Monthly Economic Letter

Keep abreast of key economic indicators.

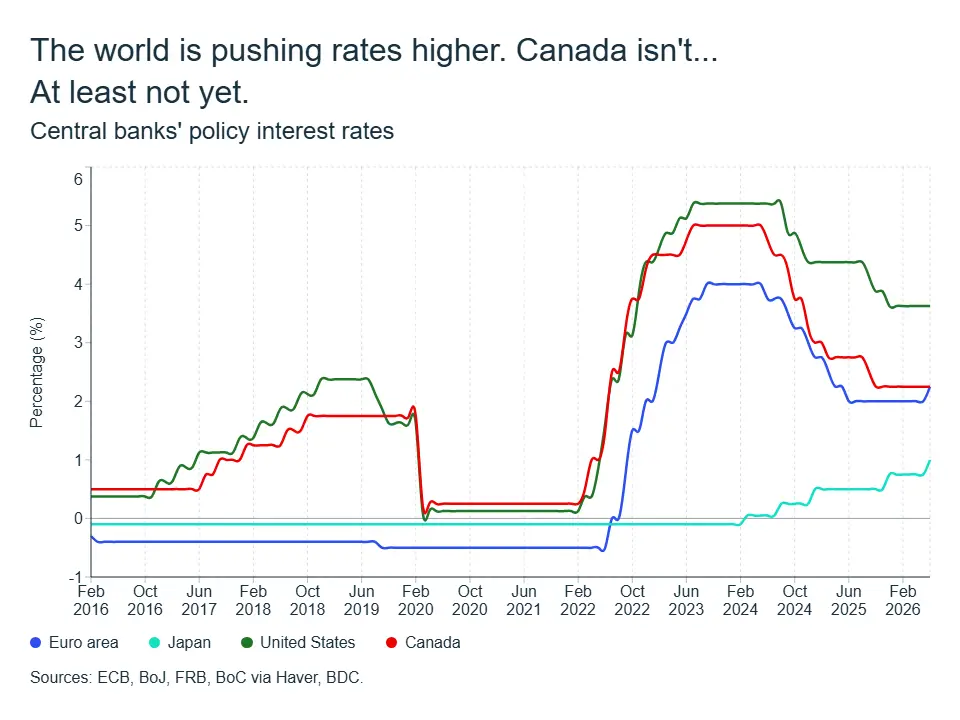

Read moreThe Bank of Canada is on hold. Your borrowing costs may not be.

The Bank of Canada's July decision confirmed a new reality for borrowers: the policy rate may be stable, but broader financing conditions are not. The Bank held its policy rate at 2.25%, weighing signs of improving growth against a recent pickup in inflation driven largely by energy prices. For businesses and households making borrowing decisions, the key question is no longer just when the Bank's next move will come. It is how bond yields, risk premiums and credit conditions will shape the rates they actually pay.

Globally, the situation is also less aligned. The United States remains in a holding pattern, with policy rates still in restrictive territory as inflation has yet to return durably to target. As a result, markets have become increasingly sensitive to any sign that rates could remain higher for longer.

In other regions, inflation pressures linked to energy markets have made central banks more cautious. The European Central Bank (ECB) and the Bank of Japan (BoJ), for example, both raised their policy rates in June. It marks the ECB's first increase since September 2023 and brings the BoJ's policy rate to its highest level in more than 30 years. This divergence reflects differences in domestic conditions but also the growing importance of global shocks, which increasingly spill over into Canadian bond yields and therefore, financing costs.

So what will happen here, at home?

Energy prices remain central to the story. Oil prices have been volatile, rising above levels seen earlier in the year before easing from their peak. Compared with the pre-conflict environment, prices remain elevated and unstable. This matters because energy is currently one of the main sources of renewed inflation pressure. The longer geopolitical tensions persist, the greater the risk that these pressures spread beyond energy into broader price dynamics.

Canada’s domestic economy, however, is not overheating. Growth has been soft, demand remains limited and the economy is still operating with some excess supply. BDC Economics continues to expect real GDP growth of about 1.0% in 2026, below the economy’s potential. That weak growth backdrop is important: it limits the ability of businesses to pass higher costs on to consumers and reduces the risk of a broad inflation spiral.

Recent data have improved, but they do not point to a boom. GDP rebounded in April and early estimates suggest another modest gain in May, putting the second quarter on track for a clear improvement after a weak start to the year. At the same time, labour market conditions have cooled. The unemployment rate has moved closer to 6.5%-7%, compared with roughly 5% during the tight labour market conditions of 2022. This increase signals the presence of excess supply in the economy.

Demographics are also reshaping the outlook. Canada’s population has declined for three consecutive quarters, an unprecedented shift in modern records. In the near term, this reduces demand for housing, consumption and some services, helping to contain broad-based inflationary pressures despite ongoing increases in some sectors. Over time, it also lowers the economy’s potential growth rate, limiting how quickly activity can expand without creating new pressures.

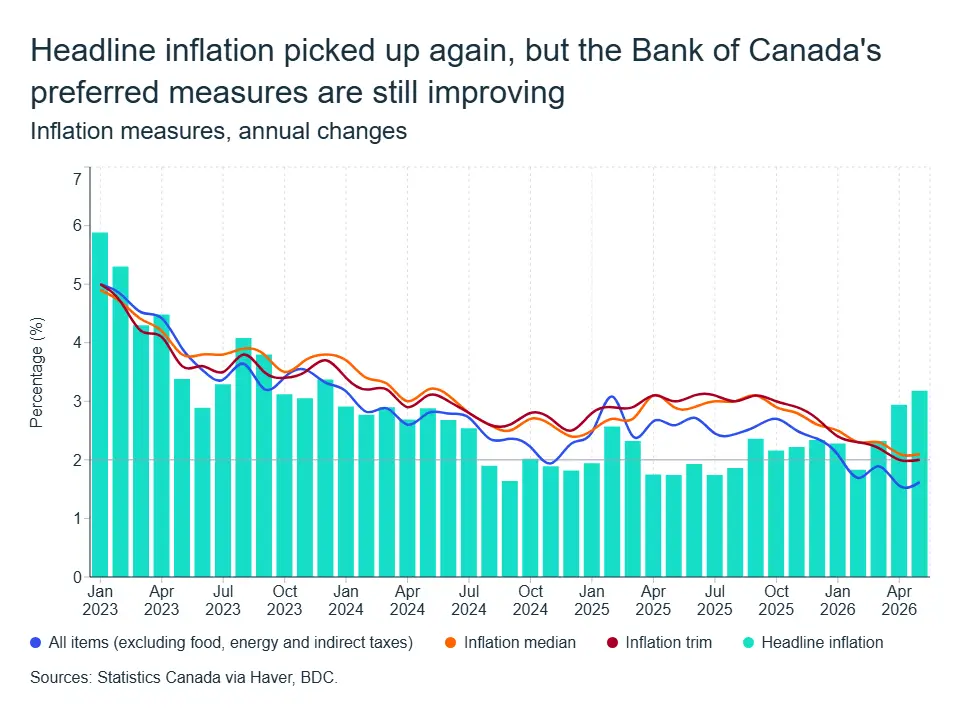

Inflation reflects this balancing act. Headline inflation has moved above 3%, driven largely by gasoline and energy-related costs. But the Bank of Canada’s preferred core measures remain close to 2%, suggesting limited evidence so far of broad-based inflation pressure. This is why the Bank can remain patient, even as it stays alert to the risk that energy costs could spill over into other prices.

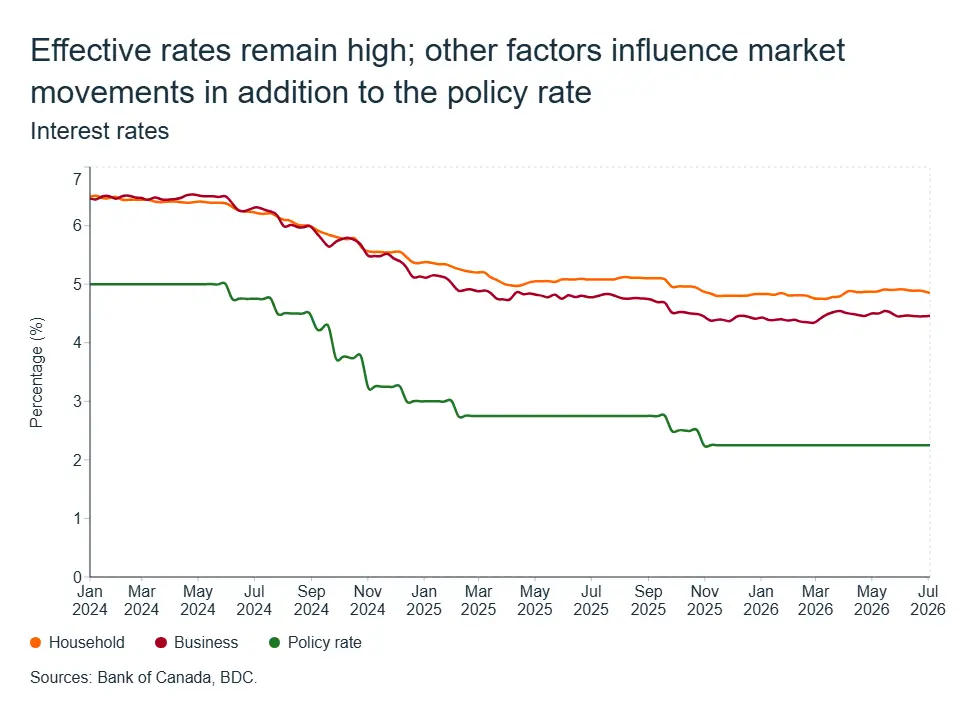

The disconnect between policy rates and borrowing costs

For entrepreneurs and households, the most important development is not simply the level of the policy rate, but the behaviour of effective borrowing rates.

The policy rate is a benchmark for short-term borrowing costs, but it does not directly determine the rates faced by borrowers. Effective rates depend on a broader set of factors, including bank funding costs, competition, credit conditions, bond yields and financial market sentiment.

Those factors still matter. Government bond yields remain elevated in a context of high global uncertainty and heightened volatility. While yields are below the peaks reached during the tightening cycle, they are still high enough to keep borrowing costs restrictive by historical standards.

For businesses, this translates into financing costs that remain sensitive to market conditions. For households, the effect is particularly visible in mortgage rates, which are even more closely linked to bond yields.

What to watch in the second half of the year

Three forces will shape the path of interest rates and borrowing conditions in the coming months:

- Energy prices. Oil remains the main upside risk to inflation. Persistent increases would raise the risk of broader price pressures, while a decline would reinforce the return toward target.

- Domestic demand. Canada’s excess supply is helping to contain inflation. A stronger rebound in consumption, housing or investment could reduce that buffer and influence future policy decisions.

- Financial markets and expectations. Bond yields and risk premiums are becoming increasingly important in the transmission of monetary policy. Their evolution will determine how much relief households and businesses actually see in Canada.

What it means for entrepreneurs and households

With second-quarter GDP tracking stronger than the first quarter, inflation firming because of energy prices and unemployment edging lower, there is little urgency for the Bank of Canada to move away from its 2.25% policy rate. Financing decisions, whether for new borrowing or upcoming renewals, should be planned around a stable, not falling, policy rate through the summer.

Behind the Bank’s steady hand, however, the environment is anything but stable. Central bank decisions remain a key driver of borrowing costs, but even with the policy rate on hold, effective borrowing rates can keep moving as markets react to inflation data, geopolitical developments and shifts in growth expectations. When uncertainty rises, investors demand more compensation for risk, pushing bond yields, and therefore borrowing costs, higher, even without any action from the Bank of Canada.

Bottom line

Stability in policy rates no longer guarantees stability in borrowing costs. The range of plausible outcomes has narrowed, but global volatility and shifting market expectations mean borrowing costs will continue to evolve even when the headline policy rate does not.

The challenge is that uncertainty can easily lead to a wait-and-see mindset. While caution is understandable, putting growth plans on hold for too long can leave businesses less prepared for future opportunities.

Waiting for perfect clarity on interest rates, trade policy or the economic outlook may prove costly. The most resilient firms are often those that keep moving forward, investing selectively and strategically to strengthen their competitiveness and position themselves for the future.

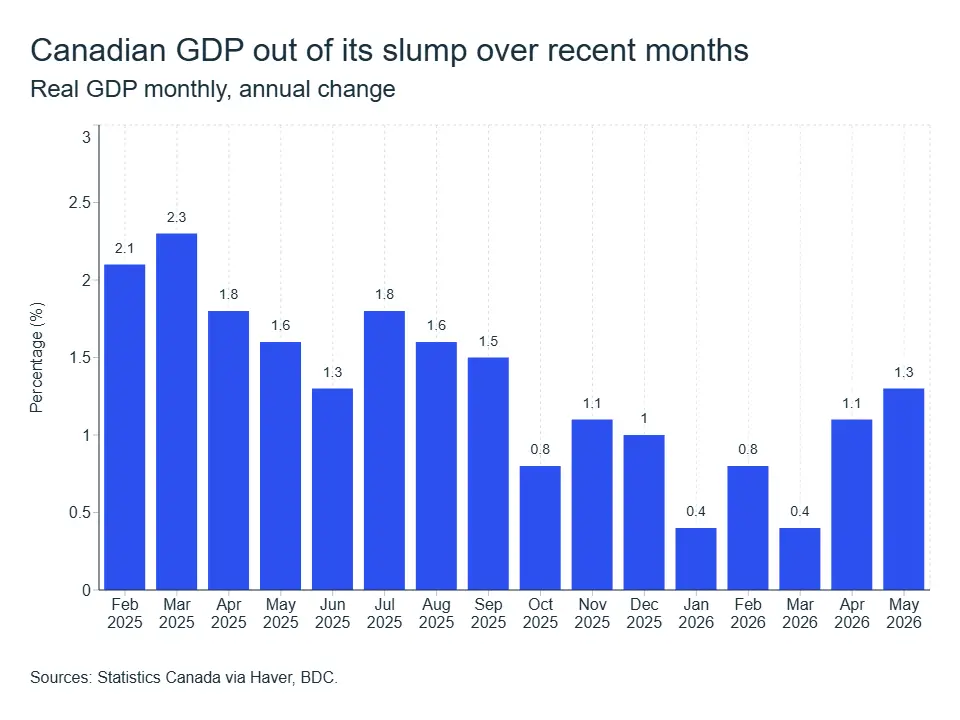

Canada’s economy regains some footing

For much of the past year, the Canadian economy has looked like a slow burn. Growth kept losing altitude, recession headlines kept resurfacing, and each new data release seemed to give entrepreneurs another reason to stay cautious. Luckily, spring brought a change in tone.

Real GDP turned positive again in April, Statistics Canada’s advance estimate pointed to another modest gain in May, employment continued to rise in June, and trade began to move in a more encouraging direction. The Canadian economy is not booming. The conflict in the Middle East, U.S. tariffs, elevated energy prices and weak population growth are still shaping the backdrop. But the data now point to an economy that is regaining some footing rather than sliding deeper into weakness. BDC Economics is maintaining its 1.0% real GDP growth forecast for 2026.

The recovery the economy needed

Real GDP edged down by 0.1% at an annualized rate in the first quarter, after a contraction in late 2025. That weakness was concentrated in a few volatile components. Net trade was the main drag, as imports rose while export volumes remained soft, and government spending also pulled back after earlier strength. At the same time, household consumption continued to provide support, and inventories offset part of the weakness. The result was not an economy in free fall, but one operating below potential and struggling to find momentum.

April changed the tone. Real GDP grew 0.5% month over month, the strongest monthly gain in several months. The improvement was broad-based: 14 of 20 industries expanded, goods-producing industries rose 1.2%, and services grew 0.3% for a third consecutive month. Mining, quarrying, and oil and gas extraction led the gain with a 2.9% increase, reflecting the support coming from higher energy prices and stronger commodity activity.

May appears to have held the line as well. Statistics Canada’s advance estimate pointed to a further 0.1% increase. Taken together, the latest data suggest that second-quarter growth came in clearly positive. The Bank of Canada now estimates that GDP growth strengthened to about 2.5% annualized in Q2, supported by stronger exports, a partial rebound from temporary weakness in Q1 and firmer residential investment.

What makes this pickup more meaningful is the context in which it is happening. The headwinds have not disappeared. The conflict in the Middle East continues to create volatility in energy and food prices. Trade uncertainty remains elevated. U.S. tariffs on metals and related products continue to weigh on trade-exposed industries. And the CUSMA review process is now adding an annual rolling layer of uncertainty for businesses. The improvement is real, but it is still fragile.

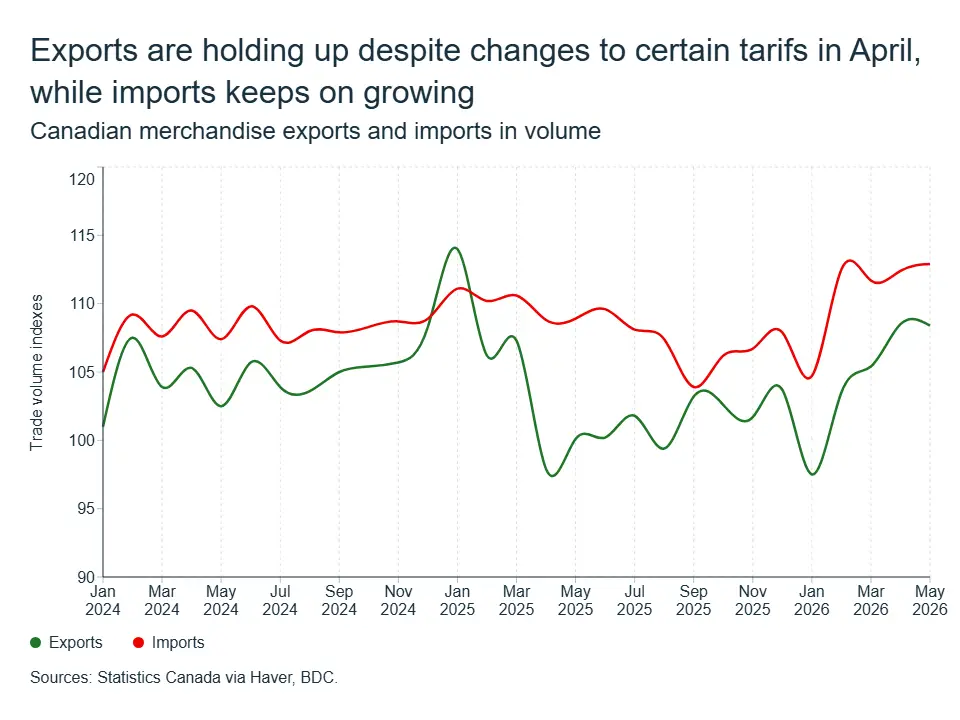

Trade is finally moving in the right direction

If one number explains why the first quarter looked so weak, it is the contribution from net trade. Rising imports and soft export volumes together subtracted roughly 3.8 percentage points from Q1 GDP growth, more than offsetting the positive contributions from household consumption and inventories.

The second-quarter picture looks materially better. Export volumes stabilized through the spring, with energy exports providing support, and the merchandise trade balance moved back toward surplus. Imports also continued to rise, which can be a drag on headline GDP. But not all imports tell the same story. A portion of machinery and equipment imports may point to businesses investing in capacity or retooling their operations, although it is too early to call this a broad investment rebound.

The key point is that trade is no longer deteriorating at the same pace. After being the main reason GDP weakened in Q1, trade should contribute more favourably to Q2 growth. That does not mean trade risks have disappeared. It means the economy is still adapting to them.

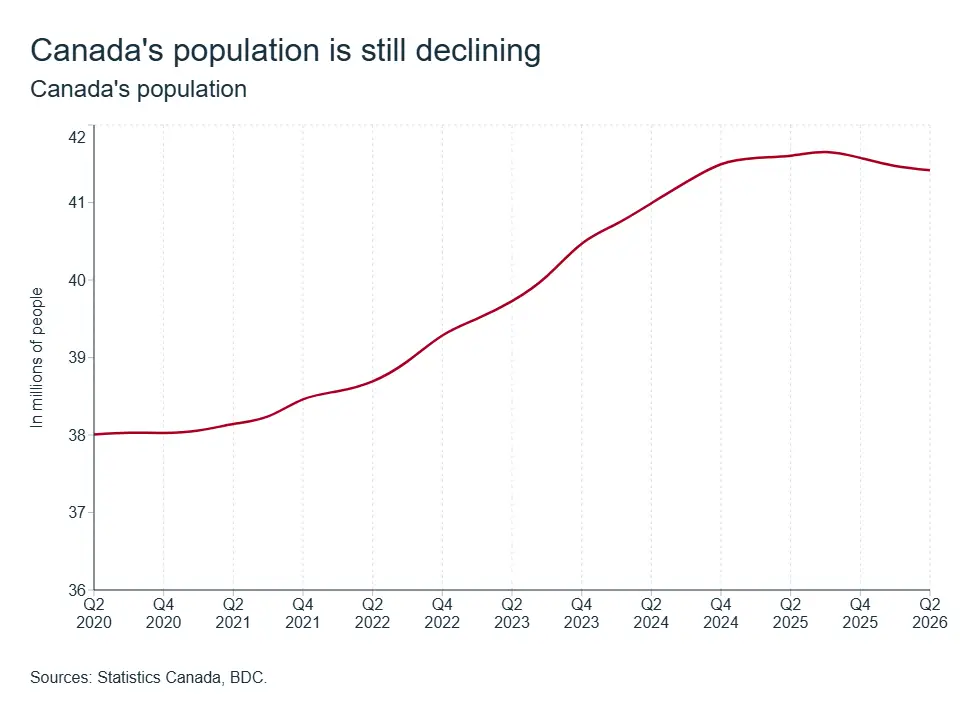

A historic demographic shift is now official

While the trade story is cautiously encouraging, the demographic story is more structural. Canada’s population declined for a third consecutive quarter at the start of Q2 2026, something unprecedented in modern Canadian demographic reporting. A historic decline in Canada's population with significant consequences for the economy and businesses, and it is now firmly entrenched in the data.

The mechanics are straightforward, with the non-permanent residents estimate falling 4.4% in a single quarter and permanent immigrant inflows also dropped roughly 20% year over year.

The economic consequences are already visible. Population growth had been one of the biggest engines of Canadian expansion since 2022. More people meant more consumers, more renters and buyers, more workers, and more baseline demand across most sectors. The Bank of Canada previously estimated that newcomers added about 2.5% to potential output between late 2022 and early 2024. Reversing part of that flow inevitably changes the outlook. Fewer new residents mean less demand for consumer goods and services, fewer new households, and lower pressure on housing demand than in recent years. This does not mean housing weakness is only demographic. Interest rates, affordability and confidence still matter. But slower population growth now adds a structural layer to what had already been a cyclical cooling in housing activity.

For businesses, the implication is simple: growth will rely less on an expanding customer base and more on productivity, market share and efficiency.

Jobs keep coming, but the labour market remains uneven

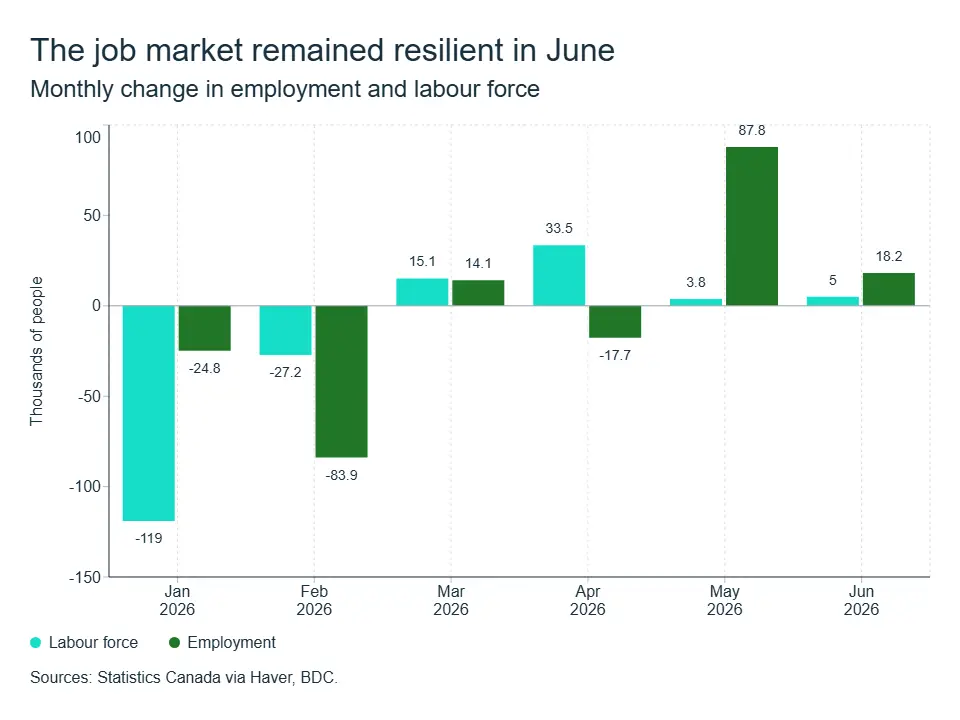

The June labour market data provided exactly the kind of confirmation the economy needed after a strong May. Employment rose by 18,000 in June, following May’s much larger gain of 87,800. That two-month combo has now clawed back most of the 112,000 jobs lost between January and April.

The unemployment rate slipped to 6.5%, down from 6.6% in May and 6.9% in April, while wage growth continued to firmed to 3.3% year over year. With population growth no longer expanding the labour force as rapidly as it did in recent years, even modest hiring can now push the unemployment rate lower. That does not mean the labour market is tight everywhere. It means the operating environment is changing.

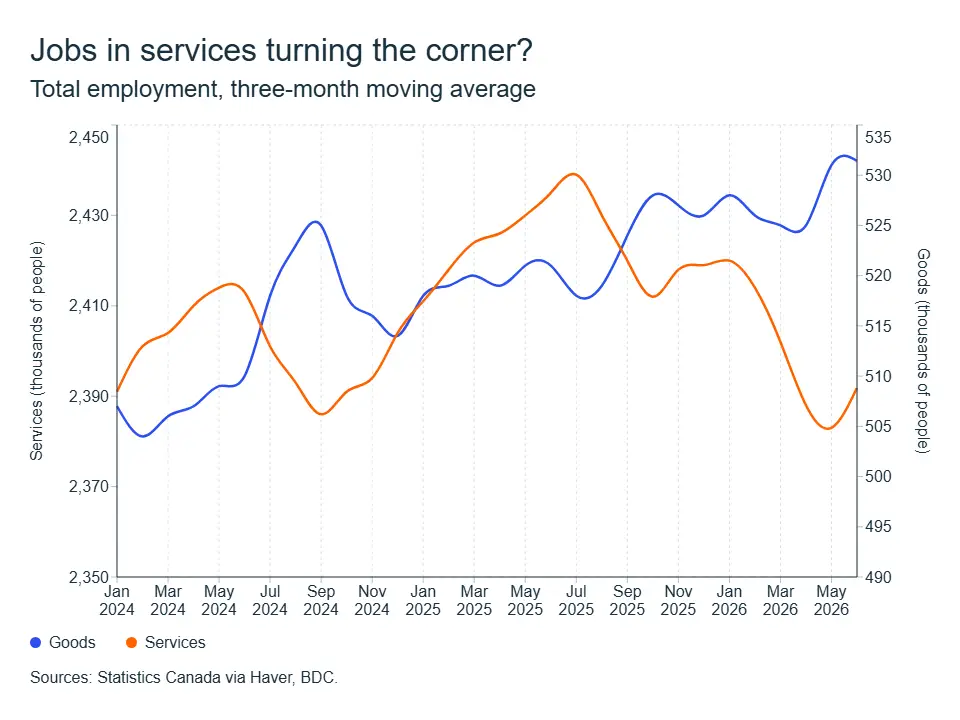

The composition of the gains matters as much as the headline. Services sectors, especially accommodation, food services, and retail and wholesale trade, are still doing most of the heavy lifting, while manufacturing lost another 17,000 jobs in June. That is the clearest reminder that the recovery remains uneven. Domestic-facing sectors are stabilizing, but trade-exposed industries are still under pressure from tariffs and weak external demand.

What it means for entrepreneurs

- Do not expect a rate cut for 2026. With Q2 GDP tracking above 2% annualized, inflation firming on the back of higher energy prices, and unemployment drifting lower, there is little urgency for the Bank of Canada to move off its 2.25% policy rate, so plan financing decisions around a stable, not falling, rate through the summer (but check out this month main article for more details on interest rates).

- The second quarter looks clearly positive, which reduces the risk that the mild technical recession narrative turns into a broader downturn story. But growth remains below potential, and the economy is still operating with excess supply, plan accordingly.

- Demographics are now part of the business environment. Slower population growth means slower expansion in baseline demand. It also means labour supply will be less forgiving. Entrepreneurs should not assume that today’s softer labour market will last. Retention, training, automation and productivity investments are becoming more important, not less.

- Trade uncertainty is still the main wildcard. Exporters and manufacturers should continue to plan for uneven conditions, especially in sectors exposed to U.S. tariffs now that CUSMA annual reviews are officials.

British Columbia

The B.C. economy is showing continued signs of stabilization. Employment increased once again in June, an encouraging sign that levels are stabilizing after a weak start to the year. While the unemployment rate fell to 6.5% (from 6.8% in May), it remains above where it stood a year earlier, and the recent movements should be interpreted cautiously given the broader uncertainty facing the provincial economy.

Consumer spending appears to be holding up, but with limited underlying momentum. Retail sales in B.C. rose by 1.0% in April, following a modest gain in March, which suggests households are still spending despite softer labour market conditions. However, core sales (adjusted for inflation) declined for a second consecutive month, and real retail volumes were flat in April, pointing to a more cautious consumer environment once price effects are stripped out.

The housing market is showing early signs that activity may be finding a floor. BCREA reported that home sales in June rose year-over-year for the first time since September 2025, helped by stronger activity in the Greater Vancouver area. Even so, sales remained well below the 10-year average for the month, and average prices were slightly lower than a year earlier. Year-to-date sales and dollar volumes are also still down compared with 2025, suggesting that the improvement in June is encouraging but not yet enough to signal a full recovery.

Overall, B.C.’s economy is showing signs of stability after a difficult start to the year. While lower unemployment and firmer housing activity are positive developments, growth is likely to remain modest and uneven in the near term. Soft consumer demand, elevated inventories in real estate and ongoing trade and interest rate uncertainty will continue to weigh on the outlook.

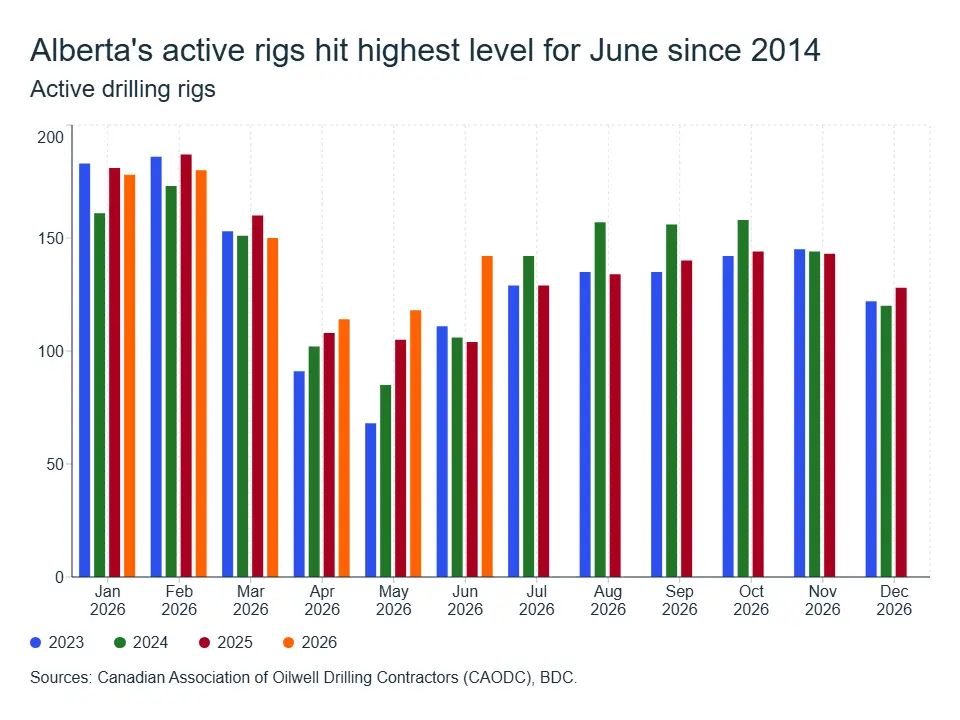

Alberta

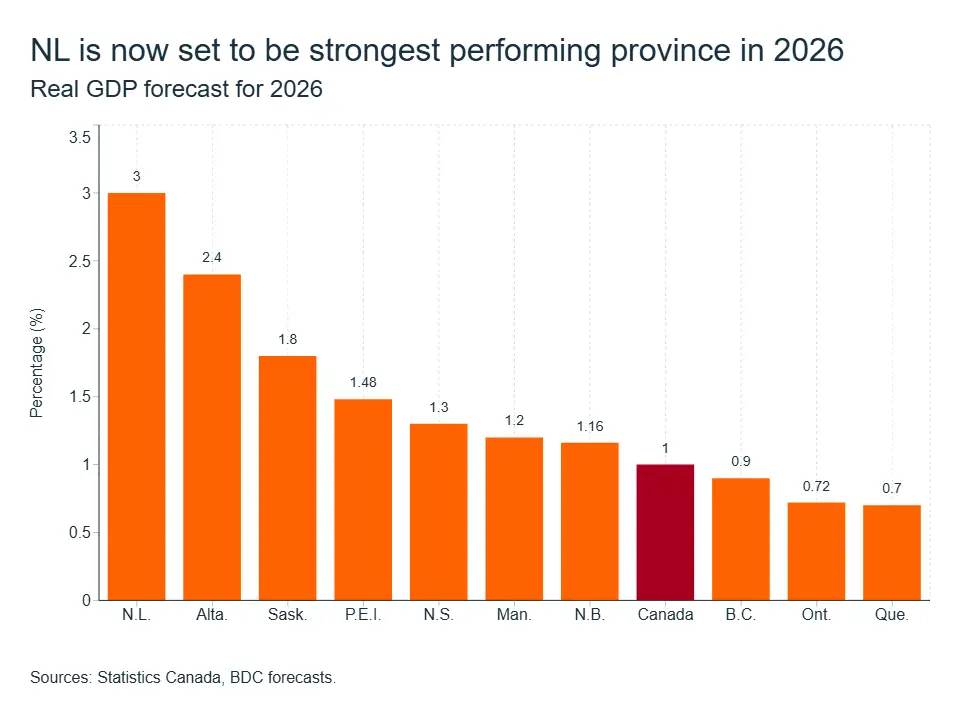

Alberta remains the province best positioned for growth in 2026. BDC Economics expects real GDP to increase by 2.4%, more than double the national forecast of 1.0% and the strongest pace among the provinces. The combination of elevated energy revenues, resilient labour market conditions and continued export diversification continues to provide Alberta with a significant advantage despite ongoing trade uncertainty.

Energy remains the key driver of the provincial outlook. Oil prices surged during the spring following disruptions in the Middle East, with WTI averaging above US$100 per barrel during May. However, prices have since retreated as supply concerns eased. The Bank of Canada now assumes oil prices will continue to moderate through the second half of 2026, although they remain above the assumptions underpinning many 2026 economic and fiscal forecasts. Higher prices have boosted provincial royalty revenues and corporate cash flow, supporting Alberta's fiscal position and business investment climate.

The current cycle differs from previous oil booms, however. Producers continue to prioritize balance-sheet strength and shareholder returns rather than aggressively expanding production. Recent analysis from Canadian financial institutions suggests that temporary geopolitical price spikes are not generating the type of long-term capital spending response seen in earlier commodity cycles. As a result, growth in the energy sector is being driven more by strong production levels, as suggested by strong drilling activity through the second quarter, and improved export revenues than by a surge in investment spending. The expansion of the Trans Mountain pipeline continues to support market diversification and has improved access to Asian markets, helping Alberta capture more value from its exports.

The labour market remains one of Alberta's strongest assets. While the unemployment rate rose to 7.0% in June, the increase largely reflects continued population and labour-force growth rather than a deterioration in hiring conditions. helping sustain consumer spending and supporting demand-oriented businesses. As such, retail activity has recovered from weakness earlier in the year, although part of the improvement reflects higher gasoline prices rather than a broad-based acceleration in real consumption.

Nevertheless, Alberta enters the second half of 2026 with stronger fundamentals than most provinces.

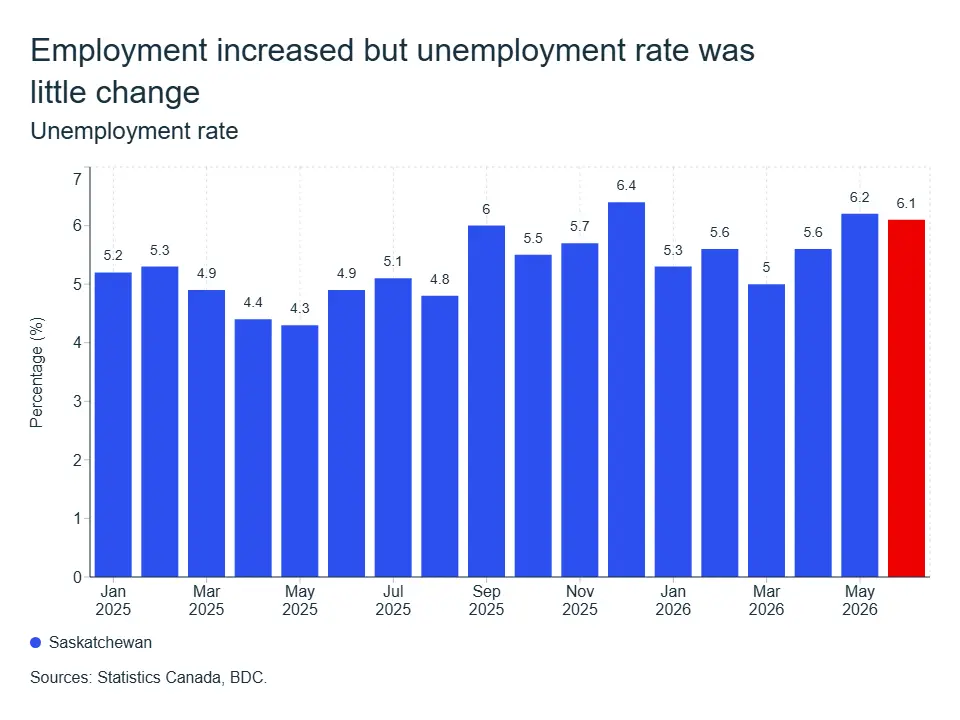

Saskatchewan

Saskatchewan is also expected to outperform the national economy in 2026. BDC Economics forecasts real GDP growth of 1.8%, well above the national projection of 1.0% and among the strongest performances in Canada. The province continues to benefit from favourable commodity markets, major mining investments and ongoing population growth, all of which help offset the impact of trade uncertainty and slower economic growth elsewhere in the country.

Resource industries remain the foundation of Saskatchewan’s economic outlook. Although oil prices have retreated from the peaks reached during the spring, they remain above the assumptions underpinning many 2026 economic and fiscal forecasts, providing support to the province’s energy sector. Mining continues to be Saskatchewan’s primary growth engine.

Mineral sales reached a record $12.8 billion in 2025, led by potash ($9.3 billion) and uranium ($3.2 billion, a record). Momentum has carried into 2026, with potash sales and production continuing to post strong gains, while weaker uranium sales in April reflected planned maintenance shutdowns rather than deteriorating market conditions. Global demand for fertilizer and nuclear energy remains a key tailwind for both industries.

The province’s medium-term outlook is further strengthened by several major resource projects, some like NexGen, that could see light of day in the coming weeks.

Manufacturing activity has also shown encouraging signs of recovery. After a sharp rebound earlier in the spring, Saskatchewan recorded one of the strongest manufacturing performances in the country in May, supported by food processing and resource-related industries. Trade conditions remain more challenging, however, with exports to the United States continuing to face pressure from tariffs and broader trade uncertainty

The labour market remains softer than it was a year ago, but Saskatchewan continues to compare favourably with most provinces. Employment was essentially unchanged in June and the unemployment rate held steady at 6.1%, below the national average of 6.5%. While labour market conditions are no longer as tight as they were a year ago, the province continues to benefit from a growing labour force and one of the lowest unemployment rates in Canada. Combined with a strong pipeline of mining investment and favourable commodity markets, these conditions should help support household spending and economic activity through the second half of 2026.

Manitoba

Manitoba's economy is expected to post moderate growth in 2026. BDC Economics forecasts real GDP growth of 1.2%, slightly above the national forecast of 1.0%. A diversified economic base, resilient household spending and supportive provincial measures should help the province navigate a slower national economy.

The provincial government has introduced several measures to support household purchasing power, including the elimination of the 7% PST on grocery items sold in grocery stores starting July 1. These measures should provide some support to consumer spending at a time when many households continue to face elevated living costs and economic uncertainty.

The labour market remains relatively resilient. Employment increased by 2,200 jobs in June, while the unemployment rate edged down to 5.4%, one of the lowest rates in the country and well below the national average of 6.5%. Population growth and labour-force expansion should continue to support consumer demand over the medium term.

Manufacturing activity has also shown signs of improvement after a weak start to the year. The agri-food industry, which accounts for nearly one-third of provincial manufacturing sales, continues to provide an important source of stability. External demand remains the main challenge, however. Total exports fell 27.2% in the first quarter, including a 34.3% decline in exports to the United States, reflecting weaker pharmaceutical shipments and ongoing trade-related pressures. Elevated energy prices also continue to pose risks by increasing transportation and logistics costs in a province that relies heavily on domestic trade.

Nevertheless, Manitoba enters the second half of 2026 with relatively solid fundamentals. Resilient consumer spending, a stable labour market and improving manufacturing activity should help support growth despite weaker export performance.

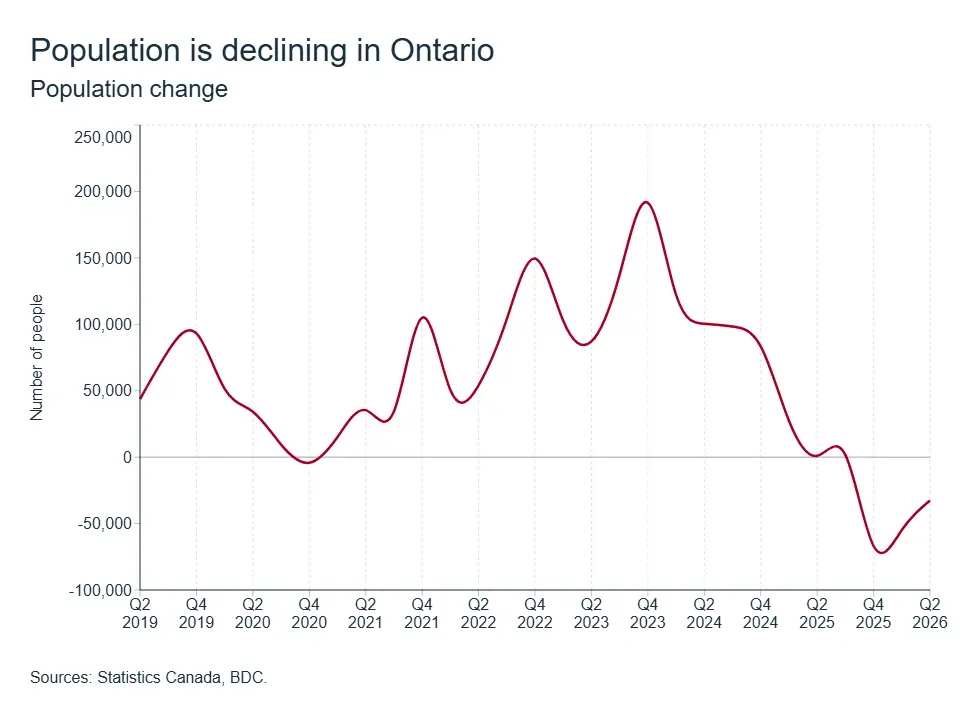

Ontario

A review of the first six months of the year shows that growth has been weak but positive.

Consumers have been the main driver of economic growth since the beginning of 2026. Retail sales increased by 1.7% in the first quarter. Although the labour market is volatile, average hourly wages have increased by 4.1% in the last 12 months, supporting consumer spending. However, the economy is facing some headwinds. Tariffs imposed by the United States continue to weigh on exports of automobiles, steel and lumber, and consequently manufacturing sales declined in the first quarter.

A decline in the population is also having an impact. The province's population fell by 0.2% in Q4 of 2025 and by 0.7% in Q1 of 2026, which marks the first time this has occurred since records began in 1951. Consequently, the housing market is weak, with a fall in home resales and housing starts. Lower population growth will continue to limit growth in this sector in 2026 and probably in 2027 too.

Therefore, consumption is the main source of economic growth in 2026. This will result in growth being well below its potential.

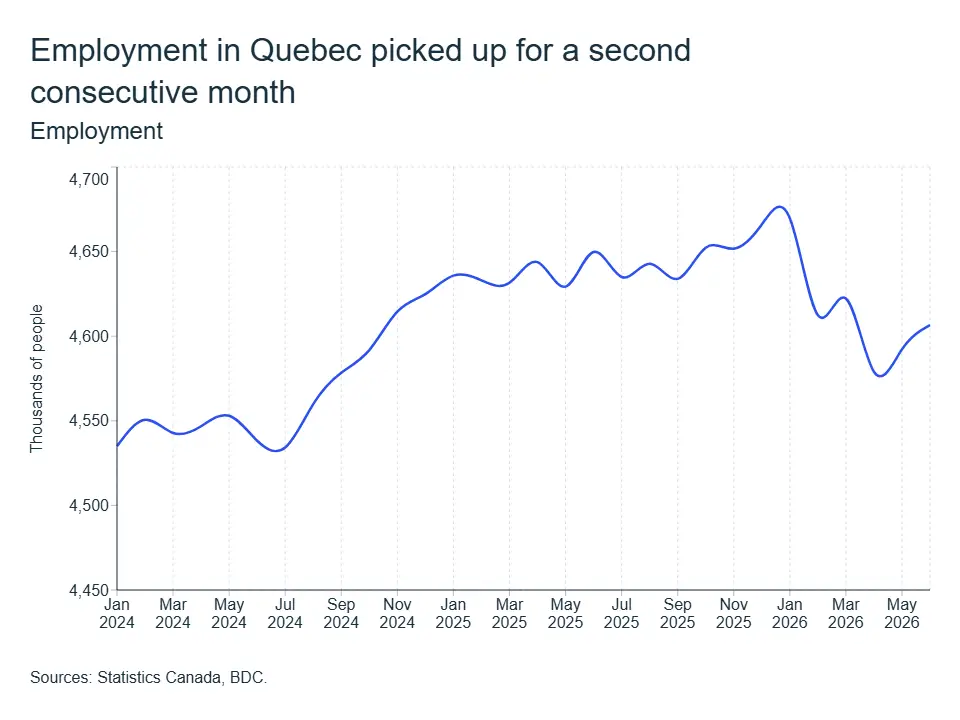

Quebec

Quebec's economy remains under pressure, with weak momentum largely reflecting the persistent impact of uncertainty and a challenging trade environment. Exports are still below last year's levels, though a pickup since March points to some early stabilization.

Economic activity stayed subdued in the first quarter, with real GDP edging up 0.3% quarter-over-quarter (1.3% annualized) and narrowly avoiding a second consecutive contraction. The gain, however, was largely driven by inventory accumulation, while exports, household spending, and investment all softened — underscoring the fragility of the province's underlying momentum.

Attention is now firmly on the labour market, which has been losing ground since the start of the year. However, June's release points to a brighter picture. The economy created 14,000 jobs and the unemployment rate dropped to 5.4%.

The real estate market is under pressure: a weaker economic backdrop, compounded by slowing population growth, is weighing on housing demand — though prices have proven more resilient. Home sales are down 3.6% year-to-date , while price growth has held firm over the same period. Together, these dynamics should cap sales activity and limit further price gains through the remainder of the year.

Looking ahead, below-potential growth is expected to persist as trade uncertainty and a cooling labour market continue to weigh on activity. GDP growth is projected at 0.7%, placing Quebec among Canada's slowest-growing economies. For now, government spending and household consumption remain the province's main engines of growth, helping it steer clear of a recession.

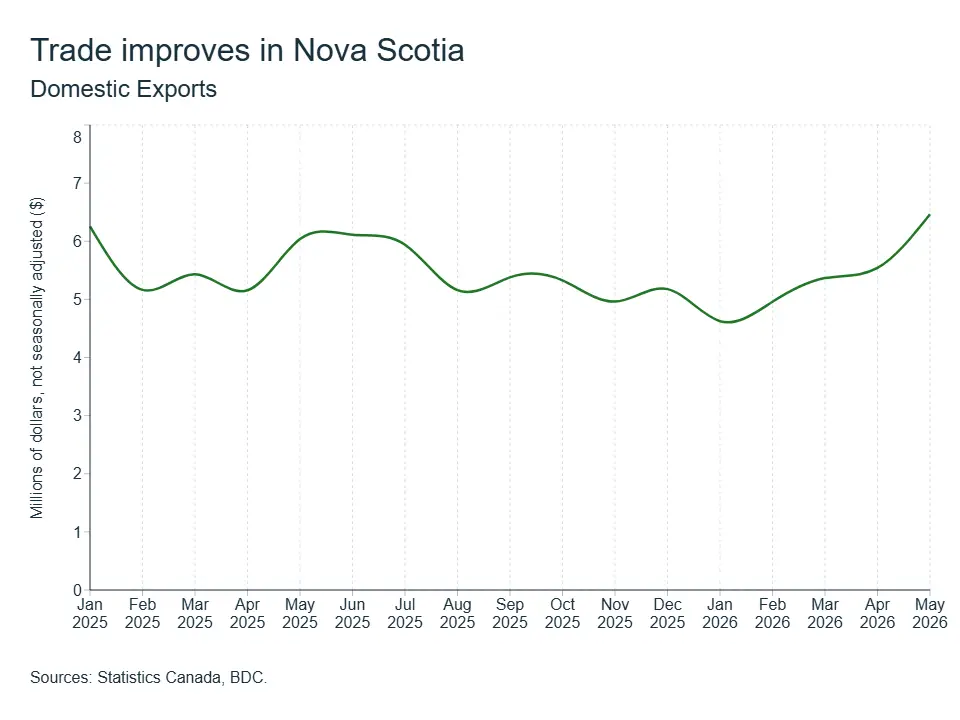

Nova Scotia

Nova Scotia’s economy is slowing this year, but growth remains supported by solid domestic fundamentals. Household spending continues to provide a stable base: retail sales rose 3.2% in Q1 2026, and continued to advance in April, up 0.7% month-over-month.

Trade conditions show tentative signs of stabilization. After exports fell 3.3% in Q1 amid tariff uncertainty, shipments have strengthened, supported by higher sales to Europe and continued diversification away from U.S. markets. China’s removal of tariffs on seafood products is also providing much-needed relief.

The labour market softened in the spring. Employment was essentially flat in May 2026 at 529,000, down 200 jobs. The strong addition of 4,800 jobs in June came as good news. The unemployment rate declined 0.6 percentage points to 6.5%.

Looking ahead, strategic investments in healthcare, housing, defence, and clean energy, together with the new Fiscal Stability Plan, should support medium-term activity. Growth is still expected to outpace the national average, with GDP projected to expand by roughly 1.3% in 2026.

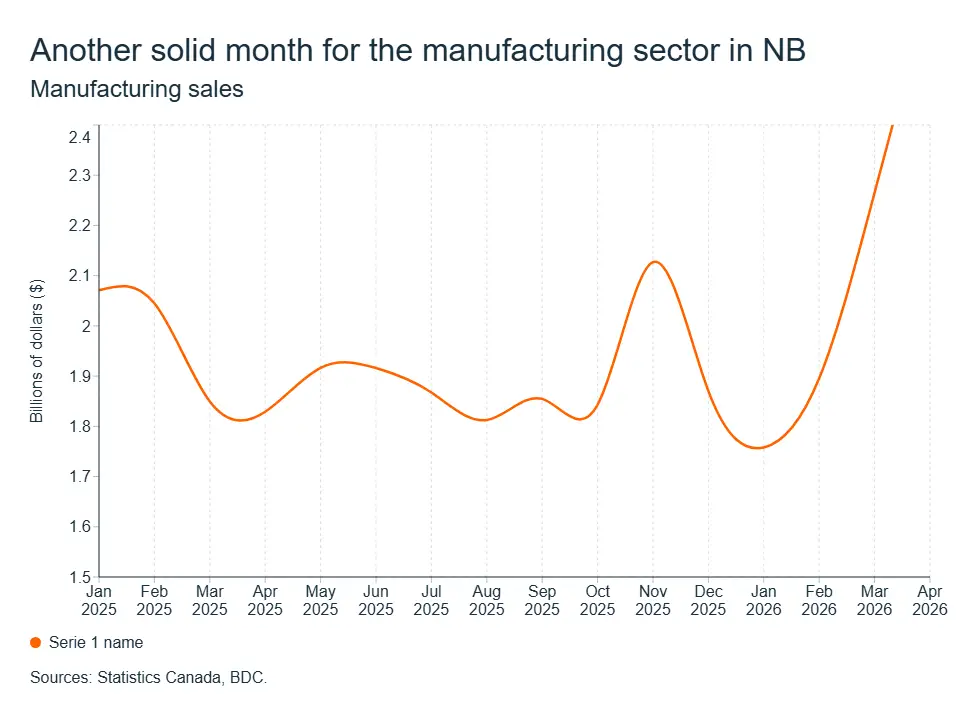

New Brunswick

New Brunswick's economy is expected to post another year of moderate growth as external headwinds and a cooling labour market temper an otherwise resilient domestic backdrop.

Consumer spending remains supportive, with retail sales still 4.6% year-to-date, suggesting household demand remains resilient. Manufacturing also improved, consistent with the national rebound in April, when sales rose 18% that month on strength in petroleum and coal products and food manufacturing.

Trade conditions appear to be stabilizing rather than slowing sharply: New Brunswick’s export base is concentrated on energy, chemicals, forestry and food products, leaving the province exposed to shifts in external demand and tariff-related uncertainty, but higher manufacturing sales and recent trade data point to some improvement in export momentum.

The labour market has softened since the start of the year. Employment rose early in 2026 and peaked in March, but losses in April, May and June brought employment down to 406,500, below January’s level of 410,000. Contrary to the national picture, the unemployment rate in New Brunswick increased from 6.7% in January to 7.3% in June.

Capital spending is expected to rise by more than 20% this fiscal year, led mainly by transportation infrastructure and health-related projects. Current forecasts point to growth near 1.2% in 2026, consistent with another year of modest expansion.

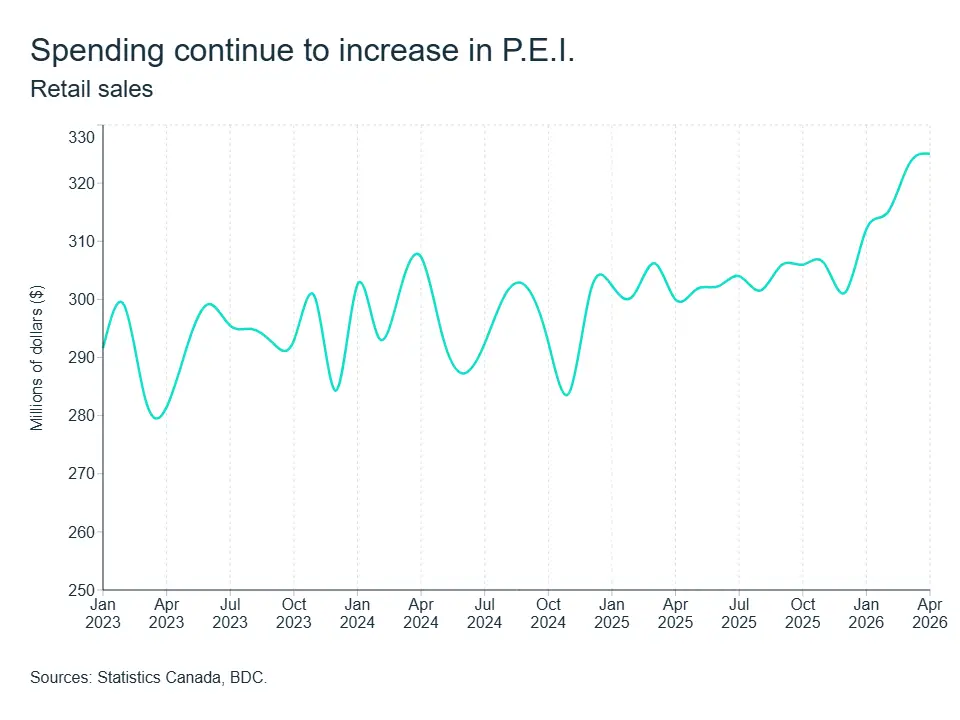

Prince Edward Island

PEI's economy is expected to slow down this year but to continue outperforming the national average, likely to grow by 1.6% in 2026.

Consumer spending remains a bright spot. Retail sales in Prince Edward Island totaled roughly $1.27 billion year-to-date through April 2026, up 8.4% from a year earlier. The labour market was broadly flat in June, with employment increasing by 200 jobs and the unemployment rate stood at 7.4%, (nearly a full point below where it was a year ago) helping support household confidence.

Trade remains the main challenge for PEI. The latest May data show exports still under pressure and below year-earlier levels, confirming that the weakness seen earlier in the spring has not fully reversed. This suggests export momentum remains soft, even as the province’s export base continues to be supported by frozen food products, seafood, aerospace-related goods and potatoes. Together with resilient domestic demand, a firm recovery in exports will be important to sustaining growth throughout the remainder of the year.

Newfoundland and Labrador

Newfoundland and Labrador is expected to be one of the strongest-performing provincial economies in 2026, supported by continued strength in the energy sector.

The province continues to benefit from favourable commodity prices, increased production and stronger resource-sector activity. The fishery sector is still recording historically high values, while gold production remains solid. Although Brent crude prices have eased as geopolitical tensions have moderated, they remain near $77 a barrel, about $17 above year-earlier levels, and the outlook remains uncertain. This should keep prices elevated in the near to medium term.

The labour market softened further in June. Despite 2,000 job losses, the unemployment rate fell sharply (to 8.2%) as the labour force shrank. Consumer spending has been essentially flat, with retail sales rising just 0.3% year-to-date from January to April 2026 compared with the same period in 2025. Slower hiring and lower population growth are expected to weigh on consumption growth this year.

Overall, strong commodity prices, robust exports and continued investment in resource projects are expected to keep Newfoundland and Labrador among the country’s growth leaders in 2026, with recent forecasts pointing to growth of around 3%.