Monthly Economic Letter

Where are interest rates headed?

In its last two rate announcements, the Bank of Canada opted to maintain the status quo, keeping its key rate at 5.0% since July 12. Now that the U.S. Federal Reserve has also hit pause on its rate hikes, many are wondering if we could actually be done with tightening for this cycle. Could we even expect the Canadian central bank to lower rates soon?

Is the Bank of Canada done with rate hikes?

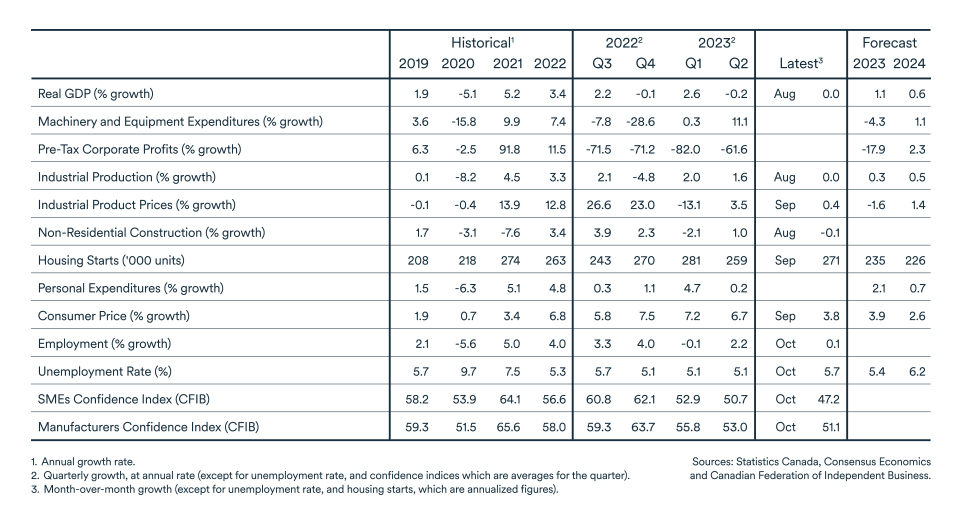

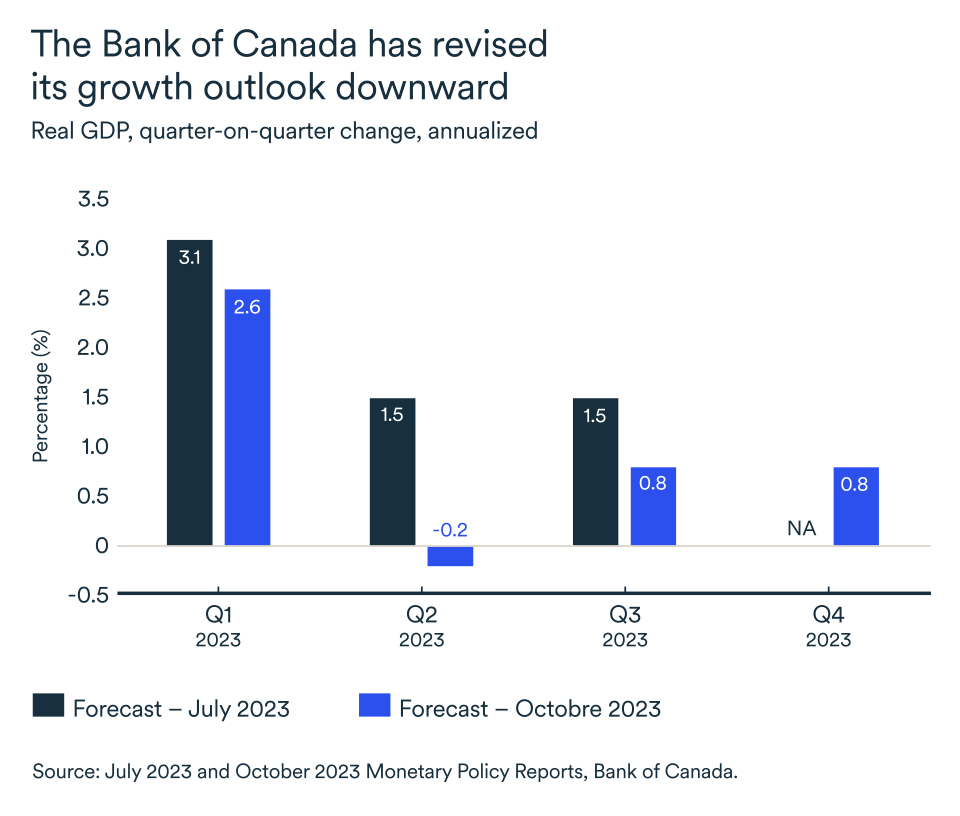

According to the Bank of Canada, the economy is set to slow much more than it had anticipated just three months ago. In July, the central bank was forecasting economic growth of 1.8% in 2023 and 1.2% in 2024. By October, the bank’s outlook had been updated to 1.2% and 0.9%.

Despite the downward growth revisions, Governor Tiff Macklem reiterates at every rate announcement that the bank is ready to proceed with further hikes if necessary. The Bank of Canada's mandate is price stability, not economic growth, and it remains focused on seeing inflation come down to its 2% target.

Although risks remain, inflationary pressures appear to be easing

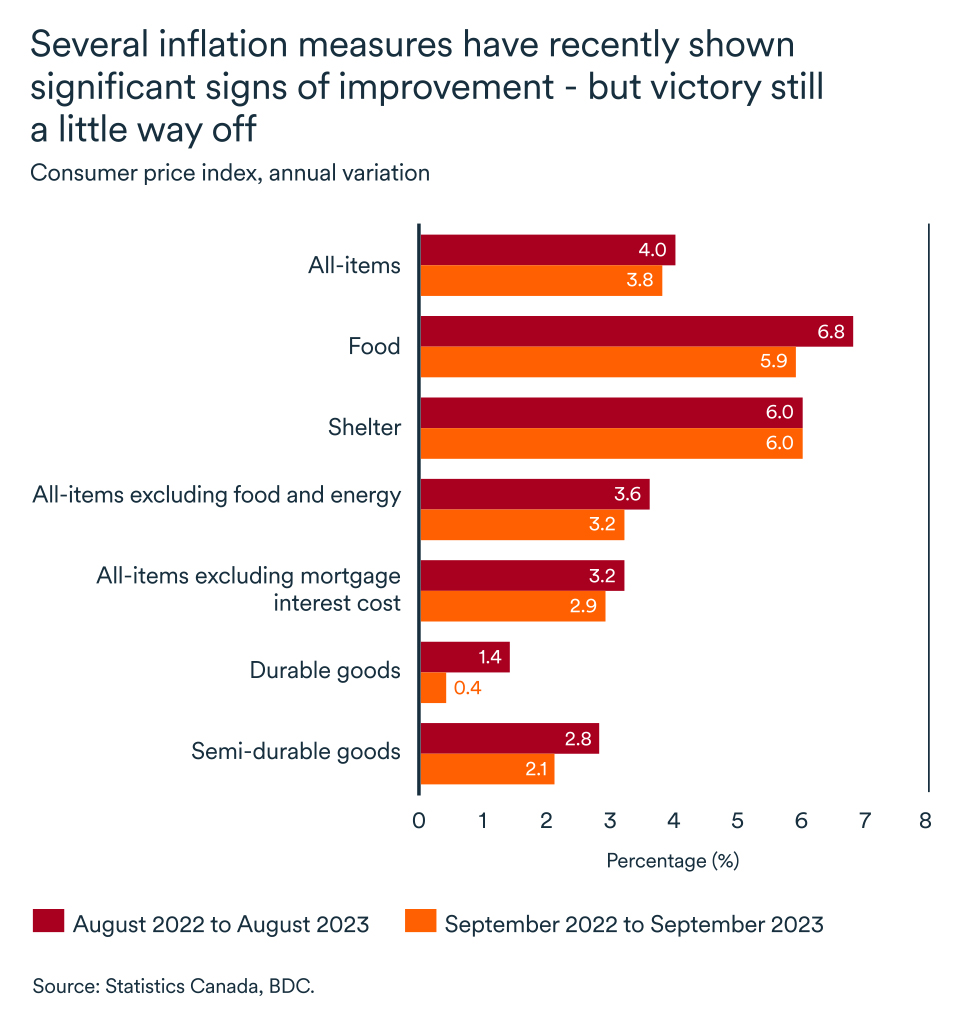

While economy was slow to react in the early stages of the tightening cycle, the inflation picture turned more positive in September.

The consumer price index edged down to 3.8% in September from 4% in August. While this was still above the Bank of Canada’s target range of 1-3%, monetary policy seemed to be working. Price increases for interest-rate sensitive items, such as debt-financed and discretionary goods, had returned to the target range.

While growth remains solid in the U.S., it’s stagnating in Canada. The differential between U.S. and Canadian rates could widen further if the Federal Reserve decides to hike again. Another increase could have a negative impact on Canada's fight against inflation because the Canadian dollar would be further devalued against the U.S. greenback, making Canadian imports more expensive.

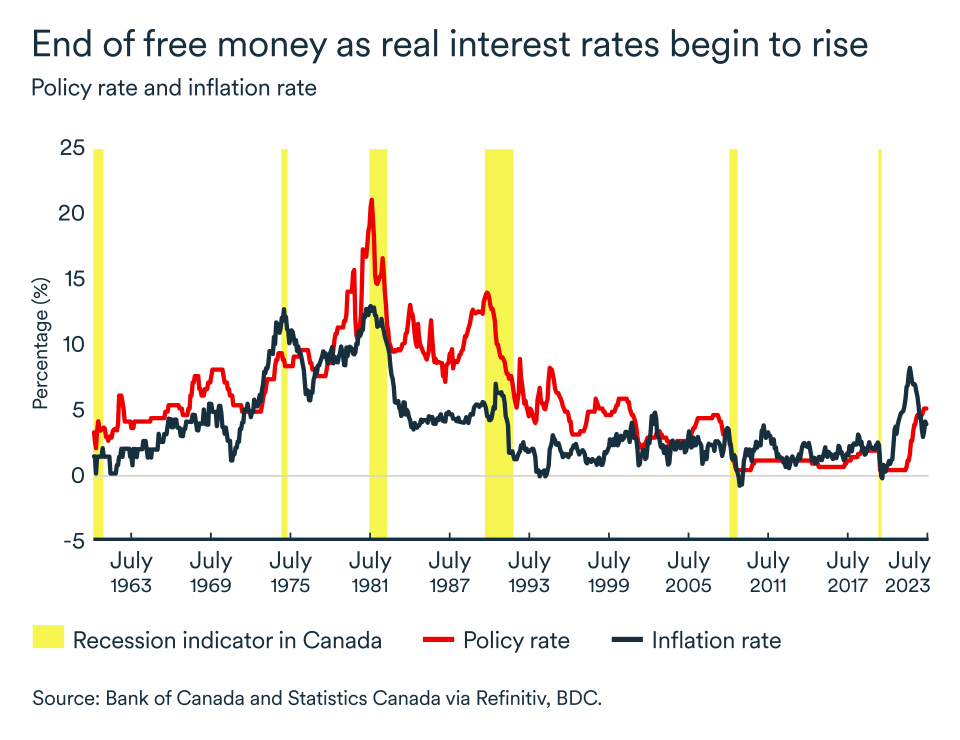

High inflation and high interest rates, the two go hand in hand

The direction of interest rates depends on the fight against inflation. Even if current high interest rates are a source of frustration and concern for many households and businesses, a policy rate of 5.0% is necessary to restore the balance between supply and demand and achieving long-term price stability.

Tighter credit conditions and the reallocation of household budgets toward debt repayment (mainly mortgage debt) will continue to slow demand in the economy. As a result, inflation should continue to fall over the coming months, but significant gains will be increasingly difficult to achieve.

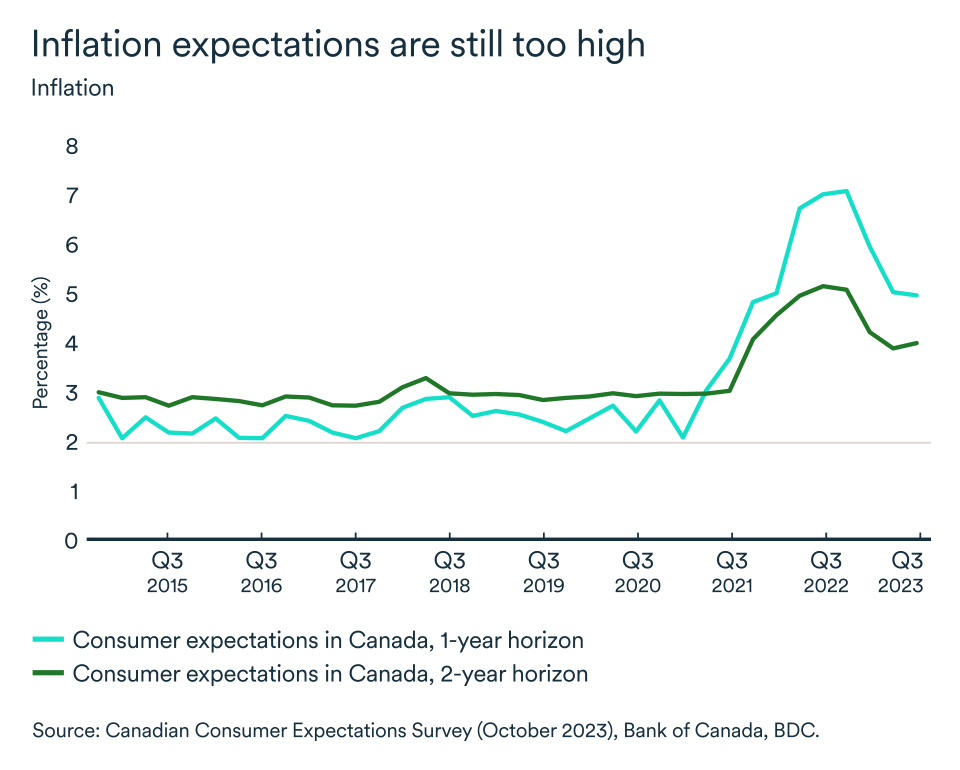

Consumer inflation expectations for the coming year are still high at 5.0%. Inflation is a highly self-fulfilling mechanism—the more consumers believe prices will rise, the more they act on that belief by, for example, demanding higher wages.

The Bank of Canada expects inflation to return to 2% by 2025. Does this mean we'll have to wait until then to see our first rate cut? Not necessarily.

Say goodbye to interest rates below 2%

Although the Bank of Canada has given no indication of when or how quickly it will cut rates, at BDC, we believe rates could start to come down as early as the summer of 2024. By then, the economy will have slowed sufficiently for pressure on production capacity to have eased domestically.

However, to reach the inflation target, interest rates will have to remain higher than we had grown accustomed to during the past decade. This is because our economy is subject to multiple constraints that will persist, including an aging population, the reorganization of supply chains following the pandemic, and rising uncertainty and geopolitical risks.

So, we shouldn't expect to see a return to the interest rate that had prevailed since the financial crisis and recession of 2007-2008, when the real rates were negative. (The real interest rate is the nominal rate adjusted to eliminate the effects of inflation, so when the policy rate is lower than the inflation rate, the real interest rate is negative).

Instead, we are likely to see a more gradual reduction in interest rates once inflation has been brought under control. Barring a major, unpredictable shock, the Bank of Canada’s key rate should be on a downward trend by mid-2024, closing the year at around 3.5%.

Ultimately, we expect the bank to bring the policy rate back close to 2.5%—considered the neutral rate—but this is not likely to happen before 2025.

Here are a few tools to help you navigate high interest rates

- Calculate your company's debt-to-equity ratio, as well as other important ratios that banks take into account when evaluating loan applications.

- The commercial loan calculator is also useful for determining the interest associated with your loan.

The bottom line

- Inflation is on a downward trend, but several factors, including the persistently high expectations of consumers, will make further gains increasingly difficult.

- We expect the Bank of Canada’s key rate to remain at 5.0% for the rest of 2023 and the first half of 2024, with a first downward revision in the summer of next year.

- The bank will not bring its key interest rate close to 2.5%, the neutral rate, until 2025. Therefore, rates will remain higher than those to which Canadians have grown accustomed to over the past 15 years.

- We will have to keep a close eye on wage growth, which could prove to be a major factor in keeping inflation stubbornly high and lead to more rate hikes in Canada.

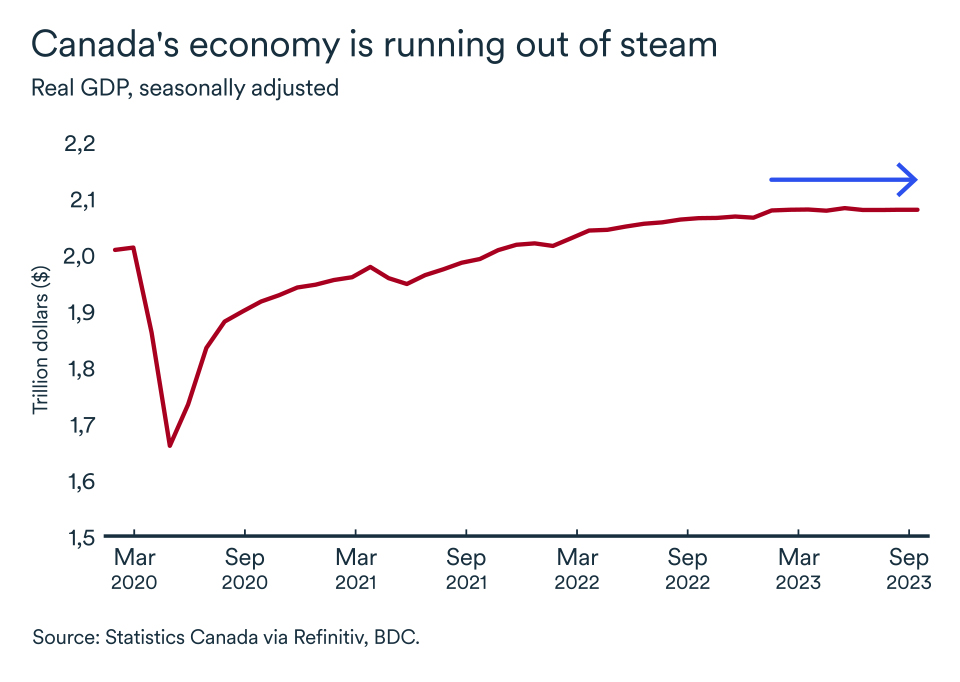

The Canadian economy is stalled

Amid inflation, high interest rates, forest fires and drought, the Canadian economy continued to be stuck in neutral in August.

Monthly real GDP growth was flat (+0.0%) compared with July. The economy was saved from an even worse performance by the service industry, which remained resilient during the month.

Growth was also sluggish in September, according to preliminary data from Statistics Canada. As a result, it appears the economy was stagnant in the third quarter.

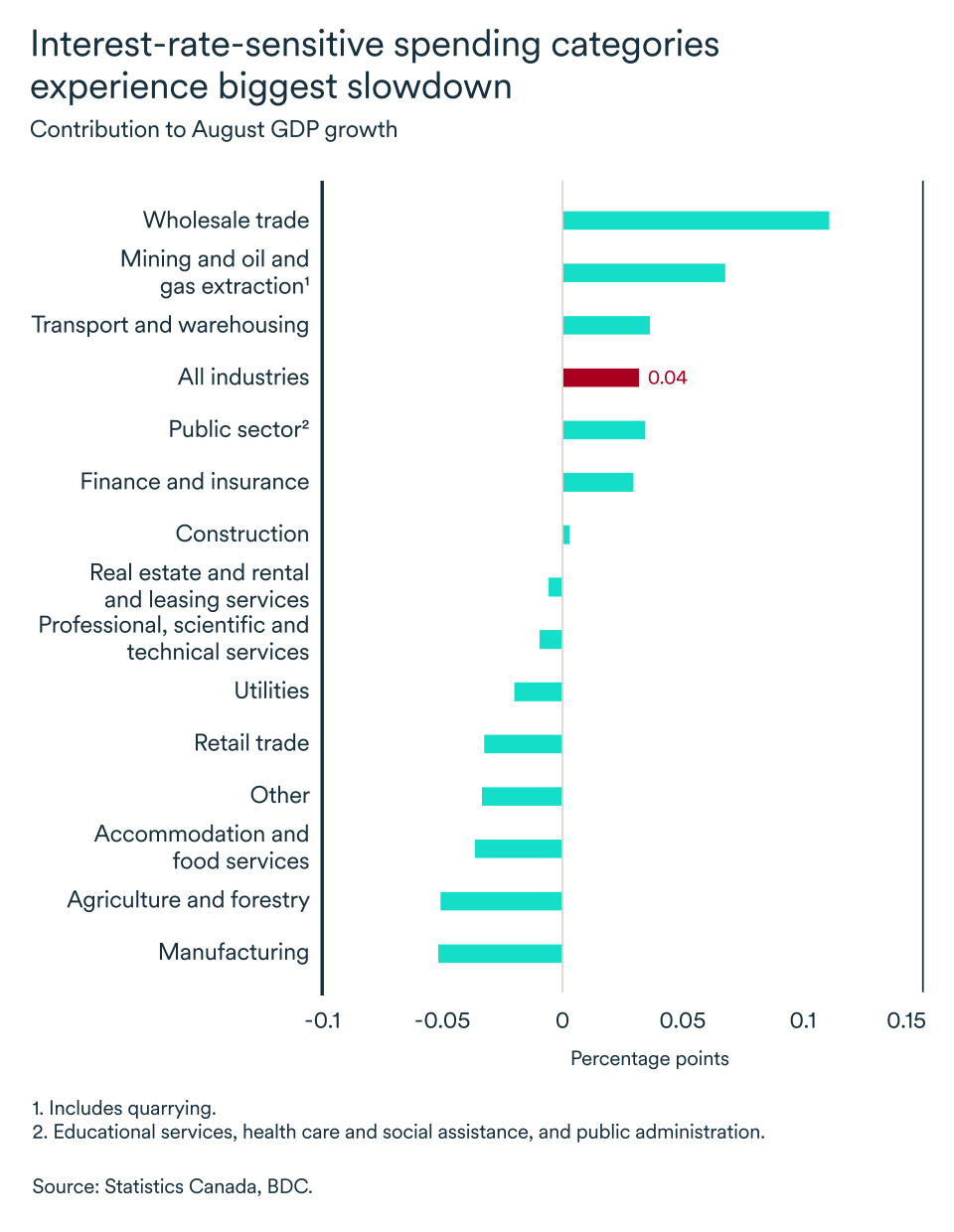

Households readjust their budgets

In addition to a decline in the agriculture and forestry sectors due to this summer's extreme conditions, the majority of other industries retreated. Past interest rate hikes continue to slow sectors that are sensitive to rates. Pullbacks in manufacturing, retail, and accommodation and food services limited overall economic growth in August, together reducing monthly growth by 0.13%.

Households are cutting back on purchases that are often financed with a loan, including vehicles, household appliances and electronics.

However, in Bank of Canada’s latest survey, 24% of households reported they still plan to spend heavily on services (travel, entertainment events) in the next six months, a reading similar to that for the last six months.

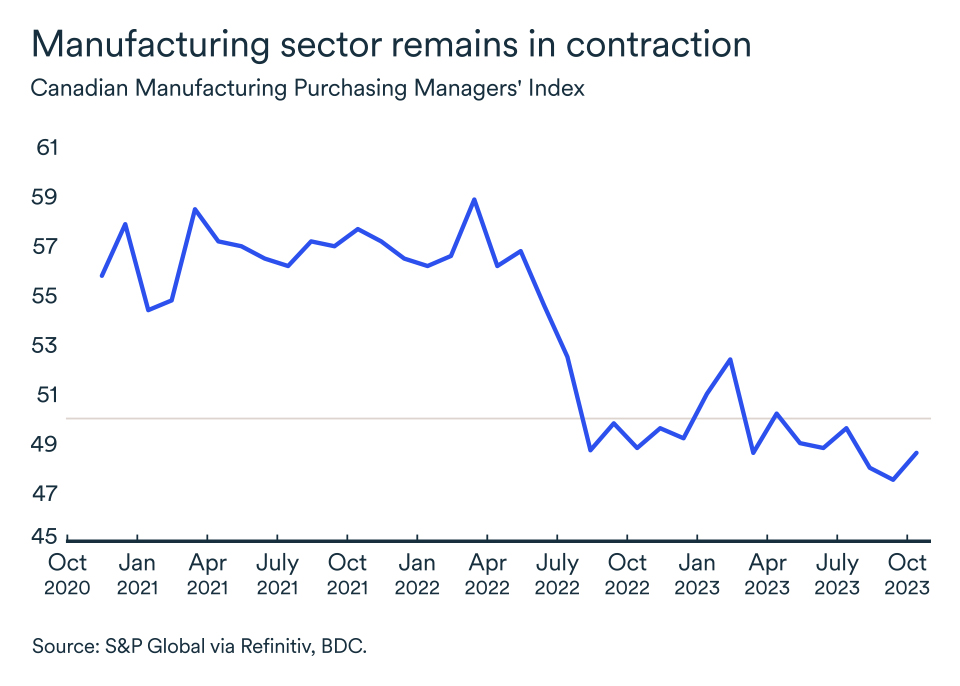

Manufacturing goes from bad to worse

The outlook for the Canadian manufacturing sector seems to worsen with each passing month.

The purchasing managers' index is still trending downward. After dipping below the 50 mark (which usually indicates a contraction in the sector) in May, the index has not recovered since. It hit 47.5 in September, the lowest level recorded since May 2020 at the height of the pandemic.

Purchasing activity continues to slow, with companies preferring to sell off their inventories than replenish them as a slowdown in demand takes hold.

Towards a more sustainable job market

While the Canadian economy continued to create jobs in October (+18,000) and the unemployment rate still low at 5.7%, pressure on the labour market eased.

The number of job vacancies fell again in August, albeit only slightly compared with July, from 698,000 to 682,400. Although this level is still high, it’s the lowest level in over two years, which should ease the competition for workers.

High economic uncertainty is causing companies to slow their hiring intentions, and workers are less likely to change jobs. The slowdown in the economy appears to be bringing the labour market into better balance, even if retirements remain high with the addition of more than 240,000 new retirees year-on-year in October.

These various factors have resulted in wage growth of 4.8% between October 2022 and October 2023, a slower pace than in recent months.

The impact on your business

- Although the Bank of Canada opted not to raise its key interest rate in October, rising debt payments by Canadian households will continue to slow domestic demand. This trend will gain momentum in the months ahead, as past rate hikes continue to work their way through the economy and households adjust their budgets.

- Despite the continuing strength of the labour market, households have less and less leeway to absorb interest rate hikes and price increases. They’re becoming increasingly cautious in their spending.

- Companies are also becoming more cautious. In addition to declining hiring intentions, many companies would rather sell off their current inventories than replenish their shelves. So, whether you're dealing with consumers directly or with other companies, be prepared to feel the effect of the slowdown sooner or later.

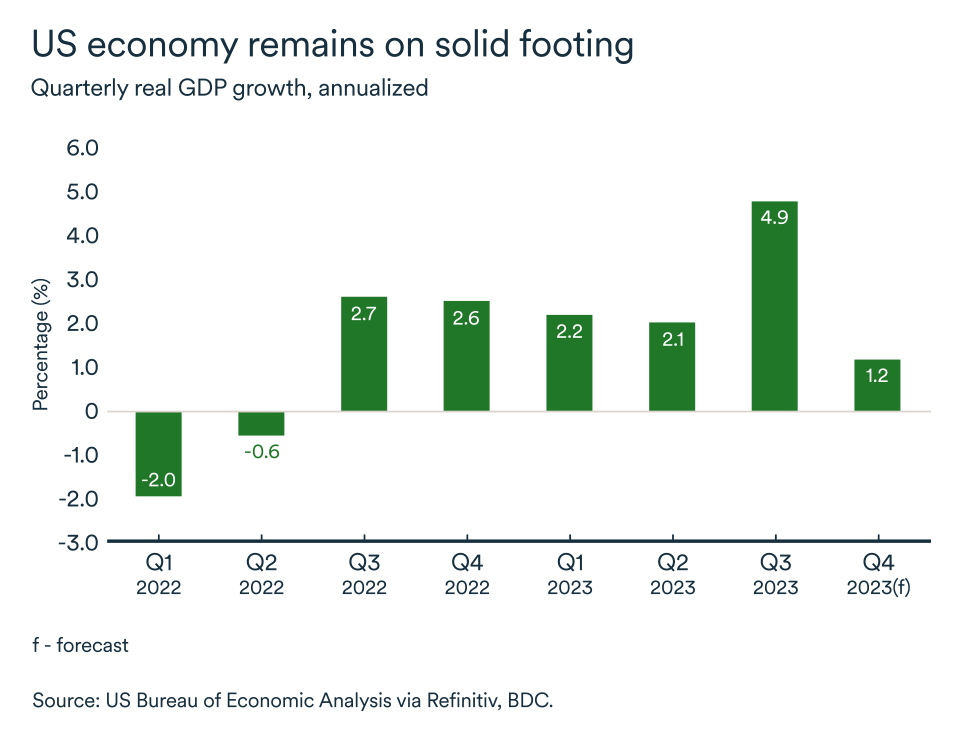

Momentum continues in the United States for the time being

Economic growth south of the border continues to defy expectations, reaching an annualized 4.9% in the third quarter. It would be surprising if the momentum continued in the fourth quarter since a significant part of the growth in recent months has come from inventory accumulation.

High inventories are a source of vulnerability that could easily tip GDP below potential growth before the end of the year.

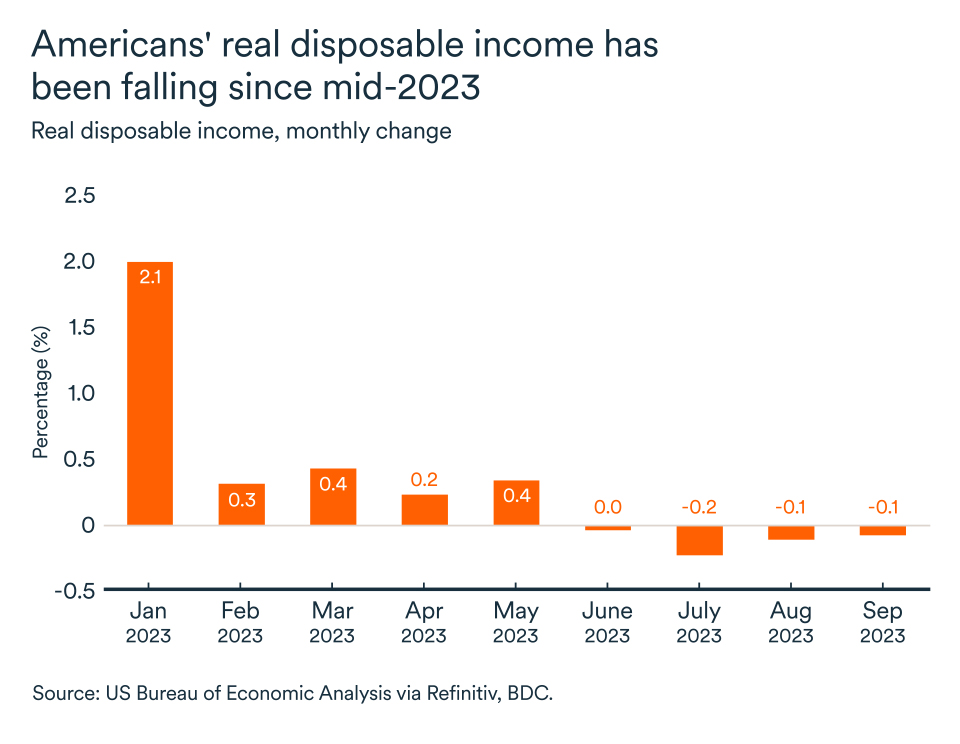

How much longer can households support the economy?

American consumers pulled out all the stops in the third quarter. Over the summer, consumer spending accelerated at a rate of 4.0%—a considerable improvement on the previous quarter's 0.8%.

American consumers appear to be less sensitive to interest rate increases than Canadians. This difference is due in large part to the fact that Americans borrowed heavily at fixed rates before the pandemic and also tend to hold 30-year mortgages. They’ve so far absorbed 500 basis points of rate hikes imposed by the Federal Reserve and kept on spending.

However, we are finally starting to see some red flags. Real disposable income has contracted by 1.0% and the savings rate continues to fall. Eventually, consumers will have to curtail their spending, especially considering the recent slowdown in the labour market and wage gains momentum.

Fed relies more on patience

The solid growth in consumer spending and a higher reading on the core Personal Expenditure Price Index (PCE) in September (+3.7% y/y) doesn’t seem to have been overly worrying for Fed officials.

They opted to keep the trend-setting interest rate steady in the Fed’s latest announcement on November 1. The federal funds rate therefore remains within a target range of 5.25% to 5.50%. It's a safe bet that rising yields in the U.S. bond market have reduced the Fed's appetite (and need) for a final rate hike this year.

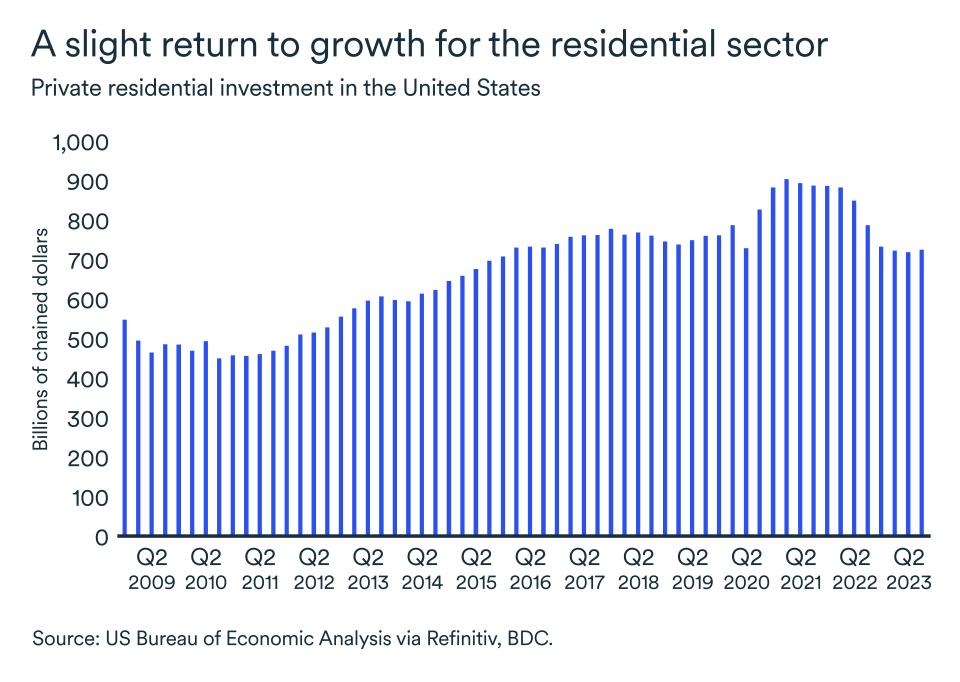

Residential investment on the rise

At the beginning of November, the average benchmark 30-year fixed mortgage interest rate was slightly above 8%, a record in over 20 years. Yet, despite the high rate, residential investment increased in the third quarter for the first time since the first quarter of 2021, when the average mortgage rate was closer to 3%.

Although the U.S. central bank has held the federal funds rate steady since the end of July, yields on long-term bonds have risen considerably, pushing up mortgage rates. Therefore, another positive quarter for residential investment would be surprising in this context.

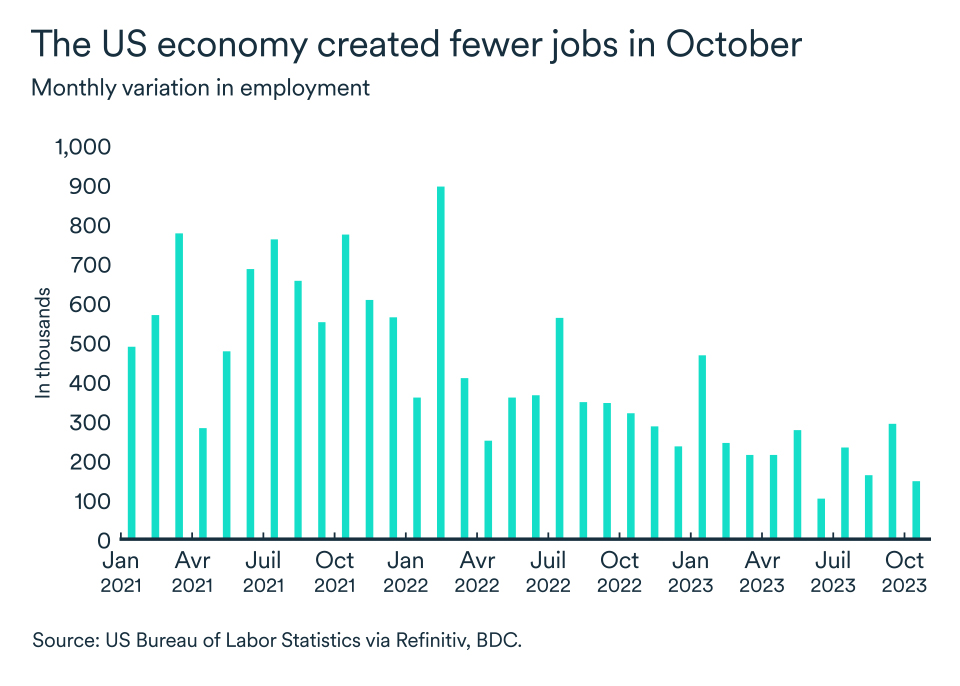

Job creation slows

Job creation has begun a downward trend. The economy added about 150,000 jobs to its balance sheet in October, one of the lowest monthly figure in the post-COVID era. The unemployment rate was up slightly at 3.9%, a sign that strong labour force growth in recent months is continuing to ease pressure on the job market.

Wage growth has slowed but remains strong at 4.1%. Inflation should therefore continue to fall in coming months, and employment gains should prove more modest as well. The October labour market report is likely to support the Federal Reserve's guidance that further rate hikes will not be necessary to rebalance the economy in the longer term.

The impact on your business

- The U.S. economy once again showed remarkable resilience in the third quarter, but the gains for Canadian companies were likely to be much more modest. Growth will be weak going forward, and what growth there is will largely come from the service sector.

- The Canadian dollar is near a six-month low against the U.S. greenback in response to an interest rate differential between the two countries. A weaker Canadian dollar tends to favour exports. On the other hand, it will cost more for Canadian companies that depend on inputs traded on world markets or that source their supplies from the United States. The CAD will likely remain around 72-73 cents for the rest of the year.

- The slowdown that has begun in the U.S. labour market should further limit U.S. consumption in coming months, which could exacerbate the slowdown in demand currently affecting Canadian companies.

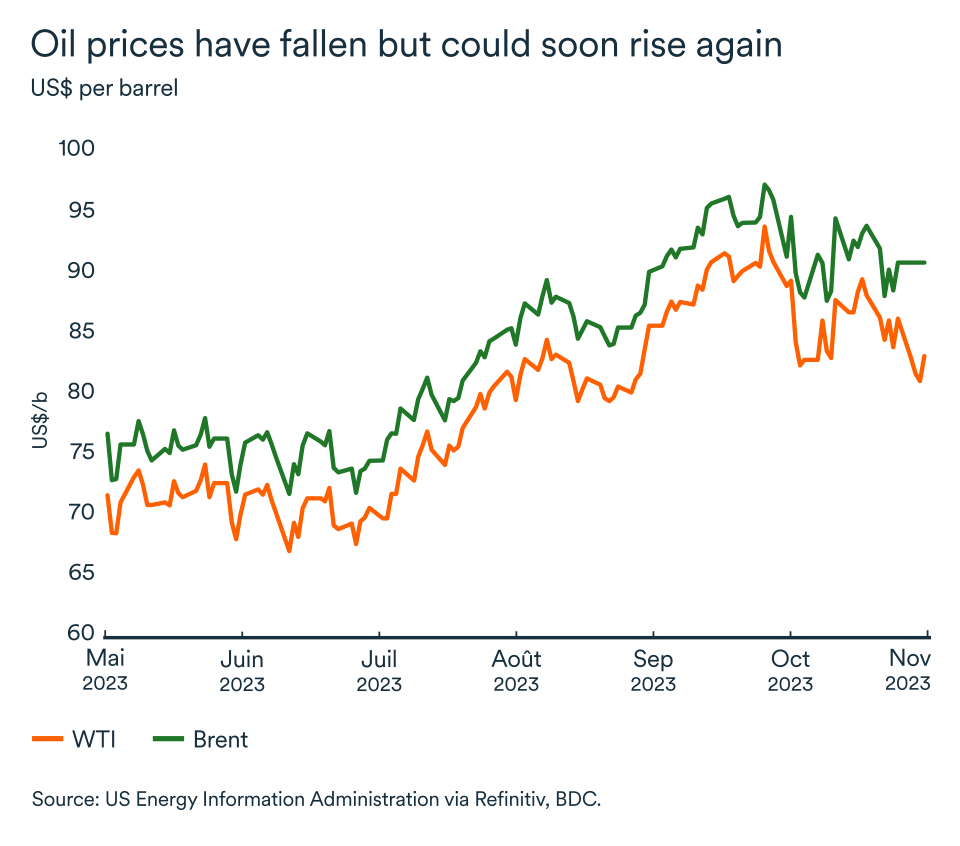

Oil prices decline, but supply disruption risks increase

The decline in crude oil prices that began in mid-October continued into November. Brent and WTI futures were trading at US$86 and US$81 a barrel, respectively, at the beginning of November, a month-on-month decline of 10%.

Oil prices are likely to stay below $90 in the short term, but risks for a price surge are on the rise. The war in the Middle East remains the main risk for a disruption in global oil supplies and rapid prices gains. Additionally, a pause in interest rate hikes should mitigate fears of recession and maintain demand for oil.

The U.S. Federal Reserve leads the way

The Federal Reserve's decision to keep the federal funds rate stable on November 1 has helped allay fears of recession. Monetary tightening around the world since 2022 has tended to reduce aggregate demand for oil. Now, many central bankers are suggesting they are finally done with rate hikes, although inflation remains high in most industrialized economies.

A pause in rate hikes reduces economic uncertainty on global markets, including the energy market. What's more, while the U.S. dollar has been gaining strength lately against other major currencies, reduced uncertainty should temper future gains. Most commodities, including oil, are traded in U.S. dollars and a stronger greenback generally leads to reduced demand for oil from buyers paying with other currencies.

Double energy shock, a major risk according to the World Bank

Since the outbreak of war in the Middle East, oil markets have remained on edge. For the time being, price changes have been muted despite the potential for a wider conflict in the region. The World Bank, however, has issued a major warning that the outlook could change rapidly.

The conflict is reminiscent of the Yom Kippur War of October 1973, which led to a spike in crude oil prices that followed an embargo imposed by Arab oil-producing countries on the United States.

With global supplies of natural gas still limited by the sanctions against Russia in response to its invasion of Ukraine, prices on the European gas market have recently risen on fears of disruption to a pipeline near the Gaza Strip.

The World Bank believes the global economy is in a better position to withstand an oil shock than during previous conflicts in the Middle East but warned of a potential double energy shock (oil and gas) that could occur in the event of a regional escalation of the conflict.

Tougher sanctions against crude-producing countries could also come into force, depending on developments in the war. The Middle East accounts for over a third of the world's seaborne oil trade.

Bottom line…

Uncertainty remains high in the oil market. As the global economic slowdown continues, a number of factors could reverse the downward price trend that has been underway for several weeks. On the one hand, the escalation of the conflict in the Middle East poses a major risk on the supply side, while the announced pause in interest rates should help to limit an expected drop in demand.

Markets will therefore continue to adjust according to the information available in the short term, increasing the risk of price volatility for the rest of the year.

The Bank of Canada remains on the sidelines

The Bank of Canada maintained the status quo on Wednesday, October 25, 2023. The key rate will therefore remain at 5.0%. With more than half of the year behind us, the Bank acknowledged that the economy has been losing momentum. It stated that consumption has been stalling, as demand for durable goods, housing and services decreased since the beginning of the year. The Bank revised its growth forecast lower for 2023, from 1.8%, to 1.2%; and for 2024, from 1.2% to 0.9%.

On the inflation side, the Bank highlighted that the progress has been slower due to higher energy prices and elevated inflation expectations. Additionally, structural factors in the housing market are playing a role in keeping shelter inflation elevated. Although the Bank did not hike rates further this time, it did mention that any upside risk to inflation would force it to raise rates again. At this stage, it has become quite clear that the Bank will need to keep rates higher for longer.

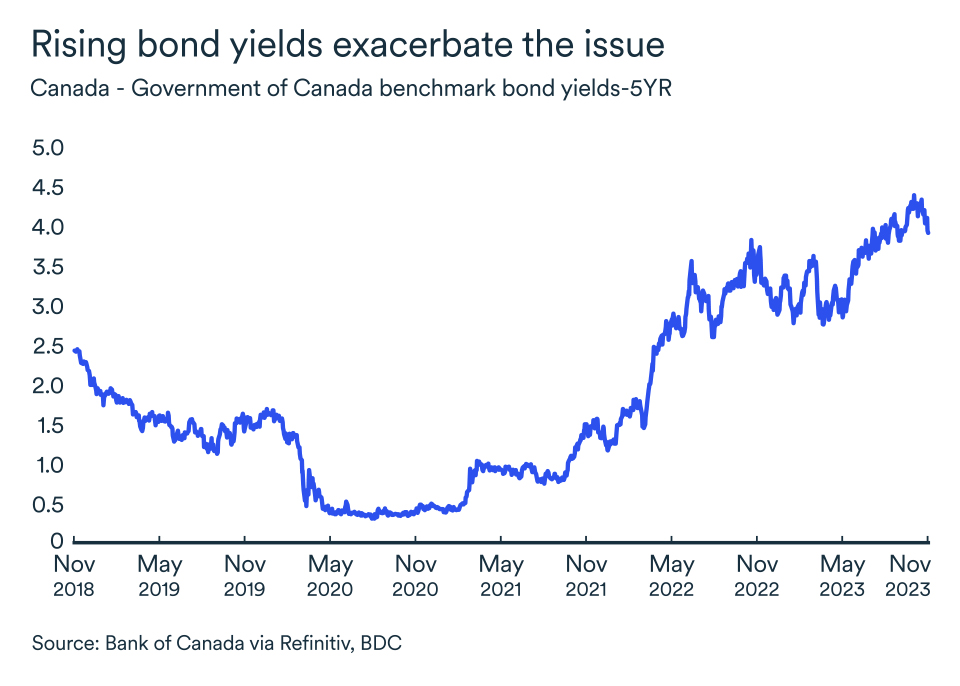

Bond yields, what are they good for?

Surging long-term bond yields have been tightening financial conditions significantly in recent months, leading to higher borrowing costs for households and businesses. In fact, Canada’s 5-year yield reached its highest levels so far this fall, hovering between 4.3% and 3.9% in recent months. These rates will be reflected on the 5-year fixed mortgage rates, directly affecting renewals this month, which will mean more pain for homeowners. While the Bank of Canada is waiting out the full impact of rate hikes, rising bond yields have given the Bank of Canada further incentive to pause on rate hikes.

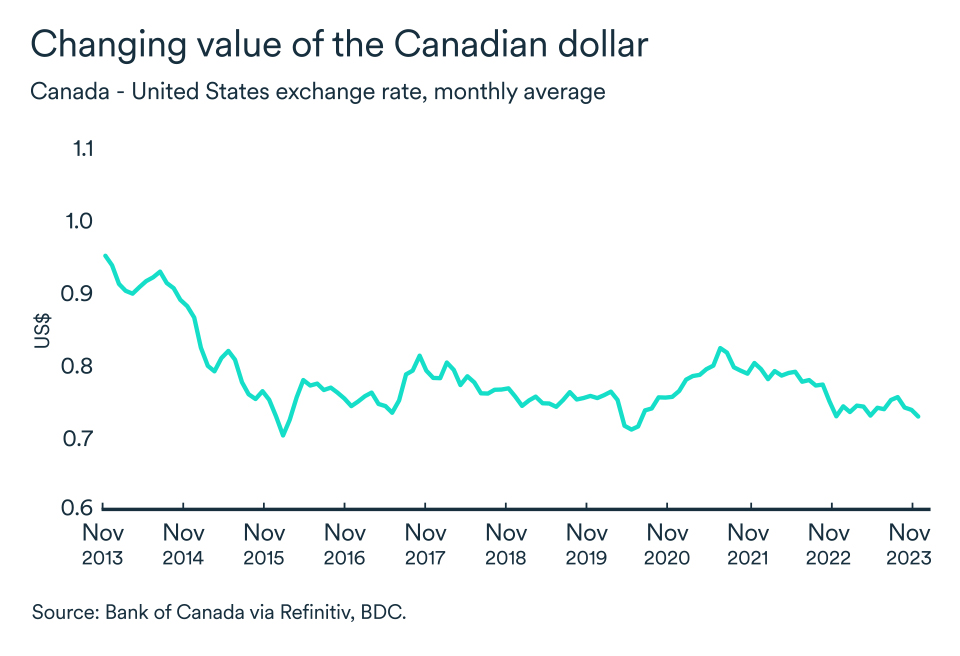

The loonie continues its slide

The Canadian dollar depreciated even further, averaging US$0.73 in October and getting closer to US$0.72 since mid-October. The Canadian dollar’s slide against the US greenback is partly explained by the interest rate differential between the two countries. The exceptional resilience of the US economy has been fuelling the rate hikes debate, as well as giving a strong push to the USD against US trading partners’ currencies. The Canadian dollar is likely to remain weak, fluctuating between US$0.73 and US$0.72 over the coming months.

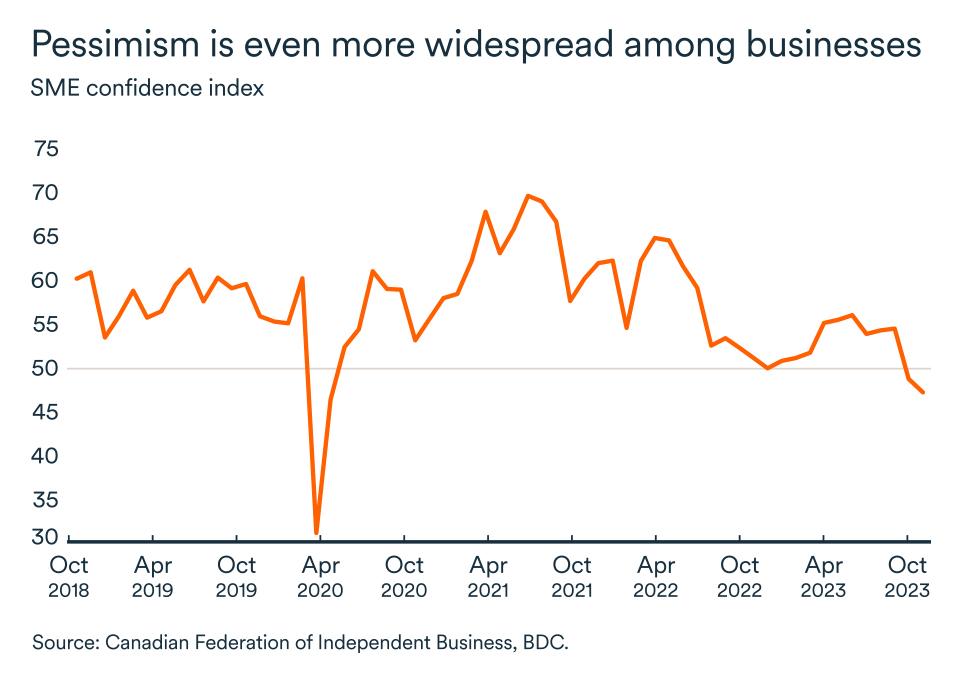

Pessimism intensifies among business leaders

CFIB’s business confidence index for the year ahead fell below the critical 50 mark—from 54.6 to 47.2 between August and October. Among provinces, confidence was lowest in Alberta, Ontario and Quebec, at 47.9, 46.5 and 46.1, respectively. Growing pessimism among businesses is not a surprise, given the economic slowdown and the tightening of credit conditions.