Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreIs Canada in a recession?

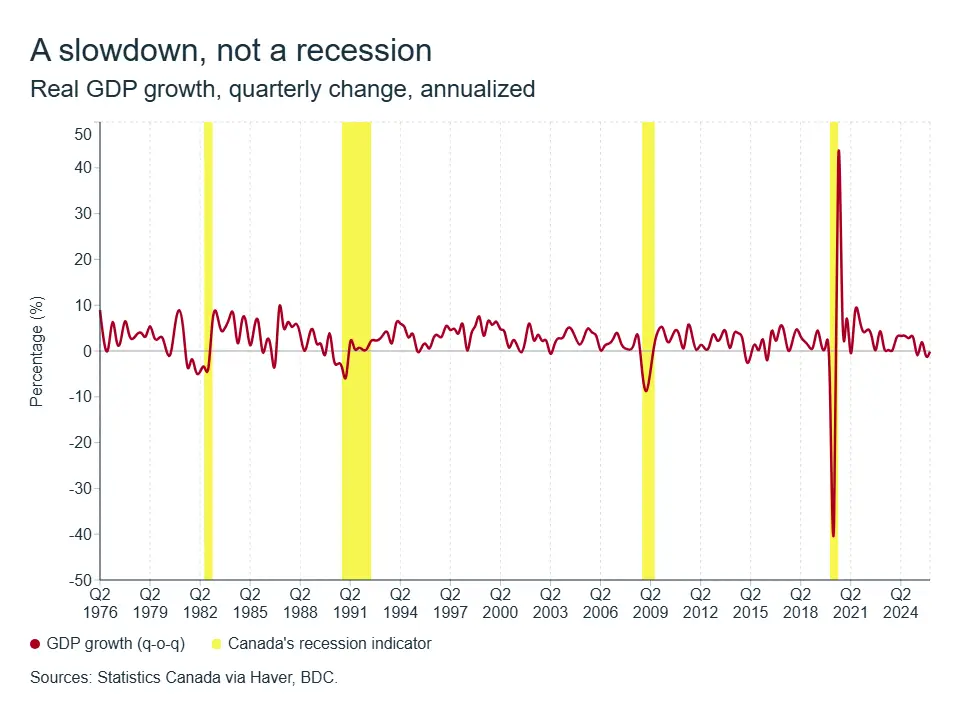

The word “recession” is back in everyday vocabulary. And for good reason: on May 29, Statistics Canada confirmed that real GDP had declined by 0.1% on an annualized basis in the first quarter of 2026, following a revised contraction of 1.0% in the fourth quarter of 2025. Two consecutive quarters in the red. Technically, that’s a recession.

But before sounding the alarm, it’s worth taking a closer look. Because there’s a significant gap between the headlines and the reality on the ground. The Canadian economy isn’t collapsing. It’s slowing down. And the distinction is far from superficial.

One word, two very different realities

There are two ways to talk about a recession, and they don’t describe the same thing at all.

The first is a “technical recession.” It’s a purely mathematical criterion: two consecutive quarters of negative real GDP growth. It’s simple, it’s clear, and it’s exactly what the numbers show right now. But this rule says nothing about the depth, composition, or duration of the slowdown. In fact, on a non-annualized quarterly basis, first-quarter GDP was essentially unchanged at 0.0%. Very small movements become dramatic when annualized. The economy is struggling to gain momentum, but even the term “technical recession” is an overstatement to describe what is happening.

The second is a recession in the full sense of the term, as defined by the C.D. Howe Institute. This refers to a pronounced, persistent, and widespread decline in economic activity, measured primarily by GDP and employment. In a true recession, we witness the destruction of an economy’s productive resources— physical capital, machinery, and equipment all become underutilized. Workers facing long-term unemployment become discouraged and leave the labour market. Bank credit tightens across the board, and the country’s income declines permanently.

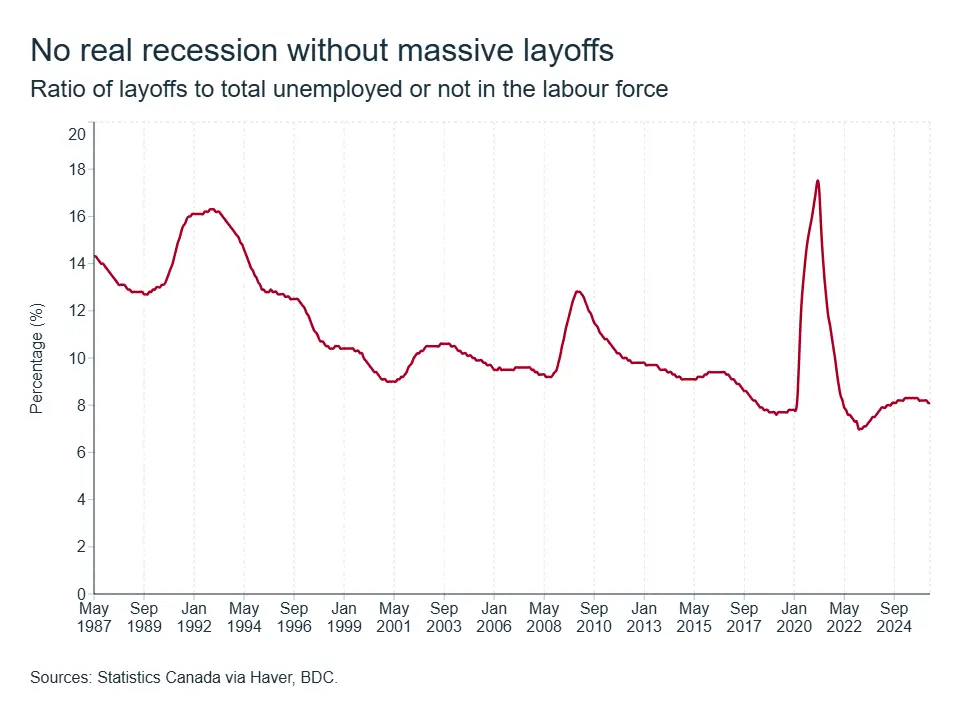

This is not what we are currently observing. The monthly layoff rate remains at 0.6%, perfectly in line with the pre-pandemic average, and the financial balance sheets of households and businesses show no signs of widespread distress. Canada is operating below its potential, to be sure. But its productive resources remain intact.

Under the hood: the five sources of growth

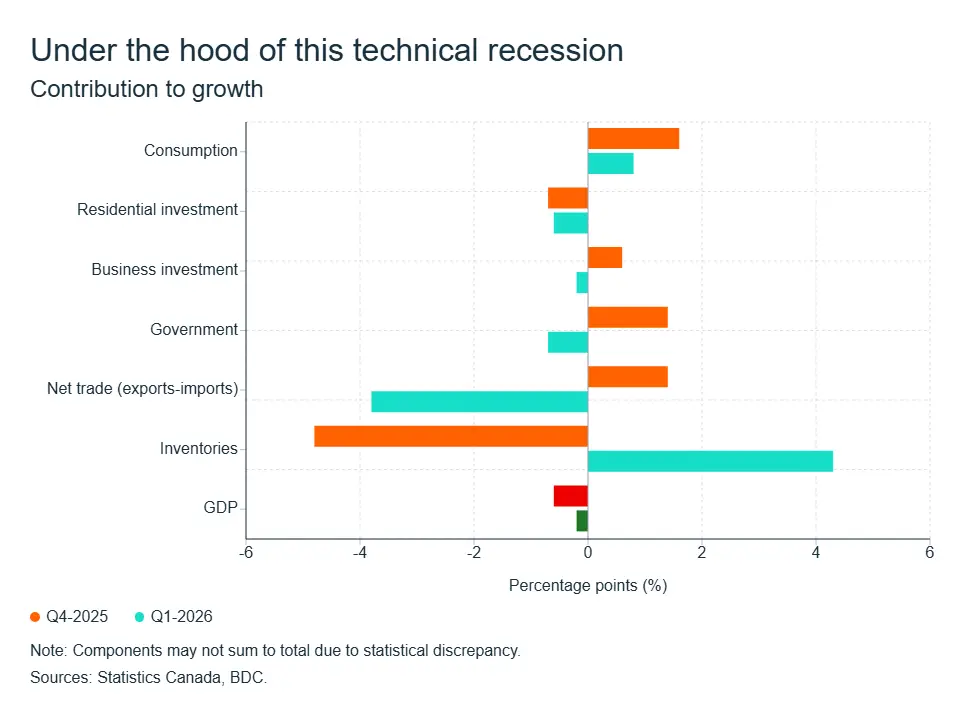

A single figure is not enough to make a diagnosis. Behind the overall change in GDP lie components pulling in opposite directions. Each component of growth plays a distinct role in predicting what the country’s economic future holds.

Household consumption remains the engine that’s still holding up

This is the most reassuring sign in an otherwise gloomy picture. Household consumption grew by 1.5% on an annualized basis in the first quarter, driven mainly by services, which grew by 2.0%, while increased spending on goods was more modest, at 0.7%. Consumption remains the main pillar of the country’s economic activity, and it is what is preventing the economy from sliding into a more severe downturn.

This observation is all the more significant given that it comes against an increasingly difficult backdrop for many households. The closure of the Strait of Hormuz has sent gasoline prices soaring, and food prices continue to rise; these pressures are directly squeezing the budget available for everything else.

Consumption is holding up, then, but the engine is weakening, with headwinds proving more persistent than expected. (We analyzed the outlook for households and business demand in the May economic letter).

Residential investment continues to weigh on growth

While consumption is the engine that’s holding up, real estate is the one that’s stalling—yet both depend largely on the same budget: household spending. Residential investment fell by 7.9% on an annualized basis in the first quarter, extending a streak of weak quarters. The decline was driven by a 9.9% drop in property transfer costs, reflecting a resale market that is struggling to recover.

The housing market landscape obviously varies from region to region. But overall, uncertainty and low consumer confidence are further slowing down major purchasing decisions. Canada’s population is also declining, which is dampening housing demand in the country compared to the record levels of recent years. Real estate therefore remains a drag on growth rather than a driver, and this is not likely to change in the short term.

Businesses continue to adopt a wait-and-see approach

This is perhaps the most concerning factor for the country’s economic future. Business investment fell by 0.2% on an annualized basis in the first quarter. Unsurprisingly, businesses are in wait-and-see mode. Uncertainty surrounding tariffs, the review of the CUSMA scheduled for July 2026, and the conflict in the Middle East is prompting executives to postpone or cancel their investment plans.

This is concerning, as business investment is the foundation of productivity growth. But there is a crucial caveat: businesses are keeping the ship afloat. Productive capital isn’t being destroyed; it’s just on hold.

Government spending in a temporary slump

Public spending amplified the surprise weakness in GDP in the first quarter. Government consumption fell by 1.0% and public investment plummeted by 9.6% on an annualized basis. But this decline follows an exceptional surge of nearly 25% in the previous quarter.

Once again, we cannot conclude that the government is scaling back; we must understand what explains this decline. It is primarily a drop in spending on weapons systems following the high levels observed at the end of 2025. In short, it’s a simple technical correction.

This type of volatility could, in fact, become more frequent in the coming quarters as Canada accelerates its defense investments and supports major projects. This represents a significant injection of funds into the economy, but in a manner that could prove sporadic. Government spending is expected to once again become a positive contributor to growth as the year progresses.

Foreign trade remains the big unknown for economic growth

If we had to pinpoint a single culprit for the contraction in GDP in the first quarter, it would be foreign trade. Exports volume declined, driven by a drop in shipments directly affected by U.S. tariffs. On the other hand, imports surged.

About half of the increase in imports came from gold and scrap metal, movements that go hand in hand with companies building up inventories. Excluding these two categories, imports rose only minimally. The widening trade deficit is therefore largely inflated by product flows that fluctuate in response to tariff uncertainty and are highly sensitive to the unstable global environment.

It is a picture clouded by volatility, in which it is difficult to discern clear signals for the future.

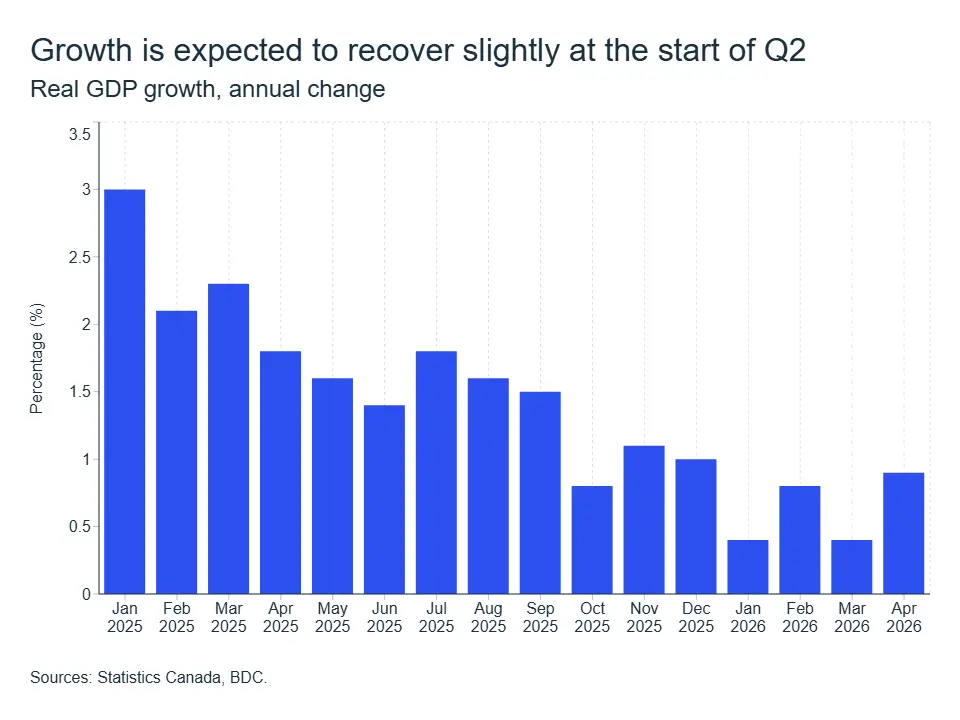

The real diagnosis: an economy running at half speed

On a year-over-year basis, GDP growth has slowed almost continuously over the past year. This is a marked slowdown and should not be downplayed.

But the hallmarks of a deep recession are not present. The labour market still shows a negative balance for 2026 despite the addition of 88,000 jobs in May. The economy as a whole is not losing its productive capacity.

BDC’s economic team maintains its growth forecast at 1.0% for all of 2026. This pace is well below potential, confirming that the economy is moving at a slow pace, but it remains in growth mode and far from a worst-case scenario.

What this means for your business

- For entrepreneurs, this slowdown is having a tangible impact on day-to-day operations. Demand will be more fragile in the coming months, but it won’t collapse.

- Your margins will remain under pressure. Production costs remain high, driven by energy and inputs, while your ability to raise prices is limited by slowing demand. Discipline in cost management is essential, but investments must not be neglected, particularly those aimed at boosting your productivity.

- Above all, do not give in to the panic associated with the term “technical recession.” The effects of the slowdown are not being felt uniformly. Some sectors and regions are faring significantly better than others. Agility, adaptability, and a keen understanding of your market will be your greatest assets.

Taking a breather, yet resilient

The Canadian economy is not in a recession, but it is clearly struggling to regain momentum. The most recent monthly data paint a picture of an economy that has gradually lost speed. BDC maintains its growth forecast at 1.0% for 2026 as a whole.

Growth remains positive; it has simply slowed

At the start of 2025, the Canadian economy was still posting annual growth of over 2%. Twelve months later, in March 2026, that rate had fallen to 0.4%. The deceleration has been nearly continuous, with no real interim rebound. This is the sharpest slowdown since the onset of the pandemic in 2020.

This slowdown did not happen overnight. Instead, it reflects the impact of a series of successive shocks: trade uncertainty linked to U.S. tariffs and the revision of the CUSMA, the closure of the Strait of Hormuz, and rising energy and food prices. Adding to these shocks is a strong deceleration in population growth, exacerbated by demographic pressures. These headwinds eroded growth momentum one month at a time. Each new shock further limits the prospects for economic recovery.

The good news is that Statistics Canada’s preliminary estimate for April points to a significant rebound from March, which would bring the year-over-year change in real GDP to about 0.9%. If this figure is confirmed, it would mark the first significant acceleration since early 2025, signaling that the trough of the slowdown may have been reached. It is still too early to speak of a reversal of the trend, but the economy is at least showing that opportunities for growth still exist.

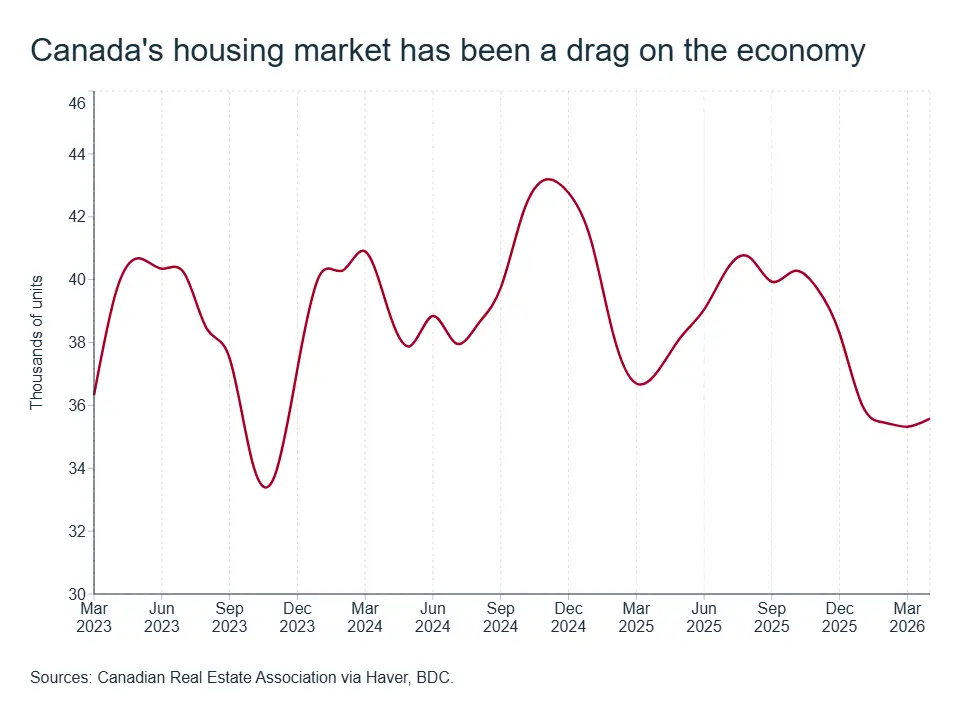

The real estate market remains stuck in a rut

Among the factors explaining this slowdown, the housing market plays a key role. Buying a home is a major financial decision. When uncertainty sets in, this is the decision people postpone first. And that is exactly what the data confirms.

In the fall of 2025, approximately 40,000 residential units were being sold monthly across the country. At that time, cuts to the Bank of Canada’s key interest rate had reignited optimism. Fast forward to April 2026, residential transactions fell to about 35,500 units, representing a decline of more than 12% in just six months and erasing nearly all of the recovery that began last year. Five-year fixed mortgage rates remain between 3.79% and 4.19% and are still high by recent historical standards.

Consumer confidence is shaken, as fear of job loss remains high according to the Bank of Canada, prompting many households to postpone major purchases such as home buying. Demographic decline is also easing pressure on housing demand compared to recent years. As long as these conditions persist, real estate will continue to weigh on growth rather than support it. The housing market landscape obviously varies from region to region.

Consumers are holding on, but inflation is weighing more heavily

While the real estate market is the leading indicator of confidence, retail sales volume is the indicator of purchasing power, and the signal they are sending deserves attention. After sustained growth in 2024, sales volumes have essentially plateaued since the beginning of 2025. The most recent months even suggest a slight slowdown.

This plateau is all the more telling given that sales in current dollars continue to show modest growth. In other words, Canadians are spending the same amount, but getting less for their money. Rising gas prices—exacerbated by the closure of the Strait of Hormuz—and accelerating food prices are directly squeezing the budget available for everything else.

The household savings rate, in fact, fell to 3.5% in the first quarter, a sign that consumers are drawing on their reserves to maintain their standard of living. Demand is not disappearing, but it is becoming more selective. Discretionary spending in particular—on dining out, leisure, and non-essential purchases—will be the first to have to offset the price increases affecting consumption of basic necessities.

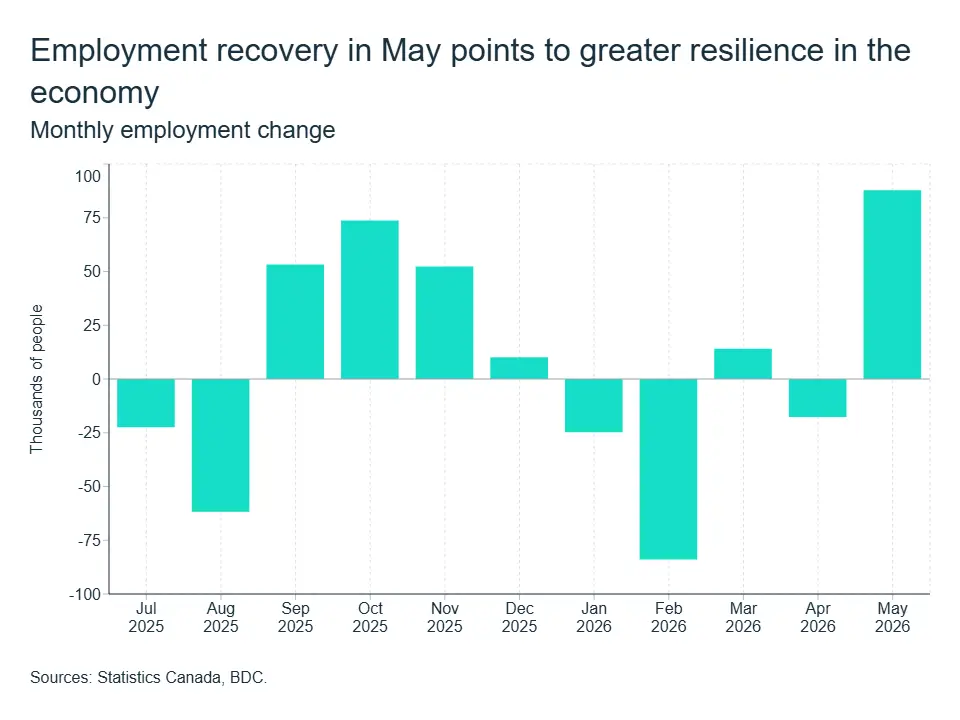

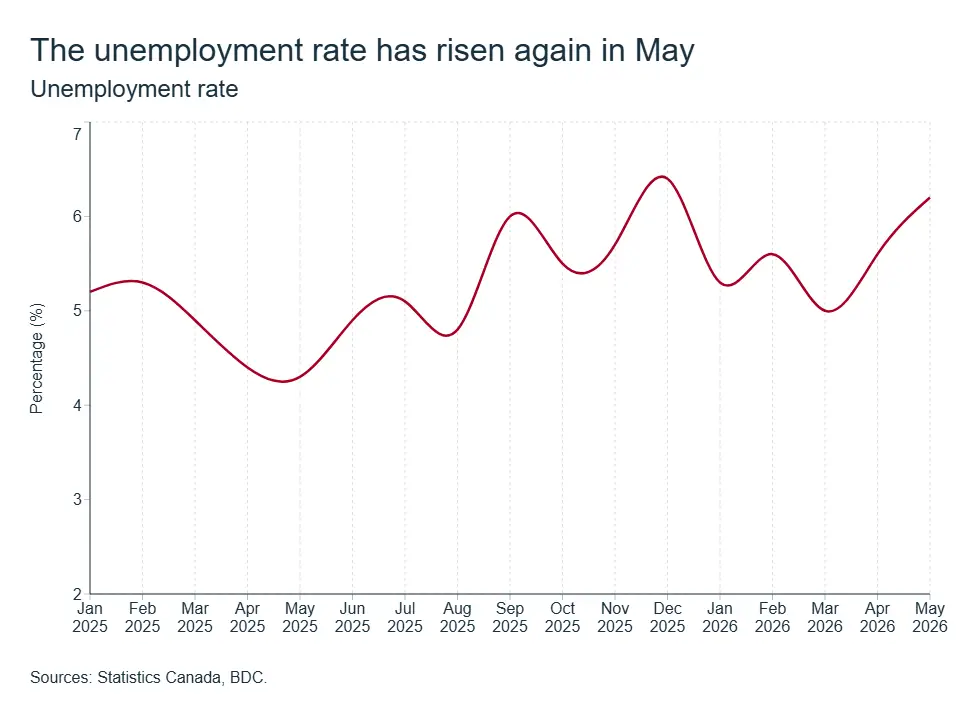

Employment rebounded strongly in May

The labour market, which had been rather sluggish since the start of the year, offered an encouraging sign in May with a gain of 88,000 jobs. This marked the best monthly performance in nearly 18 months. The rebound comes after months of turbulence, which still leaves Canada 25,000 jobs short in 2026 compared to the December 2025 level.

The up-and-down trend of 2026 clearly reflects the nature of the current slowdown. Companies are not carrying out waves of layoffs, but they are hesitant. They are hiring based on order books and the conflicting signals they receive from the geopolitical and trade environment. The May rebound is an important reminder of the Canadian economy’s resilience. This result clearly shows that the Canadian labour market still has the capacity to create jobs in significant numbers—and even full-time ones!

However, we must qualify this. A single good month does not make a trend. And volatility itself is a sign of fragility. But combined with the improved outlook for GDP in April, May’s job gains reinforce the hypothesis that the outlook is improving in the second quarter. It is too early to declare that the economy is rebounding, but it shows that it still has some resilience.

The Impact on Your Business

- The worst of the slowdown seems to be behind us, but the recovery will be gradual and uneven. Stay focused on financial discipline.

- Your customers’ purchasing power is under pressure. Energy and food costs are eating into their budgets even before they walk through your door. Adapt your offerings and focus on value.

- The job market is sending mixed signals, but one thing is clear: retaining your key employees remains your best investment. Training and retaining staff costs less than recruiting in a volatile market—and puts you in a better position when demand picks up, especially given that the population is shrinking.

British Columbia

The B.C. economy still looks subdued in mid-2026, though the latest data suggest conditions may be stabilizing rather than deteriorating further. After several weak months, employment rose by 25,000 in May, while the unemployment rate held at 6.8%, pointing to a labour market that has stopped sliding for now but remains noticeably softer than last year.

Household spending also appears restrained rather than declining. Retail sales in B.C. edged up 0.5% in March, but the broader national report showed weaker core sales and a decline in volumes, suggesting that consumer momentum remains fairly modest once higher prices are taken into account.

The housing market remains a key area of softness. Recent BCREA analysis points to subdued sales, active listings at their highest level since 2015, and modest downward pressure on prices this year, particularly in some of the province’s more expensive markets. While improved affordability should help keep activity from weakening much further, buyers are still contending with an uncertain economic backdrop and a less confident labour market.

Taken together, the B.C. economy appears to be finding a floor, but growth is still likely to remain modest and uneven through the rest of 2026.

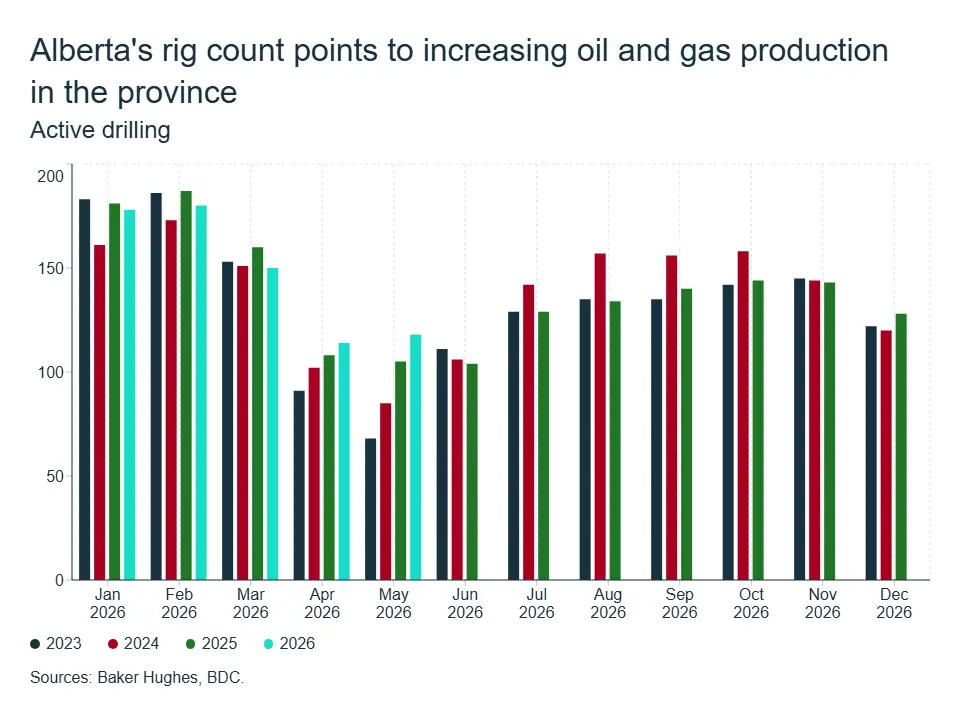

Alberta

Alberta remains the province best positioned for growth in 2026. The positive forecast is driven by high oil prices and better-than-expected economic results in late 2025. Growth is expected to reach nearly 2.5% in the region in 2026, significantly higher than the projected national rate.

The conflict in the Middle East is a major driver for Alberta’s economy. The WTI oil price averaged US$104 per barrel in May, well above the levels projected in the February provincial budget. This premium is expected to translate into a significant increase in government and corporate revenues. Oil production remains at high levels, averaging 4.17 million barrels per day over the first four months of 2026.

That said, the price increase is not translating into a production boom. Companies are maintaining financial discipline, keeping capital expenditures stable in the absence of clarity on how long the price surge will last. Drilling activity confirms this. The number of active rigs stood at 136 at the end of May, with 52% of the drilling fleet in operation—an improvement from April but still reflective of caution, according to the Canadian Association of Energy Contractors. Meanwhile, the Trans Mountain pipeline expansion is paying off, as oil exports to Asia reached a record high of over $9 billion in 2025.

The labour market in Alberta rebounded in May. Employment rose by 14,000 (+0.5%) and the unemployment rate fell to 6.6% as the province recovered from a sluggish April. Since the start of the year, Alberta has created about 40,000 jobs, and year-over-year employment growth of 4.1% leads all provinces. Average weekly wages are rising faster than the national average and are well above inflation. However, retail sales remain volatile: after falling 1.9% in February, they rebounded 2.6% in March, largely driven by higher gasoline prices—a sign that underlying consumer demand remains fragile.

Saskatchewan

As a resource-driven province, Saskatchewan's economy is well positioned to grow above the national average in 2026. Real GDP growth could reach above 2%, placing it just behind Alberta among the provinces. The ongoing closure of the Strait of Hormuz continues to support oil, gas and mining activity, with oil prices well above the province's conservative budget assumption.

The mining sector remains the province's growth engine. In 2025, total mineral sales reached $12.8 billion (+19%), led by potash ($9.3 billion, +18%) and uranium ($3.2 billion, +24%, a record). The momentum has carried into 2026, with April potash sales up 25.9% year-over-year and production up 11.1%. Uranium sales, however, fell 26.0% in April on planned maintenance shutdowns.

On the investment front, NexGen received its construction licence from the CNSC in March 2026 and will begin building the Rook I uranium mine this summer, the largest development-stage uranium project in Canada. Meanwhile, BHP's Jansen potash mine, now 75% complete, has pushed its first production to mid-2027 but recently signed rail transportation agreements with CN and CPKC to connect Saskatchewan potash to global markets.

The Middle East conflict is also driving up nitrogen fertilizer costs for farmers. Urea prices, while retreating from their spring peaks, remain elevated compared to pre-conflict levels. Many farmers had stocked up before the conflict escalated, according to the Canadian Federation of Agriculture. Manufacturing rebounded sharply in March, with sales surging 20.6% month-over-month and up 18.3% year-over-year. Despite this, exports to the United States remain under pressure from tariffs.

The labour market weakened further in May. After losing 4,000 jobs in April, the province shed an additional 6,100 jobs (-1.0%), and the unemployment rate rose to 6.2% (up from 4.3% a year ago). Saskatchewan nonetheless ranks third lowest among the provinces, just below the national average of 6.6%. The labour force, however, reached a record high in May, a sign that population growth will continue to support consumer spending over the medium term if employment follows.

Manitoba

Manitoba's economy is expected to grow moderately in 2026. The provincial budget projects real GDP growth of 1.3%, slightly above the national average, though BDC's forecast is more conservative at 1.0%.

The budget included several measures to ease the burden on households. Starting July 1, the province will eliminate the 7% PST on all grocery items sold in grocery stores, including prepared meals, soft drinks and snacks.

The labour market was largely flat in May. After a strong rebound in March (+11,000 jobs) and a slight decline in April, employment was essentially flat in May (+300). The unemployment rate rose to 5.5%, as new entrants joined the labour force while employment stalled. Year-over-year, however, employment remains up 2.6%.

Manufacturing showed signs of recovery. After falling 5.5% through February, manufacturing sales rebounded sharply in March (+9.4% month-over-month to $2.5 billion), bringing the year-to-date decline to just 0.3%. The agri-food industry accounts for nearly a third of the province's total manufacturing sales, and while the agreement reducing Chinese tariffs on canola was welcome news, international exports remain the weak spot. Total exports fell 27.2% (on a nominal basis) in the first quarter, with exports to the United States down 34.3%, largely due to a sharp drop in pharmaceutical shipments and continued tariff pressure. High energy prices could also drive-up transportation costs, a key risk for Manitoba's economy which relies heavily on domestic trade.

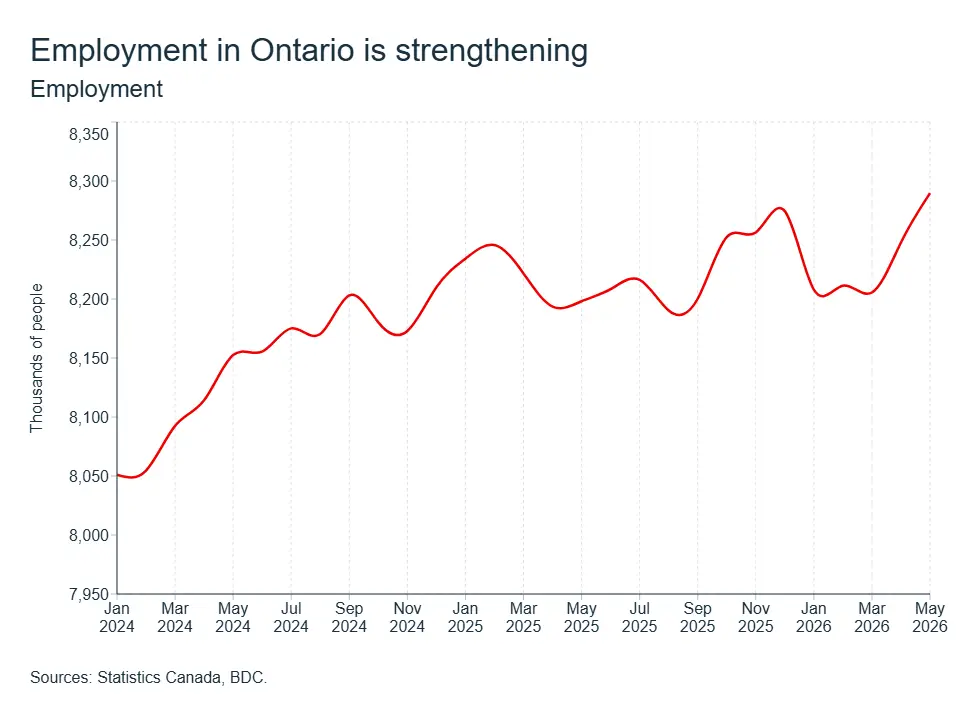

Ontario

Employment continued to grow in Ontario, with nearly 42,000 jobs added in May, following an increase of 42,500 in April. After a very slow start to the year, employment has risen sharply in recent months.

The construction sector is regaining momentum thanks to growth in the non-residential sector, driven by the acceleration of infrastructure projects by the Ontario government.

Employment in the manufacturing sector is also improving, driven by an increase in exports in recent months. Furthermore, the sharp decline in employment in the education sector appears to be stabilizing. After the initial shock of the significant drop in the number of international students, the sector seems to be in a better position.

Finally, the retail sector remains under pressure: employment continues to decline, despite growth in retail sales. It appears that the rise in oil prices over the past two months is putting significant pressure on this sector.

Quebec

Quebec's economy continues to navigate a challenging environment and much of the sluggishness stems from a difficult trade environment. Exports declined 13% in Q1 2026 under the weight of U.S. tariffs on steel, aluminum, lumber, and autos. A 19% rebound in March offered some relief, but overall trade levels have yet to recover to pre-tariff norms.

Manufacturing was the main drag on Québec’s economy in the first two months of 2026, with output declining by 4.0%, making it the largest contributor to the overall decrease in real GDP.

May’s employment data brought some welcome relief: employment increased by 13,200 and the unemployment rate dropped to 5.6%. However, the labour market is still soft: employment levels remain below last’ years average and have yet to recover.

Despite these pressures, other sectors supported growth, in the first two months of 2026, including finance and insurance (+3.0%), retail trade (+2.6%), wholesale trade (+2.2%), and real estate and rental and leasing (+1.5%).

Quebec households have shown relative resilience so far, supported by lower indebtedness and high saving rates that continue to cushion consumer spending. Retail sales were positive early in the year before dipping 0.8% in March.

Looking ahead, below-potential growth is expected to persist as trade uncertainty and a cooling labour market continue to weigh on activity. Growth is expected to reach 0.7%, placing the province among Canada's slowest-growing economies. For now, government spending and household consumption remain the province's main engines of growth, helping it avoid a recession.

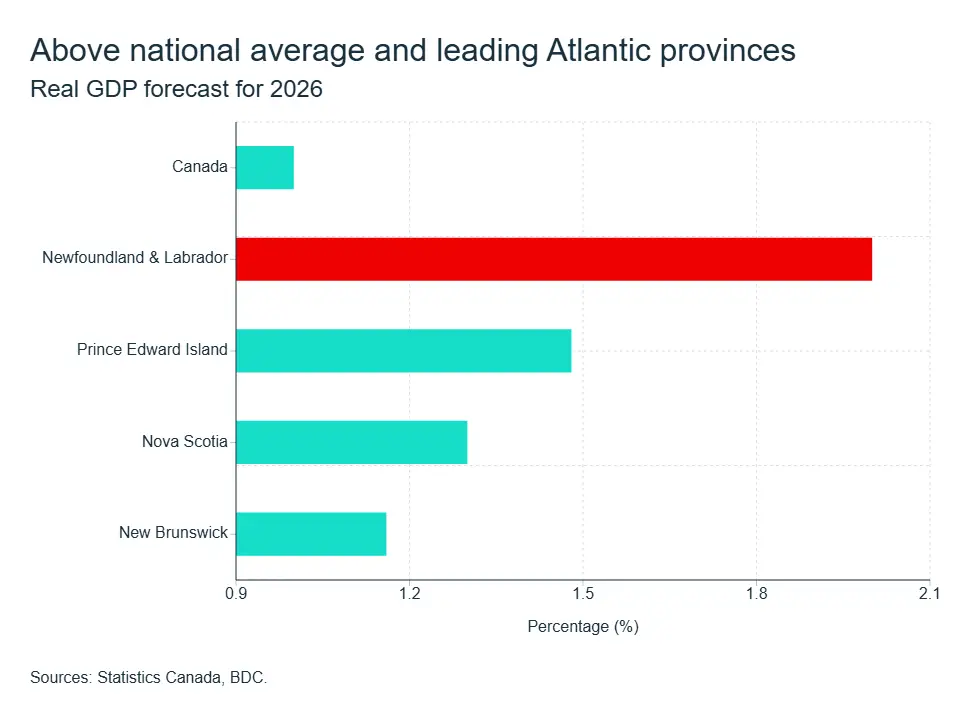

Nova Scotia

Nova Scotia's economy is anchored by solid domestic fundamentals. Retail sales rose 3.3% in 2025 and posted a 2.9% increase in the first quarter of 2026, while non-residential investment surged 10.7% in Q1 2026.

Still, the province is adjusting after several exceptional years. Real GDP growth is estimated to have slowed, as population growth moderated from a record 2.8% to just 1.0%. Growth is expected to reach 1.3% in 2026 and exceed the national average.

Headwinds persist on the trade and labour fronts. Exports declined 3.4% in Q1 2026 amid ongoing tariffs, and the labour market took a step back in May. Meanwhile, the unemployment rate surged to 7.1% — its highest level since early 2025 — driven by a sharp expansion of the labour force as more Nova Scotians entered or re-entered the job market.

Nova Scotia is planning strategic investments in healthcare, housing, defence, and clean energy, alongside a Fiscal Stability Plan to slow expense growth.

In short, domestic spending and investment provide a solid floor, even as Nova Scotia navigates softer trade and a more moderate growth path.

New Brunswick

New Brunswick's economy is expected to grow by 1.2% in 2026, a modest pace as external headwinds and a cooling labour market temper an otherwise resilient domestic backdrop.

On the consumer side, spending continues to provide a solid foundation. Retail sales grew 4.8% in 2025 and have trended upward since November, with March 2026 posting another 0.7% monthly gain.

New Brunswick's manufacturing sector staged a strong rebound in March 2026, but the broader picture remains mixed: sales through Q1 2026 were still weighed down by a weak January, and ongoing trade uncertainty.

The labour market remained soft in May, failing to participate in the broad national rebound. Employment edged down by roughly 400 jobs (-0.1%) to 408,000, while the unemployment rate held steady at 7.2%.

The province is leaning into deficit spending to sustain key priorities which will support growth. Resources are being channelled into healthcare, education, and support of industry.

Resilient consumer spending and a rebound in trade are keeping the economy afloat, but slower population growth and a softening labour market point to another year of moderate growth.

Prince Edward Island

PEI's economy is expected to grow by 1.5% in 2026, outpacing Canada's projected growth, as resilient domestic demand helps offset persistent trade pressures.

Consumer spending remains a bright spot. Retail sales continued to rise in early 2026, with Q1 posting a 4.0% increase, a sign that households are confident and ready to spend. A stable job market has been supporting this momentum. In fact, the labour market bounced back in May, as employment rose by an estimated 1,500 jobs and unemployment dipped to 6.7%.

Trade, however, has been under significant pressure. Exports declined 10.5% in Q1 2026, as trade with both the U.S. and China weakened. That said, the new agreement on trade with China is expected to provide some relief, and volumes should gradually pick up in the coming months.

Solid consumer activity and a relatively stable job market are keeping the province on a healthy growth path, even as trade headwinds remains a key challenge.

Newfoundland and Labrador

Newfoundland and Labrador is poised to be one of Canada's top-performing provinces in 2026, with GDP expected to grow by 2.0%, well above the national average.

The province continues to benefit from a favourable commodity environment, boosting its exports. The rebound in the gold sector—with the launch of the Valentine gold mine and the restart of the Hammerdown project—is supporting diversification, marking the province's first international gold shipments in over two decades.

The fishery sector also registered a record $1.3 billion in landed seafood value last year.

Meanwhile the labour market seems to be easing, a slight cause for concern. Employment decreased by 0.5% in May but levels remained close to where they were in December last year. Consumer spending gained traction, however: retail sales jumped to a new peak in March, supported by decent employment and commodity-driven confidence.

Strong commodity prices, surging exports, and solid consumer spending are powering a good year for the province, even as demographic headwinds remain longer-term concerns.