Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreThe Canadian dollar is set to remain weak

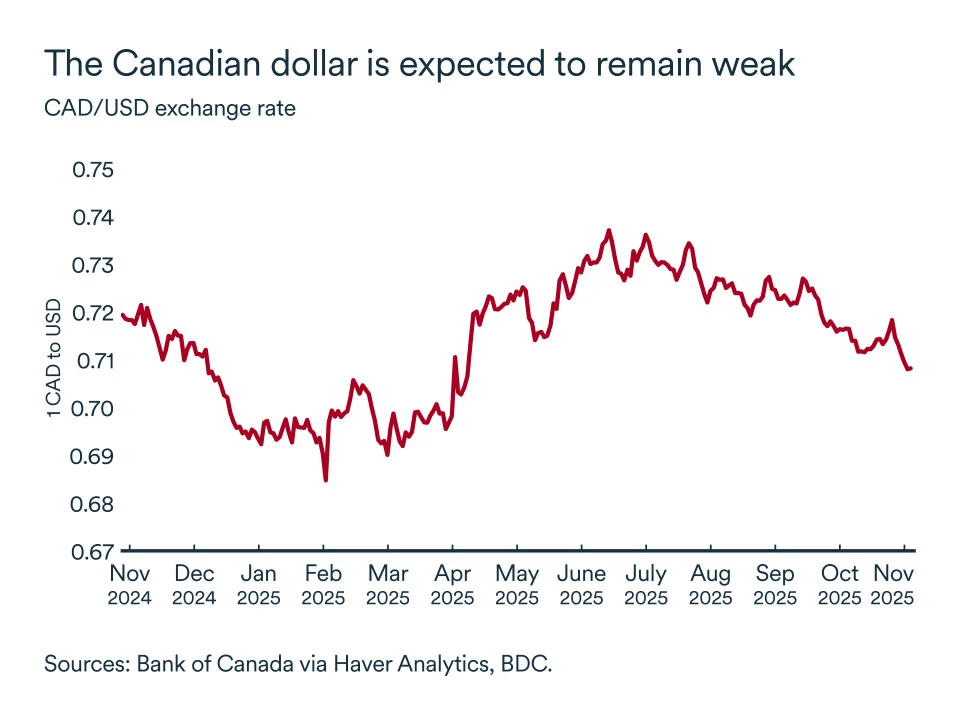

The exchange rate between the Canadian dollar and the U.S. greenback has become a major source of concern for Canadian businesses and policymakers over the past year. Amid trade uncertainty, economic volatility and difficult central bank decisions on both sides of the border, the Canadian dollar has fluctuated significantly.

Understanding the outlook for the loonie in the months ahead is essential for entrepreneurs who are trying to forecast costs and profit margins and make the right currency moves to stay competitive and grow.

Currency fluctuations are notoriously difficult to predict, but...

The exchange rate between the dollar and other free-floating foreign currencies is determined by the forces of supply and demand. These are driven by investors’ changing expectations about the future. And that’s why it’s notoriously difficult to predict the ups and downs of the dollar, especially in times of high uncertainty.

The loonie was trading at 68 cents US in February, before rising to 74 cents at the beginning of the summer and then falling back to closer to 70 cents at the time of writing. These fluctuations totalled more than 8% in just a few months, and the dollar has fallen more than other major currencies over the past year.

Despite the difficulty of making forecasts amid ongoing uncertainty, certain trends will influence currency fluctuations in 2026. For the Canadian dollar, the key indicators will be short-term interest rates, commodity prices and market volatility.

1. Monetary policy and interest rates

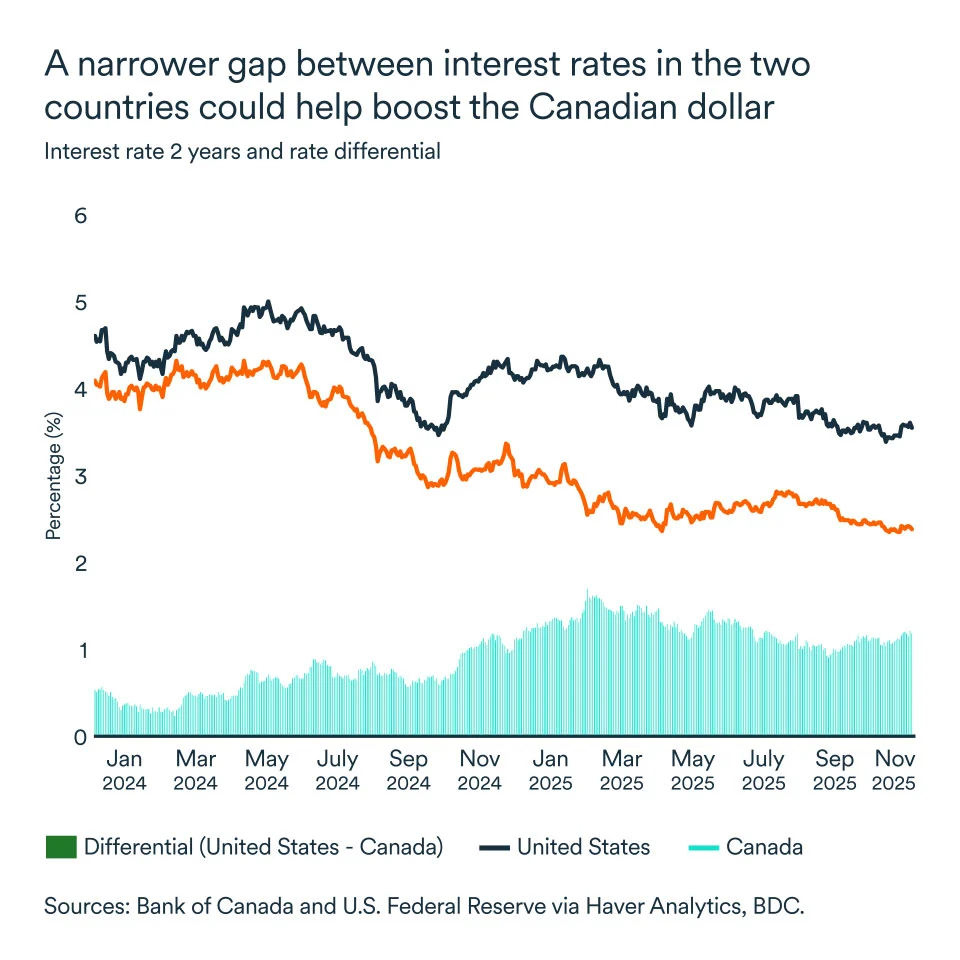

When interest rates in Canada fall faster than in the United States, the Canadian currency tends to depreciate. Over the past year, the Bank of Canada has lowered its key interest rate four times, while the Federal Reserve has limited itself to two cuts. More importantly, since their recent highs, the Bank of Canada has cut interest rates by 275 basis points–more than double the Federal Reserve's 125 basis points.

When interest rates in Canada fall faster than in the United States, the Canadian currency tends to depreciate. Over the past year, the Bank of Canada has lowered its key interest rate four times, while the Federal Reserve has limited itself to two cuts. More importantly, since their recent highs, the Bank of Canada has cut interest rates by 275 basis points, more than double the Fed's 125 basis points.

These decisions are reflected in prevailing interest rates in the two economies, particularly short-term rates. Rates have fallen more rapidly in Canada than in the U.S., explaining some of the recent downward pressure on the Canadian dollar.

No further rate cuts are expected from the Bank of Canada following its October announcement. The picture is less clear on the American side where inflation remains stubbornly high and consumption is strong, despite a slowing labour market. Further cuts are likely south of the border, but the decline will be gradual.

We expect the Canada-U.S. short-term rate differential to narrow in 2026, with the impact being modestly in favour of a stronger Canadian dollar.

Impact on the exchange rate: slight appreciation of the Canadian dollar.

2. Influence of commodities

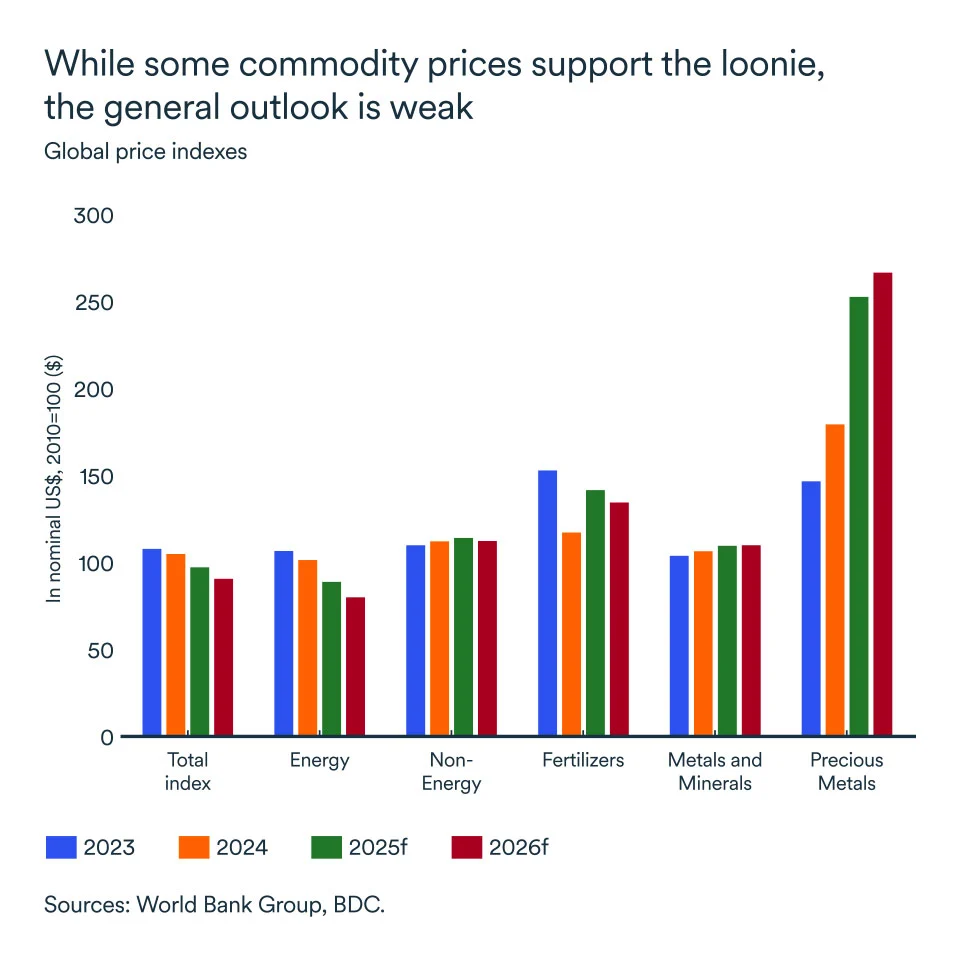

Natural resource industries account for about 10% of Canada's economic output, while representing about 50% of exports. The Canadian stock market also remains heavily weighted towards commodities. As a result, fluctuations in demand for commodities, particularly oil, metals and minerals, are another significant source of volatility in the Canada-U.S. exchange rate.

Overall, commodity prices are expected to trend downward in 2026, as the global economy slows. Uncertainty continues to weigh on global demand, with China, one of the largest consumers of commodities, being particularly vulnerable.

Manufacturing industries are more affected by international trade turmoil and are also the main customers for commodities. There is also a supply surplus in the oil market, which should keep crude prices low in 2026. One bright spot for Canada is an improvement in oil transportation and production capacity that has led to a narrowing of the gap between WCS (the Canadian price benchmark) and WTI (the U.S. price benchmark).

Some precious metals are in a bullish cycle due to economic uncertainty, and others that are essential for the energy and technology transitions are also worth watching (copper, nickel, and lithium).

Still, without an improvement in global trade in 2026, commodities will likely put downward pressure on the Canadian dollar.

3. Global context: uncertainty, risk, and the stock market

Market volatility reflects changes in investor risk appetite, global uncertainty and inflation expectations.

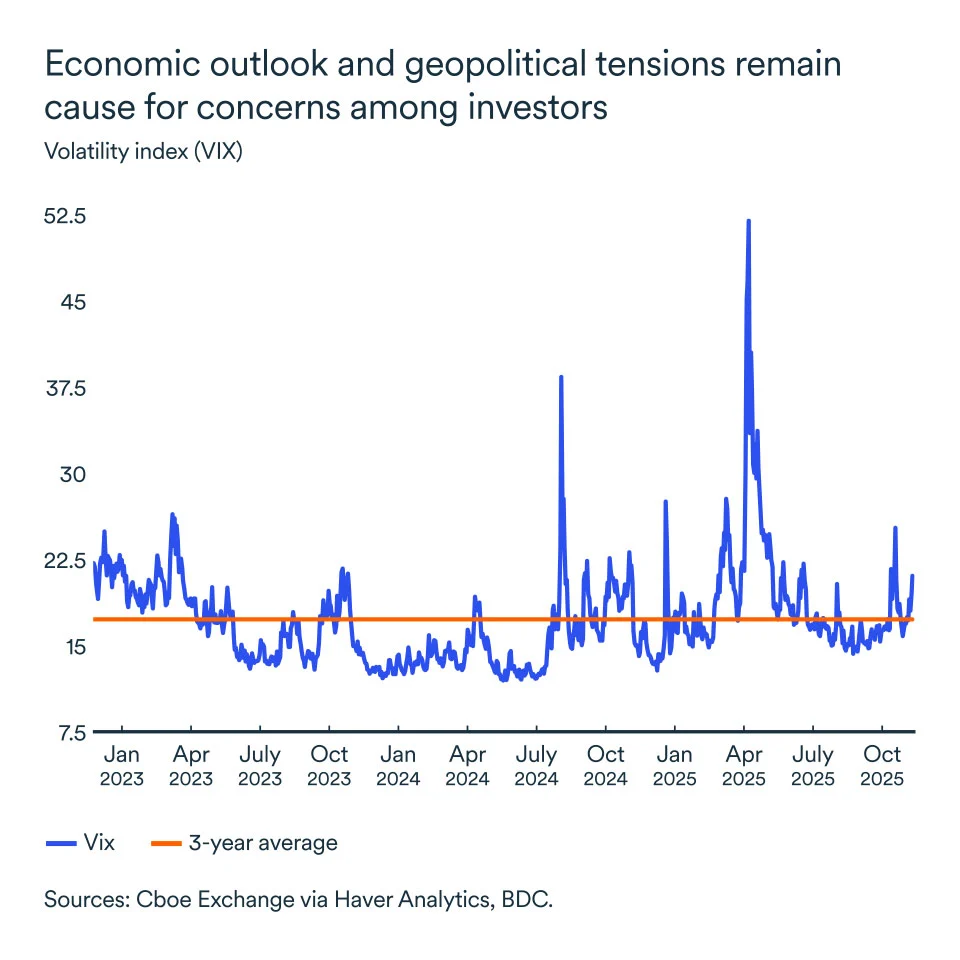

The VIX, the index that measures market volatility and is commonly known as the fear index, peaked at 60.13 in April. That was in response to so-called “liberation day,” the announcement of new U.S. tariffs on the entire world. While the stock market quickly recovered its losses from the shock, the VIX remains high compared to historical levels.

When market volatility increases, investors seek refuge in the U.S. dollar, which is considered a safe haven. Market volatility therefore generally has a negative impact on the Canadian dollar relative to the greenback. This is not because the loonie is depreciating, but because the U.S. dollar is appreciating relative to other currencies.

However, in the current environment, the potential for further appreciation of the U.S. dollar is limited. Investors appear wary of the greenback and are, instead, turning to gold to diversify their risk.

Historically, the S&P/TSX Composite Index (Canada's main stock index) has stood up well to general market turbulence, thanks to its heavy weighting in commodity producers.

The current economic situation should reinforce this trend, driven by emerging demand for resources from the energy transition, AI and other technological advances. These positive developments could continue to offset the effect of the global slowdown on demand for certain natural resources and support the TSX, and therefore the Canadian dollar.

Still, we expect global uncertainty to limit the upside potential for the Canadian dollar, despite some strengths for the TSX.

Overall, the exchange rate will remain weak in 2026

We expect the Canadian dollar to remain between US$0.70 and $0.72 through the end of 2025, but it could climb somewhat higher in 2026.

Given the current level of uncertainty, the loonie’s exchange rate could move quickly one way or the other. However, businesses should get used to a weak dollar that is unlikely to exceed US$0.75 in 2026.

In general, the impact of the value of the Canadian dollar depends on the nature of your business and its dependence on imports versus exports. A weak Canadian dollar favours exports and the tourism industry. If, on the other hand, you import inputs or machinery, your operating costs could increase in the coming months.

Mixed signals from the Canadian economy

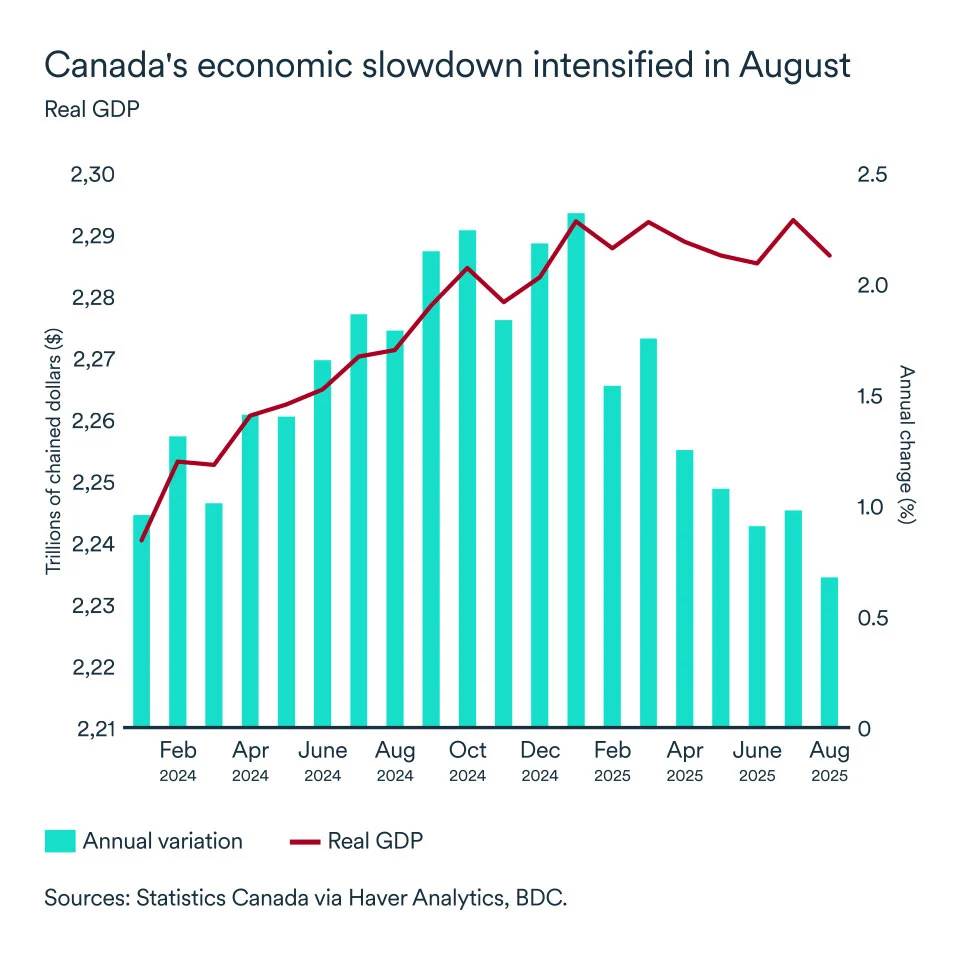

The Canadian economy appears to have avoided a technical recession in the first nine months of the year, thanks to modest growth in September. According to preliminary estimates from Statistics Canada, the economy edged up 0.1% in September, bringing growth in Q3 to an annualized rate of 0.4%.

That was a turnaround from August, when real GDP in Canada experienced a marked slowdown from a month earlier. Economic growth in fell by 0.3%, entirely erasing July's gains. In August, the goods sector continued to decline (-0.6%) to its lowest level since December 2021. The services sector, which accounts for a larger share of total GDP, also declined (-0.1%) for the first time in six months.

In the first eight months of the year, the Canadian economy grew by 1.3% compared with the same period in 2024. Considering the headwinds buffeting Canada, the chances the economy will slow further in the fourth quarter remain important, although some leading indicators point to resilience in the economy.

Employment jumps despite economic slowdown

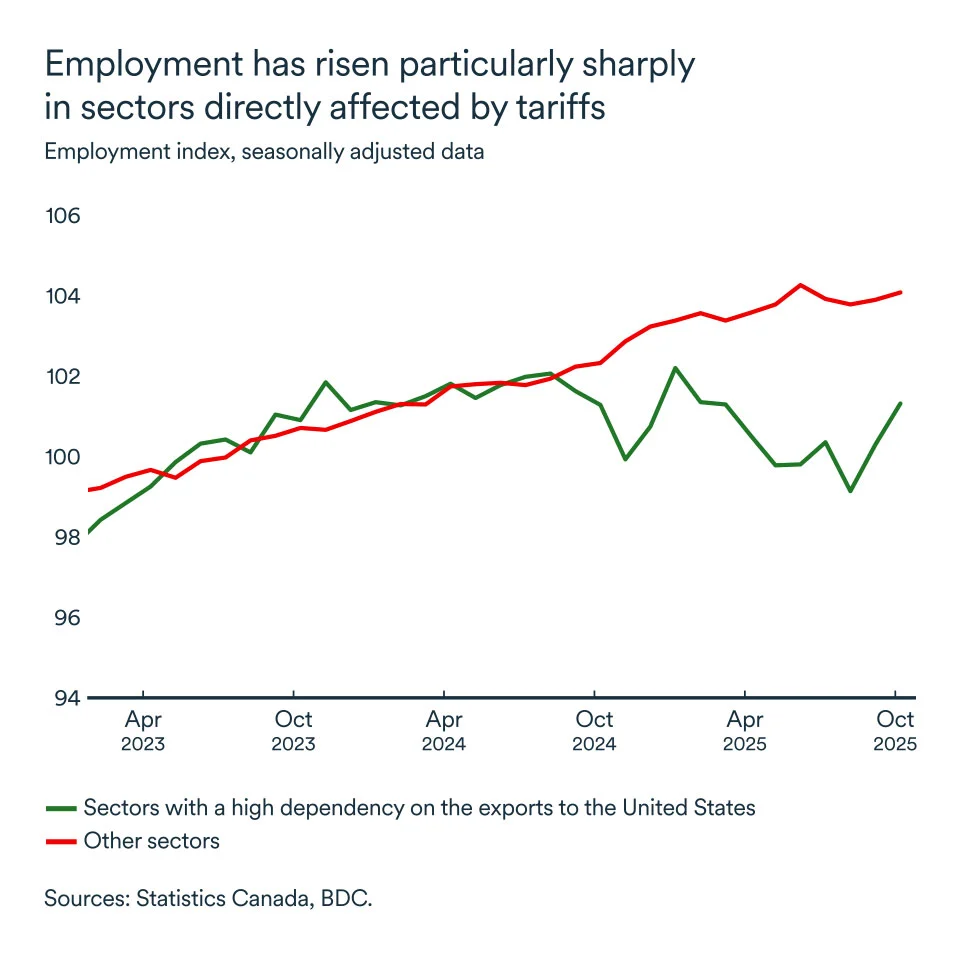

In October, the Canadian labour market posted a robust performance in contrast to the economic slowdown seen earlier in the year. Employment grew by 67,000 jobs (+0.3%), marking a second consecutive month of gains.

The increase was driven mainly by services, particularly retail trade, transportation and warehousing, and arts, entertainment, and recreation. The unemployment rate fell to 6.9%, as the labour force grew more slowly than employment in October.

In addition, full-time employment increased, suggesting some stability in hiring. Regionally, Ontario added 55,000 jobs, the first monthly increase since June, fully offsetting losses incurred since the start of trade tensions. Employment also recovered in sectors that are more dependent on U.S. exports.

Despite an uncertain economic environment, the employment data indicate a resilient labour market, which could act as a buffer against sluggish growth, which remains uneven across provinces and sectors.

Inflation remains under control

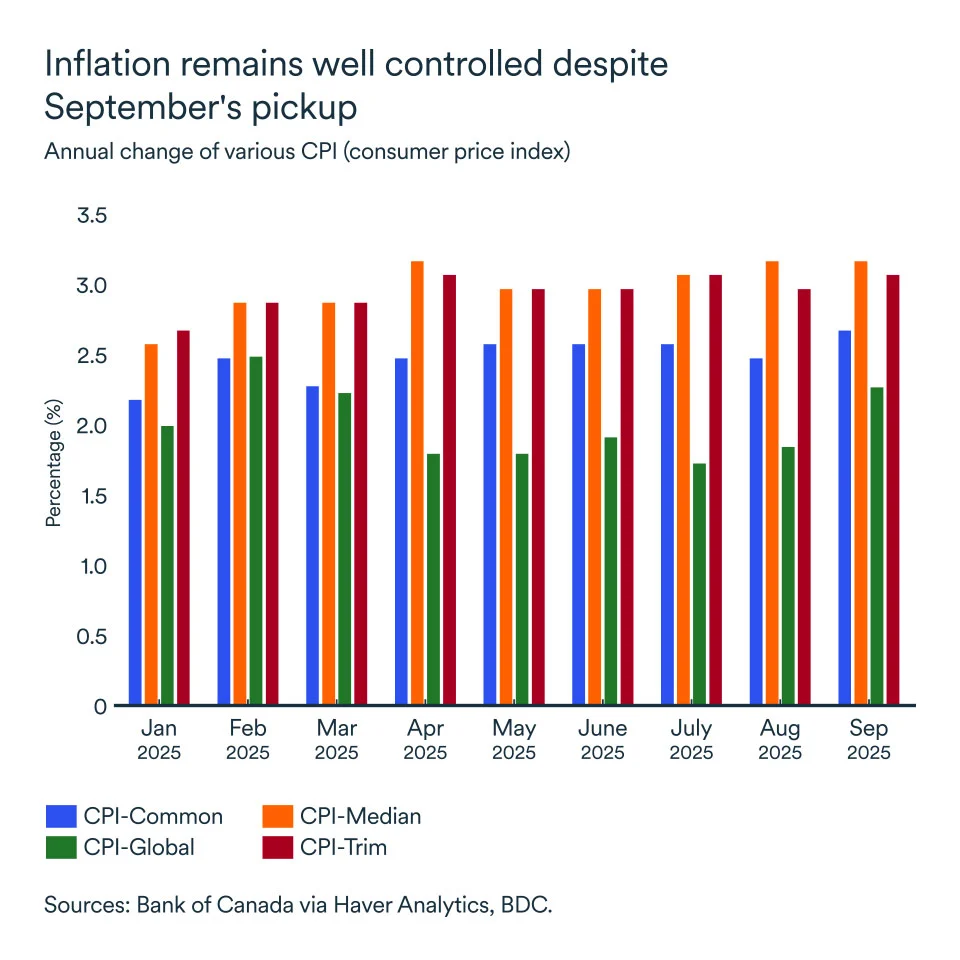

Overall, inflation remained stable, although in September it climbed 2.4%, up slightly from previous months, when it hovered around 2%.

The Bank of Canada's preferred measures of core inflation, such as the trimmed CPI and the median CPI, remained high at around 3%, indicating persistent inflationary pressures in certain segments of the economy. On the other hand, these measures were also fairly stable, which should help preserve the purchasing power of Canadian households and contribute to more balanced growth.

However, prices for food purchased in stores rose by 4.0% and rents were 4.8% higher nationally. Increases in these basic categories could slow discretionary consumption, as a larger share of income goes to unavoidable expenses. In fact, these two budget items rose faster than wages in September.

Bank of Canada is hitting pause again

A mixed dynamic is therefore emerging in the Canadian economy. On one hand, manufacturing output continues to decline amid trade tensions and rising inventories. On the other hand, consumption remains higher than last year, supported by a solid employment picture.

The Bank of Canada cut its key interest rate again in October to 2.25%—the bottom of the neutral range—which will continue to support household consumption, but Canadians should not expect further cuts, at least in the short term.

The central bank has emphasized that rate cuts can’t offset the effects of trade tensions. At the same time, while economic indicators point to ongoing inflationary risks, the economy is showing staying power with a notable improvement in employment.

The impact on your business

- Ensure your sales forecasts are up to date. Canada's economic situation is evolving rapidly. Take into account the slowdown in growth and price increases in essential categories that could slow discretionary consumer spending.

- Optimize inventory levels and logistics to avoid holding costly surpluses amid declining manufacturing shipments and a reorganization of global trade.

- Reassess your short- and medium-term staffing needs so you don't miss out on growth opportunities and maintain healthy margin management.

Atlantic provinces sail into heavy seas

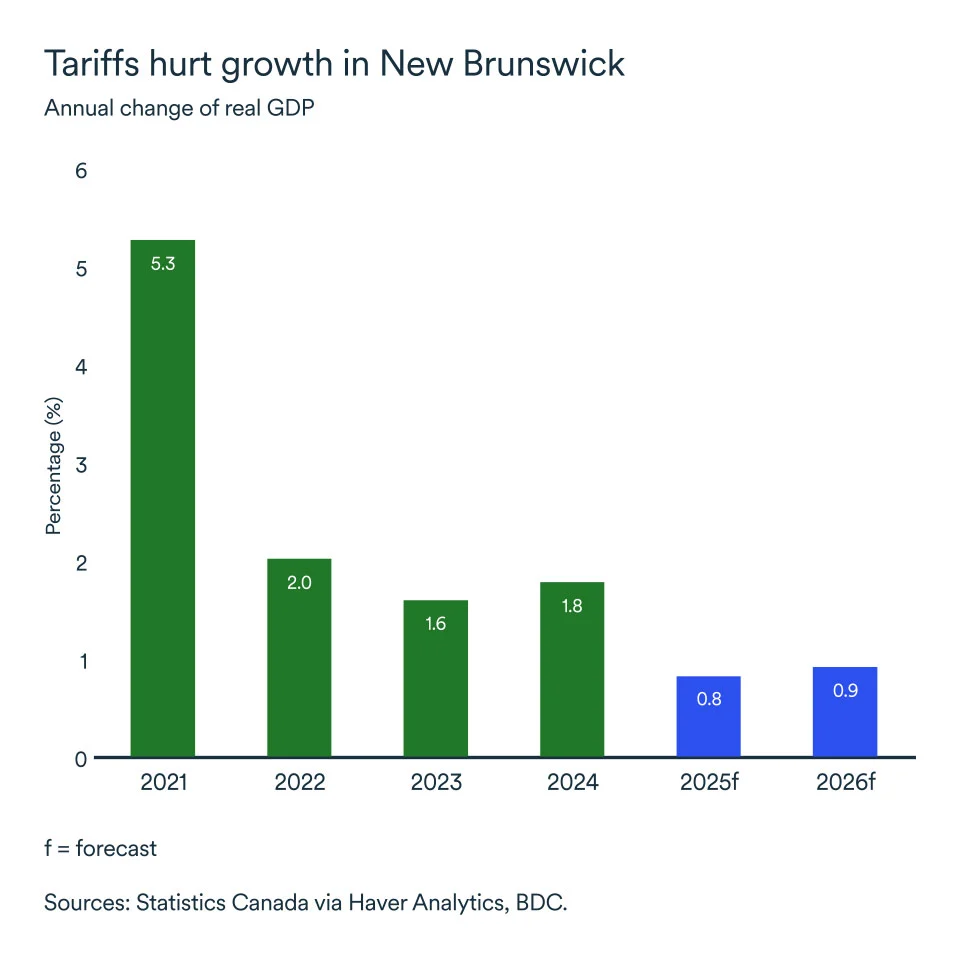

New Brunswick

Tariffs and a heavy reliance on the U.S. market weighed on trade and consumer confidence in New Brunswick this year. Key exports declined significantly, and manufacturing sales weakened.

Surprisingly, employment in manufacturing remained resilient and the rest of the economy continued to generate net job gains. Consumers, on the other hand, were cautious, putting retail sales under pressure and delaying a recovery in home sales.

Still, other sectors provided much needed support in 2025, allowing the province to avoid a recession, which we expect to also be the case in 2026. A projected increase in government spending and planned projects has helped stimulate economic activity. Residential construction also kept pace this year and we expect it to remain solid in 2026.

Overall, the economy should end the year with growth of 0.8%. Next year, we expect modest growth once again at 0.9%.

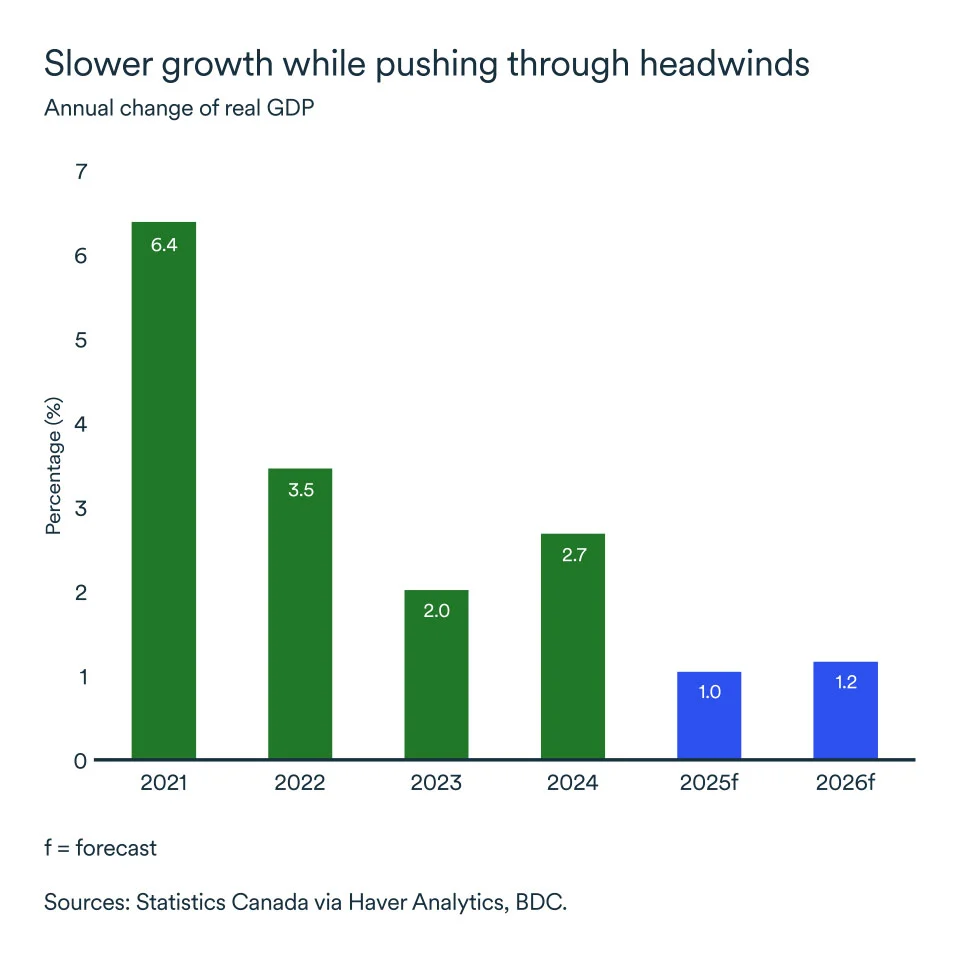

Nova Scotia

Uncertainty and tariffs from major trading partners weighed somewhat on exports but more so on employment this year. Employment in Nova Scotia was stuck in neutral with the province shedding all job gains seen earlier this year in August and September.

Consumers slowed their spending both on big ticket purchases like homes and lower priced items. On the bright side, construction was solid with housing starts averaging almost 10,000 units per month versus 8,000 units last year.

For all of 2025, provincial GDP growth will likely come in at 1.0%, down considerably from 2.7% in 2024. However, public infrastructure, defence and energy-related investments should boost growth going forward.

Prince Edward Island

Good news for P.E.I.—exports increased this year despite tariffs from major trading partners, and manufacturing has held up strongly. Exports to the U.S. rose by 10% between January and August, compared to the same period last year, offsetting a 30% decrease in exports to China.

Resilient employment supported solid consumer spending but fell short of igniting a strong recovery in home sales.

Another factor that played in favour of the island economy this year was the trend that saw fewer Canadians travelling to the U.S. The province attracted more tourists, with overnight stays increasing by 7.7%.

Nevertheless, slower population growth, and no significant new investment projects, have weighed on growth, keeping it at around 1.5% this year and a projected 1.2% in 2026.

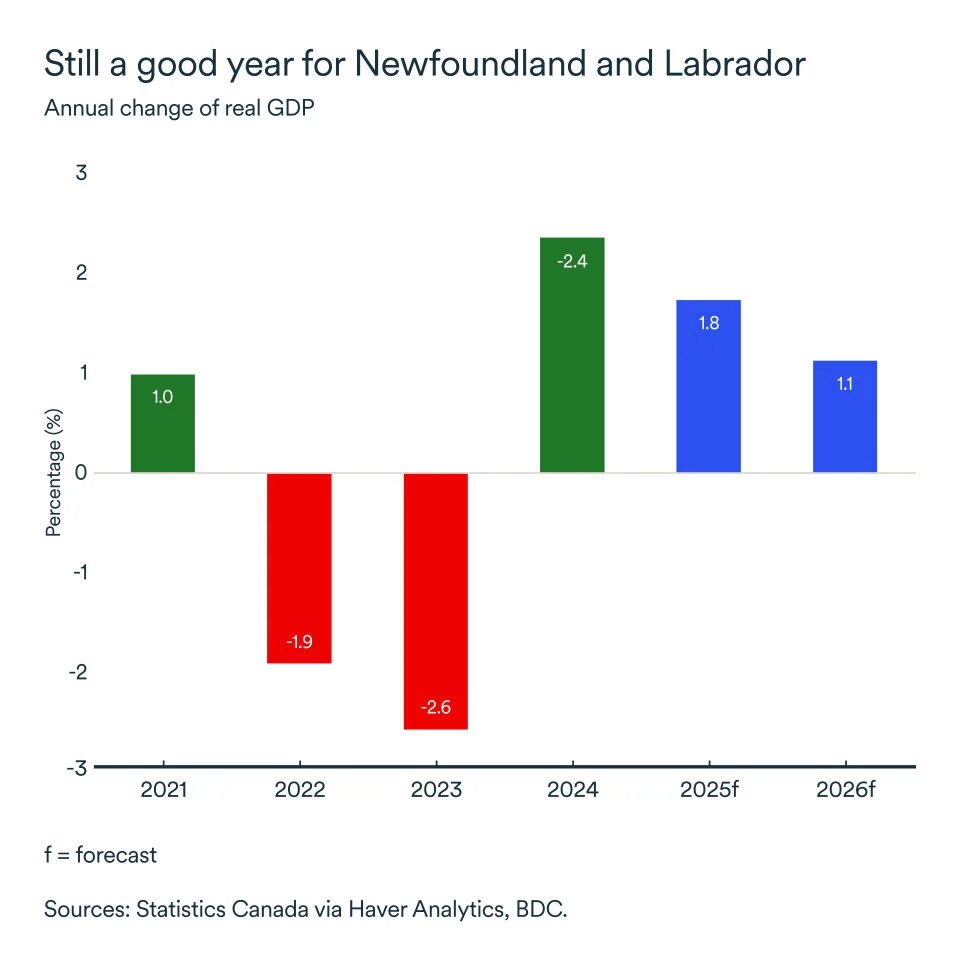

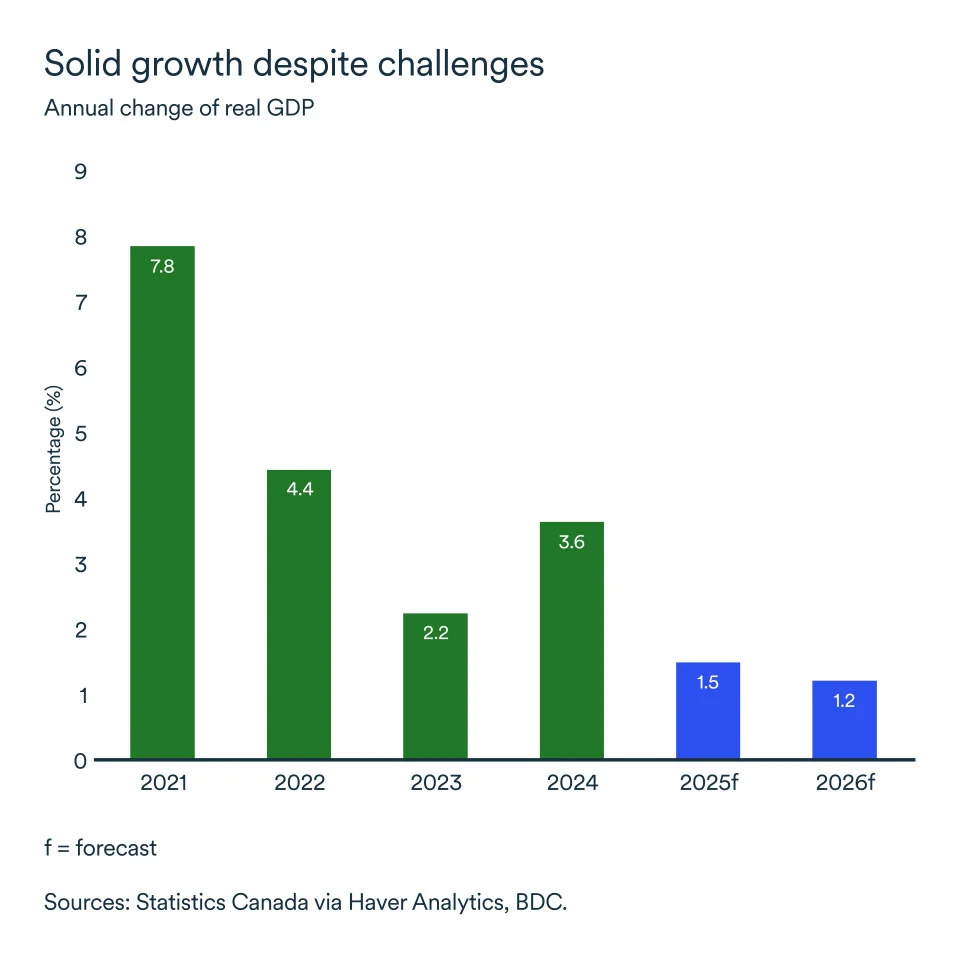

Newfoundland and Labrador

The province is expected to end the year on solid footing, despite uncertainty and tariffs on some of its top exports. An effort to diversify trading partners helped alleviate some of the pressure this year, putting seafood exports close to averages seen in past years.

The energy and mining sector boosted growth. Oil production was up by almost one million barrels in October, compared to 2024. Exports of minerals and ore kept pace throughout the year.

Households maintained their spending in the first half of the year, exceeding the national average. But home sales remained under pressure throughout the first nine months of the year.

Growing slack in the labour market, slowing population growth and no major investment projects, will limit consumer spending and GDP growth in 2026. Overall, the province is set to lead the Atlantic provinces with real GDP forecast to expand by 1.8% in 2025. The outlook is a little weaker for 2026 with growth expected to come in at 1.1%.