Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreAre rising costs here to stay?

Geopolitical tensions have done more than make headlines recently—they’ve reset the cost structure facing Canadian businesses. Energy prices, wages, financing costs, exchange rate volatility and tariffs have all been driven higher or prolonged by recent geopolitical tensions. How will these five forces evolve in the months ahead? What can entrepreneurs realistically do to adapt, protect their profits and stay competitive in a higher cost world?

A persistent cost squeeze, not a temporary shock

For many Canadians, the past few years have felt like a constant crisis during which businesses have turned to fight-flight-or-freeze responses. But the data shows something different.

Before 2020, economic conditions were exceptionally favourable. Interest rates had been at historic lows for over a decade, globalized supply chains kept costs down and wage growth remained moderate at around 2% a year. That period ended abruptly with the onset of the pandemic.

While the pandemic may have been the starting point for a period of higher costs, six years have passed since then. We can no longer talk about a transitional period. Rising costs are no longer being driven by a temporary shock but rather reflect structural shifts in the economy.

When inputs and labour become the focus

Overall production costs are being pushed upward by higher input costs—particularly for materials and industrial goods—combined with persistently rising labour expenditures.

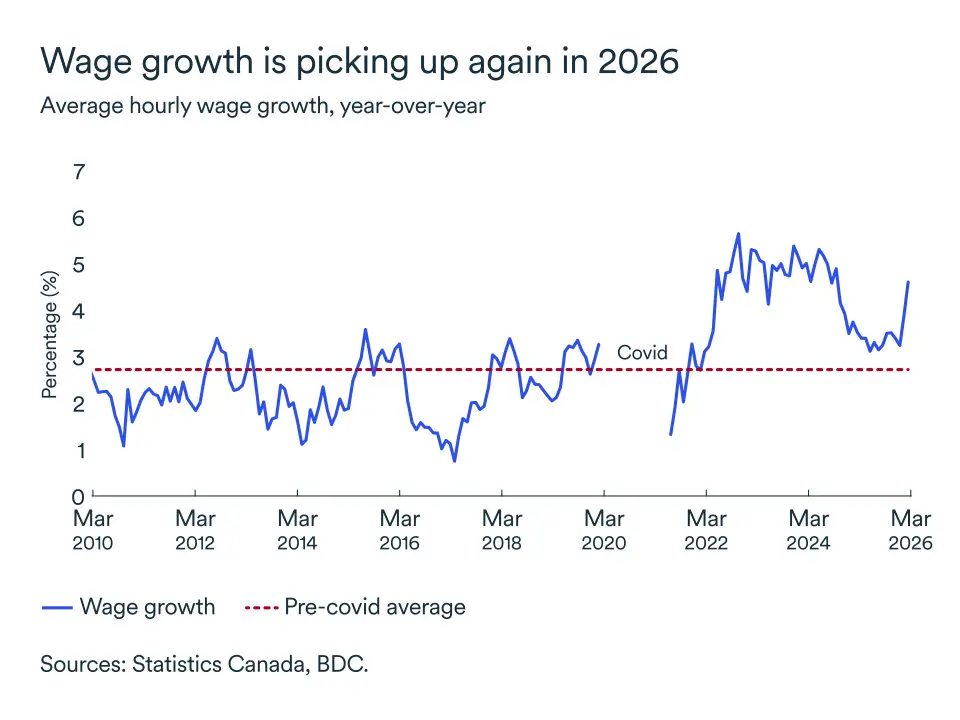

On the employment front, a slower economy means Canada is no longer dealing with a chronically tight labour market. But average hourly wages still increased by 4.7% in March, much higher than the latest inflation number (1.8%). For permanent employees, wage growth was even higher, over 5%.

Labour cost pressures may ease in the coming months since roughly 95,000 jobs have been shed in the country so far in 2026, putting the unemployment rate at 6.7%.

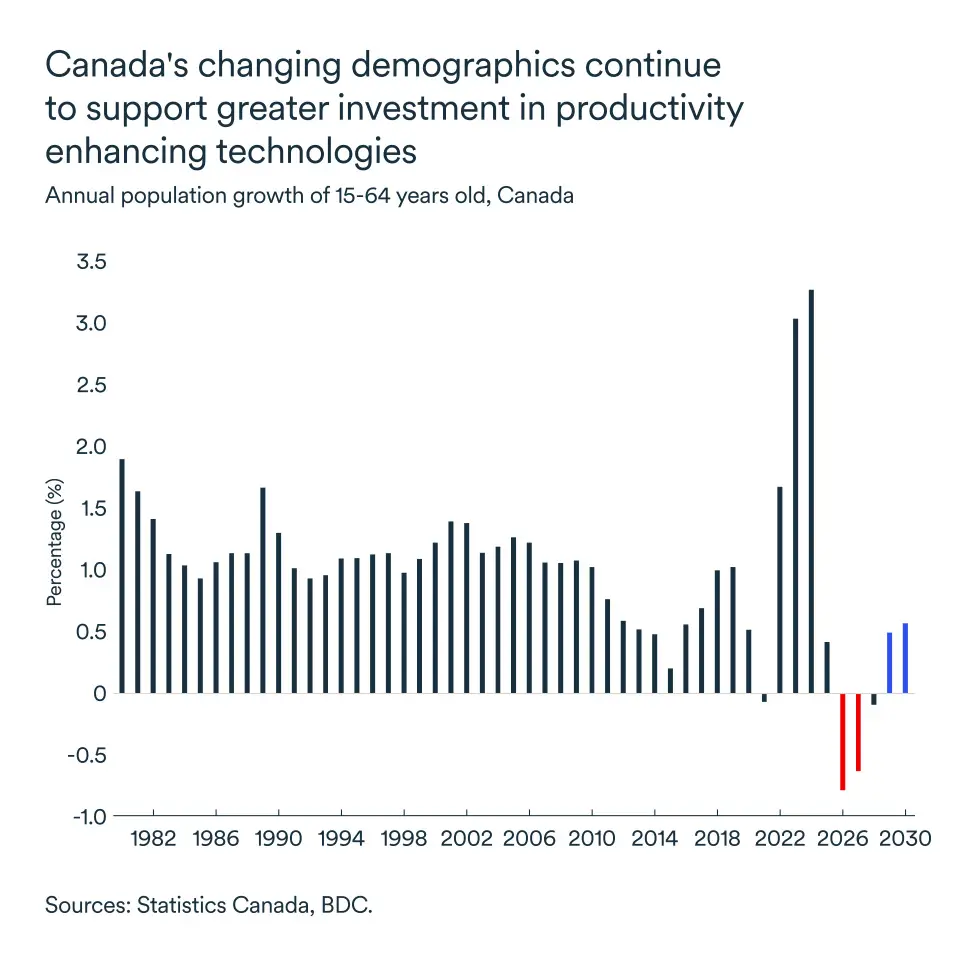

Still, Canada has long faced an aging workforce, and a recent decline in population growth is adding to labour scarcity, turning it into a structural feature of the economy that will keep wage growth elevated.

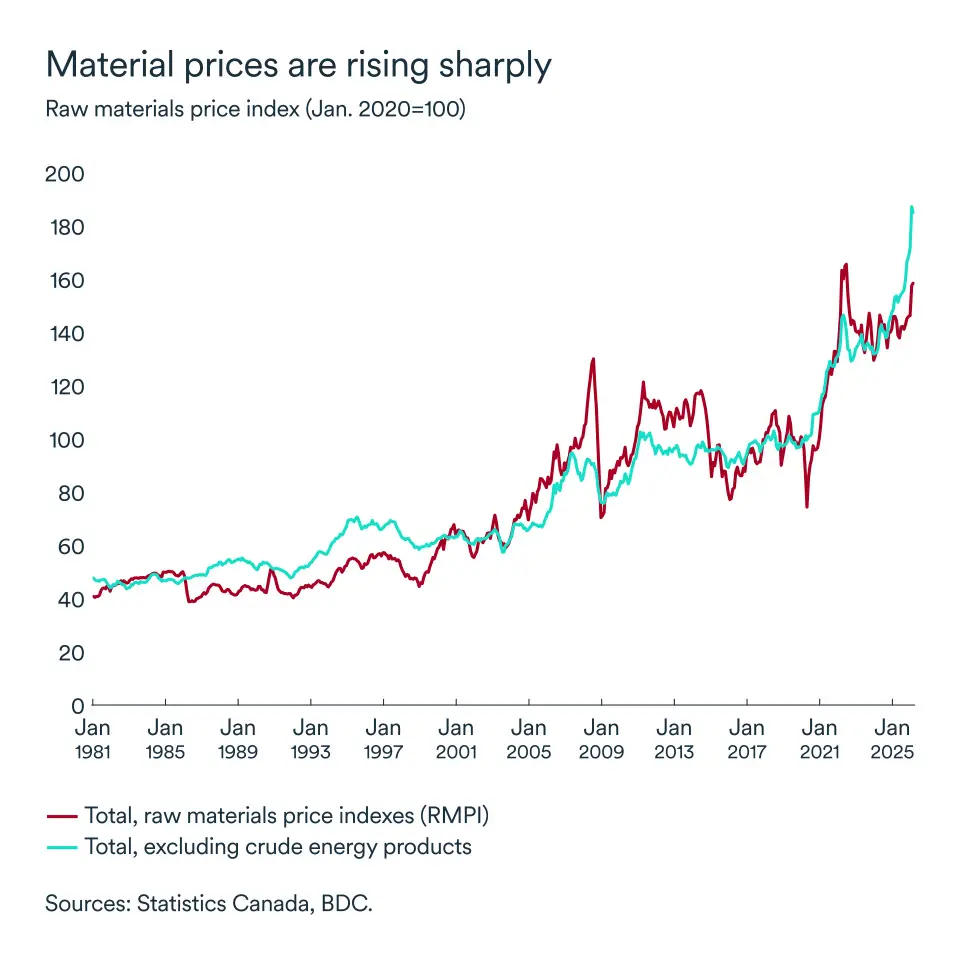

It’s a similar story for input costs, like materials and industrial goods. Here, businesses are facing acute pressure heading into spring. Canada's Industrial Product Price Index (IPPI) was up 5.4% year-over-year in February, rising to 6.4% when energy products were excluded. The raw material index, excluding energy, offered even greater cause for concern, jumping over 20% so far in 2026, a pace similar to what was experience in 2021, following the reopening of the economy during the pandemic.

Prices for crude oil and petroleum products have surged since beginning of war with Iran, but those increases haven’t been reflected in the data yet. Despite a sharp drop in the price of oil on April 8 with the announcement of a ceasefire, crude is still up by roughly 40 to 45% compared to the price before war and the closure of the Strait of Hormuz. Without a fast reopening of the strait, prices will remain high.

Trade headwinds are adding to costs as well

The global business landscape is becoming increasingly fragmented. Geopolitical tensions, the rise of protectionist industrial policies and tariff barriers are making supply chains more complex. Production and procurement costs are rising accordingly.

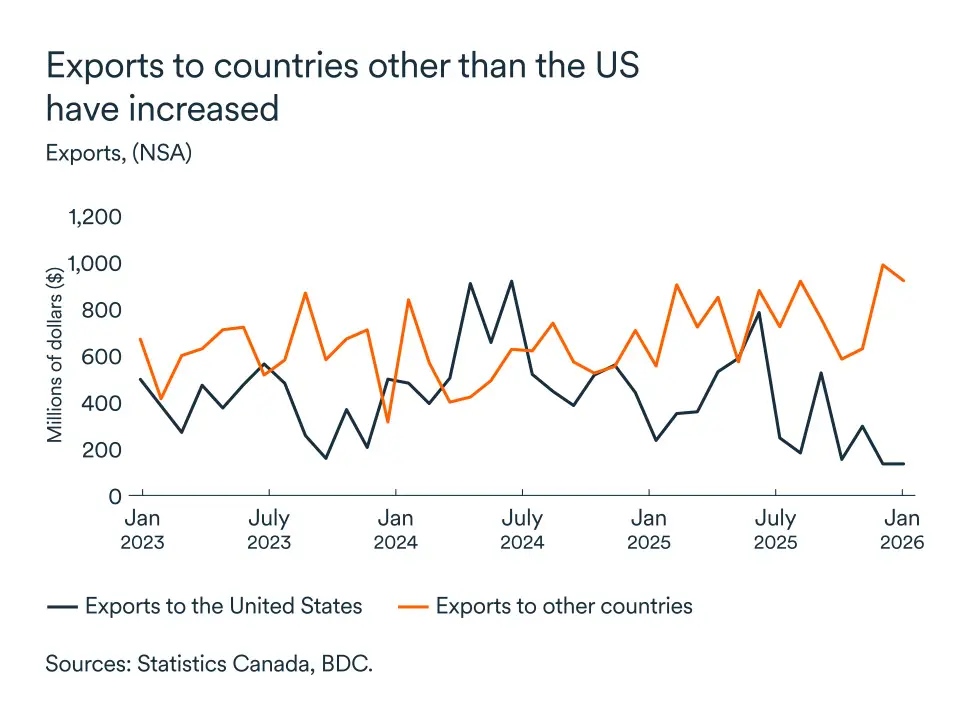

Heightened U.S. trade barriers have weighed on Canadian exporters, disrupting deeply integrated supply chains, particularly in the manufacturing and automotive industries. The reconfiguration of supply chains and search for alternative markets are adding upward pressure on production costs across the goods-producing sector.

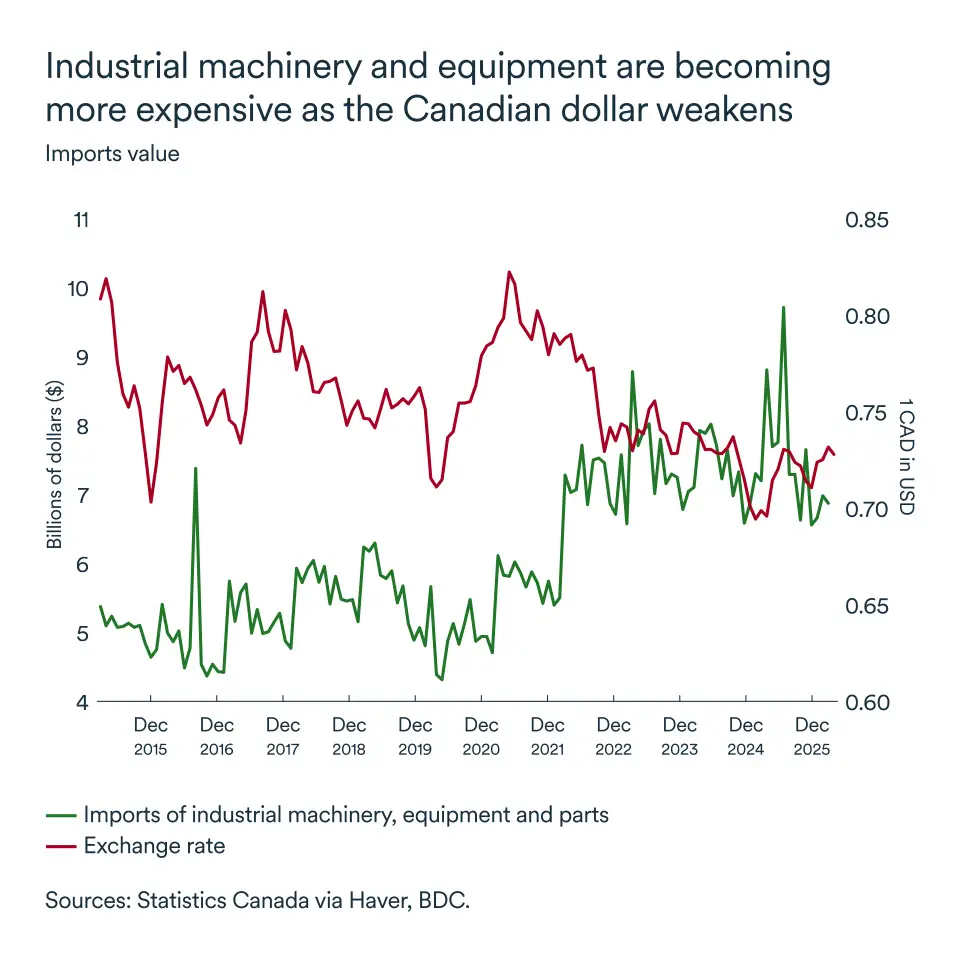

Compounding these issues, the Canadian dollar has depreciated to hover around US$0.72 in early April, pushing up the cost of imports, including the almost $90 billion in industrial machinery, equipment and parts Canada purchases abroad annually. Simply put, every 1-cent depreciation in the loonie adds roughly $900 million in annualized import costs for Canadian businesses.

Finally, while the Bank of Canada slashed its policy rate by more than half since its latest peak in 2024, interest rates are still higher than they were in the 2010s. It would be surprising to see rates go any lower, given the emerging risk of higher inflation, stemming from the Middle East conflict.

Taken together, these factors are reshaping the landscape. Above all, they point in the same direction: Rising costs are here to stay.

Margins under pressure

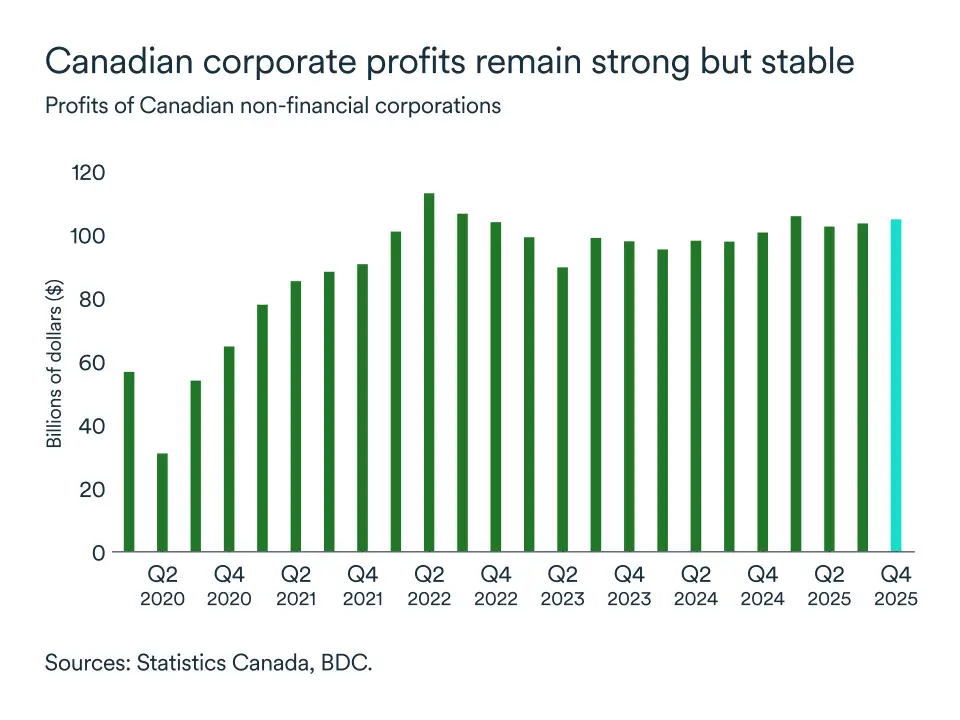

This new reality is already reflected in corporate profit margins. A recent BDC survey indicated that two out three businesses in Canada were profitable entering 2026. But entrepreneurs reported that their profits were weaker than at the beginning of the decade. After peaking in 2021—amid strong demand and the ability to adjust prices quickly—profit of non-financial firms declined in 2023-24 before stabilizing.

Businesses’ ability to pass rising costs on to consumers has become more difficult. After several years of high inflation, consumers are becoming more price sensitive and more selective in their spending.

For business owners, this creates a difficult dilemma. They have to choose between absorbing costs and watching margins shrink or raising prices and run the risk of hurting demand in an already soft economy.

Some best practices

In this context, certain realities become clearer, despite the high level of uncertainty we’re facing.

Prudent capital allocation and labour optimization have become key factors for all business decisions. This calls for greater discipline, planning and goal-setting.

Next, the need for greater productivity has shifted from a nice-to-have to a must-have. Investing in automation, digital technology and operational efficiency is often the best, most direct way to offset rising costs and maintain margins. This is also where competitive advantage is created.

Risk management, too, is becoming more important. In a more unstable world, relying on a single supplier or market becomes riskier. Diversifying supply sources, building greater flexibility into contracts and actively managing currency exposure are fundamental practices.

Finally, businesses must adapt to a new consumer landscape. The days when customers would easily absorb price increases are behind us. Successful businesses communicate their value proposition—and know when they can (or can’t) adjust their prices.

In an environment where costs are consistently higher, your company’s performance no longer depends solely on growth, but also on embracing strategies to strengthen your company and protect your margins.

Canada's economy is holding up in a difficult environment

Multiple forces are hitting the Canadian economy at once, and it’s this convergence that’s making it so hard for business owners to plan for the coming months and years.

With the current high level of geopolitical turmoil, including tariff changes and the on-going Middle East conflict, the risk of slower growth is real, but, for now, the Canadian economy is holding up.

A slow start to the year

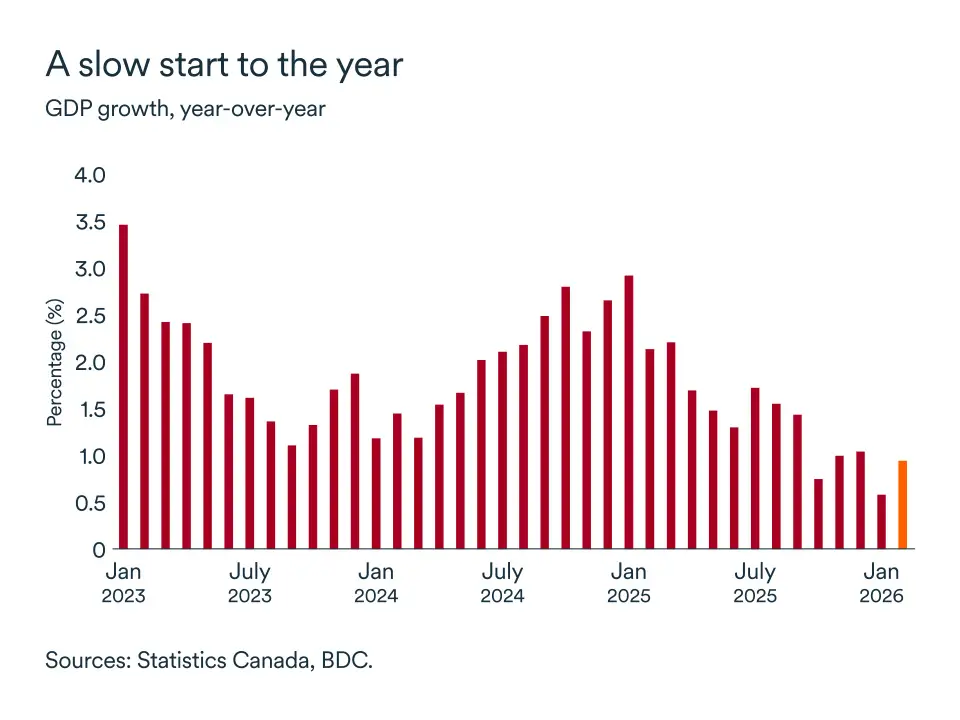

GDP growth has been decelerating for many months now, falling from a peak of nearly 3.0% in early 2025 to barely 0.6 % in January on an annualized basis. The February estimate shows only a modest uptick to under 1%.

Growth remains uneven with only 9 out of 20 industries covered by Statistics Canada expanding in January. Nonetheless, early first-quarter estimates suggest GDP recovered from Q4 of 2025, when the economy contracted by 0.6%. Canada should therefore escape two back-to-back quarters of negative growth.

BDC Economics still expects full-year growth to come in at around 1.0%, significantly below the economy’s 2.0% potential, meaning Canada isn’t in a recession but isn’t thriving either.

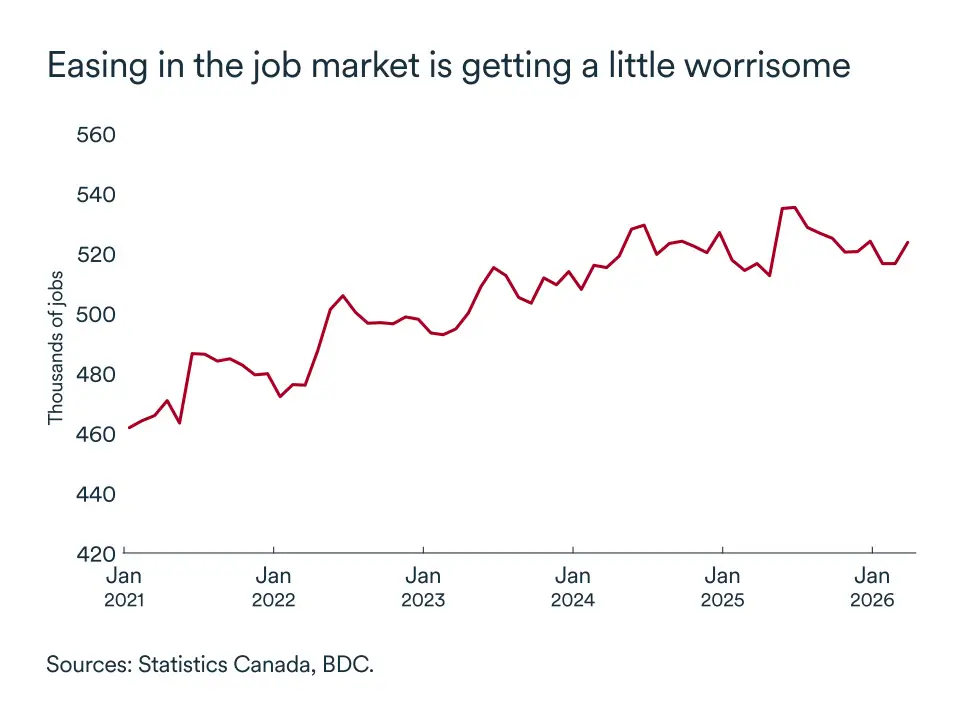

Job losses halted—finally!

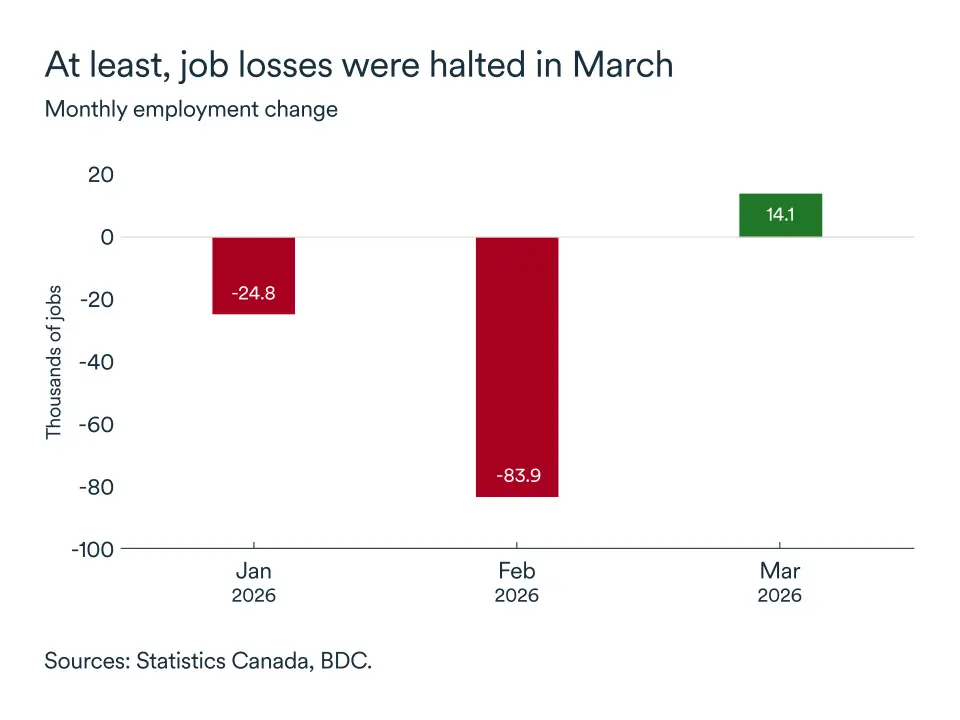

While GDP expanded early in the new year, it was a different story in the labour market. Canada shed 24,800 jobs in January and a steep 83,900 in February—numbers that triggered growing concern for the economy. However, March brought a rebound with the addition of 14,100 jobs.

This was encouraging, even if it didn’t fully make up for the damage earlier in the year. The unemployment rate sits at 6.7%, amid slower labour force growth and a hiring pullback by businesses. However, layoffs remain light, despite the cumulative 95,000 job losses in the first quarter.

Households are starting to spend again

Household spending was a bright spot to start the year, despite the soft labour market. Retail sales at constant 2017 prices climbed to $60.5 billion in January, matching the highest level reached in the past two years. This suggests that lower interest rates are encouraging consumers to spend.

For businesses serving domestic consumers, this recovery in consumer spending is good news. While it’s been bumpy, the direction in spending has remained positive in recent months. However, with the Middle East conflict and the accompanying spike in gasoline prices, Canadians’ budget priorities might start to shift. Indeed, consumer confidence has trended lower since the beginning of the war. Discretionary spending will be the first to feel the brunt of a more volatile economic context.

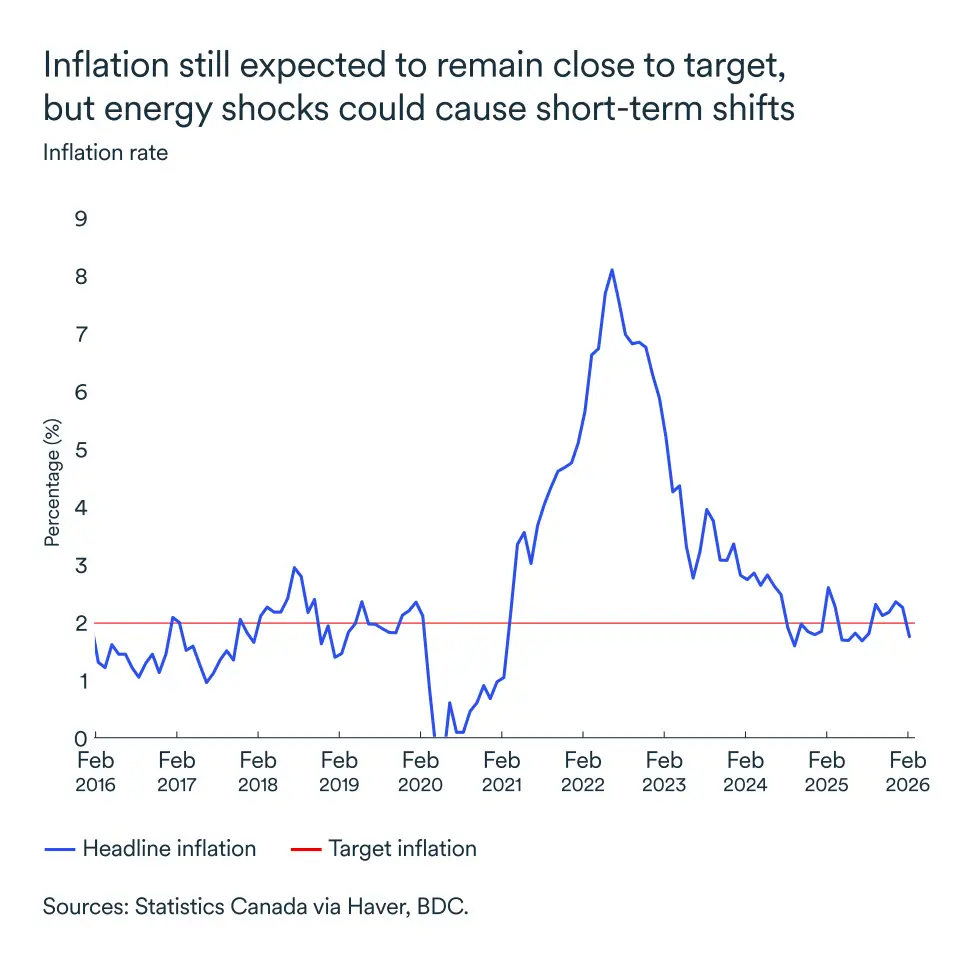

Canada’s inflation performance will be tested

After the price surge of 2022—when headline inflation rose to above 8%—Canada has largely won its battle against runaway prices.

As of February, inflation sat at 1.8% just under the Bank of Canada’s target. The bank’s policy rate currently stands at 2.25% and isn’t expected to move in the short term because the economy continues to struggle with excess capacity.

The energy shock from the Iran conflict is the wild card for inflation and, in turn, the Bank of Canada’s future decisions on interest rates. Energy prices remain roughly 45% above pre-conflict levels, and every month that passes without a resolution will add upward pressure on operating costs, commodities and markets.

The impact for your business

- Protect your cash flow now. With GDP growth hovering near 1% and consumer recovery still in its early stages, revenue growth will be positive yet modest.

- Watch your input costs closely. Energy and supply-chain costs remain elevated. Review your supplier contracts, explore domestic alternatives and identify where you can absorb costs versus where you can pass them on.

- Develop strategies to take advantage of changing consumer behaviours. Household spending has started to increase again, and the Buy Canadian trend continues. If your business serves Canadian consumers, this is a good time to review your pricing strategy and product offerings.

- Stay flexible on investments in your business. The Bank of Canada is unlikely to cut rates further in the near term. Focus capital expenditures on productivity and efficiency improvements—investments that pay off regardless of the economic cycle.

British Columbia

The B.C. economy has had a difficult start to 2026, with employment stuttering and growth in retail sales slowing versus their elevated 2025 levels. We still expect the economy to grow this year (by roughly 1%), but repeated shocks to global supply chains and a weak housing outlook for both the U.S. and Canada threaten to muddy the path of growth meaningfully.

Employment in March declined once again, with a loss of nearly 20,000 jobs. When combined with the decline in February, employment is B.C. was nearly 40,000 lower than in the first month of the year. The lion’s share of this decline was in the services sectors, while goods-production held up relatively well (only 2,000 jobs lower than the January level). The unemployment rate in the province rose to 6.7% in March, which was the highest level in decades when excluding the spike during the pandemic.

Retail sales were marginally positive in January (+0.2% month-over-month), but the rate of growth has flattened versus a strong second half of 2025. While interest rates have moderated and households should feel slightly less burden from their comparatively elevated debt levels, consumption fundamentals have been hurt by weaker labour markets and persistent uncertainty around trade.

There is still some upside to B.C.’s outlook, with several large capital projects in the works which will generate demand for businesses in the construction, logistics and manufacturing sectors. Still, global supply shocks and a weak lumber market threaten to pour cold water on what is an adjustment year for the B.C. economy.

Alberta

Alberta's GDP growth, which was on track for 1.8% in 2026, has been upgraded to above the 2.0% mark. The improvement reflects a combination of higher oil prices and stronger-than-expected economic performance in late 2025 and early 2026.

While the economic outlook improved, employment was roughly stable in the first quarter. Some 25,000 jobs were created, but the vast majority of the hiring occurred in January. The unemployment rate ticked higher to 6.5% in March.

Retail sales reversed their December decline, surging 3.5% in January, month-over-month.

Oil production continues at strong levels with Q1 averaging 4.2Mb/d, an increase of 3.3% compared to 2025. Crude oil price worldwide were still up significantly at the beginning of April pushing to US100 a barrel. Meanwhile, the WCS differential has widened to approximately US$16.25/bbl below WTI.

Depsite the increasing gap, the province will benefits from higher oil prices and ramped up production.

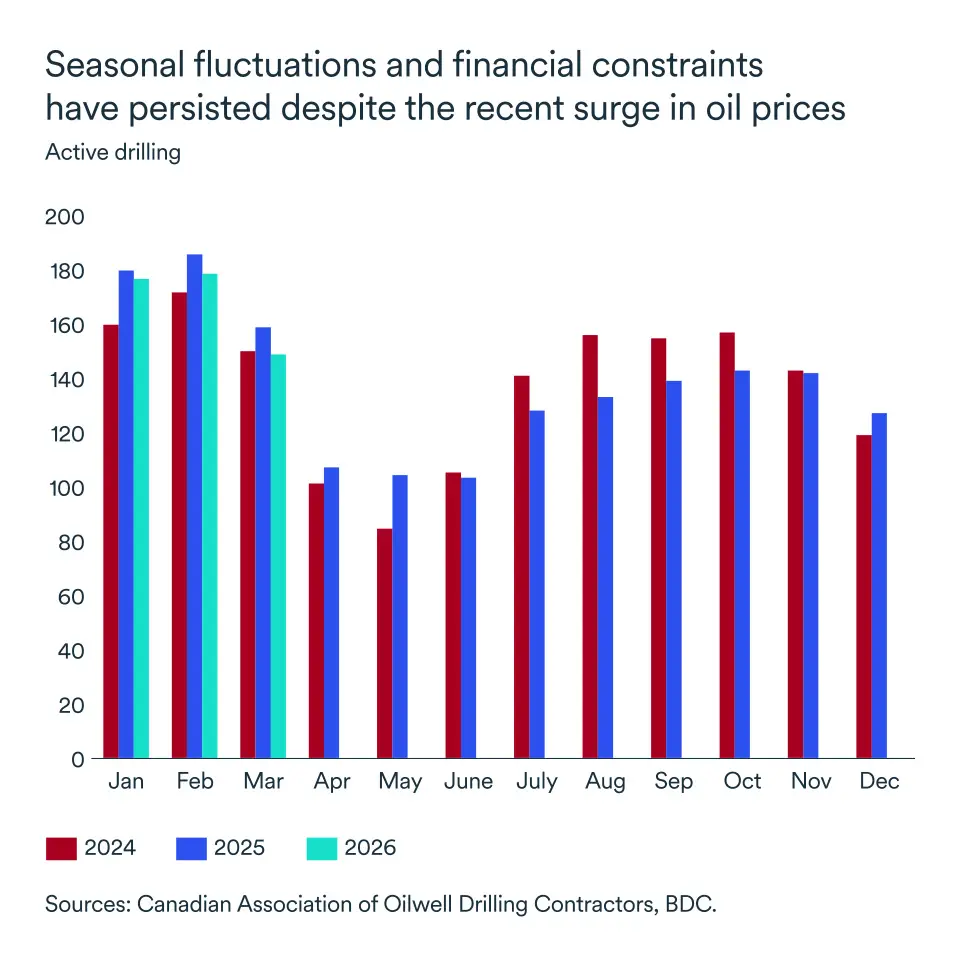

Drilling activity was lower than last year, indicating a somewhat tougher seasonal adjustment. However, as Middle East tensions escalate, Alberta producers are well-positioned to increase production while still maintaining capital discipline given the recent higher prices.

Saskatchewan

As a commodity driven province, Saskatchewan’s economy is set to grow at near potential in 2026, maintaining its position among Canada’s top-performing provinces, just behind Alberta. In the wake of a Canada-China agreement to lower tariffs on canola and other agricultural goods, we expect momentum to build in Saskatchewan’s economy.

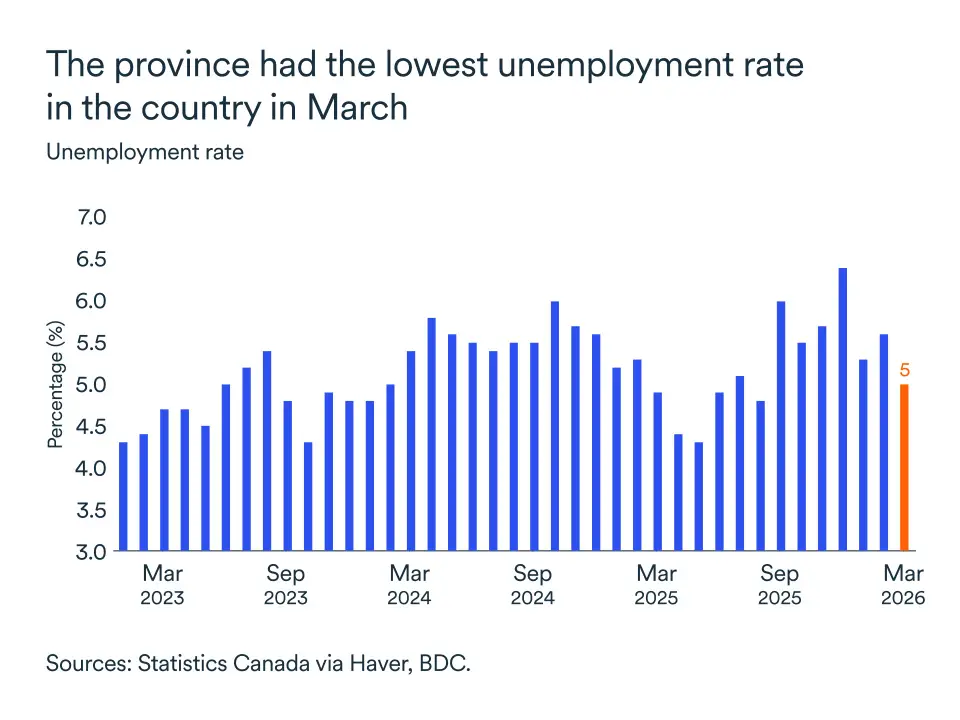

The labour market has strengthened considerably. Saskatchewan added 5,800 jobs in March and the unemployment rate came in at 5.0%—the lowest among the provinces and well below the national average of 6.7%. For the year to date, the province also posted record highs in labour force participation and full-time employment, two indicators supportive of consumer spending.

On the agricultural trade front, the Canada-China deal announced in January has now taken full effect. As of March 1, China reduced its tariff on Canadian canola seed to 14.9% from a combined level of nearly 85%, suspended tariffs on canola meal entirely through the end of 2026 and lifted tariffs on peas. However, fertilizer costs have been on the rise because of the conflict in the Middle East.

Mining of potash and uranium are both set for strong results and will also support growth in 2026.

Manitoba

Manitoba's economy is forecast to grow modestly by around 1.2% in 2026. This is a slight upward revision from the 1.0% projected earlier in the year, but still broadly in line with the national average.

The recently announced provincial budget included a few measures that should provide relief to household budgets and support spending. For instance, the province will suspend the 7% PST on all grocery food item starting July 1.

After a tepid start to the year, the labour market finally took a turn for the better in March, allowing Manitoba to join the other Prairie provinces in leading the country in job creation. Manitoba generated roughly 11,000 jobs in March, the vast majority being full time. The unemployment rate held steady at 5.6%.

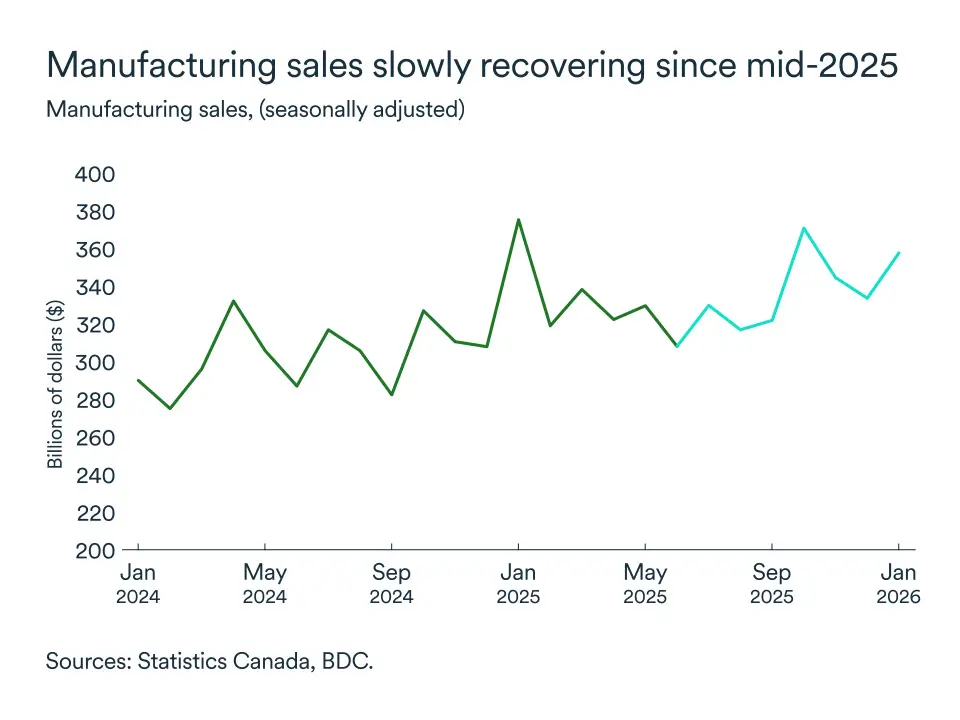

Manufacturing shipments remained under pressure. Sales in the sector were down 8% in January, compared to last year. The weakness reflected an economic slowdown that hit the province following the imposition of tariffs, mainly on agricultural goods.

Food manufacturing accounts for almost a third of the province’s total manufacturing sales. Grain and oilseed manufacturing, declined by 10.1%, largely due to lower canola oil and meal prices. But Chinese demand should support price increases now that many tariffs against Canada’s agrifood sector have been lifted.

However, caution is warranted. The uncertain trade situation and high energy prices could hurt the transportation sector—a key industry for Manitoba’s economy.

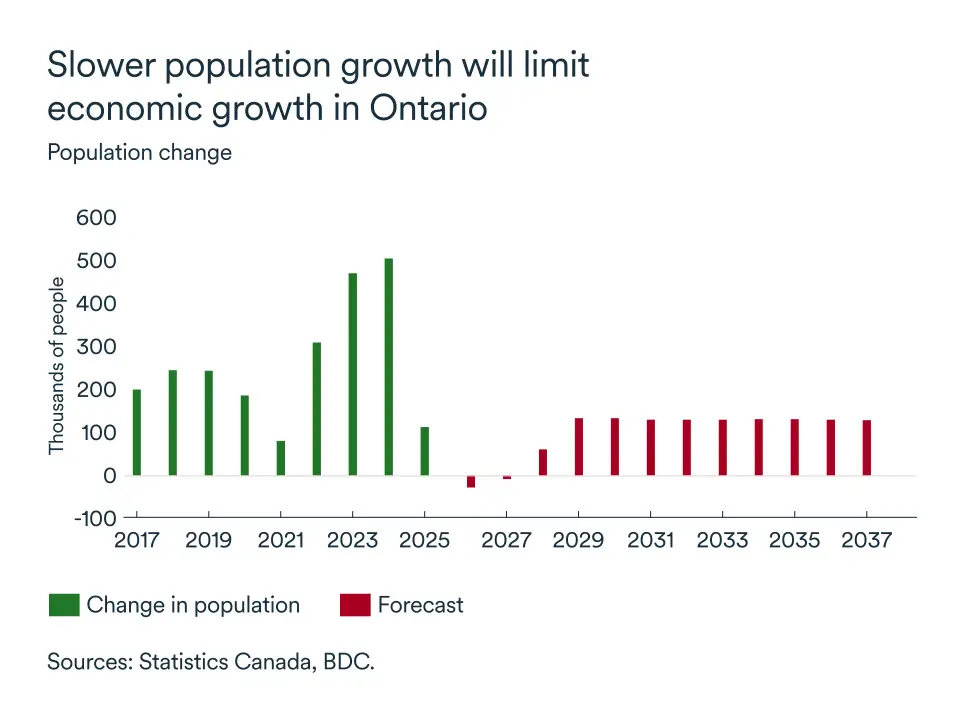

Ontario

Slow population growth will limit economic growth in Ontario this year.

First-quarter employment data show that Ontario’s economy is off to a slow start. Tariffs introduced a year ago continue to weigh on the manufacturing sector.

Furthermore, slow population growth is also limiting growth. Over the past five years, Ontario’s population increased by 1.5 million people but is expected to grow by only 300,000 over the next five years.

This decline is due to a significant drop in the number of study and temporary work permits, as well as a reduction in immigration thresholds. The slowdown is already impacting the housing market, particularly in the Greater Toronto Area. It is also affecting the post-secondary education sector and will limit consumption growth. Businesses will need to invest more in automation and technology to cope with a tighter labour market.

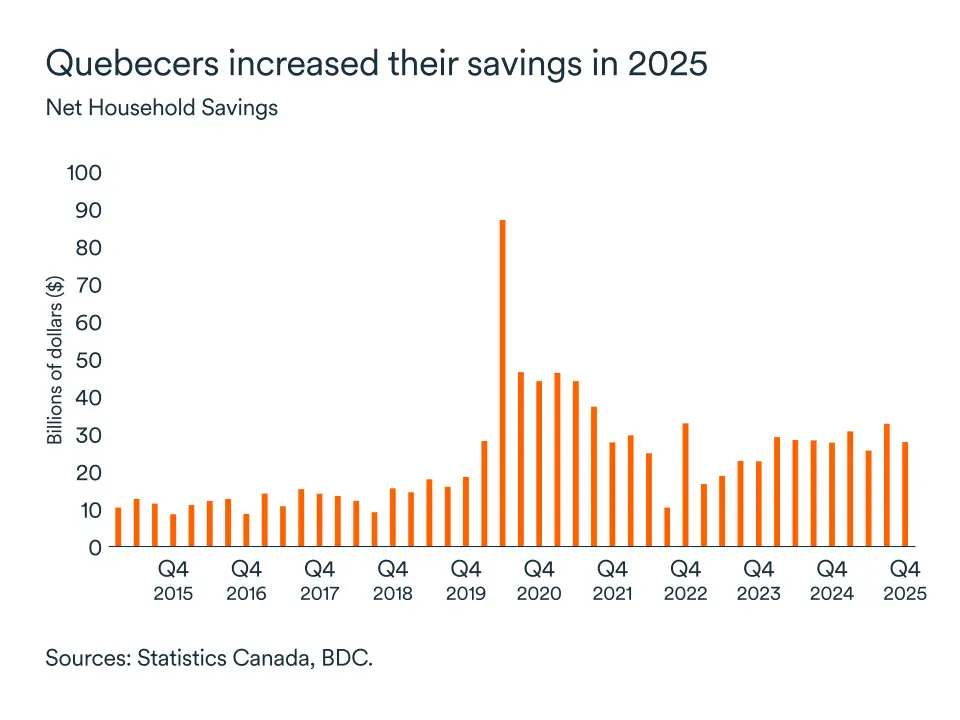

Quebec

We still expect the province to grow a modest 0.8% in 2026, dragged down by lower external demand for tariffed goods, continued uncertainty and lower population growth.

Exports regained some strength in February, when they increased by 6%, but they remain under pressure from U.S. tariffs.

The job market in Quebec is showing signs of softening. Following a significant decline in February, jobs gains were modest in March, when the province added around 10,000 positions. The unemployment rate remained among the lowest in Canada due to demographic factors.

Households increased their savings in 2025 amid an economic slowdown. A solid labour market and faster wage growth helped Quebecers build up their savings cushions. However, as uncertainty lingered, the real estate market remained under pressure for most of the year and into 2026. A small uptick in home sales in February was welcome news but a sustained upward trend has yet to be seen.

Nova Scotia

Exports increased slightly in February after several months of decline. However, the effects of U.S. and Chinese tariffs continue to weigh on the province.

Employment weakened in the first quarter of 2026, decreasing by almost 3,000 jobs. Most of the losses were in the first two months of the year. The job market has been adding fewer jobs since 2024, a trend that corresponds to a slowdown in economic growth in 2025.

Easing of trade tension with China should help the province, boosting exports and lending support to the job market. The province is on track to grow around 1.2% in 2026, slightly exceeding the national average.

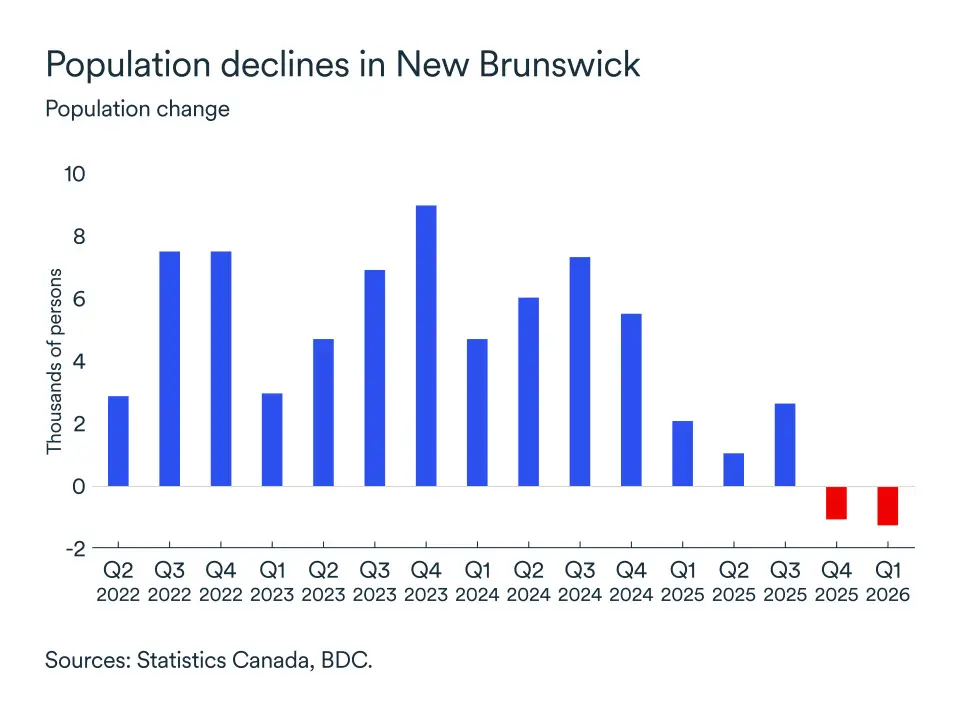

New Brunswick

Population declined in New Brunswick in the last two quarters following caps on temporary immigration in Canada. Lower population growth means slower increases in consumption, less housing demand and, of course, fewer available workers. All in all, it will limit growth in the province this year.

Exports remained under pressure, declining once again in February. While most provinces saw upticks in trade, the province continued to experience weakness.

The job market gained some traction in March after a slight decrease in February. Employment levels remains relatively high, supporting households in the province.

The province’s economy is expected to grow 0.9% in 2026, lagging its peers in the Atlantic.

Prince Edward Island

Trade remained under pressure in the province, with exports declining for the second consecutive month in February. The sharpest declines are still concentrated in tariffed goods, such as seafood. However, the island remains on track to grow 1.2% in 2026.

]The job market shed some jobs in March, but the first quarter levels remained higher than the fourth quarter in 2025. The unemployment rate remained low at 7.3% in March, down from 7.9% in same period last year.

The main driver of modest economic growth this year will remain a resilient job market, which should support consumer spending and housing activity in the province. An improvement in trade relations with China will bring much needed relief to certain parts of the economy.

Newfoundland and Labrador

The province has slowly been increasing its exports to non-U.S. countries in the past year. While total exports in 2025 initially appeared to be similar to those in 2024, initiatives to diversify trading partners helped counterbalance significant losses caused by decreased U.S. demand.

Oil producers in the province are benefitting from higher prices caused by the Iran conflict. If talks between the U.S. and Iran turn out to be successful, and the Strait of Hormuz fully reopens, prices should slowly return to pre-war levels.

The job market remained stable in March. Strong job numbers will help households and boost consumer spending. GDP is expected to grow 1.1% this year, slightly outperforming the national average.