Subordinate financing

Subordinate financing is a type of debt in which the lender has less claim on loan collateral than senior lenders.

If the borrower defaults on the loan, the senior lender gets repaid first from the proceeds of the sale of collateral. The junior lender receives what’s left over from that.

Subordinate debt commonly refers to a type of junior debt in which the borrower repays the loan on a monthly basis.

Subordinate debt and other kinds of junior debt are often used to finance quickly growing businesses, as well as mergers and acquisitions, when there aren’t enough assets to secure adequate senior financing.

“Subordinate debt fills a financing gap and is used to make sure a transaction gets done,” says Louis-David Julien, Vice-President, Portfolio Management for BDC’s Growth & Transition Capital team.

Subordinate and junior debt have loose definitions and can mean different things for different lenders.

Louis-David Julien

Vice-President, Portfolio Management, Growth & Transition Capital, BDC

What is the difference between subordinate financing, junior debt, mezzanine and quasi-equity financing?

Subordinate financing is a loosely defined term that is sometimes used interchangeably with junior debt, with different lenders using different terms.

Subordinate financing (or subordinate debt) is commonly seen as part of a larger category called junior debt. Junior debt refers to financing in which the lender’s claim to the borrower’s collateral ranks behind a senior lender’s claim in the event there is a default or restructuring.

Junior debt can take on a variety of forms and may be customized to the needs of the borrower and senior lenders.

Subordinate debt fills a financing gap and is used to make sure a transaction gets done

Louis-David Julien

Vice-President, Portfolio Management, Growth & Transition Capital, BDC

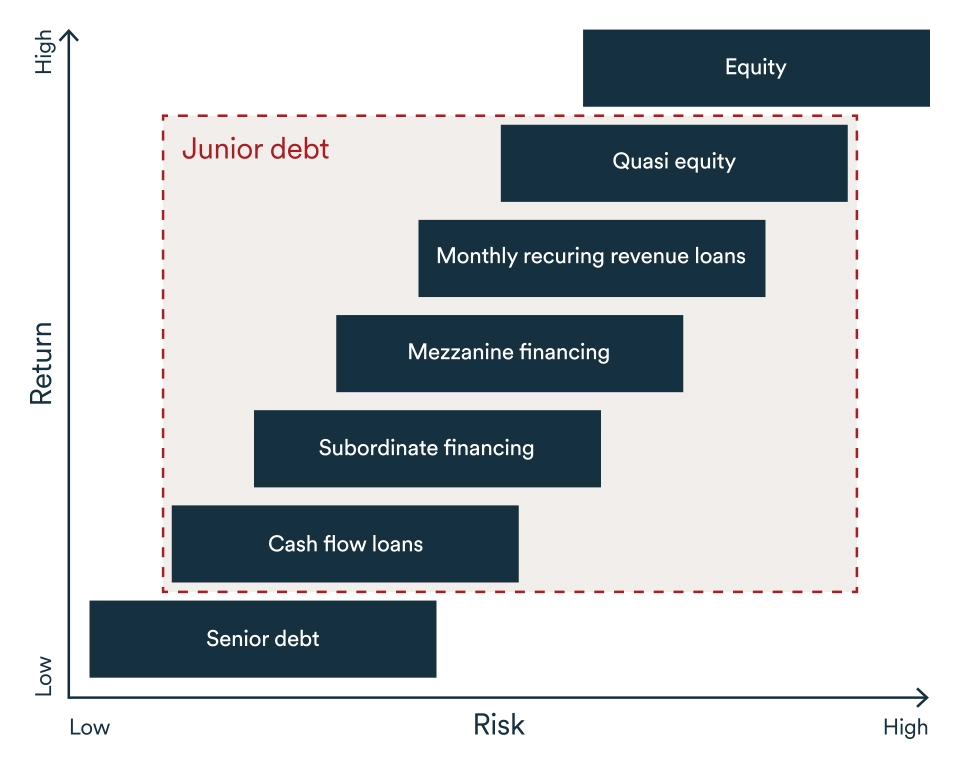

Types of junior debt

1. Subordinate financing often refers to a subcategory of junior debt in which the borrower repays the loan with monthly interest and principal payments—similar to a conventional term loan.

2. Quasi-equity financing is on the other end of the scale of junior debt. This is often repaid at the end of the amortization period, with a single “balloon” or “bullet” repayment of the entire principal and most of the return.

Quasi-equity usually includes conditions that the business pay a “return” that depends on the performance of the company. Measures for that can include sales, valuation, net profit or earnings before interest, taxes, depreciation and amortization (EBITDA).

The borrower pays the return, on top of interest and principal. Possible examples of the return:

- 1% or 2% of the company’s value when the loan matures

- 2% of the company’s EBITDA

- 4% of sales above a certain level

3. Mezzanine financing typically falls between subordinate financing and quasi-equity financing. It could consist of interest-only payments during the loan term or a mix of interest and a variable return, with a balloon payment at the end.

Repayment can also be made through “cash flow sweeps”—annual payments based on a portion of excess available funds.

4. Monthly recurring revenue financing is usually based on a multiple of the company’s monthly recurring revenue. It’s uniquely tailored to tech companies with high-margin subscription revenue, such as SaaS (software as a service) businesses.

Terms can vary by lender. “Subordinate and junior debt have loose definitions and can mean different things for different lenders,” Julien says.

“It’s so customized that one business may have a junior financing deal that looks completely different from another company’s deal, even though they have the same name.

“Some lenders use mezzanine for everything. In the end, if you negotiate a deal that fits everyone’s needs, it doesn’t matter what you call it,” he says.

Junior debt sits between equity and senior debt in terms of risks and return

What is the difference between junior debt and regular financing?

Junior debt differs from regular financing mainly in that, in the case of a default or restructuring, its holders are repaid after senior lenders.

However, assets can still retain value even after senior lenders have been paid.

1. Tangible assets—In some cases, a portion of tangible assets pledged as collateral could still hold some value for the junior lender in a default or restructuring. For example, if the asset appreciated in value while debt was paid down, such as in the case of real estate, the junior lender may be able to receive partial or full repayment of their loan even after the senior lender gets repaid.

2. Intangible assets—Senior lenders typically don’t put any value on a borrower’s intangible assets, such as intellectual property. As a result, it is sometimes pledged only to the junior lender.

Other key differences between junior and senior debt:

1. More flexibility—Subordinate debt and other types of junior financing are highly flexible and customized to the needs of the parties. “There’s a lot of flexibility and negotiation to make sure the deal suits everyone,” Julien says. “If you don’t want something complicated in life, don’t go into the junior financing world. It can be very creative, to say the least. It’s our job to find a way to make the deal fit.”

2. Shorter loan terms—Junior debt tends to have shorter loan terms than senior debt, averaging around five years. This is due to the shorter horizon of the projects it finances, such as rapid expansions or business acquisitions. Such ventures also tend to be riskier, which means junior lenders are reluctant to wait many years for balloon payments at the end of the loan term.

3. Higher cost—Because of the greater risk for the lender, junior debt tends to be more expensive for borrowers than senior debt. On the other hand, junior debt is non-dilutive and cheaper than equity financing, in which shareholders give up a portion of their business in exchange for growth capital.

4. Closer lender-borrower relationship—Junior lenders tend to have a much closer relationship with borrowers than senior lenders. Due to the risks associated with subordinate financing, junior lenders typically spend more time researching the borrower and their project.

These lenders also tend to require more robust and frequent financial reporting during the loan term. “Because it’s far riskier for the lender, we follow the clients much more closely and understand their deals better. As a result, if trouble arises, we are in a position to be able to help the company far more quickly,” Julien says.

What are the usual characteristics of subordinate financing?

Subordinate and other junior debt can come with a wide variety of repayment terms and conditions, as well as greater scrutiny. Lenders will look closely at the following areas:

1) Management—Can management deliver on the growth project or acquisition? What is their track record? “When a company runs into trouble, the one thing that will save them is a good management team. They’ll need one that’s not too thin, has gone through other difficult periods and has a lot of skills,” Julien says. “We need to spend time with management and be given the assurance that they can deliver on the project.”

2) Project—Julien lists off several questions that he says need to be asked:

- Does the proposed project make sense?

- What are the prospects for the market?

- Does the market have a future?

- Where are you going to find your people?

- How will you find the space for your new people?

- Do you have the equipment you need?

- (If it’s an acquisition) What is the integration plan to make sure you retain your employees and clients?

3. Financials—How solid are past financials and forecasts? “Every client presents a forecast that says they’ll make a lot of money and everything will be perfect,” Julien says. “They have to explain why they think they can achieve it. If they have strong historic results, we can be more confident that they’re able to deliver.”

Why would a company need subordinate financing?

Subordinate debt and other types of junior debt are typically used when a business is gearing up for rapid growth or a merger or acquisition.

Junior debt is often needed in these cases because the company typically lacks enough tangible assets to pledge as collateral for senior lenders. In this case, the senior lender may approach a junior lender to ask them to help finance the project.

“If you want to expand to the U.S., you have to invest right away. The accounts receivable and profits will only happen later,” Julien says.

“If you go to a senior lender and say, ‘I’ll have very good accounts receivable in two years,’ they’ll say, ‘Okay, come back to me in two years.’ Senior lenders are backward looking. They ask, ‘What is the security I have right now?’ Junior lenders look backward but also forward. You’re banking on the management team and their growth project.”

Fills acquisition financing gaps

This same approach applies to business acquisitions. Acquirers typically have a financing shortfall to cover the target company’s goodwill—the value of the company above its tangible assets. This can include its brand, reputation and intellectual property.

“There’s almost always a gap between the value of the target company’s tangible assets and its market price,” Julien says. “That is its goodwill. A chartered bank won’t lend against that. This is why you need additional financing, such as vendor financing, money from the acquirer or junior debt.”

Helps maintain financial ratios

A related reason companies use junior debt is that it can help maintain their financial health. For example, a junior lender can agree to delayed payments of part of their return, or a balloon repayment at the end of the loan term.

This lets the business keep more cash in the business during the initial part of the loan term, when a project is still shaky.

That also helps the borrower maintain healthy financial ratios, which lenders often require for companies as a loan condition. These can include the debt service coverage ratio and the debt-to-equity ratio.

How do senior lenders view junior financing?

Senior lenders, such as chartered banks, look favourably on junior debt. It’s often critical to ensuring the financing transaction goes through.

Junior debt often fills in gaps in financing when the borrower lacks enough tangible assets for collateral or can’t maintain adequate financial ratios.

“We have a fairly high number of deals referred to us by the chartered banks,” Julien says. “They see us a helper to get deals done. It’s a partnership for everyone. They have clients that come to them with a project, and the senior lenders say, ‘We can lend money against your assets, but you’re missing a bit of financing. Let’s call a junior lender like BDC to join the dance and try to find a solution.’

“Most of the time when a senior lender calls us, they have very specific things in mind, like managing the ratios. They want to see a financing structure that puts less pressure on the cash flow of the company. That gives the company a better chance to survive.”

Next step

Learn more about our customized financing solutions for fast-growing Canadian companies.