Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreA year that promises to be eventful

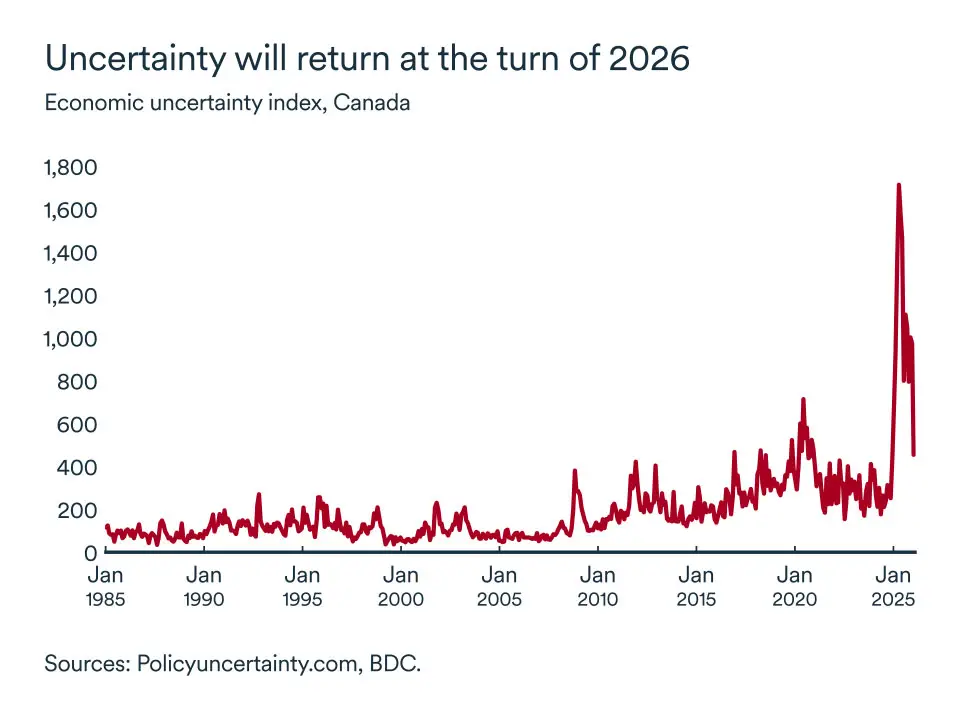

In the last edition of the Monthly Economic Letter, we shared our economic outlook for the coming year. This time, we zero in on three key trends that will affect Canadian businesses and make for an eventful 2026.

These long-standing forces are shaping the economy now more than ever: geopolitical uncertainty, demographic change and the rapid rise of AI. They will have a tangible impact on businesses over the next 12 months. With our outlook for 2026 being for positive but modest growth, businesses should take these trends into account in their strategy to better position themselves for long-term growth.

Geopolitical uncertainty

Tariffs and trade took centre stage in 2025—and they will be right there again in 2026.

As part of the mandatory review of the Canada-United States-Mexico Agreement (CUSMA), preliminary discussions between Canada and the United States will begin in mid-January. Although many U.S. tariffs were introduced in 2025 and the average level of tariffs increased significantly, to date, it remains at a manageable 5.9%. That’s because nearly 90% of exports are still protected by the CUSMA.

Some tariff increases that were scheduled to take effect in January have been postponed until January 2027. This is the case for certain wood products, including upholstered furniture, kitchen cabinets and vanity units. That’s providing a welcome respite for the affected industries, of course, but also a measure of optimism for the trade talks ahead.

Still, recent international geopolitical upheavals are reigniting uncertainty around the world and could complicate the CUSMA review that is scheduled to formally start in July.

Despite trade tensions and geopolitical uncertainty, some recent developments offer reason for optimism for entrepreneurs. Internationally, communication channels between Canada and China have reopened. At home, businesses operating nationally will benefit from simplified interprovincial trade. These developments don’t eliminate the risk of future setbacks, but they could provide help for businesses seeking to stabilize their operations and plan for growth.

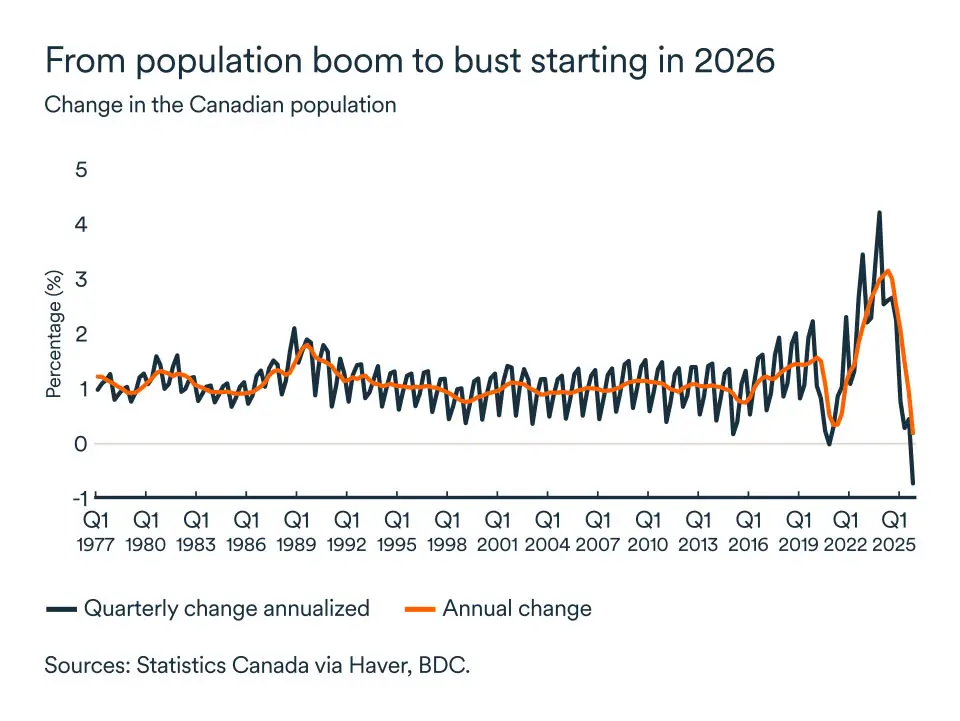

Demographic change

It's no secret that Canada is aging—and fast. What does this mean in concrete terms? First, a declining employment rate, despite ongoing job creation. In the 1970s, there were eight Canadians of working age for every person aged 65 and over. Today, that figure is closer to three, despite strong population growth in recent years, which has tempered the effect.

Ultimately, this means that there will be fewer potential workers (relative to retirees) to stimulate economic activity and fund social programs.

These demographic changes are already having a tangible impact on Canadian businesses, and the pressure will intensify in the long (and short) term.

- Labour shortages: While uncertainty has slowed economic growth, many businesses are still struggling to find staff, whether due to regional worker shortages or the type of skills required. Businesses grappling with this problem are more likely to experience slower growth, be less competitive and see a deterioration in the quality of their products and services. Even if your business is not directly affected by a labour shortage, the issue is driving up overall wage costs. Businesses can reduce their dependence on labour by adopting new technologies and by automating tasks.

- Business transitions: It’s not only employees who are aging but also business owners. That represents a major challenge for the viability of many small and medium-sized businesses and Canada’s economic vitality. Business transfers are critical for maintaining jobs and expertise in the country. But they also represent opportunities for growth through acquisitions. Buying a company gives a business access to a pool of new talent, client lists and service offerings that enhance and complement its current activities.

- Consumer demographics: As a general rule, spending slows after individuals reach a certain age. The aging of the Canadian population will, therefore, lead to a slowdown in demand for goods and services. Some sectors will fare better than others. Among the obvious winners are sectors such as healthcare, pharmaceuticals and accessibility solutions for aging at home. New retirees, ages 65-74, are big consumers of tourism but demand drops after age 75.

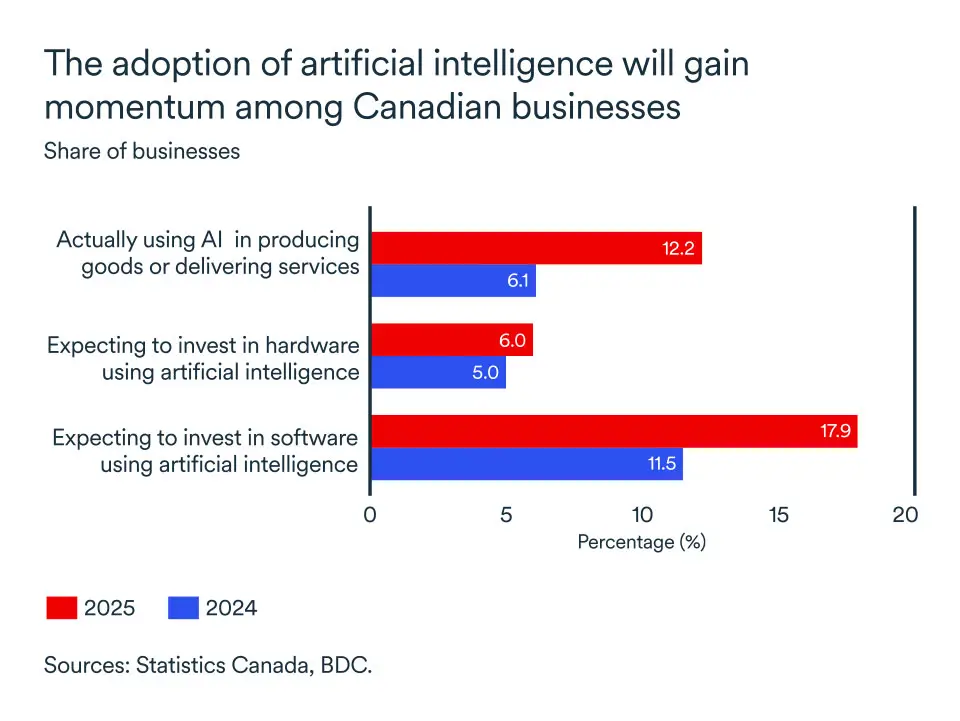

The advent of AI technology

The adoption of artificial intelligence (AI) is progressing in Canada and around the world, but the gap between its use by large companies and SMEs remains wide. Larger companies, particularly in finance, logistics and manufacturing are already deploying advanced AI to automate their processes and optimize decision-making. Conversely, many smaller businesses are hesitating, held back by the cost of the tools, a lack of internal skills and the complexity of integration. However, smaller scale AI solutions will continue to come to market.

At the same time, the issue of digital sovereignty is gaining increased attention. At both the national and provincial levels, investments in AI infrastructure to reduce dependence on foreign platforms and protect sensitive data will grow this year. This trend opens opportunities for providers of this type of service.

The rise of AI is being accompanied by increased demand for talent: engineers, cybersecurity specialists and software developers. Companies, including many SMEs, will have to compete to attract these employees. On the other hand, the resources previous devoted to performing certain repetitive, analytical or administrative tasks can be reallocated to higher value activities.

As this technology evolves, the associated risks for businesses will increase, and once again, smaller businesses will be more vulnerable. Sophisticated cyberattacks, automated disinformation and deepfakes are threats to the reputation and security of businesses. SMEs will need to invest in robust detection and protection systems to maintain the trust of customers and partners.

The impact on your business

Canadian businesses can manage these trends by learning from what larger organizations are doing, investing in their infrastructure and training their teams.

- Once again this year, businesses would be wise to prepare financial projections, especially if you export. Take advantage of interprovincial trade simplifications to diversify your markets and partners.

- Plan strategies today to prepare your business for the changes brought about by an aging population and slower immigration. This is a good time to adapt your offerings and business strategy, such as adjusting your sales cycle or seizing merger and acquisition opportunities. Technologies can help.

- The race for AI is accelerating among SMEs. New tailored solutions are arriving, so be ready to test and position yourself to quickly reap the benefits. Be curious, well-planned and financially prudent in your approach.

The recovery will have to wait

This year, like the last one, has begun with much uncertainty for the Canadian economy, and it remains to be seen if it will show the same resilience, it did in 2025. Faced with trade and geopolitical tensions last year, the Canadian economy still managed a respectable performance, with real GDP growth coming in at 1.5% between January and October.

However, the economy showed weakness late in the year. GDP declined in October (-0.3%) compared to September. The service sector, which accounts for about 70% of the economy was down by 0.2%, while the goods sector reversed course, after a strong September, to decline by 0.7%. The manufacturing and oil and gas extraction sectors accounted for much of the drop.

GDP is projected to have also declined by 0.1% in November, according to preliminary estimates from Statistics Canada. That would mean the country posted growth of no more than 1.4% for the first 11 months of 2025, compared with the same period last year.

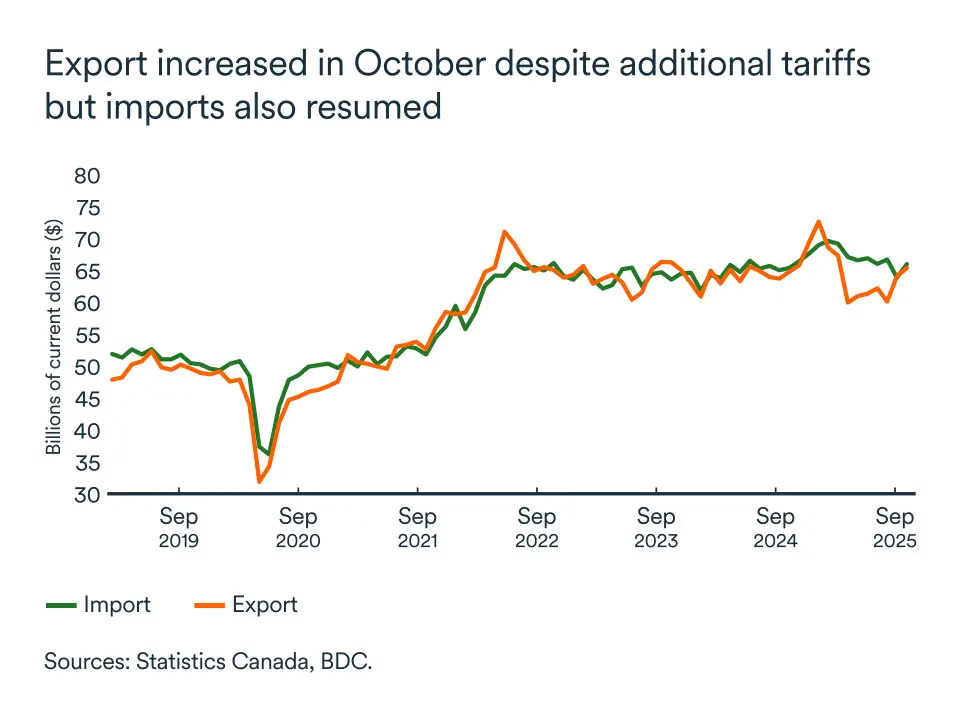

Trade continues to show no clear trend

Trade remains the wild card for Canada's economic outlook. Following high volatility earlier in the year, October data brought no clarity about the future direction of trade. Exports rose 2.1% to $65.6 billion, while imports jumped 3.4% to $66.2 billion, tipping the trade balance from a slight surplus in September to a deficit in October.

Significant movements during the year artificially inflated GDP without reflecting a sustainable improvement in the real economy.

Domestic demand remains moderate, and trade tensions with our main partner, the United States, exacerbated by tariffs on steel, aluminum and automobiles, continue to weigh on the outlook. Initial estimates suggest that exports declined for 2025 as a whole, while imports remained flat. This dynamic widens the country's trade deficit and reduces the contribution of international trade to GDP growth. This phenomenon is likely to continue in 2026.

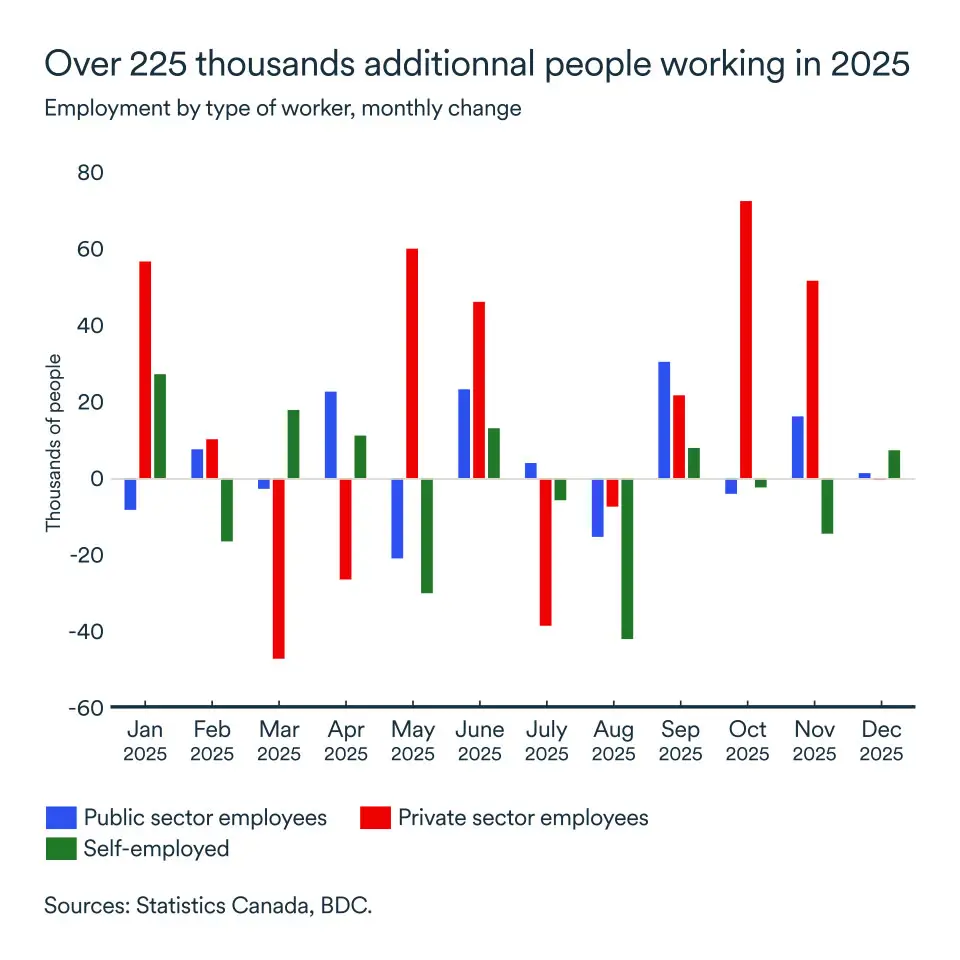

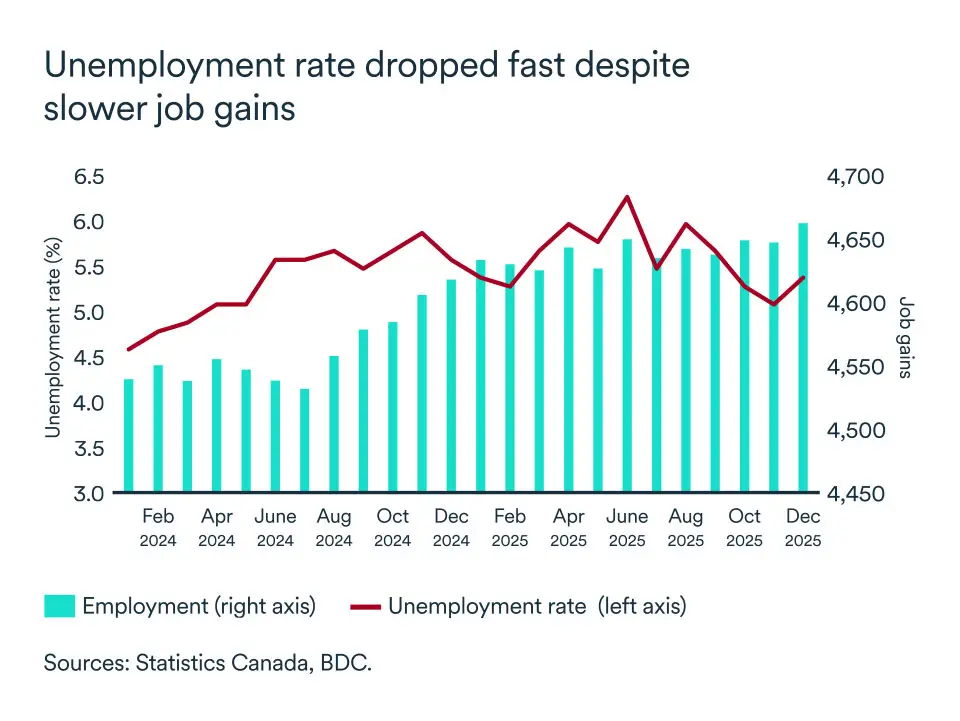

The job market was spared last year

Although job creation slowed, Canada had 226,300 more people working in 2025 than in 2024. Despite the economic uncertainty, the private sector contributed more than 200,000 of the new jobs, while the number of self-employed workers declined by just under 30,000.

Employment has nevertheless shown significant monthly variations over the past 12 months and there have also been significant regional disparities. It’s important to note that the unemployment rate remains high, while job vacancies have declined significantly.

In December, the labour market showed signs of slowing down, with Statistics Canada reporting just 8,200 more jobs than in November. The national unemployment rate rose 0.3 percentage points to 6.8%.

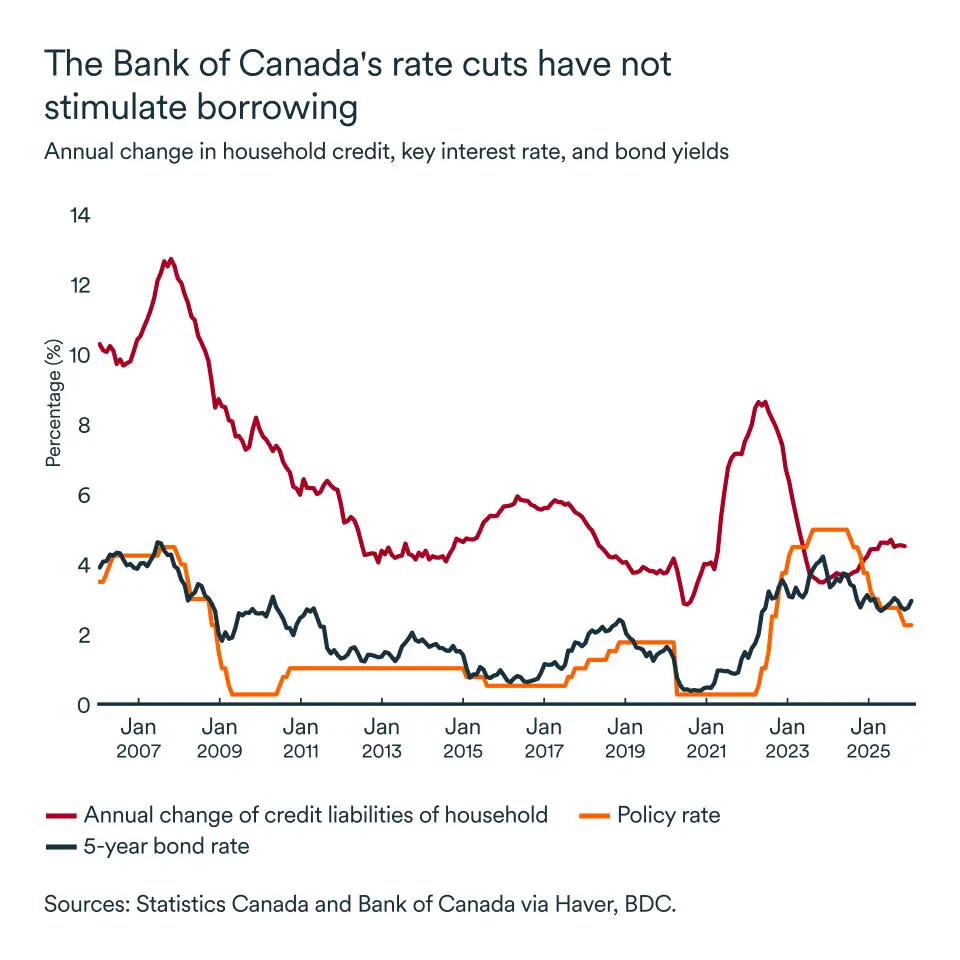

Households remain cautious despite rate cuts

The Bank of Canada cut its key interest rate by 100 basis points in 2025, from 3.25% in January to 2.25%. However, this failed to encourage households to boost their borrowing significantly.

It appears the central bank’s actions have had less of an impact than in the past in lowering prevailing market interest rates and encouraging borrowing. Five-year bond rates, for example, have remained virtually unchanged over the past 12 months.

Usually, it takes several months for central bank rate cuts to have their full effect on the economy. There is, therefore, still hope that the 2025 rate decisions will support the real economy in 2026.

However, we will probably have to hope that fixed rates in credit markets come down since Canadian households seem to be continuing to exercise caution in their borrowing, despite lower variable rates.

The impact on businesses

- Prolonged uncertainty, particularly regarding international trade conditions, and modest GDP growth are making financial and strategic forecasting more complex for businesses in 2026. Take a scenario-based approach, make sure you have up-to-date and complete financial statements in order to optimize your costs and secure your margins.

- Rate cuts have not yet stimulated borrowing, which is delaying business expansion and modernization projects. It would be surprising to see further cuts by the Bank of Canada anytime soon. If you have projects or maintenance that require financing, now is a good time to seek it out.

- Despite the economy’s resilience, domestic demand remains moderate. Labour market volatility is prompting households to be cautious, which is limiting consumption. Businesses that are more domestically oriented should expect volatility in demand. A scenario-based approach and an assessment of business optimization will be beneficial in 2026, whether you export or not.

British Columbia

The B.C. economy strengthened in 2025. Real GDP growth accelerated to an estimated 1.2%, which was above the national average and well-above the sluggish pace of 2024. Still, real GDP growth remained below the province’s 10-year average of 2.8%.

Residential construction was a key driver of growth, with housing completions hitting their highest level since the pandemic. Meanwhile, consumer spending remained remarkably robust, with retail sales growing 6.3% through October. That was the strongest inflation-adjusted increase of any province as weaker interest rates provided relief to debt-strapped households.

Employment in B.C. slipped slightly in December, but the province still created 24 000 jobs in 2025. Nevertheless, the unemployment rate increased to 6.4% as the number of people joining the labour force outpaced job creation.

Alberta

Alberta’s economy is expected to grow around 1.8% in 2026, outperforming most provinces, despite trade uncertainty and softer oil prices. The growth will be thanks to strong population inflows and steady energy exports.

The unemployment rate stood at 6.5% at the close of 2025 as Alberta’s labour market lost some steam in December. Still, the province had its best quarterly employment gains (outside the COVID recovery) in the fourth quarter with the addition of 48,500 new hires from Q3. Despite a mild pullback in October, retail sales remained resilient, supported by household spending.

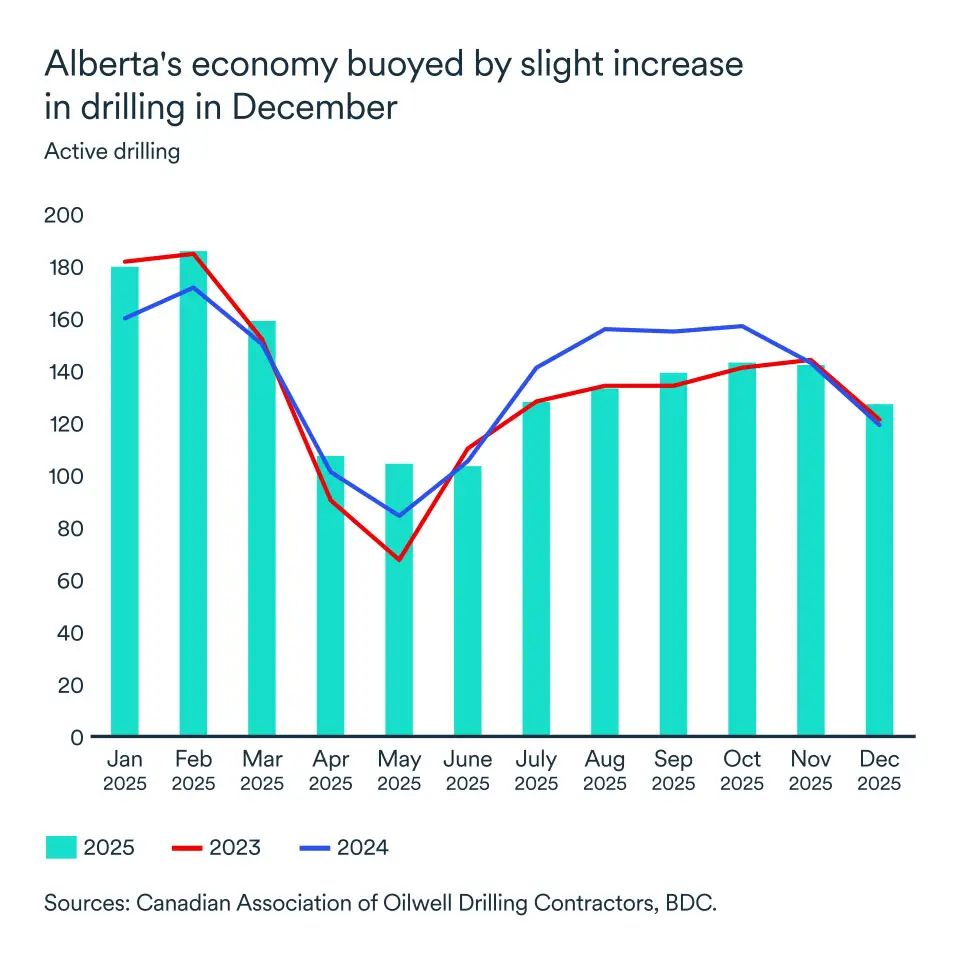

On the energy front, oil production continues at historically high levels, aided by the Trans Mountain pipeline expansion, even as WTI prices hover below US$60 a barrel in an oversupplied market.

Drilling activity increased somewhat in December compared to last year, with 128 active rigs in Alberta, signalling modest investment and ongoing field operations.

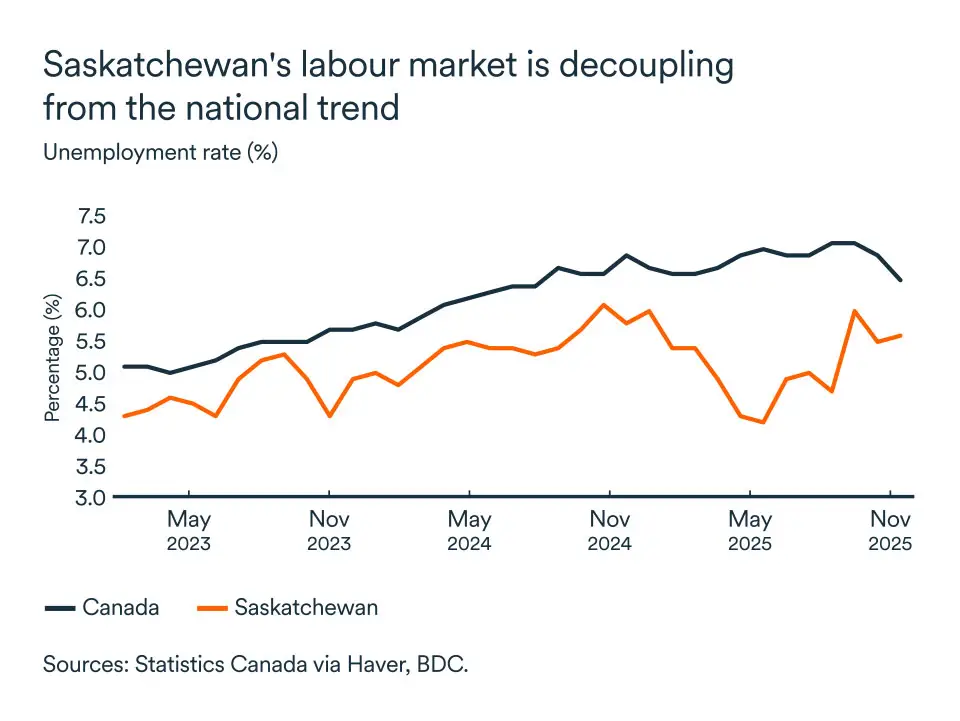

Saskatchewan

Saskatchewan’s economy is projected to grow around 1.7% in 2026, maintaining its position among Canada’s top-performing provinces, despite trade headwinds and softer commodity prices.

The labour market showed remarkable resilience earlier in 2025, posting Canada’s lowest unemployment rate at 4.0% in June.

But the pool of potential workers continued to grow in the province as greater uncertainty took hold. That led to a strong pickup in the unemployment rate to the current 6.5% at a time when the national rate is coming down.

Retail sales remained solid, but they too slowed since mid-year on the back of softer labour market conditions and Chinese tariffs on key agricultural goods.

Meanwhile, potash output is set for a major boost as the BHP Jansen mine ramps up, targeting 4.35 million tonnes annually starting in 2026, reinforcing Saskatchewan’s role as the world’s largest potash producer.

Manitoba

Manitoba’s economy is forecast to grow modestly by around 1.0% in 2026, reflecting ongoing tariff-related headwinds and weaker capital investment. Retail sales have flat-lined, with recent data indicating steady but muted consumer spending through late 2025.

The labour market continues to perform well, supported by population growth and immigration. Unemployment is expected to stay relatively low even as hiring slows in manufacturing and trade.

On the industrial side, manufacturing shipments remain a key driver, averaging about $2.2 billion monthly. Recent trends point to a strong pickup, but caution is warranted given the uncertain trade situation.

Manitoba, although well-diversified, is more sensitive to domestic economic fluctuations. Interprovincial barriers are expected to continue to ease in 2026, which is a boon for the province because it relies heavily on internal trade.

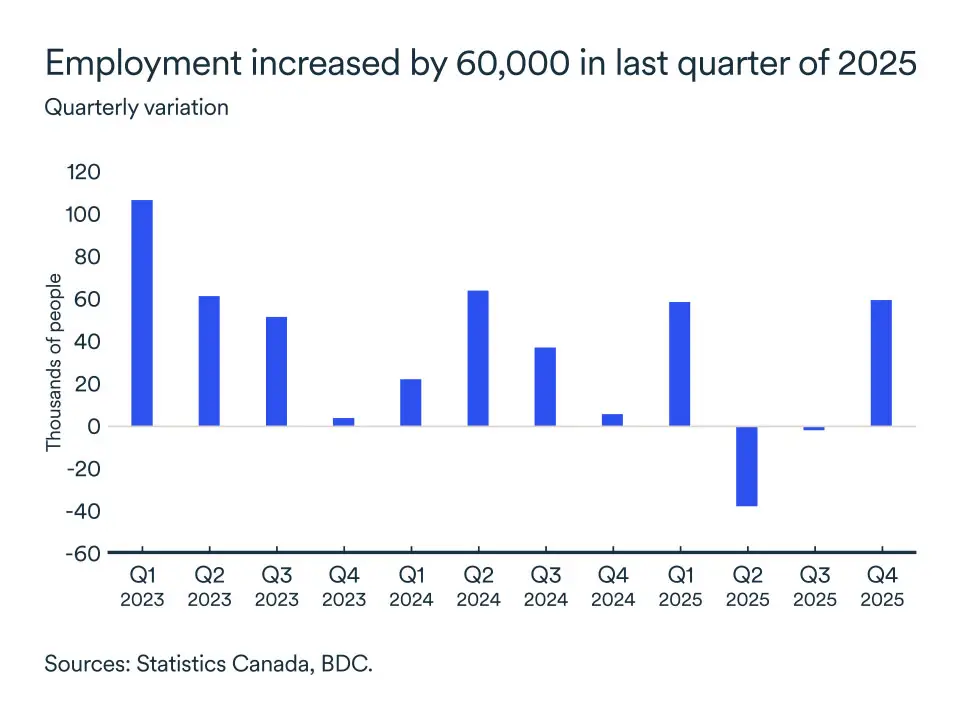

Ontario

Ontario's economy ended 2025 on a positive note. Employment rose by 13,000 jobs in December, increasing the total for the fourth quarter to 60,000. These gains offset the significant losses caused by tariffs imposed on the steel and automotive sectors earlier in the year.

Ontario ended the year with 72,000 jobs created in 2025. The improvement in employment was due to stronger exports in the third quarter. Sectors affected by tariffs, such as steel, are still in sharp decline, but automotive exports are increasing and contributing to job growth in the manufacturing sector lately.

In addition, household spending continued to increase despite economic uncertainty. As a result, retail sales increased in the third quarter as did home resales. Ontario's economy is slowly recovering from the shock of tariffs.

Quebec

Underlying conditions in Quebec weakened in the third quarter. Household consumption declined, and business investment fell sharply across machinery, equipment and intellectual property.

The unemployment rate remained low in the province at 5.4% in December, despite slower job gains during the year. This trend reflects tighter labour market conditions in the province.

Households continued to build up their savings. The net household saving rate increased from 6.7% in Q2 to 8.0% in Q3. Improvement in confidence among consumers would encourage households to spend some of these savings in the coming quarters.

Nova Scotia

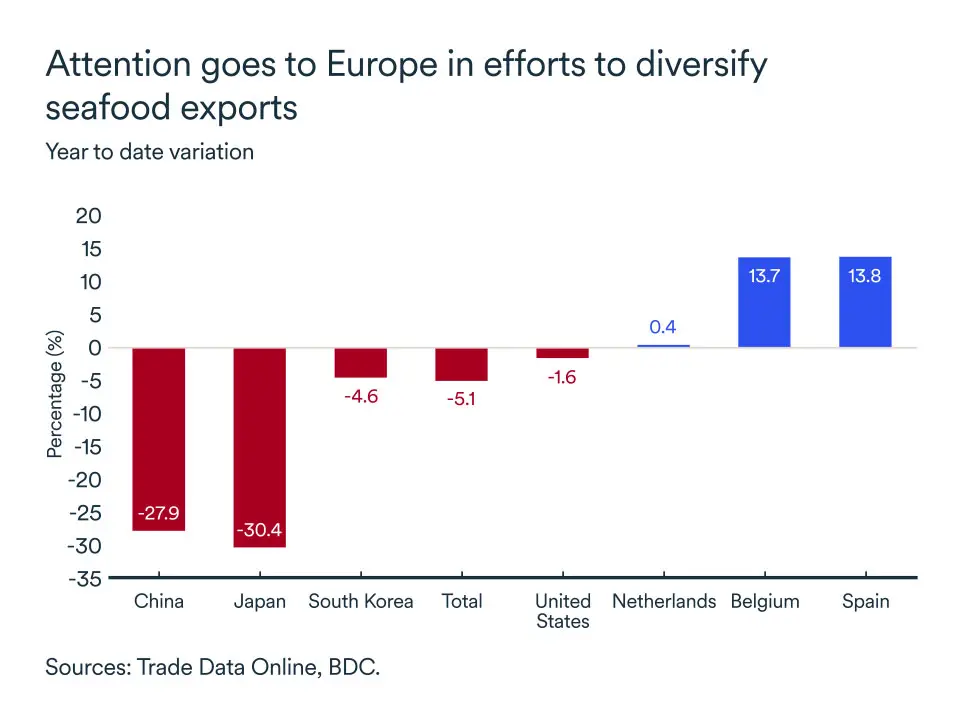

Nova Scotia’s efforts to diversify its economy are paying dividends. While total seafood exports decreased by 5.1%, dragged down by a strong decline in sales to China, the province was able to ship more to Europe, offsetting some of the losses.

Employment increased slightly in December, and the unemployment rate fell to 6.4%.

Consumers continued to spend in 2025. Retail sales increased by 3.3% from January to October, compared with the previous year. As the labour market stabilizes further, we should see more upside for consumer spending this year.

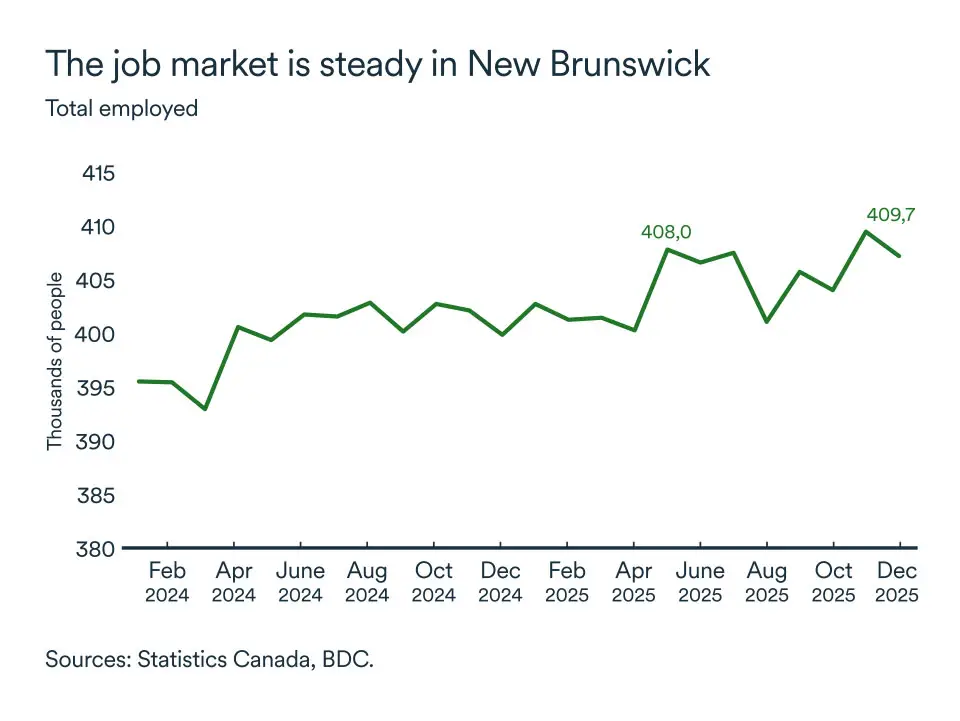

New Brunswick

New Brunswick’s economy slowed in 2025 as uncertainty and tariffs hurt trade and consumer confidence. Exports fell by 9.1%, impacting manufacturing production.

However, the job market strengthened in 2025, pushing the unemployment rate down to 6.6%.

Retail sales increased by a decent 4.5% from January to October, compared with the previous year. But sales were lower on average in recent months.

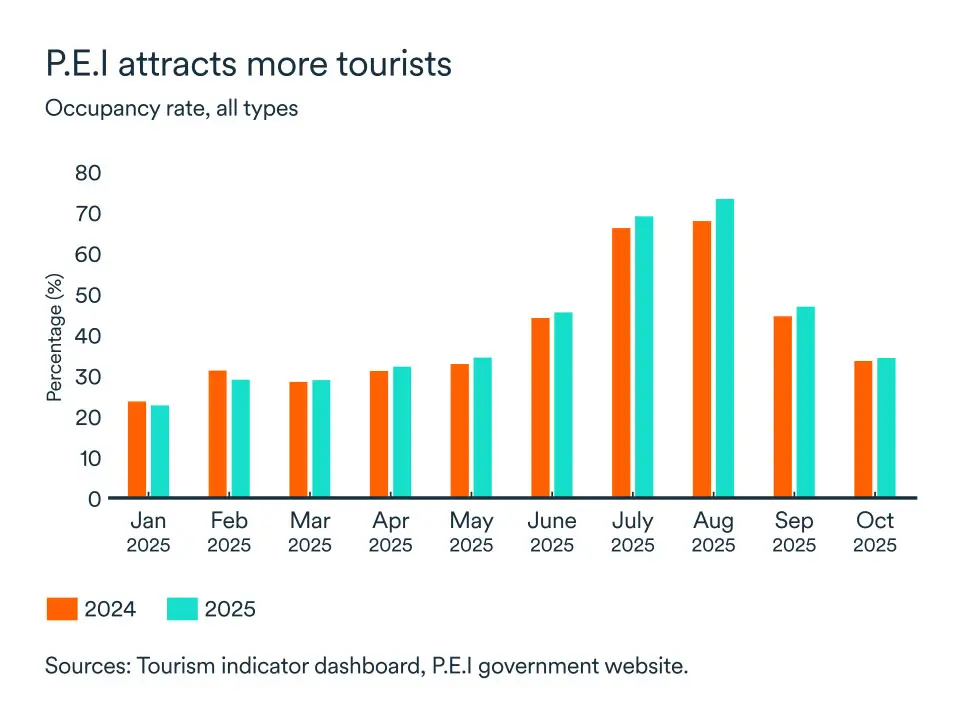

Prince Edward Island

As tension rose between the Canada and the U.S., the province was able to attract more tourists in 2025. Occupancy rates were higher each month during peak season, supporting economic growth in the island.

The job market was stronger at the end of the year. Employment increased to 94,800, recovering all job losses seen during the year.

Consumers continued to spend despite trade tensions. While retail sales were choppy in 2025, they stayed higher than 2024 levels. Households on the island should be able to continue to spend as labour market conditions stabilize.

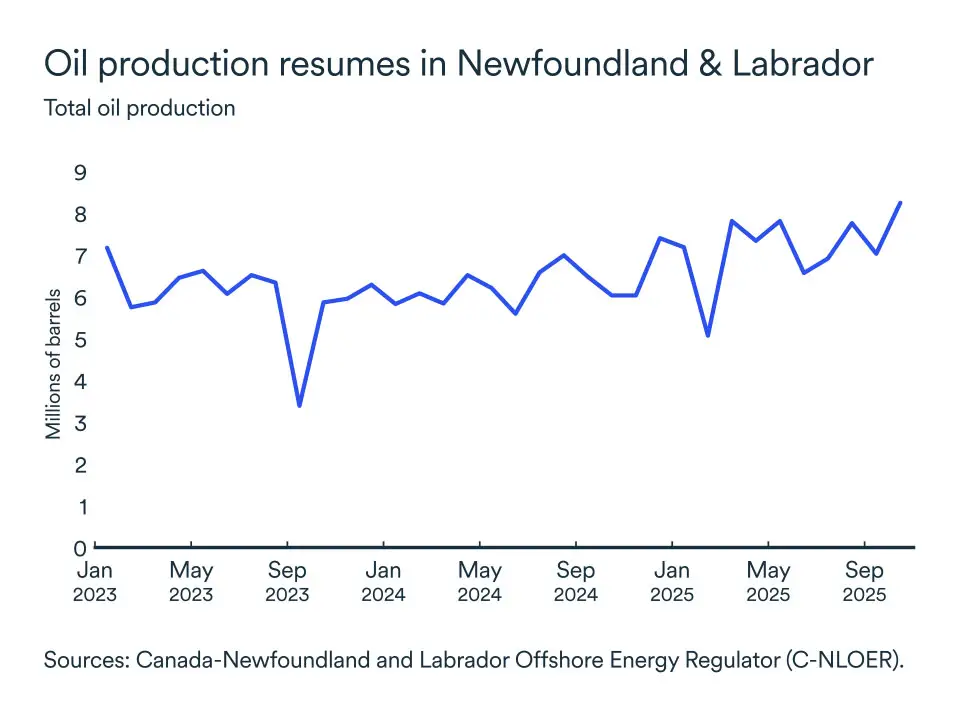

Newfoundland and Labrador

Oil production was a big driver for the province’s economy in 2025, increasing by 37% in October alone (year-over-year). While oil prices hit new lows, weighing on revenues, increased production should continue to support growth this year.

The job market was stable in the first half of the year, but decreases in recent months pushed the unemployment rate to 10.7% in December.

Consumers slowly increased their spending in the last months of 2025, reflecting an improvement in confidence. This trend should continue this year.