Canada’s defence boom is creating a three-speed SME divide

Canada is entering a period of sustained defence spending growth, creating a rare window of opportunity for SMEs. But scaling into this market is not straightforward: capacity is tight, requirements are complex and access to capital remains a key constraint. How SMEs navigate these constraints will determine who is able to scale, and who remains on the sidelines.

Executive summary

Demand for defence SMEs is rising, but their ability to scale is shaped by capacity constraints, financing gaps and complex requirements. This points to a three-speed SME landscape: firms specialized in defence working to scale up capacity to meet demand; firms balancing a predominantly civilian market with growing defence opportunities; and firms preparing to enter the sector.

This reflects a growing divide across the ecosystem, with capacity constraints, financing gaps and readiness shaping which firms are able to participate in the sector’s growth.

- Defence SMEs are operating in a high-growth environment, with many already near capacity.

- Defence SMEs span multiple industries, with concentrations in IT, manufacturing, professional services and construction.

- There are two types of defence SMEs that share similarities but also have distinct characteristics:

| Defence-heavy SMEs | Defence-light SMEs | |

|---|---|---|

| Definition | Majority of sales are in the defence sector | Minority of sales are in the defence sector |

| Outlook | Very strong growth outlook (87% expecting growth in defence) | Strong growth outlook (70% expecting growth in defence) |

| Capacity | Very limited spare capacity | Some spare capacity |

| Investment outlook | Very strong | Strong |

| Main obstacles to growth |

|

|

- Trade is important for defence SMEs, as two-thirds export and/or import goods or services. Additionally, the same proportion expect some of their sales growth over the next two years to come from abroad.

- Most defence SMEs expect to request financing in the next 12 months to support their growth (47%), develop new products or services, meet their working capital needs and prepare projects (all at 31%).

- However, 52% of businesses looking for financing think that access will be difficult. Defence SMEs find it challenging to secure financing, with financial institutions remaining cautious about the risk profile, limited customer base and unstable cash flows of the sector.

- A majority (58%) of defence-heavy SMEs are looking for equity, often for amounts above $1 million. Defence-light SMEs are looking mostly for working capital loans (38%) and lines of credit (41%).

- Many non-defence SMEs are interested in joining the defence sector and can bring a variety of expertise and capabilities: IT products, engineering services, construction, as well as ground vehicles, personal equipment, aerospace and shipbuilding. Some even have capabilities in weapons and ammunition.

- SMEs interested in joining the defence sector face challenges as well, the first being meeting defence-specific requirements.

- Growth is uneven across the ecosystem, with established firms working to scale up to meet demand while others face barriers to entry.

Canada’s defence ecosystem has entered a period of profound transformation.

Rising global demand, shifting supply chains, and renewed commitments from allies are converging to create a step-change in opportunity for Canadian industry. For Canada, this moment goes beyond strengthening sovereignty—it is an opportunity to build a more resilient, competitive industrial base for the long term.

SMEs are central to this evolution. Across the country, they are demonstrating the innovation and agility required to contribute to modern defence capabilities.

This study reinforces what we are hearing across the ecosystem: demand is accelerating, but the ability to scale remains uneven. Many firms are operating at capacity, while others are preparing to enter a complex and highly regulated market for the first time.

In more than 35 years in the Canadian Armed Forces, I have not seen strategic urgency, political commitment, and access to capital align so clearly. But translating this alignment into outcomes will require more than momentum—it will require execution.

Progress will depend on stronger coordination across the ecosystem and clearer, more accessible pathways for firms to enter and grow. It will also require sustained support for businesses—particularly those new to the sector—as they navigate its complexity and position themselves for long-term success.

At BDC, we are committed to helping Canadian SMEs meet this moment. Our goal is clear: to support the growth of Canadian companies and their enduring contribution to Canada’s security and prosperity.

As defence spending is increasing in a context of slower economic growth, opportunities will arise for Canadian SMEs to play a role in a growing defence ecosystem. This report examines the current landscape for defence SMEs and prospective entrants to the sector.

SMEs are already a driving force within the defence ecosystem. They span a wide range of industries, with concentrations in IT, manufacturing, professional services and construction. They have a strong sales outlook for the next two years, but face several challenges including long sales cycles, financing difficulties and economic uncertainty.

Among the most defence-specialized businesses, many are already producing near capacity and are planning to increase their investment significantly to meet demand. At the same time, other firms are progressing more cautiously or preparing to enter, reflecting different levels of readiness across the ecosystem.

Nearly half of defence SMEs anticipate seeking financing in the coming year to fuel growth, develop new products and meet operational needs. Yet more than half expect difficulties accessing capital, as financial institutions remain cautious due to perceived risks, limited customer bases and variable cash flows.

The defence sector is also attracting new players, with many SMEs expressing interest, bringing expertise in IT, engineering, construction and even advanced manufacturing for vehicles and equipment. These entrants face significant barriers, especially in meeting defence-specific requirements, but their participation is crucial for diversifying capabilities and strengthening supply chains.

Rising defence spending is reshaping the economic landscape, opening new growth pathways for Canadian SMEs. For sectors experiencing slowdowns, the defence sector offers a pathway to reorient parts of their operations and tap into new markets.

According to the Stockholm International Peace Research Institute, world real military spending increased by 41% between 2016 and 2025. Just in 2025, it increased by 9.2%, excluding the U.S. Global real military spending is now estimated at 2,887 billion US$ (constant $ 2024), representing 2,5% of world GDP. Recent growth has been particularly important in Eastern Europe, Asia and Africa.

The top world spenders are the United States, China, Russia, Germany and India, representing 58% of all world spending. Other large spenders are the United Kingdom, Ukraine, Saudi Arabia, France and Japan. These top ten countries account for 72% of all world spending.

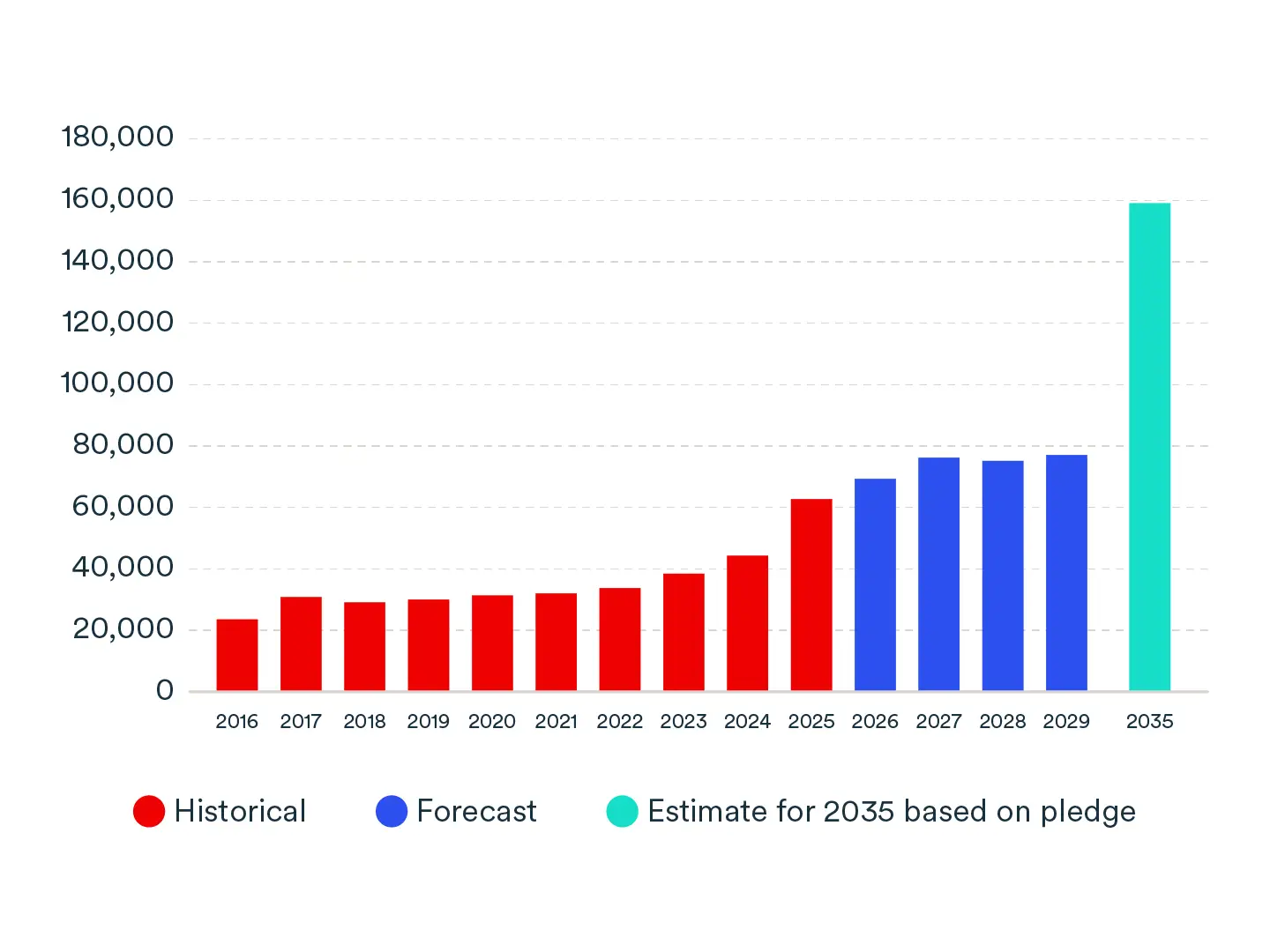

Canada was the 16th largest spender in 2025, but its ranking is expected to evolve rapidly, as the country has significantly increased spending to catch up to 2% of GDP—from 1.5% in 2024. As NATO countries pledged to spend 3.5% of their GDP on core defence spending by 2035, another major uptick in spending is expected in the next decade (Graphic 1). Considering the size of the Canadian economy, Canada will be in the top 15 largest spenders by 2035 and will even likely be in the top 10.

According to the office of the Parliamentary Budget Officer, Canada will need to spend $159 billion in core defence spending by 2035 to reach 3.5% of GDP. This implies that defence spending will more than double between 2026 and 2035. Because Canada is catching up with other countries, defence spending in Canada is expected to increase faster than the world average over the next 10 years.

Canada’s core defence expenditure based on NATO definition (millions CAD) (Graphic 1)

The defence sector is relatively small in Canada and can be difficult to define, as it does not follow the traditional industry classification. In effect, it is more a market than a sector. Additionally, many businesses can work with the Department of National Defence without publicly identifying as defence companies.

For now, Canada only has a single representative in the world’s top 100 arms producing and military service companies, but it benefits from the presence of close to 600 defence businesses, including many Canadian SMEs and foreign subsidiaries. Defence businesses work in a wide array of industries but are concentrated in manufacturing, IT and engineering services.

These businesses are just the tip of the iceberg, as they also rely on a variety of suppliers. BDC estimates that several thousand businesses in Canada are involved, from near or far, in defence supply chains. That number is likely to increase as military spending ramps up.

Many businesses in non-residential construction and construction-related services are also involved in the defence ecosystem as investment in infrastructure represent a significant portion of defence spending. Increased spending from the Department of National Defence will lead to growth opportunities for these businesses as well.

Unexhaustive list of the main defence-related and supporting industries

| Main industries for direct defence businesses | Examples of supporting industries |

|---|---|

|

Ship and boat building Aerospace product and parts manufacturing Motor vehicle body and trailer manufacturing Other transportation equipment manufacturing Other fabricated metal manufacturing Computer and electronic product manufacturing Computer systems design and related services Architectural, engineering and related services Transportation support activities Non-residential construction |

Forging, stamping and other fabricated metal product manufacturing Motor vehicle parts manufacturing Miscellaneous manufacturing Iron and steel mills and ferro-alloy manufacturing Non-ferrous metal (except aluminum) production and processing Engine, turbine and power transmission equipment manufacturing Steel product manufacturing from purchased steel Alumina and aluminum production and processing Machine shops, turned products, and screw, nut and bolt manufacturing Electrical equipment manufacturing Semiconductor and other electronic component manufacturing Plastic product manufacturing Software publishers Computing infrastructure providers, data processing, web hosting, and related services |

Source: BDC estimate using Statistics Canada input-output tables

To better understand defence-sector SMEs and those interested in joining, BDC partnered with Forum Research and the Icebreaker to survey them.

In total, 268 self-identified businesses in the defence sector and 374 businesses interested in pursuing defence opportunities completed the survey, for a total of 642 respondents.

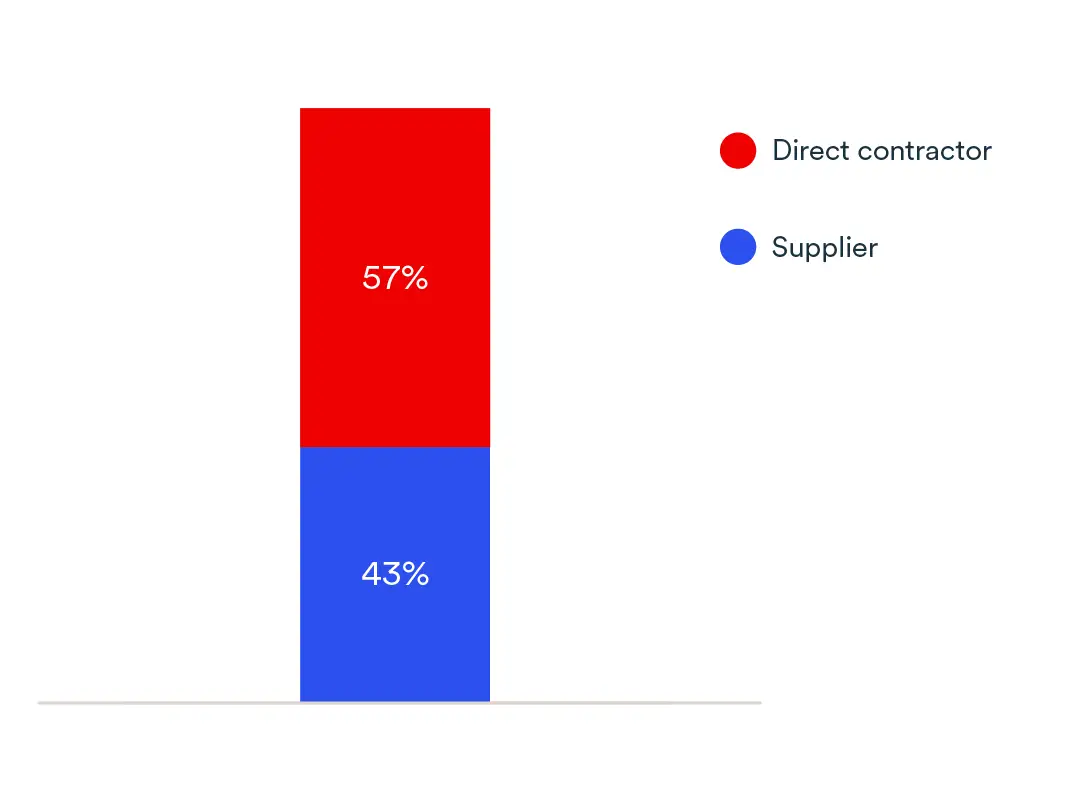

Respondents active in the defence sector were mostly directly involved in defence, but a significant minority were suppliers. Additionally, defence companies can be categorized into two groups:

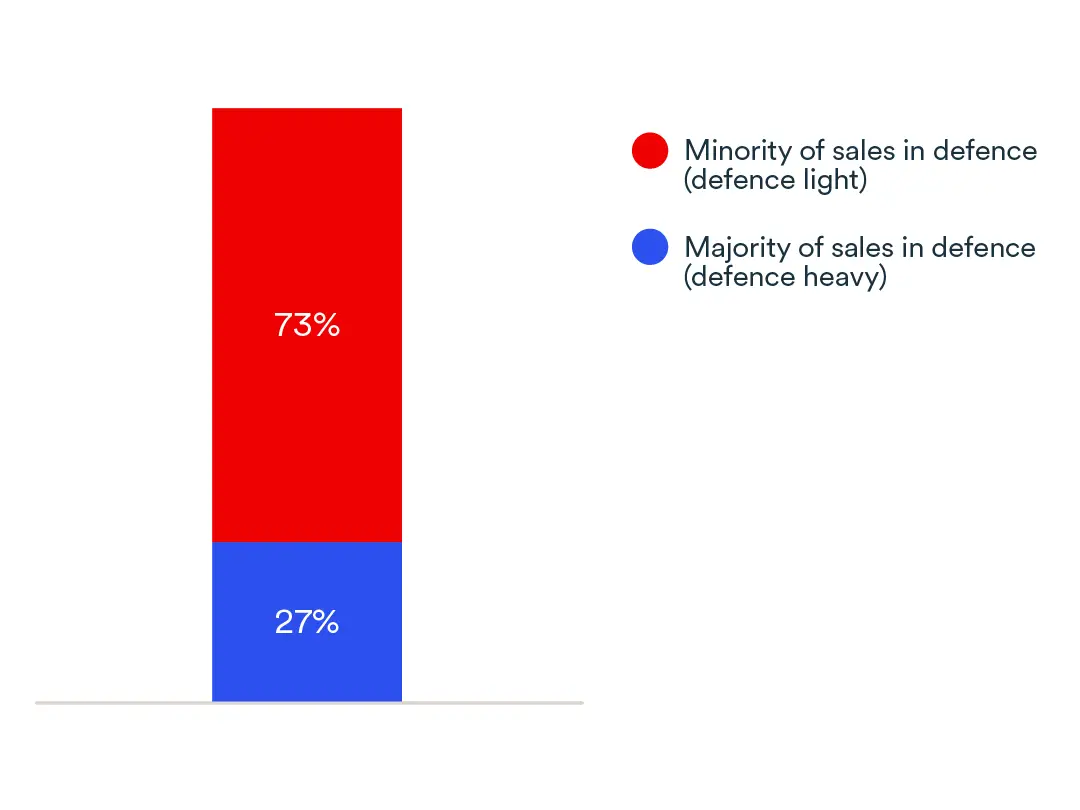

- Defence-light companies: SMEs that make a minority of their sales from defence contracts.

- Defence-heavy companies: SMEs that make a majority of their sales from defence contracts.

Most defence SMEs are defence-light (73%) and about a quarter are defence-heavy.

The results for the rest of this report are based on this survey and offer a glimpse of the situation of defence SMEs in Canada.

Key characteristics of survey respondents in the defence sector

Distribution of survey respondents by defence intensity (Graphic 2)

Distribution by role in the defence supply chain (Graphic 3)

Distribution by area of capabilities (Multiple choice) (Graphic 4)

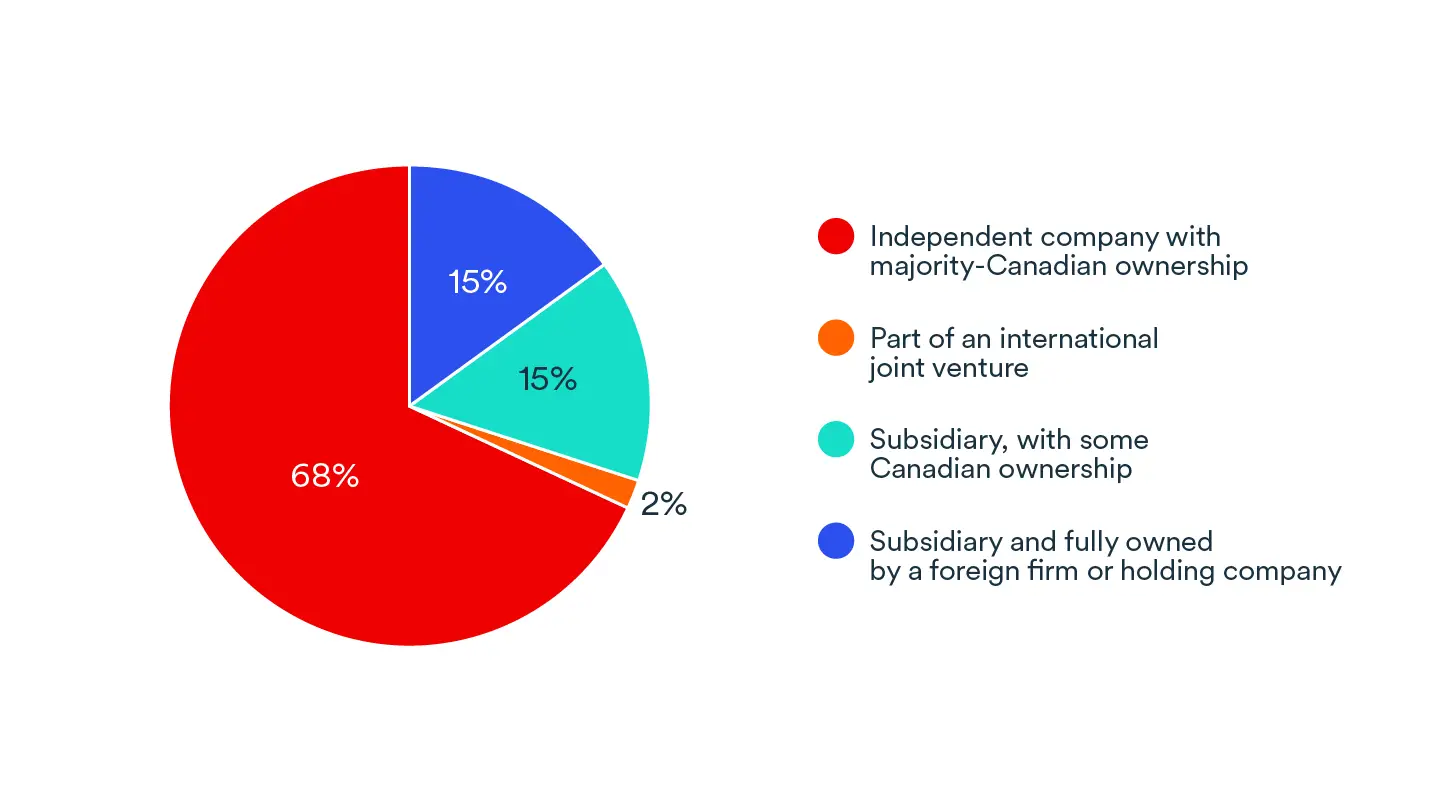

Business structure of defence SMEs (Graphic 5)

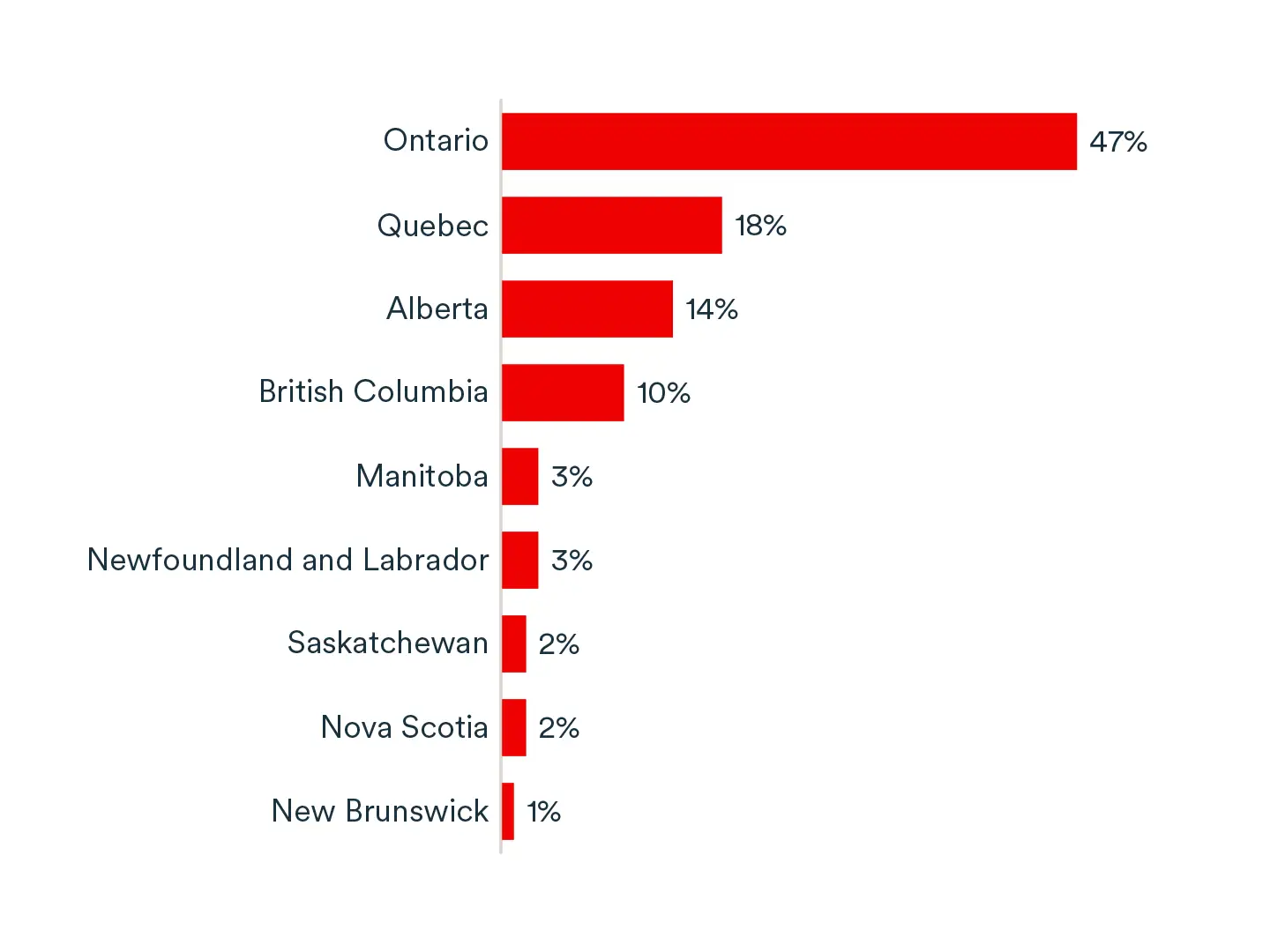

Province or territory where most of their activity take place (Graphic 6)

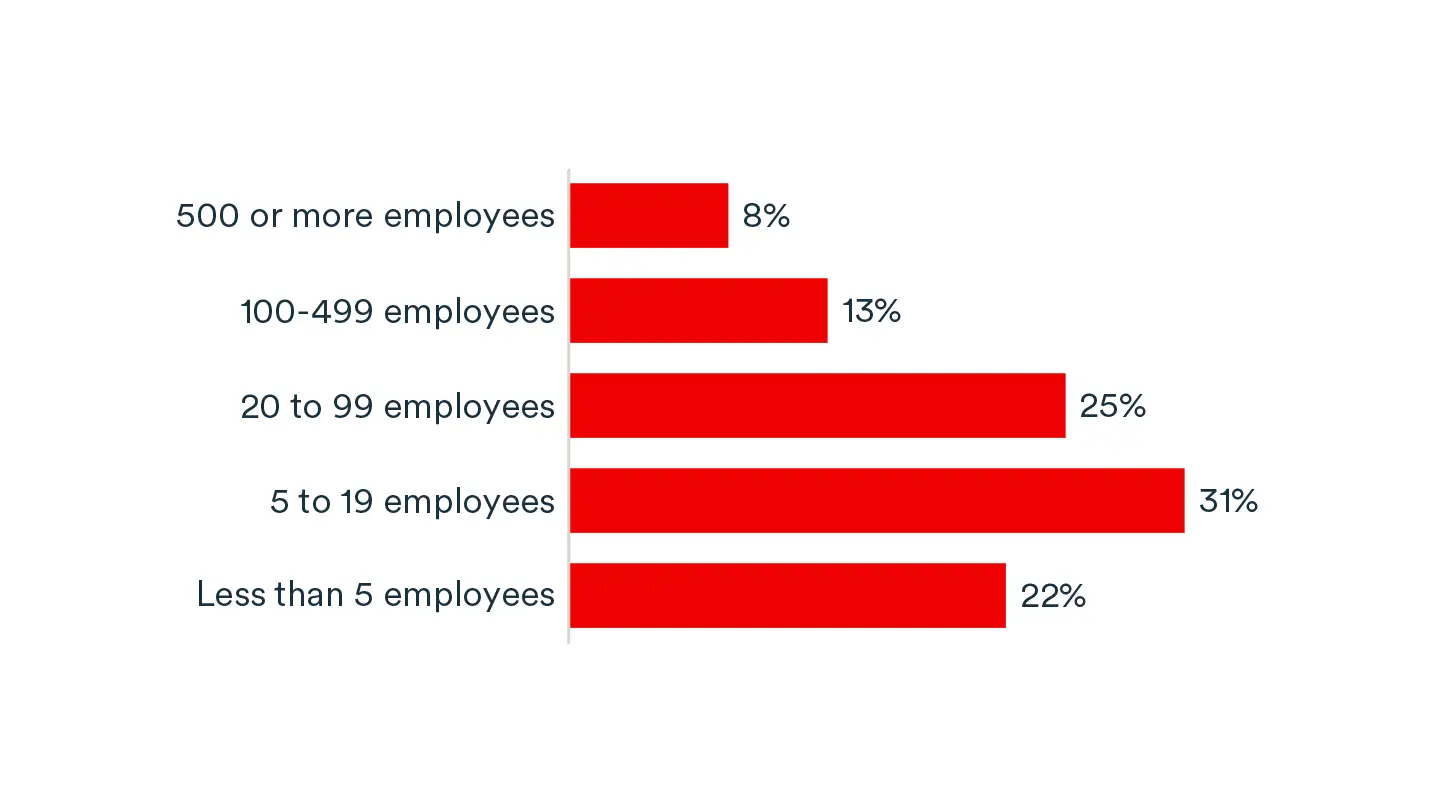

Number of employees (Graphic 7)

Taken together, these results highlight a three-speed SME landscape within the defence ecosystem: Firms specialized in defence and operating at or near capacity; firms balancing growing defence demand with their traditional civilian markets; and businesses exploring entry.

With military spending growing in Canada and the world, defence SMEs expect a strong increase in revenue from defence-related contracts over the next 24 months. However, civilian operations are important for most defence SMEs: 73% of them are defence-light companies that get most of their sales from civilian contracts.

Defence-heavy SMEs are particularly growth-oriented (75%), as most of their activity is driven by defence contracts. Securing funding is also one of their top priorities as they are looking to build capacity.

Many defence-light SMEs are also growth-oriented, but to a lesser extent. Efficiency is the second priority (42%) for these companies. While the defence market is growing, their priorities remain tied to their civilian activities, where they generate most of their revenues. The situation can vary greatly from one business line to the other, as demand for some traditional industrial goods is slowing while demand for military equipment is rising.

Companies in IT and aerospace are reporting a stronger demand for their goods and services, with respectively 48% and 51% expecting significant increase in defence sales. Overall, defence-heavy SMEs expect stronger growth of their defence revenues than defence-light SMEs.

Current priorities of defence SMEs (Graphic 8)

Expected growth in defence contract revenues over the next 24 months compared to the last 24 months (Graphic 9)

International trade is key to growing defence SMEs. According to ISED, roughly half of the Canadian defence sector’s revenues come from exports and 47% of supply chain expenditures went to businesses based abroad. The main markets for Canadian defence products or services are the U.S., (63% of exports) and Europe (21%). The Middle East and Africa are also important markets (9%). Additionally, export diversification beyond North America will become increasingly important for businesses seeking to broaden their customer base and capitalize on rising demand in Europe and Asia

Our survey shows that only 14% of defence SMEs are not involved in international trade. About two-thirds import and/or export, 40% made direct investment outside Canada and 55% have a foreign alliance or partnership.

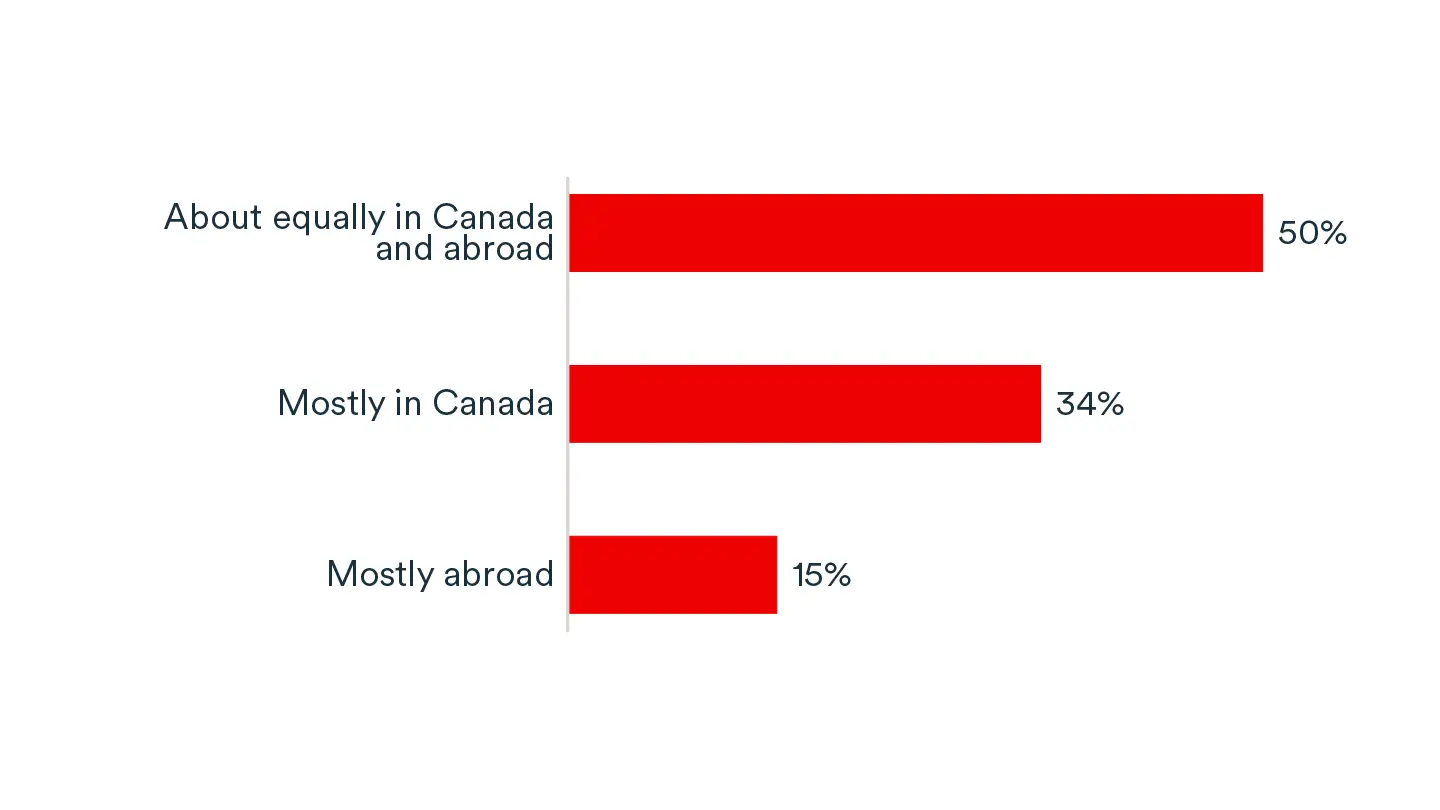

In that context, two-thirds of respondents expect some or most of their revenue growth over the next two years to come from abroad, including 15% expecting most of the growth to come from abroad. About half expect growth to come equally from Canada and abroad, and a third expect it to come mostly from Canada.

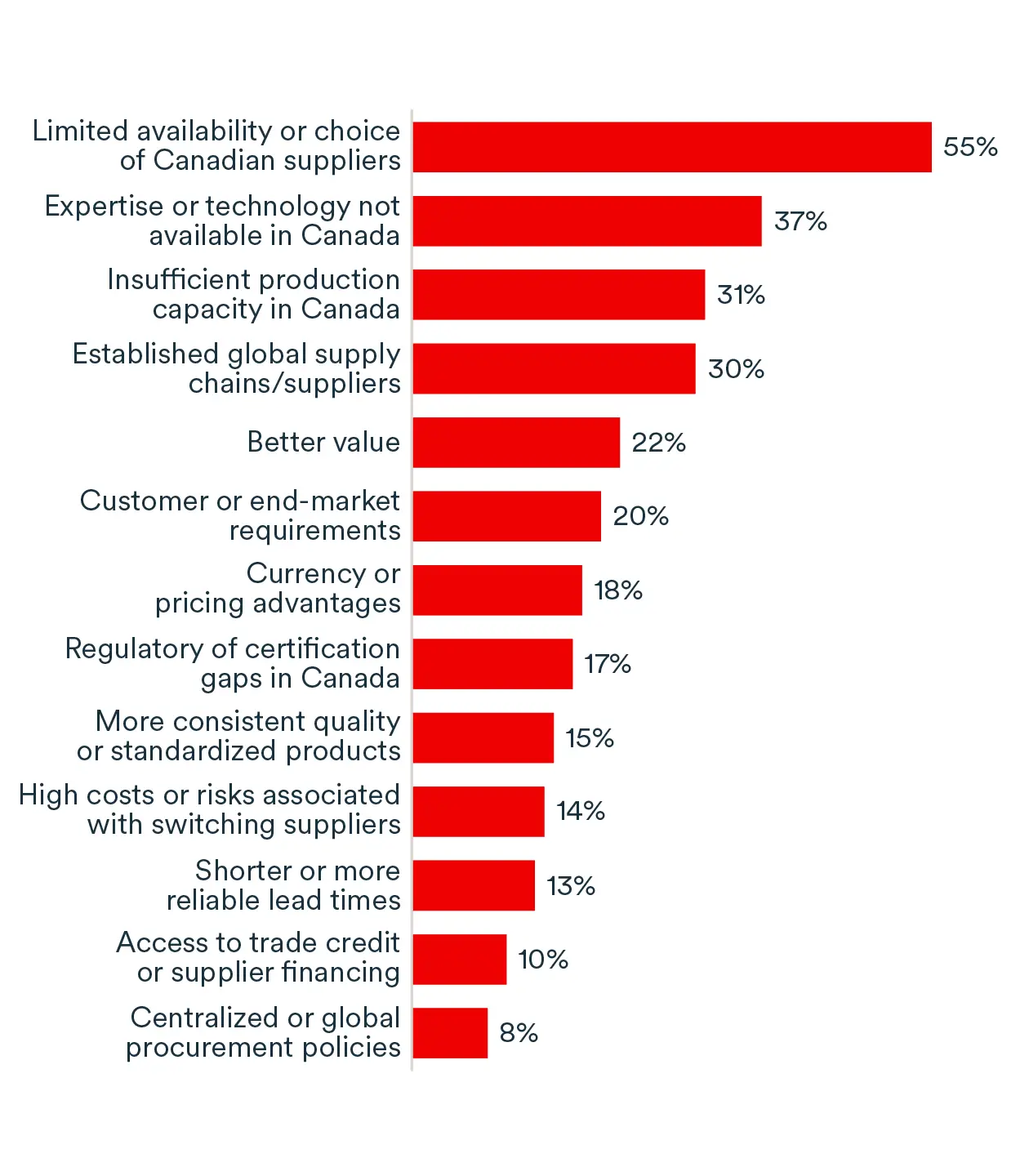

In terms of supply chain, Canadian defence SMEs tend to import what they cannot find in Canada, whether that be expertise, technology or quantity. Many importers also have established suppliers abroad. Costs is also a criterion for some importers, but it is far from being the main reason to import in most cases.

Source of revenue growth from defence-related contracts, by geographical area (Graphic 10)

Main reasons why Defence importers purchase good or services from abroad (Graphic 11)

These barriers affect firms differently depending on their level of involvement in the defence sector—shaping both their ability to scale and the pace at which new entrants can participate.

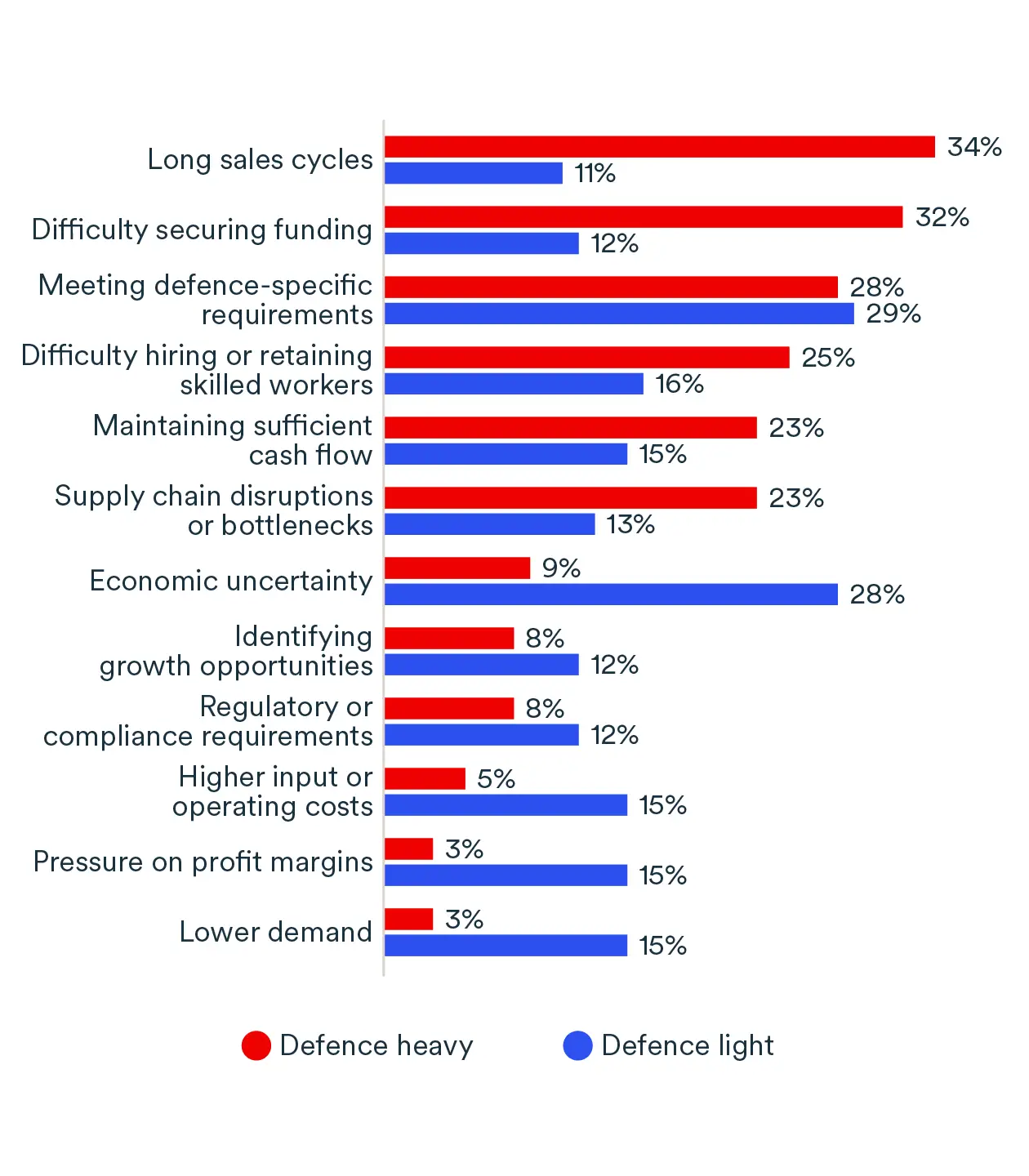

The challenges of defence SMEs vary based on their involvement level in the defence sector. For defence-heavy SMEs, long sales cycles and difficulty securing funding are the top challenges limiting growth. Meanwhile, the civilian activities of defence-light SMEs put them more at risk of overall economic uncertainty, which is less of an issue for defence-heavy SMEs.

Both types of defence SMEs face difficulties hiring workers, maintaining cash flow and managing supply chain disruptions, although these challenges seem more acute among defence-heavy SMEs. They are also both facing regulatory and compliance challenges.

Challenges can also vary based on the expertise of the SME:

- Defence SMEs specialized in ground vehicles experience more pressure on profit margins (19%) and seem to have more difficulties identifying defence-related growth opportunities (17%).

- A higher share of defence SMEs in aerospace and construction find that their growth is limited by labour shortages (29% for both).

Top factors limiting the growth of defence SMEs over the next 12 months (Graphic 12)

Defence specific requirements include cybersecurity, compliance, employee security screening, certifications, constraints linked to classified work and other specific client requirements.

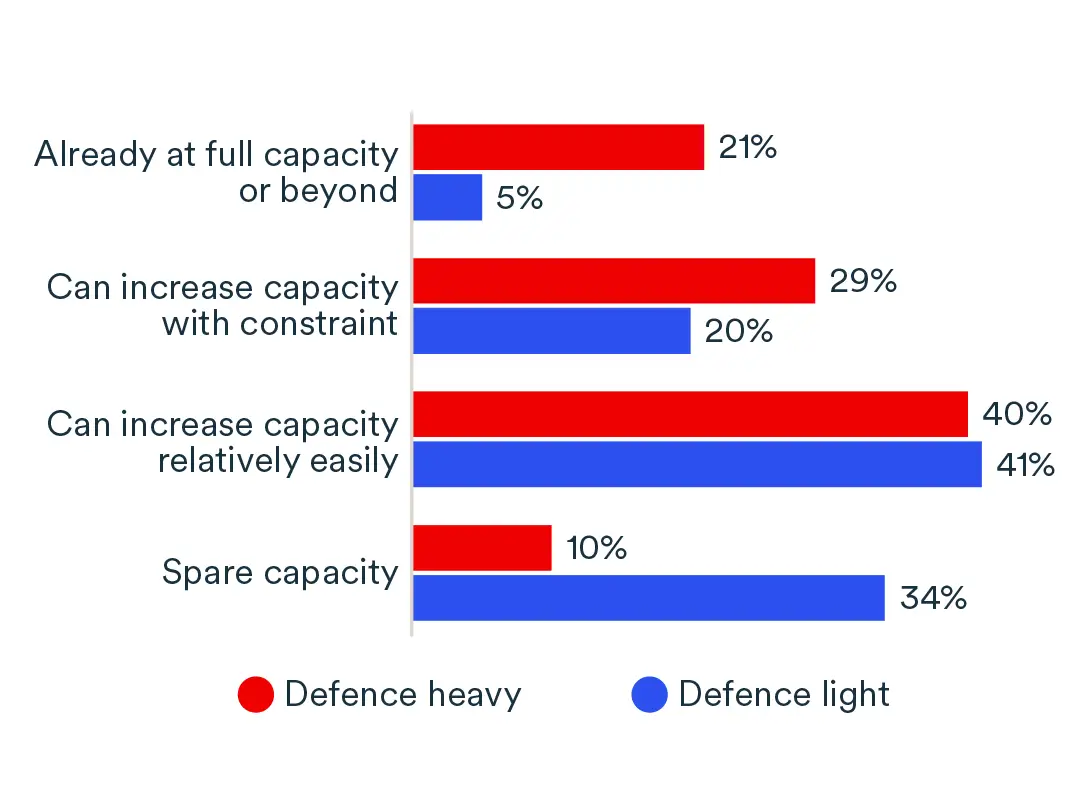

Defence SMEs expect strong growth, but many do not have the current capacity to increase production.

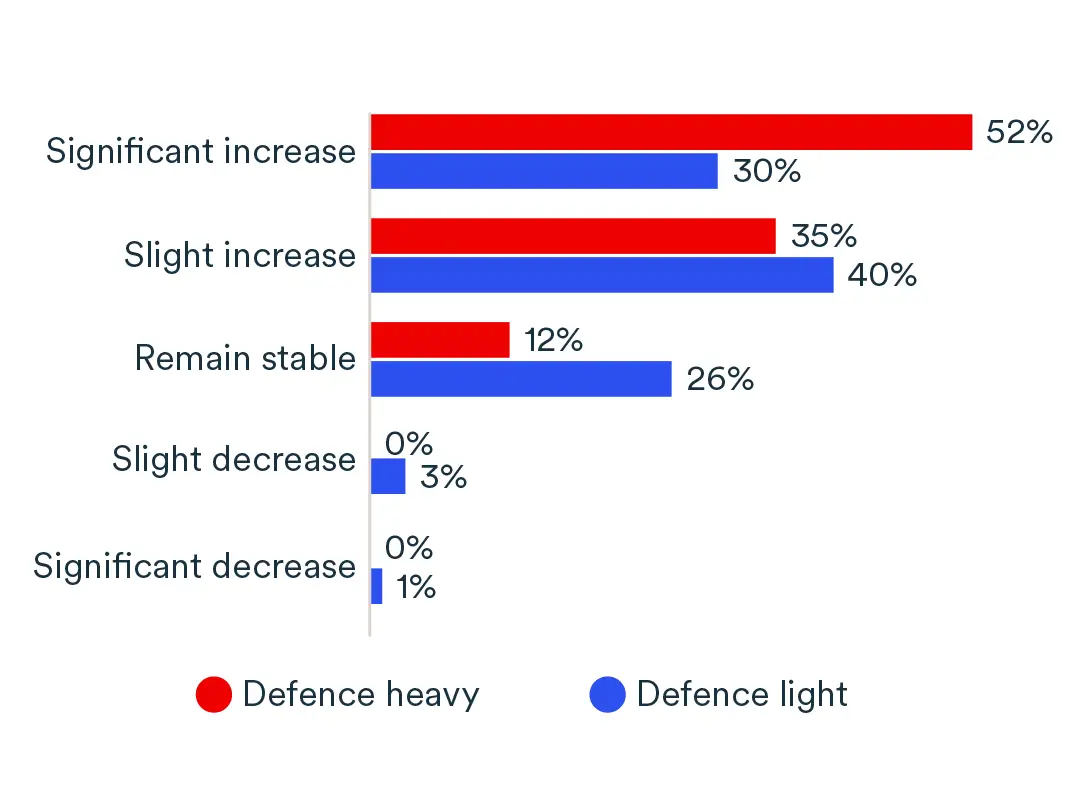

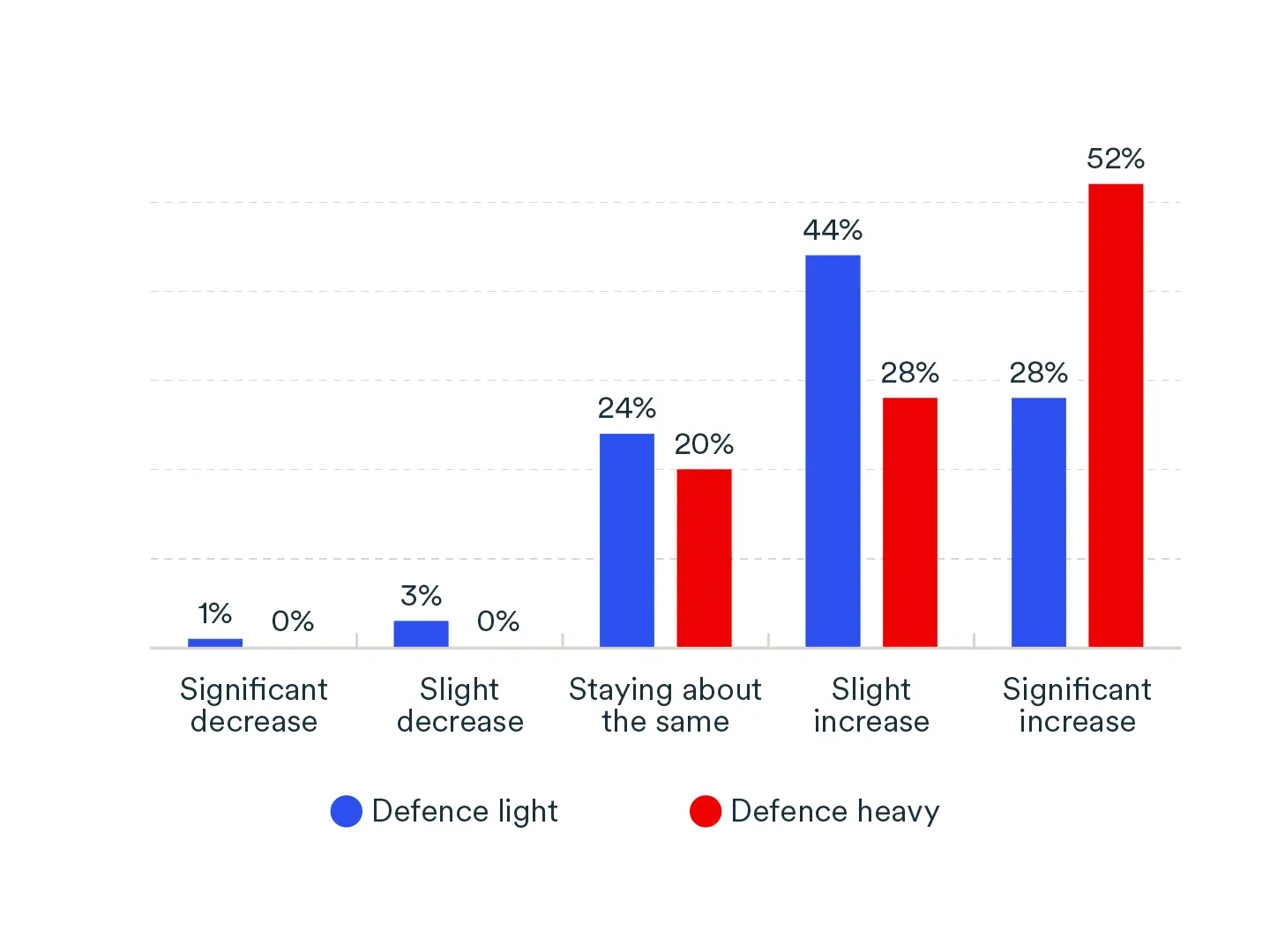

Defence-heavy SMEs have very limited spare capacity, as 21% are already producing at full capacity. They are also facing stronger labour shortages, with 30% having significant difficulty recruiting qualified workers. In that context, a majority are planning to significantly increase their level of investment in the next 12 months (Graphic 14). Not one defence-heavy respondent indicated that they were planning to reduce their level of investment.

However, Defence-light SMEs have more available capacity, as the market for some civilian goods and services has slowed down recently. They also face some labour shortage but not as much overall (16% with significant difficulties to hire). Defence-light SMEs are therefore planning to increase their investment at a slower pace, but the investment spending from these businesses is likely to be more targeted around their defence divisions.

Current operational capacity to respond to an increase in demand (Graphic 13)

Level of business investments for the next 12 months compared to the previous 12 months (Graphic 14)

As demand for real-time data accelerates, a new kind of infrastructure is emerging—not on the ground, but in orbit.

Toronto-based Kepler Communications is building a network of satellites designed to move data between space-based systems in real time. The company’s goal is ambitious: to create the “Internet in space,” enabling satellites, spacecraft and sensors to communicate instantly rather than waiting to transmit data back to Earth.

That capability has implications far beyond commercial connectivity. It is also becoming increasingly important for national security—positioning companies like Kepler at the intersection of innovation, defence and Canadian sovereignty.

“We’re building the infrastructure that allows people to access and use data from space in real time,” says Mina Mitry, co-founder and CEO of Kepler. “Whether you’re tracking wildfires or monitoring national security threats, you need that data immediately—not hours later.”

The largest orbital computing cluster in space

Building a satellite company requires more than technical ingenuity—it demands patient capital that is willing to weather long development timelines and significant upfront investment in hardware and infrastructure. That's where BDC Capital came in.

BDC Capital invested in Kepler as it moved from early development toward large-scale deployment—first in 2016 with a seed investment and again in 2021 when the Industrial Innovation Venture Fund supported Kepler’s Series B round. It has since done multiple follow-on investments. Kepler has raised over $300 million to date.

BDC continues to invest as the company expands its satellite network and pursues increasingly complex projects. But the relationship has always extended beyond financing. Mitry meets regularly with his BDC advisor to work through business challenges, describing the meetings as genuinely open exchanges.

"It’s really valuable for us to have a trusted advisor at BDC that we can talk to openly," he says. "We meet regularly, discuss challenges and work through decisions in a way that's constructive and supportive."

Thanks in part to support from BDC, Kepler has achieved several global firsts: it was the first in the world to establish a laser link between a satellite travelling at 7.5 kilometres per second and a commercial aircraft, built the largest orbital computing cluster in space, and became the first Canadian company ever to serve as prime contractor for a European Space Agency program.

Meanwhile, its growth has remained anchored in Canada despite early pressure from mentors and investors to move south.

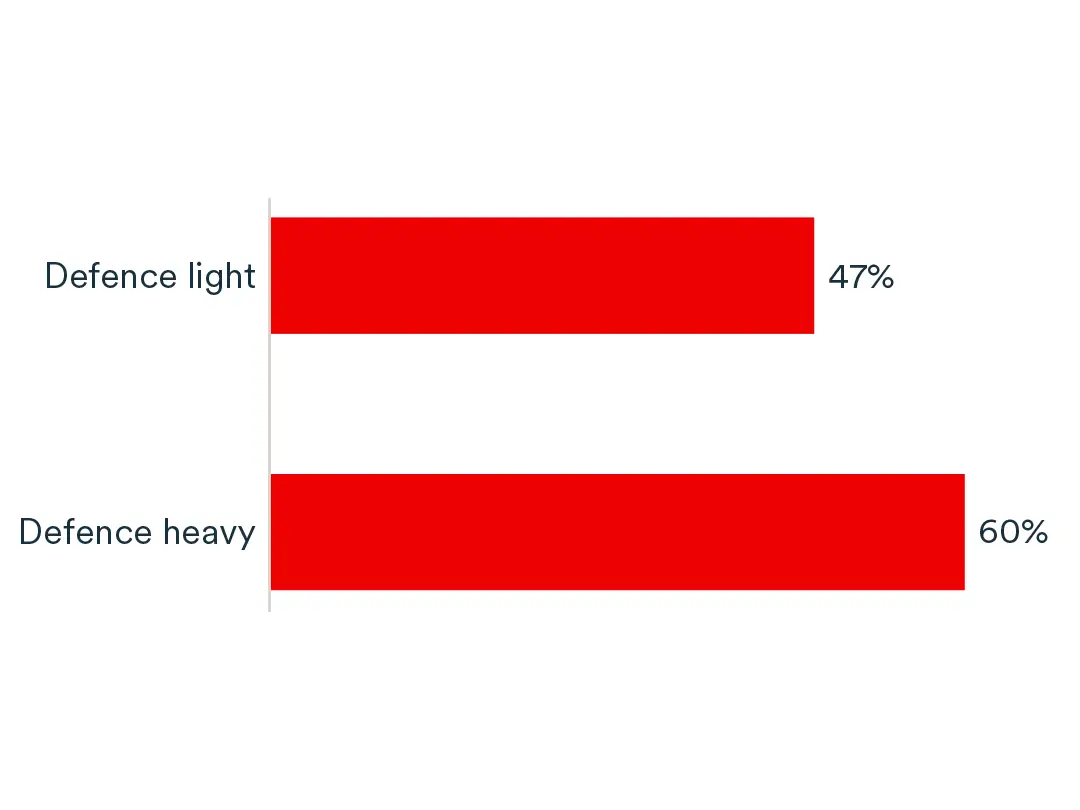

Overall, half of surveyed defence SMEs are planning to request financing over the next twelve months, with demand for financing a bit lower among defence-light SMEs (47%) than defence-heavy ones (60%). This indicates that the demand for financing is likely higher among defence SMEs than among SMEs on average (36% planning to request financing, according to the May 2026 BDC Investment and Financing Outlook Survey).

Defence SMEs plan to use financing mainly to support their growth (47%), develop new products or services, meet their working capital needs and prepare projects (all at 31%). About a quarter plan to use it to buy machines or invest in digital technologies, such as AI.

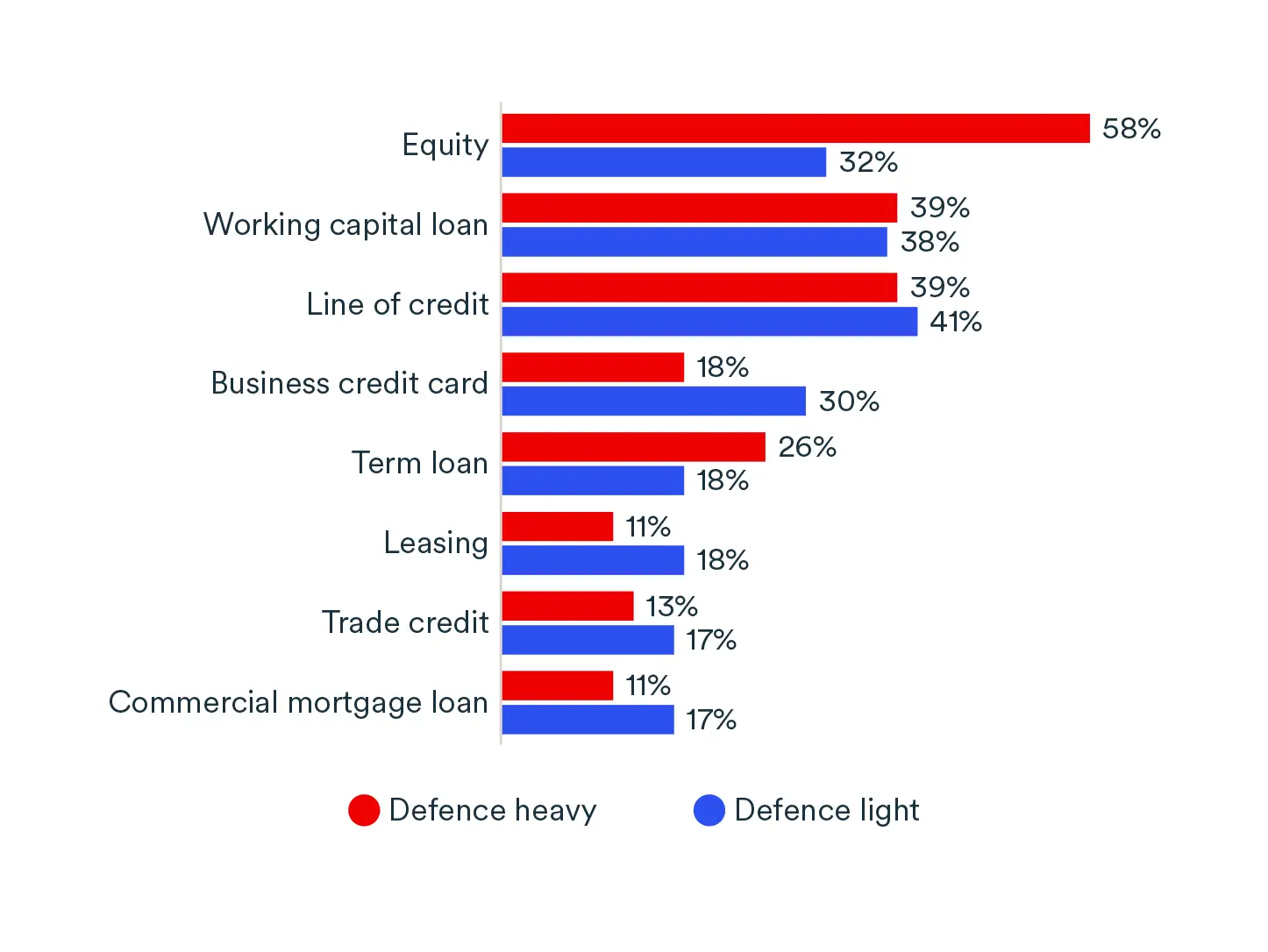

They are also looking for large amounts, especially defence-heavy SMEs, with 74% looking for $1 million or more and 39% looking for $5M or more.

Since defence-heavy SMEs are more growth oriented, they are also looking for equity as a priority, while defence-light SMEs are more in the market for lines of credit and working capital loans to manage their cash flow in an uncertain environment.

Share of SMEs intending to ask for financing over the next 12 months (Graphic 15)

Type of funding that SMEs will request (Graphic 16)

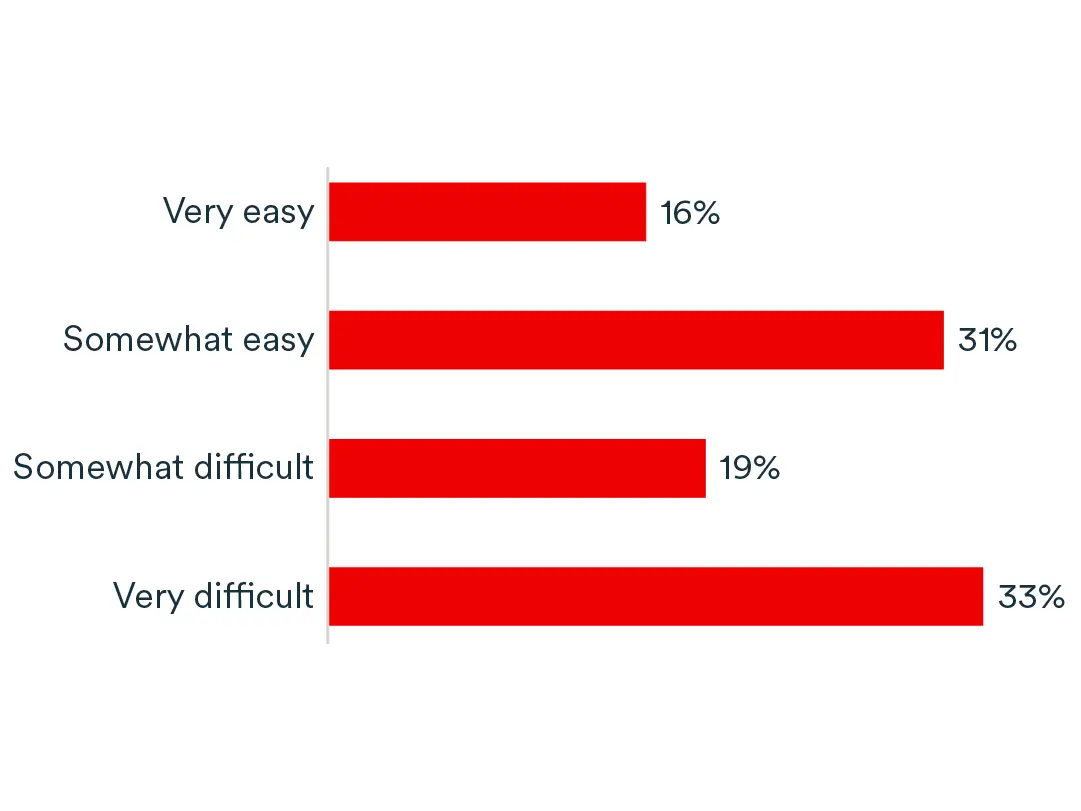

Both defence-heavy and defence-light SMEs seem to have difficulty accessing financing. Half of defence SMEs looking for financing think that it will be difficult, including one in three expecting that it will be very difficult.

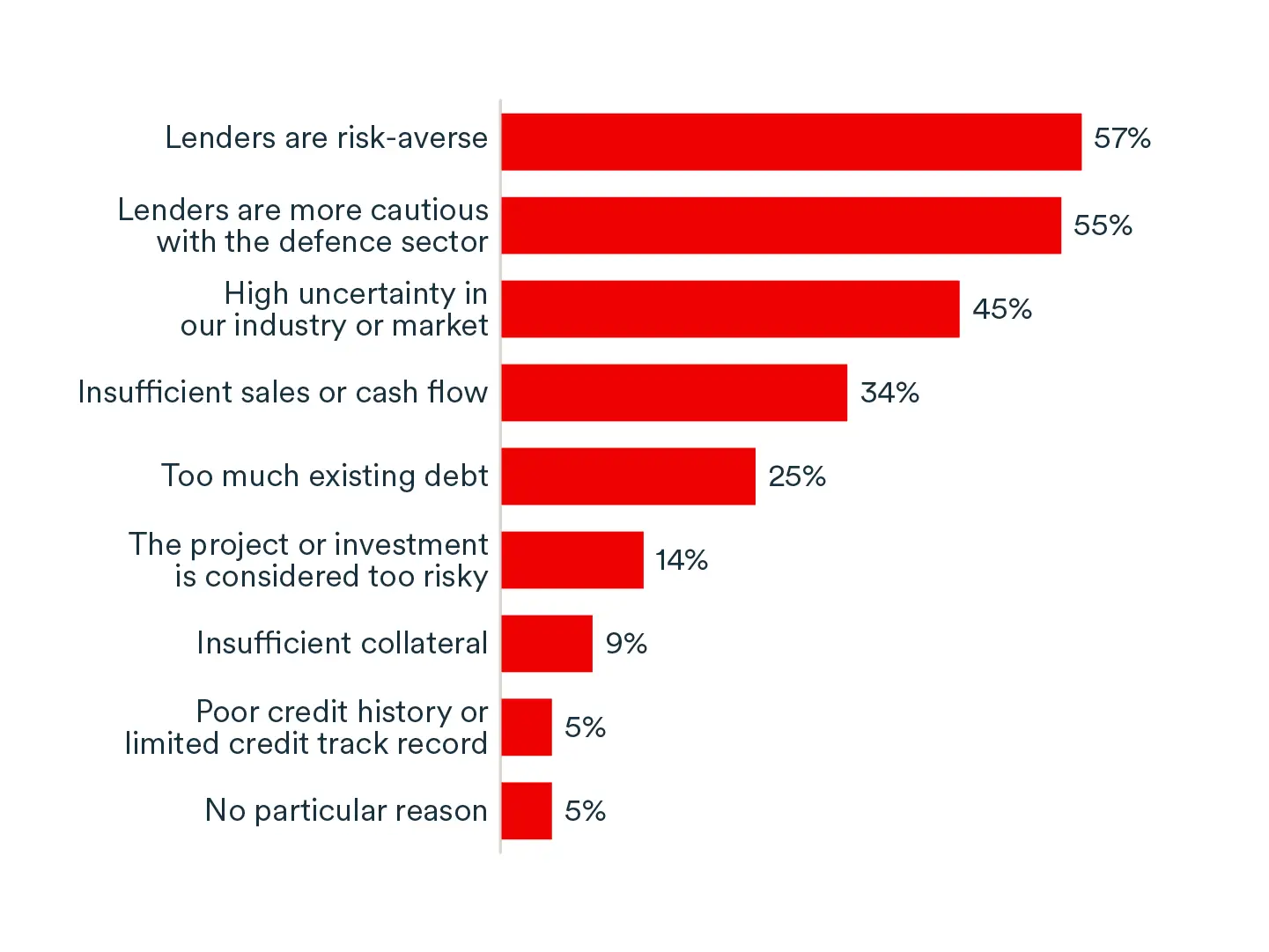

Defence SMEs find it challenging to secure financing, as financial institutions are cautious about the defence sector due to its risk profile, limited customer base and unstable cash flow. Lenders also face potential legal and reputational concerns, prompting many to avoid defence-related loans altogether. Traditional issues like insufficient guarantees or a weak credit history are rarely cited as the main obstacles.

Considering the current growth outlook and the difficulty in accessing financing, only a quarter of defence-heavy SMEs think that their current financial institutions totally meet their needs.

Expected difficulty in obtaining financing (Graphic 17)

Reasons for difficulties in obtaining financing (Graphic 18)

Besides defence-SMEs, BDC also surveyed non-defence SMEs interested in joining the sector.

Most of the respondents interested in the defence sector come from four main industries:

- IT

- Manufacturing

- Construction

- Professional services

However, some respondents were also from other sectors such as retail or healthcare.

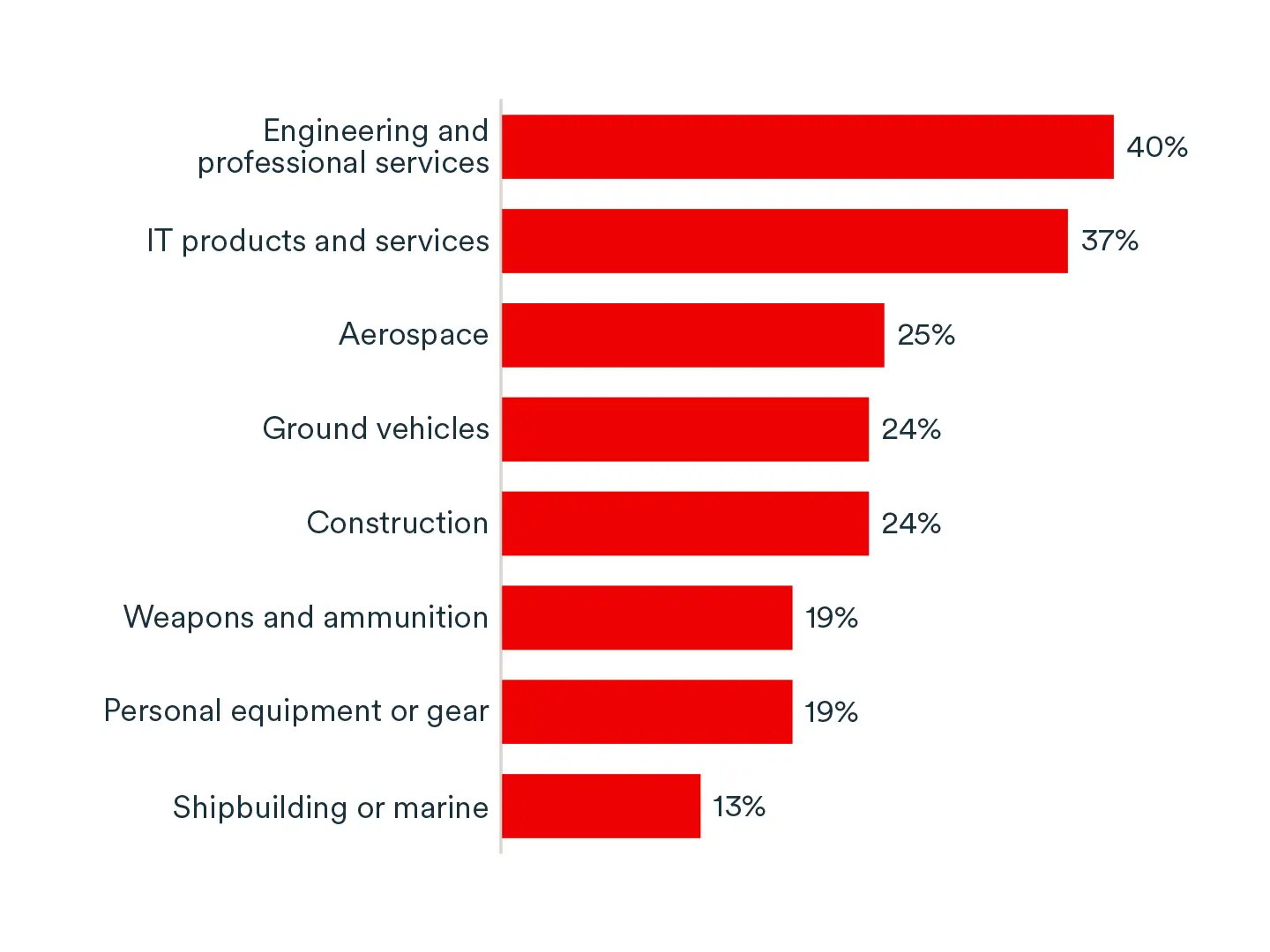

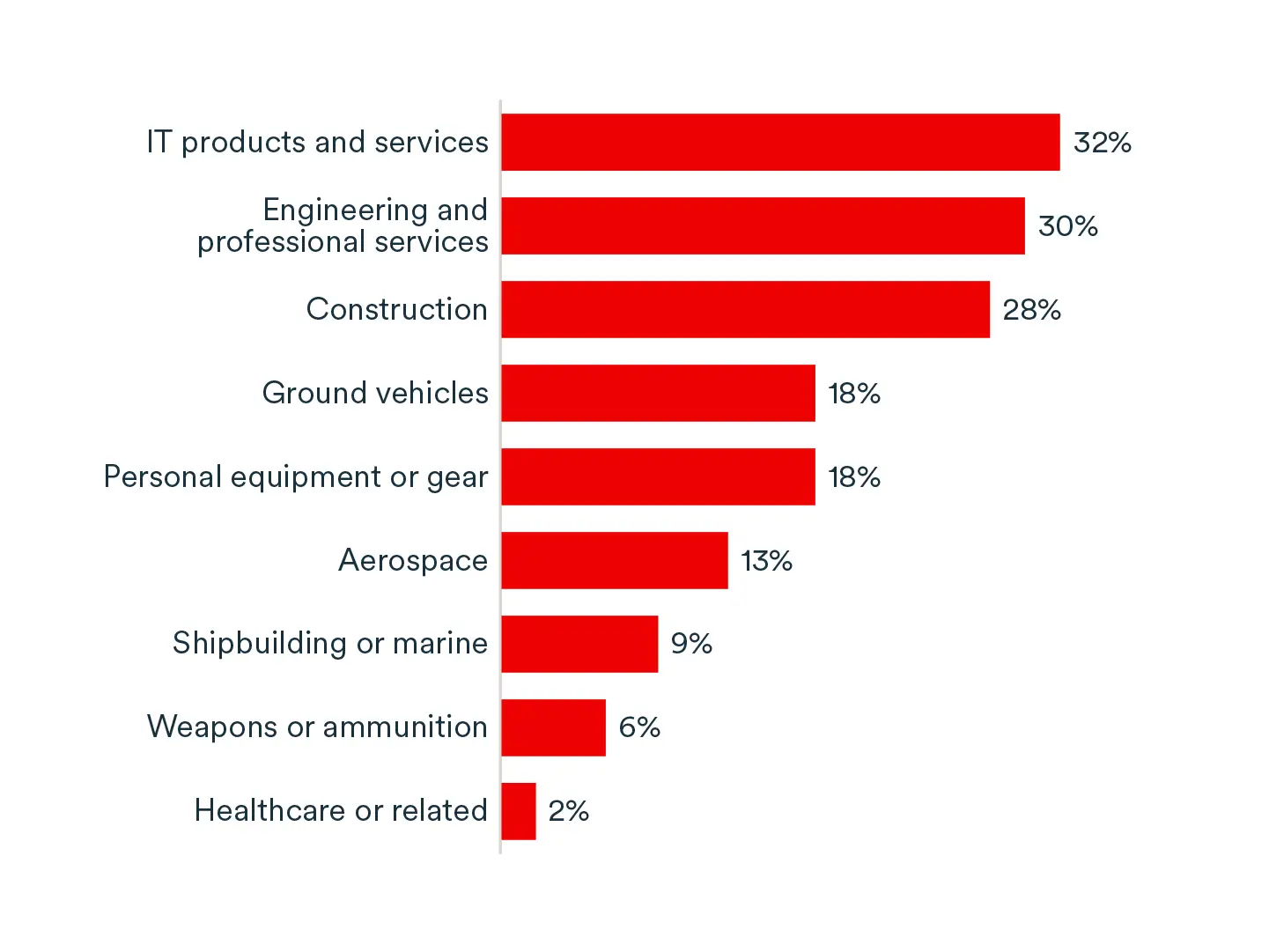

These businesses have a wide range of capabilities: IT products, engineering services, construction, but also ground vehicles, personal equipment, aerospace and shipbuilding. Some even have capabilities in weapons and ammunition.

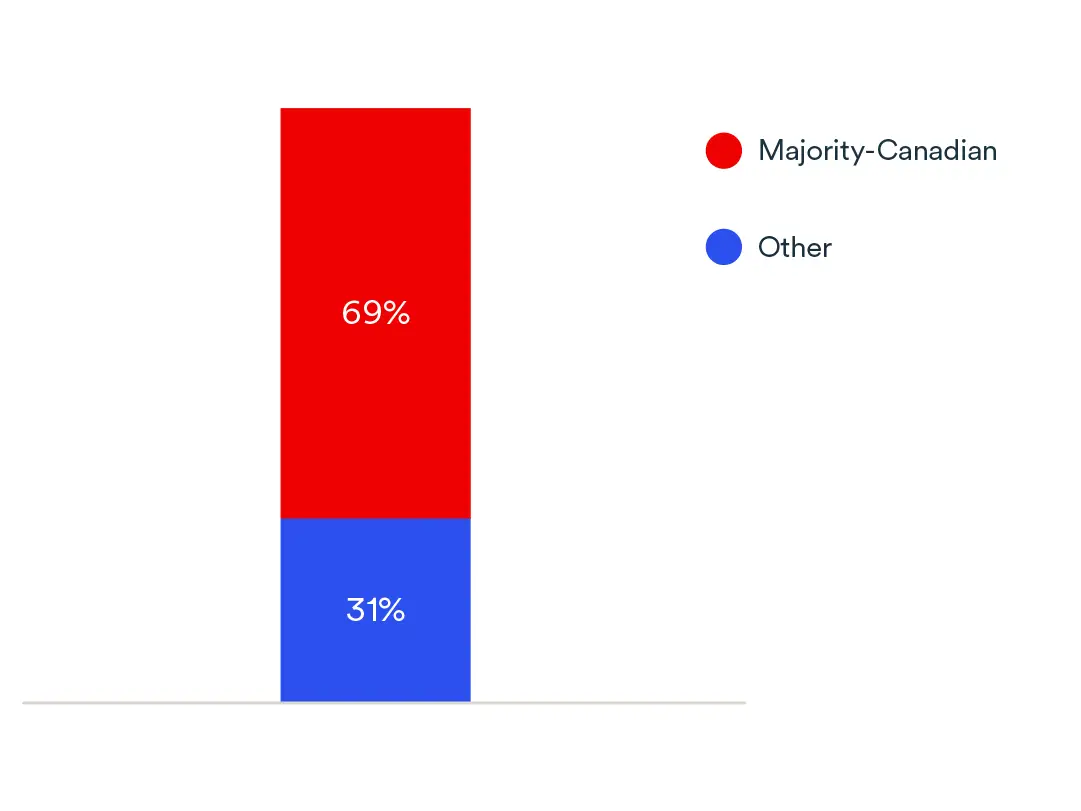

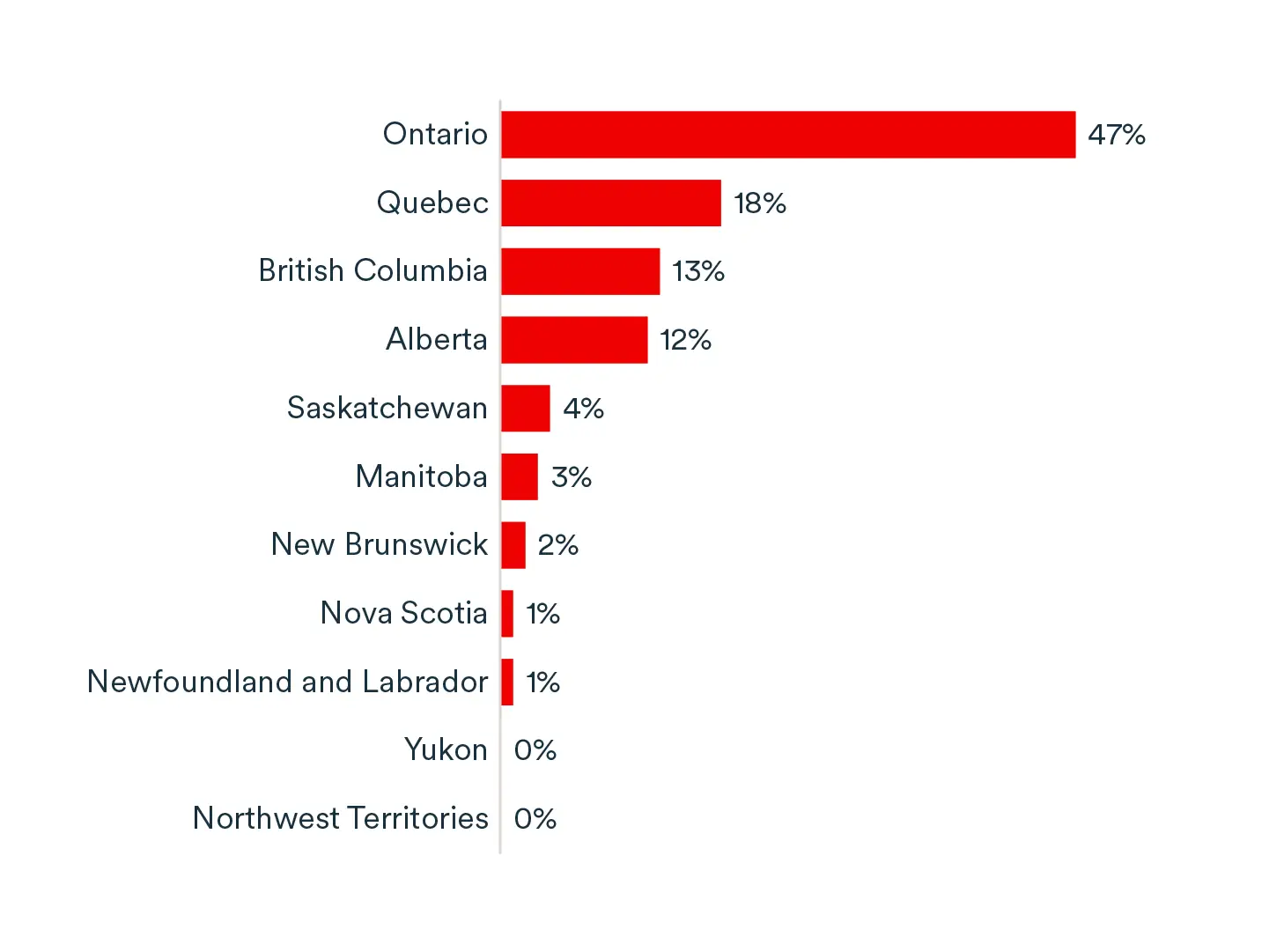

Most of the respondents were Canadian-owned SMEs, with a strong representation in Ontario (47%). Larger businesses are over-represented, with 21% of respondents having 100 employees or more. However, many smaller businesses are also interested (53% have less than 20 employees).

Key characteristics of survey respondents interested by the defence sector

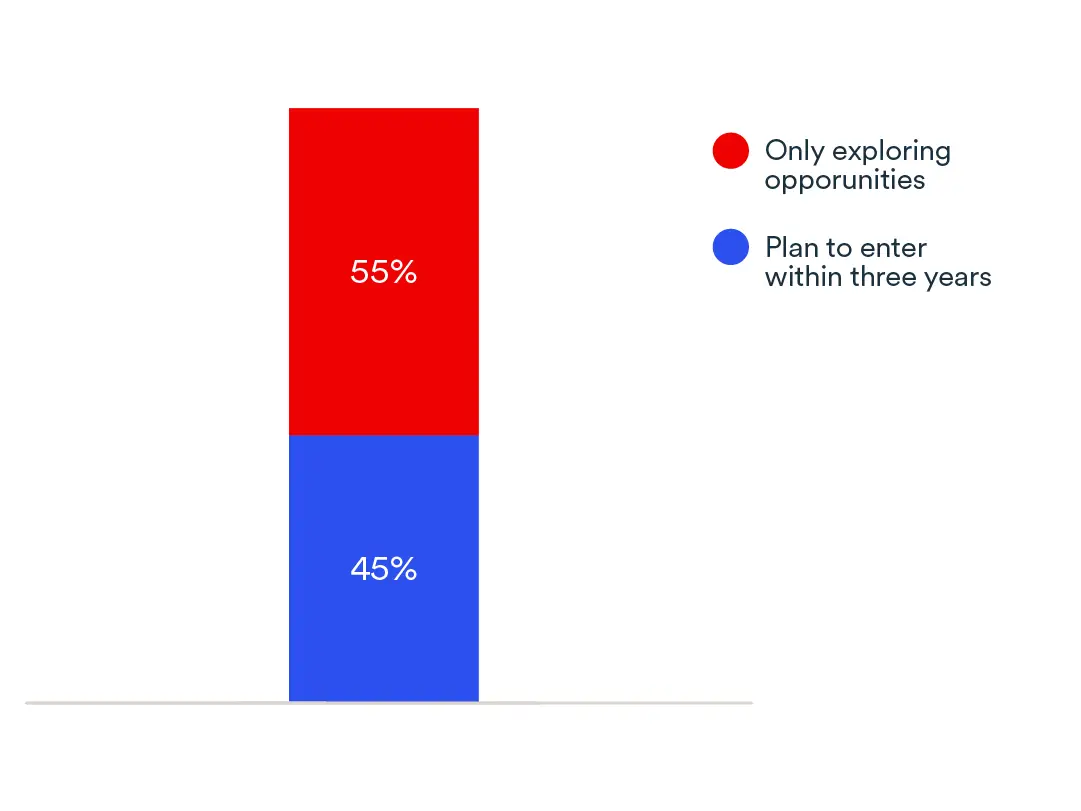

Distribution of interested SMEs by level of preparation to enter the defence sector (Graphic 19)

Distribution of interested SMEs by ownership (Graphic 20)

Distribution of interested SMEs by area of capabilities (Multiple choice) (Graphic 21)

Province or territory where most activity of interested SMEs take place (Graphic 22)

Respondents by number of employees (Graphic 23)

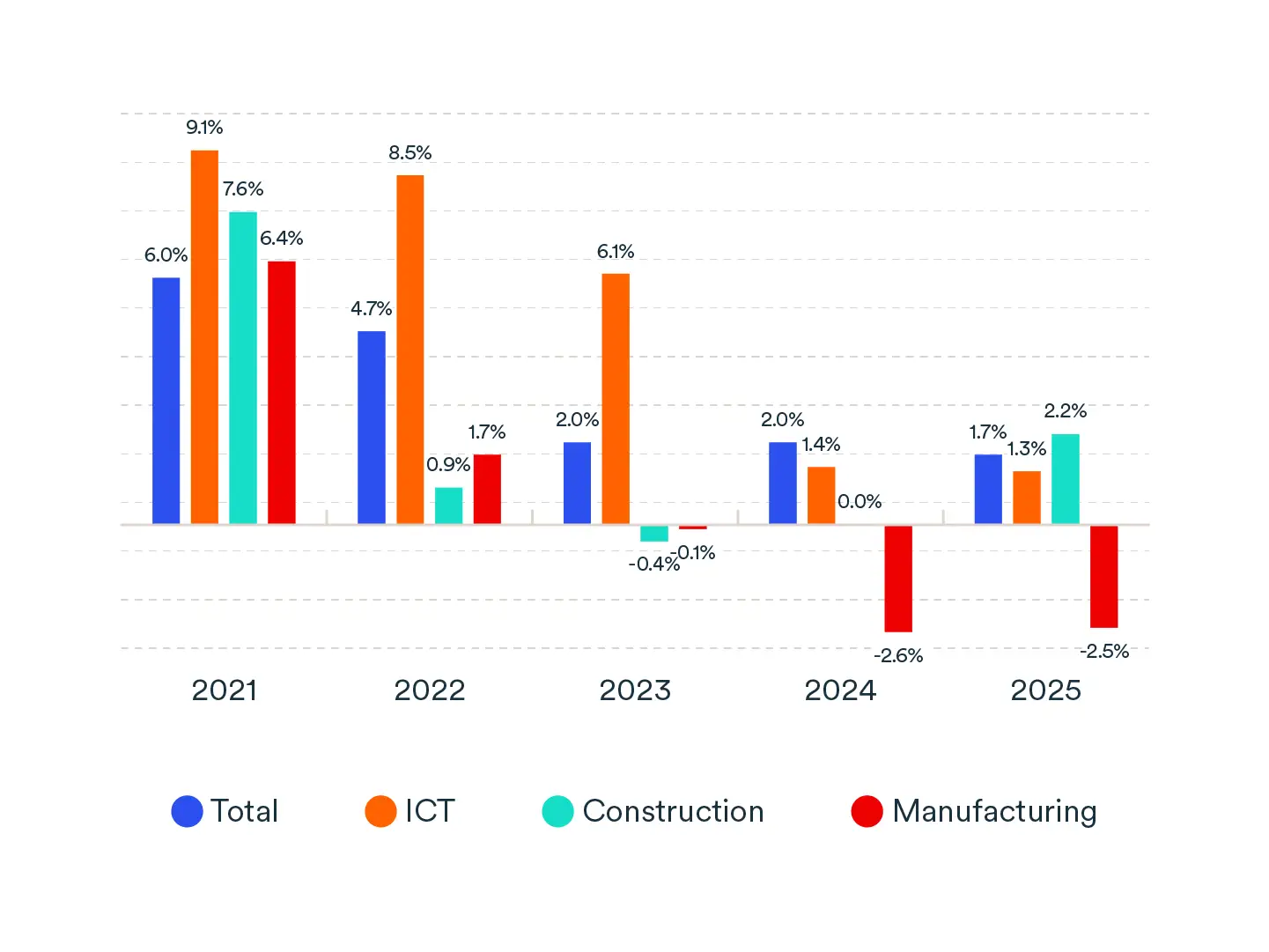

The information and communication technology sector (ICT) and the manufacturing sector, two sectors with many SMEs interested by the defence sector, have both experienced below-average growth over the past two years. Canada’s manufacturing sector has experienced three consecutive years of recession, and the ICT sector has been growing at a significantly slower pace than in the past. The survey shows that sales outlook for defence contracts among defence SMEs is higher than for civilian contracts among interested SMEs.

Economic uncertainty is a major issue for many businesses interested in the defence sector. Many businesses exploring the sector also have problems with a low demand for their goods and services (Graphic 25), which could partly explain their interest in the defence sector.

However, not all interested SMEs are facing headwinds. Many produce niche products or services in high demand in both civilian and military applications.

Real annual GDP growth (Graphic 24)

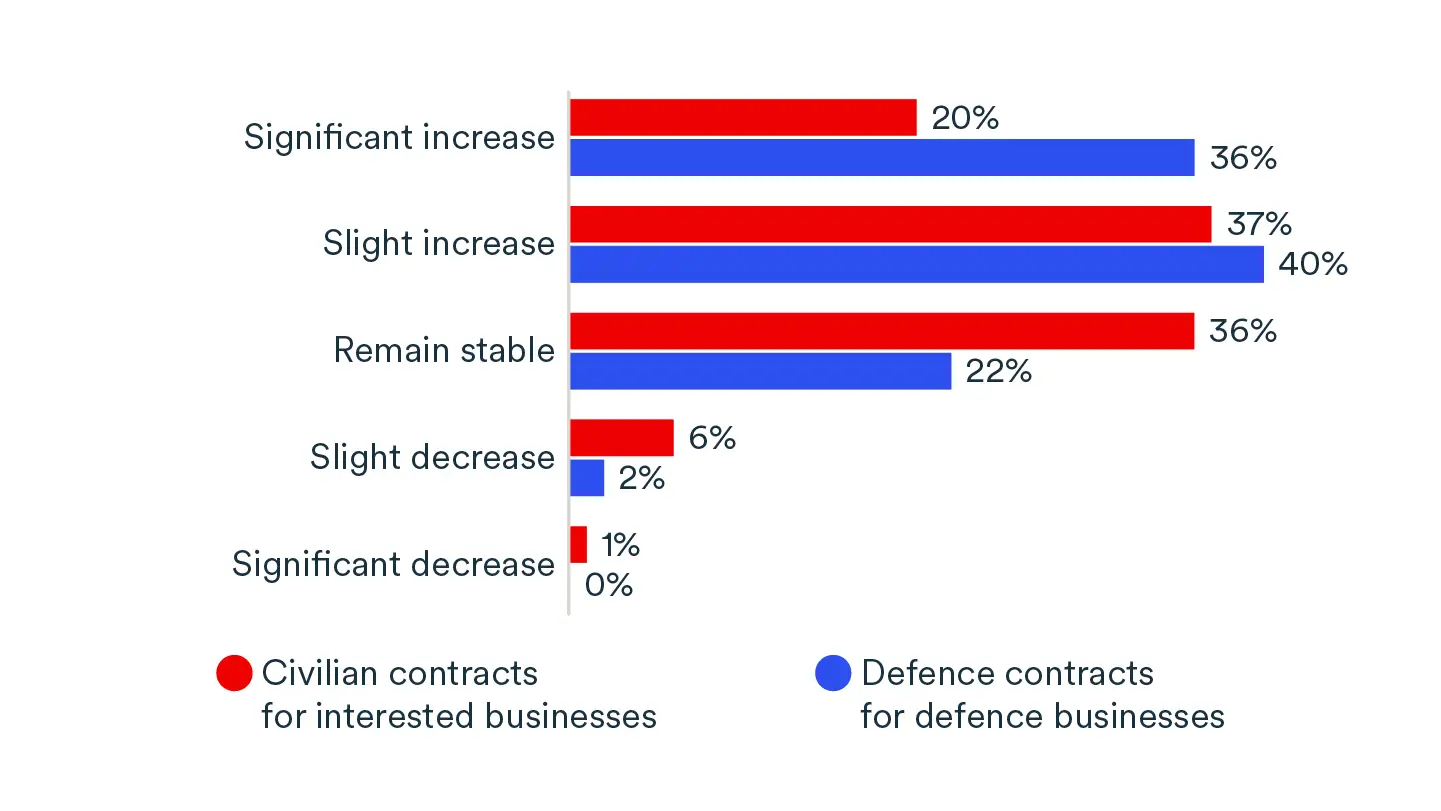

Growth outlook for defence and interested businesses (Graphic 25)

Despite economic headwinds, defence-interested SMEs remain mostly growth oriented, but less so than defence-heavy businesses (55% vs. 75%).

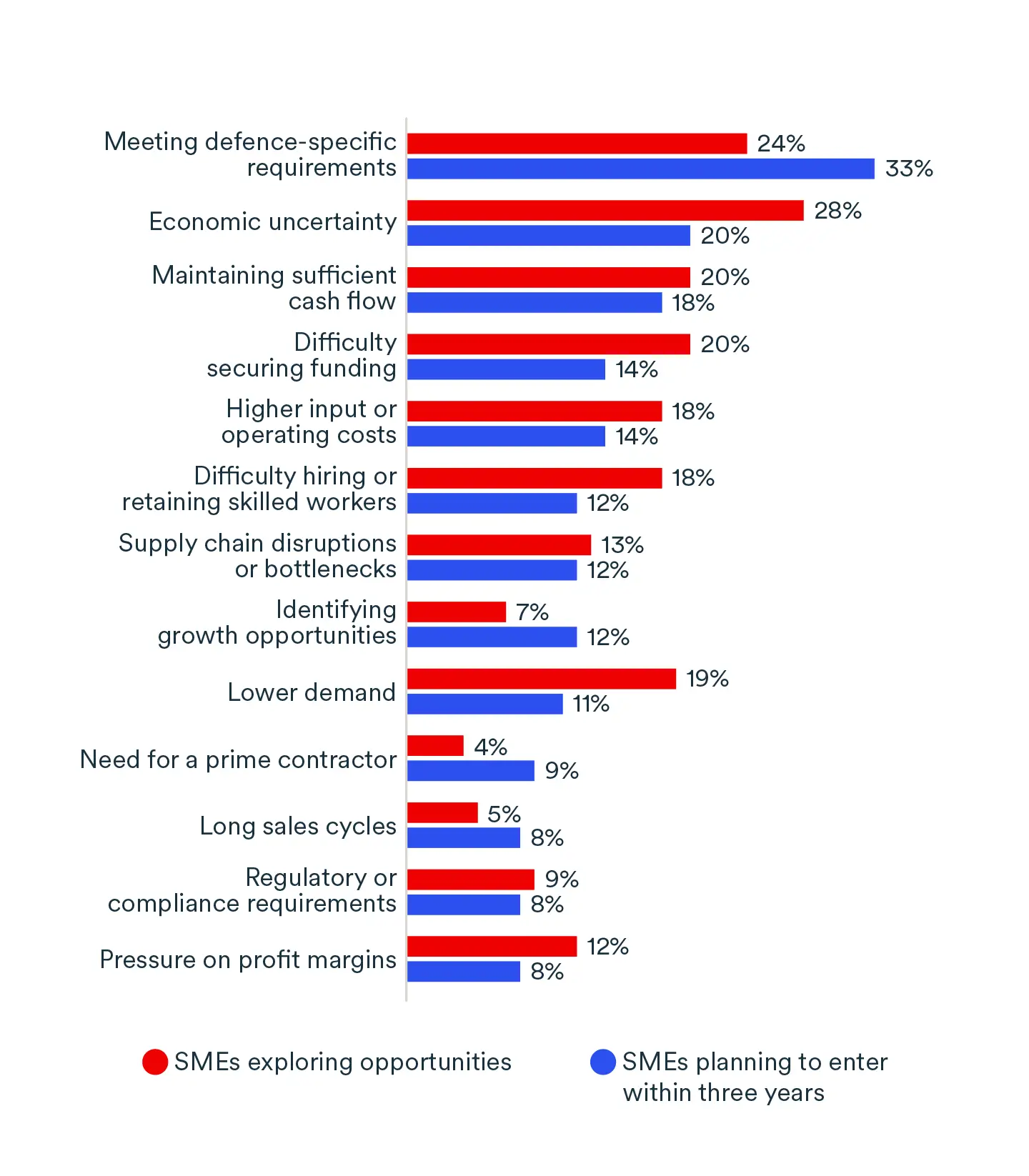

Meeting defence-specific requirements is the number one obstacle limiting growth for those planning to enter in the next three years. While those in the exploration phase are more impacted by overall economic uncertainty. However, businesses in exploration mode will likely face difficulties with requirements if they choose to move forward with defence opportunities.

Interested SMEs also face issues maintaining enough cash flow and securing the funding they need to grow.

To navigate these challenges, 38% of interested SMEs are planning to hire external consultants over the next 12 months, mostly to prepare for defence opportunities.

Top priorities for SMEs interested in the defence sector (Graphic 26)

Top factors limiting growth over the next 12 months, based on level of preparation to enter the defence sector (Graphic 27)

Defence specific requirements include cybersecurity, compliance, employee security screening, certifications, constraints linked to classified work and other specific client requirements.

Entering the defence sector requires careful preparation. It is a highly regulated sector with strict requirements in three key areas in particular:

- Security clearances

- Cybersecurity

- Quality control

Businesses may need to register under the Controlled Goods Program, implement robust cybersecurity frameworks such as ISO 27001 or meet evolving certification standards, and comply with quality systems like ISO 9001 or AS9100.

Before pursuing opportunities, companies should assess their capabilities and align their operations with industry expectations. Building strong foundations in operational efficiency, security and quality management is essential, and often costly.

Business development in defence relies heavily on reputation and relationships rather than cold outreach. Companies can gain traction through specialized expertise, initial contracts or by participating in industry events where major contractors seek suppliers.

While the barriers to entry are high, so are the opportunities. With the right strategy, systems and certifications in place, Canadian businesses can position themselves to benefit from long-term growth in the sector.

An online survey was conducted between March 24th and April 12, 2026, among 642 business owners and business decision makers active in the defence sector or with the intent or interest to join it in the coming years. Three different panels were used:

- BDC Viewpoint Proprietary with a sample from business owners and business decision-makers from BDC’s Viewpoint online survey panel

- BDC Viewpoint Proprietary with a sample from business owners and business decision-makers from the Icebreaker’s readership and parent organizations.

- Forum Research with a sample from business owners and business decision-makers from Forum Research’s online survey panel

Data processing and analysis were performed by the BDC Research and Market Intelligence team. The data has not been weighted.

For a probabilistic sample of 642 respondents, the maximum margin of error is ± 3.9% percentage points 19 times out of 20. However, as this survey is based on a non-probabilistic sample, the information above is provided for reference only.

Acknowledgements

This report was written under the direction of Arnaud Franco, director, Economic Research, BDC. It was made possible through the collaboration of Marco Santo Pires, Catherine Schwartz, Craig Segal, Samuel St-Pierre Thériault and Sophia Samilski from BDC, as well as Matthew Lombardi from The Icebreaker.

It is based on survey data and public information that was analyzed and interpreted by BDC. Any error or omission is the sole responsibility of BDC. All figures in this report have been rounded. Use of the information herein is exclusively the reader’s responsibility.