Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreShould we be concerned about rising trade tensions with China?

New Canadian import tariffs on Chinese electric vehicles came into effect on October 1 and were accompanied by the official list of steel and aluminum products from China that will be subject to surtaxes this month. The surtaxes will increase costs for Canadian companies that source these products from China. What impact will these measures have on the economy and what are the implications for businesses?

New protectionist measures against China

A new 100% tariff on imports of Chinese electric vehicles (EVs) came into effect on October 1, raising customs clearance fees from 6.1% to 106.1%. In addition to electric vehicles, the new protectionist measures also include a 25% surtax on imports of steel and aluminum products from China. The list of intermediate products subject to these new tariffs is now available (here).

Typically, protectionist measures of this kind tend to reduce trade and investment, slowing economic growth. So why implement such measures now?

Broadly speaking, the federal government's objective is to protect the automotive, steel and aluminum sectors, as well as the investments being made to achieve carbon reductions.

Both Canada and the United States are working to curb China's dominance of electric vehicles and they’re not alone. The European Commission also recently decreed an increase in taxes, currently at 10%, on electric vehicles imported from China, effective November 1.

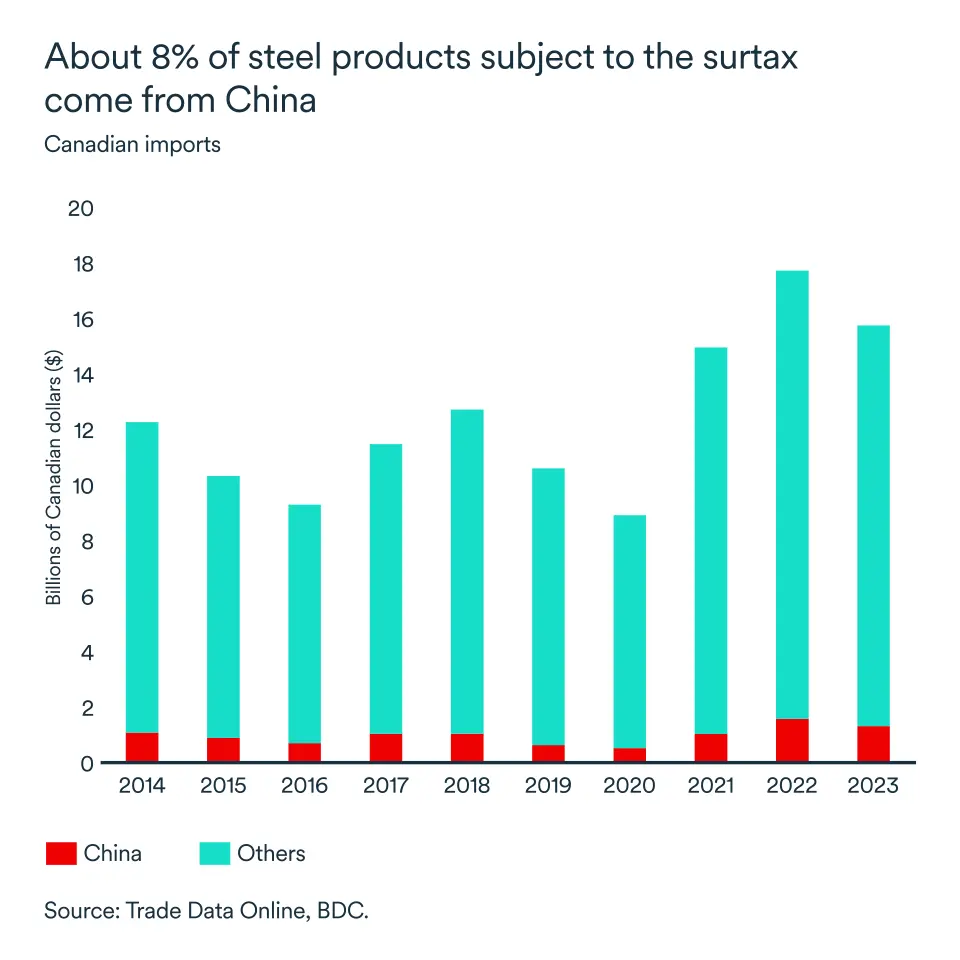

In 2023, total EV imports to Canada from China amounted to $2.3 billion, a massive increase from $116 million in the year prior. This represents over 13 % of all electric vehicles imported in the country.

The impact should be more severe for the aluminum market since more than a fifth of Canada's aluminum imports come from China, but only about 8% of the country's total imports of steel.

Who's at risk?

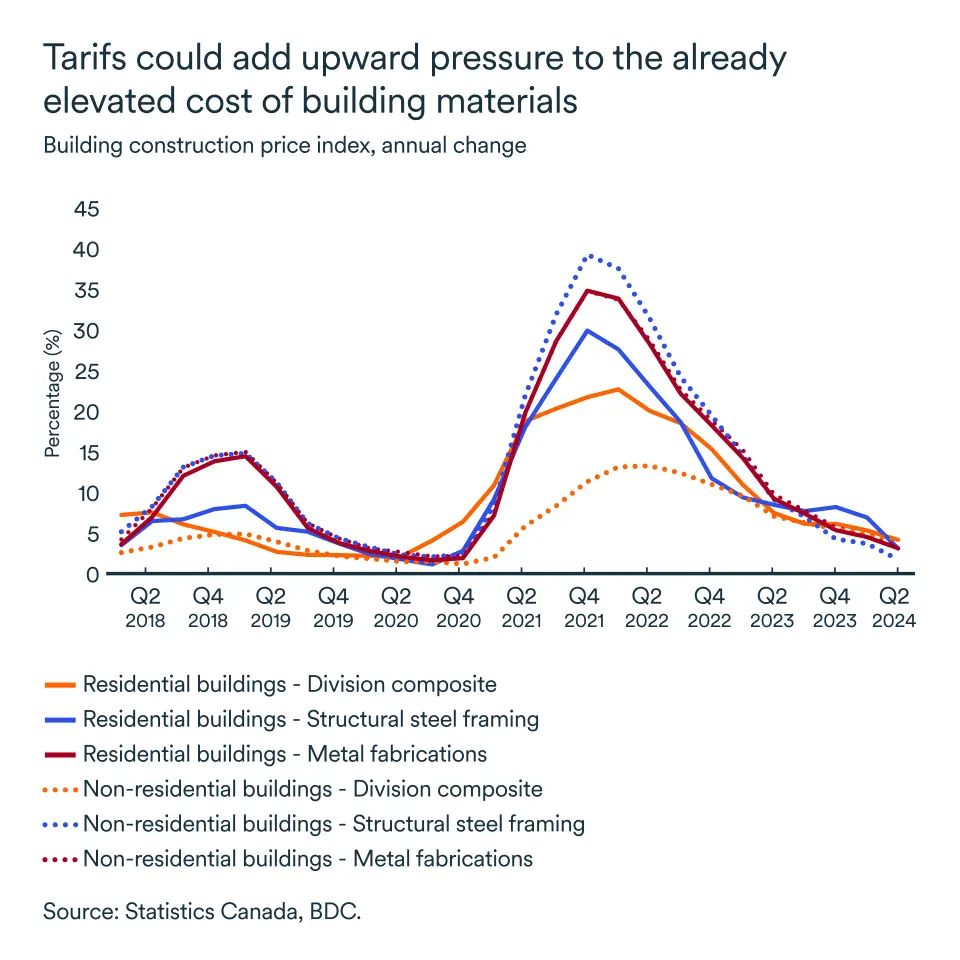

The construction and manufacturing machinery sectors are among the Canadian industries that will be most affected by the steel and aluminum tariffs. With inflation already high in these sectors, the new measures are likely to create further distortions in these key industries, including disrupted supply chains and higher material costs.

For industries not directly affected by the new tariffs, the risk of retaliation by China is the key concern. Although the U.S. remains our main export market, China is our second most important trading partner. Chinese authorities already announced an anti-dumping investigation against Canadian canola oil producers shortly after the steel and aluminum tariff increases were confirmed.

While tariff costs are often absorbed by producers initially, over time they can lead to higher inflation and slower growth—not a good combination.

Nevertheless, Canadian producers of the targeted metals stand to gain from the situation as they seek new customers. From a regional standpoint, Ontario and Quebec are home to the majority of steel and aluminum producers and therefore central Canada will benefit most from the tariffs on Chinese product.

Potential gains will be more limited in other regions of Canada. Moreover, on an economy wide scale, metal-consuming industries account for a much larger share of the economy than metal-producing industries.

Will this have an impact on inflation... and therefore interest rates?

The new tariffs will mean higher prices for Chinese EV buyers, of course, but also for some Canadian businesses.

Beyond electric vehicles, Canadian small and medium-sized businesses that import steel, aluminum or any other product on the tariff list will see their competitiveness deteriorate, as this is new cost and trade uncertainty is added.

Customs duties are essentially a tax—increasing costs for both companies and consumers. If companies can’t raise prices to customers sufficiently to make up for this new cost, they are forced to absorb some or all of it, reducing their profit margins.

It would be surprising to see prices rise too quickly, and therefore forcing the Bank of Canada to slow the pace of its rate cuts to keep inflation under control. It could lead to rising inflation and slowing growth, a double whammy that’s feared by economists and central bankers. Without massive escalations to the trade conflict, this is solely a new risk for the Canadian economy, one that remains subdue for now.

What does this mean for your company?

- Trade protectionism has been on the increase in recent years and is not going away in the short term. Whether tariffs are imposed by or against Canada, and regardless of the industries affected by the measures, protectionism creates uncertainty for businesses. It’s important to remain optimistic while staying vigilant about how to weather the storm. Diversification is often a winning strategy.

- Continue to invest in your business, adapting your products and services to new markets, both in Canada and abroad. Find out about the trade agreements Canada has signed with often overlooked partners, such as the European Union (CETA) and many Pacific Rim countries (CPTPP).

- Invest in employee training to help them adapt to changing technology and improve productivity and efficiency. This will help your company to remain competitive in an uncertain environment.

Canada’s economy is in a holding pattern

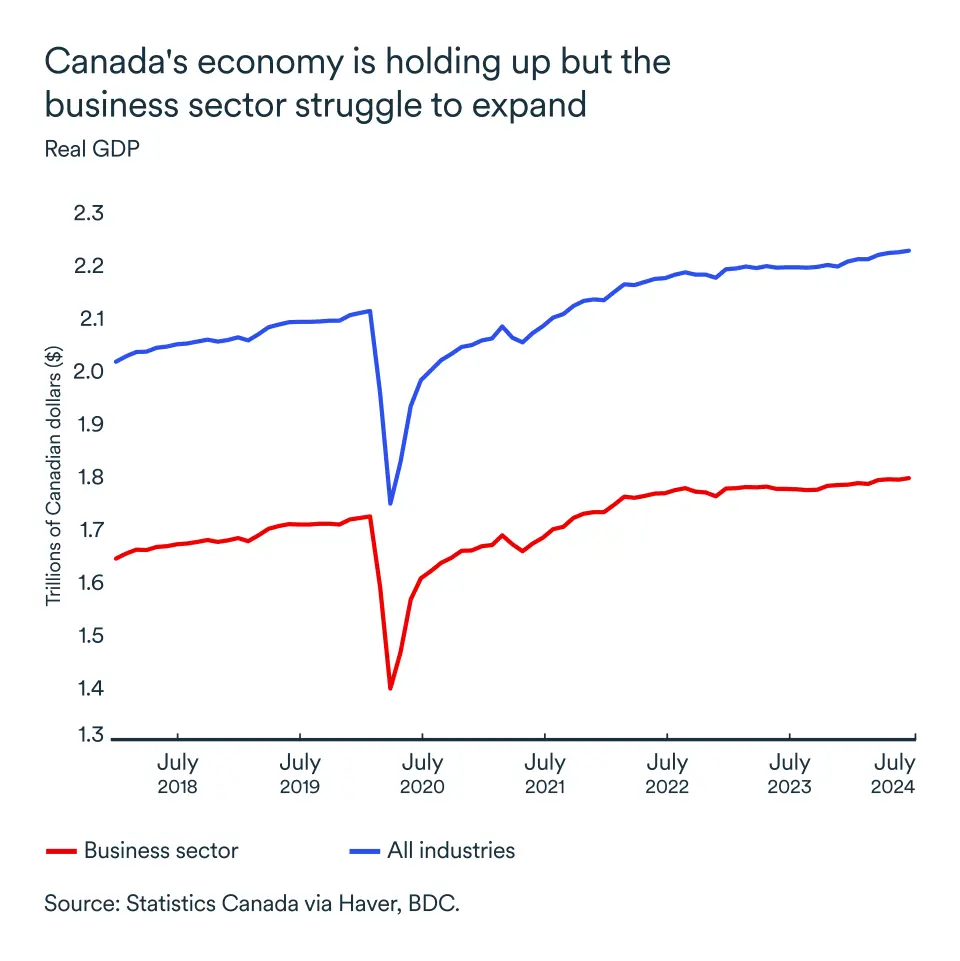

As we entered the final quarter of the year, challenges for the Canadian economy continue to mount, amid still high interest rates that are weighing on many households and businesses. Following a sluggish third quarter, we expect the economy to remain in neutral in the months ahead.

After registering no growth in June, the economy produced a slight uptick in July (+0.2% real GDP). Gains were made in both goods and services producing industries, according to Statistics Canada. The retail sector was the biggest contributor to growth in July, posting its largest monthly gain in over 18 months at +1.0%.

For August, Statistics Canada forecasted another month of neutral growth. If confirmed, this would have actually been a commendable performance in the context of Canada’s ongoing economic slowdown.

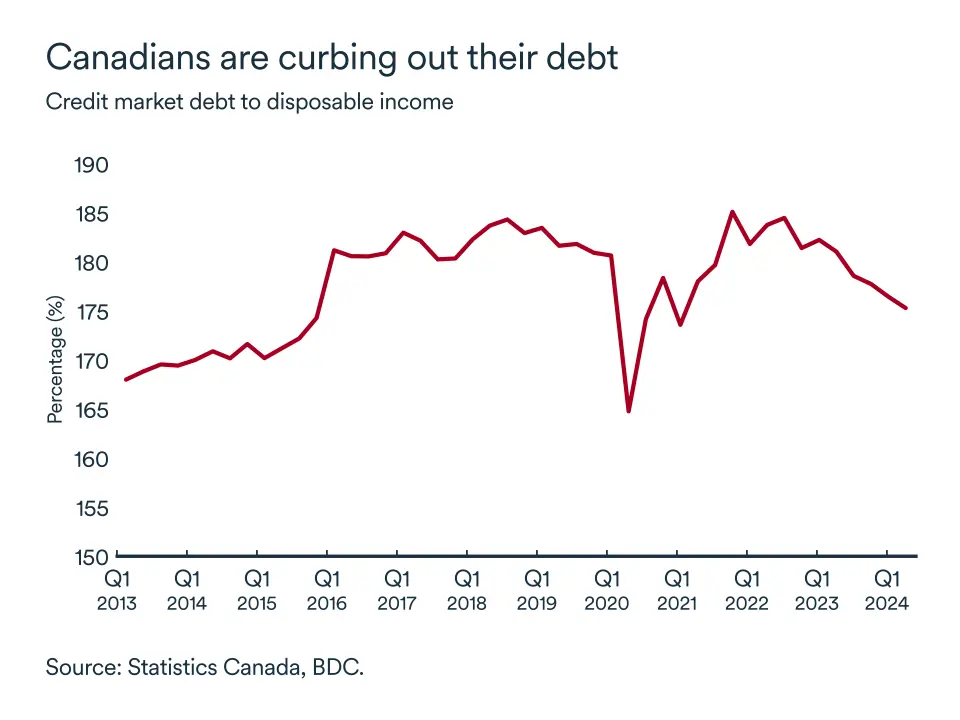

Households pay down debt

A return to solid economic growth will depend primarily on households since consumer spending accounts for 60% of GDP in good times and bad. Despite interest rate cuts by the Bank of Canada since June, borrowing costs remain relatively high and consumers continue to be cautious.

However, household debt as a proportion of disposable income continued to fall in the second quarter, reaching 175.5—the lowest level since the first quarter of 2021. This implies that income growth has outstripped credit growth, a positive sign that the Canadian economy is becoming less reliant on consumer debt.

Rate cuts are unlikely to increase the pace of borrowing unduly in the second half of the year because the interest rate level is still restrictive. Households remain cautious about spending as evidenced by rise in the savings rate in the second quarter.

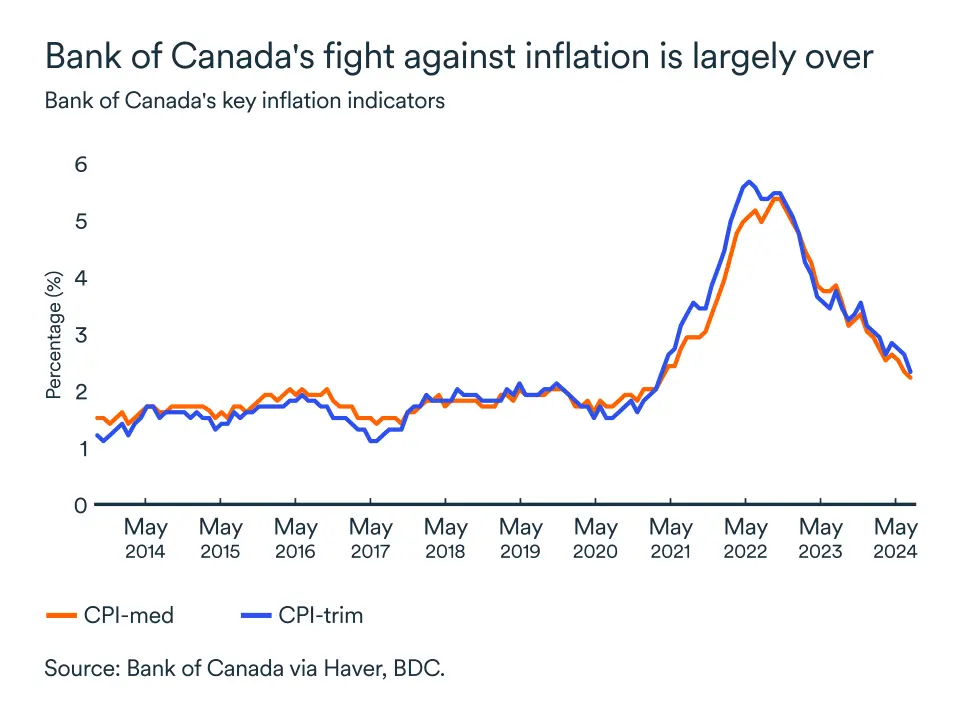

Inflation back on target

The Bank of Canada would have found much to celebrate in its latest inflation report. Not only did headline inflation as measured by the Consumer Price Index (CPI) slowed below the 2.0% target mark in September at 1.6%, but the central bank’s preferred core measures also saw significant declines compared to August.

These declines are supportive of more interest rate cuts. The economic slowdown, though well entrenched, isn’t at a pace that will be alarming to the Bank of Canada. Therefore, we expect the bank to stick to its game plan and cut the key rate by a further 25 basis points at its October meeting, but the economy and inflation could very well support a bigger cut.

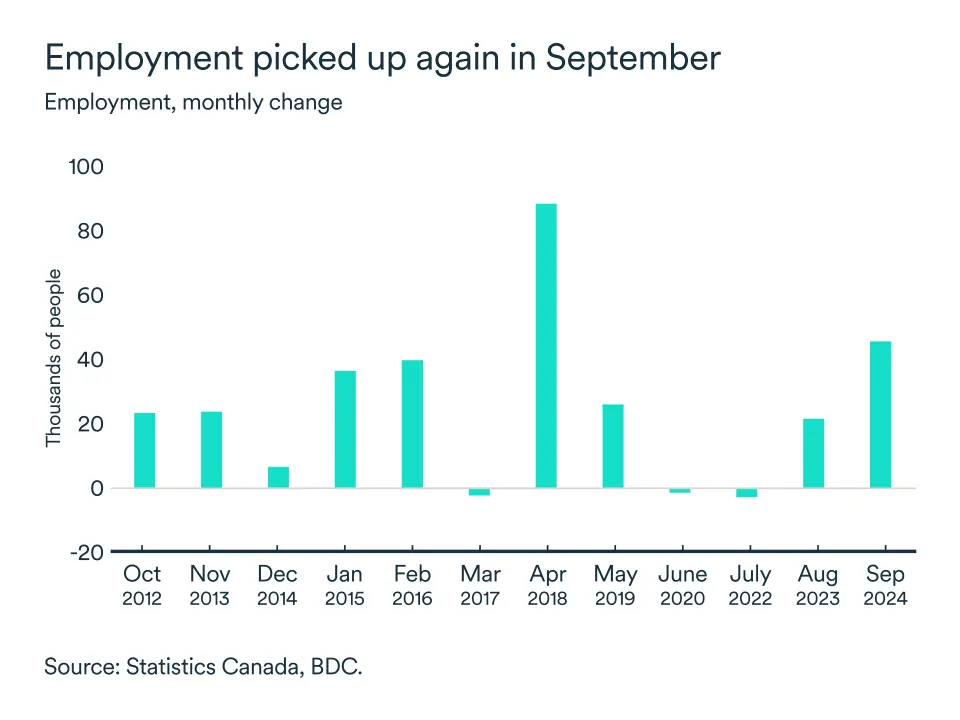

Lower unemployment rates

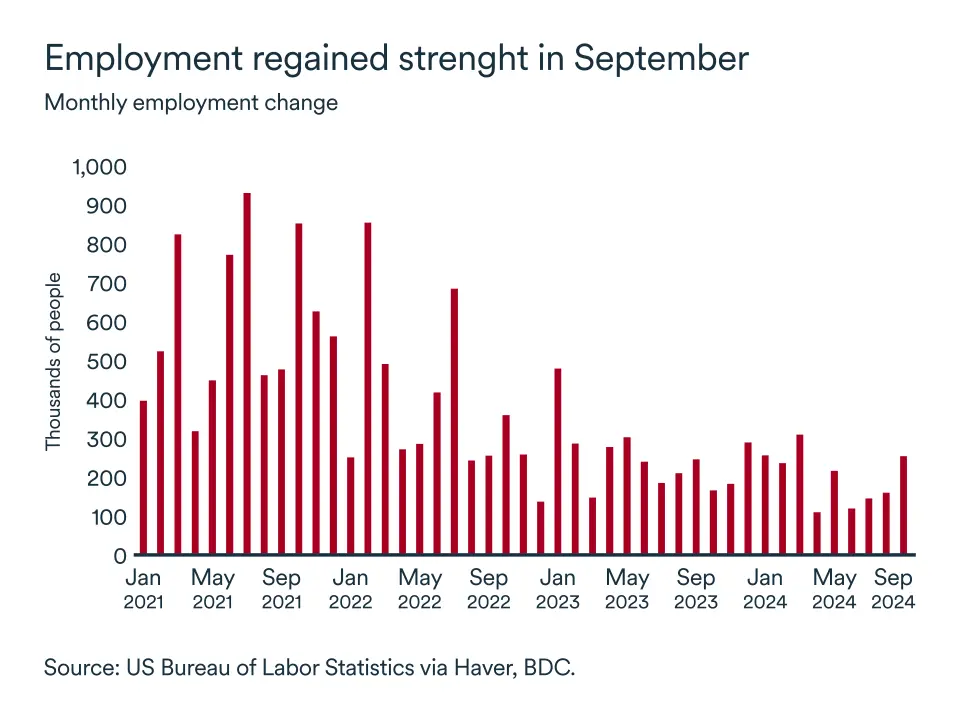

The unemployment rate ticked down in September for the first time this year, reaching 6.5%. Job creation has changed little from month to month since May but ended the third quarter with a bang. In September, 47,000 jobs were created across Canada, compared with 22,000 the previous month. Another good news is that employment gains were concentrated in the private sector (+61,000), a likely indication that businesses are slowly regaining their footing.

Since the start of 2024, overall job creation has amounted to 257,500, yet the unemployment rate has risen consistently every month (other than the recent drop in September) as the pool of workers increased. Hiring difficulties are likely to slow further in relation to an increasing labour supply.

In July, the number of vacancies fell further to just over half a million, almost half the peak reached in May 2022. A wave of retirements continued in August, at a year-on-year level of 310,400.

The impact on your business

- Consumers remain cautious and will continue to postpone purchases of expensive items or turn to substitute products to avoid borrowing more. Find out how you can improve the value of your offerings to maintain sales. Make sure your inventories are well managed.

- Interest rates should continue to fall at a steady pace. This is a good time to review your growth prospects and medium-term development plans in anticipation of a stronger economy ahead.

- The economic slowdown is still very much with us and it's not too late to adopt good practices and adjust your company's finances accordingly. It will take time for interest rate cuts to generate momentum in the economy.

U.S. economy still on track for a soft landing

The U.S. economy remains healthy with many indicators still pointing to a soft landing for our southern neighbour, which could lead the Federal Reserve to slow the pace of interest rate cuts.

At its September meeting, the Federal Reserve made its first rate cut, opting for a reduction of 50 basis points. Before the announcement, economists were in agreement that the Fed would lower rates, but there was no consensus on how large the cut would be.

While consumer and business spending has remained strong despite high interest rates, the balance in favour of a more aggressive cut seems to have been tipped by weakening labour market conditions over the summer.

However, the labour market slowdown appears to have been short-lived. In September, hiring picked up again, with a total of 254,000 jobs created. And revisions to the July and August data took average monthly job gains in the third quarter to 186,000.

Indeed, the U.S. economy continues to grow at a good pace, having expanded by 3.0% in the second quarter, a healthy improvement on the first quarter’s 1.6%. Q2 growth was driven by consumer spending, inventory restocking and non-residential investment.

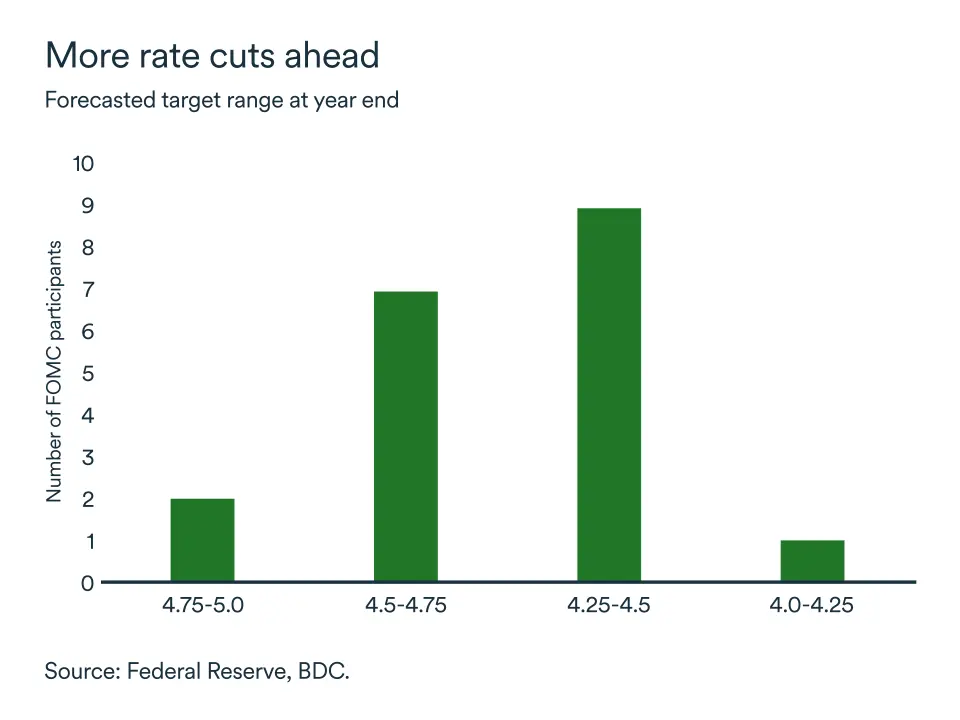

The target range for the federal funds rate is now 4.75%-5.0%. The majority (17/19) of participants on the Federal Open Market Committee believe that at a minimum a further 25 basis points should be cut by the end of 2024.

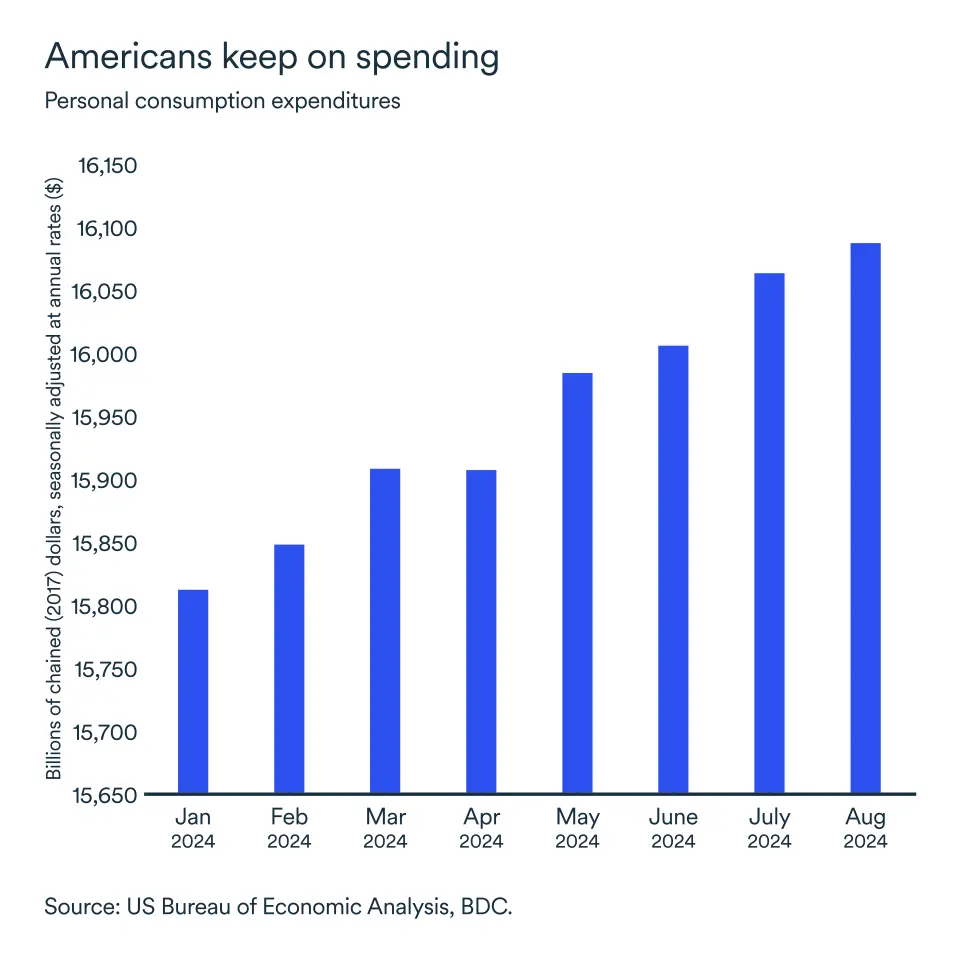

Americans continue to spend

American consumers are still on a roll. Leading indicators point to a third quarter of sustained growth for the economy with American households continuing to spend despite high interest rates.

Following a strong increase in July (+0.4%), personal consumption expenditure rose by a further 0.1% in real terms (i.e. taking into account price rises) in August. For the first two months of the third quarter, spending rose faster than disposable income.

U.S. savings have slowed continuously since May with the trend continuing in August. Savings as a percentage of disposable income stood at 4.8% in August—its lowest level for the year.

A resilient job market

The rebound in the job market in September suggests that fears over the summer of a major employment slowdown may have been misguided, although one month doesn’t make a trend.

Unemployment remains historically low at 4.1% and the job vacancy rate jumped to 4.8% in August. There were more than eight million jobs available and the ratio of unemployed to job vacancies was still below one (0.9), i.e. there were still more job vacancies than people available for work in the country.

Any deterioration in labour market conditions is likely to be reflected more in rising unemployment than in a decline in job vacancies.

Core inflation stabilizes above target

Inflation as measured by the Personal Consumption Expenditure (PCE) price index stood at 2.2% in August, and at 2.7% excluding food and energy.

However, while the overall PCE index continued to fall, core inflation data (measured by PCE excluding food and energy, on which the 2.0% target is based) have been stagnant for several months now. The core consumer price index (CPI)—another measure of inflation which also excludes volatile food and energy costs—increased at an annual rate of 3.3% in September.

So far, all the Federal Reserve's underlying inflation measures were still more than 0.50 points above target. Another sign that lead us to believe the Fed will temper the pace of rate cuts for the rest of the year.

The impact on your business

- The significant drop-in U.S. interest rates will have an impact on Canada. Anyone borrowing in U.S. dollars will see their interest costs fall, including banks borrowing on the wholesale market. Canadian businesses and consumers could therefore benefit from lower rates south of the border.

- The labour market picked up in September, and U.S. households are still spending lavishly in relation to their disposable income. Moreover, U.S. imports are still on the rise, which are all good news for Canadian exporters.

- The loonie could depreciate further against the greenback, as the interest rate differential between the two countries continues to widen. This is especially true because recent data point to a more resilient U.S. economy that could limit future interest rate cuts on that side of the border. Canadians exporting to the U.S. will be more competitive, but Canadian companies will face higher costs to import goods and services from the U.S. or to trade on international markets.

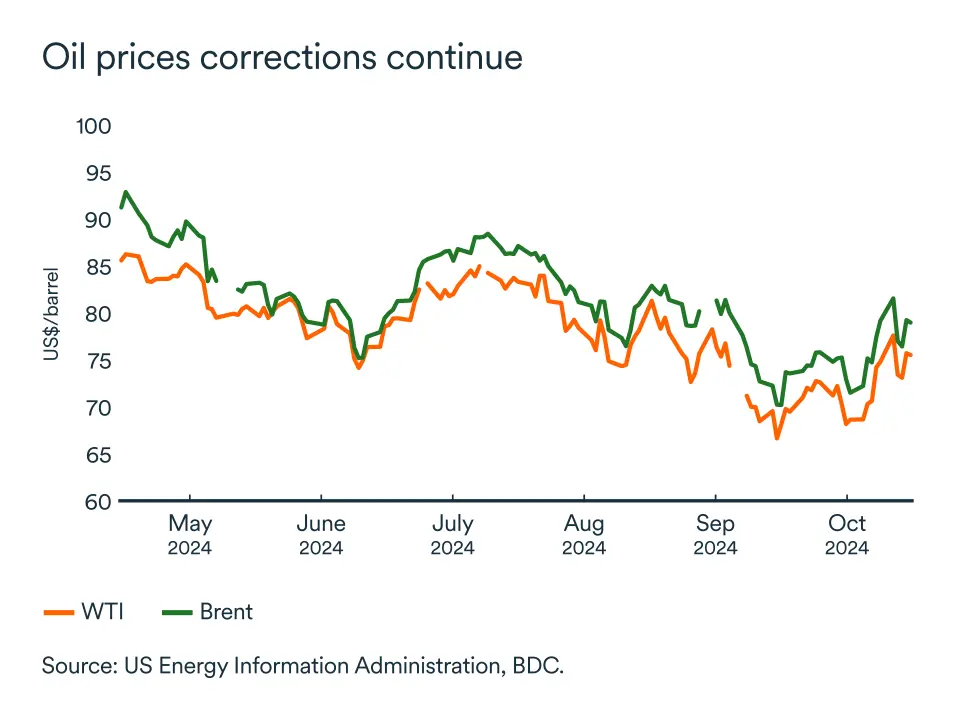

The return of fundamentals pushes prices down

At the time of writing, WTI was trading at US$74, while Brent was up slightly at US$77.8. This after the main crude benchmarks reached US$77 and US$81 per barrel respectively in early October—up 12% (around US$10 per barrel) from their late-September lows.

The geopolitical risk remains, but the associated premium on the price per barrel is diminishing. This explains the rapid rise in prices at the beginning of the month. The market was on edge, waiting for Israel to retaliate against Iran. In the absence of a major supply disruption, both WTI and Brent have fallen back—fundamentals taking over from expectations. If Iran's oil infrastructure is not hit on a large scale, prices could fall further, with Chinese demand yet to materialize and US inventories on the rise.

China's economic difficulties

Despite the announcement of greater economic stimulus to support the country's ailing real estate sector, China's economic recovery is still disappointing for the time being and has not translated into major purchases for the oil market. Demand for crude still seems to be slowing down, while imports are failing to recover. According to Kpler data, China's crude oil imports averaged just 10.8 million b/d in September, down more than 500,000 b/d on the previous month.

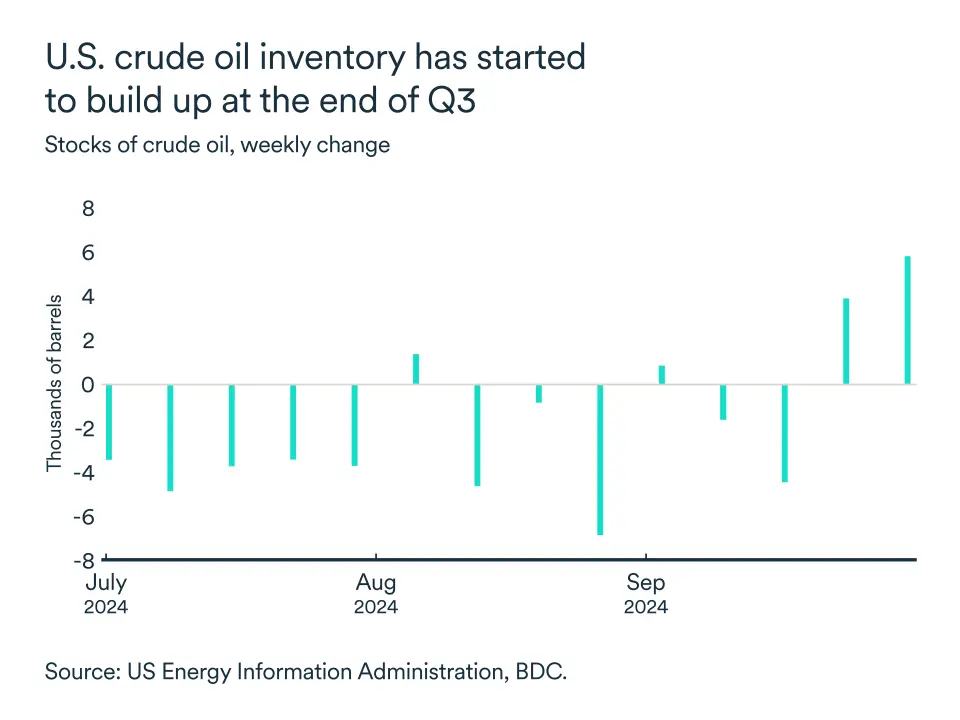

U.S. inventories on the rise

U.S. crude oil inventories recently rose more sharply than the U.S. oil market had expected. The data show a significant increase of 10.9 million barrels at the beginning of the month, far exceeding the expected increase of 1.95 million barrels.

This increase is a harbinger of a possible slowdown in U.S. fuel demand, which will have been enough to push prices further down. Concerns about U.S. demand are heightened as the Mid-South region deals with a series of destructive hurricanes.

OPEC+ hopes to push prices up

In early September, the Organization of the Petroleum Exporting Countries and its allies (OPEC+) decided to delay the increase in oil production for a further two months in an attempt to support prices, but to no avail so far. Forecasts of falling global demand, combined with new oil supplies from non-OPEC countries, point to a long period of moderation in crude oil prices.

The extension of crude oil production cuts until December, in an attempt to limit supply to the market, will not have the desired effect on prices as long as demand remains weak.

In a nutshell...

Oil prices fell back after a momentary rise in early October due to geopolitical tensions in the Middle East. Chinese demand remains weak despite stimulus measures, and US inventories have risen sharply—both signs that global demand remains weak. OPEC+ extended production cuts, but this was not enough to support prices in the face of falling global demand and a new supply of non-OPEC oil. For the time being, consumers should continue to welcome the correction in barrel prices, which is reflected in pump prices and inflation.

Policy rate to drop furthermore in Canada

We foresee the central bank to continue cutting rate by 0.25 points (if not more) at each remaining rate announcement throughout the year—meaning Canada’s policy rate could very well end the year at 3.75%. The consumer price index (CPI), 12-month growth rate slowed to 1.6% in September while the Bank’s core measures all trended downward as well. Even if CPI was to pick up slightly again in the next readings, the Canadian central bank is well positioned to continue on its easing journey of the monetary policy since the economy is slowing down and the labour market rebalancing. Moreover, consumers’ perceptions of current inflation and their expectations for inflation over the next year have declined recently, signalling that inflation expectations are getting even more anchored.

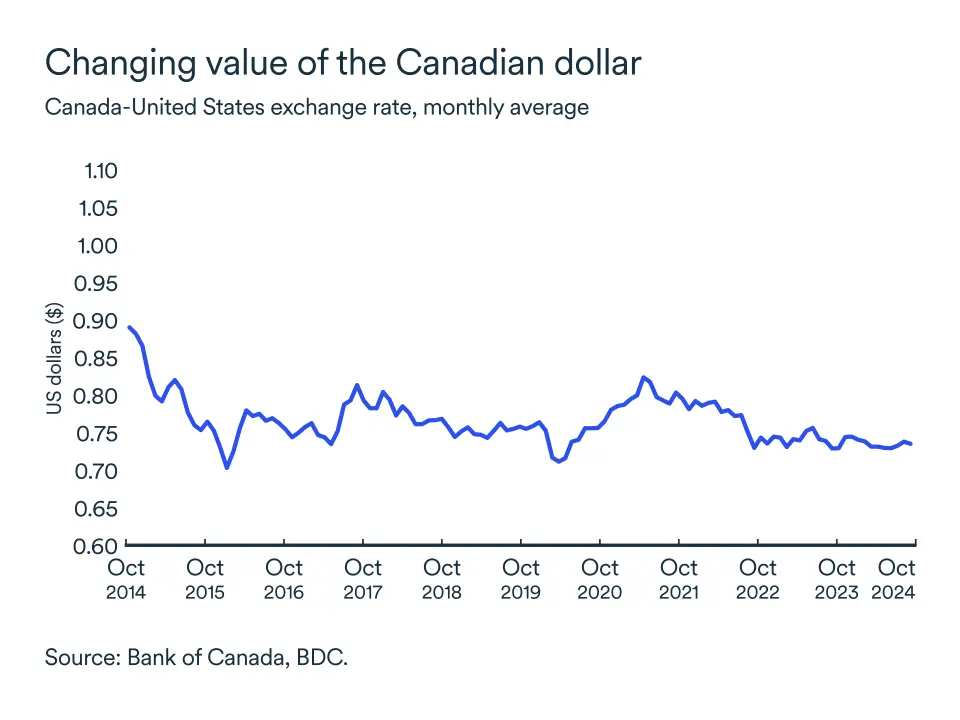

The loonie slightly drop from September level

The Canadian dollar lost a few points since the end of September. At the beginning of October, the loonie traded even below US$73 while it was worth more than US$74 just a week ago. The most recent Canadian dollar slide is stemming from the differences between the two countries’ economic situation. While the U.S. GDP is still increasing at a relatively strong pace, the economy is creating numerous new jobs and increasing consumer spending, the Canadian economy is sluggish. Therefore, the Canadian dollar is expected to remain between its latest range of US$0.73 and US$0.74.

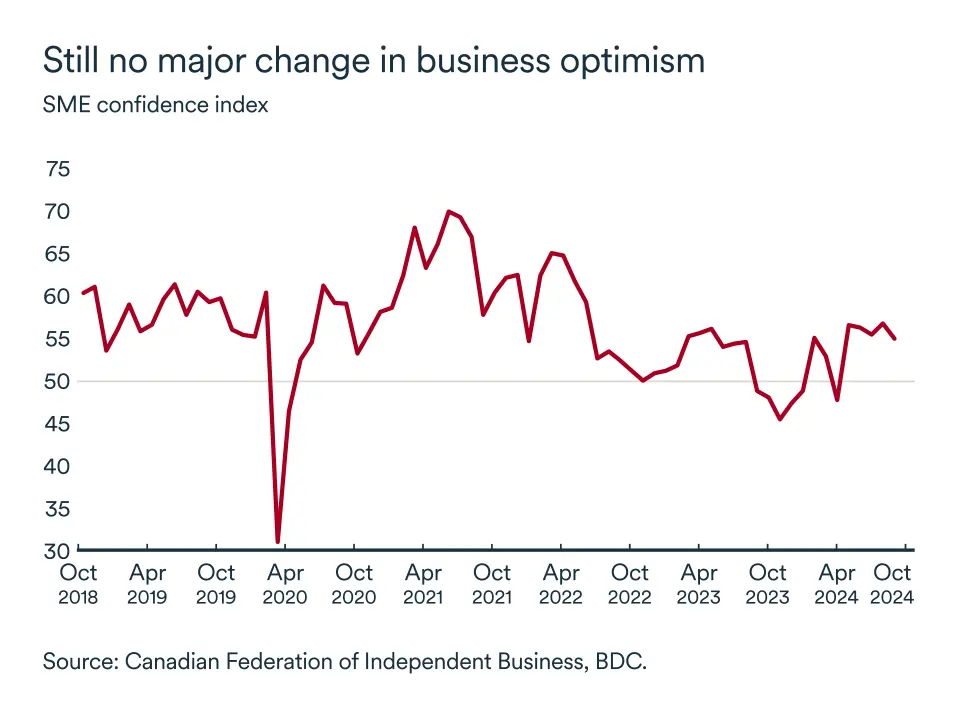

Business confidence remains

For the past few months, Canadian optimism has not changed much. In September, the CFIB business confidence index for the coming year remained broadly unchanged compared to August’s level. The index stayed above the fateful 50 threshold, gearing slightly down to 55 (from 56.8). Businesses remain on the lookout in the shorter term and optimism has been quite muted despite the interest rate cuts.

An indicator of 50 means that as many company managers expect the business environment to deteriorate versus an improvement over the period covered (either 12, or three months).