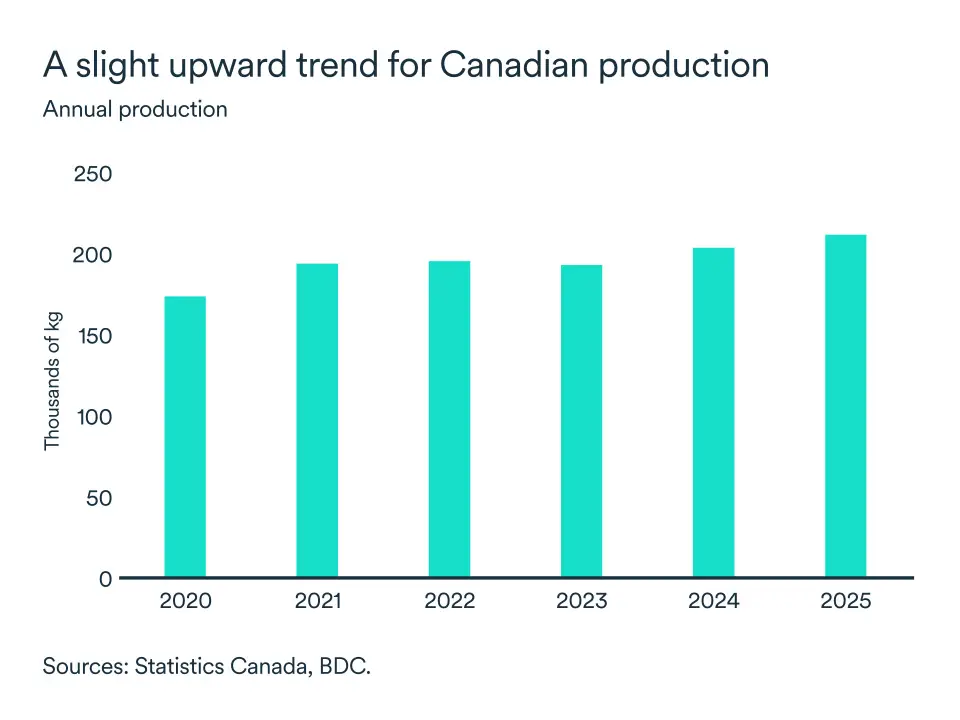

Canada is one of the world's five largest gold producers. This strategic position makes gold not only an important export, but also a key economic driver for several regions.

While Ontario dominates Canadian production, followed by Quebec and British Columbia, the rest of the country accounts for 20%. This meaning the industry is well spread across country, and the sector is growing thanks to rising gold production.

In many communities, mining (not just gold) is an essential economic pillar, generating investment, well-paid jobs, benefits for local suppliers, infrastructure development and more.

Unlike stocks, bonds or other financial assets, gold is also a physical input in several sectors, including electronics and advanced technologies, jewelry, medical equipment, aeronautics and other specialized industries. This means that price fluctuations are not only reflected in investors' portfolios, but also in the production costs of certain manufacturers.

Thus, fluctuations in the price of gold have concrete repercussions on entire regions.

A risk for the country's trade balance and the Canadian dollar

Given Canada’s position as a major gold producer, sustained increases in the metal’s price tend to favour a higher Canadian dollar. This is largely due to improved terms of trade and increased investor interest in Canadian dollar-denominated assets.

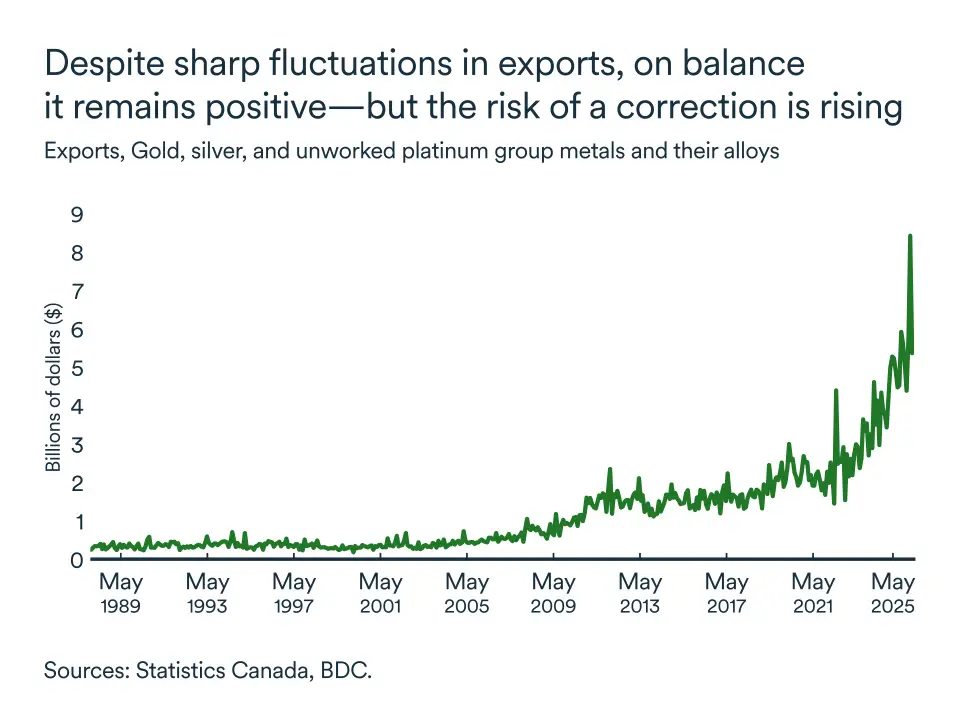

Major movements in the gold market also have a significant impact on Canada’s trade balance. Fluctuations in the market and international demand for gold add a layer of volatility to our exports.

Statistics Canada reported that exports of metal and non-metal mineral products fell by nearly 25% in November, despite gold prices continuing to climb. The gold sector carries enough weight in Canada's export structure to drag down total exports.

For entrepreneurs, this relationship has important implications.

Do you export? A stronger dollar reduces your competitiveness in foreign markets because your products become relatively more expensive for your international customers. Margins can be squeezed and volumes affected—especially in sectors where competition is international and prices are more rigid.

Do you import? Conversely, a stronger currency means that your imported inputs, equipment or technology cost less. This can provide a window of opportunity to renew your equipment, secure input stocks, negotiate supply contracts or bring forward investments planned for later in the year.

Gold and the perception of wealth

As with the stock markets, fluctuations in the price of gold sometimes influence the perceived wealth of certain households, particularly those that hold gold assets or financial products that depend on them.

While direct gold holdings by individuals are typically low, gold is often included in diversified investment portfolios. Periods of sharp increases, such as those seen recently, can support household consumption, while rapid corrections can have the opposite effect.

Thus, the impact of gold prices is felt across the Canadian economy in several ways. Even if your business doesn’t buy or sell gold, its price can influence your business environment.

What entrepreneurs need to remember

The current fluctuations in gold are a reminder of the ongoing uncertainties in the global economy.

Essentially, for businesses, the price of gold is a valuable barometer, but it does not tell the whole story. Tracking its price is a bit like checking the weather before you go out. It tells you what kind of climate to expect—especially in certain parts of Canada.

But price fluctuations often create confusion and hesitation. For businesses, it's important to look beyond the current noise.

- Strengthen your risk management and assess your exposure to exchange rates. Consider hedging strategies if your margins depend on imports or exports.

- Maintain strong cash flow. In a volatile environment, financial discipline is essential to remaining agile.

- Take advantage of windows of opportunity. Fluctuations in international demand can reveal new markets or segments.

A year of transition for the Canadian economy

The Canadian economy entered 2026 in a period of transition. After a year marked by unusual volatility—uneven growth, trade pressures, labour market adjustments—the signals emerging today point to a single conclusion: Growth is slowing. However, the economy remains resilient, buoyed by significant adjustments by both businesses and workers.

For entrepreneurs, this means navigating an environment that hasn’t yet returned to equilibrium, but which now offers more clarity than a few months ago.

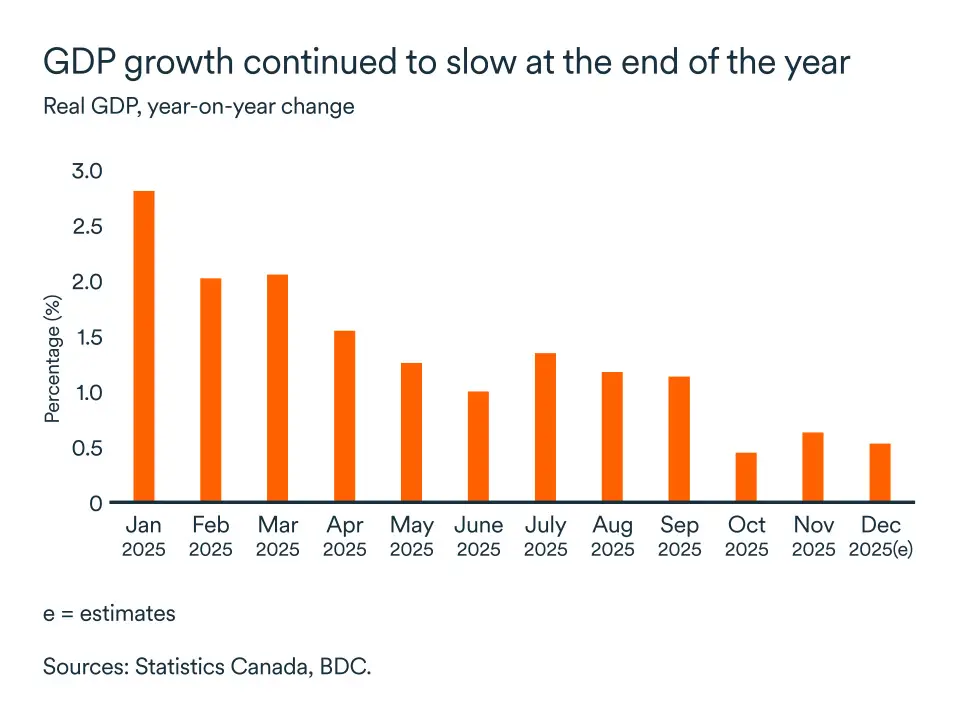

Growth is slowing but remains positive

After a notable acceleration in the third quarter of 2025 (+2.6%), economic activity plateaued at the end of the year. Fourth-quarter GDP growth came in at close to zero, or even slightly negative, according to preliminary estimates.

Moreover, growth slowed gradually through the year. For 2025 as a whole, the economy grew by 1.2%, a modest pace that is below potential.

However, this slowdown doesn’t signal a deeper downturn. Traditional drivers—consumption, residential investment, certain service industries—continue to contribute, but with less momentum. The economy continues to rebalance as it deals with the U.S. tariffs imposed a year ago.

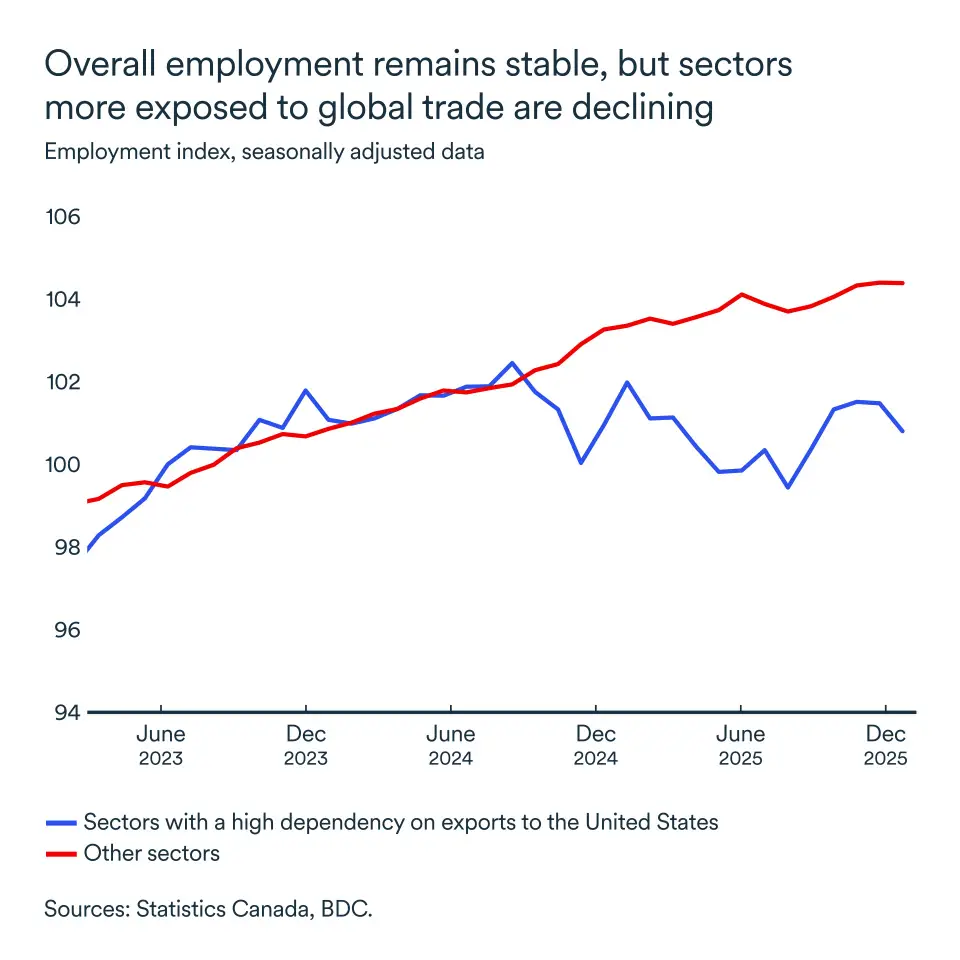

Towards stabilization for the most exposed sectors?

In sectors that are highly dependent on international trade and are particularly exposed to tariffs, employment had stabilized in 2025, but at a level below that seen before the trade crisis began.

After sharp declines recorded following the imposition of new tariffs, employment was no longer falling —which is in itself a sign of adaptation—but it was not rebounding either. January labour reports showed yet another correction in these sectors after four consecutive months of increases.

Exporting businesses continue to grapple with uncertain trade conditions, even though several tariffs have been postponed (by the U.S. for a year starting in January) or reduced (by China starting in March). Stabilization reflects producers’ gradual adjustment, likely not from tariff changes this time around but from softer demand.

Fewer jobs created and lower unemployment

At first glance, January's employment data may seem paradoxical: Job creation declined slightly (-25,000), but the unemployment rate also fell (-0.3 per cent).

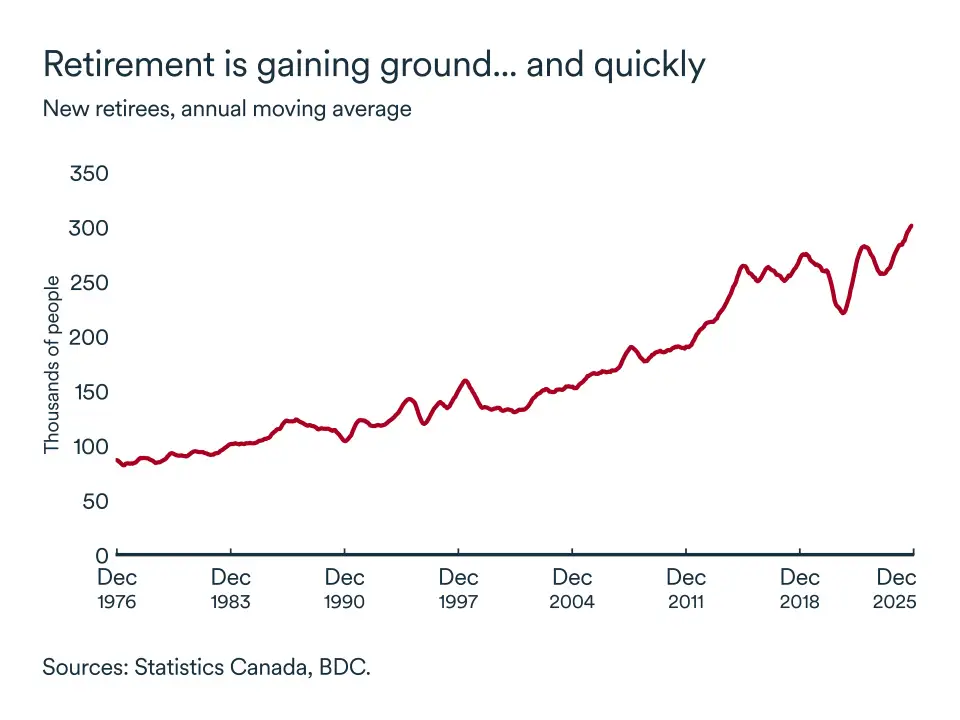

This reflects one of the most important structural changes affecting the Canadian economy. While demand for goods and services is slowing, the supply of workers is also declining, due to lower population growth and accelerating retirements.

This explains why the labour market remains surprisingly resilient despite a sluggish economy. It helps mitigate rising unemployment when the economy slows but also creates additional challenges for businesses—persistent pressure on recruitment and workforce management.

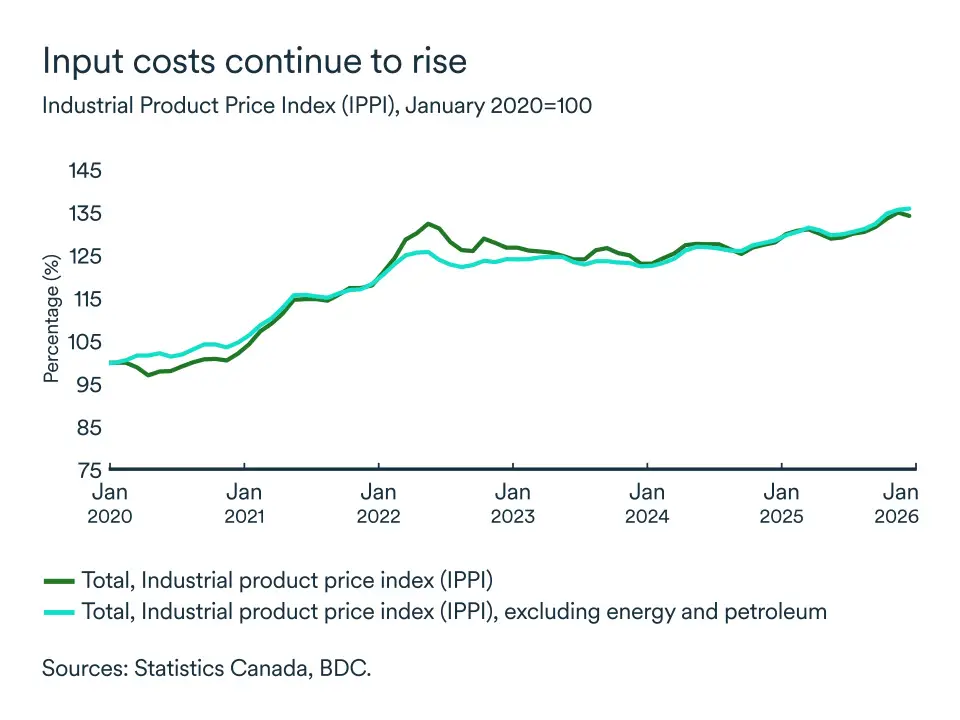

Continued cost pressure

Input costs continued to rise for most businesses. Excluding energy, industrial product prices rose 5.8% in 2025.

In many supply chains, businesses are essentially price takers, meaning they have little bargaining power or influence over prices. Although price pressure is growing less rapidly today than at the height of the post-pandemic inflation crisis, input costs remain a major issue for businesses, squeezing profit margins.

Unfortunately, the Canadian economy will not rebound quickly, but it continues to show remarkable resilience. And for businesses willing to adapt, this transition period can become an opportunity to forge ahead. Key strategic decisions will count more than ever in outpacing slower competitors.

Focusing on efficiency, reviewing investment priorities, strengthening risk management practices and remaining attentive to macroeconomic signals will be essential for positioning your company for growth.

The impact on your business

- Economic growth is moderating. This means demand will be more predictable but less dynamic. Now is a good time to review your forecasts and optimize your investment plans accordingly.

- Once again this year, expect stronger competition and tighter margins. Diversification of markets and suppliers is becoming essential.

- The decline in the size of the working population due to retirements and lower immigration levels will keep the pressure on your HR practices. Recruitment could be more difficult, despite the slowdown. This highlights the increased importance of worker retention and training within companies, but also, in the longer term, of reducing dependence on workers.

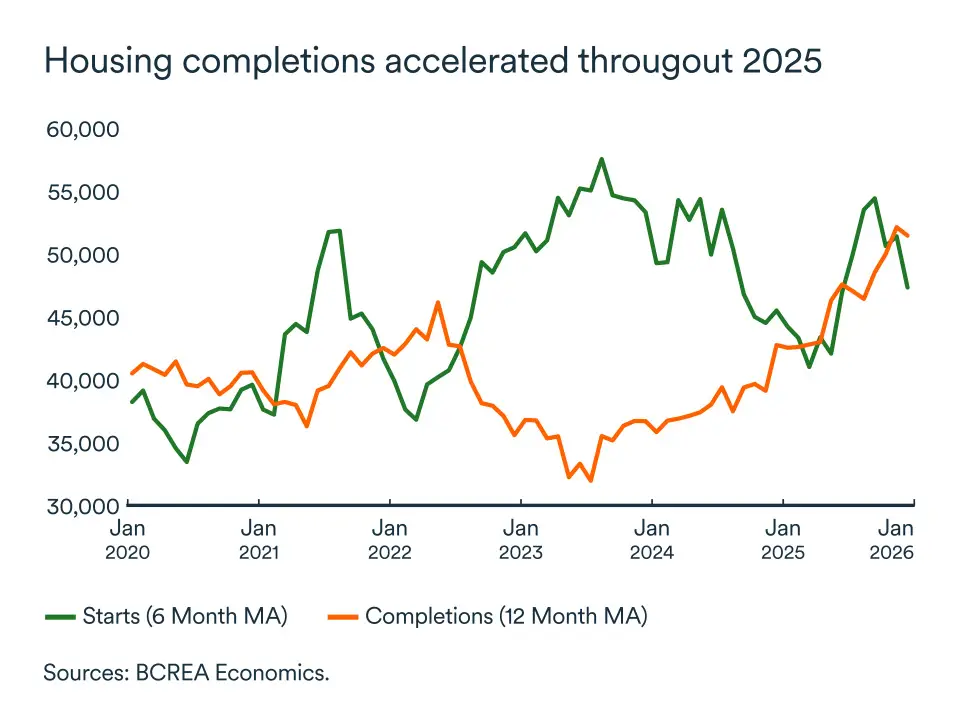

British Columbia

The B.C. economy strengthened in 2025. Real GDP growth accelerated to an estimated 1.2%, which was above the national average and well-above the sluggish pace of 2024. Still, real GDP growth remained below the province’s 10-year average of 2.8%.

Residential construction was a key driver of growth, with housing completions hitting their highest level since the pandemic. Meanwhile, consumer spending remained remarkably robust, with retail sales growing 6.3% through October. That was the strongest inflation-adjusted increase of any province, as weaker interest rates provided relief to debt-strapped households.

Employment in B.C. slipped slightly in December, but the province still created 24,000 jobs in 2025. Nevertheless, the unemployment rate increased to 6.4% as the number of people joining the labour force outpaced job creation.

Alberta

Alberta’s economy is still on track to grow around 1.8% in 2026, outperforming most provinces.

Employment surged back in January as the province turned into Canada’s primary engine of job creation over the first month of the new year. The unemployment rate went down to 6.4%. Momentum continues to be strong for Alberta’s labour market. Retail sales also climbed according to most recent data in November on the back of population growth.

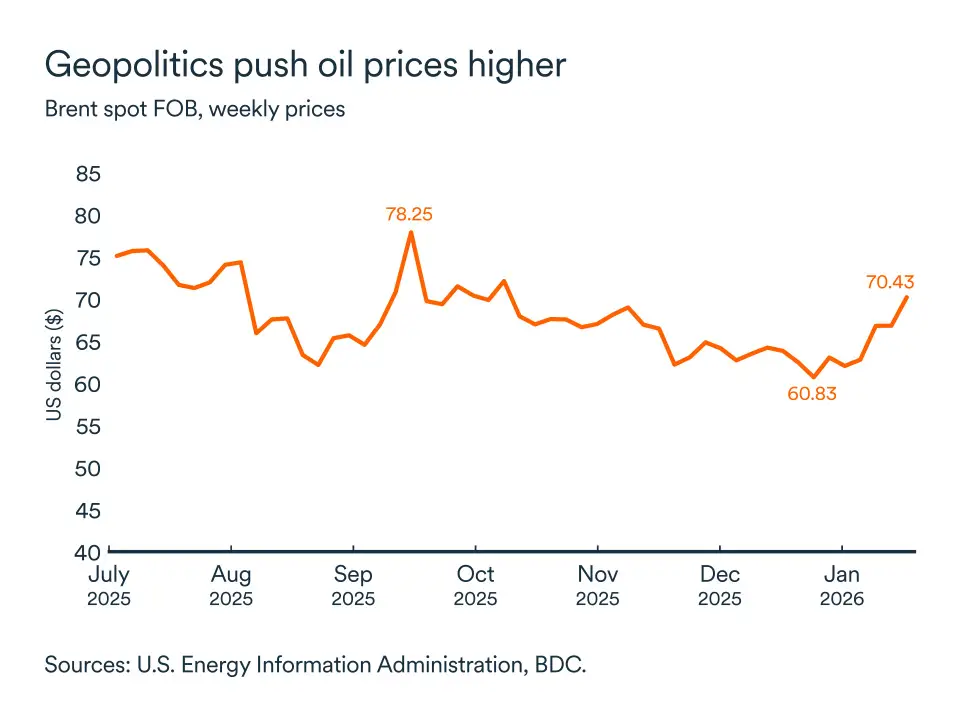

Oil production continues at historically impressive levels. WTI prices picked up closer to US$63-65 a barrel at the beginning of the month and the gap with the WCS stuck to US$11.5.

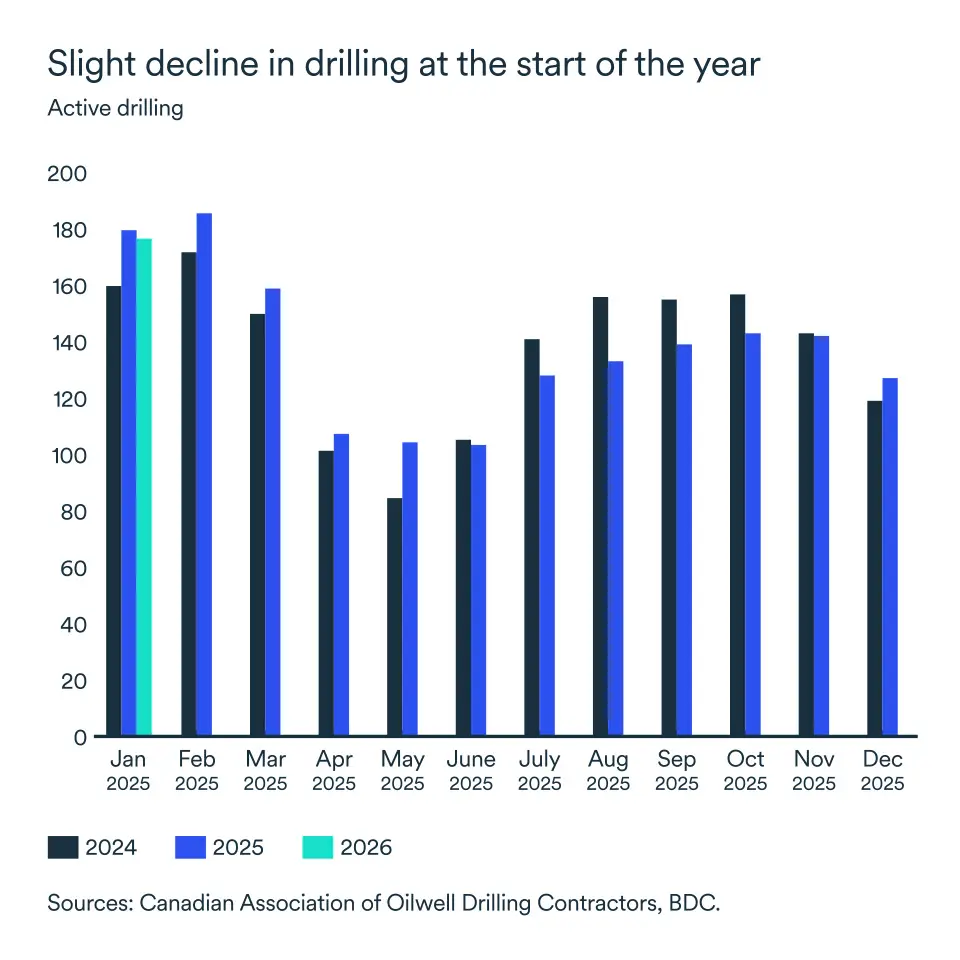

Drilling activities were marginally lower in January compared to last year, with 178 active rigs in Alberta, signalling modest, but ongoing investment and field operations as uncertainty for the sector’s future likely gathered steam amid Venezuela’s turmoil.

Saskatchewan

Saskatchewan’s economy is projected to grow around 1.7% in 2026, maintaining its position among Canada’s top-performing provinces. A Canada-China agreement to lower tariffs on canola and other agricultural goods will be a boon for the province’s economy in 2026.

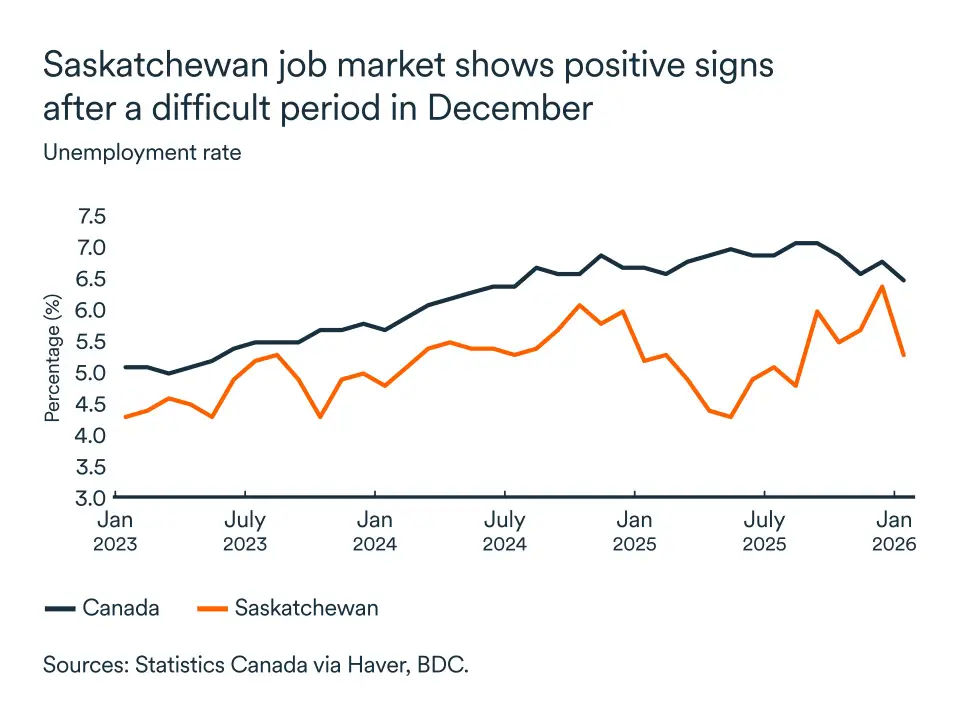

The labour market improved markedly in January with the addition of 15,000 jobs. Unemployment fell to 5.3% from 6.4% in December. This gave Saskatchewan the second-lowest unemployment rate in the country.

Retail sales growth remained positive, but a slowdown continued at year-end. The recent progress in trade talks with China, and improvement in the labour market, should help the province’s retail sector regain steam.

In January, Canadian Energy Metals Corp. released a preliminary economic assessment of its Thor critical metals project near Tisdale, northeast of Saskatoon. While mining is not imminent, this type of major project will generate optimism for the province and create some early positive economic impacts.

Manitoba

Manitoba’s economy is forecast to grow modestly by around 1.0% in 2026, an upward revision following the Canada-China trade agreement in early January.

Manitoba’s retail sales recovered some lost ground in November.

The labour market took a hit in January. While employment was flat, the unemployment rate jumped to 6.3%, a significant 0.6 point increase from December.

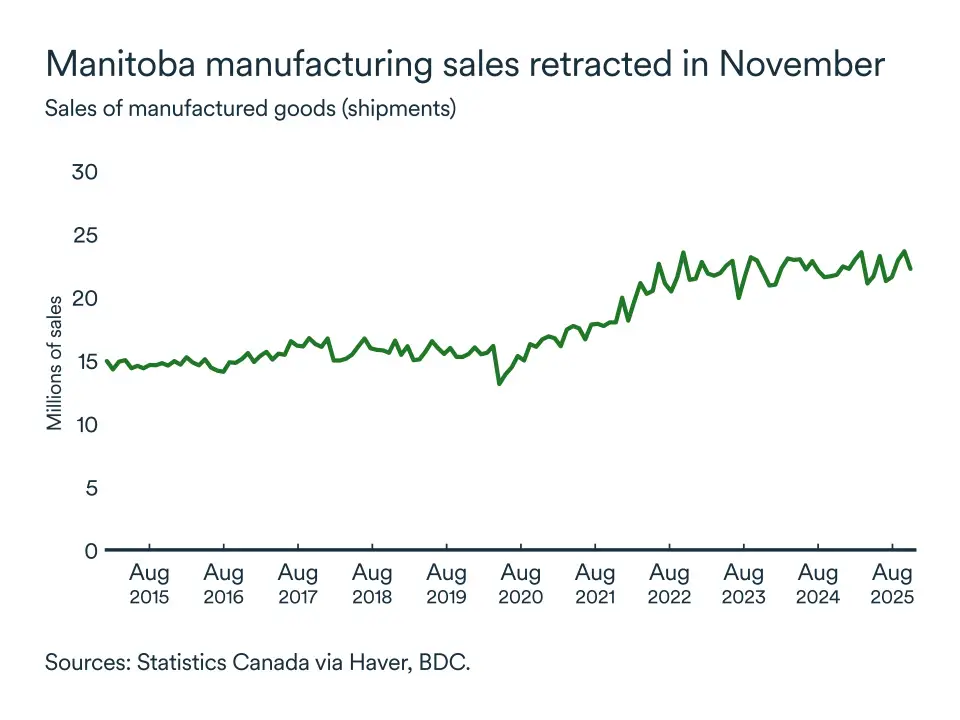

On the industrial side, manufacturing shipments fell nearly 6% in November compared to October. The deterioration reflected an economic slowdown that hit the province following the imposition of tariffs on agricultural goods.

Recent developments point to a pickup in 2026, but caution is warranted, given the uncertain trade situation. For 2025, manufacturing shipments were likely flat.

Manitoba, although well-diversified, is more sensitive to domestic economic fluctuations. Interprovincial barriers are expected to continue to come down in 2026, which will support growth in Manitoba, which relies heavily on internal trade.

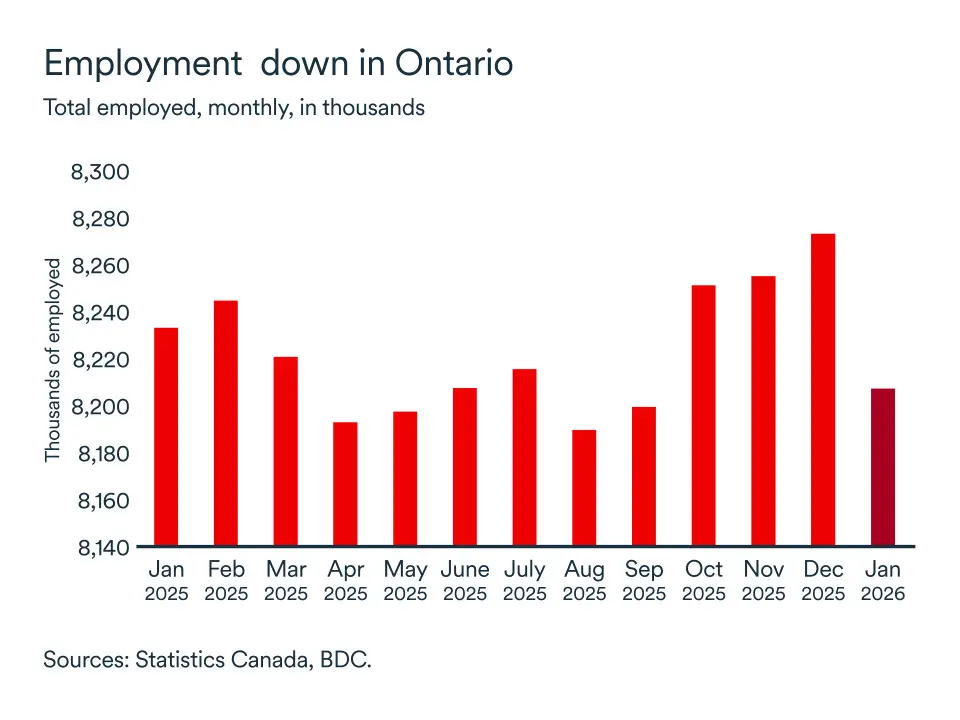

Ontario

Ontario's economy lost 66,500 jobs in January. The losses contrast with the strong employment performance recorded in the second half of 2025.

Several sectors were affected by job losses, but manufacturing experienced the worst drop. Recent layoffs at a GM plant show that tariffs continue to have a negative impact on the automotive sector.

Meanwhile, the housing market remains weak, particularly in the Greater Toronto Area. Excess inventory and slowing population growth are hurting housing starts in the province.

Our latest SME survey indicated that Ontario companies were slightly less optimistic at the start of the year.

Tariffs imposed by the United States, and uncertainty surrounding the renegotiation of the CUSMA free trade agreement, continue to weigh on growth in Ontario. Still, we expect Ontario's economy to experience positive growth in 2026, but it will be modest.

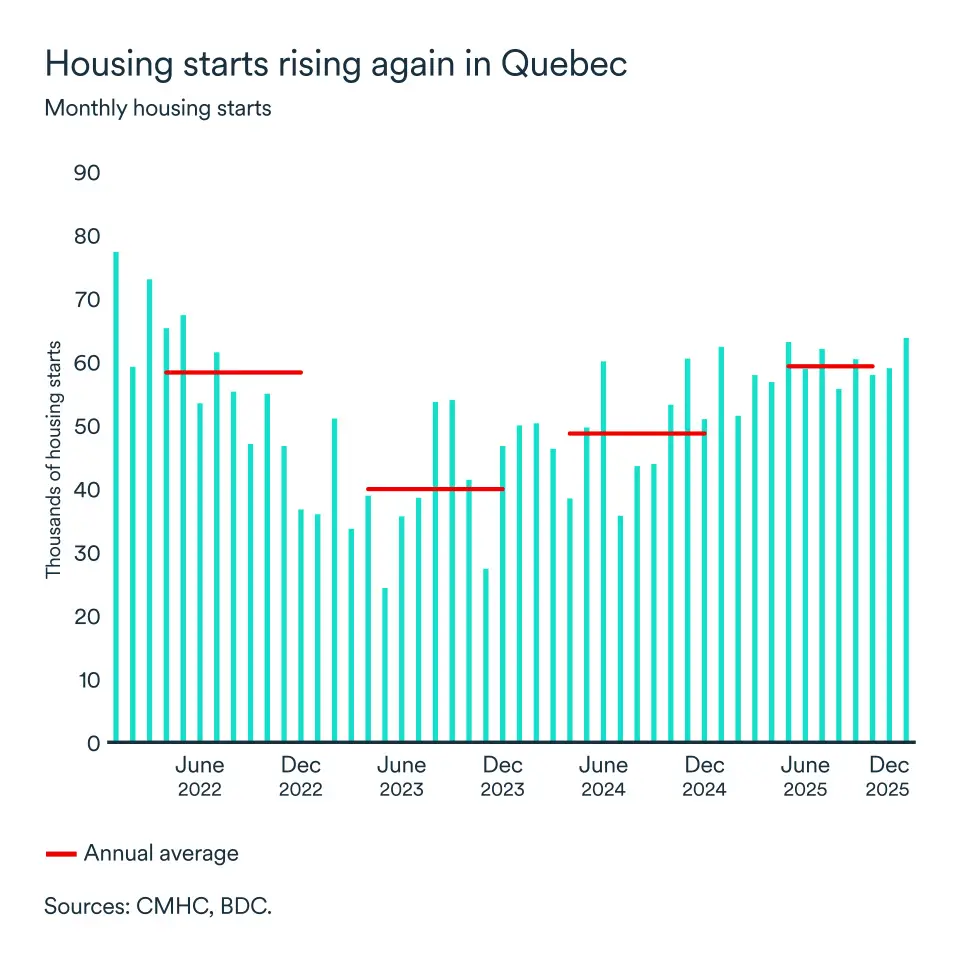

Quebec

Following two years of slow homebuilding, housing starts are rising in Quebec, reflecting a favourable environment for residential construction, despite slower population growth. Building, especially of rental units, has been stimulated by a combination of strong rent increases in 2025 and relatively lower construction costs.

While employment in Canada was down by 25,000 in January, Quebec started the year on a solid footing, adding 3,700 jobs. The unemployment rate remained low at 5.2% in January.

Trade tensions with the U.S. remain a concern. Recent data indicate export levels continue to be below their pre-tariff period. Goods targeted by U.S. tariffs saw the steepest declines, ranging from 23.4% in steel and 6% in aluminum in the first ten months of the year.

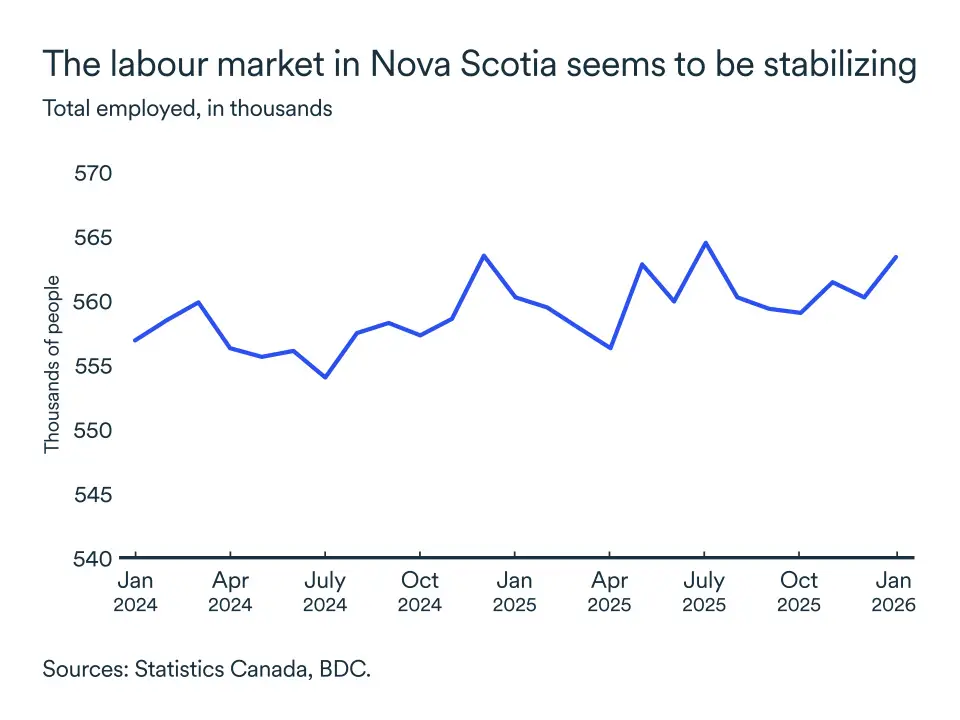

Nova Scotia

Total exports were flat in 2025, but a strong performance in computer and electronics production helped support total manufacturing sales. They increased 2.6% from January through November, compared with the previous year.

The labour market added 3,200 jobs in January, signalling employment stabilization.

Retail sales increased by 3.5% from January to November. With a continued recovery in employment, consumers are expected to continue spending in 2026.

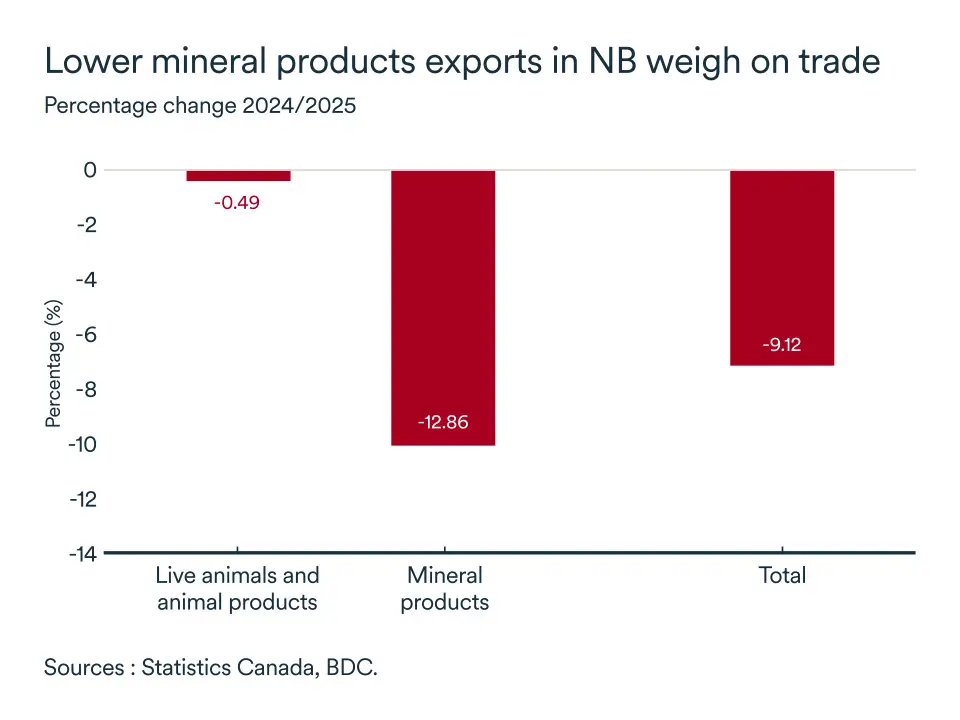

New Brunswick

Exports remained under pressure in New Brunswick, dragged down by mineral products. Weakness in trade directly impacted the manufacturing sector, where sales were down 6.5% in 2025.

The job market added 2,100 positions in January, starting the year on the right foot. Most of the gains were full-time jobs, adding a positive element to the increase in employment in the month.

Retail sales increased by a decent 5.0% from January to November. Continued strength in the labour market will support consumer spending this year.

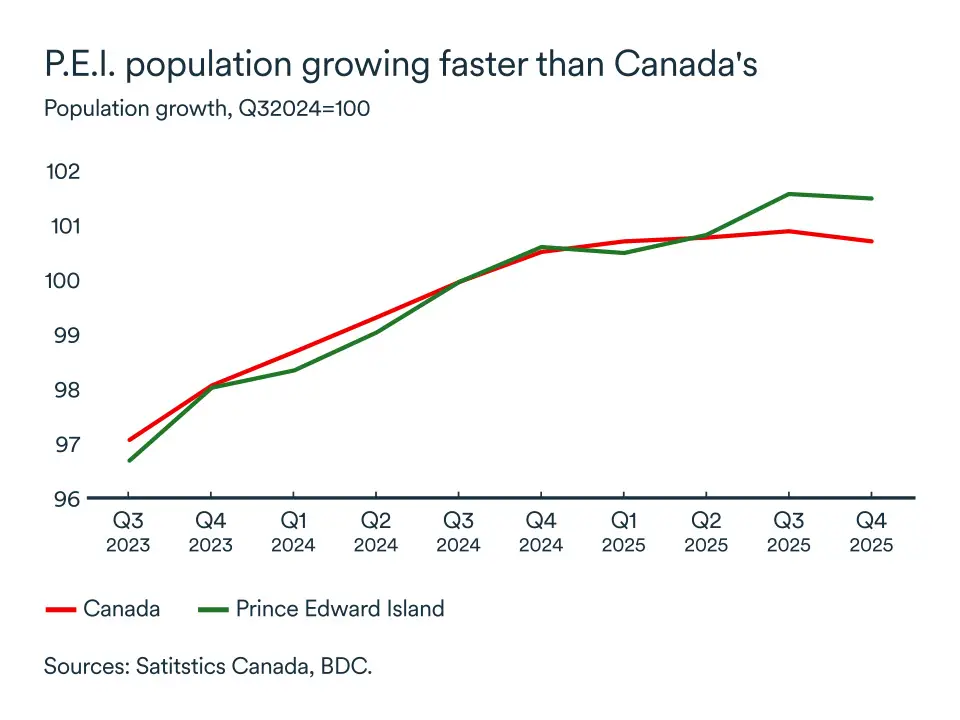

Prince Edward Island

Despite tariffs on seafood and tensions between Canada and the U.S., the island managed to stay resilient. The job market was strong in 2025 and started the year on a solid footing.

The island continued to attract newcomers in 2025. Population growth was faster in P.E.I. than in Canada as a whole. This should support demand for goods and services, as well as homes in the province.

Consumers continued to spend despite trade tensions. While retail sales were choppy in 2025, they stayed higher than 2024 levels. Households on the island should continue to spend as labour market conditions stabilize.

Newfoundland and Labrador

Geopolitical tensions in South America and the Middle East have put upward pressure on oil prices. A recent surge in prices is expected to continue as long as tensions in the Middle East remain elevated. However, fundamentals should cap oil prices because supply still exceeds demand.

Following a drop in employment at the end of 2025, the job market regained strength in January, adding 3,800 jobs. While we wait to see if the upward trend continues, this was welcome news at the start of the year.

Consumers slowly increased their spending in the last months of 2025, signalling a regain in confidence. Further improvements in the job market would stimulate consumer spending in the coming months.